Marion Post Wolcott Street scenes. Port Gibson, Mississippi 1940

And then they go after the Volcker rule. Take away their political power or else.

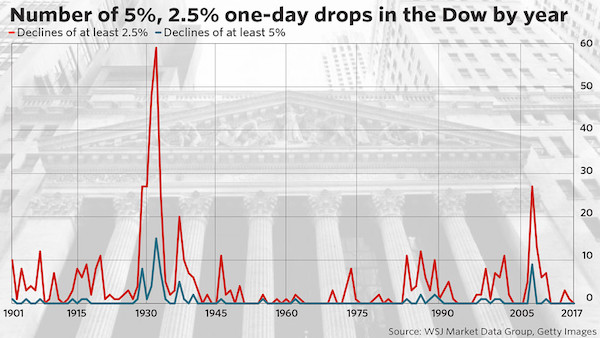

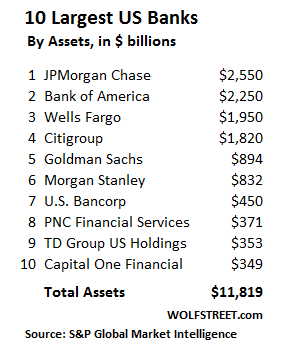

• Buybacks and Dividends Eat 100% of Bank Earnings (WS)

When tighter regulations were imposed on the banks after the Financial Crisis, the largest among them, the very ones that threatened to bring down the financial system, began squealing. Those voices are now being heard by Congress, which is considering deregulating the banks again. In particular, they claim that current capital requirements force banks to curtail their lending to businesses and consumers, and thus hurt the economy. Nonsense! That’s in essence what FDIC Vice Chairman Thomas Hoenig told Senate Banking Committee Chairman Mike Crapo and the committee’s senior Democrat, Sherrod Brown, in a letter dated Tuesday, according to Reuters. The senators are trying to find a compromise on bank deregulation. If banks wanted to increase lending, they could easily do so without lower capital requirements, Hoenig pointed out.

Rather than blowing their income on share-buybacks or paying it out in form of dividends, banks could retain more of their income, thus adding it to regulatory capital. Capital absorbs the losses from bad loans. Higher capital levels make a bank more resilient during the next crisis. If there isn’t enough capital, the bank collapses and gets bailed out. But banks that increase their capital levels through retained earnings are stronger and can lend more. Alas, in the first quarter, the 10 largest bank holding companies in the US plowed over 100% of their earnings into share buybacks and dividends, he wrote. If they had retained more of their income, they could have boosted lending by $1 trillion. The CEO of the top bank on this list has been very vocal about plowing more of the bank’s income into share buybacks and dividends, while pushing regulators to lower capital requirements.

In his “Dear Fellow Shareholders” letter in April, Jamie Dimon wrote under the heading “Regulatory Reform,” among many other things: “It is clear that the banks have too much capital.” “And we think it’s clear that banks can use more of their capital to finance the economy without sacrificing safety and soundness. Had they been less afraid of potential CCAR stress losses, banks probably would have been more aggressive in making some small business loans, lower rated middle market loans and near-prime mortgages. But the government was preventing them from doing it, he suggested.

I think it started when manufacturing was exported to China et al. How are you supposed to be productive when you don’t make anything?

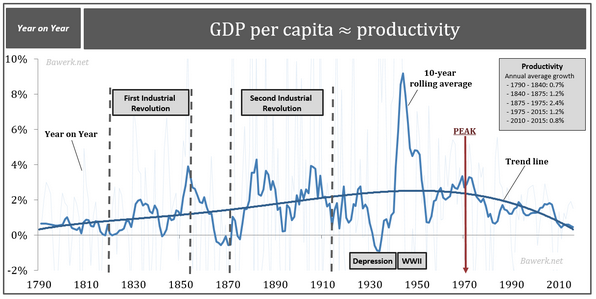

• America’s Productivity Plunge Explained (ZH)

For the first time since the financial crisis, US multifactor productivity growth turned negative last year, mystifying economists who have struggled to find something to blame for the fact that worker productivity is declining despite a technology boom that should make them more efficient – at least in theory. To be sure, economists have struggled to find explanations for the exasperating trend, with some arguing that the US hasn’t figured out how to properly measure productivity growth correctly now that service-sector jobs proliferate while manufacturing shrinks. But what if there’s a more straightforward explanation? What if the decline in US productivity measured since the 1970s isn’t happening in spite of technology, but because of it?

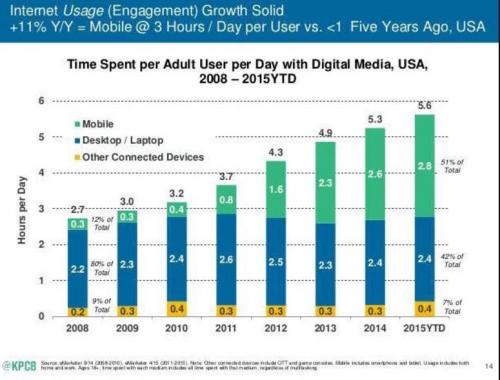

To wit, Facebook has just released user-engagement data for its popular Instagram photo-sharing app. Unsurprisingly, the data show that the average user below the age of 25 now spends more than 32 minutes a day on the app, while the average user aged 25 and older. The last time Facebook released this data, in October 2014, its users averaged 21 minutes a day on the app.

According to Bloomberg, “time spent is an important metric for advertisers, which like to hear that users are browsing an app beyond quick checks for updates, making them more likely to run into some marketing.” Maybe they should matter more to economists, too. Aside from short-lived booms in the 1990s and 2000s, US productivity growth has averaged just 1.2% from 1975 up to today after peaking above 3% in 1972. As we detailed previously, adjusting for the WWII anomaly (which tells us that GDP is not a good measure of a country’s prosperity) US productivity growth peaked in 1972 – incidentally the year after Nixon took the US off gold.

The productivity decline witnessed ever since is unprecedented. Despite the short lived boom of the 1990s US productivity growth only average 1.2 per cent from 1975 up to today. If we isolate the last 15 years US productivity growth is on par with what an agrarian slave economy was able to achieve 200 years ago. As we reported last year, users spent 51% of their total internet time on mobile devices, for a total of 5.6 hours per day snapchatting, face-booking, insta-graming and taking selfies.

The new wonders are the ones who don’t make dick all.

• Amazon is the New Tech Crash (David Stockman)

It won’t be long now. During the last 31 months the stock market mania has rapidly narrowed to just a handful of shooting stars. At the forefront has been Amazon.com, Inc., which saw its stock price double from $285 per share in January 2015 to $575 by October of that year. It then doubled again to about $1,000 in the 21 months since. By contrast, much of the stock market has remained in flat-earth land. For instance, those sections of the stock market that are tethered to the floundering real world economy have posted flat-lining earnings, or even sharp declines, as in the case of oil and gas. Needless to say, the drastic market narrowing of the last 30 months has been accompanied by soaring price/earnings (PE) multiples among the handful of big winners.

In the case of the so-called FAANGs + M (Facebook, Apple, Amazon, Netflix, Google and Microsoft), the group’s weighted average PE multiple has increased by some 50%. The degree to which the casino’s speculative mania has been concentrated in the FAANGs + M can also be seen by contrasting them with the other 494 stocks in the S&P 500. The market cap of the index as a whole rose from $17.7 trillion in January 2015 to some $21.2 trillion at present, meaning that the FAANGs + M account for about 40% of the entire gain. Stated differently, the market cap of the other 494 stocks rose from $16.0 trillion to $18.1 trillion during that 30-month period. That is, 13% versus the 82% gain of the six super-momentum stocks.

Moreover, if this concentrated $1.4 trillion gain in a handful of stocks sounds familiar that’s because this rodeo has been held before. The Four Horseman of Tech (Microsoft, Dell, Cisco and Intel) at the turn of the century saw their market cap soar from $850 billion to $1.65 trillion or by 94% during the manic months before the dotcom peak. At the March 2000 peak, Microsoft’s PE multiple was 60X, Intel’s was 50X and Cisco’s hit 200X. Those nosebleed valuations were really not much different than Facebook today at 40X, Amazon at 190X and Netflix at 217X. The truth is, even great companies do not escape drastic over-valuation during the blow-off stage of bubble peaks. Accordingly, two years later the Four Horseman as a group had shed $1.25 trillion or 75% of their valuation.

“The media don’t crow every time the price of milk goes up, so why should it cheer higher prices in a different market? It’s great only if you own the cow.”

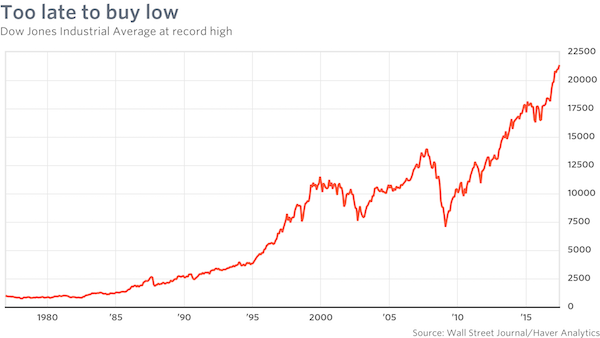

• Dow 22,000 Is Not Good News For Most Americans (MW)

The U.S. stock market hit another record Wednesday, with the Dow Jones Industrial Average surpassing 22,000 for the first time. The media acted like Dow 22,000 is a good thing. The cheerleaders in the anchor desks are wearing goofy hats and high-fiving each other like their team just won the Super Bowl. But record-high stock prices are not inherently a good thing. Whether it’s good for you individually depends on whether you own lots of shares or not. Most people do not own very many shares at all, so most of us aren’t benefiting much from high stock prices. The media don’t crow every time the price of milk goes up, so why should it cheer higher prices in a different market? It’s great only if you own the cow.

Who owns the stock market? About half of all equity is owned by the richest 1 million or so families, and another 41% is owned by the rest of the top 10%. The bottom 90% of families own about 9% of outstanding shares. [..] High stock prices might have a benefit if it meant that more capital would be invested in America’s corporations. That’s the myth of the stock market, anyway. In reality, the stock market doesn’t funnel any additional capital into corporations at all. Nonfinancial corporations have been net buyers — not sellers — of equities for the past 23 years in a row. The stock market is actually a process for extracting wealth from corporations and passing it along to the wealthy people who owns shares.

The headline bumbers are all you need really. Ponzi as far as the eye can see.

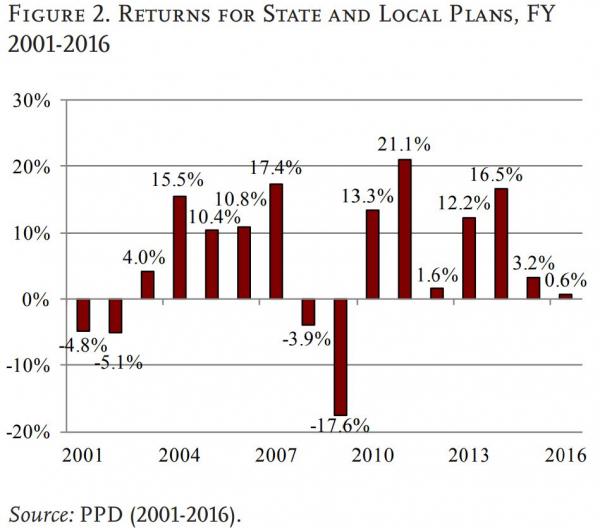

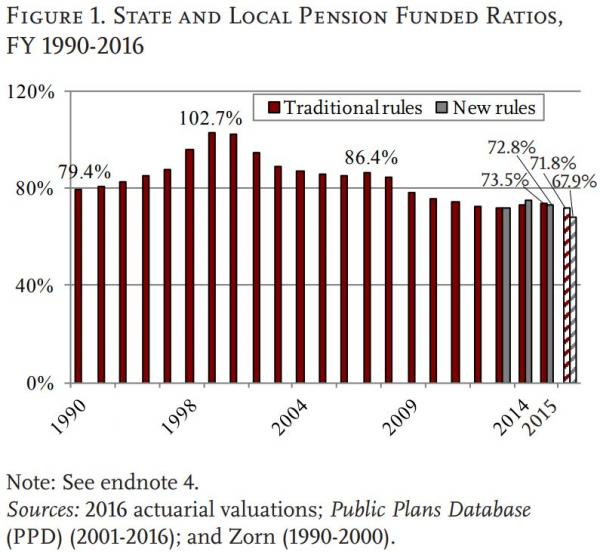

• Public Pensions Average 0.6% Return In 2016 Despite 7.6% Assumption (ZH)

We’ve frequently argued that public pension funds in the U.S. are nothing more than thinly-veiled ponzi schemes with their ridiculously high return assumptions specifically intended to artificially minimize the present value of future retiree payment obligations and thus also minimize required annual contributions from taxpayers…all while actual, if immediately intangible, underfunded liabilities continue to surge. As evidence of that assertion, we present to you the latest public pension analysis from the Center for Retirement Research at Boston College. As part of their study, Boston College reviewed 170 public pension plans in the U.S. and found that their average 2016 return was an abysmal 0.6% compared to an average assumed return of 7.6%. Meanwhile, per the chart below, the average return for the past 15 years has also been well below discount rate assumptions, at just 5.95%.

All of which, as we stated above, continues to result in surging liabilities and collapsing funding ratios.

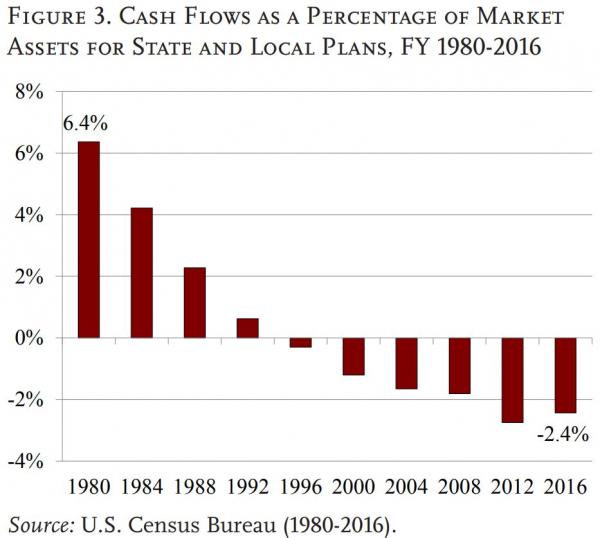

But, perhaps the most telling sign of the massive ponzi scheme being perpetrated on American retirees is the following chart which shows that net cash flows have become increasingly negative, as a percentage of assets, as annual cash benefit payments continue to exceed cash contributions.

Conclusion, you can hide behind high discount rates and a “kick the can down the road” strategy in the short-term…but in the long run actual cash flows matter.

Pensions, planning: good luck in the bubble.

• Plan For The Worst (Roberts)

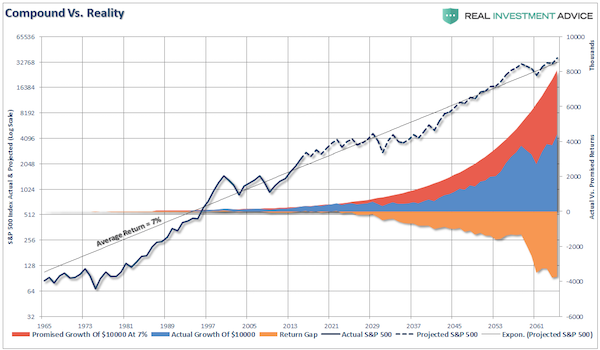

One of the biggest mistakes that people make is assuming markets will grow at a consistent rate over the given time frame to retirement. There is a massive difference between compounded returns and real returns as shown. The assumption is that an investment is made in 1965 at the age of 20. In 2000, the individual is now 55 and just 10 years from retirement. The S&P index is actual through 2016 and projected through age 100 using historical volatility and market cycles as a precedent for future returns. While the historical AVERAGE return is 7% for both series, the shortfall between “compounded” returns and “actual” returns is significant. That shortfall is compounded further when you begin to add in the impact of fees, taxes, and inflation over the given time frame.

The single biggest mistake made in financial planning is NOT to include variable rates of return in your planning process. Furthermore, choosing rates of return for planning purposes that are outside historical norms is a critical mistake. Stocks tend to grow roughly at the rate of GDP plus dividends. Into today’s world GDP is expected to grow at roughly 2% in the future with dividends around 2% currently. The difference between 8% returns and 4% is quite substantial. Also, to achieve 8% in a 4% return environment, you must increase your return over the market by 100%. The level of “risk” that must be taken on to outperform the markets by such a degree is enormous. While markets can have years of significant outperformance, it only takes one devastating year of losses to wipe out years of accumulation.

A new business model? Does this apply only to oil, or should all businesses cut their sales prices in half to increase their profits? Alternatively, maybe shareholders should sue BP and Shell for all missed profits in the past?

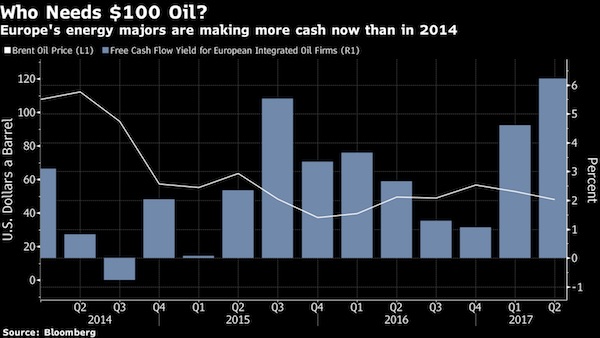

• Who Needs $100 Oil? Majors Making More Cash at $50, Goldman Says (BBG)

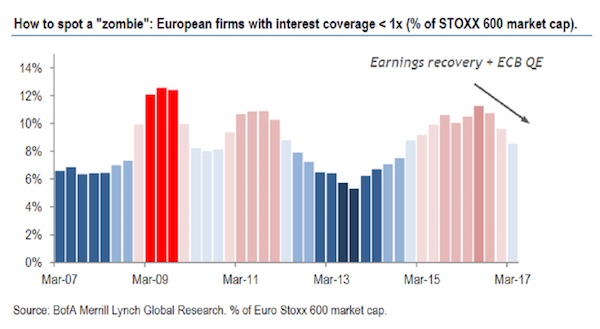

Oil majors are raking in more cash now than they did in the heyday of $100 oil, according to Goldman Sachs. Integrated giants like BP and Royal Dutch Shell have adapted to lower prices by cutting costs and improving operations, analysts at the bank including Michele Della Vigna said in a research note Wednesday. European majors made more cash during the first half of this year, when Brent averaged $52 a barrel, than they did in the first half of 2014 when prices were $109. Back then, high oil prices had caused executives to overreach on projects, leading to delays, cost overruns and inefficiency, Goldman said. Those projects are coming online now, producing more revenue, while companies have tightened their belts and divested some assets to reduce debt burdens.

“Simplification, standardization and deflation are repositioning the oil industry for better profitability and cash generation in the current environment than in 2013-14 when the oil price was above $100 a barrel,” the analysts said. In the second quarter, Europe’s big oil companies generated enough cash from operations to cover 91 percent of their capital expenses and dividends, showing that they’re close to being able to fund shareholder payments with business-generated revenue, according to Goldman. That will give companies the ability to stop paying dividends by issuing new stock, which has diluted major European energy shares by 3 to 13 percent since 2014.

Too late.

• China’s Fear of Japan-Style Economic Bust Drives Crackdown on Deals (BBG)

President Xi Jinping’s top economic adviser commissioned a study earlier this year to see how China could avoid the fate of Japan’s epic bust in the 1990s and decades of stagnation that followed. The report covered a wide range of topics, from the Plaza Accord on currency to a real-estate bubble to demographics that made Japan the oldest population in Asia, according to a person familiar with the matter who has seen the report. While details are scarce, the person revealed one key recommendation that policy makers have since implemented: The need to curtail a global buying spree by some of the nation’s biggest private companies. Communist Party leaders discussed Japan’s experience in a Politburo meeting on April 26, according to the person, who asked not to be identified as the discussions are private.

State media came alive afterward, with reports trumpeting Xi’s warning that financial stability is crucial in economic growth. Then in June came a bombshell: reports that the banking regulator had asked lenders to provide information on overseas loans made to Dalian Wanda Group Co., Anbang Insurance Group Co., HNA, Fosun International Ltd. and the owner of Italian soccer team AC Milan. While the timing of those requests is unclear, other watchdogs soon issued directives to curb excessive borrowing, speculation on equities and high yields in wealth-management products. Jim O’Neill, previously chief economist at Goldman Sachs and a former U.K. government minister, said Chinese policy makers are constantly looking to avoid the mistakes of other countries — and Japan in particular.

“You see it in repeated attempts to stop various potential property bubbles so China doesn’t end up with a Japan-style property collapse,” O’Neill said in an email. “There does appear to be some signs that some Chinese investors don’t invest in clear understandable ways, but they wouldn’t be the only ones where that is true!” [..] The moves reflect concerns that China’s top dealmakers have borrowed too much from state banks, threatening the financial system and ultimately the party’s legitimacy to rule — a key worry ahead of a once-in-five-year conclave later this year that will cement Xi’s power through 2022.

Well argued by Russia’s PM, and it shows just how extensive the sanctions are. Does America need decades more of Cold War?: “The sanctions codified into law will now last for decades, unless some miracle occurs. [..] the future relationship between the Russian Federation and the United States will be extremely tense, regardless of the composition of the Congress or the personality of the president.”

• The US Just Declared Full-Scale Trade War On Russia (Medvedev)

The signing of new sanctions against Russia into law by the US president leads to several consequences. First, any hope of improving our relations with the new US administration is over. Second, the US just declared a full-scale trade war on Russia. Third, the Trump administration demonstrated it is utterly powerless, and in the most humiliating manner transferred executive powers to Congress. This shifts the alignment of forces in US political circles.

What does this mean for the U.S.? The American establishment completely outplayed Trump. The president is not happy with the new sanctions, but he could not avoid signing the new law. The purpose of the new sanctions was to put Trump in his place. Their ultimate goal is to remove Trump from power. An incompetent player must be eliminated. At the same time, the interests of American businesses were almost ignored. Politics rose above the pragmatic approach. Anti-Russian hysteria has turned into a key part of not only foreign (as has been the case many times), but also domestic US policy (this is recent).

The sanctions codified into law will now last for decades, unless some miracle occurs. Moreover, it will be tougher than the Jackson-Vanik law, because it is comprehensive and can not be postponed by special orders of the president without the consent of the Congress. Therefore, the future relationship between the Russian Federation and the United States will be extremely tense, regardless of the composition of the Congress or the personality of the president. Relations between the two countries will now be clarified in international bodies and courts of justice leading to further intensification of international tensions, and a refusal to resolve major international problems.

What does this mean for Russia? We will continue to work on the development of the economy and social sphere, we will deal with import substitution, solve the most important state tasks, counting primarily on ourselves. We have learned to do this in recent years. Within almost closed financial markets, foreign creditors and investors will be afraid to invest in Russia due to worries of sanctions against third parties and countries. In some ways, it will benefit us, although sanctions – in general – are meaningless. We will manage.

No, Hersh is not some kind of nut.

• Seymour Hersh: RussiaGate Is A CIA-Planted Lie, Revenge Against Trump (Zuesse)

During the latter portion of a phone-call by investigative journalist, Seymour Hersh, Hersh has now presented “a narrative [from his investigation] of how that whole fucking thing began,” including who actually is behind the ‘RussiaGate’ lies, and why they are spreading these lies.

In a youtube video upload-dated August 1st, he reveals from his inside FBI and Washington DC Police Department sources — now, long before the Justice Department’s Special Counsel Robert Mueller will be presenting his official ‘findings’ to the nation — that the charges that Russia had anything to do with the leaks from the DNC and Hillary Clinton’s campaign to Wikileaks, that those charges spread by the press, were a CIA-planted lie, and that what Wikileaks had gotten was only leaks (including at least from the murdered DNC-staffer Seth Rich), and were not from any outsider (including ’the Russians’), but that Rich didn’t get killed for that, but was instead shot in the back during a brutal robbery, which occurred in the high-crime DC neighborhood where he lived. Here is the video…

So maybe Paul Craig Roberts lays it on a bit thick sometimes. But what happens in America is dangerous, and Trump is not the principal danger.

• The Witch Hunt for Donald Trump Surpasses the Salem Witch Trials (PCR)

In 1940 US attorney general Robert Jackson warned federal prosecutors against “picking the man and then putting investigators to work, to pin some offense on him. It is in this realm—in which the prosecutor picks some person whom he dislikes or desires to embarrass, or selects some group of unpopular persons and then looks for an offense—that the greatest danger of abuse of prosecuting power lies. It is here that law enforcement becomes personal, and the real crime becomes that of being unpopular with the predominant or governing group, being attached to the wrong political views or being personally obnoxious to, or in the way of, the prosecutor himself.” Robert Jackson has given a perfect description of what is happening to President Trump at the hands of special prosecutor Robert Mueller.

Trump is vastly unpopular with the ruling establishment, with the Democrats, with the military/security complex and their bought and paid for Senators, and with the media for proving wrong all the smart people’s prediction that Hillary would win the election in a landslide. From day one this cabal has been out to get Trump, and they have given the task of framing up Trump to Mueller. An honest man would not have accepted the job of chief witch-hunter, which is what Mueller’s job is. The breathless hype of a nonexistent “Russian collusion” has been the lead news story for months despite the fact that no one, not the CIA, not the NSA, not the FBI, not the Director of National Intelligence, can find a scrap of evidence.

In desperation, three of the seventeen US intelligence agencies picked a small handful of employees thought to lack integrity and produced an unverified report, absent of any evidence, that the hand-picked handful thought that there might have been a collusion. On the basis of what evidence they do not say. That nothing more substantial than this led to a special prosecutor shows how totally corrupt justice in America is. Furthermore the baseless charge itself is an absurdity. There is no law against an incoming administration conversing with other governments. Indeed, Trump, Flynn, and whomever should be given medals for quickly moving to smooth Russian feathers ruffled by the reckless Bush and Obama regimes. What good for anyone can come from ceaselessly provoking a nuclear Russian bear?

Spent so much time in that stadium watching baseball etc. Good memories.

• Canada Opens Montreal’s Olympic Stadium To House Asylum Seekers (R.)

Canadian health authorities and aid workers are using an Olympic stadium to shelter asylum seekers as a growing number of people walk into the country from the United States. The Quebec Red Cross and local health authorities opened Montreal’s Olympic Stadium on Wednesday to asylum seekers brought in by bus after having crossed the U.S. border, Red Cross spokeswoman Stephanie Picard said. The city is seeing a growing influx in refugee claimants coming from the United States and is scrambling to house them all. The Red Cross is assisting with beds and providing bedding and other personal-care items. Montreal’s health authority would not provide exact numbers on how many people are being housed in the stadium, built for the 1976 Olympics and which now serves as an event space.

More than 4,300 people have walked across the U.S. border into Canada this year seeking refugee status. The vast majority of them come to Quebec, according to figures from the federal government. Many asylum seekers who spoke to Reuters say they left the United States fearing President Donald Trump’s immigration crackdown. People who cross the border illegally to file refugee claims are apprehended and held for questioning by both police and border officials before being allowed to file claims and live in Canada while their application is processed. Montreal Mayor Denis Coderre welcomed the asylum seekers on Twitter Wednesday afternoon, saying 2,500 people had come in July alone. He said on Twitter that providing for the new arrivals is a “humanitarian gesture.”

Look, there have to be limits, or we will not survive this, none of us. Locking up children just because they have fled bombs is beyond insane.

• Number Of Child Refugees In Greek Detention Centres Rises ‘Alarmingly’ (PA)

The number of unaccompanied child migrants living in “dirty” Greek detention centres has increased “alarmingly”, a human rights organisation has warned. An estimated 117 children were in police cells or custody centres in Greece at the end of July, compared to just two in November 2016, according to figures released by the country’s government. Under Greek law, the authorities should separate minors into safe accommodation, where they are appointed guardians who represent them in legal proceedings. But when there is no space in safe shelters, the authorities detain them in police stations and immigration detention facilities, sometimes with unrelated adults. “Instead of being cared for, dozens of vulnerable children are locked in dirty, crowded police cells and other detention facilities across Greece, in some cases with unrelated adults,” said Eva Cossé, the country’s researcher at Human Rights Watch.

“The Greek government has a duty to end this abusive practice and make sure these vulnerable kids get the care and protection they need.” Human Rights Watch has written to Migration Policy Minister Yiannis Mouzalas to stop the automatic detention of unaccompanied children. It suggested the government should amend legislation and significantly shorten the amount of time a child can be detained in protective custody. While they wait for a space in a shelter, many children are not provided with information about their rights and are not told how to apply for asylum, the organisation said. Aid workers have previously reported that the uncertainty and distress caused by the asylum process, exacerbated an ongoing mental health crisis among migrants living on the islands. Children as young as nine have harmed themselves, while 12-year-olds have attempted to kill themselves, Save the Children said in March.

Too big NOT to fail.

• We Got Too BIG For The World (Kingsnorth)

Living through a collapse is a curious experience. Perhaps the most curious part is that nobody wants to admit it’s a collapse. The results of half a century of debt-fueled “growth” are becoming impossible to deny convincingly, but even as economies and certainties crumble, our appointed leaders bravely hold the line. No one wants to be the first to say the dam is cracked beyond repair. To listen to a political leader at this moment in history is like sitting through a sermon by a priest who has lost his faith but is desperately trying not to admit it, even to himself. Watch your chosen president or prime minister mouthing tough-guy platitudes to the party faithful. Listen to them insisting in studied prose that all will be well. Study the expressions on their faces as they talk about “growth” as if it were a heathen god to be appeased by tipping another cauldron’s worth of fictional money into the mouth of a volcano.

In times like these, people look elsewhere for answers. A time of crisis is also a time of opening up, when thinking that was consigned to the fringes moves to center stage. When things fall apart, the appetite for new ways of seeing is palpable, and there are always plenty of people willing to feed it by coming forward with their pet big ideas. But here’s a thought: what if big ideas are part of the problem? What if, in fact, the problem is bigness itself? The crisis currently playing out on the world stage is a crisis of growth. Not, as we are regularly told, a crisis caused by too little growth, but by too much of it. Banks grew so big that their collapse would have brought down the entire global economy. To prevent this, they were bailed out with huge tranches of public money, which in turn is precipitating social crises on the streets of Western nations. The European Union has grown so big, and so unaccountable, that it threatens to collapse in on itself.

Corporations have grown so big that they are overwhelming democracies and building a global plutocracy to serve their own interests. The human economy as a whole has grown so big that it has been able to change the atmospheric composition of the planet and precipitate a mass-extinction event. One man who would not have been surprised by this crisis of bigness, had he lived to see it, was Leopold Kohr. Kohr has a good claim to be the most interesting political thinker that you have never heard of. Unlike Karl Marx, he did not found a global movement or inspire revolutions. Unlike Friedrich Hayek, he did not rewrite the economic rules of the modern world. Kohr was a modest, self-deprecating man, but this was not the reason his ideas have been ignored by movers and shakers in the half-century since they were produced. They have been ignored because they do not flatter the egos of the power-hungry, be they revolutionaries or plutocrats. In fact, Kohr’s message is a direct challenge to them.

“Wherever something is wrong,” he insisted, “something is too big.”