Paul Gauguin Tahitian village 1892

“It is spring again.

The earth is like

a child that knows

poems by heart.”

~ Rainer Maria Rilke

This from Forbes is actually part of the sales job. It’s “only” 3 people. And:

“just because you catch the virus after getting fully vaccinated doesn’t mean that the vaccine didn’t help you. You don’t know how much worse the infection could have been without the vaccine”

• 3 Fully Vaccinated People Catch Covid-19 Coronavirus in Hawaii (F.)

While the Covid-19 vaccines may protect you against Covid-19, their protection is not perfect. Even after getting vaccinated , you can still catch the virus. You can still get Covid-19. Case in point. Or rather three cases in point. According to the Hawaii Department of Health (DOH), three people in Hawaii who had received both doses of either the Moderna or the Pfizer/BioNTech vaccine subsequently tested positive for the Covid-19 coronavirus. Additionally, a fourth person who had received the first of two doses of the vaccine ended up catching the B.1.1.7 variant of the severe acute respiratory respiratory syndrome coronavirus 2 (SARS-CoV2). That be a more contagious version of the SARS-CoV2.

Don’t press the panic button just because you saw this news though. In general, pressing a button labeled “Panic” is a bad idea. Plus, three people catching the Covid-19 coronavirus does not mean that the Covid-19 vaccines do not work. Getting the vaccine does not mean that a giant six-feet thick concrete condom forms around your body. The vaccine does not serve as a solid 100% effective barrier to the virus. Even though the vaccines may be quite effective at preventing more severe Covid-19, you still have a chance of getting Covid-19 after being fully vaccinated. And there is still a chance that this Covid-19 can be severe. It’s just that your chances after vaccination may be significantly lower.

Ultimately, three people is not that many people. It’s not even enough to form a four-person bobsled team or a typical boy band or a combination of the two. And it’s only a tiny fraction of the people who have been fully vaccinated to date. According to the Centers for Disease Control and Prevention (CDC) Covid-19 Vaccine Tracker, over 35 million people have gotten both doses of the Pfizer/BioNTech or Moderna Covid-19 vaccines. [..] just because you catch the virus after getting fully vaccinated doesn’t mean that the vaccine didn’t help you. You don’t know how much worse the infection could have been without the vaccine, unless you’ve somehow mastered time travel.

Sales job continued:

“A rebound in travel and day-to-day life most likely won’t be complete until after a vaccine for children becomes available..”

• Travel Changes For Those Who Are Fully Vaccinated (F.)

The coronavirus vaccine is becoming available to more people across the United States and the world. Given the uptick in travel, it seems that more people are becoming confident to travel once they become fully vaccinated. Here are some travel changes to know about for those who have been (or will soon be) vaccinated. What Does “Fully Vaccinated” Mean? Your body must develop antibodies after receiving the recommended coronavirus vaccine dosage before you are “fully vaccinated.” The waiting period is 14 days after receiving your final dose. The 14-day period starts after receiving your second dose if you receive the Moderna or Pfizer vaccine. The Johnson & Johnson (Janssen) vaccine only requires one dose.

If you want to travel after getting the vaccine, your travel dates should start 14 days after receiving the second dose. As always, you should stay home if you’re showing potential signs and symptoms. People can still contract the coronavirus after being fully vaccinated. Vaccines For Children Are Coming A rebound in travel and day-to-day life most likely won’t be complete until after a vaccine for children becomes available. Moderna is currently testing a children’s vaccine for recipients between ages 6 months and 12 years. For now, fully vaccinated adults have fewer social distancing restrictions. Current social distancing guidelines remain in place for unvaccinated households and travelers.

Being fully vaccinated isn’t a free pass to unrestricted travel as it was before the pandemic. The CDC interim guidelines do not expressly state that those who are fully vaccinated should avoid non-essential travel. However, the vaccinated must limit their exposure to the unvaccinated, who can be at more risk of getting the virus in close contact. The fully vaccinated can visit these people without masks or social distancing: • Other fully vaccinated persons (in small groups only) • Visit with unvaccinated people from a single household if they are “low-risk”.

“EMA did not rule out a possible link, however..”

• European Trust In AstraZeneca COVID-19 Vaccine Plunges (R.)

Confidence in the safety of AstraZeneca’s COVID-19 vaccine has taken a big hit in Spain, Germany, France and Italy as reports of rare blood clots have been linked to it and many countries briefly stopped using it, poll data showed on Monday. The polling firm YouGov said it had already found in late February that Europeans were more hesitant about the AstraZeneca vaccine than about those from Pfizer Inc/BioNTech and Moderna Inc, and that the clot concerns had further damaged public perceptions of the AstraZeneca shot’s safety. At least 13 European countries in the past two weeks stopped administering the AstraZeneca shot, co-developed with scientists at Oxford University, after reports of a small number of blood disorders.

Many resumed its use on Friday after the European Medicines Agency regulator said in a preliminary safety review on Thursday that the vaccine was safe and effective and not linked with a rise in the overall risk of blood clots. EMA did not rule out a possible link, however, with rare cases of blood clots in the brain known as cerebral venous sinus thrombosis (CVST). YouGov’s poll – which covered about 8,000 people in seven European countries between March 12 and 18 – found that in France, Germany, Spain and Italy, people were now more likely to see the AstraZeneca vaccine as unsafe than as safe. Some 55% of Germans say it is unsafe, while less than a third think it is safe, the poll showed. In France, where AstraZeneca’s COVID vaccine was already unpopular, 61% of people polled say they now see it as unsafe.

In Italy and Spain, most people previously felt the AstraZeneca vaccine was safe – at 54% and 59% respectively – but those rates have fallen to 36% and 38% respectively, in the latest poll. The survey showed that only in Britain, where the AstraZeneca COVID-19 vaccine has been used in a national rollout since January, have the blood clot concerns had little to no impact on public confidence. The majority of people polled in the UK – 77% – still say the shot is safe. Their trust in it is on a par with Pfizer’s 79% perceived safety rating.

A lot of material here. Good for the Philippines.

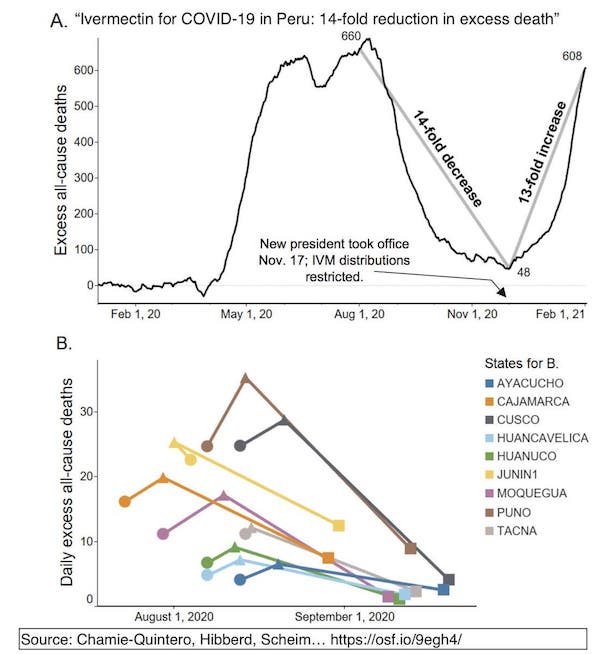

• Ivermectin: Game changer vs Covid-19? What’s the Controversy? (Manila Times)

Desperation time is arriving at our door. Our infection rates are reaching all-time highs, hospitals are full, people are unnerved already and the Philippines is far behind other countries in the recovery. Most of us will survive, but many will die unnecessarily; millions of jobs are lost.Real tests are needed, not speeches. Let’s not kid ourselves that survival is proof of resilience and innovativeness; we must improve all performance indicators, including time to adopt the best practical practices. Can we improve this reality test of our nation’s ability to anticipate, select talent, plan and execute by turning around the Covid health and economic situation quicker? When do we kick out demagogues and incompetents?

One potentially very powerful decision that is simple to execute can bypass the costs, vaccine availability and logistics issues we have (but not the pharma politics and traditional medical bureaucracy?) is the properly managed use of ivermectin.Game changer? Worldwide cases on ivermectin have been accumulating since the middle of 2020. Many highly competent doctors and research institutions are asserting that it can massively decrease infection rates, periods, and severity, at low risk, even prior to the arrival and use of vaccines. What are the arguments for or against ivermectin use for Covid control and treatment? The National Institute of Health (NIH) of the US in January 2021 had upgraded their recommendation on ivermectin, from “against” to “neither for nor against,” making it an option for use against Covid-19.

With the All-Indian Institute of Medical Sciences of Bhubaneswar, India’s Dr. Batmanabane says of his experience: “Earlier, at least 20 to 25 health care workers were getting infected with the virus daily. After the workers started taking Ivermectin, the number of infections has come down to one or two per day.” Their study indicates an over 70 percent overall improvement. While ivermectin is associated at times with some nausea or dizziness or other mild reactions, there have not been serious cases. The Association of American Physicians and Surgeons (AAPS) notes that of 49 ivermectin studies, all show favorable results. Patients are dying, while over a billion doses have been used since the 1980s of this “very safe drug”. “Perhaps with this change, patients won’t need a court order to get a lifesaving drug,” according to AAPS executive director Dr. Jane Orient.

“Greece will start offering Covid-19 self-testing kits next month to the entire population of the country.” “Greece will be the first EU member-state to offer these tests to the entire population free-of-charge.”

• Greece Mobilizes Private Doctors to Cope With Surging Covid Infections (GR)

Greece announced on Monday it is mobilizing private doctors in an effort to contain the pressure on public hospitals struggling to cope with surging Covid-19 infections.Minister of Health, Vassilis Kikilias, said that despite an appeal for volunteers in the last few weeks “very few doctors came forward.” Of about 200 doctors requested by the government to assist their colleagues in the public sector, just 50 have come forward. Worse yet, attempts over the weekend to woo them with bonus fees failed. “Taking into account the emergency conditions and the urgent need for treatment of our fellow human beings, the Ministry of Health is mobilizing the services of Pathologists, Pulmonologists and General Practitioners in Attica,” Kikilias announced.

Doctors associations say the government should first recruit residents at state hospitals and other medical staff waiting to be hired before proceeding with the order, which they describe as absolutely extreme. On Sunday, Greece recorded another 1,514 new Covid-19 cases and the country broke yet another grim record, as a total of 674 people are now intubated in ICU units.The situation in Greece’s hospitals remains critical, with the capacity of many of them in Athens and other large cities being almost overwhelmed. Kikilias confirmed last week that Greece is “at the toughest point of the pandemic’s development.”He added that public hospitals are “on high emergency mode.”

Greece will start offering Covid-19 self-testing kits next month to the entire population of the country, the government said on Saturday.This comes as the latest addition to a series of measures that aim to curve the rising coronavirus infections in the country.Information and details on the new self-tests were announced by the Greek authorities, who claim that Greece will be the first EU member-state to offer these tests to the entire population free-of-charge.

“The government’s response has lacked a risk variant analysis on all our populations.”

• Growing Rebellion Against Draconian Covid Restrictions By Canadians (RT)

Some Canadians, armed with knowledge of the Charter of Rights and Freedoms, aren’t complying with the draconian and absurd measures, and instead are walking out of airports instead of being incarcerated in quarantine hotels. In March, nurse Jessica Faraone made headlines for doing just that and walking out of Toronto’s Pearson airport instead of subjecting herself to a costly $2,000-plus quarantine hotel stay. In a later interview, Faraone said a border guard had attempted to intimidate and shut her up, but she knew her rights. She added: “I have worked in the hospitals and more than ever I’m seeing suicide, depression, strokes, heart attacks, addiction issues. Masking people and children, oppressing health-care workers’ opinions that go against the grain, socially isolating people, and instilling fear into Canadians… is not how we solve this problem.”

And it’s not just well-informed individuals who are contesting the drastic measures. The Justice Centre for Constitutional Freedoms has been active in challenging the government both on quarantine hotels and on tickets issued to citizens for alleged violations of public health orders. The centre is also disseminating resources for Canadians to know their rights regarding Covid measures. Liberty Coalition Canada was formed after Covid restrictions were brought in. The coalition is a “national network of clergymen, elected officials, small business owners, legal experts and other concerned citizens” that now has a number of sub-groups addressing specific aspects of the measures Canada has taken. These include the social media campaign Save Our Youth, Reopen Ontario Churches, and the End the Lockdowns Caucus.

The latter comprises a number of current and former elected representatives who came together in February “resolved to ensure there is open, honest, and public debate regarding the Covid government response.” This body espouses what many ordinary Canadians have been feeling: “After careful examination and scrutiny of mitigation measures undertaken by all levels of government, it is now evident that the lockdowns cause more harm than the virus and must be brought to an end.” Likewise, the newly-formed Professionals Against Lockdowns – already listing over 100 professionals, including doctors, nurses, healthcare professionals, legal experts, police and teachers – aims to provide “evidence-based, scientific research that will educate and empower the public.”

Noting the widespread censorship of any dissenting voices on issues Covid, its statement reads: “It is our professional duty to protect the public, our communities, and our children. We will advocate for what is right and speak up against harm. Together, we will continue to be the voice for the voiceless to ensure that the truth about these lockdowns is heard. “The government’s response has lacked a risk variant analysis on all our populations. We are seeing the harm being done first-hand. We know lockdowns, isolation of healthy individuals, and the violation of our rights are causing more harm than good.”

“They’re strangely compelled to seek every possible opportunity to insult the public’s intelligence while destroying what’s left of American culture..”

• V. Putin Ain’t No Corn Pop (Kunstler)

Pretty soon, the president’s handlers will have to forbid him to open his pie-hole in public altogether. No more one-on-one interviews even with slow-pitch party shills like Mr. Stephanopoulos. They’ll just wheel him into the rose garden periodically like a cigar store Indian for proof-of-life demonstrations and leave the management of the nation… to others.

And how’s that going after a couple of months? Apparently, economic collapse is not enough for the party in charge of things now. They’re strangely compelled to seek every possible opportunity to insult the public’s intelligence while destroying what’s left of American culture. Case in point out of Nancy Pelosi’s Congress: HR1, the so-called “For the People Act,” institutionalizing ballot fraud in US elections. The law would make permanent the Covid-19 emergency mail-in voting system, over-riding whatever each state’s election law says — which makes the act appear patently unconstitutional — plus permitting same-day motor-voter registration of any live body, citizen or not, plus removing all voter ID requirements, and much more to ensure the country is never again threatened by a fair election.

Next up: HR5, the so-called “Equality Act,” institutionalizing the notion that categories of “male” and “female” are mere cultural constructs and must in no way be allowed to order any cultural activity from school to work to leisure. The bill was initially conceived to harden into law President Obama’s EO expanding the Department of Education’s Title IX rules on school sports — which eventuated in “trans women” disrupting girls’ sports. Now, men pretending to be women (and vice-versa) will be allowed to disrupt everything else in American life, especially the civil courts, with frivolous lawsuits.

Also in the pipeline: HR6, the so-called “American Dream and Promise Act,” and its Senate companion, S264, the plain “Dream Act,” that will grant permanent residency and then citizenship to currently “undocumented” people who snuck into the USA as children. The dreams and promises have already been delivered, even before the final passage of any new act, with an unprecedented flood of unaccompanied migrant children crashing the border, as well as a surge of adults fleeing Mexico and Central America. Apparently, the thinking in Washington these days is that we don’t have enough poor people in America, that their lives are not difficult enough. The message couldn’t be clearer to millions outside the United States: by all means, cross the border and we will do nothing about it.

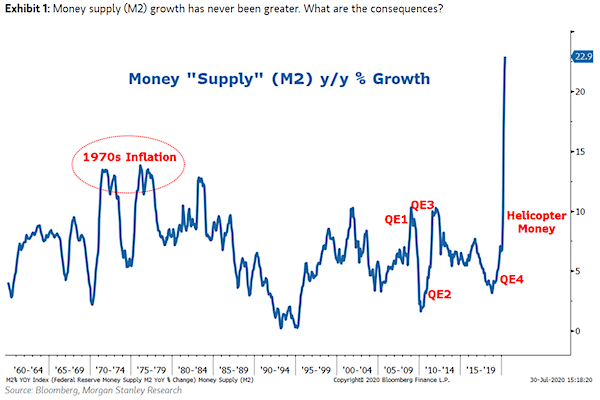

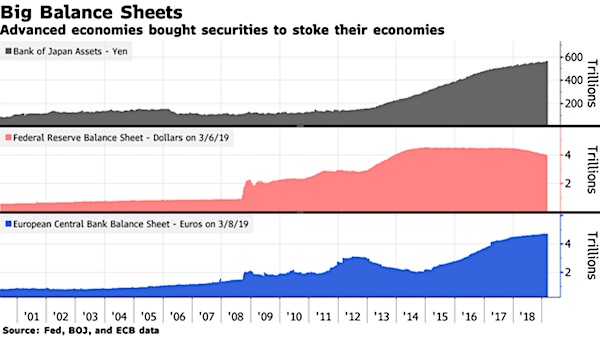

“When overspending does cause inflation, the MMT remedy is to remove money from circulation through progressive taxation, rather than by reducing spending and sacrificing the poor to unemployment.”

• Welcome To The Age Of Modern Monetary Theory (Kodrik)

Congress has authorized $6 trillion in deficit spending to defeat the coronavirus. That’s more than the United States spent fighting World War II, when $4 trillion of government spending released the country from the clutches of the Great Depression. Naturally, politicians and pundits debate whether the amount is excessive. But implicit in their seemingly routine deficit debate is a remarkable shift: Inflation has replaced debt — the old stalking horse for defeating progressive legislation — as the primary concern with deficit spending. It’s a subtle change, with profound consequences. And it augurs the rise of a revolutionary approach to political economy, Modern Monetary Theory (MMT), as the dominant paradigm in the politics of money.

Like Keynesians of yesteryear, Modern Monetary Theorists urge government to achieve full employment through fiscal policy, even when it requires deficit spending. Their comfort with large deficits emerges from an understanding that an obsession with national debt is a relic of another time, the age of gold standards and fixed currency arrangements. Today, in the age of national monetary sovereignty and free-floating currencies, countries like the United States can fulfill all financial obligations with a simple keystroke. Still, MMT economists don’t exactly scoff at deficits. Their point is that inflation, rather than rising national debt, is the best indicator of whether deficits are too large.

Short of extreme inflation, MMT encourages policymakers to juice the economy through government spending. Seen through MMT goggles, a tenet of economic orthodoxy is flipped on its head: Deficits appear as virtuous public investments, while surpluses become scourges, condemned for sucking money out of the economy. In this brave new world, the refusal of monetary sovereigns to run substantial deficits seems cruel and inefficient. According to MMT economist Stephanie Kelton, deficit spending can and should continue while additional spending can be absorbed by an economy’s productive resources. When overspending does cause inflation, the MMT remedy is to remove money from circulation through progressive taxation, rather than by reducing spending and sacrificing the poor to unemployment.

We are all MMT now.

• Next Round Of Us Fiscal Legislation Could Reach $4 Trillion – Goldman (FXS)

Analysts at Goldman Sachs eye another US fiscal stimulus, ranging to as high as $4.00 trillion, in their latest note published recently. The US bank suggests a minimum of $2.00 trillion of the infrastructure spending package, which could go to $4.00 trillion if including health care, education, and child care initiatives, in the next round of relief from US President Joe Biden. It should be noted that the bank anticipates higher taxes as a resource for paying the fiscal relief bill. “The tax plan proposed by President Biden in his election campaign would raise the statutory corporate tax rate on domestic income from 21% to 28%, partially reversing the cut from a rate of 35% passed in the 2017 Tax Cuts and Jobs Act. The plan would also raise the tax rate on foreign income (also called the “GILTI” tax) and institute a minimum corporate tax rate,” said the note further.

Edward Curtin starts out alright, but then…

• Media Pseudo-Debates and the Silence of Leftist Critics (Curtin)

You’ve heard of them, no doubt, the U.S. rulers who can’t rule too well and are always getting surprised by events or fed bad advice by their underlings. Their “mistakes” are always well intentioned. They stumble into wars through faulty intelligence. They drop the ball because of bureaucratic mix-ups. They miscalculate the perfidy of the elites whom allegedly they oppose while ushering them into the national coffers out of necessity since they are too big to fail. They never see the storm coming, even as they create it. Their incompetence is the retort to all those nut cases who conjure up conspiracy theories to explain their actions or lack thereof. They are innocent. Always innocent.

They and their media mouthpieces offer Americans, who are most eager to accept, what Lutheran pastor and anti-Nazi dissident Dietrich Bonhoeffer, executed at age thirty-nine by Hitler, called cheap grace: “Cheap grace is the grace we bestow on ourselves. Cheap grace is the preaching of forgiveness without requiring repentance…” These incompetents are, in the immortal words of the New York newspaper columnist Jimmy Breslin, “The Gang Who Couldn’t Shoot Straight.” Except they could and can. They’ve actually shot a lot of people, here and abroad. It’s one of their specialities. But they mean well. They screw up sometimes, but they mean well. They care, even while they kill millions with their guns and bombs. But they have their followers.

As another dissident thirty-nine-year-old pastor, executed by the American state, Martin Luther King, Jr. said: “Nothing in the world is more dangerous than sincere ignorance and conscientious stupidity.” The US rulers have their defenders. Most are corporate mainstream journalists whose jobs are to defend the ruling elites of both political parties. They will criticize across the political divides depending on their organizations’ political leanings at the moment. But they will never attack the fundamentals of the oligarchic war system since they are part of it. Their jobs depend on it. So CNN and The New York Times will obsessively attack Trump while Fox News will do the same to Obama or Biden. This is a game.

These days such massive media conglomerates are seemingly starkly divided and basically serve as adjuncts of one political party or the other. They are essentially political propagandists for either the Democrats or the Republicans and have abandoned any pretense to be anything else. They speak to their respective audiences in self-enclosed vacuums. They promote the divide that runs down the middle of the USA, a divide they helped to create.

Round-Up used to destroy entire crops. Anything else you wish to know?

• Biden Pushes Colombia to Restart Glyphosate Spraying Program

After a six-year halt, Colombia plans to restart the toxic aerial spraying of glyphosate on coca crops as early as next month—drawing “most welcome” support from U.S. President Joe Biden and sharp criticism from 150 regional experts who wrote to Biden, “your administration is implicitly endorsing former President Trump’s damaging legacy in Colombia.” On March 2nd, the Biden administration welcomed Colombia’s decision to restart its aerial coca eradication program in Biden’s first annual 2021 International Narcotics Control Strategy Report: “The government of Colombia has committed to re-starting its aerial coca eradication program, which would be a most welcome development.”

Colombia halted the controversial spraying program in 2015. In 2018, Colombia’s then-new President Ivan Duque vowed to resume the program but has yet to restart the aerial spraying The country faced increasing pressure from the United States to restart the program. “You’re going to have to spray,” former US President Donald Trump told Duque at the White House during a March 2, 2020 meeting. Aerial fumigation had been a central component of Plan Colombia, the 2005 multi-billion dollar U.S. program to finance the Colombian government war on coca cultivation and their war on FARC, which was Colombia’s largest rebel group before being disbanded in 2017.

But in 2015, the Colombian Supreme Court ruled that the spraying must end if the spraying of glyphosate was creating health problems. Also, in 2015, the World Health Organization found that glyphosate—also known as “Roundup”—was harmful to the environment and health, potentially causing cancer. In 2014, ending aerial fumigation was central to peace negotiations with FARC, with the Colombian government agreeing with FARC negotiators that it would transition away from aerial spraying. The Colombian government was also facing significant pressure from the rural poor, who were organizing national protests against aerial fumigation and other forms of forced eradication.

Hmmm. Sounds pretty weak.

• Bipartisan Australian MPs Meet With US Embassy About Julian Assange (SMH)

A cross-party delegation of Australian MPs has met with Washington’s top envoy in Canberra in their continued attempts to encourage the United States to drop its extradition attempts against the WikiLeaks founder. Nationals MP George Christensen, Independent Andrew Wilkie and Labor’s Julian Hill lobbied the US embassy’s charge d’affaires, Michael Goldman, on Monday morning, arguing the Australian citizen should be allowed to return home. The US Justice Department has appealed a British judge’s ruling that prevents Mr Assange from being extradited from London to face espionage charges. Judge Vanessa Baraitser ruled last month that while the case against the Australian was sound, his fragile mental health put him at “substantial risk” of taking his own life in prison.

Supporters of Mr Assange had hoped that new US President Joe Biden’s administration would opt to drop the case, which the Obama administration had declined to charge over concerns that doing so would put press freedoms at risk. He is accused of helping former army private Chelsea Manning obtain and leak classified information on the wars in Afghanistan and Iraq. Mr Wilkie, a whistleblowing intelligence officer-turned-MP, said the delegation raised numerous issues with Mr Goldman, including the increasing cross-party and public support for the US extradition of Mr Assange from the UK to be dropped. The trio argued the US was at risk of “reputational damage” over the inconsistency that WikiLeaks source, Chelsea Manning, had her sentence commuted while WikiLeaks founder, Julian Assange, was still being pursued.

[..] “It was heartening that Mr Goldman agreed to the meeting and gave us a fair hearing,” Mr Wilkie said. “Hopefully our representations this morning impressed upon him the broad concern in Australia, and indeed right around the world, at the shocking injustice being meted out to Julian Assange. The US’s pursuit of Mr Assange is obviously not in the public interest and must be dropped.”

We try to run the Automatic Earth on donations. Since ad revenue has collapsed, you are now not just a reader, but an integral part of the process that builds this site. Thank you for your support.

If the Queen moves four squares forward the Bishop can take her.

Support the Automatic Earth in virustime. Click at the top of the sidebars to donate with Paypal and Patreon.