Henri Matisse Open window, collioure 1905

Tariffs not taxes

This is an eye opener for understanding tariffs. People need to understand why they are such a useful tool. pic.twitter.com/tWcBpvAzAf

— Michelle Maxwell (@MichelleMaxwell) April 29, 2025

Bessent

NEW – Bessent Announces Move to Make it Insanely Profitable to Bring Factories Back to America — FULL Expensing for Equipment and Buildings

This could be a game-changer.

Treasury Secretary Scott Bessent just revealed a massive new plan: full expensing for American factories,… pic.twitter.com/AyQWRHUBRa

— Overton (@overton_news) April 29, 2025

NOW – Bessent Just Blew the Lid Off 50 Years of American Failure—Trump’s First 100 Days Are About to Change Everything

Treasury Secretary Scott Bessent just said the quiet part out loud and it was a direct shot at the political class that ran Washington for the last… pic.twitter.com/QlndueYjLX

— Overton (@overton_news) May 1, 2025

Woke

DOGE: How do you get half of the woke lawyers in the DOJ to quit? Tell them they're going to have to combat antisemitism and keep men out of women's bathrooms. Assistant AG Harmeet Dhillon managed to get 50% of the woke lawyers in the Civil Rights Division to voluntarily resign. pic.twitter.com/rE7iijf7K8

— @amuse (@amuse) April 29, 2025

ARO

EXCLUSIVE: Raytheon Whistleblower Who Exposed The Neutrino Earthquake Weapon In Antarctica Gives Major Updates & Responds To President Trump's Announcement That The US Has Top Secret Super Weapons

Eric Hecker Discusses Directed Energy Weapons, Faster-Than-Light Communication… pic.twitter.com/3KiDw3bZHP

— Alex Jones (@RealAlexJones) April 29, 2025

Orban

Apparently, democracy now comes stamped “Approved by Brussels.” So they claim. Last time we checked, it was built by nations, defended by voters, and decided in elections. Our democracies do not need permission from unelected suits. pic.twitter.com/z1MECF3rM4

— Orbán Viktor (@PM_ViktorOrban) April 29, 2025

Meta

Today I’m announcing a major multi-million dollar defamation lawsuit against @Meta, the owner of @Facebook & @Instagram.

The case is WILD and has implications for ALL OF US. On top of falsely calling me a criminal, Meta suggested my kids be taken from me.

Here’s a summary of… pic.twitter.com/Pu8gTQpPq0

— Robby Starbuck (@robbystarbuck) April 29, 2025

FISA

https://twitter.com/Real_RobN/status/1917250091213292014

Fed

Edward Griffin on the Federal Reserve:

“It must be abolished for 7 reasons:

▪️It is incapable of accomplishing its stated objectives

▪️It is a cartel operating against the public interests

▪️It is the supreme instrument of usury

▪️It generates our most unfair tax

▪️It encourages… pic.twitter.com/OPC4phc21Z— Not A Number (@myhiddenvalue) April 29, 2025

Fleury

Ladies and Gentlemen your new Prime Minister!!! Good luck and may God have mercy on your souls!!!! pic.twitter.com/d5GylCReoC

— Theo Fleury (@TheoFleury14) April 29, 2025

Alberta

Alberta has reportedly surpassed the required 177,000 signatures to trigger a referendum process. And all of that in just one day…

If this happens, Canada is finished. pic.twitter.com/eD5B55XAgO

— Dr. Clown, PhD (@DrClownPhD) April 30, 2025

Rose

Catherine Fitts on @TuckerCarlson mentioned this clip of Sir James Goldsmith explaining globalization to Charlie Rose in 1994.

It seems like things went exactly the way he said.

The most important thing I took from it is that the economy should be there to serve society, not… pic.twitter.com/tKvE9VIwjk

— Calvin Correli (@calvincorreli) April 29, 2025

Let’s do a few “first 100 days” articles..

• ‘We Are Just Getting Started’: Trump Hails His First 100 Days (DS)

President Donald Trump declared it the “most successful 100 days” in American history. “They all want to come back to Michigan and build cars again. You know why, because of our tax and tariff policy,” Trump said in his remarks at the Macomb County Community College Sports and Expo Center in Warren, Michigan, to mark his 100th day in office. “I’m here in the heartland of our great nation to celebrate the most successful 100 days of any administration in the history of our country, and that’s according to many, many people,” Trump said. “Everyone is saying. We are just getting started.” Trump delivered a wide-ranging speech covering innumerable topics. “We are taking back our jobs and protecting American autoworkers and all of our workers. We are restoring the rule of law,” the president continued.

“We are ending the inflation nightmare, the worst that we’ve had probably in the history of our country,” Trump said. “Getting lunacy and transgender insanity the hell out of our government. We are stopping the indoctrination of our children, slashing billions of dollars in waste, fraud, and abuse. And above all, we’re saving the American dream, we are making America great again, and it’s happening fast.” Trump asserted he is telling “incompetent deep state bureaucrats, ‘You’re fired. Get out of here.’” “We are ushering in the golden age of America,” he said. Trump asserted that border crossings had dropped “99.999%” since he returned to office. “The number of illegal border-crossers released into the United States is down. Listen to this, please: 99.999%,” Trump said, before making a joke about his border czar Tom Homan. “Three people got in. Three. And I got angry as hell at Tom Homan. How did you allow three, Tom?”

Trump issued executive orders to end the “catch and release” of illegal immigrants trying to sneak into the country; reinstated the “Remain in Mexico” policy for those seeking asylum here; designated MS-13, Tren de Aragua, and other gangs as foreign terrorist organizations; and greatly ramped up deportations. “You’ve seen a change at the southern border that Sleepy Joe said couldn’t happen,” Trump said, referring to his predecessor, the 46th president, Joe Biden. “I stand before you today and can report to you that we have achieved the safest border in American history.” Trump asserted if he hadn’t won the 2024 election, Democrats “would have imported the next round” of illegal immigrants. “It would have only been a matter of time before America became a Third World country.” The president also made a comparison to Democrats’ unwillingness to prosecute illegal immigrants, but their enthusiasm to prosecute him.

“They’re claiming that we’re not allowed to deport illegals, and they’re the ones who orchestrated an eight-year campaign to jail their political opponents,” including himself, he said. “That’s all they can do. Jail their political opponents.” Continuing a reference to his predecessor, Trump said, “Whoever operated the autopen was in charge.” Trump was referring to an autopen that appears to have been used by someone other than Biden in the Biden administration to sign off on several executive orders. The Oversight Project, a watchdog group, recently issued a legal memo asserting presidential pardons may be invalid if the president doesn’t sign them himself, since clemency is a responsibility the Constitution only grants to the president. On the economy, Trump also took a verbal swipe at Federal Reserve Board Chairman Jerome Powell, who the president appointed during his first term.

“Interest rates came down, despite the fact that I have a Fed person who’s not really doing a good job. But I won’t say that,” Trump said. “I want to be very nice. I want to be very nice and respectful to the Fed. You’re not supposed to criticize the Fed. You’re supposed to let him do his own thing. But I know much more than he does about interest rates. Believe me.” Trump said he was the president of “the workers, not the outsourcers,” and the “president for Main Street, not Wall Street.” The president boasted about his tariffs—which have been controversial even among many Republicans. He noted, “In many cases, friends have abused us more than foes on trade.”

However, China is the biggest problem, he said. “China has taken more jobs from us than any country has ever taken from another country,” Trump said.“That doesn’t mean we’re not going to get along. We’ll get along with China. Their tariff now is at 145%. That’s a big difference between that and zero. I think it’s going to work out. They want to make a deal. We’re going to make a deal. It’s not going to be a deal where we lose $1 trillion a year like they did with Biden.” Trump touted his executive order on election integrity that he signed this month. A U.S. District Court recently blocked part of that executive order. “I also signed an order to require proof of citizenship to vote in American elections. That was easy,” he said. “The Democrats fought me on that. Think of it. Why would they want no voter ID? Because they want to cheat. Why would they want no proof of citizenship? ‘We don’t want it. We trust everybody.’ No, they want to cheat. That’s what they do.”

The Trump administration has also dismantled federal mandates regarding diversity, equity, and inclusion, or DEI for short. “I banned men from competing in women’s sports. They say that’s an 80-20 issue. No, I’d say it’s about a 97-3 issue,” the president said, referring to his ban on biological males who “identify” as females playing in girls and women’s sports. Trump also said he stopped the spread of DEI in the military academies. “I signed executive orders to abolish critical race theory and transgender insanity from our schools, and from our military,” Trump continued. “We fired the woke boards of visitors at our military academies. We have. We have great people running our military academies now.”

“It’s clear that most of the federal apparatus, even including the FBI, is run and operated by partisan Democrats who, in many cases, are willing to use their power to punish or at least impede their domestic political enemies..”

• Trump’s Counterrevolution at 100 Days (Stepman)

The first 100 days of President Donald Trump’s second term have been stunningly transformative, even as the Left has begun to mount some counteroffensives in the judiciary and in the media. For a president to be successful, he must apply principles that one might apply to warfare or sports. The early days of a presidency are about maintaining tempo—about keeping the ball moving on issues that the president was elected to promote. Any kind of slowdown usually means the president’s power to reform the system has come to an end, as this signals the natural shifting of the tide to the out-of-power party. On this end, Trump 2.0 has been one of the most successful early presidencies since FDR. This is Trump’s Dark New Deal, to borrow language from Elon Musk. He’s effectively flooded the zone with dramatic changes in policy that range from immigration to trade to foreign affairs and much more.

Whereas Trump’s predecessor was a virtually comatose upholder of an old regime, one that had become quite radical in its aims and tyrannical in its operation, Trump is a disruptor. He is pushing the envelope to an extent far beyond even his first term in office. This is Trump’s populist counterrevolution. Here’s a quick review of his more significant accomplishments thus far.

Border Secured On the border, the Trump effect has been stunningly effective. By making it known that the law will be enforced and then enforcing those laws, Trump has virtually solved the border problem overnight. Getting control of the border was one of the central planks of Trump’s message since he became active in politics, and he’s succeeded spectacularly. The Trump administration justly spiked the football on this issue Monday.

“Since President Donald J. Trump took office, he and his administration have ushered in the most secure border in modern American history—and he didn’t need legislation to do it,” read a statement from the White House. “President Trump has made good on the promises he made on the campaign trail to usher in an unprecedented era of homeland security.” The problem is now dealing with former President Joe Biden’s mess internally, which was always going to be the greater challenge. The Left’s commitment to open borders won’t abate even as the popular tide has turned against it. The Left has retreated to the dubious position of just wanting “due process” for the millions of people it brought here illegally, but that’s a tough case to make when the previous administration gleefully undermined the U.S. legal process for years to create this crisis.

Deep State Defanged The Trump administration’s actions against the administrative state, or the deep state, have been nothing short of remarkable. From the new Department of Government Efficiency to the State Department to even the departments of Energy and Education, Trump has taken aim at neutering the “fourth” branch of government. This has served two purposes. First, it’s restoring some level of accountability to our federal government that has over time become untethered from any kind of genuine democratic accountability. A mid-level career bureaucrat should not be dictating how the executive branch operates, nor should a government job be treated as an inviolable right. The Trump administration is using every tool it can to change that dynamic.

The second purpose is that by cutting loose large chunks of the administrative state, Trump is also severing the Left’s patronage networks. It’s clear that most of the federal apparatus, even including the FBI, is run and operated by partisan Democrats who, in many cases, are willing to use their power to punish or at least impede their domestic political enemies. To make matters worse, the federal government also distributes countless billions of dollars in grant funding to essentially left-wing activists in badly misnamed nongovernmental organizations. There’s a reason why the Left lost its collective mind when Trump dramatically curtailed the U.S. Agency for International Development, for instance. It knows that this strikes at not only its domestic power but also at its global ability to conduct social engineering.

DEI Regime Crumbling Given everything else that’s happening, Trump has quietly begun the process of dismantling the diversity, equity, and inclusion regime. The Left has essentially warped civil rights law to move away from shared notions of equality under the law. The Biden administration and its elite institutional allies used the prior four years to racialize our government and society based on their notions of who qualifies as an oppressor and who is oppressed. The result has been a massive backlash. Now, Trump is taking aim at DEI, not only eliminating it from federal departments but using civil rights law to ensure that any institution receiving government support will no longer be able to discriminate based on race. He is now using this to push Ivy League schools to drop their DEI programs or else lose billions of dollars in federal funding.

Another example of how Trump is blowing up DEI is his executive order ending “disparate impact” analysis from government policy. The disparate impact theory posited that any example of racial disparity, even unintentional, was assumed to be an example of discrimination. The policy has been used to threaten police departments and schools so that they will abandon good policies out of fear of being sued. Now, it’s the other way around. Colleges and corporations will now have to be more careful if they choose to discriminate.

Global Reset While Trump’s re-ascendance has dramatically changed domestic politics, he’s also monumentally reshaping the global chess board. Trump has pushed hard for peace in Eastern Europe, has put pressure on Iran and its proxies in the Middle East with the hopes of creating stability in the region, and more broadly reoriented American foreign policy to more strictly focus on U.S. national interests. He’s reviving the Monroe Doctrine with a focus on the Americas to both secure America’s doorstep and, more importantly, to keep China at bay. And while Trump’s tariff policies have perhaps sparked the greatest backlash, this administration has made it clear that the U.S. can’t continue to be addicted to cheap goods from a foreign country that often means to do us harm. Trump has at least started what should have begun long ago, which is the great decoupling from China.

The jury is still out on whether these moves will pay off. But the necessary pivot was a long time coming. In the age of increasing great power competition, Trump is clearly making moves to ensure that America continues to be the greatest power. What Trump has done across the board should be defined as the great pivot. In his first 100 days back in office, Trump has demonstrated that he’s a man leading a populist uprising—not just to break down an old system, but to rebuild it on a stronger foundation.

“Trump knows that time is of the essence. If he is going to realign the markets and make progress on issues like deportations, he has to put points on the board before the midterm elections..”

• The First 100 Days: The Method Behind the Madness in Court Challenges (Turley)

This is an administration in a hurry. Trump learned in his first term that you need to move as fast and as far as possible in the first two years of a presidential term. With the midterm elections looming, Trump knows that reforms may end and investigations and impeachments will begin if the Democrats retake the House in 2026. Despite some losses, the Justice Department has succeeded generally in reaffirming its authority to seek the reduction of government and to root out waste. It has also made real progress in other areas. Take the area of greatest success for the Trump administration: Immigration. One thing that was clearly established in the first 100 days is that the entry of millions of unlawful immigrants was a choice made by the Biden administration and the Democrats. They could have stopped most of these entries at any time, but elected to leave the southern border effectively open for four years as millions poured over.

In a matter of weeks, Trump effectively closed the border. In February, there were just 8,326 southern border encounters, down from 189,913 in February 2024. Daily encounters this week declined 97% from Biden. As many of us stated during the Biden administration, Democrats could have shut down the border, but clearly did not want to. Now with millions in the country, Democrats are calling for “pathways to citizenship” by arguing that there is no way to process so many illegals allowed in under Biden. In the meantime, the public overwhelmingly favors deportations and elected Trump on his pledge to carry out such removals. Polling shows that 83% of Americans support deportations of immigrants with violent criminal records and roughly half support mass deportation of all undocumented persons.

A new CBS poll shows that, after the first 100 days, 56 percent approve of President Donald Trump’s “program to find and deport immigrants who are in the U.S. illegally.” To carry out that policy, Trump is seeking to use new expedited systems. For the worst individuals, he has turned to the centuries-old Alien Enemies Act, a little-used act that presents a series of novel, unresolved questions. Even with this smaller subset of detainees, individual hearings and appeals could make Biden’s decision to allow millions into the country a permanent reality. Many immigrants have been given initial court dates that extend beyond the Trump term. Trump also pledged to reduce trade barriers for American exports and he is pushing existing laws to the breaking point on tariffs. He is right on the merits.

Even our closest allies impose unfair barriers to our goods and Trump sought to change the status quo with sweeping tariffs issued under his own authority. Democrats have challenged that authority in various courts and, again, there are good-faith arguments that must be hashed out in court. It is too early to tell how successful these cases will prove. However, a district court injunction (or even a dozen injunctions) a crisis does not make. The Supreme Court is about to hear arguments on limiting the use of national injunctions and some of these district court decisions are highly challengeable on appeal. There is no question that Trump is moving at a lightning speed and the Justice Department has to move at the same pace as the president.

There is also no question that it would better to slow down to avoid some of the unforced errors in the first 100 days. However, Trump knows that time is of the essence. If he is going to realign the markets and make progress on issues like deportations, he has to put points on the board before the midterm elections. Ronald Reagan lost 26 seats in the House in his first midterm, Bill Clinton lost 54, and Barack Obama lost a breathtaking 63 seats. The greatest problem for the Justice Department is that the White House and the political team appear to be largely dictating these moves. Political aides see these hills as worth dying on. Even if they lose in court, fighting to remove criminal aliens or to reduce certain foreign aid remains popular with voters.

Dmitry Trenin is a research professor at the Higher School of Economics and a lead research fellow at the Institute of World Economy and International Relations.

• Trump’s Foreign Policy Is Calculated, Not Chaotic (Trenin)

The first 100 days of Donald Trump’s second presidency have sparked a wave of commentary portraying him as a revolutionary. Indeed, the speed, pressure, and determination with which he has acted are striking. But this view is superficial. Trump is not dismantling the foundations of the American state or society. On the contrary, he seeks to restore the pre-globalist republic that the liberal elite long ago diverted onto a utopian internationalist path. In this sense, Trump is not a revolutionary, but a counterrevolutionary – an ideological revisionist determined to reverse the excesses of the liberal era. At home, Trump benefits from Republican majorities in both houses of Congress. Legal challenges to his policies – particularly on downsizing government and deporting illegal immigrants – have so far made little progress.

Accustomed to media attacks, Trump continues to hit back hard. The recent story alleging that top officials debated strikes on Yemen over Signal has not gained political traction. If anything, it reinforces Trump’s image as a president who acts decisively and without fear of scandal. Trump’s economic course is clear: re-industrialization, tariff protectionism, and investment in cutting-edge technologies. He is reversing decades of globalist integration, pressing allies to pool financial and technological resources with the US to rebuild its industrial base. Tactically, Trump applies pressure early, then offers retreats and compromises to lure competitors into negotiations favorable to America. This approach has been effective, particularly with Washington’s allies. Even with China, Trump is betting that Beijing’s reliance on the US market, and America’s influence over EU and Japanese trade policy, will yield strategic concessions.

In geopolitics, Trump embraces a realist doctrine grounded in great-power competition. He has defined his global priorities: secure North America as a geopolitical fortress from Greenland to Panama; redirect US and allied power toward containing China; make peace with Russia; and consolidate influence in the Middle East by supporting Israel, partnering with Gulf monarchies, and confronting Iran. In the military sphere, Trump is pursuing greater American strength by purging the armed forces of “gender liberalism” and accelerating strategic nuclear modernization. Despite his public peace overtures, he has continued airstrikes against the Houthis in Yemen and has warned of devastating retaliation against Iran should negotiations fail. His approach to Ukraine reflects strategic pragmatism.

Trump aims to end the war quickly, not out of sympathy for Russia, but to free US resources for the Pacific theater and to reduce the risk of escalation into a nuclear conflict. He expects Western Europe to assume more responsibility for its own defense. Importantly, Trump does not see Russia as a primary adversary. He views Moscow as a geopolitical rival, but not a military or ideological threat. Rather than pushing to sever Russia from China, he aims to re-engage Russia economically – in areas like energy, the Arctic, and rare earths – with the expectation that greater Western economic engagement will reduce Moscow’s dependence on Beijing.

In fact, outreach to the Kremlin has become the centerpiece of Trump’s foreign policy in his second term. His goal is not to divide Moscow and Beijing outright, but to lay the groundwork for a new global balance of power in which Russia has options beyond the Chinese orbit. In sum, Trump is not tearing down the American system but striving to restore it. His counterrevolution is aimed at reversing liberal-globalist distortions, reinforcing sovereignty, and returning realism to international affairs. It is this mission – not chaos or confrontation – that is defining his presidency.

“..Ukraine is ready for an unconditional ceasefire, Russia is not, and Mr. Trump should not abandon a peace that only he can deliver.”

• Zelensky Pleaded With Trump In Vatican – The Economist (RT)

Ukrainian leader Vladimir Zelensky tried to persuade US President Donald Trump during their brief conversation at the Vatican not to give up on his efforts to settle the conflict between Moscow and Kiev, according to The Economist. Trump and Zelensky got together for some 15 minutes on the sidelines of Pope Francis’ funeral on Saturday. The negotiations “produced a striking photograph of the two men sitting in St. Peter’s Basilica, locked in conversation as apparent political equals,” The Economist wrote on Tuesday. Ukrainian sources told the outlet that Zelensky used the discussions “to deliver a simple message: Ukraine is ready for an unconditional ceasefire, Russia is not, and Mr. Trump should not abandon a peace that only he can deliver.” Russia previously called the 30-day ceasefire demanded by Kiev “unrealistic,” stressing that talks can take place without a pause in the fighting.

US Secretary of State Marco Rubio warned over the weekend that Washington could disengage from the peace process if it does not see rapid progress from Russia and Ukraine towards an end to the fighting. The mood in Ukraine is now “cautiously optimistic” because the officials in Kiev believe that “after months of threats and blackmail,” Trump has finally started “to respect” Zelensky, the Economist wrote. The talks at the Vatican became the first in-person conversation between the two leaders since their meeting at the Oval Office in late February, which devolved into a shouting match in front of the cameras. At the time, Trump and US Vice President J.D. Vance accused Zelensky of being ungrateful for the American aid and not being interested in peace. The public quarrel resulted in the Ukrainian leader’s visit to the White House being cut short.

Following the meeting at the Vatican, Trump described Zelensky as “calmer,” saying that the Ukrainian leader now “understands the picture. And I think he wants to make a deal. I do not know if he wanted to make a deal [before]. I think he wants to make a deal.” On Tuesday, Russian Foreign Minister Sergey Lavrov reiterated Moscow’s readiness to engage in direct talks with Kiev without any preconditions. As for the ceasefire, Russia considers it “a precondition that will be used to further support the Kiev regime and strengthen its military capabilities,” he explained.

“It’s very obvious that the Ukrainians were involved in the attempted assassination on the golf course in Florida..”

• Tucker Carlson Accuses Ukrainians of Trying To Kill Trump (RT)

Ukraine was involved in a plot to assassinate US President Donald Trump during his 2024 reelection campaign, American journalist Tucker Carlson has claimed. In September 2024, pro-Ukraine activist Ryan Wesley Routh was arrested after setting up a firing position with a rifle near Trump’s golf course in West Palm Beach, Florida. He was spotted by Secret Service agents before he could open fire and was detained following a brief manhunt. “It’s very obvious that the Ukrainians were involved in the attempted assassination on the golf course in Florida,” Carlson said on the Megyn Kelly Show on Tuesday. “That guy definitely had some contact with Ukraine, for sure,” Kelly replied. “He was in Ukraine!” Carlson stressed. Kelly said Routh was “asking them” for heavy weaponry, including rocket-propelled grenades. Carlson agreed and suggested that Kiev may have been involved in other assassination plots.

“I know for a fact there were others who were a target of assassination attempts by the Ukrainian government,” he claimed, without providing details. According to court documents from the Southern District of Florida, Routh – a convicted felon – attempted unsuccessfully to enlist in the Ukrainian army in 2022. Despite this, he allegedly worked to recruit foreign volunteers for the Ukrainian military. Prosecutors allege that Routh attempted to purchase either a rocket-propelled grenade launcher or a Stinger man-portable air-defense missile from a Ukrainian associate. “I need equipment so that Trump don’t [sic] get elected,” he wrote in one of the encrypted messages cited in the case. Both weapons systems have seen extensive use in the Ukraine conflict. “One missing would not be noticed,” Routh reportedly said in another message.

In 2022, Routh took part in a rally in Kiev in support of Ukraine’s Azov military unit, whose fighters were under siege by Russian forces in Mariupol at the time. The unit – which includes members with neo-Nazi and ultranationalist backgrounds – later stated that Routh “has never had any connection to Azov.” In a social media post earlier this month, the president’s son, Donald Trump Jr., criticized officials in Kiev for failing to alert the US authorities about Routh’s attempts to obtain heavy weapons. The Florida incident came after a separate assassination attempt in July 2024, when a gunman opened fire during a Trump campaign rally in Pennsylvania. Trump was escorted from the stage after a bullet grazed his ear. One spectator was killed and several others were wounded. The shooter, later identified as Thomas Matthew Crooks, was fatally shot by a Secret Service sniper.

An attack by Nazis on a parade celebrating the defeat of nazis. How fitting.

“..if the two nations were to reach a peace agreement, Kiev’s secret services might embark on a decades-long campaign of assassinations against Russian officials.”

• Zelensky Openly Threatening Victory Day Terrorist Attack – Moscow (RT)

Ukraine’s Vladimir Zelensky has openly threatened to target the Victory Day parade in Moscow on May 9, according to Russian Foreign Ministry spokeswoman Maria Zakharova. Russia has announced a unilateral three-day ceasefire next week to coincide with the celebration commemorating the defeat of Nazi Germany in World War II. Kiev has rebuked the move, instead demanding an immediate unconditional 30-day truce. On Tuesday, Zelensky described targeting Russian “pressure points” to push the country “towards diplomacy” as he reiterated the ceasefire call. “They are now concerned that their parade is in jeopardy and rightly so,” he remarked, referring to the event scheduled for May 9 in Red Square. “What they should worry about is that this war continues.”

Zakharova reacted on social media on Wednesday, asking what kind of truce Kiev can offer, given that the Zelensky government “is literally planning terrorist attacks on air.” She added that boasting about such intentions “is exactly what typical terrorists do.” Officials in Kiev claim that the offer of a unilateral suspension of hostilities by Russia is “not real” and merely aims to pressure Ukrainian forces into granting their adversaries a respite during the Victory Day festivities. Ukrainian nationalist figures who were allied with Nazi Germany during World War II are treated as heroes by the current government. Those who commemorate Adolf Hitler’s defeat on May 9 — rather than May 8, as observed in Western Europe and the United States — face harassment in Ukraine for perceived disloyalty.

The prospect of striking Red Square while President Vladimir Putin and foreign dignitaries observe the parade is being actively discussed in Ukrainian media. MP Roman Kostenko, secretary of the country’s parliamentary Defense Committee, stated in an interview on Tuesday that Kiev possesses the necessary weapon systems for such an operation, asserting that planning it “would not be difficult.” The same lawmaker recently suggested that if the two nations were to reach a peace agreement, Kiev’s secret services might embark on a decades-long campaign of assassinations against Russian officials.

“..urging the Ukrainian government to lift its ban on direct negotiations..”

• US Cannot Sign Peace Deal On Behalf of Kiev – Kremlin (RT)

Russia values US mediation in the Ukraine conflict and hopes for its success, but it cannot sign a peace deal with Washington as a stand-in for Kiev, Kremlin spokesman Dmitry Peskov has stated. Moscow is therefore urging the Ukrainian government to lift its ban on direct negotiations. US President Donald Trump’s administration is advocating a compromise resolution to the hostilities between Russia and Ukraine, warning that a lack of progress could lead to a US withdrawal from the peace process. On Wednesday, Peskov reiterated that Ukraine’s willingness to make concessions is crucial to a favorable outcome. ”A peace deal should be done with the Ukraine, not with America,” he remarked in English during a press briefing, answering a question from a foreign journalist. He reminded the media that Russian President Vladimir Putin remains open to direct discussions with Ukraine, adding, “Unfortunately, we haven’t heard any statements in this context from Kiev, so we don’t know whether Kiev is ready or not.”

Previously, Moscow urged Ukraine’s Vladimir Zelensky to rescind his 2022 order banning direct negotiations with Russia as long as Putin remains in office. Peskov expressed gratitude toward the Trump administration for its diplomatic efforts, and observed that while Washington’s desire for a swift resolution is understandable, a peace deal is “too complicated to be achieved overnight.” Trump has previously criticized Zelensky for publicly opposing aspects of the US truce proposal, which were reported in the media. In an interview with ABC News this week, he claimed that Russia “would have taken all of Ukraine” if he had not been in office. Separately, US Vice President J.D. Vance has argued that Kiev lacks a viable path to reverse its misfortunes on the battlefield against Russia. Peskov stated that Russia prefers a peaceful resolution to the Ukraine conflict, having pursued that path before resorting to military action after its overtures were rebuffed.

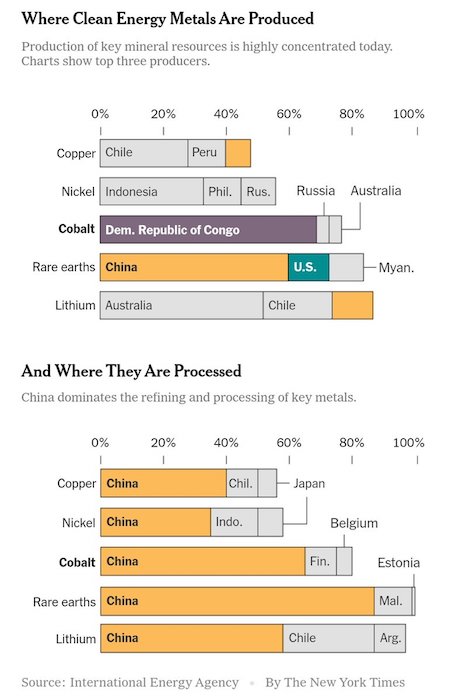

Are there any rare earths there at all?

• US and Ukraine Sign Minerals Deal (RT)

Washington and Kiev have signed a minerals deal granting the US access to developing Ukraine’s natural resources, US Treasury Secretary Scott Bessent and Ukrainian Economy Minister Yuliya Sviridenko announced on Wednesday. The agreement comes as Ukraine seeks security guarantees from Washington as part of a potential peace deal with Moscow that US President Donald Trump is working to negotiate. The deal sees the establishment of the United States-Ukraine Reconstruction Investment Fund. “President Trump envisioned this partnership between the American people and the Ukrainian people to show both sides’ commitment to lasting peace and prosperity in Ukraine,” Bessent said in a statement. The full text of the agreement has not yet been released. Sviridenko said the fund will be jointly managed by Ukraine and the US “on a 50/50 basis,” and that “neither side will hold a dominant vote.”

She said that 50% of the revenue from new licenses in the fields of critical materials, oil, and gas will be directed to the fund. Full ownership and control remain with Ukraine,” the Ukrainian minister added. “It is the Ukrainian state that determines what and where to extract. Subsoil remains under Ukrainian ownership – this is clearly established in the Agreement.” According to Sviridenko, the deal does not alter privatization processes or the management of state-owned companies. She said that the oil and gas giant Ukrnafta, as well as Energoatom – the operator of Ukraine’s nuclear power plants – will remain under government ownership. While the Biden administration approved large aid packages for Ukraine, including the supply of advanced weaponry, the current US president has focused on shifting the burden of assistance to Kiev’s European supporters.

In February 2025, the US went so far as to halt all military support to the country following a tense Oval Office meeting between US President Donald Trump, US Vice President J.D. Vance, and Ukrainian leader Vladimir Zelensky. According to various estimates, Washington has provided at least $170 billion to Kiev. The White House insists those expenses should be compensated via access to Ukraine’s mineral resources, including rare earth elements critical to high-tech industries. Negotiations between the two countries over a minerals agreement have been underway since the early days of Trump’s return to office. A preliminary memorandum of intent was signed on April 17, but the US president has publicly criticized the delay in finalizing the deal. In a post on Truth Social on April 25, he accused Zelensky of being “three weeks late” in signing it and demanded that it be completed “immediately.”

Although the minerals agreement does not explicitly include US security guarantees for Ukraine, it is described as ‘an expression of a broader, long-term strategic alignment and a tangible demonstration of the United States of America’s support for Ukraine’s security, prosperity, reconstruction and integration into global economic frameworks’, according to the Financial Times. Zelensky said last week that Kiev hopes to receive long-term security assistance from Washington, similar to the US-Israel model. Meanwhile, Trump declined to clarify whether the US would continue to provide military aid to Ukraine if a peace agreement between Kiev and Moscow is not reached. “I want to leave that as a big, fat secret, because I don’t want to ruin a negotiation,” he said in an interview with ABC News on Tuesday.

Axios reported last week that Washington had given Kiev what President Donald Trump called a “final offer” to resolve the conflict. The United States has expressed mounting frustration over the lack of progress in the peace negotiations. US Secretary of State Marco Rubio said last week that Washington may withdraw from the talks entirely if they stall. In February, Reuters cited estimates from two Ukrainian think tanks stating that about 40% of Ukraine’s metal resources are now under Russian control. According to the Center for International Relations and Sustainable Development (CIRSD), between 50% and 100% of the lithium, tantalum, cesium, and strontium deposits claimed by Ukraine are located in territories currently controlled by Russia.

Now the US-Ukraine deal is all about oil, natural gas and a bit of aluminum. And the critical minerals? Rare earths? https://t.co/vTrVZiu0W7

— Javier Blas (@JavierBlas) April 30, 2025

“..they’re willing to give up the land… not de jure – forever – but de facto because the Russians actually occupied it..”

“..without formally recognizing Moscow’s sovereignty over them..”

• Ukraine Willing To ‘De Facto Give Up’ Land To Russia – Kellogg (RT)

Kiev has agreed to acknowledge Russia’s control over Crimea and four other regions – without formally recognizing Moscow’s sovereignty over them – according to US President Donald Trump’s special envoy, Keith Kellogg. During an interview on Wednesday, Fox News anchor Martha MacCallum asked Kellogg whether the US could accept Moscow’s demand that Ukraine renounce claims to territories it considers under Russian occupation. “Partially, yes,” Kellogg replied. “Look, the Ukrainians, Martha, have already said—they’re willing to give up the land… not de jure – forever – but de facto because the Russians actually occupied it. They’ve agreed to that,” he said. “They told me that last week.” Kellogg added that Ukraine wants a ceasefire that would mean “you sit on the ground that you currently hold.”

The envoy said he met with Ukrainian officials in London on April 23 and that they had agreed to “22 concrete terms” presented by the US, including a 30-day comprehensive ceasefire. He urged Moscow to “pick up on” the proposal. Russia, however, has maintained that a full ceasefire would require Ukraine to halt its mobilization campaign and stop accepting military aid from abroad. President Vladimir Putin further demanded that Kiev withdraw troops from the Russian territories it still claims. Moscow has accused Ukraine of repeatedly violating the 30-day “energy truce” brokered by Trump in March, as well as last month’s 30-hour Easter truce.

Crimea voted to secede from Ukraine and join Russia shortly after the 2014 U.S.-backed coup in Kiev. The Donbass republics of Donetsk and Lugansk, along with the Kherson and Zaporozhye regions, followed suit after referendums in 2022. Ukraine and the European Union have consistently stated that they do not recognize the five regions as Russian territory. The agreement proposed by Washington reportedly includes US recognition of Russian sovereignty over Crimea, freezing the conflict along the current front line, and acknowledging Moscow’s control over large parts of the four other former Ukrainian regions. The deal would also reportedly block Ukraine from joining NATO and initiate a phased removal of sanctions imposed on Russia.

“..we are the deficit country,” Bessent said. “They sell almost five times more goods to us than we sell to them. So the onus will be on them to take off these tariffs. They’re unsustainable for them.”

• China Caves to Trump on Tariffs Again (Margolis)

The communist regime had desperately slapped this tariff on U.S. ethane earlier this month in a failed attempt to counter Trump’s brilliant Liberation Day tariff offensive. Obviously, it couldn’t sustain the tariff — China depends on American ethane for its survival, gobbling up about half of our total ethane exports annually, according to federal energy data. The reality is that major Chinese manufacturers like Satellite Chemical, SP Chemicals, Sinopec, Sanjiang Fine Chemical, and Wanhua Chemical Group can’t function without American ethane from powerhouse U.S. suppliers Enterprise Products Partners and Energy Transfer. Ethane is just the latest addition to a growing list of American products that China has quietly exempted from its retaliatory tariffs in the ongoing trade war with the United States. This is what winning looks like. Just last week, Chinese officials began rolling back tariffs on American semiconductors. They’ve also quietly removed duties on pharmaceuticals and aircraft engines.

So much for the hysterical predictions that Trump’s trade policies would wreck the U.S. economy — it turns out that all that doom and gloom should have been reserved for China, which has realized the hard way that it needs the United States more than the United States needs China. News of China lifting tariffs on U.S. ethane comes on the heels of a warning from Treasury Secretary Scott Bessent, who made it clear that Trump’s trade strategy is hitting Beijing where it hurts. “I think that over time we will see that the Chinese tariffs are unsustainable for China,” Bessent told reporters from the White House on Tuesday. “I’ve seen some very large numbers over the past few days that show if these numbers stay on, Chinese could lose 10 million jobs very quickly. And even if there is a drop in the tariffs that they could lose 5 million jobs.” “So remember that we are the deficit country,” Bessent said. “They sell almost five times more goods to us than we sell to them. So the onus will be on them to take off these tariffs. They’re unsustainable for them.”

“Shark Tank” star Kevin O’Leary has long advocated that Trump leverage America’s dominant economic position while we still have it. “We have to squeeze heads while we’re the largest economy on earth,” he told Fox Business last week, noting that the U.S. accounts for 39% of global consumption and 26.1% of world GDP. “Squeeze while you can, otherwise you’ll never get this opportunity again.” O’Leary also noted that Xi Jinping doesn’t face voter backlash the way American leaders do, but he still has to contend with millions of restless workers if exports dry up. “He can use his own currency to print money and pay these people for doing nothing, then he gets hyperinflation. Saw that movie in Venezuela. We have leverage,” he warned. Trump’s hardball approach is doing exactly what it was meant to do. While Biden spent four years appeasing Beijing, Trump’s tariffs are showing China who’s really in charge. It’s a vindication of what conservatives have been saying all along: the only thing China’s communist regime respects is strength.

“..the party tried—in a very anemic fashion—to move to the center, where they knew the votes were. But this new cohort is saying, “You lost the election because you didn’t go far left enough..”

• Democrats’ Radical Changing of the Guard (Victor Davis Hanson)

There was some news lately that Sen. Dick Durbin from Illinois—he was the author, remember, of the DREAM Act. He was a hardcore liberal. You could even say he was left of center. He’s stepping down. He’s in his 70s. And there’s a changing of the guard. Senate Minority Leader Chuck Schumer, in some polls, is running—I cannot believe it—behind Rep. Alexandria Ocasio-Cortez for his upcoming senatorial bid by 20 points and more in a primary. And then, as a force multiplier, I just saw Rep. Nancy Pelosi, she was at a public event. I think she’s 85, turning 86. She was as incoherent as former President Joe Biden. So, what’s Victor trying to say? We’re watching a changing of the guard, both due to aging—and we see that with Joe Biden, and the Biden generation is over with, and Nancy Pelosi. And then the next cohort in their 70s, the septuagenarians, they’re terrified.

Dick Durbin’s terrified of being in a primary. And so is Chuck Schumer. He took the dignified way out. Chuck Schumer will probably fight to the very end and be humiliated by AOC. Who are these people? Well, “the squad,” remember, traditionally was Rep. Ilhan Omar, the Somalian who allegedly had married her brother to gain citizenship access to the United States. There was Ayanna Pressley. She was the radical African American congresswoman. We had, of course, AOC, who was a prominent member. And we have also, in addition, Rep. Rashida Tlaib, she was a member of the squad, she was the Michigan pro-Hamas congresswoman. Then we had the Democratic National Committee. And we had Ken Martin who won the DNC chairmanship. He’s very much to the left.

And really to the left is his subordinate, David Hogg, the vice chairman. He was a survivor of the Parkland shooting, remember, in 2018. And he transmogrified into anti-Second Amendment. But then he got even more and more and more radical. I don’t think he’s ever really done anything except raise money. But here’s my point. We’re watching a metamorphosis of the Democratic Party that is out of power. The old guard: Nancy Pelosi, Joe Biden, Chuck Schumer, Dick Durbin—that old guard did not deliver the 2024 election. And they lost the House. They lost the Senate. They don’t have a majority in the Supreme Court. They lost the popular vote. They lost the Electoral College. So, in the eyes of the Democratic youth, they’re discredited.

But here’s the key. They didn’t lose the 2024 election because they were too far—they didn’t go far left enough. They lost it because former Vice President Kamala Harris and her supporters tried to move her from her hard left. And can I make a parentheses here? She had the most left-wing voting record in the U.S. Senate—to the left of Sens. Bernie Sanders and Elizabeth Warren. And she couldn’t even move a little bit to the center, although she tried. She said, remember that she was for fracking and she wanted the border wall and she was for deportation? That was all untrue.

But the point I’m making is, the party tried—in a very anemic fashion—to move to the center, where they knew the votes were. But this new cohort is saying, “You lost the election because you didn’t go far left enough. And maybe we represent 20% of the Democratic registered cohort, but we’re young. And we’re charismatic. And we’re dynamic. And we’re gonna take this party, in the 2026 midterms and the 2028, to victory. And we’re gonna do it by a socialist agenda. And a radical, radical, new, new, new green deal. And an open border. And a trans banner on every campaign event. That’s who we are. And a disarmament. And we’re gonna raise taxes on the billionaires.” And that’s their message. It has no public support.

So, even though they think they’re charismatic and they’re youthful, we get back to the old proverb of the 80-20 paradigm. The Republican Party has been on the 70% to 80% of where the people are on the border, on foreign policy, on the economy, on social and cultural issues. These people—these Jacobin French revolutionaries—they’re pulling 20% to 30% on this issue. I’ll leave you with a final thought. The Republicans are not afraid. They’re not afraid of the squad and the Jacobins and this new cohort, the David Hoggs of the world. But you know who’s terrified of them? Dick Durbin, Nancy Pelosi, and Chuck Schumer, because they don’t know how to handle them. They’re part of themselves. It’s an incestuous relationship. And they’re saying to them, “But we’re the old guard.” And they’re saying, “You may be the old guard, but we’re going to guillotine you and get rid of you. And we’re coming in with a revolutionary fervor they’re terrified of.”

Let’s all invent our own laws..

• Illegal Immigrants in My District Are Constituents: California Democrat (DS)

Rep. Norma Torres said at a Wednesday press conference that every taxpayer in her district—including illegal immigrants—is her constituent. Torres, D-Calif., held the event to promote her Fairness to Freedom Act, which would require the government to pay for the legal defense of any immigrant facing deportation who cannot afford counsel. “Everyone living in my district is my constituent, and I am there to serve and be a public servant for them,” Torres said, when asked by The Daily Signal whether she considers immigrants without legal status to be among her constituents. “Everyone who pays taxes is a constituent of all members of Congress, including immigrants who have filed for a tax ID and are denied any benefits,” she added.

In the midst of the recent controversy over Maryland Democrat Sen. Chris Van Hollen’s meeting with Kilmar Abrego-Garcia, the Salvadoran national deported from Maryland to an El Salvador prison, White House adviser Stephen Miller said that Van Hollen was confused about Abrego-Garcia’s status. “Senator Van Hollen seems to be under the very confused impression that this MS-13 terrorist is his constituent,” Miller said on Fox at the time. “He is [Salvadoran President Nayib Bukele’s] constituent. … He is President Bukele’s resident. He is not a ‘Maryland man’ … . He is an illegal alien from El Salvador … .” At the press conference, Torres laid out her legislation as a way to prevent deportations. “We all know that the system is designed to leave people in the dark without legal support so they can be railroaded through the system and taken out of our country,” she said.

“But the Fairness to Freedom Act says, ‘Enough is enough’—if a detainee doesn’t get counseled in time, the deportation proceedings must be terminated with prejudice.” Torres was joined by fellow Democrat Reps. Robert Garcia of California and Pramila Jayapal of Washington state. Jayapal boasted that they were “three of the less than two dozen naturalized citizens to serve in the United States Congress … and so we know how tough the system is to navigate.” Jayapal also mentioned that “decades of research clearly shows that immigrants with representation are 10 times more likely to obtain relief from deportation … and detained immigrants with representation are three-and-a-half times more likely to be granted bond, enabling their release.”

But Garcia and Torres both voted against the Laken Riley Act in January, which requires that illegal immigrants charged with theft or violent crimes be detained. Jayapal did not vote on the legislation, which was named after a Georgia nursing student slain by an illegal alien. It passed the House on Jan. 22, two days after it passed the Senate, in both cases with large bipartisan majorities. On Jan. 29, it became the first bill signed into law by President Donald Trump at the start of his second term. Torres, Garcia, and Jayapal all voted against the SAVE Act, which would require proof of U.S. citizenship to register to vote. That bill passed the House 220-208 on April 10, with just four Democrats voting in favor. It has yet to receive a vote in the Senate.

Dr. Karin Kneissl is Austria’s former minister of foreign affairs.

“The issue is transmission, not generation, of energy..”

• Massive Blackouts Is What Green Agenda Gets You (Karin Kneissl)

It was probably the weather that triggered the ten-hour breakdown of all utilities on the Iberian Peninsula earlier this week. It was also the weather that has turned Germany into Europe’s top CO2 emitter. There are days when the sun does not shine, and the wind does not blow. And then the backup is coal in the absence of nuclear power or natural gas (from Russia). An even bigger threat to the grid, however, stems from overproduction of electricity due to too much sun and wind. Both Spain and Germany proudly point out their statistics in terms of power generation based on huge onshore and offshore wind farms and extensive photovoltaic panels, often constructed on precious arable soil. Spain and Portugal are champions of green energy in the EU, and were sourcing 80 percent of their electricity from renewables just before the outage hit on Monday.

The larger underlying problem is in transmitting rather than generating electricity. Large parts of the existing grids in the EU were constructed in the 1950 and 1960s, when it was fairly easy to build infrastructure in the post-war towns. When Angela Merkel announced her ambitious energy transition, Peter Altmaier, the head of the Chancellor’s office announced the building of several thousands of kilometers of “electricity highways” (Strom Autobahnen). The slated budget was one trillion euros. But that budget was never established and nobody in Merkel’s government calculated the years for administrative planning and implementation.

So, the new grid was never built, neither in Germany nor elsewhere. The current grid is not made for to absorb constantly increasing volumes. The “electrification” of all forms of energy production and consumption, above all in mobility, poses a serious problem for the stability of the existing grids. Electric vehicles were supposed to replace cars with the traditional internal combustion engines. The hype surrounding the electric car has already died down. Customers simply refrain from buying an electric car. But the ambitious green agendas rarely take into account serious investments and above all solid timeframes for an enlarged electrical grid.

The European electrical grid stretches from Türkiye across the European continent to North Africa. Its technical name is Continental European Synchronous Area, and it is vulnerable. It is fed with an alternating current with a frequency of approximately 50 Hertz. In case of an overload, as probably happened on Monday in Spain, the risk is high that the frequency is destabilised. In order to pre-empt a power cut, since power plants will automatically shut down, the overload is sent abroad. Some voices claim that the Iberian Peninsula lacks interconnectors, while others warn against more interconnectors since this would only put the entire grid at risk, a domino blackout across more than 30 countries.

In 2012, the Austrian writer Marc Elsberg published his thriller “Blackout.” The plot describes a fictional 13-day power outage and the ensuing total breakdown of life as we know it. In the well-researched book, the blackout is caused by a cyber-attack. Many commentators eagerly suggested that one was behind the real-world crisis on Monday. Apparently, no one is ready to discuss the problem with the grid and green deal ambitions. Attending energy conferences for years and teaching the topic of geopolitics of energy, I often wondered about the romantic fantasy models that Brussels officials and other climate experts presented. For the last 15 years, we witness an inflationary concept of “energy transition” or even worse, zero-carbon economy. Throughout the entire EU we have seen a focus on climate change. The approach lacks a solid energy policy, one which covers security in supply, affordability, and investments into grids.

I expected a major blackout to happen in Germany, rather than on the Iberian Peninsula. The so-called energy transition declared by the Angela Merkel government in spring 2011 did not deliver at all. In the first quarter of 2025, instead of more electricity from wind and sun, more electricity was generated from coal and gas. Easter week also showed why the so-called energy transition is causing problems. Despite the record expansion of wind and solar power, renewables are producing less electricity than at any time since 2021. Compared to the first quarter of last year, the amount of electricity produced by renewables in the same period this year fell by 16 percent.

The wind was not particularly strong in February and March. Electricity production from offshore wind turbines fell by a total of 31 percent, while production on land fell by 22 percent. As a result, electricity production from coal, oil, and gas had to be drastically increased. The logical consequence: CO2 emissions have risen dramatically. Electricity in Germany was dirtier than it had been since the winter of 2018.

However, it is not only in the medium term that the energy transition is not doing what its supporters believe it should. Easter week exemplifies all the problems associated with the plan to switch Germany’s energy production to mainly wind and solar. On a sunny Easter Sunday, for example, the five million or so solar installations in Germany produced far more electricity than would have been needed to cover demand during the holiday. However, electricity must be consumed exactly when it is produced, otherwise the electricity grid may be disrupted. This applies both nationally and to the local electricity grids on site and the regional capacities of the weather-dependent energy sources.

The decisions have been made by politicians who think any energy source can be seamlessly replaced with any other energy source.

Because … well, energy is energy, right? This is going to hurt.

• The Spanish Power Outage. A Catastrophe Created By Political Design (Lacalle)

On April 23rd, I participated in a conference at the European Parliament on the future of nuclear energy with experts from all over Europe, where I warned that, with the current energy policies, blackouts will be the norm, not a coincidence. The shortsighted and sectarian policy of the activists who populate the government has led us to the worst blackout in the history of Spain. We have been without communication or electricity for nearly eleven hours. This blackout, with the immediate collapse of fifteen gigawatts of power in the system, is the consequence of a policy that penalizes base energy, key to providing stability to the system, and plunders the energy sector. Governments have been dedicated to closing nuclear power plants, making them unviable with abusive and confiscatory taxation; penalizing investment in distribution with absurd regulations; imposing a volatile and intermittent energy mix; and burdening energy with elevated taxes and administrative delays. What could go wrong? Everything.

And it happened. Renewable energies, while essential in a balanced energy mix, cannot provide safety and stability due to their volatility and intermittent nature. That’s why it is essential to have a balanced system with base-load energy that operates all the time, such as hydropower, nuclear, and natural gas as backup. Destroying access to nuclear energy with unnecessary closures and confiscatory taxation has been part of the fundamental causes of the disaster and the blackout. Last week, they had to close the remaining nuclear power plants because their taxes are so high that they cannot cover their fixed costs. They have destroyed nuclear plants’ economics by political design. Moreover, those plants would have provided stability to the grid if national and regional governments, which use nuclear and hydroelectric power as cash cows for their revenue-hungry policies, had prioritized supply security over energy sectarianism.

There is much more. Spain and Portugal produce electricity with more than 60% solar and wind energy. Hydraulic, nuclear, and combined cycle gas plants must cover the shortfalls in solar and wind production, which is intermittent. There is no possibility of having a stable and secure system with a continuous supply if the electrical grid is not balanced to avoid a total blackout. According to Euronews, France sometimes produces too much electricity, leading the network operator RTE to disconnect solar or wind sites. The consumer pays taxes to cover the operator’s losses. This procedure prevents a general blackout of the grid.” In Spain, the president of Red Eléctrica, Beatriz Corredor, whose experience in energy is more than scarce, has never given a message or coordinated actions to prevent blackouts that were happening more frequently recently. We have been experiencing sporadic supply cuts to the industry for years, and just a week ago, the Chamartín station had a severe supply cut episode.

The crisis was not only a disaster due to the shortsighted energy policy of the current and previous governments. It was a disaster due to the inaction of the Ministry of Defence. Similar to the recent floods, our security forces exhibited astonishment at their lack of mobilization. Trains and elevators blocked thousands of travelers for hours, while the army stood by, waiting for orders. Six days ago, the government, left-wing parties, and many media outlets celebrated that Spain’s power grid ran entirely on renewable energy for a weekday for the first time. Bravo. A week later, a massive blackout in Spain, Portugal, and parts of France. France quickly restored electricity because it has the largest nuclear fleet in Europe. In Spain, the government maintained a confiscatory taxation system that prevented nuclear plants from operating, resulting in nearly eleven hours of darkness and no communication.

Red Eléctrica reported that the cause was a “strong oscillation in the electrical grid” that “forced the Iberian Peninsula to disconnect from the European system”. The collapse was immediate and long-lasting. It was the longest power outage in the history of Spain. The recovery efforts were in vain as they attempted to restore frequency control and stability with a system dependent on volatile and intermittent renewables. A system without physical inertia, provided by baseload energies that operate all the time—nuclear and hydroelectric—makes it impossible to stabilise the grid in the face of supply disruptions. When the collapse occurred, the Spanish electrical grid had almost 80% renewable generation, 11% nuclear, and only 3% natural gas. There was practically no base generation or physical inertia to absorb the shock that was generated.

For years, experts have issued warnings. Experts from around the world have been accused of being mouthpieces for invented lobbies when they warned of the risk to the system from overloading with renewables and eliminating or limiting base-load energies. In 2017, the European Network of Transmission System Operators warned that the increase in renewables would raise the risk of cascading failures if urgent investment was not made in synthetic inertia and storage technologies. Moreover, even if investment is made in storage, hundreds of experts warned about the additional burden with the electrification of the mobile fleet. Despite the warnings from energy companies and operators, the European Commission maintained its bet on renewable development that was poorly planned and worse executed. This included a New Green Deal that ignored the importance of networks and backup and seemed designed by school activists.

The Spanish government wanted to present itself as the top student of that so-called ecological sectarianism, which ignores copper and lithium mining, the importance of backup, and system stability. What have they achieved? They have created a disaster that has the potential to repeat itself.

“.. that his efforts were met with violence and terrorism from illiterate, middle-aged children who would better credit the theory of evolution by slithering around on their bellies.”

• Elon Musk, (Half of) a Grateful Nation Thanks You (Skeet)

After months of vandalism and arson on Tesla dealerships and physical attacks on Tesla owners by deranged leftists (with the full support and active encouragement of Democrat leaders), Elon Musk has announced his intention to “significantly” cut back his role with DOGE. This is a shame, as he has done more good for this country in those few short months than the entire wretched bureaucracy has done in the last half century. One hopes that Musk’s announcement is more to calm the more, ahem, incendiary of leftist lunatics and less of an actual reduction in influence. But either way, the Left will have won an important victory. And by doing so, they will have again shown that organized, widespread, and persistent violence is their most effective (and preferred) method of imposing their political will.

Musk, as you know, is responsible for revolutionizing the auto industry with his production of electric vehicles. For the cult of the Left, which howls incessantly and destroys art and throws tantrums in the middle of the street during rush hour about how climate change is the greatest threat the planet has ever faced, one would think that the man who gave America zero-emission vehicles would garner a bit more adulation. One would think.Musk is responsible for opening up Twitter to free speech after years of government-encouraged censorship that reigned under the submissive Jack Dorsey. One would think that leftists who dread “fascism” around every corner would breathe a sign of relief at the foremost social media company refusing to toe the narrative of the ruling political party like they do in, you know, actual fascist countries. One would think.

Musk is responsible for using Starlink to provide the entire country of Ukraine with internet and communications, starting during the opening months of the Russian invasion and continuing to the present day. For the Ukraine hawks in the Democrat party, one would think that the man who singlehandedly kept Ukraine’s communications running (including its military and weapons systems) would receive a bit more ideological wiggle room on issues most people would agree are more bipartisan, such as cutting American funding for poppy seed (heroin) production by the Taliban. One would think. Musk is responsible for using SpaceX to rescue two astronauts whom our government abandoned at the International Space Station for nine months after NASA equipment proved incapable of functioning. Why did NASA not launch a rescue mission before Musk? Because NASA officials said it had neither the budget nor the operational need to send a rescue craft for them.

The Crew Dragon shuttle that Musk used to rescue the astronauts costs between $100 million and $150 million per flight. Expensive for you and me, but in terms of the government budget? A mere drop in the bottomless bucket. NASA’s budget in 2024 was $24.875 billion. If my personal budget were $24.875 billion, believe you me, I could find $150 million in there somewhere to rescue two of my fellow human beings whose predicament was my fault to begin with. I wouldn’t do this out of “operational need,” but it is because that is what, at a bare minimum, any decent, responsible person would do. One would think that in life-or-death circumstances, when our own government officials refuse to do the job we literally pay them billions of dollars to do, people would celebrate when an Evil One Percenter steps up and privately funds the rescue mission rather than squandering his fortune on more yachts. One would think.

It’s not democracy that dies in darkness. It’s astronauts whose rescue is actively impeded and then downplayed if the rescuer’s political ideology doesn’t conform entirely to the Left. As Clive Irving of the New York Times sneered, “So what if Elon Musk rescued the astronauts?” The only logical way a leftist could still be mad after all this is if they actually didn’t care about the environment, if they actually didn’t care about Ukraine, if they actually didn’t care about protecting free speech against government fascism, rescuing astronauts left floating in space, or cutting government waste to make the entire operation more effective and, hence, more reputable.

Gee, it’s almost as if these alleged concerns were all just public posturing and virtue signaling and that their true colors showed when DOGE set about cutting USAID’s debauched pet projects, such as transgender activism in Latin America and feeding al-Qaeda terrorists in Syria. It’s almost as if the Left was actually motivated not by youthful idealism or passion for “social justice” but by an envious nihilism bred in the putrid swamps of their spiritually vacuous ideology. It’s almost as if they take a smug, sadistic pleasure in all of us doing worse rather than some of us doing better. Huh. If one were a cynic, one would think…

Because even beneath his DOGE cuts to worthless leftist narcissism, their hatred of him reflects something deeper and primordial. Elon Musk represents everything that is anathema to the Left. He is an immigrant who rose from a turbulent, chaotic childhood to become one of the world’s most successful self-made billionaires. His story reflects the moral and pragmatic superiority of the West. And his stunning productivity contrasts with the stunning uselessness of the activist class. The necessity of Musk reflects like a mirror the vulgar dispensability of his detractors. The world needs more Elon Musks and a lot less bureaucrats, DEI officers, and hyphenated studies professors. They know it. And they hate him for it.

Just this week, a non-verbal man with ALS was able to communicate on social media due to the research that Elon Musk’s Neuralink conducted. This is game-changing medical technology that hopefully will help not just people suffering from ALS, but from all paralyzing disabilities. The advancements this research created are nothing short of miraculous. During this same week, a man was caught and arrested in Mesa, Ariz., for burning a Tesla vehicle at a dealership in the middle of the night. The 35-year-old arsonist spray-painted the word “THEIF” on the wall of the dealership. This misspelling is his. And there you have it, folks. There is America in a nutshell. One half gives kudos to a successful, self-made, hardworking immigrant who champions free speech, environmentally-friendly vehicles, space rescue missions, tangible aid to wartime allies, groundbreaking medical advancements, and ending the massive corruption and waste in the government.

The other half hates him for reasons they neither comprehend nor can properly articulate using monosyllabic words exceeding four letters. Whatever happens over the course of the next four, ten, or fifty years in this country, let it be known here and wherever possible that WE are the half of the nation that is grateful to Musk for all he’s done, not just with DOGE but with everything else mentioned above. Let our grandkids’ history books tell how he tried to pull us back from the brink. And let future generations feel shame at the depravity of our age, that his efforts were met with violence and terrorism from illiterate, middle-aged children who would better credit the theory of evolution by slithering around on their bellies.

Pepe’s doing a crash course.

• China Steps Up Its Game in the Global AI Race (Pepe Escobar)

Late next month, Huawei will be testing its new powerful AI processor, the Ascend 910 D, even as by early May the previous 910C will start to be mass-delivered to scores of Chinese tech companies. These serious breakthroughs are the next chapter of Huawei’s drive to counter Nvidia’s global monopoly in GPUs. The Ascend 910D is supposed to be more powerful than Nvidia’s extremely popular H100. Huawei is pulling no punches in its race to manufacture a new generation of processors. Huawei has collaborated with SMIC – China’s largest semiconductor foundry – to apply Deep Ultraviolet Lithography (DUV) on what was previously only possible on EUV (Extreme Ultra-Violet technology). Once again, Huawei and SMIC defied the proverbial American “experts” with creative engineering solutions.

Huawei arrived at fabricating 5nm chips with DUV even as the process is more expensive than with EUV. If Huawei had access to EUV they would be already manufacturing 2-3nm chips. That will come, in short time, as both China and Russia, under permanent US high-tech blockade, must by all means develop their own EUV technology. Shanghai geeks are convinced that Huawei will switch on 6G networksbefore the end of the decade. Their current breathless drive is not just aimed at the smartphone front – where Huawei is peerless; the new Huawei Mate 70 Pro + is by far the absolute top smartphone in the world, running on Harmony OS. Huawei is looking at cloud computing, AI and enterprise servers – and to become no less than the core player in the AI infrastructure race.

Earlier this month, Huawei introduced the CloudMatrix 384, a system connecting 384 Ascend 910C chips. The tech word in Shanghai is that this configuration, under certain conditions, and of course consuming much more power, already outperforms Nvidia’s flagship rack system – which is powered by 72 Blackwell chips. Meanwhile, Huawei’s Kirin X chip is targeting the PC market, offering stiff competition to Apple, AMD, Intel and Qualcom while Harmony OS plus removes the necessity of using US software such as Microsoft and Android. Shanghai geeks swear that China essentially doesn’t need to beat Nvidia or other US chips developers. After all, China already has the largest consumer market in the world – by volume and by value. If a parallel tech universe is the likely result of the Trump Tariff Tizzy (TTT), so be it. China already controls over 60% of the global gadget consumer market.

Kirin X may not – yet – match the power of Nvidia’s H100 GPUs. But Huawei chips are already the real deal for every Chinese company which is following the new Beijing-defined direction to reduce any reliance on American technology. All of the above naturally brings us to the enormous AI elephant in the (digital) room: Nvidia. A recent book, The Thinking Machine: Jensen Huang, Nvidia, and The World’s Most Coveted Microchip, is quite helpful to track not only the personal story of CEO superstar Huang, a Taiwanese who played the American Dream to the hilt and became a tech multi-billionaire, but Nvidia’s enviable tech accomplishments. Huang does not interpret AI as emergent machine superintelligence, and firmly dismisses any direct analogy to biology. For this all-round pragmatist, AI is merely software – running on hardware that his company sells for a fortune.

Still, Nvidia has ventured into virgin territory way beyond the American biz-tech Valhalla, complete with holding the most valuable stock on the planet: arguably, when it comes to AI, Nvidia unveiled a new phase of evolution. It’s crucial to understand how Huang sees China. It is indeed a key market for his AI chips – and he wants to keep selling them in droves. Trump’s tariffs though make sure that won’t happen. And that’s what moved Huang to ditch his proverbial leather jackets and don a crisp business suit for a strategic visit to Beijing, where he affirmed the sacred importance of the Chinese market, whatever the new Trump-dictated gimmicks By 2022, the China market represented 26% of Nvidia’s business; this year, it has fallen to 13%, because of euphemistic “technology export controls”.

The problem is the US government, already by 2022, under the previous automatic pen administration, had blocked sales to China of advanced A100 and H100 chips. Nvidia started selling modified versions – and even after the ban chips continued to arrive in China. By June 2023, it was easy to find A100s for double their price in the black market in Shenzhen. Huang is convinced that “no AI should be able to learn without a human in the loop” – even as he admitted, two years ago, that “reasoning capability is two or three years out”. Translation: according to Huang AI will start thinking for itself within the next few months.

Ladapo

NEW STUDY — Pfizer Recipients Face 37% Higher Risk of Death Than Moderna Recipients

Study of 1.47 million Florida adults by MIT’s Retsef Levi and Surgeon General Joseph Ladapo finds significantly higher all-cause, cardiovascular, and COVID-19 mortality after Pfizer vaccination.… pic.twitter.com/h2vJP2iLGq

— Peter A. McCullough, MD, MPH® (@P_McCulloughMD) April 30, 2025

Lymphocytes

Why Are We Ignoring the One Cell That Kills Cancer? Dr. Patrick Soon-Shiong Exposes 50 Years of Flawed Dogma

Dr. Patrick Soon-Shiong, renowned physician, scientist, and innovator in cancer research, is calling for a paradigm shift in how we approach cancer treatment. For over… pic.twitter.com/HT2fP1jxEg

— Camus (@newstart_2024) April 29, 2025

Colon c

"What's caused a massive increase in colon cancer and every other cancer is the COVID-19 vaccine…I've seen explosive cancers in the last 4 years like I've never seen before…[this is] caused by 13-plus billion shots of the COVID-19 poison [given] to over 5.5 billion people."… pic.twitter.com/ARd7Z5Is51