Lewis Hine A heavy load for an old woman. Lafayette Street below Astor Place, NYC 1912

Selling vehicles to vehicles: “The WMPs [wealth management product] used to be predominantly sold to the public, but now they’re increasingly being sold to banks and other WMPs.”

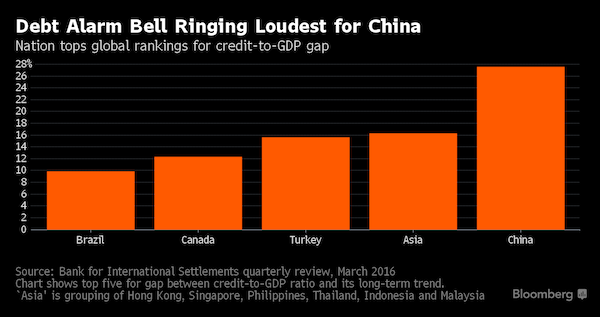

• ‘Massive Bailout’ Needed in Debt-Saddled China: Charlene Chu (BBG)

Charlene Chu, a banking analyst who made her name warning of the risks from China’s credit binge, said a bailout in the trillions of dollars is needed to tackle the bad-debt burden dragging down the nation’s economy. Speaking eight days after a Communist Party newspaper highlighted dangers from the build-up of debt, Chu, a partner at Autonomous Research, said she was yet to be convinced the government is serious about deleveraging and eliminating industry overcapacity. She also argued that lenders’ off-balance-sheet portfolios of wealth-management products are the biggest immediate threat to the nation’s financial system, with similarities to Western bank exposures in 2008 that helped to trigger a global meltdown.

The former Fitch Ratings analyst uses a top-down approach to calculating China’s bad-debt levels as the credit to GDP ratio worsens, requiring more credit to generate each unit of GDP. She’s on the bearish side of the debate about the outlook for China and has sounded warnings since the nation’s credit binge began in 2008. “China’s debt problems are large and severe, but in some respects a slow burn. Over the near term, we think the biggest risk is banks’ WMP [wealth management product] portfolios. The stock of Chinese banks’ off-balance-sheet WMPs grew 73% last year. There is nothing in the Chinese economy that supports a 73% growth rate of anything at the moment.

Regardless of all of the headlines and announcements about the authorities cracking down on WMPs, they have done very little, really, and issuance continues to accelerate. “We call off-balance-sheet WMPs a hidden second balance sheet because that’s really what it is – it’s a hidden pool of liabilities and assets. In this way, it’s similar to the Special Investment Vehicles and conduits that the Western banks had in 2008, which nobody paid attention to until everything fell apart and they had to be incorporated on-balance-sheet. “The mid-tier lenders is where these second balance sheets are very large. China Merchants Bank is a good example. Their second balance sheet is close to 40% of their on-balance-sheet liabilities. Enormous.”

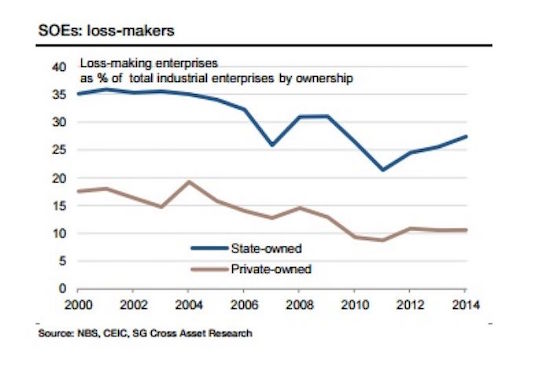

“Although contributing to less than one-third of economic output and employment, SOEs take up nearly half of bank lending..”

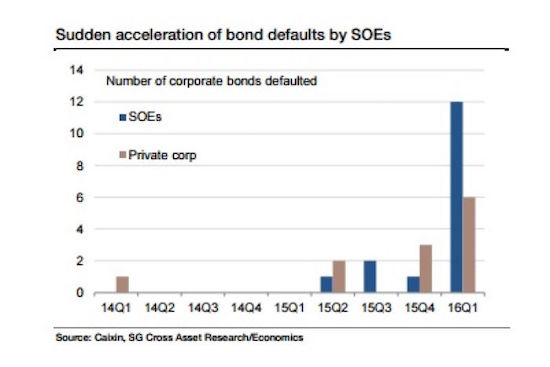

• SOE Debt Could Easily Overwhelm China’s Banking System (Abc.au)

Chinese banks are looking down the barrel of a staggering RMB 8 trillion – or $1.7 trillion – worth of losses according to the French investment bank Societe Generale. Put another way, 60% of capital in China’s banks is at risk as authorities start the delicate and dangerous process of reining in the debt-bloated and unprofitable state-owned enterprise (SOE) sector. Disturbingly though, debt is not only not shrinking, it is accelerating, making the eventual reckoning far worse. China’s overall non-financial debt grew by 15.2% in 2015 to RMB 167 trillion ($35 trillion) or almost 250% of GDP. That is up from 230% of GDP the year before and the 130% it was eight years ago before the global financial crisis hit.

The problem is largely centred on China’s 150,000 or so SOEs, which suck-up an entirely disproportionate amount of the nation’s capital. “Although contributing to less than one-third of economic output and employment, SOEs take up nearly half of bank lending (RMB 37 trillion) and more than 80% of corporate bond financing (RMB 9.5 trillion),” Societe Generale found. “While the inefficiency of SOEs is gradually dragging down economic growth, recognising even a small share of SOEs’ non-performing debt would easily overwhelm the financial system.” Despite their moribund financial performance, the SOEs still enjoy a considerable advantage in access to funding through the banking system than the private sector.

“To put things into perspective, a quarter of SOEs’ loans and bonds are equivalent to the entire capital base of commercial banks plus their loan-loss reserves, equivalent to 23% of GDP,” Societe Generale’s China economist Wei Yao said. On the bank’s figures, if just 3% of loans to SOEs sour, commercial banks’ non-performing loans would double.

Wanting to control the yuan exchange rate is a threat to reserves.

• China Takes Back Control Over Yuan (WSJ)

Behind closed doors in March, some of China’s most prominent economists and bankers bluntly asked the People’s Bank of China to stop fighting the financial markets and let the value of the nation’s currency fall. They got nowhere. “The primary task is to maintain stability,” said one central-bank official, according to previously undisclosed minutes of the meeting reviewed by The Wall Street Journal. The meeting left little doubt China’s top leaders have lost interest in a major policy shift announced in a surprise move just nine months ago. In August 2015, the PBOC said it would make the yuan’s value more market-based, an important step in liberalizing the world’s second-largest economy.

In reality, though, the yuan’s daily exchange rate is now back under tight government control, according to meeting minutes that detail private deliberations and interviews with Chinese officials and advisers who spoke with The Wall Street Journal about the country’s currency policy. On Jan. 4, the central bank behind closed doors ditched the market-based mechanism, according to people close to the PBOC. The central bank hasn’t announced the reversal, but officials have essentially returned to the old way of adjusting the yuan’s daily value higher or lower based on whatever suits Beijing best. The flip-flop is a sign of policy makers’ deepening wariness about how much money is fleeing China, a problem driven by its slowing economy.

For now, at least, officials believe the benefits of freeing the yuan are outnumbered by the number of threats. Re-emphasizing the yuan’s stability would also bring a sigh of relief to trading partners who worried a weaker currency would boost Chinese exports at the expense of those produced elsewhere. Freeing the yuan, the biggest overhaul of China’s currency policy in a decade, was meant to empower consumers and help invigorate the economy. The negative reaction, from financial markets world-wide and Chinese who sped their efforts to take money out of the country, was so jarring that the top leadership, headed by President Xi Jinping, began to have second thoughts.

At a heavily guarded conclave of senior Communist Party officials in December, Mr. Xi called China’s markets and regulatory system “immature” and said “the majority” of party officials hadn’t done enough to guide the economy toward more sustainable growth, according to people who attended the meeting. To the central bank, there was only one possible interpretation: Step on the brakes.

Turns out, it can still get worse.

• Negative Rates Prompt Japan Banks to Opt Out Via Derivatives (BBG)

Japanese banks reluctant to pay for the privilege of lending are opting out by using derivatives. The options set a floor on rates used to determine interest on loans, and the holder will be paid if the rates fall below that level, according to Aozora Bank and Tokyo Star Bank. The benchmark three-month Tokyo interbank offered rate has plunged to a record low of 6 basis points since the Bank of Japan announced it would start charging fees on some lenders’ reserves in January. Options with floors at zero% or minus rates have been traded recently, according to Aozora Bank. “There’s a need to hedge against money-losing lending that could happen if the Tibor falls to negative levels,” said Tetsuji Matsuka, the head of the ALM planning treasury department at Tokyo Star Bank.

“We think demand will increase” for such products, he said. Japanese banks are getting hurt as the negative-rate policy compresses their lending margins, with the top-three firms including Mitsubishi UFJ Financial forecasting this month that net income will fall a combined 5.2% in the year started April 1. The BOJ’s radical stimulus has already dragged yields on more than 70% of Japanese government bonds to below zero, meaning that investors will have to effectively pay a fee to hold such debt to maturity. In the yen London interbank offered rate market, where some rates are already below zero, options have been traded with floors as low as minus 1%, according to Nobuyuki Takahashi, the general manager of the derivatives sales division at Aozora Bank.

The three-month yen Libor was at minus 0.02% on Friday. Companies that borrow at floating rates may also be able to use floor options to ensure that interest-rate swaps they use to hedge against rising rates don’t end up costing them due to negative rates, Takahashi said. Actual trades of such derivatives are still not that common because the contracts are expensive to buy now, he said. “It will be hard to price these options unless we get more liquidity,” said Tateo Komatsu, a deputy general manager of global markets at Sumitomo Mitsui Trust Bank Ltd. “It will take time for the market to get used to minus rates.”

Roller coaster in a casino.

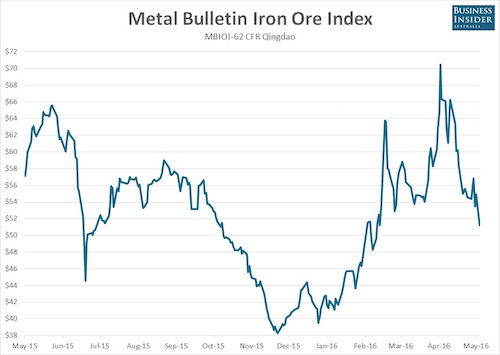

• Iron Ore Price Falls 27% In Past Month (BI)

The iron ore price is imploding. Following the ugly lead provided by Chinese futures on Monday, the spot iron ore price followed suit, suffering one of the largest declines seen in years. According to Metal Bulletin, the spot price for benchmark 62% fines fell by 6.69%, or $3.67, to $51.22 a tonne, leaving it down 27.3% from the multi-year peak of $70.46 a tonne struck on April 21. The decline was the third-largest in percentage terms in the past two years, and left the price at the lowest level seen since March 3 this year. The losses in physical and futures markets followed news that Chinese iron ore port inventories swelled to over 100 million tonnes last week, leaving them at the highest level seen since March last year.

That followed the revelation that Chinese crude steel output contracted in April after hitting a record high in March, declining marginally according to figures released by the China Iron and Steel Association (CISA). Given the increasing correlated relationship between the two, it’s also clear that an unwind of speculative positioning in Chinese iron ore futures is also impacting prices in the physical iron ore market. After watching prices in many bulk commodity futures rally more than 50% in less than two months, regulators at both the Dalian Commodities Exchange and Shanghai Futures Exchange introduced measures in recent weeks to discourage excessive levels of speculation in these markets.

Slow death?!

• Deutsche Bank Ratings Cut by Moody’s (BBG)

Deutsche Bank had its credit rating cut by Moody’s Investors Service, which said the German lender faces mounting challenges in carrying out its turnaround. The bank’s senior unsecured debt rating was lowered to Baa2 from Baa1, Moody’s said Monday in a statement. That left the grade two levels above junk. The firm’s long-term deposit rating fell to A3 from A2. “Deutsche Bank’s performance over the last several quarters has been weak, and substantial operating headwinds, including continuing low interest rates and macroeconomic uncertainty, will challenge the firm,” Moody’s said in the statement. CEO John Cryan’s planned overhaul of the bank, laid out in October, ran into an industrywide slump in trading and investment banking, as well as interest rates that have gone from low to negative in parts of Europe and Asia.

Net income fell 61% in the first quarter, leaving the company at risk of a second straight annual loss this year as it tries to resolve legal cases. Results so far and the challenges ahead, including a chance of further slumps in retail and market-linked businesses, will probably force Deutsche Bank to balance restructuring costs with the need to amass capital for stiffened regulatory requirements, Moody’s wrote. “The plan they’re trying to execute is a good plan for the bondholder in the long run, but they face some pretty challenging headwinds when you look at the current operating environment,” Peter Nerby, a senior vice president at Moody’s, said in a phone interview. “They’re working on it, but it’s tougher than it was.”

“A whole generation will have been consigned to the scrapheap.”

• Greece Is Never Going To Grow Its Way Out Of Debt (Coppola)

The IMF has just released its latest Debt Sustainability Analysis (DSA) for Greece. It makes grim reading. Greece is never going to grow its way out of debt. And the 3.5% primary surplus to which the Syriza government seems hell-bent upon committing is frankly unbelievable: the IMF thinks sustaining even 1.5% would be a stretch. Banks will need another €10bn (on top of the €43bn the Greek government has already borrowed to bail them out). Asset sales are a lost cause, mainly because the banks – which were a large proportion of the assets up for sale – won’t be worth anything for the foreseeable future. Like it or not, debt relief will be necessary. If there is no debt relief, by 2060 debt service will soar to an impossible 60% of government spending. Of course, Greece would default long before that – but that would make the situation in Greece even worse.

None of this is news. The IMF has been saying for nearly a year now that Greece will need debt relief. This latest DSA is designed to shock the Europeans into giving it serious consideration. It is not surprising, therefore, that the debt sustainability projections are significantly worse than in previous DSAs. No doubt the European creditors will disagree with them, the Syriza government will side with the Europeans because the only alternative is Grexit, and the European Commission will claim there is “progress” when all that is really happening is that a very battered can is being kicked once again. But buried in the IMF’s report are some very unpleasant numbers indeed – the IMF’s projections for population and employment out to 2060. And I think the world should know about them. Here is what the IMF has to say about the outlook for Greek unemployment:

Demographic projections suggest that working age population will decline by about 10 percentage points by 2060. At the same time, Greece will continue to struggle with high unemployment rates for decades to come. Its current unemployment rate is around 25%, the highest in the OECD, and after seven years of recession, its structural component is estimated at around 20%. Consequently, it will take significant time for unemployment to come down. Staff expects it to reach 18% by 2022, 12% by 2040, and 6% only by 2060. So even if the Greek economy returns to growth and its creditors agree to debt relief, it will take 44 years to reduce Greek unemployment to something approaching normal. For Greece’s young people currently out of work, that is all of their working life. A whole generation will have been consigned to the scrapheap.

Think Britain is bad? Try Greece.

• Austerity Means Privatizing Everything We Own (G.)

Almost everyone who gives the matter serious thought agrees that George Osborne and David Cameron want to reshape Britain. The spending cuts, the upending of the NHS, even this month’s near-miss over the BBC: signs lie everywhere of how this will be a decade, maybe more, of massive change. Yet even now it is little understood just how far Britain might shift – and in which direction. Take austerity, the word that will define this government. Even its most astute critics commit two basic errors. The first is to assume that it boils down to spending cuts and tax rises. The second is to believe that all this is meant to reduce how much the country is borrowing. What such commonplaces do is reduce austerity to a technical, reversible project.

Were it really so simple all we would need to do is turn the spending taps back on and wash away all traces of Osbornomics. Austerity is far bigger than that: it is a project irreversibly to transfer wealth from the poorest to the richest. It’s doing the job very nicely: while the typical British worker is still earning less after inflation than he or she was before the banking crash, the number of UK-based billionaires has nearly quadrupled since 2009. Even while he slashes benefits, Osborne is deep into a programme to hand over much of what is still owned by the British public to the wealthiest. Privatisation is the multibillion-pound centrepiece of Osborne’s austerity – yet it rarely gets a mention from either politicians or press. The Queen mentioned it in her speech last week, but the headline writers ignored it.

And if you don’t know that this Thursday is the closing date for consultation on the sale of the Land Registry, our public record of who owns what property, that’s hardly your fault – I haven’t spotted it in the papers, either. But without getting rid of prize assets, Osborne’s austerity programme falls apart. At a time when tax revenues are more weak stream than healthy flood, those sales bring much-needed cash into the Treasury and make his sums add up. The independent Office for Budget Responsibility has ruled that the only reason the chancellor met his debts target last year was because he flogged off our public assets. And what a fire sale that was, with everything from our last remaining stake in the Royal Mail to shares in Eurostar shoved out the door in the biggest wave of privatisations of any year in British history.

And maybe sometime in the next century something will be done. But they’re all still too big to fail.

• US Court Opens Door Over Libor Claims (FT)

A US appeals court has opened the door for more claims against the big banks for rigging benchmark interest rates, by overturning a three-year-old ruling which threw out a host of private antitrust-related lawsuits. Monday’s decision by the 2nd US Circuit Court of Appeals in Manhattan could be a setback for the likes of Bank of America, JPMorgan Chase and Citigroup, which had hoped that most of the wave of post-crisis litigation was behind them. The decision reverses a lower court decision from 2013, in which US District Judge Naomi Reice Buchwald dismissed claims on the grounds that the plaintiffs had failed to plead antitrust injury.

The lawsuits had accused 16 major banks of collusion in manipulating the London interbank offered rate, or Libor, which approximates the average rate at which a select group of banks can borrow money. Beginning in 2007, the plaintiffs argued, the banks engaged in a horizontal price-fixing conspiracy, with each submitting an artificially low cost of borrowing US dollars in order to drive Libor down. At the time of her rejection, Judge Buchwald reasoned that the Libor-setting process was co-operative rather than competitive, and so any attempt to depress the rate did not cause investors to suffer anti-competitive harm. At best, she said, investors had a fraud claim based on misrepresentation.

But the appeals court on Monday disagreed and sent the case back to the lower court for further proceedings. A three-judge panel found that price-fixing was an antitrust violation in itself, and therefore needed no separate plea of harm. “The crucial allegation is that the banks circumvented the Libor-setting rules, and that joint process thus turned into collusion,” the panel said. The private suits are separate from the criminal and civil probes into Libor rigging, which have ensnared banks and traders around the world and drawn about $9bn so far in penalties.

Do we even still notice?

• Italy Helps Rescue 2,600 Migrants From Sea In 24 Hours (R.)

Italian vessels have helped rescue more than 2,600 migrants from boats trying to reach Europe from North Africa in the last 24 hours, the coastguard said on Monday, indicating that numbers are rising as the weather warms up. Some 2,000 migrants were rescued off the Libyan coast from 14 rubber dinghies and one larger boat in salvage operations by the Italian navy and coastguard, the medical charity Medecins Sans Frontieres and an Irish navy vessel, the coastguard said. Another 636 migrants were rescued from two boats in Maltese waters, in operations involving Maltese and Italian vessels, it said. It gave no information about the nationalities of those saved. More than 31,000 migrants have reached Italy by boat so far this year, slightly fewer than in the same period of 2015.

Humanitarian organizations say the sea route between Libya and Italy is now the main route for asylum seekers heading for Europe, after an EU deal on migrants with Turkey dramatically slowed the flow of people reaching Greece. Officials fear the numbers trying to make the crossing to southern Italy will increase as conditions improve in warmer weather. More than 1.2 million Arab, African and Asian migrants fleeing war and poverty have streamed into the European Union since the start of last year. Most of those trying to reach Italy leave the coast of lawless Libya on rickety fishing boats or rubber dinghies, heading for the Italian island of Lampedusa, which is close to Tunisia, or toward Sicily.

Peaceful until now.

• Greece Starts Clearing Makeshift Refugee Camp On Border (R.)

Greek police started moving migrants and refugees out of a sprawling tent camp on the sealed northern border with Macedonia on Tuesday where thousands have been stranded for months trying to get into western Europe. Reuters witnesses saw several bus loads of migrants leaving the makeshift camp of Idomeni early on Tuesday morning, with about another dozen buses lined up. It appeared to be mainly families who were on the move. Greek authorities said they planned to move individuals gradually to state-supervised facilities further south in an operation expected to last several days. “The evacuation is progressing without any problem,” said Giorgos Kyritsis, a government spokesman for the migrant crisis.

A Reuters witness on the Macedonian side of the border said there was a heavy police presence in the area but no problems were reported as people with young children packed up huge bags with their belongings. Media on the Greek side of the border were kept at a distance and a group of people dressed as clowns waved balloon hearts and animals as the buses drove past. “Those who pack their belongings will leave, because we want this issue over with. Ideally by the end of the week. We haven’t put a strict deadline on it, but more or less that is what we estimate,” Kyritsis told Reuters. At the latest tally, 8,199 people were camped at Idomeni after a cascade of border shutdowns throughout the Balkans in February barred migrants and refugees from central and northern Europe. More than 12,000 lived in the camp at one point.

Home › Forums › Debt Rattle May 24 2016