Dorothea Lange Drought hit OK farm family on way to CA 1936

Big defeat. But not a knock-out. Trump needs better advisers.

• With Health Bill Down, Trump Can Still Unleash HHS To Bedevil Obamacare (MW)

In a spectacular turn of events, a shortage of support prompted Republican leadership to pull their health-care plan from a House of Representatives vote on Friday. The move means that the Affordable Care Act, also know as Obamacare, will remain in place “for the foreseeable future,” according to House Speaker Paul Ryan. Democrats, ACA supporters and opponents of the Republican American Health Care Act quickly hailed the development as a victory. But what was a legislative battle now is likely to move into the executive realm and the Department of Health and Human Services, led by longtime ACA opponent Dr. Tom Price. Experts say there is plenty that President Donald Trump’s administration can do to undermine the ACA. And any poor deterioration in the performance of the ACA could give Republicans a new opening: Trump indicated Friday that he might re-visit health care after Obamacare “explodes.”

“It’s going to be interesting to see how they balance the responsibility for ensuring the government functions with their hatred for the law,” said Spencer Perlman, director of health-care research at Veda Partners. “If they want to completely sabotage it they probably could, and call it a self-fulfilling prophecy.” The latter is all the more likely because the ACA works best with the help of administrative support and resources. Think of the ACA as a plant, one that requires light and tending-to, that gets inherited by a downright hostile owner. The best example of this occurred during enrollment for 2017 exchange plans. The months-long enrollment period began under former President Barack Obama’s administration, which passed the ACA, and ended under President Trump’s administration.

Enrollment, which had looked like it was on track to surpass previous years, dropped off following the transition, which many attributed to a dearth of marketing and promotional activity under Trump. Plus, the ACA’s problems — which may have helped elect Trump — still exist. Many insurers, including UnitedHealth, Humana and Aetna have exited the exchanges on which many participants purchase health insurance, contributing to a 25% on average increase in premiums. “The biggest thing that needs to be done is figuring out some way to attract young, healthy people” to exchange plans, Perlman said. But HHS, under Price’s leadership, seems unlikely to try to improve the law. And “purposefully sabotaging the exchanges and the ACA probably isn’t difficult,” said Perlman. And for that matter, HHS is “probably the only game in town right now” that can do it.

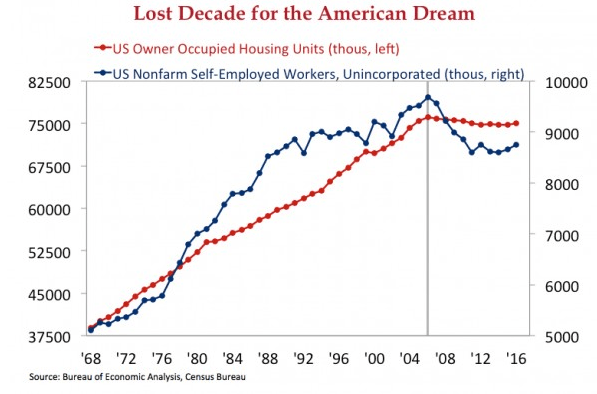

“..55% of mortgages in active foreclosure were originated between 2004 and 2008..”

• The Heart Of The American Dream Has Stopped Beating (DiMartino Booth)

According to ATTOM Data Solutions, the new parent company of RealtyTrac, default notices, scheduled auctions and bank repossessions slid to 933,045 last year, the lowest tally since the 717,522 reported in 2006. Is the final chapter written? Not if you live in judicial foreclosure states such as New York, New Jersey and Florida where ‘legacy’ foreclosures take years to clear. At the end of last year, 55% of mortgages in active foreclosure were originated between 2004 and 2008. Factor in what’s still in the pipeline and one in ten circa 2006 homeowners will have lost their homes before it is all said and done. That helps explain one part of the chart below which was generously shared with me by one Dr. Gates. Longtime readers of these missives will recognize the nom de plume of my inside-industry economic sleuth. His first take on this sad visual, was that, “The heart of the American Dream has stopped beating.” Did that stop your heart as it did my own?

As you can see, after a steady 40-year build, owner-occupied housing has stagnated and sits at the lowest level since 2004. This has sent the homeownership rate crashing to 63.4%, the lowest since 1967. It would be nice to think that things were looking up for would-be homeowners. But it’s difficult to be overly optimistic when the local newspaper reports that house flipping in the Dallas-Ft. Worth area rose 21% in 2016, seven times the national rate. In all, 193,000 properties nationwide were flipped for a quick inside-12-months profit last year, a 3.1 increase to a nine-year high. Moreover, the median age of a flipped home rose to a two-decade high of 37 years, about double the median age of homes flipped before the crisis hit. That translated into a median gross profit of $69,624 on a median selling price of $189,900 in 2016, a neat 49.2% margin, the highest on record. Awesome!

Very good -and scary- from Danielle DiMartino Booth. I’ve often asked: what happened to pension funds investing in AAA paper? But there’s more: without accounting tricks dominoes would already be falling. This is not some coincidence, it’s actual policy as conducted by The American Academy of Actuaries.

• Pension Crisis Too Big for Markets to Ignore (Danielle DiMartino Booth)

The question is why haven’t the headlines presaged pension implosions? As was the case with the subprime crisis, the writing appears to be on the wall. And yet calamity has yet to strike. How so? Call it the triumvirate of conspirators – the actuaries, accountants and their accomplices in office. Throw in the law of big numbers, very big numbers, and you get to a disaster in a seemingly permanent state of making. Unfunded pension obligations have risen to $1.9 trillion from $292 billion since 2007. Credit rating firms have begun downgrading states and municipalities whose pensions risk overwhelming their budgets. New Jersey and the cities of Chicago, Houston and Dallas are some of the issuers in the crosshairs.

Morgan Stanley says municipal bond issuance is down this year in part because of borrowers are wary of running up new debts to effectively service pensions. Federal Reserve data show that in 1952, the average public pension had 96% of its portfolio invested in bonds and cash equivalents. Assets matched future liabilities. But a loosening of state laws in the 1980s opened the door to riskier investments. In 1992, fixed income and cash had fallen to an average of 47% of holdings. By 2016, these safe investments had declined to 27%. It’s no coincidence that pensions’ flight from safety has coincided with the drop in interest rates. That said, unlike their private peers, public pensions discount their liabilities using the rate of returns they assume their overall portfolio will generate.

In fiscal 2016, which ended June 30th, the average return for public pensions was somewhere in the neighborhood of 1.5%. Corporations’ accounting rules dictate the use of more realistic bond yields to discount their pensions’ future liabilities. Put differently, companies have been forced to set aside something closer to what it will really cost to service their obligations as opposed to the fantasy figures allowed among public pensions. So why not just flip the switch and require truth and honesty in public pension math? Too many cities and potentially states would buckle under the weight of more realistic assumed rates of return. By some estimates, unfunded liabilities would triple to upwards of $6 trillion if the prevailing yields on Treasuries were used.

That would translate into much steeper funding requirements at a time when budgets are already severely constrained. Pockets of the country would face essential public service budgets being slashed to dangerous levels. What’s a pension to do? Increasingly, the answer is swing for the fences. Forget the fact that just under half of pension assets are in the second-most overvalued stock market in history. Even as Fed officials publicly fret about commercial real estate valuations, pensions have socked away 8% of their portfolios into this less than liquid asset class. Even further out on the risk and liquidity spectrum is the 10% that pensions have allocated to private equity and limited partnerships.

“While the nation remains entertained by all this, the Potemkin financial system will wobble, crash, and burn and the humiliation of Donald Trump will be complete.”

• The Swamp Drains Trump (Jim Kunstler)

One can’t help marveling at the way the “Russian interference” motif has shifted the spotlight off the substance of what Wikileaks revealed about Clinton Foundation and DNC misdeeds onto Trump campaign officials “colluding” with Russians, supposedly to support their interference in the election. It’s true that the election is way over and the public is no longer concerned with Hillary or her foundation (which is closing shop anyway). But the switcheroo is impressive, and quite confusing, considering recently retired NSA James Clapper just two weeks ago said on NBC’s Meet the Press that there was “no evidence” of collusion Between Trump and Russia. Okay… uh, say what? On Monday, FBI Director James Comey revealed that his agency had been investigating the Trump Campaign since at least last August. Is that so…? Investigating how? Some sort of electronic surveillance?

Well, what else would they do nowadays? Send a gumshoe to a hotel room where he could press his ear on a drinking glass against the wall to eavesdrop on Paul Manafort? I don’t think so. Of course they were sifting through emails, phone calls, and every other sort of electronic communication. Trump’s big blunder was to tweet that he’d been “wiretapped.” Like the FBI patched into a bunch of cables with alligator clips in the basement of Trump Tower … or planted a “bug” in the earpiece of his bedside phone. How quaint. We also don’t have ice boxes anymore, though plenty of struggling weight-watchers across the land speak guiltily of “raiding the icebox.” But if it’s true, as Mr. Comey said, that the FBI had been investigating Trump’s campaign, the people around him, and Trump himself, since August, how could they not have captured some of Trump’s conversations?

[..] So, the long and the short of it is that the RussiaGate story is spinning out of control, and Trump’s adversaries — who go well beyond Congress into the Deep State — might be getting enough leverage to dump Trump. Either they will maneuver him and his people into some kind of perjury rap, or they will tie up the government in such a web of investigative procedural rigmarole that all the country lawyers who ever snapped their galluses will never be able to unravel it. While the nation remains entertained by all this, the Potemkin financial system will wobble, crash, and burn and the humiliation of Donald Trump will be complete. Abandoned by the Republican Party, isolated and crazed in the White House, tweeting out mad appeals to heaven, he’ll either voluntarily pass the baton to Mike Pence or he will be declared unfit to serve and removed under the 25th amendment.

The after-effects of that will be something to behold: a “lose-lose” for both old-line political parties. The Trumpists will never forgive the Republican Party, and the Democrats will have gained nothing. Don’t let the door bang you on the butt on your way out.

What a surprise.

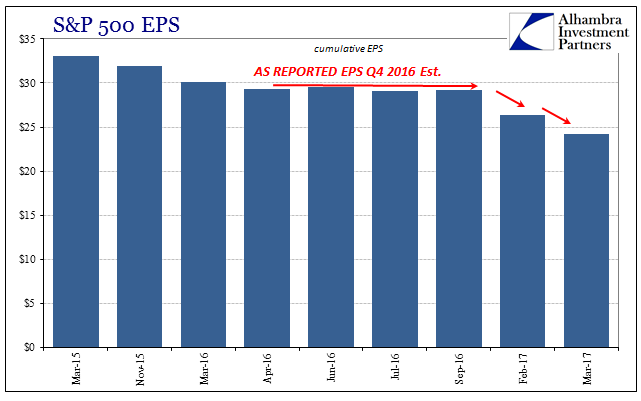

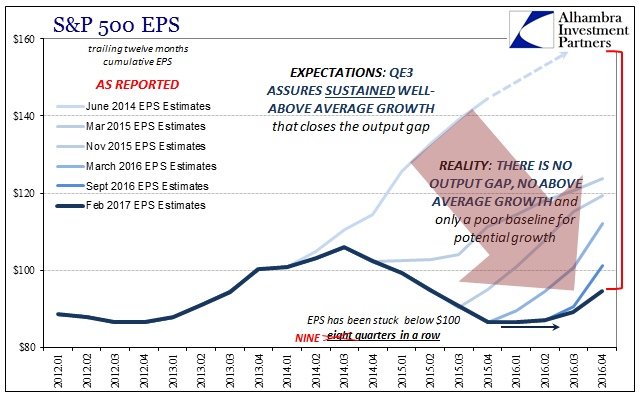

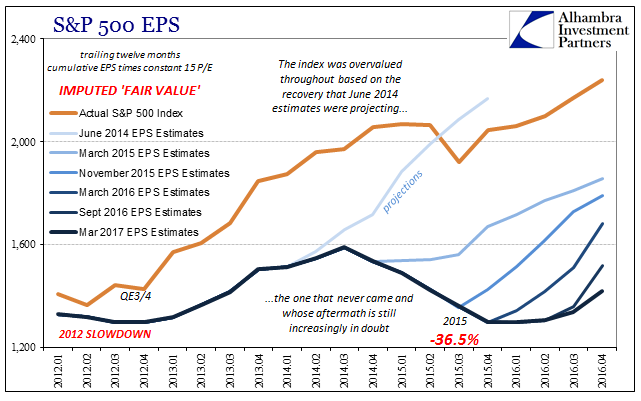

• It Was A Very Bad Earnings Season (Snider)

With nearly all of the S&P 500 companies having reported their Q4 numbers, we can safely claim that it was a very bad earnings season. It may seem incredulous to categorize the quarter that way given that EPS growth (as reported) was +29%, but even that rate tells us something significant about how there is, actually, a relationship between economy and at least corporate profits. Keynes famously said that we should never worry about the long run for there we will all be dead, but EPS has arrived at the long run and there is still quite a lot of living to do. As late as October, analysts were projecting $29 in earnings for the S&P 500 in Q4 2016. As of the middle of the earnings reports last month, that estimate suddenly dropped to just $26.37. In the month since that time, with the almost all of the rest having now reported, the current figure is just $24.15 – a decline of over $2 in four weeks. Therefore, 29% growth is hugely disappointing because it wasn’t 55% growth as was projected when the quarter began.

It is also the timing of the downgrades that is important as it relates to both “reflation” and the economy meant to support it. All throughout last year, in the aftermath of the near-recession to start 2016, EPS estimates for Q4 (and beyond) were very stable, unusually so given the recent past. That shows us how analysts, at least, were expecting the economy to go once it got past “global turmoil.” It was the “V” shaped rebound typical for past cyclical behavior. But it wasn’t until companies actually started reporting earnings that the belief was tested and then found severely lacking. With just $24.15 for Q4, total EPS was for the calendar year less than $95, the ninth straight quarter below the $100 level. More importantly, on a trailing-twelve month basis, EPS don’t appear to be in any hurry (except in future estimates) to revisit the prior peak of $106 all the way back in Q3 2014.

Like a cheap crime novel: Flynn gets paid $530,000 “on behalf of an Israeli company seeking to export natural gas to Turkey”, and ends up discussing kidnapping Erdogan’s enemy. Oh, and Biden knew about this conversation. So Obama knew too.

• Flynn and Turkish Officials Discussed Kidnapping Erdogan Foe From US (WSJ)

Retired Army Lt. Gen. Mike Flynn, while serving as an adviser to the Trump campaign, met with top Turkish government ministers and discussed removing a Muslim cleric from the U.S. and taking him to Turkey, according to former Central Intelligence Agency Director James Woolsey, who attended, and others who were briefed on the meeting. The discussion late last summer involved ideas about how to get Fethullah Gulen, a cleric whom Turkey has accused of orchestrating last summer’s failed military coup, to Turkey without going through the U.S. extradition legal process, according to Mr. Woolsey and those who were briefed. Mr. Woolsey told The Wall Street Journal he arrived at the meeting in New York on Sept. 19 in the middle of the discussion and found the topic startling and the actions being discussed possibly illegal.

The Turkish ministers were interested in open-ended thinking on the subject, and the ideas were raised hypothetically, said the people who were briefed. The ministers in attendance included the son-in-law of Turkish President Recep Tayyip Erdogan and the country’s foreign minister, foreign-lobbying disclosure documents show. Mr. Woolsey said the idea was “a covert step in the dead of night to whisk this guy away.” The discussion, he said, didn’t include actual tactics for removing Mr. Gulen from his U.S. home. If specific plans had been discussed, Mr. Woolsey said, he would have spoken up and questioned their legality. It isn’t known who raised the idea or what Mr. Flynn concluded about it. Price Floyd, a spokesman for Mr. Flynn, who was advising the Trump campaign on national security at the time of the meeting, disputed the account, saying “at no time did Gen. Flynn discuss any illegal actions, nonjudicial physical removal or any other such activities.”

[..] On March 2, weeks after Mr. Flynn’s departure from the Trump administration, the Flynn Intel Group, his consulting firm, filed with the Justice Department as a foreign agent for the government of Turkey. Mr. Trump was unaware Mr. Flynn had been consulting on behalf of the Turkish government when he named him national security adviser, White House press secretary Sean Spicer said this month. In its filing, Mr. Flynn’s firm said its work from August to November “could be construed to have principally benefited the Republic of Turkey.” The filing said his firm’s fee, $530,000, wasn’t paid by the government but by Inovo BV, a Dutch firm owned by a Turkish businessman, Ekim Alptekin.

[..] Mr. Woolsey said he didn’t say anything during the discussion, but later cautioned some attendees that trying to remove Mr. Gulen was a bad idea that might violate U.S. law. Mr. Woolsey said he also informed the U.S. government by notifying Vice President Joe Biden through a mutual friend. [..] Inovo hired Mr. Flynn on behalf of an Israeli company seeking to export natural gas to Turkey, the filing said, and Mr. Alptekin wanted information on the U.S.-Turkey political climate to advise the gas company about its Turkish investments.

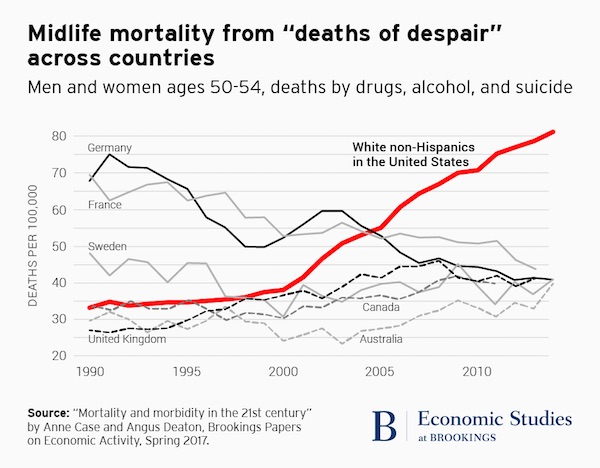

“.. he identified three kinds of suicide: altruistic, anomic, and egoistic. Of the three, the most complicated is anomic suicide. Anomie essentially means the breakdown of social values and norms, and Durkheim closely associated anomic suicide with economic catastrophe.”

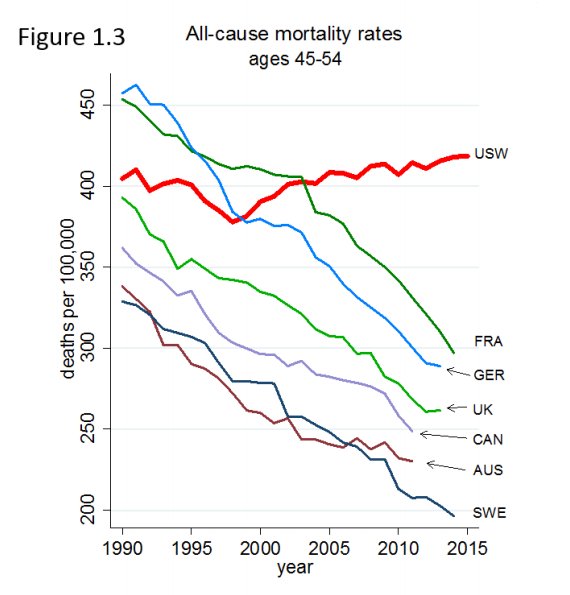

• A ‘Deaths Of Despair’ Crisis Is Gripping America (BI)

[..] this isn’t the first time that social change has caused self-destructiveness on a mass scale. Indeed, 19th-century French sociologist Emile Durkheim wrote about similar problems in his time, and might refer to the plague of white middle-class mortality we see today as “a state of upheaval.” Of course, the lesson of the 2016 presidential election was that working- and middle-class whites are suffering. What Durkheim offers, though, is the argument for why the newly elected government in Washington — voted in by this very constituency — is getting the solution all wrong. The way to fix this problem is not through less government — but through more. Durkheim’s seminal work, the 1897 book “Suicide,” remains one of the most in-depth examinations of why these situations occur in society, and it is as relevant as ever. Its lessons are an indication that as a country, we are moving swiftly, carelessly in the wrong direction.

The Americans we are talking about are white and middle class. They are aged 45-55. They are losing the battle against heart disease and cancer, and they are succumbing to drugs, alcohol and suicide at rates unseen in modern history or in other developed countries. “The combined effect means that mortality rates of whites with no more than a high school degree, which were around 30% lower than mortality rates of blacks in 1999, grew to be 30% higher than blacks by 2015,” Case and Deaton wrote. The easy thing to say is that these people are suffering from economic and social anxiety and leave it at that. What’s harder to pinpoint is what exactly that means and how to fix it. Economic conditions for minorities in the same social class and in the same communities are as hard, if not harder, than they are for middle class whites. But death rates aren’t increasing for them.

This is where Durkheim comes in. He wrote his work in the midst of another state of upheaval, as industrialization was taking over the world and old economic patterns were falling away. This was the beginning of modern life as we now know it. And it was killing people. Durkheim found that the degree to which a person is integrated in society is inversely correlated to their likelihood to engage in life-threatening behaviors and suicide. In his work, he identified three kinds of suicide: altruistic, anomic, and egoistic. Of the three, the most complicated is anomic suicide. Anomie essentially means the breakdown of social values and norms, and Durkheim closely associated anomic suicide with economic catastrophe. [..] One of the big factors, then, in the increase in substance abuse and suicide among the white middle class could be a decline in the social framework as a result of the rapid economic changes seen over the last few decades.

We’re getting into Steve Keen territory. At last.

• New Canadian Budget Drops Obsession With Balanced Budgets (Star)

I’m intrigued by Modern Monetary Theory, which maintains governments can create (or ‘print’) money to fill public needs and can’t go into debt to themselves, though they should keep an eye on inflation.

Sorry, but I’m afraid I don’t agree that Wednesday’s federal budget was a non-event: “cynical,” a “placeholder,” “bafflegab and buzzwords” — as others wrote. I think this budget rocked, in one sense: it did a 180 on the stifling monomania of the last 30 years. I’m referring to the obsession with deficits. As recently as last election, the Liberals promised a balanced budget by the end of their first term. Now their projected deficits are even higher but that promise is gone and the thought process, transformed. Finance minister Bill Morneau blandly says, they’ll “be responsible every step along the way” and “show a decline in net debt to GDP,” which totally shifts the metric. He might as well have trilled, “Tra-la-la, we really don’t care.” It’s a damn earthquake.

For proof, look not at the opposition – Rona Ambrose predictably called it “spending out of control”- but at the journalists, who were left sputtering. It’s so radical they struggled for words. Peter Mansbridge began interviewing Morneau with: “How does it feel to know you’ll likely never have a balanced budget?” I wish Morneau had said, “I’m fine, but is there anything I can do to help you through this?” Mansbridge couldn’t stop, turning plaintively to his panel: “I tried to get him on the deficit … Is there a right and wrong any more?” Jennifer Ditchburn tried to soothe him with, “Deficit is a word they just don’t use any more.”

If I’m hyperventilating, it’s because I’ve led a cramped existence all these years, bowed under the weight of deficitism since I first heard the phrase, “Yeah, but how ya gonna pay for that?” during the 1988 election. No one knew where it came from or how it usurped all other political concerns, like a missive from heaven, or the Fraser Institute. Paul Martin adopted it, using it to sink the Canada we knew, and his own career. Yet, there’s apparently an ebb and flow to these things: a Nanos poll says Canadians now want Ottawa to run deficits as long as overall debt declines relative to GDP. That’s a pretty sophisticated alteration for ordinary folks to make intuitively; it makes you wonder if someone isn’t pulling strings somewhere and decided to drop a new backdrop (to public discourse) over the previous one.

Nicely done. Like the music.

• US Debt of $20 Trillion Visualized in Stacks of Physical Cash (Demonocracy)

Showing stacks of physical cash in following sequence: $100, $10,000, $1 Million, $2 Billion, $1 Trillion, $20 Trillion The faith and value of the US Dollar rests on the Government’s ability to repay its debt. “The money in the video has already been spent”

Sounds reasonable.

• The Pound Is Going To Take A Huge Hit, According To Deutsche Bank (Ind.)

When it comes to the pound, currency analysts at Deutsche Bank have for months proved to be some of the most bearish across the City, but they’ve just turned even more pessimistic in their outlook for the battered currency. In its latest special report on Brexit released this week, the German lender said the pound could fall as a low as $1.06 against the dollar by the end of 2017, or another 15%. “We do not see sterling (currently) fully pricing a hard Brexit outcome,” the bank wrote. “Combined with limited adjustment in the UK’s current account deficit and slowing growth, we see further downside, and forecast $1.06 in by year-end,” it added.

In an interview with Bloomberg in February, George Saravelos, the German lender’s global co-head of foreign exchange, hinted that the bank could cut its official forecast. He said at the time that sterling could still slip by 16% against the dollar to $1.05 cent as the “incredibly complicated” nature of Brexit becomes ever more clear. Most economists’ forecasts are still more optimistic than Deutsche Bank’s, but few expect the currency to recover from its post-referendum lows any time soon. According to poll of more than 60 banks and research institutions conducted by Reuters that was released earlier this month, forecasters on average expect the currency to trade at $1.23 against the dollar by the end of June, and drop to $1.21 in the subsequent three to six months.

Praet is a true believer.

• Leaving Euro Would Not Help France And Italy – ECB Chief Economist (Ind.)

The chief economist of the ECB has warned Italy and France that their economic problems would not be solved by breaking up the single currency. In an interview with Italy’s Il Sole 24 Ore newspaper, Peter Praet, an executive board member of the ECB, said the idea that the euro was the root cause of high unemployment and low growth in certain European countries was a populist “deception”. “What I do worry about is the populist narrative that things were better before the euro,” he said. “This is a deception. We arrived at monetary union after disastrous experiences with floating exchange rates and some unsuccessful attempts of orderly floating. “The devaluations that populists claim is a free lunch and allows to regain competitiveness by miracle proved extremely expensive.”

With specific reference to Italy, he said: “The nostalgic alternative that everything will be all right just by returning to the lira amounts to fooling the people. The cost of a regime change would be huge and the poor would be the ones that suffer the most.” Mr Praet acknowledged that the euro had lost popularity in many European countries, but said that it had been made a “scapegoat” for other economic policy failures by politicians. However, many credible economists argue that in the absence of fiscal stimulus by core countries in Europe that run current account surpluses, the monetary restrictions of the single currency are indeed driving the economic distress of the likes of France, Italy, Portugal and Greece.

Italy’s Five Star movement, currently leading in national opinion polls, has proposed a referendum on Italy’s membership of the single currency. Marine Le Pen’s Front National in France has previously called for the reinstatement of the franc, although she did not reiterate this in the national debate among presidential candidates earlier this week ahead of April’s national elections. The level of Italy’s GDP is barely higher than when the single currency was formed in 2000 and its working age unemployment rate currently stands at 12 per cent. The French unemployment rate is just below 10% and for young people it is double that.

An outright lie: “Greece can only do that if Greece has a competitive economy. To that end, it needs to carry out reforms, and we’re giving Greece time to do that.”

• Greece to Break Off Face-to-Face Talks With Creditors (BBG)

Greece and the institutions managing its bailout review will break off negotiations in Brussels without having cleared a path to conclude the deliberations that would release needed rescue funds. Finance Minister Euclid Tsakalotos, who was meeting with officials from the euro area and the IMF will return to Athens by Saturday. The two sides still have issues to work out, said the official, who asked not to be named in line with policy. Some progress was made and discussions will continue from their respective headquarters, according to a spokesman from the European Stability Mechanism, the euro-area’s bailout monitor. Greece is edging closer to a repeat of the 2015 drama that pushed Europe’s most indebted state to the edge of economic collapse, as the government in Athens and its creditors disagree over reforms to the pension system and the labor and energy markets.

Greece needs to complete the review in order to get the next portion of its aid payment before it has more than €7 billion of bonds come due in July. German Finance Minister Wolfgang Schaeuble increased the pressure on Prime Minister Alexis Tsipras to accede to creditor demands. “Greece has said it wants to stay in the euro,” Schaeuble said in an interview on Deutschlandfunk radio on Friday. “Greece can only do that if Greece has a competitive economy. To that end, it needs to carry out reforms, and we’re giving Greece time to do that.” [..] European Commission President Jean-Claude Juncker urged Greece and its creditors in an emailed statement to reach a deal that respects commitments made on all sides. In response to Tsipras’s letter, Juncker called on the Greeks not to reverse reforms and creditors “to give Greece the desired and necessary room for maneuver to build its own future.”

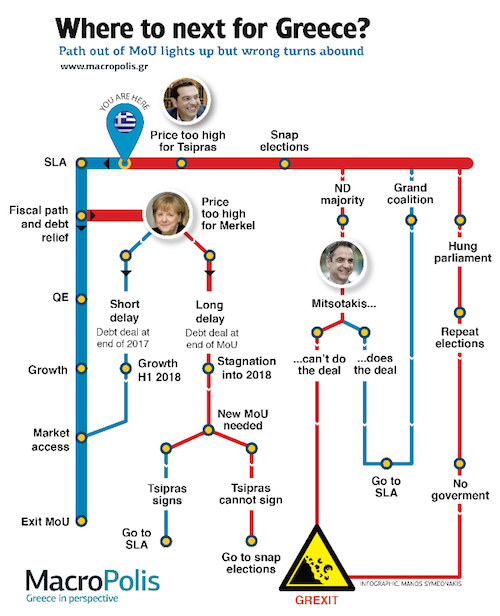

Reasonable overview, but any talk of agreements that could lead Greece back to growth is nonsense. The EU would never sign such an agreement. Theie attitude to date has made that abundantly clear.

• Where Next For Greece? (Makropolis)

In September last year, when Alexis Tsipras visited New York to speak at the UN Assembly, he held a meeting with some heavyweights of the international investment community. The Greek prime minister was reportedly advised by the participants that if he wanted to build trust in Greece as an attractive investment destination, he should shift focus from his main objective of debt relief towards ensuring Greece’s participation in the ECB’s QE programme. The investors apparently pointed out to the SYRIZA leader that such a development would have a wide range of benefits for Greece and provide the steadiest path towards regaining market access and the successful completion of the current programme, without the need to follow it up with a fourth memorandum of understanding (MoU).

Tsipras seemingly heeded the advice and, just as the second review was about to start, he charted a path out of the crisis. He set out his intention to close the review by December 2016, secure QE at the start of 2017 and dip his toe back into the markets with a small issue or two early this summer when Greece has to roll over the bond that it issued in 2014, when Antonis Samaras was prime minister. However, the timetable Tsipras identified last autumn has gone up in smoke.