Arthur Siegel Zoot suit, business district, Detroit, Michigan Feb 1942

QE blows up the financial system instead of saving it. But some people and corporations will be much richer after.

• Fears Grow Over QE’s Toxic Legacy (Tracy Alloway/FT)

“Bankruptcy? Repossession? Charge-offs? Buy the car YOU deserve,” says the banner at the top of the Washington Auto Credit website. A stock photo of a woman with a beaming smile is overlaid with the promise of “100% guaranteed credit approval”. On Wall Street they are smiling too, salivating over the prospect of borrowers taking Washington AutoCredit up on its enticing offer of auto financing. Every car loan advanced to a high-risk, subprime borrower can be bundled into bonds that are then sold on to yield-hungry investors. These subprime auto “asset-backed securities”, or ABS, have, like a host of other risky assets, been beneficiaries of six years of quantitative easing by the US Federal Reserve, which is due to come to an end this week. When the Fed began asset purchases in late 2008 the premise was simple: unleash a tidal wave of liquidity to force nervous investors to move out of safe investments and into riskier assets.

It is hard to argue that the tactic did not work; half a decade of low interest rates and QE appears to have sparked an intense scrum for riskier securities as investors struggle to make their return targets. Wall Street’s securitization machine has kicked back into gear to churn out bonds that package together corporate loans, commercial mortgages and, of course, subprime auto loans. At $359 billion sold last year, according to Dealogic data, issuance of junk-rated corporate bonds is at a record as companies take advantage of low rates to refinance debt and investors clamor to buy it. The question now is whether the rebound in sales of risky assets will prove to be a toxic legacy of QE in a similar way that the popularity of subprime mortgage-backed securities was partly spurred by years of low interest rates before the financial crisis. “QE has flooded the system with cash and you’re really competing with an entity with an unlimited balance sheet,” says Manish Kapoor of West Wheelock Capital. “This has enhanced the search for yield and caused risk appetites to increase.”

That’s the goal.

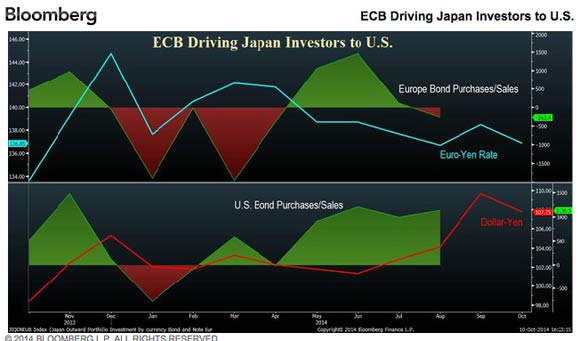

• Draghi QE May Help Europe’s Rich Get Richer (Bloomberg)

European Central Bank President Mario Draghi, fighting a deflation threat in the euro region, may need to confront a concern more familiar to Americans: income inequality. With interest rates almost at zero, Draghi is moving into asset purchases to lift inflation to the ECB’s target. The more he nears the kind of tools deployed by the Federal Reserve, the Bank of England and the Bank of Japan, the more he risks making the rich richer, said economists including Nobel laureate Joseph Stiglitz. In the U.S., the gap is rising between the incomes of the wealthy, whose financial holdings become more valuable via central bank purchases, and the poor. While monetary authorities’ foray into bond-buying is intended to stabilize economic conditions and underpin a real recovery, policy makers and economists are increasingly asking whether one cost may be wider income gaps – in Europe as well as the U.S.

“The more you use these unusual, even unprecedented monetary tools, the greater is the possibility of unintended consequences, of which contributing to inequality is one,” said William White, former head of the Bank for International Settlements’ monetary and economic department. “If you have all these underlying problems of too much debt and a broken banking system, to say that we can use monetary policy to deal with underlying real structural problems is a dangerous illusion.” The divide between rich and poor became part of a widespread public debate following the publication in English this year of Thomas Piketty’s “Capital in the Twenty-First Century.” He posited that capitalism may permit the wealthy to pull ahead of the rest of society at ever-faster rates.

“As James Grant recently observed, it’s quite remarkable how, thus far, savers in particular have largely suffered in silence.”

• Quantitative Easing Is Like “Treating Cancer With Aspirin” (Tim Price)

Shortly before leaving the Fed this year, Ben Bernanke rather pompously declared that Quantitative Easing “works in practice, but it doesn’t work in theory.” There is, of course, no counter-factual. We’ll never know what might have happened if the world’s central banks had not thrown trillions of dollars at the banking system, and instead let the free market work its magic on an overleveraged financial system. But to suggest credibly that QE has worked, we first have to agree on a definition of what “work” means, and on what problem QE was meant to solve. If the objective of QE was to drive down longer term interest rates, given that short term rates were already at zero, then we would have to concede that in this somewhat narrow context, QE has “worked”. But we doubt whether that objective was front and centre for those people – we could variously call them “savers”, “investors”, or “honest workers”. As James Grant recently observed, it’s quite remarkable how, thus far, savers in particular have largely suffered in silence.

So while QE has “succeeded” in driving down interest rates, the problem isn’t that interest rates were / are too high. Quite the reverse: interest rates are clearly too low – at least for savers. All the way out to 3-year maturities, investors in German government bonds, for example, are now faced with negative interest rates. And still they’re buying. This isn’t monetary policy success; this is madness. We think the QE debate should be reframed: has QE done anything to reform an economic and monetary system urgently in need of restructuring? We think the answer, self-evidently, is “No”. The answer is also “No” to the question: “Can you solve a crisis of too much indebtedness by increasing debt and suppressing interest rates?” The toxic combination of more credit creation and global financial repression will merely make the ultimate endgame that much more spectacular.

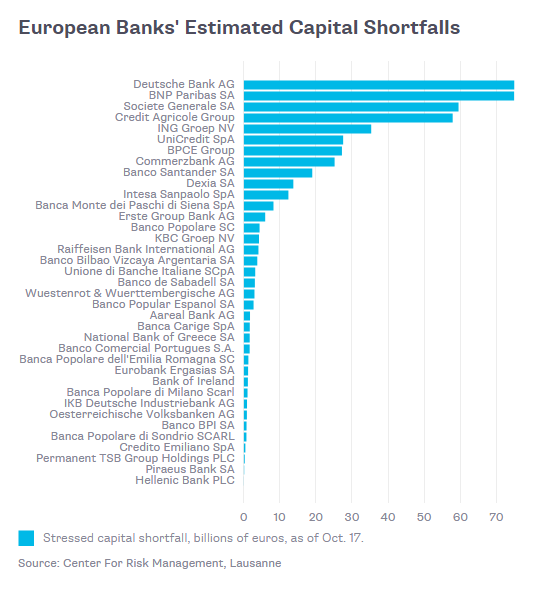

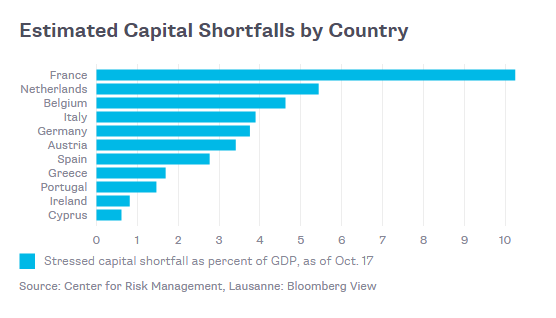

Good summary of – part of – the reasons the tests are such a joke. “… the 39 largest European banks would alone need up to €450bn in fresh capital”. That’s so close to the Swiss estimates I quoted on Sunday, it sounds quite credible. And so different from the €9.5 billion cited by the test results, it’s ridiculous. Off by a factor of 50…

• ECB Stress Tests Vastly Understate Risk Of Deflation And Leverage (AEP)

The eurozone’s long-awaited stress test for banks has been overtaken by powerful deflationary forces and greatly understates the risk of high debt leverage in a crisis, a chorus of financial experts has warned. George Magnus, senior advisor to UBS, said it was a “huge omission” for the European Central Bank to ignore the risk of deflation, given the profoundly corrosive effects that it can have on bank solvency. “Most of the eurozone periphery is already in deflation. They can’t just leave this out of their health check. It is a matter of basic due diligence,” he said. The ECB’s most extreme “adverse scenario” included a drop in inflation to 1pc this year, but the rate has already fallen far below this to 0.3pc, or almost zero once tax effects are stripped out. Prices have fallen over the past six months in roughly half of the currency bloc, and the proportion of goods in the EMU price basket in deflation has jumped to 31pc. “The scenario of deflation is not there, because indeed we don’t consider that deflation is going to happen,” said the ECB’s vice-president, Vitor Constancio.

The ECB had vowed to be tough in its first real test as Europe’s new super-regulator, promising to restore credibility after the fiasco of earlier efforts by the European Banking Authority in 2010 and 2011. The aim is to clean up the financial system once and for all, hoping that this will create more traction for the ECB’s mix of stimulus measures. Yet the bank has to walk a fine line since tough love would risk a further contraction of lending, and possibly a fresh crisis. The results released over the weekend suggest the ECB has opted for safety. Just 13 banks must raise fresh capital, mostly minor lenders in Italy and peripheral countries. They have nine months to find €9.5bn, a trivial sum set against the €22 trillion balance sheet of the lending system. Europe’s banks will have set aside an extra €48bn in provisions. Non-performing loans have jumped by €136bn.

Independent experts say the ECB has greatly under-played the threat of a serious shock. A study by Sachsa Steffen, from the European School of Management (ESMT) in Berlin, and Viral Acharya, at the Stern School of Business in New York, calculated that the 39 largest European banks would alone need up to €450bn in fresh capital. “The major flaw in the ECB test is that they don’t allow for systemic risk where there are forced sales and feedback effects, which is what happened in the Lehman crisis,” said Professor Steffen. Their study looked at levels of leverage rather than risk-weighted assets, which are subject to the discretion of national regulators and can easily be fudged. Most Club Med banks can defer tax assets, for example.

That’s just Basel, you could add a whole lot more criteria.

• Under Full Capital Rules, 36 EU Banks Would Have Failed Test (Reuters)

Europe’s banking health check has shown countries and lenders are implementing global capital rules at vastly different speeds, and 36 companies would have failed if new capital rules were fully applied. The euro zone is lagging behind countries outside the bloc in implementing the Basel III capital rules that are due to come into full force in 2019, potentially adding another challenge for the European Central Bank when it takes over supervision of euro zone lenders next month. “On a fully loaded basis, many banks have only passed the stress test by very thin margins or could be challenged in meeting the requirements, so they will be expected to do more,” said Carola Schuler, managing director for banking at ratings agency Moody’s. Some 25 European banks failed a health check of whether they could withstand a recession, and another 11 would have failed if the full Basel III rules had been applied, according to data from the European Banking Authority released on Sunday.

Europe had gained credibility, said Karen Petrou, co-founder of Federal Financial Analytics in Washington. But a similar exercise by the U.S. Federal Reserve was still tougher, among others because it requires banks to fully load Basel. “It’s still an easier and different one than the Fed stress test in many, many respects,” she said. “The Fed’s test is very qualitative. You can get all the numbers right and still fail.” The wider capital gap with fully implemented Basel rules could put pressure on more banks to improve the amount and quality of their capital, potentially impacting their profitability, growth plans and dividend payouts. Banks failed if they had common equity of 5.5% or less under a 2014/16 recession scenario. The EBA’s “stress test” was based on transitional capital rules, which vary by country, depending on how quickly they are phasing in rules. But for the first time, so-called ‘fully loaded’ Basel III ratios – applying all the new global rules – were released across Europe’s top 130 banks for analysts and investors to compare their capital strength.

30% seems low.

• 3 Reasons Why You Should Expect A 30% Market Meltdown (MarketWatch)

In a commentary for MarketWatch just over two months ago, I predicted that the U.S. stock faced at least a 20% correction. The signals now point to a 30% downturn. This recent market volatility is just the beginning. The declines that corrected prices more than 10% in both the Russell 2000 Index and the Nasdaq Composite Index encompassed the majority of the market, and these stocks have begun their descent. Meanwhile, both the Dow Jones Industrial Average, containing 30 stocks, and the S&P 500 have yet to correct 10%, but historically they are the last to fall. My proprietary indicator called the CCT gave an ominous sell signal in the summer. Since then, the sell signal has increased in intensity and entered a 30% correction zone. The CCT measures several internal market components. It is a leading indicator that actually can be quantified.

The strongest component is the duration of buying versus the duration of selling. A healthy bull market sees mostly buying, indicated by the NYSE tick. The longer the buying persists with NYSE Tick readings in the plus column, the stronger the share price advances. But what happens when prices increase and the duration of the plus-column NYSE tick is less than the duration of the minus tick? This is a divergence, indicating lessening volume dedicated to the buying of a wide array of stock sectors. This duration buying has been lessening since July. Every rally shows less broad participation in all sectors of NYSE stocks. This is what happens in bear markets. A second component of the CCT focuses on the NYSE “big block” buying and selling in isolated segments of time. This is different than the duration component, as it measures isolated situations of what fund managers are doing.

A strong bullish market has numerous big blocks of buying. A print on the NYSE tick in excess of +1000 signifies fund buying by numerous entities, which accompanies a healthy bull market. But what happens when prices are climbing but no +1000 NYSE ticks are printed? This is a divergence indicating lack of interest by fund managers to commit large amounts of cash. Prices are getting ahead of buying interest, and that divergence cannot persist. We saw this phenomenon frequently in September as the S&P 500 recorded all-time highs. This also occurs in bear markets. A third and final component is the cumulative number of the NYSE tick. Each day I record the amount of total plus tick, less the amount of minus tick, on the NYSE. A bull market has a tight correlation of a up day for stock prices corresponding to a plus day in the cumulative NYSE tick.

Why interest rates must and will rise.

• US Banks See Worst Outflow of Money in ETF Since 2009 (Bloomberg)

The Financial Select Sector SPDR (XLF), an exchange-traded fund targeting banks and investment firms, had the biggest withdrawal last week since 2009 amid concern that low interest rates and market swings will hurt profits. Investors pulled $913.4 million from the $17.5 billion ETF, whose top holdings include Berkshire Hathaway, Wells Fargo and JPMorgan Chase, a shift that turned its flow of funds negative for the year. About 143 million shares of the ETF have been borrowed and sold to speculate on declines, the most since June 2012, according to exchange data compiled by Bloomberg. Banks have waited for years for higher rates and more robust trading to boost revenue from lending and market-making.

Weaker-than-expected global growth could prompt the U.S. central bank to slow the pace of eventual interest-rate increases, Federal Reserve Vice Chairman Stanley Fischer said Oct. 11. The severity of market swings this month also boosts the risk that banks will incur losses while facilitating client bets, and it may slow mergers and acquisitions. “Investors should have less exposure to financials than the broader market because we don’t think the prospects are that strong,” said Todd Rosenbluth, director of mutual-fund and ETF research at S&P Capital IQ in New York, referring to interest rates. If the Fed keeps rates low, “the upside in these financials is taken away,” said Charles Peabody, an analyst at Portales Partners LLC in New York.

Is that even a question?

• The Great Recession Put Us in a Hole. Are We Out Yet? (Bloomberg)

In October 2007, U.S. stocks were hitting an all-time high, jobs were plentiful and homes were expensive. Two months later, the Great Recession began to eviscerate the economy, ultimately sucking $10 trillion out of U.S. stocks, collapsing a housing bubble and pushing the unemployment rate to 10%. A lot of talk of financial irresponsibility – people living beyond their means – followed. Seven years later, most Americans have put their finances in order, reducing all kinds of consumer debt. So it’s no small insult, after the injury of the recession, that many aren’t being rewarded for smarter spending. Americans are making a lot less money and own fewer assets, the Federal Reserve said last month, even as stocks reach new highs. Housing prices recovered, though they’re still 13% below 2007 levels. Fewer Americans own houses they can’t afford – sending rents up 16%, to an average of $1,100 per apartment in metro areas.

On the bright side, housing’s collapse taught consumers about the dangers of debt. Americans have shed $1.5 trillion in mortgage debt and $139.4 billion in credit card and other revolving debt over the last six years. They were pushed by tighter credit rules and enticed by the chance to refinance at lower rates. But they also saved more diligently. The U.S. savings rate has doubled since 2007, to 5.4% in September. Educational loans are up, by $2,500 for the median family paying off student loans. But that’s prompted by tuition increases and a surge of people going back to school. Post-secondary enrollment jumped 15%, or 2.8 million, from 2007 to 2010, according to the U.S. Department of Education. Jobs may be coming back, but good jobs are still scarce. More than 7 million people are working part-time jobs when they’d prefer a full-time gig, 57% more than in 2007. And more than 3% of adults have left the workforce entirely since 2007, according to the U.S. labor force participation rate.

What else are they faking?

• China Fake Invoice Evidence Serve To Inflate Trade Data (Bloomberg)

The gap between China’s reported exports to Hong Kong and the territory’s imports from the mainland widened in September to the most this year, suggesting fake export-invoicing is again skewing China’s trade data. China recorded $1.56 of exports to Hong Kong last month for every $1 in imports Hong Kong registered, leading to a $13.5 billion difference, according to government data compiled by Bloomberg. Hong Kong’s imports from China climbed 5.5% from a year earlier to $24.1 billion, figures showed yesterday; China’s exports to Hong Kong surged 34% to $37.6 billion, according to mainland data on Oct. 13.

While China’s government has strict rules on importing capital, those seeking to exploit yuan appreciation can evade the limit by disguising money inflows as payment for goods exported to foreign countries or territories, especially Hong Kong. The latest trade mismatch coincided with renewed appreciation of China’s currency, leading analysts at banks and brokerages including Everbright Securities Co. and Australia & New Zealand Banking Group Ltd. to question the export surge. “This is definitely another important piece of evidence of over-invoicing exports to Hong Kong to facilitate money inflow into China,” said Shen Jianguang, chief Asia economist at Mizuho Securities. in Hong Kong. “So we shouldn’t be too optimistic about recent export data from China.” Doubts over the data raise broader concerns, as a surge in exports was believed to have underpinned economic growth in the third quarter. Shen said the economic outlook is “challenging” and more easing is “necessary.”

Krugman wins again.

• Riksbank Cuts Key Rate to Zero as Deflation Fight Deepens (Bloomberg)

Sweden’s central bank ventured into uncharted territory as it cut its main interest rate to a record low and delayed tightening plans into 2016 in a bid to jolt the largest Nordic economy out of a deflationary spiral. “The Swedish economy is relatively strong and economic activity is continuing to improve,” the Stockholm-based bank said in a statement. “But inflation is too low.” The benchmark repo rate was lowered to zero from 0.25%, the third reduction in less than a year. The bank was seen cutting to 0.1% in a Bloomberg survey of 17 economists. Only two economists had predicted a cut to zero. The Riksbank said it won’t raise rates until mid-2016 compared with a September forecast for the end of 2015. The “assessment is that the repo rate needs to remain at this level until inflation clearly picks up,” the Riksbank said in a statement. “It is assessed as appropriate to slowly begin raising the repo rate in the middle of 2016.” The move follows calls from former board members, politicians and economists to do more to prevent deflation from taking hold.

Consumer prices have dropped in seven of the past nine months and inflation has stayed below the bank’s 2% target for almost three years. Governor Stefan Ingves, who’s also chairman of the Basel Committee on Banking Supervision, has been reluctant to lower rates out of fear of stoking a build-up in consumer debt. Ingves raised the benchmark rate quickly after the financial crisis showed signs of easing in 2010. His reluctance since then to cut rates prompted Nobel Laureate Paul Krugman in April to accuse the Riksbank of a “sadomonetarist” approach to policy he said risked creating a Japan-like deflation trap. Now, Ingves is shaping Swedish policy to reflect moves elsewhere and bringing rates in line with those at the European Central Bank, whose benchmark is 0.05 percent, and the U.S. Federal Reserve, which has held its key rate close to zero since 2008. The ECB and Fed have also expanded their balance sheets through asset purchases to further stimulate growth.

Don’t think they need the IMF to tell them they need to keep their young people satisfied or else.

• IMF Warns Gulf Countries Of Spending Squeeze (CNBC)

Oil exporters in the crude-rich Gulf need to rationalize spending amid a deteriorating global economic outlook, the International Monetary Fund has warned. “In the GCC (Gulf Co-operation Council), years of fast growth since the global financial crisis, rising asset prices, rapid credit growth in some countries, and accommodative global monetary conditions call for a return to fiscal consolidation,” the IMF said in its biannual economic outlook for the Middle East and Central Asia. But the fund also cautioned against immediate policy responses, especially given that GCC exporters were were well-placed to handle the current volatility in global energy markets. “It is not likely to have an effect on economic activity this year or the next. We don’t think that it would make sense to have a knee-jerk reaction,” Masood Ahmed, Director, Middle East and Central Asia Department at the IMF, told CNBC. “It’s important to gradually moderate the base of fiscal spending”. The fund expected the GCC oil exporters’ economies to grow by 4.4% in 2014, accelerating to 4.5% in 2015.

A sharp decline in oil prices over the past month has prompted fierce debate about potential policy responses from Gulf governments. Over the weekend, Kuwaiti Finance Minister Anas Al-Saleh Gulf Arab joined those calling for cuts in spending to cover the shortfall in income. Global prices fell to four-year lows earlier this month, putting at risk abundant fiscal surpluses and savings generated in recent years. OPEC members are due to meet on November 27 in Vienna. According to Mohamed Lahouel, Chief Economist at the Department of Economic Development in Dubai, current or lower oil prices for a period of around four months would elicit spark fiscal decisions on the part of regional government as they scramble to safeguard capital gains. Not all industry experts agree that low oil prices are here to stay. Mohamed Al-Mady, CEO of Saudi Basic Industries (SABIC), one of the world’s largest petrochemical companies, told reporters on Sunday in Riyadh the recent declines would prove to be temporary, and that demand growth was firmly underpinned.

Make sure to make them pay a sh*tload of money for the extension, see if they still want it.

• Shell Seeks 5 More Years for Arctic Oil Drilling Drive (Bloomberg)

Royal Dutch Shell is asking the Obama administration for five more years to explore for oil off Alaska’s coast, saying set backs and legal delays may push the start of drilling past the 2017 expiration of some leases. Shell, which has spent eight years and $6 billion to search for oil in the Arctic’s Beaufort and Chukchi seas, said in letter to the Interior Department that “prudent” exploration before leases expire is now “severely challenged.” “Despite Shell’s best efforts and demonstrated diligence, circumstances beyond Shell’s control have prevented, and are continuing to prevent, Shell from completing even the first exploration well in either area,” Peter Slaiby, vice president of Shell Alaska, wrote to the regional office of the Bureau of Safety and Environmental Enforcement. Shell’s plans to produce oil in the Arctic were set back in late 2012 by mishaps involving a drilling rig and spill containment system, and the company has been sued by environmental groups seeking to block the Arctic exploration.

The Hague-based company halted operations in 2012 to repair equipment and hasn’t resumed its maritime operations off Alaska’s northern coast. The July 10 letter from the company, released yesterday by the environmental group Oceana that got it after a public records request, seeks to pause Shell’s leases for five years. That would, in effect, extend the deadline to drill on its Beaufort and Chukchi leases. Leases issued by the government for the right to drill for oil in the Arctic expire in 10 years unless the holder can show significant progress toward development. Shell has left open the possibility of returning to Arctic drilling as soon as next year. Spokesman Curtis Smith said that timeline remains on the table. “We’re taking a methodical approach to a potential 2015 program,” Smith said in an e-mail. The U.S. has ordered that any drilling in the Arctic end each year before Oct. 1, when ice starts forming.

Not in centralized grid systems.

• Wind Farms Can ‘Never’ Be Relied Upon To Deliver UK Energy Security (Telegraph)

Wind farms can never be relied upon to keep the lights on in Britain because there are long periods each winter in which they produce barely any power, according to a new report by the Adam Smith Institute. The huge variation in wind farms’ power output means they cannot be counted on to produce energy when needed, and an equivalent amount of generation from traditional fossil fuel plants will be needed as back-up, the study finds. Wind farm proponents often claim that the intermittent technology can be relied upon because the wind is always blowing somewhere in the UK. But the report finds that a 10GW fleet of wind farms across the UK could “guarantee” to provide less than two per cent of its maximum output, because “long gaps in significant wind production occur in all seasons”. Modelling the likely output from the 10GW fleet found that for 20 weeks in a typical year the wind farms would generate less than a fifth (2GW) of their maximum power, and for nine weeks it would be less than a tenth (1GW).

Output would exceed 9GW, or 90% of the potential, for just 17 hours. Britain currently has more than 4,500 onshore wind turbines with a maximum power-generating capacity of 7.5GW, and is expected to easily surpass 10 GW by 2020 as part of Government efforts to tackle climate change. It is widely recognised that variable wind speeds result in actual power output significantly below the maximum level – on average between 25 and 30 per cent, according to Government data. However, the report from the Adam Smith Institute found that such average figures were “extremely misleading about the amount of power wind farms can be relied up to provide”, because their output was actually “extremely volatile”. “Each winter has periods where wind generation is negligible for several days,” the report’s author, Capell Aris, said. Periods of calm in winter would require either significant energy storage to be developed – an option not readily available – or an equivalent amount of conventional fossil fuel plants to be built.

No, really, the World Economic Forum pays people generous salaries to look into their crystal ball and tell us what the world will look like in 80 years time.

• Equal Footing For Women At Work? Not Till 2095 (CNBC)

Women may not achieve equal footing in the workplace until 2095, according to the World Economic Forum’s (WEF) new ‘Global Gender Gap’ report. The economic participation and opportunity gap between the sexes stands at 60% worldwide, an improvement of only 4 percentage points since WEF measurements began in 2006. The economic sub-index reflects three measurements: the difference between genders in labor force participation rates; wage equality; and the female-to-male ratio across a range of professions. The organization estimates it will take 81 years for the world to close this gap completely.

Two sub-Saharan African nations took top spots on the economic sub index: Burundi and Malawi ranked first and third respectively. Burundi is one of the few countries in the world to adopt a gender quota for its legislature – an attempt to promote the participation of women in politics. “Much of the progress on gender equality over the last ten years has come from more women entering politics and the workforce. In the case of politics, globally, there are now 26% more female parliamentarians and 50% more female ministers than nine years ago,” said Saadia Zahidi, head of the gender parity program at the World Economic Forum and lead author of the report.

Recovery.

• Lloyds Bank Confirms 9,000 Job Losses And Branch Closures As Profit Rises (BBC)

Lloyds Banking Group has confirmed 9,000 job losses and the closure of 150 branches over the next three years. The group, which operates the Lloyds Bank, Halifax and Bank of Scotland brands, reported pre-tax profits of £1.61bn for the nine months to 30 September. The group is setting aside another £900m to cover possible payouts for the PPI mis-selling scandal. The scandal has cost Lloyds, in total, about £11bn. Fines for the Libor rate-rigging scandal have topped £200m. The government still holds a 25% stake in the bank, but has reduced its holding from about 39% through two separate share sales since September last year.

Earlier this year, Lloyds spun off the TSB bank as a separate business to appease European Union competition authorities. The group also said it would invest £1bn in digital technology as more customers switch to mobile banking. But the banking group has returned to profitability under chief executive Antonio Horta-Osorio. On Monday, shares in Lloyds Banking Group fell 1.8% after the European Banking Authority’s results revealed that the bank only narrowly passed the test.

Not what the Founding Fathers had in mind for the land of the free.

• IRS Seizes 100s Of Perfectly Legal Bank Accounts, Refuses To Return Money (RT)

The Internal Revenue Service has been seizing bank accounts belonging to small businesses and individuals who regularly made deposits of less than $10,000, but broke no laws. And the government is refusing to return all the money taken. The practice, called civil asset forfeiture, allows IRS agents to seize property they suspect of being tied to a crime, even if no charges are filed, and their agency is allowed to keep a share of whatever is forfeited, the New York Times reported. It’s designed to catch drug traffickers, racketeers and terrorists by tracking cash deposits under $10,000, which is the threshold for when banks are federally required to report activity to the IRS under the Bank Secrecy Act. It is not illegal to deposit less than $10,000 in cash, unless it is specifically done to avoid triggering the federal reporting requirement, known as structuring.

Thus, banks are required to report any suspicious transactions to authorities, including patterns of deposits below that threshold.“Of course, these patterns are also exhibited by small businesses like bodegas and family restaurants whose cash-on-hand is only insured up to $10,000, and whose owners are wary of what would be lost in the case of a robbery or a fire,” the Examiner noted. Carole Hinders, a victim of civil asset forfeiture, owns a cash-only Mexican restaurant in Iowa. Last year, the IRS seized her checking account and the nearly $33,000 in it. She told the Times she did not know of the federal reporting requirement for suspicious transactions, and that she thought she was doing everyone a favor by reducing their paperwork.

“My mom had told me if you keep your deposits under $10,000, the bank avoids paperwork,” she said.“I didn’t actually think it had anything to do with the I.R.S.” And her bank wasn’t allowed to tell her that her habits could be reported to the government. If customers ask about structuring their deposits, banks are allowed to give them a federal pamphlet.“We’re not allowed to tell them anything,” JoLynn Van Steenwyk, the fraud and security manager for Hinders’ bank, told the Times. Last year, banks filed more than 700,000 suspicious activity reports, according to the Times. The median amount seized by the IRS. was $34,000, according to an analysis by the Institute for Justice, while legal costs can easily mount to $20,000 or more, meaning most account owners can’t afford to fight the government for their money.

Is it any wonder? This may be the only way to get rid of the IRS.

• Bulk Of Americans Abroad Want To Give Up Citizenship (CNBC)

A staggering number of Americans residing abroad are tempted to give up their U.S. passports in the wake of tougher asset-disclosure rules under the Foreign Account Tax Compliance Act (FATCA), according to a new survey. The survey by financial consultancy deVere Group asked expatriate Americans around the world “Would you consider voluntarily relinquishing your U.S. citizenship due to the impact of FATCA?” 73% of respondents answered that they had “actively considered it”, “are thinking about it” or “have explored the options of it.” On the other hand, 16% said they would not consider relinquishing their U.S. citizenship, and 11% did not know. The survey carried out in September 2014 polled almost 420 Americans living in Hong Kong, China, Indonesia, Thailand, Philippines, Japan, India, UK, UAE and South Africa. FATCA, which came into effect on July 1, requires foreign banks, investment funds and insurers to hand over information to the IRS about accounts with more than $50,000 held by Americans.

The controversial tax law is intended to detect tax evasion by U.S. citizens via assets and accounts held offshore. “For long-term retired U.S. expats, of which I am one, who are paying significant U.S. taxes, the value of U.S. citizenship often comes to mind,” a U.S. citizen residing in Bangkok told CNBC. “What do we get in return for our U.S. passport? Only three things in my opinion,” said the 69-year-old, who requested to remain anonymous. “First of all, a passport that is extremely convenient for worldwide travel, second we can vote in U.S state and national elections and third we can pay taxes on both our U.S. and foreign income. That’s it. When you add the new FATCA policies, it obviously adds more thought to the question: Is it worth keeping?” It’s alarming that nearly three quarters of Americans abroad said that they are going to or have thought about giving up their U.S. citizenship, said Nigel Green, founder and chief executive of deVere Group.

” … what happens now to the regularly issued treasury bonds and bills? Do they just sit in an accordian file on Jack Lew’s desk next to his Barack Obama bobblehead?”

• Tapering, Exiting, or Just Punting? (Jim Kunstler)

Oh, that sound you hear this morning is the distant roar of European equity markets puking after the latest round of phony bank “stress tests” — another exercise in pretend by financial authorities who understand, at least, the bottomless credulity of the news media and the complete mystification of the general public in monetary matters. I rather expect that roar to grow Niagara-like as US markets catch the urge to upchuck violently. Problem is, unlike Ebola victims, they can’t be quarantined. The end of the “taper” is upon us like the night of the hunter, conveniently just a week before the US election. If the Federal Reserve is politicized, the indoctrination must have been conducted by the Three Stooges. America’s central bank never did explain the difference between tapering and exiting their purchases of US treasury paper. I guess that’s because it has other interventionary tricks up its sleeves.

Three-card Monte with reverse repos… ventures into direct stock purchases… the setting up of new Maiden Lane type companies for scarfing up securities with that piquant dead carp aroma. Who knows what’s next? It’s amazing what you can do with money in a desperate polity with a few dozen lawyers. Of course, there is the solemn matter as to what happens now to the regularly issued treasury bonds and bills? Do they just sit in an accordian file on Jack Lew’s desk next to his Barack Obama bobblehead? The Russians don’t want them. The Chinese are already stuck with trillions they would like to unload for more gold. Frightened European one-percenters may want to park some cash in American paper to avoid bail-ins and other confiscations already rehearsed over there — but could that amount to more than a paltry few billion a month at the most?

What do the stock markets do without up to $85 billion a month (peak QE) sloshing around looking for dark pools to settle in? Can US companies keep the markets levitated by buying back their own shares like snakes eating their tails? Isn’t that basically over and done? And exactly how do interest rates stay suppressed when only a few French tax refugees want to buy American debt? I don’t think anybody knows the answer to these questions and the scenarios are too abstruse for the people who get paid for supposedly writing learned commentary in the sclerotic remnants of the press.

The chief investogator can’t get his hands on the evidence?!

• MH17 Might Have Been Shot Down From Air – Chief Dutch Investigator (RT)

The chief Dutch prosecutor investigating the MH17 downing in eastern Ukraine does not exclude the possibility that the aircraft might have been shot down from air, Der Spiegel reported. Intelligence to support this was presented by Moscow in July. The chief investigator with the Dutch National Prosecutors’ Office Fred Westerbeke said in an interview with the German magazine Der Spiegel published on Monday that his team is open to the theory that another plane shot down the Malaysian airliner. Following the downing of the Malaysian Airlines MH17 flight in July that killed almost 300 people, Russia’s Defense Ministry released military monitoring data, which showed a Kiev military jet tracking the MH17 plane shortly before the crash. No explanation was given by Kiev as to why the military plane was flying so close to a passenger aircraft. Neither Ukraine, nor Western states have officially accepted such a possibility.

Westerbeke said that the Dutch investigators are preparing an official request for Moscow’s assistance since Russia is not part of the international investigation team. Westerbeke added that the investigators will specifically ask for the radar data suggesting that a Kiev military jet was flying near the passenger plane right before the catastrophe. “Going by the intelligence available, it is my opinion that a shooting down by a surface to air missile remains the most likely scenario. But we are not closing our eyes to the possibility that things might have happened differently,” he elaborated. In his interview to the German media, Westerbeke also called on the US to release proof that supports its claims.

“We remain in contact with the United States in order to receive satellite photos,” he said. German’s foreign intelligence agency reportedly also believes that local militia shot down Malaysia Airlines flight MH17, according to Der Spiegel. The media report claimed the Bundesnachrichtendienst (BND) president Gerhard Schindler provided “ample evidence to back up his case, including satellite images and diverse photo evidence,” to the Bundestag in early October. However, the Dutch prosecutor stated that he is “not aware of the specific images in question”. “The problem is that there are many different satellite images. Some can be found on the Internet, whereas others originate from foreign intelligence services.”

• MH17 Chief Investigator: No Actionable Evidence Yet In Probe (Spiegel)

SPIEGEL: Germany’s foreign intelligence agency, the Bundesnachrichtendienst (BND), believes that pro-Russian separatists shot down the aircraft with surface-to-air missiles. A short time ago, several members of the German parliament were presented with relevant satellite images. Are you familiar with these photos?

Westerbeke: Unfortunately we are not aware of the specific images in question. The problem is that there are many different satellite images. Some can be found on the Internet, whereas others originate from foreign intelligence services.

SPIEGEL: High-resolution images – those from US spy satellites, for example – could play a decisive role in the investigation. Have the Americans provided you with those images?

Westerbeke: We are not certain whether we already have everything or if there are more — information that is possibly even more specific. In any case, what we do have is insufficient for drawing any conclusions. We remain in contact with the United States in order to receive satellite photos.

SPIEGEL: So you’re saying there hasn’t been any watertight evidence so far?

Westerbeke: No. If you read the newspapers, though, they suggest it has always been obvious what happened to the airplane and who is responsible. But if we in fact do want to try the perpetrators in court, then we will need evidence and more than a recorded phone call from the Internet or photos from the crash site. That’s why we are considering several scenarios and not just one.

SPIEGEL: Moscow has been spreading its own version for some time now, namely that the passenger jet was shot down by a Ukrainian fighter jet. Do you believe such a scenario is possible?

Westerbeke: Going by the intelligence available, it is my opinion that a shooting down by a surface to air missile remains the most likely scenario. But we are not closing our eyes to the possibility that things might have happened differently.

It gets serious: “20% of men and 12% of women who want to have children cannot”.

• Having Babies New Sex Ed Goal as Danes Face Infertility Epidemic (Bloomberg)

Sex education in Denmark is about to shift focus after fertility rates dropped to the lowest in almost three decades. After years of teaching kids how to use contraceptives, Sex and Society, the Nordic country’s biggest provider of sex education materials for schools, has changed its curriculum to encourage having babies under the rubric: “This is how you have children!” Infertility is considered “an epidemic” in Denmark, said Bjarne Christensen, secretary general of the Copenhagen-based organization. “We see more and more couples needing to get assisted fertility treatment. We see a lot of people who don’t succeed in having children.” Denmark’s fertility rate is at its lowest in more than a quarter of a century, with one in 10 children conceived only after treatment. Health professionals are urging the government to do more to address the declining birth rate and prevent it becoming a bigger demographic problem. Declining fertility is affecting demographics across Europe, where the birthrate has hardly grown for two decades.

The trend has profound effects not only on individuals but also on the economy and the outlook for standards of life, with fewer young people supporting older, retired populations. The European Commission says it considers the growing gap between the number of young and old citizens one of the region’s biggest challenges. According to Christensen at Sex and Society, the issue needs to be addressed at the school level if there is to be change. “We hope to raise a discussion in society about how to advise young people,” said Christensen, whose group helps organize an annual Sex Week to focus schools’ attention on the subject. “It’s a problem that fertility in Denmark is reduced.” Sex and Society’s new focus, unveiled on Sunday, includes information for school children explaining what fertility is, when the best times to have children may be, and what the effects of aging are. [..] 20% of men and 12% of women who want to have children cannot, according to Dansk Fertilitetsselskab, a professional organization for health providers and researchers.

Stunning. You’d think there are contingency plans, but they seem to make it all up one step at a time.

• Medical Journal To Governors: You’re Wrong About Ebola Quarantine (NPR)

The usually staid New England Journal of Medicine is blasting the decision of some states to quarantine returning Ebola health care workers. In an editorial the NEJM describes the quarantines as unfair, unwise and “more destructive than beneficial.” In their words, “We think the governors have it wrong.” The editors say the policy could undermine efforts to contain the international outbreak by discouraging American medical professionals from volunteering in West Africa. “The way we are going to control this epidemic is with source control and that’s going to happen in West Africa, we hope. In order to do that we need people on the ground in West Africa,” says Dr. Jeffrey Drazen, editor-in-chief of the journal. Speaking to Goats and Soda, he says it doesn’t make any sense to “imprison” healthcare workers for three weeks after they’ve been treating Ebola patients. The editorial explains his rationale, arguing that healthcare workers who monitor their own temperatures daily would be able to detect the onset of Ebola before they become contagious and thus before they pose any public health threat to their home communities:

“The sensitive blood polymerase-chain-reaction (PCR) test for Ebola is often negative on the day when fever or other symptoms begin and only becomes reliably positive 2 to 3 days after symptom onset. This point is supported by the fact that of the nurses caring for Thomas Eric Duncan, the man who died from Ebola virus disease in Texas in October, only those who cared for him at the end of his life, when the number of virions he was shedding was likely to be very high, became infected. Notably, Duncan’s family members who were living in the same household for days as he was at the start of his illness did not become infected.”