RT : What is the likelihood that the US will go through with and actually impose economic sanctions on China if it does not implement the new sanctions regime against North Korea? Jim Rogers : Sanctions are sanctions. They could do sanctions which are not very important or don’t do much damage. And then they will have good public relations which says they have sanctions, but it is meaningless. I would suspect if anything, that is what they will start with. If they put sanctions on China in a big way, it brings the whole world economy down. And in the end, it hurts America more than it hurts China because it just forces China and Russia and other countries closer together. Russia and China and other countries are already trying to come up with a new financial system. If America puts sanctions on them, they would have to do it that much faster and in the end America will lose its monopoly on the financial system, which will hurt America more than anybody.

RT : What do you think, is it an empty rhetoric and saber-rattling from Donald Trump because he said “those [UN] sanctions are nothing compared to what ultimately will have to happen” without specifying what he meant by that. Do you think this is just mere bluff on the part of the US, or would it really use the ‘nuclear option’? JR : If it uses a nuclear option for sanctions, it will hurt America much more than will hurt North Korea, it will hurt America much more than it will hurt China, Russia and everybody else. It will force the rest of the world to find an alternative to the US financial system. If he does that, it is going to cause a lot of turmoil in the world financial economy and in the end it is going to hurt America more than it is going to hurt anybody else. I would give you an example, if you look at Russian agriculture right now – America put sanctions on Russian agriculture trying to hurt Russia, but it has helped Russian agriculture. Russian agriculture is booming now. In the end, America has hurt itself more than it has hurt anybody else.

RT : If that happens, what would the consequences be for the global economy? Could this end up becoming a global economic crisis? JR : We are probably going to have a global economic problem, maybe even crisis, in the next couple of years. This may be one of the things that start it. There is always something which starts a crisis. If America does something like this, this could be the thing that did it. In 1929, it started when America started a huge trade war with the rest of the world and the economists said, “please, this is a mistake,” but America did that anyway. And then we had a great collapse and The Great Depression of the 1930s.

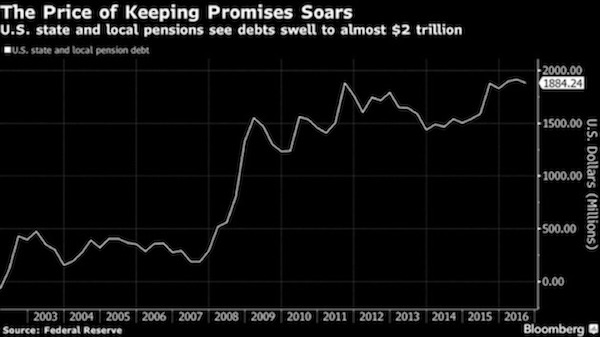

Total unfunded liabilities in state and local pensions have roughly quintupled in the last decade. You read that right – not doubled, tripled or quadrupled: quintupled. That’s nice when it happens on a slot machine, not so nice when it’s money you owe. The graph [shows] that unfunded pension liabilities for state and local governments was $2 trillion. But that assumes an average 7% compound return. What if we assume 4% compound returns? Now the admitted unfunded pension liability is $4 trillion. But what if we have a recession and the stock market goes down by the past average of more than 40%? Now you have an unfunded liability in the range of $7–8 trillion.We throw the words a trillion dollars around, not realizing how much that actually is. Combined state and local revenues for the US total around $2.6 trillion.

Following the next recession (whenever that is), the unfunded pension liabilities for state and local governments will be roughly three times the revenue they are collecting today, and that’s before a recession reduces their revenues. Can you see the taxpayer stuck between a rock and a hard place? Two immovable objects meeting? The math just doesn’t work. Pension trustees don’t face personal liability. They’re literally playing with someone else’s money. Some try very hard to be realistic and cautious. Others don’t. But even the most diligent can’t control when the next recession comes, or when the stock market will crash, leaving a gaping hole in their assets while liabilities keep right on rising. I have had meetings with trustees of various government pensions.

Many of them want to assume a more realistic discount rate, but the politicians in their state literally refuse to allow them to assume a reasonable discount rate, because owning up to reality would require them to increase their current pension funding dramatically. So they kick the can down the road. Intentionally or not, state and local officials all over the US made pension promises that future officials can’t possibly keep. Many will be out of office when the bill comes due, protected from liability by sovereign immunity. We are starting to see cities filing for bankruptcy. That small ripple will be a tsunami within 7–10 years.

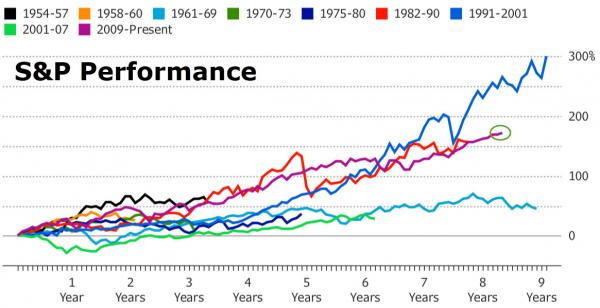

U.S. stocks have risen more in the past eight years than in almost any other post-World War II time of economic growth, as defined by the National Bureau of Economic Research. The logic here is that economic expansions fuel bull markets and so it’s reasonable to measure market recoveries after a period of macro contraction ends. Using that definition, let’s review how the S&P 500 has performed during the last ten economic recoveries. To be precise, the birth of the stock market’s bull market is dated as the first day after an NBER-defined recession has ended. The market run continues through the peak. The S&P 500 Index jumped 172% from July 2009, when the current expansion started, through Wednesday. The biggest advance was about 300% and occurred from April 1991 to March 2001, when Internet-related stocks soared.

As Capital Speculator blog’s James Picerno notes, the question before the house: Will the momentum of late endure long enough to overtake the 1991-2001 record in duration and/or magnitude? If so, the bull market in the here and now has to last another 463 trading days, which translates into a market rally that goes deep into 2019. There’s just one thing wrong… Remember – the ‘market’ is not the ‘economy’… or maybe it is in the new normal?

I provide a simple numerical explanation of how austerity works at the micro (individual person, industrial sector, or country) and the macro level (country, or group of countries in a currency union).

Dan Davies, senior research adviser at Frontline Analysts, argued there’s no point in attempting to value bitcoin as if it were just another type of security. “It’s not a security with some intrinsic value, rather it’s a currency that in the long term is governed by an exchange rate driven by trade or volume of transactions,” Davies said. The fact that a significant proportion of bitcoins is hoarded or held for investment doesn’t disqualify it from being a currency, according to Davies. But the BTC/USD BTCUSD, -3.37% exchange rate is entirely determined by speculative portfolio capital flows right now, he said, leaving it difficult to assign fair value. Viewing bitcoin as a currency makes it possible, at least in theory, to come up with a long-term exchange rate by using the quantity theory of money.

The formula is: MV = PT, where money supply multiplied by its velocity equals the price level multiplied by the transaction volume. Since both price and transaction volume is expressed in U.S. dollars, the price of bitcoin would be 1/BTCUSD, Davies said. In this case, bitcoin’s supply is fixed at 21 million and money velocity for normal currencies is usually at around 10, according to Davies. So, the long-term fundamental value of bitcoin equals the long-term value of transactions that will be carried out in bitcoin divided by 210 million (21 million bitcoins multiplied by velocity). The hardest value to plug into this formula is the transaction volume. If, for example, bitcoin was used primarily for global trade in illicit drugs, the figure would be around $120 billion, which is an estimate the U.N. used in 2014.

“I used that number a few years ago, but we would have to come up with a different estimate, as bitcoin is clearly used for things other than illicit drugs now,” Davies said. Davies declined to offer an updated number, saying he needed to do more research. But doubling that transaction volume number to $240 billion, for example, and dividing by 210 million produces a value of $1,142, around a third of the current exchange rate of $3,569. That isn’t far from an estimate that Mohamed El-Erian, chief economic adviser at Allianz Global Investors, recently suggested as a fair value for bitcoin. In an interview with CNBC, El-Erian said the fair price should be about half or a third of what it is now. El-Erian argued the currency will only survive as a peer-to-peer means of payment and governments won’t allow mass adoption.

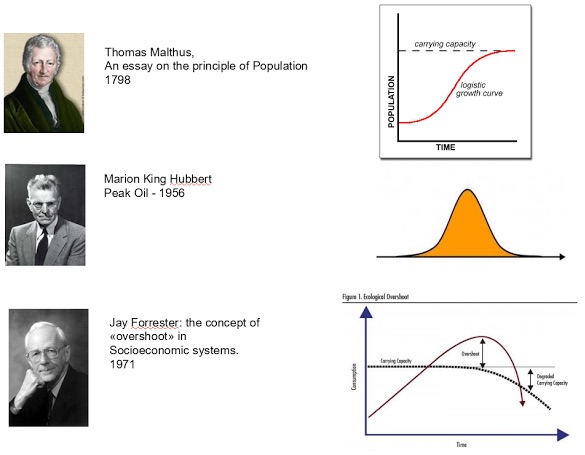

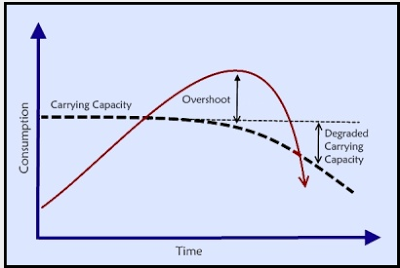

My talk at the Summer Academy of the Club of Rome was mainly a presentation of my latest book, “The Seneca Effect” (Springer 2017). In practice, of course, a book contains many more things than you can say in a 40 minute speech. So, I tried to concentrate on the idea that the behavior I call “the Seneca Curve” is very common, even universal. Below, you can see the Seneca Curve: things go up slowly but collapse rapidly, as the Roman philosopher Seneca said first some two thousand years ago. You may have heard the old Latin motto, “Natura non facit saltus” (Nature doesn’t make jumps) meaning that things change gradually, not abruptly. It may be true in many circumstances but, in practice, it is wholly normal that Nature accumulates energy potentials (as when you inflate a balloon) and then releases them all of a sudden (as when you puncture a balloon).

There are reasons why Nature behaves in this way, but the point I made at the school was not so much about why the curve is so common but how human beings are not normally aware of it. In fact, our thought is often shaped by the idea that things will continue evolving the way they have been evolving up to a certain point. Just think about economic growth, and you’ll notice how economists expect it to continue forever. It goes without saying that the economy is one of those complex systems which are most vulnerable to the Seneca collapse. So, I tried to stress that the understanding that the Seneca Curve exists and it is common is a recent discovery. Even though Seneca had understood it by intuition already almost 2000 years ago, in its modern form it is less than a century old. It was proposed for the first time by Jay Forrester in the 1960s and it was enshrined in “The Limits to Growth” study of 1972, even though the term “Seneca Effect” was not used.

During my talk, I showed this image to evidence how our ideas on the path that complex systems follow evolved over time. You see how modern the idea of “overshoot” (and the subsequent collapse) is. Malthus just didn’t have it. Despite being often accused of catastrophism, he couldn’t envisage societal collapse; he lacked the necessary intellectual tools. He was an optimist! Today, we have this concept. We know that complex systems tend not just to decline, they tend to collapse. But this perception is totally missing in the general debate. When you mention societal collapse, there are two possible reactions. The most common one is that such a thing will never happen.

Then, if you manage to convince people that it is possible, they endeavor to do everything they can to keep the system going; whatever it takes. They don’t realize that when you exceed the carrying capacity of the system, you have to come back, one way or another. And the more you try to stay above the limit, the faster and the harsher the return will be. What you have to do is to ease the collapse, follow it, not try to stop it. Otherwise, it will be worse.

Only business owners with no real estate properties will qualify for a partial write-off of corporate debts in the context of the extrajudicial settlement mechanism. This criterion excludes the owner’s main residence and the production properties, i.e. the professional properties used for the entrepreneurial activity. That was the decision that the technical experts of the country’s creditors are said to have reached with representatives of Greek banks and the Independent Authority for Public Revenue, while there was also convergence on setting the criteria for debt settlement for companies owing between €20,000 and €50,000. In this latter category of debtors, which mostly comprise small enterprises, a standardized procedure will be adopted for assessing repayment capacity and the determination of the amount that the debtor will have to pay on a regular basis.

The Greece firesale will never come anywhere near the €60 billion, but everyone keeps mentioning the number. Their entire railway system went for €45 million. Selling off an entire country is a very bad idea. Europe will find out, but too late.

“It is obvious. Our policies have changed radically, ” says Stergios Pitsiorlas, the deputy economy and development minister, whose airy office is visited daily by bankers, hedge-fund managers and industrialists jockeying for bargains. “Being leftwing doesn’t mean you are also a fool. It doesn’t mean, in the words of Lenin, that we are useful idiots. Let’s speak seriously. Those who complain that Greece is being sold off, that Greece will lose out, don’t know what they are talking about.” Tall, bearded and bespectacled, Pitsiorlas is the point man in Athens’s attempt to raise €60bn (£53bn) through privatisations – sales that, increasingly, have become the focus of international creditors keeping the debt-stricken country afloat. In what has been called the most ambitious sell-off in modern European history, assets ranging from public utilities and transport companies to marinas and hotels are up for grabs.

[..] Privatisations are central to completion of a new round of bailout negotiations with the EU and IMF. Greece’s third, €86bn, rescue programme is due to end next summer and Tsipras has made a clean exit from it, which would herald Athens’s return to the markets, an overarching goal. But hurdles lie ahead. On Friday, eurozone finance ministers warned that continued persecution of the country’s former statistics chief, Andreas Georgiou, could dent international confidence and derail chances of recovery. Officials also raised the prospect of fresh austerity should Greece fail to hit the primary surplus target of 3.5% – a prospect made likely by a huge shortfall in tax revenues. But in a week when the Italians finally took control of Greece’s state-owned train network (acquired by Italy’s own state operator for a paltry €45m) Pitsiorlas is optimistic.

He cites the takeover of Piraeus port by the Chinese shipping conglomerate Cosco as an example of what privatisations can bring: “They will make it the biggest port in Europe and that will boost other professions, create thousands of jobs, revitalise shipyards, which they are also looking at, pave the way to better trains, roads and logistic centres, and trigger development and growth.” In five years, he enthuses, Greece will be a very different place, cosmopolitan and vibrant. “There are rules which need to be observed but ultimately everything will be solved,” he insisted, referring to the obstacles Eldorado and others have encountered. “A miracle will happen. There will be huge change … but the state can’t do it alone, the private sector has to be involved.”

Beijing will suspend construction of major public projects in the city this winter in an effort to improve the capital’s notorious air quality, official media said on Sunday, citing the municipal commission of housing and urban-rural development. All construction of road and water projects, as well as demolition of housing, will be banned from Nov. 15 to March 15 within the city’s six major districts and surrounding suburbs, said the Xinhua report. The period spans the four months when heating is supplied to the city’s housing and other buildings. China is in the fourth year of a “war on pollution” designed to reverse the damage done by decades of untrammelled economic growth and allay concerns that hazardous smog and widespread water and soil contamination are causing hundreds of thousands of early deaths every year.

Beijing has promised to impose tough industrial and traffic curbs across the north of the country this winter in a bid to meet key smog targets. In the capital, it is aiming to reduce airborne particles known as PM2.5 by more than a quarter from their 2012 levels and bring average concentrations down to 60 micrograms per cubic metre. Last year the city experienced near record-high smog in January and February, which the government blamed on “unfavourable weather conditions” Some ‘major livelihood projects’ such as railways, airports and affordable housing may be continued however, providing they are approved by the commission, said the report.

The European Union said President Donald Trump’s administration is shifting its approach to a landmark global agreement on climate change, an assertion which was quickly denied by the White House. The U.S. signaled that it’s no longer seeking to withdraw from the pact and then renegotiate it, but rather wants to re-engage with the Paris Agreement from within, said EU’s climate chief Miguel Arias Canete. He spoke in an interview from Montreal, where the U.S., China, Canada and almost 30 other countries gathered to discuss the most-sweeping accord to date to protect the environment. “Our position on the Paris agreement has not changed. @POTUS has been clear, US withdrawing unless we get pro-America terms,” White House Press Secretary Sarah Huckabee Sanders said on Twitter.

Announcing plans to quit the pact, Trump said in June that the agreement favored other countries at the expense of U.S. workers and amounted to a “massive redistribution” of U.S. wealth. Trump’s administration last month began the formal process of exiting from the climate accord, drawing fire from allies and foes alike. EU climate commissioner Canete made the comments about a change of stance after meeting with Everett Eissenstat, deputy director of the National Economic Council and deputy assistant to the president for international economic affairs. “Now we don’t see the messages that they are withdrawing from the Paris agreement radically,” Canete said, adding that the countries at Saturday’s meeting agreed not to seek a re-negotiation of the Paris deal.

Thomaston, Ga. — Not so long ago, this rural town an hour outside Atlanta was a hotbed of textile manufacturing. In the late 1990s, there were six major mills here. Their machines spun children’s clothing for Carter’s, made tire cords for B.F. Goodrich and produced bed sheets for J.C. Penney, Sears and Walmart. In all, they employed about 4,000 workers. By 2001, all of those jobs were gone. What has happened here in the 15 years since then tracks the slow comeback of manufacturing in the United States. Two textile companies have come in, investing millions in new technology and adding about 280 jobs in this town where one-third of the residents still live below the poverty line. It is becoming more affordable to produce textiles in the United States as machines become more efficient, companies say.

Major firms are more willing to pay higher prices for domestically sourced products, and rising wages in China mean there is less of an advantage to making products overseas. Last week, there was new cause for celebration when Marriott International announced that all towels in its 3,000 U.S. hotels would be manufactured by Standard Textile in plants here and in Union, S.C., a move expected to bring $23 million worth of business and 150 jobs back to the United States. The hotelier joins a number of other companies, including Walmart, Apple and General Electric, that have pushed for more U.S.-made products in recent years. But manufacturing employment here is a small fraction of what it was. Although a company such as Standard Textile once might have employed close to 1,000 people, today it has a couple of hundred workers who oversee machines that spin, scour and weave cotton.

“We’ve had to redefine who we were because we were a mill town for so long,” said Kyle Fletcher, executive director of the Thomaston-Upton Industrial Development Authority. “We lost a lot of the middle class.” The United States lost 30% of its manufacturing jobs between 1998 and 2016, according to Federal Reserve data. As of February, the country had 12.3 million workers in the sector, down from 17.6 million in April 2008. In February 2010, that figure was 11.5 million. There are hints that manufacturing is returning to the United States in small ways: The nation’s quarterly output has climbed steadily since the end of the recession, growing 35% and adding 650,000 jobs since mid-2009, according to the Fed. But the glory days are gone, Fletcher said. About one-third of Thomaston’s 9,000 residents live below the poverty line, compared with 23% in 1999. Average income has dropped more than 20% since 1999, to $14,243 from $18,193, according to U.S. Census data.

Dreams of lengthy cruises and beach life may be just that, with 20 of the world’s biggest countries facing a pension shortfall worth $78 trillion, Citi said in a report sent on Wednesday. “Social security systems, national pension plans, private sector pensions, and individual retirement accounts are unfunded or underfunded across the globe,” pensions and insurance analysts at the bank said in the report. “Government services, corporate profits, or retirement benefits themselves will have to be reduced to make any part of the system work. This poses an enormous challenge to employers, employees, and policymakers all over the world.” The total value of unfunded or underfunded government pension liabilities for 20 countries belonging to the OECD – a group of largely wealthy countries — is $78 trillion, Citi said. (The countries studied include the U.K., France and Germany, plus several others in western and central Europe, the U.S., Japan, Canada, and Australia.)

The bank added that corporates also failed to consistently meet their pension obligations, with most U.S. and U.K. corporate pensions plans underfunded. Countries with large public pension systems in Europe appear to have the greatest problem. Citi noted that Germany, France, Italy, the U.K., Portugal and Spain had estimated public sector pension liabilities that topped 300% of GDP. Improvements in health care mean retirees need to string out their income for longer. Meanwhile, the increase in the retirement-age population versus the working population is straining government pension schemes. Several countries, including the U.K., France and Italy are gradually hiking retirement ages. Citi recommended that governments explicitly link the retirement age to expected longevity. It also advised that government-funded pensions should serve merely as a “safety net,” rather than the prime pension provider, and that corporate pensions should be “opt out” rather than “opt in” to encourage greater enrollment.

George Osborne’s latest Budget pretended to be many things it wasn’t. The Chancellor talked repeatedly about “borrowing falling”, yet in the next three years, borrowing on our behalf goes sharply up. He warned about “financial instability” and “storm clouds” on the economic horizon, yet he’s relying on growth assumptions that are surely too optimistic. While barely mentioning the EU referendum, the Chancellor’s determination to avoid Brexit pervaded almost every paragraph of his 63-minute Commons statement. Far from being “a Budget for the next generation” – a phrase wielded 18 times – his policies were aimed at attracting as many “Remain” voters as he could, while doing as little as possible to upset those still undecided. Rather than a “long-term Budget” (19 mentions), the package was designed for the next three months, ahead of the EU vote that will decide Osborne’s political future.

What we’ve just seen, then, was possibly the most short-term “long-term budget” in history. Bound to get the chattering classes chuntering (“G&T slimline, anyone?”), Osborne’s flab-fighting “sugar levy” was cynically tactical, broadening his appeal among non-Conservatives, while diverting attention from the statistical sleight of hand at the heart of this Budget. “Borrowing continues to fall,” the Chancellor told us. Really? It’s astonishing that, a full eight years after the financial crisis, and after a surge in growth and employment, the UK is still borrowing more than £72bn a year. Government debt stands at £1,591bn, 50pc up since Osborne took office, more than £50,000 per person in full or part-time employment. The Government is spending £46bn annually on interest payments alone – more than on defence – and that’s with interest rates at historic lows.

As the debt and rates spiral upwards, that interest bill can only rise, all at the expense of spending on services. Instead of cutting borrowing on Wednesday, the Budget fine print shows that, over the next three years, we’ll be adding another £116bn to our national debt – more than £36bn up on the borrowing projections in last November’s Autumn Statement. We’ll probably end up borrowing even more, of course, than these already gargantuan numbers, not least if growth is lower than forecast. Since last November, some £5 trillion has been wiped off global stock markets. Morgan Stanley now warns clients of a 30pc chance of global recession over the next year. Many financiers privately judge the chance of a financial collapse to be far higher. “As one of the most open economies in the world, the UK isn’t immune to global slowdowns and shocks,” Osborne told the Commons. Yet, over each of the next six years, the Budget borrowing projections rest on growth of 2pc or more. While I obviously hope that happens, it amounts to a mighty optimistic assumption.

Well, here’s another nice mess you’ve gotten us into, Janet. U.S. Fed Chair Janet Yellen left rates unchanged this week, and confided after the Fed’s two-day policy meeting that, despite continuing improvement in the U.S. economy, weak global economic growth and turbulent markets had spooked the Fed into halving the number of times it expects to raise rates this year, to two from four. Yellen’s capitulation is already producing a predictable whoop of jubilation in Asian markets, as it confirms this column’s observation that the hot money crowd has succeeded in cry-bullying global central bankers into keeping the punchbowl of cheap cash full to overflowing. Stocks in Shanghai and Hong Kong rose by more than 1%, while Philippine stocks were up almost 2%.

While it’s often the case that Asian stocks move reflexively with those on Wall Street, today it’s all about the U.S. dollar, which fell 1% against the Japanese yen and about 0.7% against the Euro. Even though Tokyo stocks are up, the Fed’s move is bad news for Japan and Europe as well as their respective central bankers, Haruhiko Kuroda and Mario Draghi. As this column explained yesterday, both gentlemen are working furiously to use a negative interest-rate policy to weaken their currencies, boost inflation and revive economic growth. Hearing that Yellen won’t be riding to the rescue soon with another rate hike will come as bad news to them. But it’s excellent news for Asia’s smaller markets, since investors hunting for higher yields can no longer count on getting more bang for the buck out of Yellen.

Indonesia’s rupiah, which has risen 6% already this year, gained another 0.8% after the Fed’s announcement. Malaysia’s ringgit – what corruption scandal? – rose 1% and South Korea’s won soared by 2.5%. Don’t get too excited. While a more reluctant Fed extends the risk-on rally for Asian assets, it does not bode well for investors looking for fundamental value or an upturn in corporate profitability. For starters, the Fed is once again behind the market. Even as they’ve kicked and screamed after the Fed ended a 10-year, zero interest-rate policy by raising rates last December, sending Asian stocks down roughly 15% by mid-February, investors are starting to adjust to the reality that the U.S. economy is not sinking into recession. Jobs and inflation are improving and markets that early this year were predicting no rate hike until 2017 were yesterday betting on another hike as early as July. Yellen has surrendered after achieving victory.

The yuan’s swings are becoming a headache for the Chinese companies that should have been the biggest beneficiaries of last year’s devaluation. In rare overt comments, exporters including Midea and TCL are expressing apprehension about the nation’s exchange-rate policy. Two said the increased volatility has made it difficult to manage costs because customers are choosing to place only short-term orders, while a third said the yuan was allowed to strengthen far too much in the past few years. “Overseas clients are taking into account losses that can be caused by exchange-rate swings and are placing shorter-term orders with smaller volumes, which creates difficulty for our operations,” said Yuan Liqun, VP at Midea, China’s biggest maker of household appliances by market share.

“The fluctuations last year were relatively significant. Companies can accept a market-based yuan that moves within a reasonable range.” Exports slumped 25% in February from a year earlier and a gauge of overseas orders contracted for the 17th month in a row, while the currency’s volatility held near the highest levels since August’s shock devaluation. This illustrates the challenge facing Premier Li Keqiang as he balances the need to nudge the exchange rate lower to help an economy growing at the slowest pace in 25 years, while trying to avoid a run that would create financial instability. The currency, which has plunged 4.8% since last year’s devaluation, climbed in September and October, and dropped in the following three months before rebounding in February. It has strengthened 0.5% in March so far, almost wiping out this year’s losses. The wild swings contributed to an estimated $1 trillion in capital outflows last year.

The yuan, which Royal Bank of Canada says is currently overvalued, will face renewed selling pressure once the Federal Reserve decides to raise borrowing costs again. The median forecast in a Bloomberg survey of economists is for a drop of 4.1% by the end of the year. Its decline against the dollar in 2015 – the most in 21 years – masked a sixth straight annual gain against the exchange rates of China’s main trading partners, according to a BIS index. This shows that there is more room for depreciation, according to Fuyao Glass Industry, which makes automobile windows and whose clients include BMW and Volkswagen. “The yuan is strong, so Chinese companies can’t go abroad and most exporters are making losses,” Cho Tak Wong, chairman of Fuqing, Fujian-based Fuyao, said in an interview over the weekend. “China should allow the yuan to weaken. If the currency doesn’t depreciate, exports will be negatively influenced and export-focused firms will suffer.”

Chinese banks are starting to create a web of risk through their wealth management products (WMPs), raising concerns about the health of the financial system just as China’s economic growth has slowed to its weakest pace in 25 years. Retail investors are the majority of buyers of WMPs, which offer higher interest rates than a bank deposit. But it isn’t always clear what assets the funds are buying to finance those payouts. The industry publishes aggregated data on where WMPs tend to invest, but the disclosures of individual products can be vague. Overall, WMPs tend to invest in the industrial sector as well as industries related to local government and real estate, according to Fitch. All of these are segments of the economy suffering from overcapacity.

Most WMPs – as many as 74% – don’t carry the issuing bank’s guarantee that investors will be made whole at the end of the product’s term, which is usually less than six months, Fitch said. But even if the products fail to meet performance expectations, banks may choose to repay investors anyway to avoid the spectacle of mom and pop protesters in front of its branches – something that occurred outside a Hua Xia Bank branch near Shanghai in 2012, according to a Reuters report. When the WMP’s performance isn’t up to snuff, it can become a risk for more than just the issuing bank. “The fear is that investments are in industries that might not be generating cash so when they come due, the cash to repay investors might not be there.

There’s always pressure to roll them over,” Jack Yuan, associate director for financial institutions at Fitch, said last week. Additionally, some banks are investing in other banks’ WMPs – those investments are usually on banks’ balance sheets in a category called “investments classified as receivables,” Yuan noted. “There are a lot of interlinkages in the banking sector in terms of banks investing in other banks’ WMPs and calling on the interbank market for funding if they do go bad,” he said. “It’s going to be more and more difficult to resolve these if they do go bad.” There were around 23.5 trillion yuan ($3.60 trillion) worth of WMPs outstanding at the end of 2015, up from around 15 trillion yuan a year earlier, Fitch noted, with around 3,500 new ones offered each week.

Peabody Energy, the U.S.’s biggest coal miner, Wednesday posted a going-concern notice in a regulatory filing, warning of possible bankruptcy. A chapter 11 filing by Peabody, which operates 26 mines in the U.S. and Australia, would be the latest in a wave of bankruptcies to hit top American coal producers, including Arch Coal, Alpha Natural Resources, Patriot Coal and Walter Energy, as they wrestle with low energy prices, new regulations, and the conversion of coal-fired power plants to natural gas. Punctuating Peabody’s woes, the Energy Information Administration Wednesday said that 2016 “will be the first year that natural gas-fired generation exceeds coal generation.”

The EIA said Americans would get 33% of their electricity from gas in 2016, and 32% from coal. As recently as 2008, coal fed half of U.S. electricity consumption. The weakening demand is hurting markets. Coal prices have fallen 62% since 2011, and 18% in the past year, according to the EIA. That drop is crushing companies like Peabody. The company has now lost money in nine straight quarters, and in 2015 posted a $2 billion deficit. As of Dec. 31, it had $6.3 billion in debt and $261.3 million in cash. Peabody, whose biggest mining operations are in Wyoming, has also been weighed down by its ill-timed acquisition of Australia’s Macarthur Coal for $5.1 billion in 2011. Prices have been declining ever since. Company shares, which have already lost more than 95% of their value in the past 12 months, fell 44% in midday trading.

Peabody’s share price has fallen to under $2.50 from more than $1,300 in 2008. On Wednesday, Peabody pointed to uncertainty around global coal fundamentals, economic growth concerns of some major coal-importing nations and the potential for additional regulatory requirements on coal producers as reasons for its notice. Because of operating problems and other financial problems, “we may not have sufficient liquidity to sustain operations and to continue as a going concern,” the St. Louis-based miner said in a filing with the SEC. “We may need to voluntarily seek protection under chapter 11 of the U.S. bankruptcy code.” Peabody said it had delayed an interest-rate payment on two loans, triggering a 30-day grace period. If the payments aren’t made within 30 days, an event of default would be declared.

Energy-sector bond defaults – and for some producers, bankruptcy risks – are piling up and coal liabilities aren’t the only culprit. Oil-and-gas producers, suffering with low crude prices after a shale revolution made the U.S. a viable energy producer, are smothered under their own junk bonds. Small- and medium-sized U.S.-based producers, especially those that expanded with the shale boom, are most vulnerable; any small blip in oil prices may not be high enough or fast enough to protect all producers. And just this week at least two more have warned about their near-term future. It’s a climate that’s driven some of this sector’s high-yield paper to trade at 30 cents on the dollar or less.

Peabody Energy said Wednesday it filed a “going concern” notice with regulators. Peabody has opted to exercise the 30-day grace period with respect to a $21.1 million interest payment due March 16 on its 6.50% notes due in September 2020, as well as a $50 million interest payment due March 16 on its 10% senior secured second lien notes due in March 2022. Costs and lost business to tougher coal regulation were cited. But Linn Energy – which on Tuesday filed its own “going concern” after missed interest payments now in a grace period — is primarily an oil-and-gas producer with shale interests in western U.S. states. If it files for bankruptcy protection, its $10 billion in debt would make it the largest U.S. oil company to do so since oil prices began their sharp decline in 2014.

In all, about 40 oil and gas producers have filed for bankruptcy protection globally since 2014, according to a February report from Deloitte. Crude traded to 12-year lows, below $30 a barrel, in February before a recent, mild rebound. Energy consulting firm Rystad Energy says smaller players typically need a minimum $50-a-barrel oil price to make a profit. Last week, Fitch said it’s raising its 2016 forecast for U.S. high-yield bond defaults to 6% from 4.5%, and said it expects energy and materials issuers to default on $70 billion of debt this year, including $40 billion for energy alone. The new rate of default is the highest that Fitch has ever forecast during a non-recessionary period, beating the 5.1% it forecast for 2000.

The check is not in the mail. Bludgeoned by falling energy prices, at least a dozen oil and natural gas companies have opted to cut dividends this year to preserve cash, cannibalizing payouts considered sacrosanct by many investors. The cost to shareholders: more than $7.4 billion in lost income, compared to what they would have received this year if the payouts remained the same. It’s another painful measure – along with tens of thousands of layoffs and more than $100 billion in canceled investments – of the toll taken on the industry by the worst oil and gas price slump in decades. The quarterly payments, prized by conservative shareholders as a source of steady income, are unlikely to be restored any time soon. “It really reinforces the necessity of having a margin of safety if you are buying a stock primarily for its dividend,” said Josh Peters, editor of Morningstar’s DividendInvestor newsletter.

“What we have found for some of the energy companies is that the margin of safety was either slim or nonexistent.” Kinder Morgan’s 75% dividend cut was the biggest, amounting to a $3.44 billion loss for shareholders over the course of 2016. The announcement from North America’s largest pipeline operator “came as a shock to some people and obviously was deplored by some people,” founder and Executive Chairman Richard Kinder told analysts at a Jan. 27 meeting. The move was necessary to help the Houston-based company keep its investment-grade credit rating while ensuring it has enough money to pay debts and grow, Kinder said. Since the Dec. 8 announcement, shares have risen about 20%, compared with a 3% gain for the Alerian MLP stock index, which tracks energy infrastructure companies.

Pemex, Mexico’s state-owned oil giant, cannot seem to get a break these days. It notched up 13 straight quarters of rising losses. It now owes over $80 billion to international investors and banks. It needs to raise $23 billion this year to stay afloat. The cost of servicing that gargantuan debt mountain continues to rise. So it tries desperately to rein in its spending, without tackling — or even discussing — its endemic culture of corruption. In recent days, Pemex received a 15 billion peso ($840 million) lifeline from three of Mexico’s homegrown development banks, Banobras, Bancomext and Nafinsa, to help the firm pay back some of its smallest providers, consisting mainly of domestic SMEs. The loan was part of an arrangement cobbled together between the banks and the Mexican government.

By today’s standards the amount involved is pretty meager, but the operation was about more than just raising funds: it was meant to restore confidence among both investors and suppliers in the firm’s ability to repay its debts. “This sends a sign of stability and confidence to the sector, which has been very nervous” payments would not be made, explained Erik Legorreta, President of the Mexican Oil Industry Association, which represents around 3,000 service providers. “Members of the industry now have the confidence and certainty that the payments will be honored.” Not everyone agrees. Last week the U.S. credit rating agency Moody’s flagged concerns that the loan will significantly increase the three banks’ combined exposure to Pemex’s debt, calculated to grow from 44% to 62%.

“The three lenders now have high concentration risks with their 20 biggest creditors,” cautioned Moody’s, which already downgraded Pemex’s debt in November to Baa1, with a negative outlook. In its report last week, the agency piled on the pressure by warning that there’s “a high likelihood” that it will downgrade Pemex’s rating another notch in the coming weeks. What this all means is that rather than restoring investor confidence in Pemex, the loan operation has merely served to reinforce investors’ fears that lending to the debt-laden oil giant is fast becoming a very dangerous risk.

Munich Re is resorting to the corporate equivalent of stuffing notes under the mattress as the world’s second-biggest reinsurer seeks to avoid paying banks to hold its cash. The German company will store at least €10 million in two currencies so it won’t have to pay for the right to access the money at short notice, Chief Executive Officer Nikolaus von Bomhardsaid at a press conference in Munich on Wednesday. “We will also observe what others are doing to avoid paying negative interest rates,” he said. Institutional investors including insurers, savings banks and pension funds are debating whether to store cash in vaults as overnight deposit rates fall deeper below zero and negative yields dent investment returns. The costs associated with insurance and logistics may outweigh the benefits of taking this step.

Munich Re’s move comes after the ECB last week cut the rate on the deposit facility, which banks use to park excess funds, to minus 0.4%. Munich Re’s strategy, if followed by others, could undermine the ECB’s policy of imposing a sub-zero deposit rate to push down market credit costs and spur lending. Cash hoarding threatens to disrupt the transmission of that policy to the real economy. Munich Re wants to test how practical it would be to store banknotes having already kept some of its gold in vaults, von Bomhard said. This comes at a time when consumers are increasingly using credit cards and electronic banking to pay for transactions. Deutsche Bank CEO John Cryan in January predicted the disappearance of physical cash within a decade. Munich Re also said on Wednesday that it expects its profit to decline this year as falling prices for its products and low interest rates weigh on investment earnings.

The Dutch parliament has voted to ban arms exports to Saudi Arabia in protest against the kingdom’s humanitarian and rights violations. It sees the Netherlands become the first EU country to put in practice a motion by the European Parliament in February urging a bloc-wide Saudi arms embargo. The bill, voted through by Dutch MPs on Tuesday, quoted UN figures which suggest almost 6,000 people – half of them civilians – have been killed since Saudi-led troops entered the conflict in Yemen. It also cited the mass execution of 47 people, largely political dissidents, ordered by the Saudi judiciary on 2 January this year.

According to Reuters, the Dutch bill asks the government to implement a strict weapons embargo that includes dual-use exports which could potentially be used to violate human rights. The vote adds to the growing pressure on Britain, one of the main arms suppliers to Riyadh, to reconsider its stance. According to Campaign Against Arms Trade figures from the start of the year, the UK has sold more than £5.6 billion worth of weapons to the Saudi government under David Cameron. France is the other major European supplier of arms to the Saudi kingdom. Germany’s exports amounted to almost £140 million in the first six months of 2015, while figures for the Netherlands itself were not available.

Austria’s asylum cap to 37,500 refugees has been declared unlawful by the country’s Constitutional Court on Tuesday, March 15. While Chancellor Werner Faymann is calling on Germany to introduce its own cap, the president of Austria’s Constitutional Court, Gerhart Holzinger, stated that Austria is obliged to grand asylum to everyone that meets the legal requirements. Vienna allows 80 asylum seekers per day and allows 3,200 to transit to Germany. Meanwhile, the Austrian Defense Minister, Peter Doskozil, suggested on Tuesday that the EU should help the Former Yugoslav Republic of Macedonia (FYROM) – an EU candidate state – to secure its borders with Greece, an EU member state. Doskozil praised the government in Skopje for the work it has done “for the whole of the EU.” Austria’s Vice-President, Reinhold Mitterlehner, reiterated that “the Balkan route must stay closed.”

How the EU sees this: “We have a week to build a Greek state..” Insane, but true. It smells like the efficiency goal of German camps 70 years ago. If you don’t put people first, you’re going to get it wrong.

On paper the EU’s latest migration plan promises a straightforward solution to a crisis that has vexed European leaders for months. But in practice, it is anything but simple. By returning thousands of migrants to Turkey, Brussels and Berlin are hoping that others will become convinced the route is now impassable and join a formalised system instead. But its implementation poses an enormous administrative test, with little time to prepare. One of the EU’s weakest states, Greece, will be asked to play a central role. “We have a week to build a Greek state,” joked one senior EU official intimately involved with the planning. Frans Timmermans, the European Commission vice-president, acknowledged: “You don’t need to tell me that this is going to be very complicated in legal and logistical terms.” Here are five Herculean tasks ahead:

Preparing the ground — legally and literally Europe’s return plan violates Greek law. To address this, Greece must overhaul its asylum laws in a matter of days to enshrine Turkey as a “safe third country” to receive asylum seekers. The next step is harder: clearing the backlog. There are around 8,000 migrants on Greek islands, such as Lesbos and Chios. Officials say they ideally need to be moved before the so-called “X Day” -as early as Friday- when the returns policy officially begins. Yet Greek facilities are strained. Shelter is lacking on the mainland, where almost 40,000 migrants are already stranded. Mixing the groups — those who are trapped in Greece, awaiting relocation to Europe, and those who will be sent straight back to Turkey – could get ugly.

Creating a functioning asylum system in Greece “Unacceptable”, “degrading” and “unsanitary” were a few of the words used to describe Greece’s asylum system when the European Court of Human Rights banned other EU members from sending asylum seekers there in 2011. Yet the Greek system will now be the fulcrum of the EU’s deal with Turkey. Greece is the place where thousands of asylum seekers will land, be processed, housed and then returned to Turkey. This will require more manpower, particularly on the Aegean Islands. Everyone from judges -estimates range from 50 to 200- to a small army of Arabic or Pashto translators are required. “We’re far away from having the people, let alone trained people,” said one European official involved in preparations.

An asylum seeker’s claim is supposed to take a week to process, according to the EU plan. But the legal hoops are multiplying as Brussels attempts to guard against court challenges. This requires an assessment of each individual case and an interview. Applications must be dealt with fast – but not too fast. (In October, the European Commission criticised Budapest for rejecting applications in under an hour.) Most difficult is the appeals procedure, which must be heard by a judge. If Greece fails to jump through any of these legal hoops then judges in Greece, Luxembourg or Strasbourg could strike down the agreement. “That would bring the whole system to a halt,” said one senior EU official.

Managing unco-operative migrants So-called “hotspots” in Greece were first promised in September, yet these registration and sorting centres are only now taking shape. They can accommodate around 8,050 arrivals, according to the European Commission. Yet their role is about to change drastically. For a returns policy to work efficiently, hotspots must not simply register migrants but detain them. The centres will become containment facilities, according to EU plans, from which migrants who are about to be returned cannot escape. That requires more fences, more overnight shelter and more security guards. This is a horrible challenge. The UNHCR survey of Syrian refugees in February found almost half to be children. Some detainees will be desperate and angry at the prospect of return, having just risked their lives on a sea journey that possibly cost their life savings. The risk of disorder is high.

The EU is preparing to scale back the number of Syrian refugees offered resettlement in Europe, as part of a controversial pact being drawn up with Turkey. The bloc’s 28 leaders will hold a summit in Brussels on Thursday, before a meeting the Turkish prime minister, Ahmet Davutoglu on Friday, to hammer out the final details of a plan aimed at stemming the flow of refugees and migrants coming to Europe. The EU has pledged to resettle Syrian refugees currently in Turkey, but figures that emerged on Wednesday suggested only 72,000 places would be available, with uncertainty about the bloc’s commitment beyond this number. As the UNHCR stepped up calls for a coordinated approach to manage the number of people, European diplomats were scrambling to finalise a deal with Turkey.

Under a proposed “one-for-one” scheme, for every Syrian refugee in Turkey who is resettled in Europe, a Syrian in Greece would be sent back across the Aegean. The vast majority of refugees and migrants in Greece can also expect to be sent back to Turkey. When these broad principles were agreed at an EU-Turkey summit 10 days ago, the numbers were vague but details are now emerging. Of the 72,000 places identified by the Commission for Syrian refugees, 18,000 places would be available under a voluntary resettlement scheme agreed last year. A further 54,000 places may be available “if needed” under a separate scheme designed to spread asylum seekers more evenly around the bloc, although this would require a change to EU law.

Frans Timmermans, vice-president of the European commission, said the EU would continue to help after these places were used up. It pointed to “a coalition of the willing”, made up of EU member states including Germany and Austria, who have pledged to resettle Syrians once irregular arrivals had stopped. “When we succeed in breaking the pattern of irregular arrivals one-for-one will not become none-for-none,” Timmermans said. But the various EU schemes to rehouse refugees are painfully slow. A plan to find homes for 160,000 refugees has led to only 937 being resettled, according to the latest data. Several countries are concerned that the Turkey deal could mean large-scale resettlement of Syrians in Europe.

A senior EU official said there “cannot be an open-ended commitment on the EU side”. The numbers discussed indicate that the EU wants to scale back help in Europe offered to refugees. Syrians in Greece will go to the back of the queue for resettlement in Europe once they are returned to Turkey. “Priority will be given to Syrians who have not previously entered the EU irregularly,” states an unpublished draft. The commission argues the plan will kill the business model of people smugglers, as potential migrants will have no incentive to come to Europe if they think they will be turned away. But the UN’s human rights chief has warned that the EU risks compromising its human rights values if it cuts corners on asylum standards.

More than 2,400 migrants and three corpses have been recovered from people smugglers’ boats off Libya since Tuesday, Italy’s coastguard said Wednesday. After several quiet weeks, the figures represent a pick-up in the flow of migrants attempting to reach Italy via Libya, a route through which around 330,000 people have made it to Europe since the start of 2014. Prior to the latest rescues, the UN refugee agency (UNHCR) had reported 9,500 people landing at Italian ports since the start of the year. This compares with more than 143,000 who have reached Greek islands by crossing the Aegean Sea since January 1.

With efforts underway to close the entry route through Greece, Italian authorities are wary of a surge in the number of migrants attempting to come through Libya. So far there has been no indication of that happening. Numbers arriving from Libya have always fluctuated in line with weather conditions in the Mediterranean and other factors. Arrivals were slightly down in 2015 compared with 2014 – a trend that may be related to the political chaos in Libya which might have deterred some migrants and has made it harder for those that do make the journey to find work there while awaiting boats to Italy.

The danger lurking in the risk asset markets was succinctly captured by MarketWatch’s post on overnight action in Asia. The latter proved once again that the casino gamblers are incapable of recognizing the on-rushing train of global recession because they have become addicted to “stimulus” as a way of life:

Shares in Hong Kong led a rally across most of Asia Tuesday, on expectations for more stimulus from Chinese authorities, specifically in the property sector…….The gains follow fresh readings on China’s economy, which showed further signs of slowdown in manufacturing data released Tuesday (which) remains plagued by overcapacity, falling prices and weak demand. The dimming view casts doubt that the world’s second-largest economy can achieve its target growth of around 7% for the year. The central bank has cut interest rates six times since last November.

More stimulus from China? Now that’s a true absurdity – not because the desperate suzerains of red capitalism in Beijing won’t try it, but because it can’t possibly enhance the earnings capacity of either Chinese companies or the international equities. In fact, it is plain as day that China has reached “peak debt”. Additional borrowing there will not only prolong the Ponzi and thereby exacerbate the eventual crash, but won’t even do much in the short-run to brake the current downward economic spiral. That’s because China is so saturated with debt that still lower interest rates or further reduction of bank reserve requirements would amount to pushing on an exceedingly limp credit string. To wit, at the time of the 2008 crisis, China’s “official” GDP was about $5 trillion and its total public and private credit market debt was roughly $8 trillion.

Since then, debt has soared to $30 trillion while GDP has purportedly doubled. But that’s only when you count the massive outlays for white elephants and malinvestments which get counted as fixed asset spending. So at a minimum, China has borrowed $4.50 for every new dollar of reported GDP, and far more than that when it comes to the production of sustainable wealth. Indeed, everything is so massively overbuilt in China – from unused airports to empty malls and luxury apartments to redundant coal mines, steel plants, cement kilns, auto plants, solar farms and much, much more – that more borrowing and construction is not only absolutely pointless; it is positively destructive because it will result in an even more destructive adjustment cycle. That is, it will only add to the immense already existing downward pressure on prices, rents and profits in China, thereby insuring that even more trillions of bad debts will eventually implode.

[..] When peak debt is reached, additional credit never leaves the financial system; it just finances the final blow-off phase of leveraged speculation in the secondary markets.

Manufacturing in the U.S. unexpectedly contracted in November at the fastest pace since the last recession as elevated inventories led to cutbacks in orders and production. The Institute for Supply Management’s index dropped to 48.6, the lowest level since June 2009, from 50.1 in October, its report showed Tuesday. The November figure was weaker than the most pessimistic forecast in a Bloomberg survey. Readings less than 50 indicate contraction. The report showed factories believed their customers continued to have too many goods on hand, indicating it will take time for orders and production to stabilize.

Manufacturers, which account for almost 12% of the economy, are also battling weak global demand, an appreciating dollar and less capital spending in the energy sector. “There are some clear signs of weakness — industries that are tied to oil and gas, agriculture or are heavily dependent on exports are all clearly slowing,” Mark Vitner at Wells Fargo Securities said before the report. “It wouldn’t surprise me if the manufacturing numbers remain soft for the next five to six months.”

It’s seven years after the financial crisis and the banking industry is still in receipt of state support – support that will be available for two more years, and perhaps for longer. The Treasury and the Bank of England have decided to extend their Funding for Lending Scheme (FLS), which supplies banks with cheap money with the aim of keeping the supply of credit flowing. What ought, in theory, to be the scheme’s final outing will be very specifically targeted at lending to small and medium-sized enterprises (SMEs). This is a sector which is still struggling to obtain the funding it needs at a time when lending to other sectors has largely recovered. The Bank says that things are improving, and its figures bear that out. But not quickly, and the growth in small business lending pales by comparison to the growth in consumer lending.

The expansion of the latter is starting to cause concern, with the Bank’s chief economist, Andy Haldane, fretting about personal loans. He says they’re picking up at a rate of knots. Britain has long nursed an addiction to the drug of debt that it’s never really addressed and the growth in unsecured lending is an indication of a return to bad habits. Given that Mr Haldane and his colleagues are engaged in the unenviable task of walking an economic tightrope, it’s no wonder that he’s getting twitchy. But consumers are not, as yet, shooting up with the sort of wild abandon they exhibited in the run-up to the crisis. And, as Investec’s Philip Shaw points out, it wasn’t so long ago that we were still talking about the need to make more credit available.

Workers in the UK will have the worst pensions of any major economy and the oldest official retirement age of any country, according tothe Organisation for Economic Co-operation and Development. The typical British worker can look forward to a pension worth only 40% of their pay , once state and private pensions are combined. The Paris-based thinktank said on Tuesday that this compares with about 90% in the Netherlands and Austria and 80% in Spain and Italy. Only Mexico and Chile offer their workers a worse prospect after retirement, although Turkey is the surprise table-topper, giving its retirees an average pension equal to 105% of average wages, according to the OECD report. Britain has begun an auto-enrolment scheme that will offer millions of low-paid workers a private pension for the first time.

But with contribution rates low, the payouts will not be generous. Last week the chancellor, George Osborne, gave employers a six-month delay to planned increases in their contribution rates. Pensions expert Tom McPhail of Hargreaves Lansdown said: “This analysis makes embarrassing reading for the politicians who have been responsible for the UK’s pensions over the past 25 years. “The state pension was in steady decline for years. Even though it is improving for lower earners now, average payouts will not be rising. It is in the private sector though where the real damage has been done; the collapse in final salary pensions has not yet been replaced with well-funded alternatives.” The age at which workers qualify for a state pension in the UK will, at 68 years old, be the highest of any country in the world, equalled only by Ireland and Czech Republic.

The prize for earliest retirees goes to France and Belgium. “Workers stay the longest in the labour market in Korea, Mexico, Iceland and Japan; men exit the soonest in France and Belgium while women leave the earliest in the Slovak Republic, Slovenia and Poland,” said the OECD. While many European countries offer significantly better pensions than in Britain, the cost is now close to sustainable, said the OECD. In recent years there have been frequent warnings about the “demographic timebomb” that will wreck the finances of ageing European nations. But the OECD said that changes to taxation, contribution rates and pensionable ages means that the burden of paying pensions will rise from the current level of 9% of GDP to just 10.1% by 2050.

Standard and Poor’s cut Volkswagen’s credit rating to “BBB+” from “A-” on Tuesday, shortly after the automaker reported that an emissions-cheating scandal took a serious bite out of its U.S. sales last month. The German automaker said that November U.S. sales fell almost 25% from a year ago. The company blamed the decline on stop-sale orders for diesel-powered vehicles that the government says cheated on pollution tests. The VW brand sold just under 24,000 vehicles last month compared with almost 32,000 a year ago.

S&P noted the emissions scandal also contributed to its ratings cut. The agency said it expects Volkswagen to “experience ongoing adverse credit impacts.” The U.S. is a relatively small market for Volkswagen. The VW brand sold 490,000 vehicles worldwide in October, 5% below a year ago. VW has admitted that 482,000 2-liter diesel vehicles in the U.S. contained software that turned pollution controls on for government tests and off for real-world driving. The government says another 85,000 six-cylinder diesels also had cheating software.

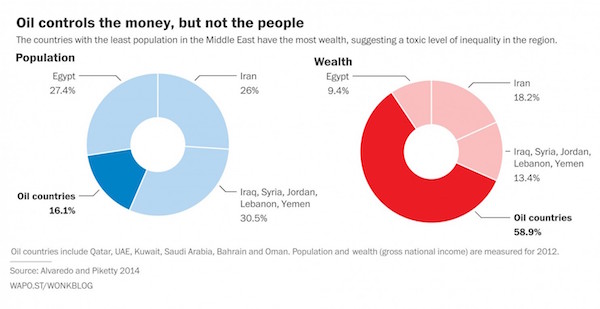

Thomas Piketty is out with a new argument about income inequality. It may prove more controversial than his book, which continues to generate debate in political and economic circles. The new argument, which Piketty spelled out recently in the French newspaper Le Monde, is this: Inequality is a major driver of Middle Eastern terrorism, including the Islamic State attacks on Paris earlier this month — and Western nations have themselves largely to blame for that inequality. Piketty writes that the Middle East’s political and social system has been made fragile by the high concentration of oil wealth into a few countries with relatively little population.

If you look at the region between Egypt and Iran — which includes Syria — you find several oil monarchies controlling between 60 and 70% of wealth, while housing just a bit more than 10% of the 300 million people living in that area. (Piketty does not specify which countries he’s talking about, but judging from a study he co-authored last year on Middle East inequality, it appears he means Qatar, the United Arab Emirates, Kuwait, Saudia Arabia, Bahrain and Oman. By his numbers, they accounted for 16% of the region’s population in 2012 and almost 60% of its gross domestic product.) This concentration of so much wealth in countries with so small a share of the population, he says, makes the region “the most unequal on the planet.”

Within those monarchies, he continues, a small slice of people controls most of the wealth, while a large — including women and refugees — are kept in a state of “semi-slavery.” Those economic conditions, he says, have become justifications for jihadists, along with the casualties of a series of wars in the region perpetuated by Western powers. His list starts with the first Gulf War, which he says resulted in allied forces returning oil “to the emirs.” Though he does not spend much space connecting those ideas, the clear implication is that economic deprivation and the horrors of wars that benefited only a select few of the region’s residents have, mixed together, become what he calls a “powder keg” for terrorism across the region.

Piketty is particularly scathing when he blames the inequality of the region, and the persistence of oil monarchies that perpetuate it, on the West: “These are the regimes that are militarily and politically supported by Western powers, all too happy to get some crumbs to fund their [soccer] clubs or sell some weapons. No wonder our lessons in social justice and democracy find little welcome among Middle Eastern youth.” Terrorism that is rooted in inequality, Piketty continues, is best combated economically.

All totlly legal, no doubt. “..an emerald and diamond jewellery set containing a ring, earrings, bracelet, and necklace, which was valued at $780,000 [was given to] Teresa Heinz Kerry, wife of US Secretary of State John Kerry.

Three quarters of the value of all official gifts given to the US administration in 2014 came from Saudi Arabia, according to US government records. US President Barack Obama, First Lady Michelle Obama, their daughters and US federal government employees received official gifts estimated to be worth a total of $3,417,559 last year. Analysis of the annual disclosure, released by the US Department of State’s Office of the Chief of Protocol, found Saudi Arabia gave the US gifts valued at around $2,566,525. It dominated the report and represented 75% of the value of all gifts received by Obama and his government employees last year.

When all other Arab countries are added to the mix the total value rises to nearly $3 million, with the Arab region accounting for 87% of the value of all gifts. The most lavish gift was an emerald and diamond jewellery set containing a ring, earrings, bracelet, and necklace, which was valued at $780,000. It was not given to Obama, his wife Michelle or his children, but Teresa Heinz Kerry, wife of US Secretary of State John Kerry. The jewels were given to Mrs Kerry in January 2014 by the late King Abdullah bin Abdulaziz Al-Saud. First Lady Michelle Obama is included in the top five with two gifts of jewels from Saudi Arabia, each worth well over half a million dollars.

The president himself is further down the list, behind his children and wife, and ranked 7th with a white gold men’s watch worth $67,000. The six other Gulf states also gave lavish gifts to the Obama administration. Qatar gave Eric Holder, US Attorney General, a $24,150 gold and silver ship depicting United States and the State of Qatar flags in a case, in addition to an engraved Cartier bracelet. The UAE also gifted a gold necklace and earring set with white stones worth around $3,200 to Deborah K. Jones, Ambassador of the US to the State of Libya. The gift was presented in March 2014 on behalf of Sheikh Khalifa bin Zayed Al Nahyan, President of the UAE.

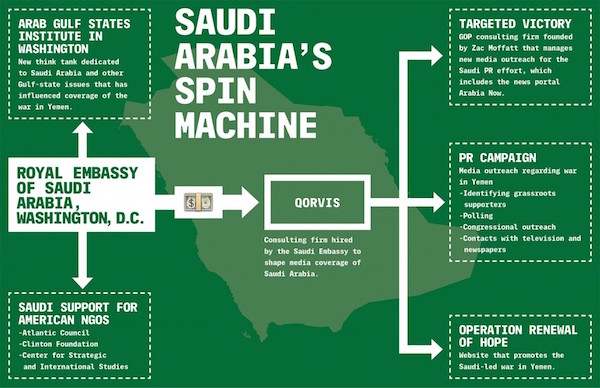

Soon after launching a brutal air and ground assault in Yemen, the Kingdom of Saudi Arabia began devoting significant resources to a sophisticated public relations blitz in Washington, D.C. The PR campaign is designed to maintain close ties with the U.S. even as the Saudi-led military incursion into the poorest Arab nation in the Middle East has killed nearly 6,000 people, almost half of them civilians. Elements of the charm offensive include the launch of a pro-Saudi Arabia media portal operated by high-profile Republican campaign consultants; a special English-language website devoted to putting a positive spin on the latest developments in the Yemen war; glitzy dinners with American political and business elites; and a non-stop push to sway reporters and policymakers. That has been accompanied by a spending spree on American lobbyists with ties to the Washington establishment.

The Saudi Arabian Embassy, as we’ve reported, now retains the brother of Hillary Clinton’s campaign chairman, the leader of one of the largest Republican Super PACs in the country, and a law firm with deep ties to the Obama administration. One of Jeb Bush’s top fundraisers, Ignacio Sanchez, is also lobbying for the Saudi Kingdom. Saudi Arabia’s relationship with the U.S. has come under particular strain in recent years as the government has not only launched the brutal war in Yemen, but has embarked on a wave of repression. Following the appointment of Salman bin Abdulaziz Al-Saud to the Saudi throne in January, the Kingdom sharply increased the number of people executed — often by beheading and crucifixion — for daring to protest or criticize the government or for crimes as minor as adultery or “witchcraft.” On November 17, a Saudi court sentenced Ashraf Fayadh, a famed poet, to death for “apostasy.”

There have also been reports that Saudi Arabia continues to be a leading driver of Sunni terror networks worldwide, including in Syria and Iraq. The Saudi Arabian government is currently supplying weapons to a Syrian rebel coalition that includes the Nusra Front, al Qaeda’s affiliate in the region. As the New York Times has reported, private donors in Saudi Arabia have also worked as fundraisers for the Islamic State, or ISIS. And there is a renewed, bipartisan push by lawmakers to declassify the 28 pages of the 9/11 Commission Report, a censored section that reportedly relates to Saudi state support for al Qaeda’s operation.

Pope Francis, galvanized by a scandal over Vatican finances, has ordered the most powerful bodies in the city-state to launch an unprecedented audit of its wealth and crack down on runaway spending. At the suggestion of his economic chief, Cardinal George Pell, Francis has set up a “Working-Party for the Economic Future” which brings together the Secretariat of State, or prime minister’s office, the Vatican Bank and other agencies. Francis has told the panel “to address the financial challenges and identify how more resources can be devoted to the many good works of the Church, especially supporting the poor and vulnerable,” Danny Casey, director of Pell’s office at the Secretariat for the Economy, said in an interview.

The pope’s initiatives come as five people stand trial in the Vatican over the leak of confidential documents in two books published last month that described corruption, mismanagement and wasteful spending by church officials. Those on trial deny wrongdoing. Francis, 78, has pushed for more openness and transparency in Vatican financial and economic agencies but he has faced resistance from the Rome bureaucracy. On the flight back to Rome on Monday after a visit to Africa, Francis told reporters that the so-called Vatileaks II scandal was an indication of the mess that he’s trying to sort out.

The trial of two former Vatican employees alongside the books’ authors highlighted Church efforts “to seek out corruption, the things which aren’t right,” he said, according to a transcript provided by the Vatican. The working group, which held its first meeting last week, will study measures to cut costs and raise revenue as part of a long-term financial plan. “This will include comparing actual expenditure against budgets at a consolidated level, which is a new initiative,” Casey said.

The IMF’s decision to add China’s yuan to its reserves basket is a triumph for Beijing, but the fund’s verdict that the currency met its “freely usable” test will have little financial impact unless Beijing recruits more users. The desire of Chinese reformers to internationalize the currency has a clear economic rationale; a yuan in wide circulation overseas would reduce China’s dependence on the dollar system and on policy set in Washington. It would also make it easier for Chinese firms to invoice and borrow offshore in yuan, reducing the risk of exchange rate fluctuations and prompting China’s inefficient state-owned banks to improve their performance or lose business. Those concerned about a potential global liquidity crisis caused by overdependence on the United States might also welcome the yuan as an alternative to the dollar, as would countries locked out of dollar capital markets by sanctions.

But to serve these purposes, there needs to be a much bigger pool of yuan outside China, which requires offshore institutions – and not just in Hong Kong – to buy and hold yuan. Few believe the IMF decision alone, which economist Alicia Garcia-Herrero called a “beauty contest”, will change investor behavior much. For that, says Swiss bank UBS, Beijing needs to continue financial reforms and capital account liberalization to improve the efficiency of capital allocation in China. Foreign investors want Beijing to provide predictable and transparent legal and taxation treatment, and drop its penchant for pilot programs and quotas in favor of consistency. They also want to know they can freely sell their yuan assets, not just buy, a concern that only grew over the summer, when Beijing stepped into its stock markets to stop a sell-off.

Foreign investors aren’t making full use of the existing channels to buy Chinese assets that Beijing allows – quotas for the two Qualified Foreign Institutional Investor programs (QFII and RQFII) and the Shanghai-Hong Kong Stock Connect have yet to be used up. And for all the impressive trade statistics, much of the “offshore” yuan isn’t traveling the globe but bouncing to and fro across the internal border with Hong Kong, largely traded between Chinese companies. “The number one thing we would like to see changed is that the QFII and RQFII quotas are dropped, just as they dropped in July the quotas for central banks, sovereign wealth funds and supernationals. It’ll make it a lot easier for global institutional investors,” said Hayden Briscoe at AllianceBernstein in Hong Kong.

“Over the past several decades, the U.S. dollar has been the main reserve currency, and the U.S. has experienced huge capital inflows, especially from countries such as China.”

Why would China want the IMF to put the yuan in the SDR? It may want to engineer a bump in capital inflows, at a time when money is trying to leave China. Generating some foreign demand for yuan-denominated assets might help stabilize the Chinese currency, which is expected to depreciate a bit in the months ahead. The IMF might be motivated to help China limit the moves in its currency in order to promote global macroeconomic stability, or it might want to lure China into making sovereign loans through the fund instead of on its own. Ultimately, the yuan’s status as a reserve currency will be driven by China’s further liberalization of its capital account. The easier it becomes to move money in and out of yuan, the more asset managers will be willing to put their money in.

And if China ascends to true reserve currency status, the most important effects will be in the long term – not all of them good. True reserve currency status makes it cheaper for a government to borrow, which means that – all else equal – more borrowing will happen. That will increase net capital inflows. And as many countries have learned during the last decade, capital inflows can cause trouble. That doesn’t make a lot of sense, intuitively. How could it harm a country to allow it to borrow cheaply? If countries were rational and foresighted, they would borrow no more than is healthy. But sovereign borrowing decisions are the result of government decisions not market ones, and no one would argue that governments always make wise choices. Even the private sector, though, could be harmed by capital inflows.

As economists Gianluca Benigno, Nathan Converse, and Luca Fornaro have found, large influxes of foreign money can lead to booms and busts. They can also cause a country to shift resources out of manufacturing, where productivity growth is often high, into service-oriented industries where productivity is relatively stagnant. Over the past several decades, the U.S. dollar has been the main reserve currency, and the U.S. has experienced huge capital inflows, especially from countries such as China. Those capital inflows in turn have caused a large, persistent trade deficit. Perhaps not coincidentally, U.S. manufacturing hasn’t grown very fast since the late 1990s. In the year ahead, reserve-currency status might help cushion the country’s economic slowdown. But in the long term, it might be a poisoned chalice for China.

The indefatigable Mr. Keen presents lecture no. 8 in the series. The ‘logic’ of a government aiming for a budget surplus is that the people must run a deficit.

The EU is warning Greece it faces suspension from the Schengen passport-free travel zone unless it overhauls its response to the migration crisis by mid-December, as frustration mounts over Athens’ reluctance to accept outside support. Several European ministers and senior EU officials see the threat of pushing out Greece over “serious deficiencies” in border control as the only way left to persuade Alexis Tsipras, Greece’s prime minister, to deliver on his promises and take up EU offers of help. If the EU follows through on its threat, it would mark the first time a country has been suspended from Schengen since its establishment in 1985. The challenge to Athens comes amid a bigger rethink on tightening joint border control to ensure the survival of the Schengen zone.

The European Commission will this month propose a joint border force empowered to take charge of borders, potentially even against the will of frontline states such as Greece. Greece’s relatively weak administration has been overwhelmed by more than 700,000 migrants crossing its frontiers this year. Given the severity of the crisis, EU officials are vexed by Athens’s refusal to call in a special mission from Frontex, the EU border agency; its unwillingness to accept EU humanitarian aid; and its failure to revamp its system for registering refugees. EU home affairs ministers, who meet on Friday, are to make clear that more drastic measures will be considered if Greece fails to take action before a summit of EU leaders in mid-December, according to four senior European diplomats.