JMW Turner Vignette Study of a Ship in a Storm c.1830

Nicole sent me this video, which I know next to nothing about. I don’t know where it was filmed, or when, or why, nada. But, apart from the fact that listening to Nicole is always interesting, and I haven’t heard her talk nearly enough recently, because we live on opposite ends of the world these days, this is interesting because it relates directly to energy issues that have lately been a recurring theme at the Automatic Earth.

That is, once the net energy we gain from our energy sources falls by enough, our complex systems become untenable. This is not an easy-to-grasp thing for many, but it’s nevertheless true. The energy return on energy invested (EROEI) on the vast majority of our present energy sources is already dangerously close to the point where we will have to make our lives, and our societies, simpler.

We can discuss whether that’s such a bad thing, but it doesn’t really matter. We can’t beat thermodynamics. The initial reactions to this will in all likelihood by very dramatic, and in cases violent, since many individuals will try to escape having to adapt, and since individuals, societies, nations will realize that energy provides political -and military- power. Trust is a delicate topic.

There can be no doubt that in the immediate future we will attempt to build even more complex systems and societies, just to solve the problems caused by complexity, only to find out later that these systems are all built around centers that cannot hold. And we can all imagine what this will mean for our economies.

Theodor Horydczak “Dome of US Capitol through trees at night” 1943

For the second time in a few weeks (see ‘End of Growth’ Sparks Wide Discontent), former British diplomat Alastair Crooke quotes me extensively, and I gladly return the favor. Crooke here attempts to list -some of- the difficulties Donald Trump will face in executing the -economic- measures he promised to take in his campaign. Crooke argues that, as I’ve indicated repeatedly, for instance in America is The Poisoned Chalice, the financial crisis that never ended may be one of his biggest problems.

Here, again, is Alastair Crooke:

We are plainly at a pivotal moment. President-Elect Trump wants to make dramatic changes in his nation’s course. His battle cry of wanting to make “America Great Again” evokes – and almost certainly is intended to evoke – the epic American economic expansions of the Nineteenth and Twentieth centuries.

Trump wants to reverse the off-shoring of American jobs; he wants to revive America’s manufacturing base; he wants to recast the terms of international trade; he wants growth; and he wants jobs in the U.S. – and he wants to turn America’s foreign policy around 180 degrees.

The run-down PIX Theatre sign reads “Vote Trump” on Main Street in Sleepy Eye, Minnesota. July 15, 2016. (Photo by Tony Webster Flickr)

It is an agenda that is, as it were, quite laudable. Many Americans want just this, and the transition in which we are presently in – dictated by the global elusiveness and search for growth (whatever is meant now by this term “growth”), clearly requires a different economic approach from that followed in recent decades.

As Raúl Ilargi Meijer has perceptively posited, greater self-reliance “is the future of the world, ‘post-growth’, and post-globalization. Every country, and every society, needs to focus on self-reliance, not as some idealistic luxury choice, but as a necessity. And that is not as bad or terrible as people would have you believe, and it’s not the end of the world … It is not an idealistic transition towards self-sufficiency, it’s simply and inevitably what’s left, once unfettered growth hits the skids. …

“Our entire world views and ‘philosophies’ are based on ever more and ever bigger and then some, and our entire economies are built upon it. That has already made us ignore the decline of our real markets for many years now. We focus on data about stock markets and the like, and ignore the demise of our respective heartlands, and flyover countries …

“Donald Trump looks very much like the ideal fit for this transition … What matters [here] is that he promises to bring back jobs to America, and that’s what the country needs … Not so they can then export their products, but to consume them at home, and sell them in the domestic market …There’s nothing wrong or negative with an American buying products made in America instead of in China.

“There’s nothing economically – let alone morally – wrong with people producing what they and their families and close neighbours themselves want, and need, without hauling it halfway around the world for a meagre profit. At least not for the man in the street. It’s not a threat to our ‘open societies’, as many claim. That openness does not depend on having things shipped to your stores over 1000s of miles, that you could have made yourselves, at a potentially huge benefit to your local economy. An ‘open society’ is a state of mind, be it collective or personal. It’s not something that’s for sale.”

A Great Wish

That’s Trump’s ostensible great wish, (it seems). It is not an unworthy one, but things have changed: America is no longer what it was in the Nineteenth or Twentieth centuries, neither in terms of untapped natural resources, nor societally. And nor is the rest of the world the same either.

Mr. Trump rather unfortunately may find that his chief task will not be the management of this Great Re-orientation, but more prosaically, fending off the headwinds which he will face as he hauls on the tiller of the economy.

In short, there is a real prospect that his ambitious economic “remake” may well be prematurely punctured by financial crisis.

These headwinds will not be of his making, and for the main part, they lie beyond human agency per se. They are structural, and they are multiple. They represent the accumulation of an earlier monetary doctrine which will fetter the President-elect into a small corner from which any chosen exit will carry adverse implications.

Ditto for anyone else trying to steer any ship of state in this contemporary global economy. Paradoxically – in an era moving toward greater self-sufficiency – what success Trump may have, however, will likely depend not on self-reliance so much as he would like.

For his foreign policy about turn, he will depend on finding common interest with Russian President Vladimir Putin (that should not be too hard) – and for the economic “about turn” – on Trump’s ability not to confront China, but to come to some modus vivendi with President Xi (less easy).

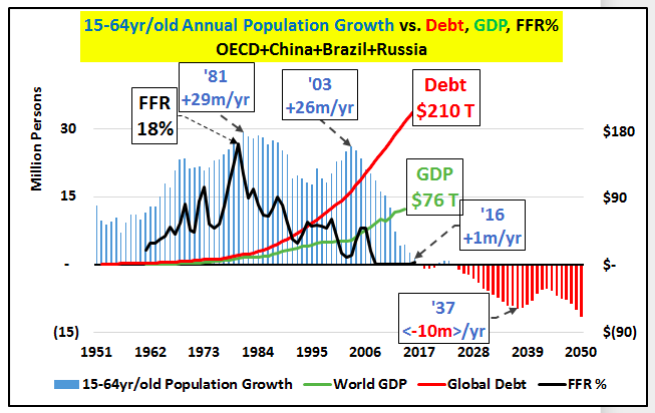

“Things are not what they were.” Complexity “theory” tells us that trying to repeat what worked earlier – in very different conditions – will likely not work if repeated later. In the Clinton era, for example, 85 percent of the U.S. population growth derived from the working-age population. The headwind that Trump will face is that, over the next eight years, 80 percent of the population growth will comprise 65+ year olds. And 65+ year olds are not a good engine of economic growth. This is not an uniquely American problem; it is a global trend too.

“The peak growth” (according to Econimica blog), “in the annual combined working age population (15-64 year/olds) among all the 35 wealthy OECD nations, China, Brazil, and Russia has collapsed since its 1981 peak. The annual growth in the working age population among these nations has fallen from +29 million a year to just +1 million in 2016 … but from here on, the working age population will be declining every year … These nations make up almost three quarters of all global demand for oil and exports in general. But their combined working age populations will shrink every year, from here on (surely for decades and perhaps far longer). Global demand for nearly everything is set to suffer.”

(FFR stands for Federal Funds Rate: i.e. the US key interest rate) Source: https://econimica.blogspot.it/2016/11/trump-lies-no-different-than-obama-or.html

And then there is China: It too is passing through a difficult “transition” from the old economy to an “innovative” one. It too, has an aging population and a debt problem (with a debt-to-gross domestic ratio reaching 247 percent). Trump argues that China deliberately holds down the value of its currency to gain unfair trade advantage, and he further suggests that he intends to confront the Chinese government on this key issue.

Again, Trump does have a point (many nations are managing their exchange rates precisely in order to try to “steal” a little bit extra growth from the diminished global pot). But as noted at Zerohedge, citing the analysis of One River Asset Management executive Eric Peters:

“What’s good for the US in this case [the rising dollar and interest rates in anticipation of ‘Trumponomics’], is not good for emerging markets (EMs). Emerging markets benefit from a weaker dollar, and you’re not going to get that. Emerging markets benefit from global capital flows moving in their direction and that’s not happening either. Back in February, emerging markets were in sharp decline, driven by (1) a strong dollar, (2) rising US interest rates, and (3) slowing Chinese growth. Then China spurred a massive credit stimulus, the Fed became wildly dovish, and the dollar declined sharply.

“Interest rates collapsed throughout the year. As the growing pool of dollar, euro and yen liquidity searched for a decent return, it headed to emerging markets. Trump has reignited the dollar rally, and his fiscal stimulus will force interest rates higher. This reversed everything. [the dollars are heading home]

“And to be sure, the Beijing boys don’t want to see material weakness ahead of next autumn’s Party Congress. But we’re currently near peak impulse from China’s Q1 stimulus.”

In short, Peters is saying that, with the appreciating dollar and rising interest rate environment, growth from emerging markets as a whole will falter, since emerging markets have effectively leveraged their economies to Chinese growth. It used to be the case that they were closely tied to U.S. growth, but it is now China which dominates the EMs’ trade flows [i.e. without China growth, the EMs languish]. The question is, can America reboot its growth whilst China and the EMs languish? It is another structural shift, whereas heretofore, it was vice versa: without U.S. growth, the EMs and China languished. Now it is the converse.

Hollowed-Out Economies

There are other structural changes of course which will make it harder for the industrially hollowed-out economies of the West to recuperate jobs off-shored earlier. Firstly, there has been a systemic shift of innovation and technology eastwards (often to a more skilled and better-educated workforce). This represents not only an economic event, but a redistribution of power too. In any case, technology in this new era is being more job destructive than creative.

In one sense, Trump’s economic plan to “get America working again” through massive debt-financed, infrastructure projects, harks back to the Reagan era, which was also a period in which the dollar was strong. But yet again, “things today are not what they were then.” Inflation then was at 13 percent, Interest rates were around 20 percent, and crucially, the U.S. debt to GDP ratio was a mere 35 percent (compared to today’s estimate of 71.8 percent or 104.5 percent with external debt included).

Then, as Jim Rickards has suggested, the strong dollar was deflationary (deliberately so), and interest rates had nowhere to go, but down. It was the beginning of the three decades’ bond boom, which finally seems to have come to an end, coincident with Trump’s election. Today, inflation has nowhere to go but up – as have interest rates – and the bond market, nowhere to go, but (perilously) down.

Growth and Jobs?

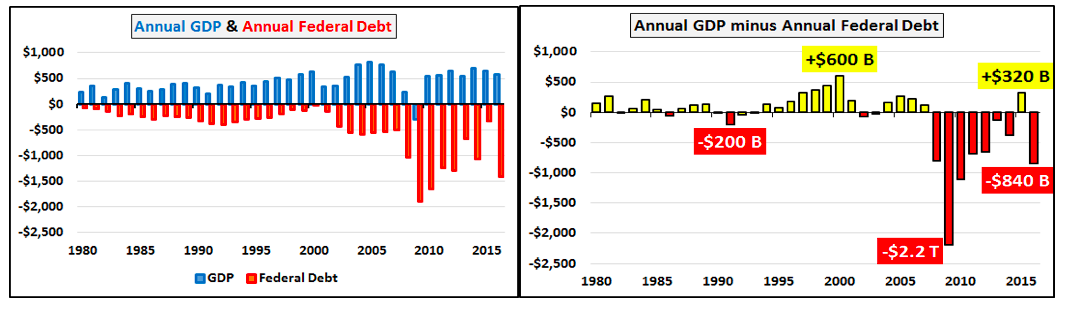

Can Trump then achieve growth and jobs through infrastructure expenditure? Well, “growth” is an ambiguous, shape-shifting term. The first chart shows both sides of the equation … the annual GDP growth and the annual federal debt incurred, spent, and (thus counted as part of the growth) to achieve the purported growth.

The second chart shows the annual GDP minus the annual growth in federal debt to achieve that “GDP growth.” In other words, unlike in the earlier Reagan times, more recently, the debt is producing no growth – but … well … just more debt, mostly.

In fact, what the second chart is reflecting is the dilution – through money “printing” – of purchasing power: away from one entity (the American consumer), through the intermediation of the financial sector, to other entities (mostly financial entities, and to corporations buying back their own shares). This is debt deflation: the American consumer ends having less and less purchasing power (in the sense of residual discretionary income).

The point here is that “growth” is becoming rarer everywhere. Russia and China, like everyone else, are in search for new sources for growth.

As Rickards has said, debt is the “devil” that can undo Trump’s whole schema: a “$1 trillion infrastructure refurbishment plan, along with his proposal to rebuild the military, will — at least in the short-term — significantly increase annual deficits. In fact, deficits are already soaring; the fiscal 2016 budget hole jumped to $587 billion, up from $438 in the prior year, for a huge 34% increase…in addition to this, Trump’s protectionist trade policies would implement either a 35% tariff on certain imports or would require these goods to be produced inside the United States, at much higher prices. For example, the increase in labor costs from goods made in China would be 190% when compared to the federally mandated minimum wage earner in the United States. Hence, inflation is on the way.”

In sum, self-sufficiency implies higher domestic costs and price rises for consumers.

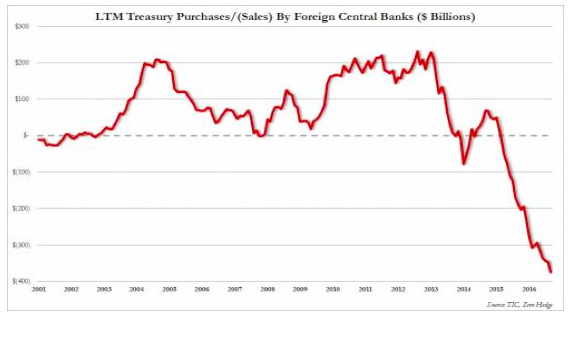

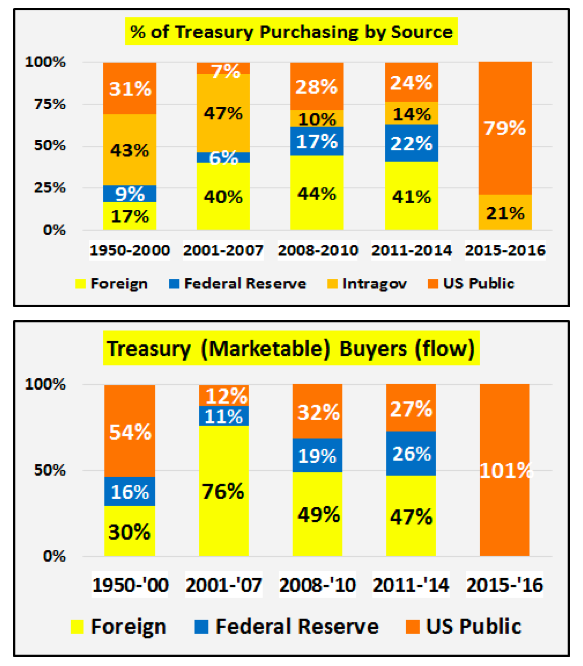

Debt will rise. And there is seemingly already a buyers’ strike against U.S. government debt underway: well over a third of a $1 trillion worth of Treasuries were disposed of, and sold in the year to Aug. 31 by foreign Central Banks. And who is buying it? (Below, the chart shows what this purchasing looks like, as a percentage of total debt issued by the Treasury). Well, foreign central banks have disappeared. (The Chinese have not bought a U.S. Treasury bond since 2011.)

(Above: who purchased the marketable debt as a percentage, by period) Source.

It is the American public who are buying. Will they be willing to take on Trump’s $1 trillion infrastructure spree? Or, will it be “printed” in yet another dilution of the American consumer’s purchasing power? The question of whether the infrastructure splurge does give growth hangs very much in the balance to such answers. (Equity shares in construction firms will do okay, of course).

The bottom line: (Michael Pento, Pento Report): “If interest rates continue to rise it won’t just be bond prices that will collapse. It will be every asset that has been priced off that so called ‘risk free rate of return’ offered by sovereign debt. The painful lesson will then be learned that having a virtual zero interest rate policy for the past 90 months wasn’t at all risk free. All of the asset prices negative interest rates have so massively distorted including; corporate debt, municipal bonds, REITs, CLOs, equities, commodities, luxury cars, art, all fixed income assets and their proxies, and everything in between, will fall concurrently along with the global economy.

“For the record, a normalization of bond yields would be very healthy for the economy in the long-run, as it is necessary to reconcile the massive economic imbalances now in existence. However, President Trump will want no part of the depression that would run concurrently with collapsing real estate, equity and bond prices.”

A Pending Financial Crisis

Trump, to be fair, has said consistently throughout the election campaign that whoever won the Presidential campaign to take office in January would face a financial crisis. Perhaps he will not face the “violent unwind” of the QE and bond bubble as some experts have predicted, but many more – according to Bank of America’s survey of 177 fund managers over the last six days, and controlling just under half a trillion of assets – expect a “stagflationary bond crash.”

This has major political implications. Trump is setting out to do no less than transform the economy and foreign policy of the U.S. He is doing this against a backdrop of many of the followers of the liberal élite, so angered at the election outcome, that they reject completely his electoral legitimacy (and, with the élites themselves staying mum at this rejection of the U.S. democratic process). Movements are being organized to wreck his Presidency (see here for example). If Trump does indeed experience a severe financial “unwind” at a time of such domestic anger and agitation, matters could turn quite ugly.

Alastair Crooke is a former British diplomat who was a senior figure in British intelligence and in European Union diplomacy. He is the founder and director of the Conflicts Forum, which advocates for engagement between political Islam and the West.

Gustave Doré Dante before the wall of flames which burn the lustful 1868

We’re doing something a little different. Nicole wrote another very long article and I suggested publishing it in chapters; this time she said yes. Over five days we will post five different chapters of the article, one on each day, and then on day six the whole thing. Just so there’s no confusion: the article, all five chapters of it, was written by Nicole Foss. Not by Ilargi.

Energy – Demand Collapse Followed by Supply Collapse

As we have noted many times, energy is the master resource, and has been the primary driver of an expansion dating back to the beginning of the industrial revolution. In fossil fuels humanity discovered the ‘holy grail’ of energy sources – highly concentrated, reasonably easy to obtain, transportable and processable into many useful forms. Without this discovery, it is unlikely that any human empire would have exceeded the scale and technological sophistication of Rome at its height, but with it we incrementally developed the capacity to reach for the stars along an exponential growth curve.

We increased production year after year, developed uses for our energy surplus, and then embedded layer upon successive layer of structural dependency on those uses within our societies. We were living in an era of a most unusual circumstance – energy surplus on an unprecedented scale. We have come to think this is normal as it has been our experience for our whole lives, and we therefore take it for granted, but it is a profoundly anomalous and temporary state of affairs.

We have arguably reached peak production, despite a great deal of propaganda to the contrary. We still rely on the giant oil fields discovered decades ago for the majority of the oil we use today, but these fields are reaching the end of their lives and new discoveries are very small in comparison. We are producing from previous finds on a grand scale, but failing to replace them, not through lack of effort, but from a fundamental lack of availability. Our dependence on oil in particular is tremendous, given that it underpins both the structure and function of industrial society in a myriad different ways.

An inability to grow production, or even maintain it at current levels past peak, means that our oil supply will be constricted, and with it both the scope of society’s functions and our ability maintain what we have built. Production from the remaining giant fields could collapse, either as they finally water out or as production is hit by ‘above ground factors’, meaning that it could be impacted by rapidly developing human events having nothing to do with the underlying geology. Above ground factors make for unpredictable wildcards.

Financial crisis, for instance, will be profoundly destabilizing, and is going to precipitate very significant, and very negative, social consequences that are likely to impact on the functioning of the energy industry. A liquidity crunch will cause purchasing power to collapse, greatly reducing demand at personal, industrial and national scales. With production geared to previous levels of demand, it will feel like a supply glut, meaning that prices will plummet.

This has already begun, as we have recently described. The effect is exacerbated by the (false) propaganda over recent years regarding unconventional supplies from fracking and horizontal drilling that are supposedly going to result in limitless supply. As far as price goes, it is not reality by which it is determined, but perception, even if that perception is completely unfounded.

The combination of perception that oil is plentiful, falling actual demand on economic contraction, and an acute liquidity crunch is a recipe for very low prices, at least temporarily. Low prices, as we are already seeing, suck the investment out of the sector because the business case evaporates in the short term, economic visibility disappears for what are inherently long term projects, and risk aversion becomes acute in a climate of fear.

Exploration will cease, and production projects will be mothballed or cancelled. It is unlikely that critical infrastructure will be maintained when no revenue is being generated and money is very scarce, meaning that reviving mothballed projects down the line may be either impossible, or at least economically non-viable.

The initial demand collapse may buy us time in terms of global oil depletion, but at the expense of aggravating the situation considerably in the longer term. The lack of investment over many years will see potential supply collapse as well, so that the projects we may have though would cushion the downslope of Hubbert’s curve are unlikely to materialize, even if demand eventually begins to recover.

In addition, various factions of humanity are very likely to come to blows over the remaining sources, which, after all, confer upon the owner liquid hegemonic power. We are already seeing a new three-way Cold War shaping up between the US, Russia and China, with nasty proxy wars being fought in the imperial periphery where reserves or strategic transport routes are located. Resource wars will probably do more than anything else to destroy with infrastructure and supplies that might otherwise have fuelled the future.

Given that the energy supply will be falling, and that there will, over time, be competition for increasingly scarce energy resources that we can no longer take for granted, proposed solutions which are energy-intensive will lie outside of solution space.

Declining Energy Profit Ratio and Socioeconomic Complexity

It is not simply the case that energy production will be falling past the peak. That is only half the story as to why energy available to society will be drastically less in the future in comparison with the present. The energy surplus delivered to society by any energy source critically depends on the energy profit ratio of production, or or energy returned on energy invested (EROEI).

The energy profit ratio is the comparison between the energy deployed in order to produce energy from any given source, and the resulting energy output. Naturally, if it were not possible to produce more than than the energy required upfront to do so (an EROEI equal to one), the exercise would be pointless, and ideally one would want to produce a multiple of the input energy, and the higher the better.

In the early years of the oil fuel era, one could expect a hundred-fold return on energy invested, but that ratio has fallen by something approximating a factor of ten in the intervening years. If the energy profit ratio falls by a factor of ten, gross production must rise by a factor ten just for the energy available to society to remain the same. During the oil century, that, and more, is precisely what happened. Gross production sky-rocketed and with it the energy surplus available to society.

However, we have now produced and consumed the lions’s share of the high energy profit ratio energy sources, and are depending on lower and lower EROEI sources for the foreseeable future. The energy profit ratio is set to fall by a further factor of ten, but this time, being past the global peak of production, we will not be able to raise gross production. In fact both gross production and the energy profit ratio will be falling at the same time, meaning that the energy surplus available to society is going to be very sharply curtailed. This will compound the energy crisis we unwittingly face going forward.

The only rationale for supposedly ‘producing energy’ from an ‘energy source’ with an energy profit ratio near, or even below, one, would be if one can nevertheless make money at it temporarily, despite not producing an energy return at all. This is more often the case at the moment than one might suppose. In our era of money created from nothing being thrown at all manner of losing propositions, as it always is at the peak of a financial bubble, a great deal of that virtual wealth has been pursuing energy sources and energy technologies.

Prior to the topping of the financial bubble, commodities of all kinds had been showing exponential price rises on fear of impending scarcity, thanks to the human propensity to extrapolate current trends, in this case commodity demand, forward to infinity. In addition technology investments of all kinds were highly fashionable, and able to attract investment without the inconvenient need to answer difficult questions. The combination of energy and technology was apparently irresistible, inspiring investors to dream of outsized profits for years to come. This was a very clear example of on-going dynamics in finance and energy intertwining and acting as mutually reinforcing drivers.

Both unconventional fossil fuels and renewable energy technologies became focii for huge amounts of inward investment. These are both relatively low energy profit energy sources, on average, although the EROEI varies considerably. Unconventional fossil fuels are a very poor prospect, often with an EROEI of less than one due to the technological complexity, drilling guesswork and very rapid well depletion rates.

However, the propagandistic hype that surrounded them for a number of years, until reality began to dawn, was sufficient to allow them to generate large quantities of money for those who ran the companies involved. Ironically, much of this, at least in the United states where most of the hype was centred, came from flipping land leases rather than from actual energy production, meaning that much of this industry was essentially nothing more than an elaborate real estate ponzi scheme.

Renewables, as we currently envisage them, unfortunately suffer from a relatively low energy profit ratio (on average), a dependence on fossil fuels for both their construction and distribution infrastructure, and a dependence on a wide array of non-renewable components.

We typically insist on deploying them in the most large-scale, technologically complex manner possible, thereby minimising the EROEI, and quite likely knocking it below one in a number of cases. This maximises monetary profits for large companies, thanks to both investor gullibility and greed and also to generous government subsidy regimes, but generally renders the exercise somewhere between pointless and counter-productive in long term energy supply terms.

For every given society, there will be a minimum energy profit ratio required to support it in its current form, that minimum being dependent on the scale and complexity involved. Traditional agrarian societies were based on an energy profit ratio of about 5, derived from their food production methods, with additional energy from firewood at a variable energy profit ratio depending on the environment. Modern society, with its much larger scale and vastly greater complexity, naturally has a far higher energy profit ratio requirement, probably not much lower than that at which we currently operate.

We are moving into a lower energy profit ratio era, but lower EROEI energy sources will not be able to maintain our current level of socioeconomic complexity, hence our society will be forced to simplify. However, a simpler society will not be able to engage in the complex activities necessary to produce energy from these low EROEI sources. In other words, low energy profit ratio energy sources cannot sustain a level of complexity necessary to produce them. They will not fuel the simpler future which awaits us.

Proposed solutions dependent on the current level of socioeconomic complexity do not lie within solution space.

Wyland Stanley Boeing 314 flying boat Honolulu Clipper. 1939

A few days before I arrived in Melbourne, The Automatic Earth’s Nicole Foss was one of the key speakers in The Great Debate, which this year took place on February 13. It’s sort of the main event in Melbourne’s annual Sustainable Living Festival, which in 2015 runs from February 7 to March 1. Apart from Nicole, other speakers included George Monbiot and David Holmgren.

In an impressive ‘take no prisoners’ speech, Nicole makes short shrift of the vast majority of idea(l)s about ‘softly transitioning’ into the world that lies beyond the dual credit ponzi and cheap energy bubbles. Everybody who harbors such idea(l)s should take note, lest they end up finding themselves in any one of a large variety of dead end alleyways.

Something along the vein of what my buddy Scott used to say: ‘it’s a good idea but it’s wrong’. People need to think about how much energy use and how much complexity is involved in what they would like to see as their way forward. If there’s too much of either, let alone of both, that way is simply not viable, and it’s back to the drawing board.

I’m not going to transcribe too much of her talk, it’s well worth watching the few minutes she talks. Still, here’s one quote from Nicole:

Our society will be forced to simplify. The paradox with low-energy-profit-ratio energy sources is they cannot sustain the level of complexity necessary to produce them. [..] If your solution rests on complexity, it’s not going to work. We’re going to contract and simplify, like it or not.