David Hockney Nichols Canyon 1980

McAfee

The late John McAfee explains the real reason for the crackdown on TikTok.

— Ian Miles Cheong (@stillgray) March 24, 2023

Suramin

https://twitter.com/i/status/1639006754355683330

Remdesivir

https://twitter.com/i/status/1639319822667218944

Orthodox

Ukraine had given Orthodox priests a deadline by which to leave certain monasteries. The priests refused to leave and now they are breaking in and arresting the Orthodox Priests.

◾ Ukrainian religious persecution, the arrest of Orthodox priests continues including inside the… pic.twitter.com/b2EAogIn7Y

— GraphicW (@GraphicW5) March 24, 2023

Morons

Everyone needs to watch thispic.twitter.com/u7YtweRfYN

— Meatball Slayer (@MAGADevilDog) March 24, 2023

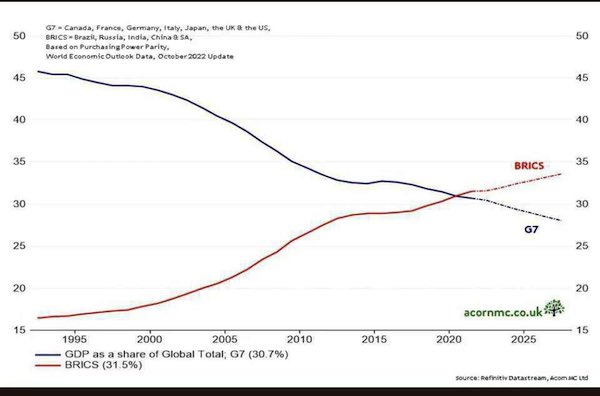

Brazil of course means BRICS. Next, bring in India. Their GDP(PPP) is already higher than G7. After that, all the countries who want to join BRICS. 60+% of world population, 60+% of GDP. Impossible to ignore.

• Brazil To Propose Ukraine ‘Peace Club’ With China (RT)

Brazilian President Luiz Inacio Lula da Silva will present his vision for an international “peace club” aimed at resolving the conflict in Ukraine when he meets with Chinese President Xi Jinping in Beijing this week, his foreign minister told the Financial Times on Friday. Lula, who has remained neutral on the conflict, believes non-aligned nations like Brazil have the best chance of brokering a peace deal. “We are very interested in promoting or helping generate some kind of meeting that would lead to a peace process,” Brazilian Foreign Minister Mauro Vieira told the newspaper. “The president has said so many times he hears a lot about war but very few words about peace. He is interested in peace conversations.”

Since defeating the right-wing Jair Bolsonaro in last October’s elections, Lula, as he is most commonly called, has largely stuck to his predecessor’s policy of neutrality on Ukraine. However, Lula has taken a more active role internationally than Bolsonaro, announcing in January that he intends to rally a G20-like group “to put an end to the Russia-Ukraine conflict.” “It is necessary to constitute a group with enough strength to be respected at a negotiating table, and sit down with both sides,” he said at the time. During his election campaign, Lula declared Ukrainian President Vladimir Zelensky “as responsible as [Russian President Vladimir] Putin for the war,” and condemned US and EU leaders for promising NATO membership to Ukraine.

Since taking office, the Brazilian leader has met with US President Joe Biden and German Chancellor Olaf Scholz, and has spoken by phone to Zelensky and Putin. Stressing the need to find “a way out to end this war” after meeting Biden last month, Lula’s calls for peace were echoed by China, which released its 12-point ‘Position on the Political Settlement of the Ukraine Crisis’ two weeks afterwards. The Chinese plan was welcomed by Putin, but rejected by the US. US Secretary of State Antony Blinken on Monday described Beijing’s proposal as a “tactical move” to stall the conflict in Russia’s favor, while in Ukraine, Zelensky said last month that he only agrees with a handful of points in the document.

Any plan put forward by Lula and his potential “peace club” may be received the same way, as was the case when Mexico proposed a peace plan of its own at the United Nations last year. Ukrainian government adviser Mikhail Podoliak dismissed the Mexican proposal as a “Russian plan,” and Kiev released its own ten-point peace plan two months later. However, Kiev’s plan included demands that Russia cede the territory of Crimea to Ukraine and send its officials to war crimes tribunals, and as such was dismissed as a non-starter by Moscow.

China did the Iran-Saudi deal. Russia is doing the same with Saudi-Syria. Get rid of the US, and peace becomes possible.

• The Iran-Saudi deal: A Bid To End Endless War (Shakil)

The China-mediated Saudi-Iran peace agreement, inked on 10 March in Beijing, marks a significant geopolitical shift with far-reaching implications for the Persian Gulf and Iran’s neighboring countries. For decades, Saudi Arabia and Iran have been engaged in ideological and economic competition on the territories of their neighbors, causing regional tensions to escalate. If the agreement is successful and relations between Riyadh and Tehran improve as envisioned, tensions will likely begin to significantly subside in the Persian Gulf, Levant, and further afield in neighboring Pakistan and Afghanistan. The former, long concerned about its security and energy supply vulnerabilities, will potentially benefit from improved relations between Saudi Arabia and Iran, which could help address its oil and gas crises.

Similarly, Afghanistan, whose Taliban-led government is still struggling to gain international recognition and is in dire need of reconstruction and investment initiatives, may also benefit from the kingdom’s rapprochement with the Islamic Republic. An early litmus test for the Saudi-Iranian reconciliation will be its impact on Lebanon, Iraq, Syria, and Yemen, where a perceived proxy war has wreaked havoc on their respective economies and in their public spheres. One of the most critical areas where the impact of the peace agreement will be tested is Yemen, where Iran and Saudi Arabia have backed opposing sides in the country’s eight-year war. The conflict has resulted in one of the world’s worst humanitarian crises after a Saudi-UAE-led coalition in 2015 launched military attacks against Yemen’s pro-Iran Ansarallah movement, which had seized control of the capital, Sanaa.

Iran’s permanent mission to the UN said in a statement that the Iran-Saudi deal will “accelerate the ceasefire, help start a national dialogue, and form an inclusive national government in Yemen.”

“Xi’s visit to Putin and remaining there for a couple of days I think sends a very troubling message, a message of support..”

• China’s Xi Has Sent ‘Very Troubling Message’ – Pentagon (RT)

Chinese President Xi Jinping’s recent state visit to Russia should be regarded as a matter of grave concern for Washington, US Secretary of Defense Lloyd Austin told lawmakers on Thursday. Speaking at the House of Representatives’ subcommittee on defense appropriations, Austin was asked to comment on Xi’s trip to Moscow, and its ramifications for Sino-US competition. “Xi’s visit to [Russian President Vladimir] Putin and remaining there for a couple of days I think sends a very troubling message, a message of support,” the Pentagon chief replied. He stated that while the Pentagon has not seen signs that China had been providing Russia with military equipment for use against Ukraine, it is watching the situation “very closely,” cautioning that “if they were to go down that path, I think that would be very troubling for the international community.”

He went on to warn that if Xi decided to arm Moscow, “it would prolong the conflict and certainly broaden the conflict potentially – not only in the region, but globally.” On Monday, the Chinese leader embarked on a three-day state visit to Moscow, holding talks with Russian President Vladimir Putin. During the summit, the two sides signed more than a dozen documents on increased defense, industrial and economic cooperation.Moscow and Beijing also pledged to “deepen relations of comprehensive partnership and strategic interaction entering a new era.”

The US has claimed that China has been considering sending arms to Russia, while threatening “consequences” should it make such a move. Beijing, however, has dismissed such plans, accusing Washington of “spreading false information” and “fanning the flames” of the Ukraine conflict. “It is the United States and not China that is endlessly shipping weapons to the battlefield,” Chinese Foreign Ministry spokesman Wang Wenbin said last month. Since the start of the Ukraine conflict more than a year ago, Western countries have supplied Kiev with large amounts of military equipment, with the US alone having committed more than $32.5 billion in security assistance. Moscow has repeatedly warned the West that such support will only prolong the conflict while making it a direct participant in the hostilities.

“..I would not speculate on whether one army is stronger than the other. A fighting army is a strong army..”

• There Could Be No Winner In War Between Russia, US – Medvedev (TASS)

Russian Security Council Deputy Chairman Dmitry Medvedev warned of the disastrous consequences of a potential confrontation between the armies of Russia and the United States. In an interview with Russian media outlets and users of leading Russian social media network VKontakte, Medvedev said, “The first thing is, only a real conflict can decide which army is first, second or 21st. Secondly, it would be wrong to say that the US army is No. 1, while ours is No.2 for one simple reason. If these armies start a war, how could we say who the winner is? Obviously, there will be no winner.”

A potential confrontation “would cause disastrous consequences,” the politician warned. “And it would be impossible to say whose army is superior,” he added. According to Medvedev, the US army could have been considered the best “at least during that period when it was active on the ground – as usual, not on its own soil, at that,” referring to the US occupation of Vietnam. He said he was shocked to learn that 3 million Vietnamese people had been killed in that conflict. “Therefore, I would not speculate on whether one army is stronger than the other. A fighting army is a strong army,” Medvedev concluded.

Conte

Former Prime Minister of Italy, leader of the Five Star movement Giuseppe Conte https://t.co/AtQgDl1flp pic.twitter.com/iRESz6mokC

— Victor vicktop55 (@vicktop55) March 24, 2023

“..reducing any export of agricultural produce from Ukrainian territory for many decades, if not centuries to come..”

• Russia Warns Of Radioactive Disaster In Ukraine (RT)

The potential use of Western-supplied depleted uranium shells by Ukraine would have a devastating impact on the country’s economy and population, lasting for centuries to come, the Russian Defense Ministry warned on Friday. Speaking at a briefing, Lieutenant General Igor Kirillov, who is in charge of Russia’s Nuclear, Biological and Chemical Defense Forces, issued a scathing criticism of the UK’s plans to support Kiev with armor-piercing rounds containing depleted uranium. He noted that such munitions have only ever been deployed in combat by NATO countries, most notably during the Iraq War, when the US used at least 300 tons of depleted uranium.

“As a result, the radiation situation in the [Iraqi] city of Fallujah was much worse than in the cities of Hiroshima and Nagasaki after the nuclear bombings by the United States,” Kirillov stated, recalling that Fallujah had been dubbed “the second Chernobyl,” while the local population suffered from a skyrocketing number of cancer cases. The West is well aware of the consequences of using such weapons, the general stressed. Even though it “will cause irreparable harm” to the health of Ukrainian troops and civilians, “NATO countries, in particular the UK, express a readiness to supply this type of weapon to the Kiev regime,” Kirillov stated.

He warned that the use of the munitions will contaminate farmland. “In addition to infecting its own population, this will cause tremendous economic damage to the agro-industrial complex of Ukraine… reducing any export of agricultural produce from Ukrainian territory for many decades, if not centuries to come,” the general said. The UK’s plans to send depleted uranium shells to Ukraine for use with Challenger 2 battle tanks were first unveiled on Monday, prompting an outcry from the Russian Foreign Ministry, which called the move a sign of “absolute recklessness, irresponsibility and impunity” on the part of London and Washington. While the US has said it does not plan to support Ukraine with such ammunition, it shrugged off Russian concerns over the matter, describing depleted uranium shells as “a commonplace type of munition” which has “been in use for decades.”

“..the DSA includes a ‘crisis-management mechanism’, added last year in a last-minute amendment. The Commission argued it needs to be able to direct how platforms respond to events like the Russian invasion of Ukraine..”

• EU Censorship Regime Is About To Go Global (Spiked)

Not many people know that 16 November 2022 was the day that freedom of speech died on the internet. This was the day the European Union’s Digital Services Act (DSA) came into law. Under the DSA, very large online platforms (VLOPs) with more than 45million monthly active users – like Twitter, Facebook and Instagram – will have to swiftly remove illegal content, hate speech and so-called disinformation from their platforms. Or they will face fines of up to six per cent of their annual global revenue. Larger platforms must be DSA compliant by this summer, while smaller platforms will be obliged to tackle this content from 2024 onwards. The ramifications of this are immense. Not only will the DSA now enforce the regulation of content on the internet for the first time, but it is also set to become a global standard, not just a European one.

In recent years, the EU has largely realised its ambition to become a global regulatory superpower. The EU can dictate how any company worldwide must behave if it wants to operate in Europe, the world’s second-largest market. As a result, its strict regulatory standards often end up being adopted worldwide by both firms and other regulators, in what is known as the ‘Brussels effect’. Take the General Data Protection Regulation (GDPR), a privacy law which came into force in May 2018. Among many other things, it requires individuals to give explicit consent before their data can be processed. These EU regulations have since become the global standard, and the same could now happen for the DSA.

The EU’s enforcement of GDPR has been somewhat tentative. It has issued only about €1.7 billion in penalties since 2018, according to The Economist, which is peanuts in an industry that generates more than a trillion euros in revenue annually. But the EU seems to have learnt from this: the DSA has enormous enforcement capabilities built into it. The European Commission expects its internal industry watchdog to have over 100 full-time staff by 2024. Plus, contract workers and national experts will be expected to supervise Big Tech’s operations, too. It amounts to what EU internal-markets commissioner Thierry Breton calls a ‘historic moment in digital regulation’. The VLOPS are expected to fund this enforcement operation themselves, paying up to 0.05 per cent of their global annual turnover each year to the Commission.

This gives the EU an extraordinary amount of power. The regulation of the DSA will be overseen by the Commission itself, not an independent regulator. What’s more, the DSA includes a ‘crisis-management mechanism’, added last year in a last-minute amendment. The Commission argued it needs to be able to direct how platforms respond to events like the Russian invasion of Ukraine. Apparently, in a crisis, the ‘anticipatory or voluntary nature’ of obligations on tech companies to tackle disinformation would be insufficient. Under the DSA, the Commission has given itself the power to determine whether such a ‘crisis’ exists, defined as ‘an objective risk of serious prejudice to public security or public health in the Union’.

“..simple issues of legal procedure, of due process, are no longer allowed to stand in the way when a demand to do something of this nature appears.”

• Biden and the ICC: ‘A New Level of Farce’ (Patrick Lawrence)

There was talk among the Western powers for most of last year, readers may recall, of the U.N. forming a special court to try Putin and other Russian officials on charges of war crimes allegedly committed in the course of the Ukraine conflict. But Washington and its allies overestimated international sentiment: They could get no appreciable support among member states for any such project. They similarly failed when, as an alternative, they tried to get the U.N. General Assembly to authorize the ICC, a U.N. body, to investigate the numerous allegations of war crimes leveled since the start of hostilities in February 2022. It was at this point that the West—reportedly led by Britain—began an intense lobbying campaign at The Hague to get the ICC to act even without a U.N. referral behind it. The arrest warrant announced last Friday appears to be the result of this pressure.

The legalities here are important. While Russia is not a signatory to the ICC’s founding treaty, a U.N. referral such as the U.S. and its allies sought would extend the court’s jurisdiction even to nations that do not recognize it. This is why the Western powers spent all those months trying to bring the General Assembly around. Is our conclusion other than obvious? The ICC’s action last week has no sound legal basis, and the court has no jurisdiction over a nation that does not recognize it. “But as we have seen on so many occasions, over so many matters in the past few years,” Alexander Mercouris observed in an informed webcast over the weekend, “simple issues of legal procedure, of due process, are no longer allowed to stand in the way when a demand to do something of this nature appears.”

The charges of criminal abduction and forced deportation of children appear to be equally flimsy. The Russian Federation has made no secret of its effort to remove thousands of children from harm’s way over the past year. Some of these children were parentless and living in orphanages, by the Russian account; when parental consent was involved, the Russians running the program say they had it. These children, not to be missed, were removed from areas under constant artillery bombardment from Ukrainian forces in the eight years following the U.S.–cultivated coup in 2014.

I think this is the Hersh piece that was behind a paywall.

• Biden’s Nord Stream Cover-up Enters New Slippery Phase (Seymour Hersh)

It’s been six weeks since I published a report, based on anonymous sourcing, naming President Joe Biden as the official who ordered the mysterious destruction last September of Nord Stream 2, a new US$11 billion pipeline that was scheduled to double the volume of natural gas delivered from Russia to Germany. The story gained traction in Germany and Western Europe, but was subject to a near media blackout in the US. Two weeks ago, after a visit by German Chancellor Olaf Scholz to Washington, US and German intelligence agencies attempted to add to the blackout by feeding the New York Times and the German weekly Die Zeit false cover stories to counter the report that Biden and US operatives were responsible for the pipelines’ destruction.

Press aides for the White House and Central Intelligence Agency (CIA) have consistently denied that America was responsible for exploding the pipelines, and those pro forma denials were more than enough for the White House press corps. There is no evidence that any reporter assigned there has yet to ask the White House press secretary whether Biden had done what any serious leader would do: formally “task” the American intelligence community to conduct a deep investigation, with all of its assets, and find out just who had done the deed in the Baltic Sea. [..] In early March, President Biden hosted German Chancellor Olaf Scholz in Washington. The trip included only two public events—a brief pro forma exchange of compliments between Biden and Scholz before the White House press corps, with no questions allowed; and a CNN interview with Scholz by Fareed Zakaria, who did not touch on the pipeline allegations.

The chancellor had flown to Washington with no members of the German press on board, no formal dinner scheduled, and the two world leaders were not slated to conduct a press conference, as routinely happens at such high-profile meetings. Instead, it was later reported that Biden and Scholz had an 80-minute meeting, with no aides present for much of the time. There have been no statements or written understandings made public since then by either government. But I was told by someone with access to diplomatic intelligence that there was a discussion of the pipeline exposé and, as a result, certain elements in the Central Intelligence Agency were asked to prepare a cover story in collaboration with German intelligence that would provide the American and German press with an alternative version of the destruction of Nord Stream 2. In the words of the intelligence community, the agency was to “pulse the system” in an effort to discount the claim that Biden had ordered the pipelines’ destruction.

Pepe Escobar tweets it was not Scholz, but Robert Habeck. He’s the vice-chancellor, from the Green Party(!).

Pepe Escobar: “Sy Hersh’s sources told him that it was during a one-hour Biden-Scholz meeting that the CIA plan was concocted – to plant the Ukrainian group story as a misdirection to cover up the US blowing up the Nord Streams. It was HABECK, not Scholz who discussed this on site with Biden.”

“A Biden-HABECK meeting green lit the whole Nord Stream scam + misdirection. Scholz knew what HABECK was doing. These revelations WILL explode. And they will bring down both Biden and liver sausage Scholz. This may well end up as Sy Hersh’s greatest scoop.”

• Seymour Hersh Makes Claim Over Reasons For Nord Stream Sabotage (RT)

US President Joe Biden ordered the sabotage of the Nord Stream pipelines because he was unhappy with the level of support provided by German Chancellor Olaf Scholz to Ukraine in its conflict with Russia, veteran investigative journalist Seymour Hersh has claimed. Hersh first accused Washington of destroying the key European energy route in an article released in February, and made more allegations in an interview with the China Daily newspaper published on Friday. “The [US] president was afraid of Chancellor Scholz not wanting to put more guns and more arms [forward for Kiev]. That’s all. I don’t know whether that it was anger or punishment, but the net effect is that it cut off a major power source through Western Europe,” Hersh claimed.

Despite attempts by the US to deny its involvement in the Nord Stream attack, “Europe is in crisis now” and Biden will receive “a lot of criticism for what he did” in the coming months, the journalist argued. The Pulitzer Prize winner alleged that “the people that were initially asked to do the job” of destroying the pipelines were contacted by US National Security Advisor Jake Sullivan towards the end of 2021. The initial purpose of mining Nord Stream 1 and 2, built to deliver Russian gas to Europe through Germany, was “to give the [US] president an option to say to [Russian] President Putin, ‘If you go to war [in Ukraine], we’re going to destroy the pipelines,’” Hersh claimed. Biden himself publicly confirmed that stance but “unfortunately, those people in the Western press seemed to have forgotten,” the journalist stated.

Just under three weeks before the launch of Moscow’s military operation in Ukraine, Biden warned during a press conference on February 7 that “if Russia invades… there will no longer be a Nord Stream 2. We will bring an end to it.” According to Hersh, the US leader decided to order the detonation of mines at the bottom of the Baltic Sea last September because the conflict “wasn’t going great in Ukraine” from a US perspective. There was “at best a stalemate” during that period, in what Hersh described as “the American war that President Biden was so eager to support.”

”Their “leaders” are all on the same team, the one that keeps the masses warring with each other rather than turning their pitchforks and torches against the ruling class..”

• US Rulers Keep The Masses Divided And Distracted From Demanding Justice (Cox)

Washington is where securing political power means never having to say you’re sorry – regardless of how many thousands or millions of people you might have gotten killed. Tribalism is what keeps the perpetrators from ever being held accountable. Consider, for example, this month’s Axios/Ipsos poll showing that more than six in ten US adults believe that George W. Bush’s 2003 invasion of Iraq was a mistake. While it might seem encouraging that most Americans have come to realize that the Iraq debacle was a bad move – sort of like recognizing that the sun comes up in the East – a glance beneath the headline number reveals that voters haven’t really learned anything. You see, two decades on from a war that was started on false pretenses and was illegal under the UN Charter, 58% of Republicans still believe that the Bush administration was right to launch the invasion (compared to 26% of Democrats).

They still feel this way despite a bevy of troubling truths that should be clear to everyone by now, including the fact that the whole basis for the invasion – the hype that Saddam Hussein had obtained weapons of mass destruction – was a sham. It was a sham that cost US taxpayers over $2 trillion, helped give rise to ISIS and killed or maimed tens of thousands of American troops. Along the way, this bogus war also killed hundreds of thousands of Iraqis and left the country shattered, even to the present day. The cherry on top is that it also strengthened Washington’s arch-enemy, Iran. It’s almost incomprehensible that any Americans, other than the war criminals themselves, would still defend such a fiasco – unless one factors in the level of tribalism that currently pervades the US political system.

Rank-and-file members of the red team and the blue team can see no evil nor hear no evil when it comes to their tribe. Their “leaders” are all on the same team, the one that keeps the masses warring with each other rather than turning their pitchforks and torches against the ruling class. No one was punished for the Afghan debacle. Biden, Blinken and the Pentagon brass still refuse to admit to any mistakes. The only person fired over the withdrawal was Stuart Scheller, the Marine Corps lieutenant colonel who dared to publicly criticize the evacuation and call for senior officials to be held accountable. He was court-martialed for his temerity.

Meanwhile, the so-called experts in Washington continue advancing their careers, regardless of how many lives they destroy. It’s a town where Victoria Nuland can play a key advisory role in the Bush administration’s Iraq debacle, help engineer the Obama-Biden administration’s overthrow of Ukraine’s elected government in 2014 – setting the table for the current crisis in Eastern Europe – then land a job as the Biden administration’s undersecretary of state. It’s also where former secretary of state Madeleine Albright can say in a television interview that the deaths of 500,000 Iraqi children resulting from US sanctions were “worth it” – then be eulogized by three presidents upon her death last year and praised by Biden for her “humanity.”

“..everybody… the formerly Woke, the unvaxxed, the penitent and unrepentant, the middle and lower orders especially, who suffer most harshly… will find themselves all on one side of that line in opposition to the wicked who have brought a hard rain upon them..”

• The Season is Here (Kunstler)

Expect three evolving dynamics to stipulate our country’s zeitgeist in the stirring months to come. First, the collapse of our project for using Ukraine to destabilize Russia, an enterprise so feckless it could have only been conceived by the dead-of-brain. Our geniuses of foreign affairs screwed the pooch on this one. It’s almost too obvious that they never cared about the people of that sore-beset land. Notice, they do not even use the word “peace” in any of their confabulations about what’s going on there, because it is the opposite of what they seek, which is…chaos unending. Thus, others will end the project for us — namely, our antagonist there, Russia — and the regime of “Joe Biden,” for the second time in its mortifying two years-plus of rule, will be left holding its limp, generative member in its collective hand, another humiliation for our over-reaching imperial soldiery — and the deluded empty suits commanding it.

Will they be able to pretend this time, as they did in Afghanistan, 2021, that there’s nothing to see here, folks? Just a blizzard of press-releases declaring “mission accomplished” or some-such other craven bullshit? I don’t think so. The reaction may be enough to bum-rush “Joe Biden” and Company out of office. His grotesque family rackets (including the Ukraine grifts) will finally and magically come to the public’s attention, and that’ll be all she wrote for “JB”— except for the historians waking from their own long catatonic spells to record the disaster they will swear they couldn’t see coming. Next, we will go through the tipping-point where a critical mass of the population — not just in America, but throughout Western Civ, and even beyond — realizes that they have been poisoned and injured by the mRNA “vaccines” they were so eager to line up for.

It will produce a special sort of collective agony centered around a raging despair that leads with astonishing speed to prosecutions. The torpor and uncertainty of the past three years evaporates and the machinery of law actually starts cranking again, and in the right way — not as a mere instrument of coercion and intimidation, but to actually seek justice. Third will be the transformation of a raging inflation into a ruinous debt deflation that leaves Americans, one way or another, with no money. At the same time, the people will wake to the wrecking of their energy and food supply. A line will appear drawn in the ground from sea to shining sea, as by a cosmic power, and everybody… the formerly Woke, the unvaxxed, the penitent and unrepentant, the middle and lower orders especially, who suffer most harshly… will find themselves all on one side of that line in opposition to the wicked who have brought a hard rain upon them. And there you will finally see the beginning of your long-promised hope and change. No need even to wait for it. At long last, it’s upon us.

“As interest rates continue rising, to fight inflation, razor-sharp needles are popping up in every direction.”

• EU Is Melting Down And Contagion Spreading To UK Economy (Mitch Feierstein)

In 2008, the Bank of England’s Mervyn King began quantitative easing (QE) and bank bailouts. Increased debt levels devalued British pound sterling by 34 percent vs. the US Dollar. Sterling has not recovered since. In 2013, George Osborne hired central bank “rock star” Mark Carney to replace King. Carney maintained misguided ‘easy money’ interest rate policies through 2020. Zero Interest Rate Policy set the table for more dire future economic downturns far worse than the Great Financial Crisis. Carney inflated asset bubbles across UK markets, the most prominent bubble was in the UK’s commercial and residential property markets. As interest rates continue rising, to fight inflation, razor-sharp needles are popping up in every direction. When variable rate mortgages reset, a credit event will impair banks’ asset quality and impact our financial system.

King’s QE devaluation, Carney’s asset bubbles, and Boris and Rishi’s COVID money printing have caused the most significant cost of living crisis in UK history. Last week, the USA’s Silicon Valley Bank failed because it did not manage its risks. SVB made lending, business, and employment decisions that prioritised social justice, DEI (Diversity, Equity, and Inclusion), and ESG (Environmental, Social, and Corporate Governance), ahead of profitability! So, what happened? SVB – Got woke & went broke. EU and USA Bank failures bode poorly for the UK. UK taxpayers still own NatWest bank shares from Kings 2008 bank bailouts. Biden, Yellen, and UK regulators promised that SVB depositor bailouts: “Will not cost taxpayers anything.” The US Fed created a $2.5 TRILLION bailout fund calling it a Bank Term Funding Program or “BTFP.”

BTFP is highly inflationary QE and the program signals a de facto nationalisation of the banking system. Was SVB a “one off”? Not at all, in fact, later that week, Credit Suisse went bust. Despite the “The banking system is sound, it’s all fine”, mantra from those responsible for this mess, continued currency declines, bank failures, bankruptcies and defaults are likely. What dishonest diversions will the media unwittingly spread? The blame shifting for the coming credit crisis will include: COVID, Russia, Putin, the Climate Emergency! Arrest Trump! Bring Back Boris from his £4m speaking tour, implement CBDCs.

“Bank credit quality today is the best in a generation. The crisis stems from the now-impossible task of financing America’s ever-expanding foreign debt.”

• US Bank Trouble Heralds End Of Dollar Reserve System (David Goldman)

The US banking system is broken. That doesn’t portend more high-profile failures like Credit Suisse. The central banks will keep moribund institutions on life support. But the era of dollar-based reserves and floating exchange rates that began on August 15, 1971, when the US severed the link between the dollar and gold, is coming to an end. The pain will be transferred from the banks to the real economy, which will starve for credit. And the geopolitical consequences will be enormous. The seize-up of dollar credit will accelerate the shift to a multipolar reserve system, with advantage to China’s RMB as a competitor to the dollar.

Gold, the “barbarous relic” abhorred by John Maynard Keynes, will play a bigger role because the dollar banking system is dysfunctional, and no other currency—surely not the tightly-controlled RMB—can replace it. Now at an all-time record price of US$2,000 an ounce, gold is likely to rise further. The greatest danger to dollar hegemony and the strategic power that it imparts to Washington is not China’s ambition to expand the international role of the RMB. The danger comes from the exhaustion of the financial mechanism that made it possible for the US to run up a negative $18 trillion net foreign asset position during the past 30 years.

Germany’s flagship institution, Deutsche Bank, hit an all-time low of 8 euros on the morning of March 24, before recovering to 8.69 euros at the end of that day’s trading, and its credit default swap premium—the cost of insurance on its subordinated debt—spiked to about 380 basis points above LIBOR, or 3.8%. That’s as much as during the 2008 banking crisis and the 2015 European financial crisis, although not quite as much as during the March 2020 Covid lockdown, when the premium exceeded 5%. Deutsche Bank won’t fail, but it may need official support. It may have received such support already. This crisis is utterly unlike 2008, when banks levered up trillions of dollars of dodgy assets based on “liar’s loans” to homeowners. Fifteen years ago, the credit quality of the banking system was rotten and leverage was out of control. Bank credit quality today is the best in a generation. The crisis stems from the now-impossible task of financing America’s ever-expanding foreign debt.

“On one hand they’re kind of stuck with her; it would be bad to get rid of a Treasury Secretary during a banking crisis..” “On the other hand, they know they don’t have anyone good to be their face in terms of a response.”

• White House Worried Over Janet Yellen’s Fumbling Of US Bank Crisis (Gasparino)

Janet Yellen is once again on thin ice inside the Biden Administration over her bungling of the banking crisis that keeps roiling markets, The Post has learned. The question is when will Sleepy Joe & Co. finally act? They need to put Yellen out of her misery and end ours by handing her job to someone who knows how to deal with the very real possibility of banks failing on a scale not seen since the 2008 financial crisis and a possible deep recession. As we have reported, the political types in the White House — the people that craft messaging and give input on cabinet choices — have been increasingly wary of Yellen’s ability to do the job despite her expansive resume and years running the Fed, people with direct knowledge tell the Post.

They grew sour over her bungled response to inflation (recall how she said it was transitory as it was exploding). It’s why they floated possible replacements last year, including Commerce Secretary Gina Raimondo, and Brian Moynihan, the CEO of Bank of America. Both are seen as policy heavyweights. Unlike Yellen, they have real-world business experience (Yellen’s been in academia and government throughout her career). Yet she survived that attempt to get her removed because her ultimate boss, the president, didn’t want to fire a woman in such a high-profile post, these people say. Sleepy Joe might not have much choice now given the growing severity of what she and the country are facing: The collapse of large regional banks Silicon Valley and Signature banks. First Republic, with more than $200 billion in assets, is on the precipice.

Credit Suisse nearly imploded and was forced to merge with its Swiss neighbor, UBS. On Friday, investors began freaking out about another European banking giant, Deutsche Bank and began predicting its failure. Yellen’s response to this has been bewildering from a messaging standpoint. White House advisers are pointing to her multiple flip-flops on whether the government will back up all deposits in a failed bank — even those well past the FDIC insurance threshold of $250,000. I get it, she doesn’t want people to pull money out of regional banks at just the hint of weakness, but what she is saying lacks credulity. Will the federal government or the underfunded FDIC insurance fund really cover a deposit of more than a million dollars?

Another criticism: Her slow-walking the possible severity of weakness in the plumbing of banks as failures begin to pile up. She says the system is safe and secure, but it’s obviously not. Years of historical and super-low interest rates distort asset values and risk-taking, and banks can’t be immune from the consequences. “On one hand they’re kind of stuck with her; it would be bad to get rid of a Treasury Secretary during a banking crisis,” said one of my sources, who works at a large DC-based think-tank and has heard the griping firsthand. “On the other hand, they know they don’t have anyone good to be their face in terms of a response.” [..] ..check your calendar: We’re going on week three of a fast-moving banking contagion that could spark a significant recession if banks collapse en masse and lending dries up, so whatever she’s doing is still far too late.

“..nitrogen fertilizer [derived from fossil fuels] now supports approximately half of the global population.”

• Carbon War ‘Net Zero’ Would Starve Half the Planet (Celente)

That victory Dutch farmers just won in provincial elections might literally save the world. After massive demonstrations against government targeting of nitrogen fertilizers to fulfill a UN zero carbon agenda, the BBB (BoerBurgerBeweging or “Farmer-Citizen Movement”) party picked up a significant bloc of senate seats. It was a major rejection of Prime Minister Mark Rutte’s environmental policies, as Reuters reported in “Dutch farmers’ protest party scores big election win, shaking up Senate.” According to a final tally reported by Eva Vlaardingerbroek on 19 March, the number of seats gained was 17, more than enough to turn back environmental directives that would destroy the Dutch farming sector. But the significance is far greater than just farmer livelihoods in the Netherlands.

Nitrogen fertilizers are crucial to sustaining the world’s food supply, and banning their use as part of “net-zero” carbon goals could literally starve half the world. That’s the warning of a new report called “Challenging ‘Net Zero’ with Science,” compiled by two longtime pre-eminent climates scientists, William Happer, Professor of Physics, Emeritus, of Princeton University, and Richard Lindzen, Alfred P. Sloan Professor of Atmospheric Science, Emeritus, of MIT. The report was released by co2coalition.org. It says that extreme goals of the so-called “green energy” movement are built on decidedly unscientific premises. And they make no bones about the disastrous consequences that would result from following a course that continues to try to phase out the use of nitrogen fertilizers:

“As to the disastrous consequences of eliminating fossil fuels, it ‘is estimated that nitrogen fertilizer [derived from fossil fuels] now supports approximately half of the global population.’ As one of us (Happer) has made clear, without the ‘use of inorganic fertilizers’ derived from fossil fuels, the world ‘will not achieve the food supply needed to support 8.5 to 10 billion people.’ The authors cited Sri Lanka as a cautionary example of how devastating this one facet of the “zero carbon” agenda is already playing out: “The recent experience in Sri Lanka provides a red alert. ‘The world has just witnessed the collapse of the once bountiful agricultural sector of Sri Lanka as a result of government restrictions on mineral fertilizer.’5 The government of Sri Lanka banned the use of fossil fuel derived nitrogen fertilizers and pesticides, with disastrous consequences on food supply there. If similarly misguided decisions are made eliminating fossil fuels and thus nitrogen fertilizer, there will be a starvation crisis worldwide.”

Catfight

https://twitter.com/i/status/1639175659418435584

Pandas

https://twitter.com/i/status/1639163711280562176

Octopi

Nature: Octopi can run!

— Ben Proj (@ben_proj) March 24, 2023

https://twitter.com/i/status/1639400762068582401

Support the Automatic Earth in virustime with Paypal, Bitcoin and Patreon.