Andrew Wyeth Christina’s world 1948

24 hours without internet at home. A little bit of improvisation today.

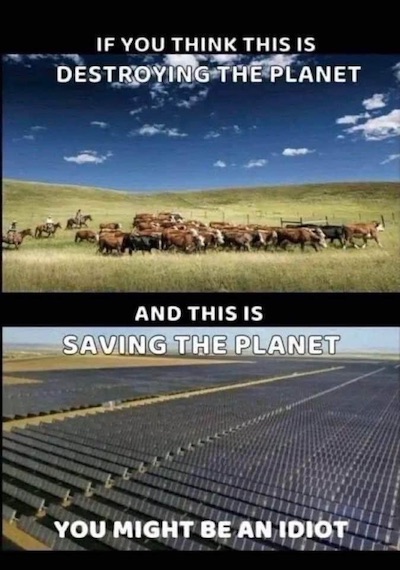

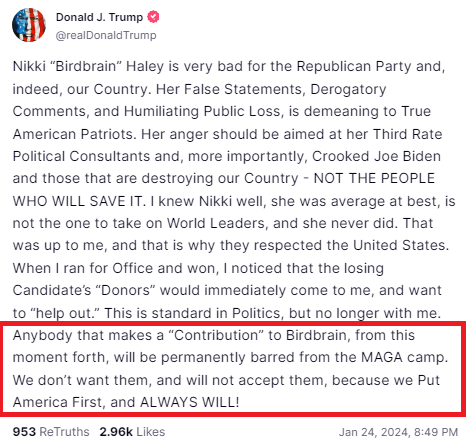

Vivek Trump SS

The swamp is hellbent on keeping Trump out of office. First they sued him. Then they prosecuted him. Then they tried to take him off the ballot. None of it worked & now they’re trying to strip his Secret Service protection. I wonder what they’re rooting for? pic.twitter.com/3fdnM7eXUi

— Vivek Ramaswamy (@VivekGRamaswamy) April 20, 2024

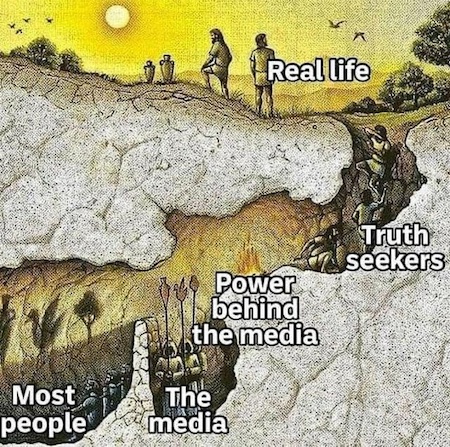

Third eye

Obama’s Third Eye in the White House is THIS man.

He’s calling the shots… He is why Iran/Hamas attacked Israel.

Now he’s panicking. @OANN #Iran pic.twitter.com/eAx2Y7n37r

— Chanel Rion OAN (@ChanelRion) April 20, 2024

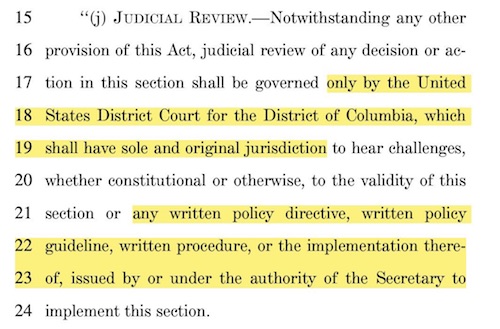

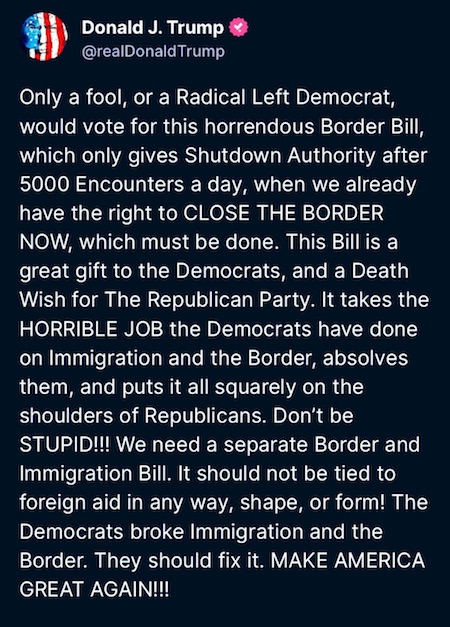

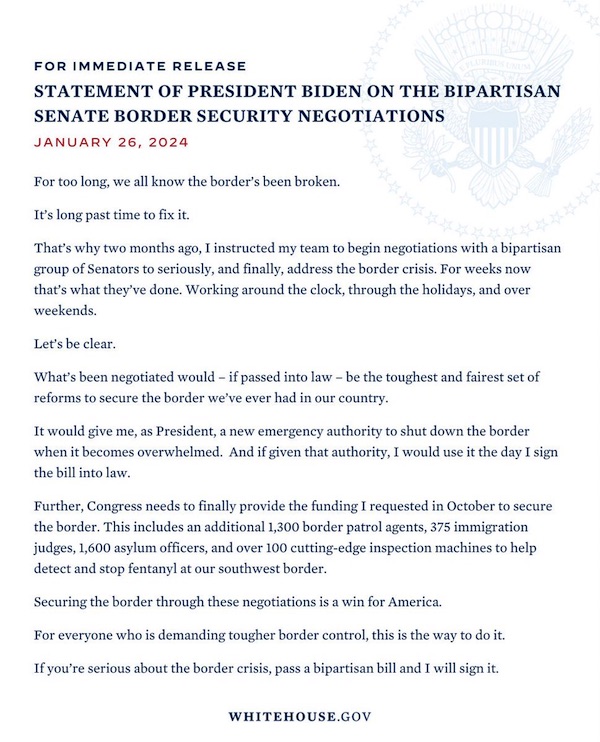

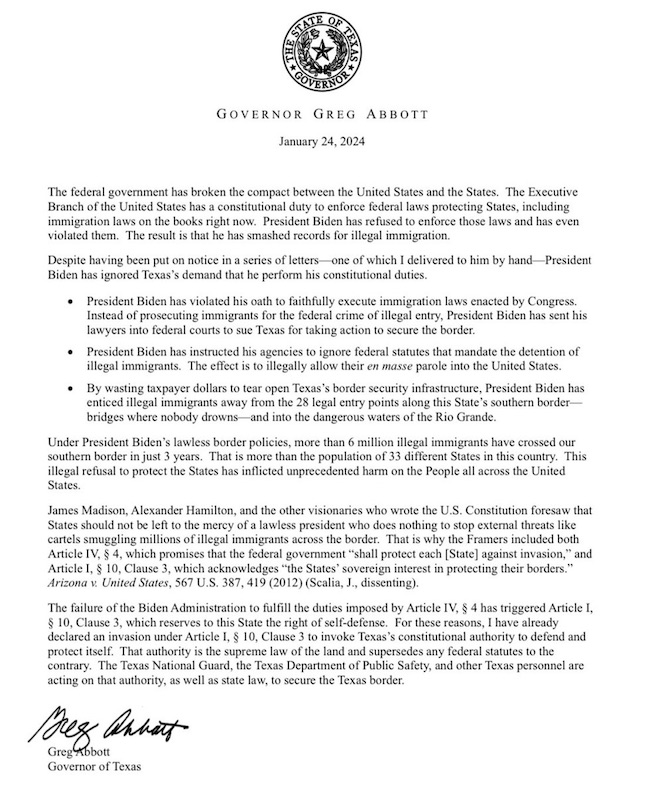

But not the border. Mike Johnson became speaker BECAUSE he said he’d protect the border.

• House Passes $95 Billion Aid Package For Ukraine, Israel And Taiwan (ZH)

The House on Saturday passed a set of foreign aid bills that would send $61 billion to Ukraine, $26 billion to Israel, and $8 billion to the Indo-Pacific region. In total, the foreign assistance package totals $95 billion – which only passed after Speaker Mike Johnson cut a deal with Democrats in order to force it through by a vote of 311 to 112. The Senate is expected to pass the package, which was negotiated in conjunction with the White House, marking a victory against conservative lawmakers who insisted on protecting the US border before sending money abroad to protect those of other countries. “We cannot be afraid of our shadows. We must be strong. We have to do what’s right,” House Foreign Affairs Chairman Michael McCaul, a Texas Republican, said. Democrats and some Republicans waved Ukrainian flags during the vote, a rare moment of bipartisanship in a bitterly and narrowly divided House.

“Traditional House Republicans led by Speaker Mike Johnson have risen to the occasion,” House Democratic leader Hakeem Jeffries said. “We have a responsibility to push back against authoritarianism.” -Bloomberg. Earlier in the day, the House passed an $8 billion aid package aimed at countering Chinese aggression towards Taiwan, as well as a bill that would force Chinese-controlled ByteDance Ltd to divest from TikTok or face a US ban. The bill also allows for the confiscation of Russian dollar assets in order to help fund more assistance to Ukraine. Breaking down the Ukraine aid – of the $61 billion, $13 billion will replenish US stockpiles of weapons, and $14 billion will go towards US defense systems for Ukraine. $7 billion will go toward US military operations in the region. We assume the remainder will go directly to Ukrainian oligarchs.

The Israel bill, which passed by a vote of 366 to 58, includes $4 billion for missile defense. Notably absent was so much as a dime for the US border… “Nothing is done to secure our border or reduce our debt,” said Rep. Marjorie Taylor Greene (R-GA), whose outrage was shared with Reps. Thomas Massie of Kentucky and Paul Gosar of Arizona, who say they’re ready to boot Johnson from his Speakership. “Ukraine is not even a member of NATO,” Greene continued. Who would have known!

The history of corruption, that is.

• American Aid ‘Keeps History On Right Track’ – Zelensky (RT)

The decision by the US House of Representatives to allocate tens of billions of dollars to Kiev will bring Ukraine closer to a “just end” in its conflict with Russia, President Vladimir Zelensky wrote on X (formerly Twitter), thanking Speaker Mike Johnson for his support. The nearly $61 billion package approved on Saturday contains funding for the purchase of weapons and military equipment, as well direct financial assistance to Ukraine. Passed after months of delays and political wrangling, the bill next moves to the Senate, which already indicated in February that it will approve it.“I am grateful to the United States House of Representatives, both parties, and personally Speaker Mike Johnson for the decision that keeps history on the right track,” Zelensky wrote, suggesting that the aid will “keep the war from expanding,” and “save thousands and thousands of lives.”

“Just peace and security can only be attained through strength,” he wrote. Zelensky added that Ukraine “will undoubtedly use American assistance to strengthen both of our nations and bring a just end to this war closer.” Republican lawmakers had previously refused to back the bill, tying their approval to demands for better protection of the border with Mexico and a crackdown on illegal immigration. Kiev was forced to deal with increasing ammunition shortages after aid from the US – Ukraine’s biggest sponsor – began to dry up. Biden blamed Ukraine’s recent setbacks on the battlefield, including the loss of the strategic city of Avdeevka, on “congressional inaction.” Kremlin spokesman Dmitry Peskov called Saturday’s vote “predictable,” adding that it will “further enrich the US and further ruin Ukraine,” and “cause more Ukrainians to die because of the Kiev regime.”

“..very little change will be noted by those actually fightin..,”

• Who Gets What From Congress’ $61 Bln Bag of Goodies? (Sp.)

The House approved nearly $100 billion in assistance to Washington’s overseas allies, partners and client states on Saturday, with supporters of the aid managing to overcome opposition after a six-month deadlock in the chamber. Nearly $61 billion of the $95 billion from the proposed funding package is committed to fueling the conflict in Ukraine (at least $23 billion of that to be spent replenishing depleted US weapons stocks). Over $26 billion in additional commitments are made to Israel (nearly eight times what Washington normally sends Tel Aviv’s way in a given year). $8.12 billion is committed to stirring up tensions with China in Taiwan and the Indo-Pacific region more broadly. Passing the House, the aid package is now set to be voted on by the Senate, where leaders from both parties have been clamoring for months for the foreign assistance to be urgently passed. If it passes the Senate, the legislation will end up on President Biden’s desk for signature.

Supporters and opponents of the foreign aid package gave stirring speeches ahead of the Saturday’s House vote restating their positions. “I often say it’s never too late to do the right thing. But waiting to do the right thing comes at a cost,” Maryland Democrat Steny Hoyer said. “We saw that cost in Israel this week as an emboldened Iran launched an unprecedented attack on our ally. For Ukraine the cost of our inaction is great if incalculable. It is measured in Ukrainian lives, towns and territory lost…Today we act. We act to make it clear to the world that America is still the defender of freedom, democracy and international law.” Georgia Republican Representative Marjorie Taylor Greene, a staunch opponent of further US assistance to Ukraine, military or otherwise, proposed an amendment to slash support for Kiev to zero. “The United States taxpayer has already sent $113 billion to Ukraine, and a lot of that money is unaccounted for,” Greene said.

“The federal government continues to fund the military-industrial complex, and this is a business model that requires Congress to continue to vote for money to fund foreign wars. This is a business model that the American people do not support. They don’t support a business model built on blood and murder and war in foreign countries while this very government does nothing to secure our border. The American people are over $34 trillion in debt and the debt is rising by over $40 billion every single night while we all sleep. But yet nothing is done to secure our border or reduce our debt.” Pointing to polling indicating that a majority of Americans disapprove of new aid to Ukraine, Greene said Congress has chosen to vote to “protect Ukraine” instead of protecting “the American citizens that pay your paycheck.” “

Ukraine is not even a member of NATO. But the most important thing you hear in Washington, DC is that we have to send Americans’ hard-earned tax dollars over to Ukraine and keep the money going, to continue to murder Ukrainians, wipe out an entire generation of Ukrainian men…What kind of support is that? It’s repulsive,” the Georgia Republican said. The tens of billions of dollars in new US aid doled out via the legislation passed by the House Saturday may prolong the Ukrainian crisis, but won’t be able to secure a NATO victory in the proxy war against Russia, says former DoD senior security policy analyst Michael Maloof. “Now, the money that’s going to Ukraine for the most part will probably go to US defense contractors in various states, but to make newer equipment for our own stockpiles, which will then allow the US to unload older stuff for Ukraine,” Maloof told Sputnik.

“It’s not going to be enough for Ukraine to overcome its current geostrategic position at this point, simply because they don’t have a consistent ability to arm,” the observer added, pointing out that along with the weapons themselves is the ability to find the men to use them, something the Kiev regime is having increasingly severe difficulty doing as it is. “Other money to be provided to Ukraine is intended to pay government employees,” US Air Force Lt. Col. (ret.) Karen Kwiatkowski, a former DoD analyst, told Sputnik. “Thus presumably it will include meeting soldiers’ needs but it goes to Kiev bureaucrats first. Given how it will be allocated, very little change will be noted by those actually fighting,” Kwiatkowski believes, estimating that of the $61 billion allocated, $45 billion will remain in the US and $16 billion will be sent to Ukraine as so-called direct aid.

“Likely the $16 billion that makes it to Ukraine will be instantly absorbed to pay government bills rather than the war effort,” she said, pointing to Kiev’s massive budget deficit. “They have no means to undertake a counteroffensive, and just given the amounts of artillery that they burn through, what even the US is proposing probably wouldn’t last more than six months at best. And it’s undetermined what Europe is going to provide. So I think the Ukraine basically is over. It’s just a mop up [operation for] the Russians. And it’s just going to take time for that reality to sink in to Zelensky, who should begin considering getting out of there fast because I don’t think the country is going to politically last much longer,” Maloof said.

“If you vote to send our money abroad while waving a foreign flag, you’ll be called an American patriot. If you vote to keep our money at home to fund domestic priorities like the border, you’ll be called a foreign agent.”

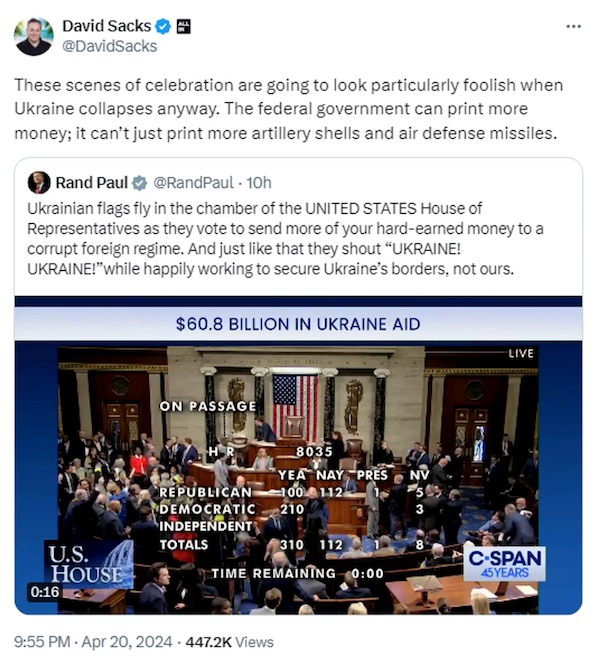

• David Sacks Warns Ukraine Will ‘Collapse Anyway,’ Despite Aid Bill (Sp.)

Previously, the US billionaire investor David Sacks underscored the need to “cut a deal” and seek a detente with Russia to avoid a third world war. He told a gala for the Republican think-tank American Moment in Washington that US involvement in the ongoing proxy conflict in Ukraine was only prolonging the standoff. The collapse of Ukraine is inevitable, despite the US House of Representatives having passed a foreign aid package that includes $61 billion in aid for Kiev, American entrepreneur David Sacks wrote on the X social media platform. “These scenes of celebration are going to look particularly foolish when Ukraine collapses anyway. The federal government can print more money; it can’t just print more artillery shells and air defense missiles,” the investor wrote, reacting to the jubilant scene in the House, where some of the lawmakers were seen waving Ukrainian flags. He continued by saying, “And I should have added, they can’t print more soldiers.”

The post by Sacks was in reply to a similarly deprecatory one by GOP Sen. Rand Paul of Kentucky, who posted footage from the House after the bill was passed, commenting that, “they vote to send more of your hard-earned money to a corrupt foreign regime. And just like that they shout ‘UKRAINE! UKRAINE!’ while happily working to secure Ukraine’s borders, not ours. The billionaire investor pointed out in his thread on X that, “It’s not “just” $61 billion. Ukraine will need massive annual cash infusions to stave off total defeat. So it’s $61 billion as the baseline for an annual appropriation in a new forever war.” He pointed out that the Iraq and Afghanistan wars also began with “annual appropriations in the $60B range. Those wars ended up costing trillions.” “Simple math,” the investor remarked, showed that the new funding bill could do no more than possibly buy Ukraine “precisely half of a Summer Counteroffensive.”

And, of course, everyone knows full well how that much-heralded counteroffensive attempt ended up last year – limited battlefield achievements coupled with massive manpower and hardware losses. According to Sacks, it is a bizarre world, where “If you vote to send our money abroad while waving a foreign flag, you’ll be called an American patriot. If you vote to keep our money at home to fund domestic priorities like the border, you’ll be called a foreign agent.” The entrepreneur recalled that according to US investigative journalist Seymour Hersh, “CIA Director Burns had to warn [Ukraine’s President Volodymyr] Zelensky to stop stealing so much money. His subordinates were angry that he wasn’t sharing the spoils.” “Do you think that problem has been resolved and Zelensky will share more this time?” queried David Sacks.

“Russia has been quite successful in its goal of ‘demilitarizing’ both Ukraine and NATO..”

• US Aid Bill ‘Insufficient’ for Ukraine’s Needs, Bolsters US Military (Sp.)

After more than 2 month of hard negotiations, the US House of Representatives has passed a multi-billion foreign aid package. However, the bill has sparked debate and criticism, with experts questioning its efficacy and allocation. David Pyne, a former US Department of Defense officer and executive vice president of Task Force on National and Homeland Security, offered a critical assessment of the aid package. He argued that the allocated funds are “woefully insufficient” for Ukraine’s wartime needs. The bill “will not change the outcome of the war which will inevitably end with a Russian victory and Ukraine being forced to accept Russia’s peace terms”, Pyne believes. Questions also arise regarding the distribution of the aid, since House Speaker Mike Johnson indicated that only a fraction, approximately $12-14 billion, would directly provide weapons to Ukraine.

However, Pyne raised concerns that a substantial portion, around 80%, would benefit US defense industries. He highlighted the potential for President Biden to utilize drawdown authority, enabling the redirection of additional funds from existing military stocks to Ukraine. Furthermore, Pyne shed light on Ukraine’s critical shortages of artillery shells and air defense missiles. He outlined Russia’s success in inflicting significant casualties on Ukrainian forces and emphasized the challenges in addressing Ukraine’s munitions deficits. “Russia has been quite successful in its goal of ‘demilitarizing’ both Ukraine and NATO, causing the US and its NATO allies to unilaterally disarm themselves of tens of thousands of its most modern weapon systems and transfer them to Ukraine”, stated Pyne.

Pyne highlighted the stark disparity between Russian and Ukrainian&NATO artillery capabilities, noting that “Russia produces over three times as many artillery munitions than all of NATO combined”. “Russian forces have been successful in inflicting half a million Ukrainian military casualties including about 250,000 killed in action and 250,000 seriously wounded with as many or more Ukrainian amputations over the past two years than France suffered… on the Western Front during World War One,” Pyne said. The assessment underscores the complexity of providing effective support to Ukraine amidst escalating conflict. As the aid bill moves forward, discussions surrounding its implementation, distribution, and broader geopolitical implications are likely to persist, as well as questions regarding US true purposes and intentions towards Ukraine as a nation.

“..the FBI had illegally used its surveillance powers against American citizens more than 278,000 times in a 12-month period..”

• US Lawmakers Approve More Government Spying (RT)

The US Senate has passed legislation renewing and expanding an expiring law that enables the government to conduct warrantless surveillance of Americans under the guise of protecting them from foreign threats. The bill was approved by a 60-34 vote in the early morning hours of Saturday, authorizing a two-year extension of the so-called Section 702 program of the Foreign Intelligence Surveillance Act (FISA). President Joe Biden is expected to quickly sign the legislation, renewing the spying tool after it expired at midnight on Saturday. Section 702 is ostensibly about surveilling the communications of foreigners for intelligence purposes, including detection of possible terrorist plots against the US. However, many of the phone calls and messages that are tapped by Washington’s spying apparatus occur between foreigners and US citizens.

The FBI has accessed the 702 database of intercepted communications to investigate targeted Americans, such as Black Lives Matters activists, journalists, members of Congress, political donors, and possible participants in the January 2021 US Capitol riot. Such searches normally require investigators to secure a warrant, meaning a court has found probable cause to suspect that the targeted person has committed a crime. Critics of the program had demanded that reforms be made before renewing Section 702 to protect US citizens from unconstitutional spying. A 2023 investigation by the US FISA court found that the FBI had illegally used its surveillance powers against American citizens more than 278,000 times in a 12-month period. Congress voted down an amendment that would have required warrants for probes of communications involving Americans.

“Section 702 has been abused under presidents from both political parties, and it has been used to unlawfully surveil the communications of Americans across the political spectrum,” said Kia Hamadanchy, senior policy counsel at the American Civil Liberties Union. “By expanding the government’s surveillance powers without adding a warrant requirement that would protect Americans, the House has voted to allow the intelligence agencies to violate the civil rights and liberties of Americans for years to come.” Senate Majority Leader Chuck Schumer (D-New York) hailed the fact that the FISA program was reauthorized “in the nick of time,” just as it was expiring. Senator Marco Rubio (R-Florida) said that failure to renew the spying powers could cause US officials to “miss a key piece of intelligence,” such as a threat to American troops stationed overseas or a potential terrorist attack.

Senator Rand Paul (R-Kentucky) lamented the fact that lawmakers declined to pass his amendments to the FISA bill, which would have enabled the government to continue spying on foreigners while protecting the civil liberties of Americans. His proposal was voted down by an 82-11 margin. “We could have ensured both constitutional rights and national security were protected,” Paul said. “Yet again, the Senate was asked to consider the question: ‘Can liberty be exchanged for security?’ And sadly, the majority of senators said, ‘Yes, it can.’”

“..lack of control [by the owners] over assets is not a good basis of any currency.”

• US Confiscation of Russian Assets Will ‘Supercharge’ De-Dollarization

On Saturday, the US House of Representatives passed the cheekily-named REPO Act, which would enable US President Joe Biden to confiscate roughly $6 billion in frozen Russian assets held in US banks and send it to Ukraine.The provision is part of a package bill that also includes over $95 billion in aid to Ukraine, Israel and the Indo-Pacific, as well as a potential TikTok ban.The bill is expected to pass in the Senate and then be immediately signed by US President Joe Biden. While the $6 billion represents only a fraction of the more than $300 billion in Russian assets frozen by the G7 countries in 2022, most of that money is held in Europe and US lawmakers hope that it will encourage European lawmakers to do the same.

“We’re making good progress in how to access that funds on an agreed basis that I think we can take forward to the G7,” UK foreign minister David Cameron, whose government has already come out in support of seizing Russian assets, told reporters earlier this month. The decision to confiscate Russian assets and provide them to Ukraine represents a major escalation in the West’s sanction war against Russia. However, the move is short-sighted by the US because it will accelerate global de-dollarization, which will remove one of the most powerful tools the US has.

“It’s reinforcing the need to de-dollarize on the part of any third-party country. Be it Russia, be it China – be it anybody else, including any country in the G-7 that may be marginally supportive of the United States. This is pure and simple economic blackmail,” Paul Goncharoff, an analyst and management consultant at Dezan Shira & Associates in Moscow told Sputnik. “Now they’re wondering ‘Am I putting it into something that will be seized or frozen?’ So lack of control [by the owners] over assets is not a good basis of any currency.” “So it just supercharges de-dollarization. And that’s not good, especially when you have an America that is used to living on larger and larger debt raised by people placing the trust and buying treasuries and bonds,” Goncharoff added.

“The drones’ accuracy exceeds 90%, the NYT said, adding that they are also capable of hitting heavy armor in its weakest spots..”

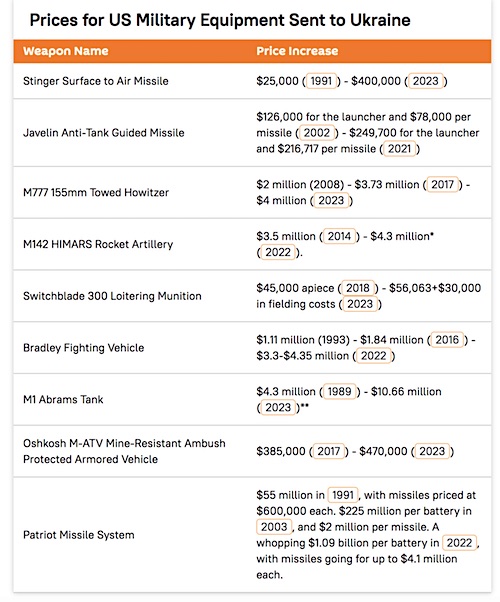

• $500 Russian Drones Destroying $10,000,000 American Tanks – NYT (RT)

Expensive American M1 Abrams tanks delivered to Ukraine are increasingly falling prey to Russian drones that cost only a fraction as much, the New York Times reported on Saturday. Even “one of the most powerful symbols of American military might” is not invulnerable to such attacks, it said. At least five US-supplied tanks out of the 31 provided by Washington have already been destroyed by Russia, the American media outlet said, adding that three others had been “moderately damaged.” In most cases, the tanks have been destroyed by first-person-view (FPV) kamikaze drones, also known as loitering munitions. Such drones are capable of actively maneuvering before hitting their target.

In at least one instance, though, an Abrams tank was taken out in a duel against a Russian T-72B3 main battle tank. The Russian military has published upwards of a dozen clips, mostly taken from drones, showing the destruction of US-supplied equipment. According to the NYT, the tanks turned out to be “more easily taken out by exploding drones than some officials and experts had initially assumed.” The media outlet cited an Austrian historian and military expert, Colonel Markus Reisner, who described such a situation as “unbelievable.” The paper also described the Russian UAVs as “highly-accurate, low-cost tank killers.”

The drones’ accuracy exceeds 90%, the NYT said, adding that they are also capable of hitting heavy armor in its weakest spots. The UAVs “can cost as little as $500,” the paper reported, are capable of “taking out a $10 million Abrams tank.” The paper also admitted that there was no “easy, or single” way to defend a tank against a drone attack. US-made Abrams tanks made their long-expected appearance on the front line in late February amid the Ukrainian effort to halt advancing Russian troops after the capture of the Donbass town of Avdeevka. A batch of 31 M1 Abrams tanks was pledged to Kiev early last year, ahead of the ultimately disastrous Ukrainian counteroffensive. The delivery was made in full only by mid-October, when the ill-fated push had already largely been exhausted.

“The United States government for so long now, hasn’t seen a war they didn’t want to be a part of.”

• ‘Pariah’ Israel Dragging US ‘Into Garbage Bin of History’ (Sp.)

On Friday, the US vetoed granting Palestine full membership in the UN, which was promised to the Palestinians in 1948 when the state of Israel was created. The US has been Israel’s strongest supporter in the UN, previously vetoing three ceasefire resolutions before finally allowing a fourth to pass through abstention last month. Earlier, Israel struck Iran in response to Iran’s attack last week, which was itself a response to Israel attacking Iran’s consulate in Damascus earlier this month. The attack, which was described by both sides as minor, came after Israeli PM Benjamin Netanyahu said Israel would not respond until after Passover, which runs from April 22 to April 30. Israel’s apparent insistence on launching a regional war in the Middle East is dragging the United States with it “Into the garbage bin of history,” and US lawmakers seem willing to watch it happen, journalist Esteban Carrillo, the head of news at The Cradle, told Sputnik’s Political Misfits on Friday.

While discussing the recent US vote against Palestinian statehood in the UN, Carrillo explained that it is working against US interests “It’s completely a case of the tail wagging the dog. And US politicians just seem so content to just go along with it,” he explained. “What does Netanyahu have over the heads of these people? Because it doesn’t seem like they are even willing to consider at this point stepping away from this pariah that is just dragging them down into the garbage bin of history.” Tensions between Iran and Israel seem to have cooled somewhat after Israel’s attack was so minor. Explosions were heard near an Iranian base outside of Isfahan, but Iran claimed there was no damage or injuries. A second attack against the city of Tabriz was likewise thwarted.

The attack, which Iran claims came from within its own territory, seemed designed to make Israel not appear “as weak as they are,” Carrillo explained. “After six months of flattening Gaza and killing tens of thousands of Palestinians, they have failed to achieve a single strategic objective against Hamas.” However, the small scope of the attack also seemed designed to allow Israel to “play tough guy” without igniting a larger conflict. “Iran’s response over [Friday morning’s] attack is essentially summed up in ‘what strike? What happened? Our air defenses took everything down,’” said Carrillo. But that doesn’t mean Israel is finished. Israeli Prime Minister Benjamin Netanyahu is still determined to keep the war going to ward off political and legal challenges facing him. “I don’t think that we’re out of the water yet in terms of [Israel] dragging the United States into a regional war,” Carrillo explained, adding earlier that it isn’t hard to convince US lawmakers to join fights. “The United States government for so long now, hasn’t seen a war they didn’t want to be a part of.”

‘A vote for Trump is a vote for Putin’ – Hillary Clinton. Yawn…

• Trump Wants To ‘Kill His Opposition’ – Hillary Clinton (RT)

Former US presidential candidate Hillary Clinton has claimed that the man who defeated her in the 2016 election, Donald Trump, is a wannabe strongman who aims to murder his political enemies. Speaking in a podcast interview posted on Friday by Democrat activist Mark Elias, Clinton said American voters had underestimated how “dangerous” Trump would be as president. She likened Trump, now the presumptive Republican nominee in this year’s US presidential election, to Russian President Vladimir Putin. “Putin does what [Trump] would like to do – kill his opposition, imprison his opposition, drive journalists and others into exile, rule without any check or balance,” Clinton said. “That’s what Trump really wants.” Ironically, Clinton and her husband, former President Bill Clinton, have themselves long been accused by some conservatives of eliminating people who pose a threat to their power or wealth.

In fact, investigative journalist Danny Casolaro coined the conspiracist term “Clinton Body Count” in the late 1980s, in reference to the allegedly mysterious deaths of people with connections to the Clintons. Casolaro was found dead in a West Virginia hotel room in 1991 with his wrists slashed 10-12 times. His death was ruled a suicide. Hillary Clinton also has made a habit of linking Trump to Russia and Putin. Her presidential campaign helped trigger allegations of Russian meddling in the 2016 election by funding the since-discredited Steele dossier. She told Elias that Putin is just one of the US adversaries whom Trump would like to emulate, and that his other role models include Chinese President Xi Jinping and North Korean leader Kim Jong-un.

“We have to be very conscious of how he sees the world because in that world, he only sees strongman leaders,” Clinton said. “He sees Putin. He sees Xi. He sees Kim Jong-un in North Korea. Those are the people he is modeling himself after, and we’ve been down this road in our world history. We sure don’t want to go down that again.” If Trump is elected president again, Clinton warned, “it will be like having a dictator. I don’t say that lightly. Go back and read Project 2025. They’re going to fire everybody. The person in the government who knows about what may be the next pandemic? ‘Get rid of him, he didn’t vote for me, or I don’t like the way he looks.’”

She added: “It’s really important to think about what could happen to our world with Trump back in the White House – withdrawing us from NATO, not caring about what happens in Europe… the idea that he wants Ukraine to fail, the idea that he doesn’t want us to be able to surveil our enemies. I mean, this is a very scary prospect.” Clinton expressed optimism that Trump will not be able to defeat incumbent President Joe Biden in November because Democrats will be running the election in key states, including Michigan, Wisconsin, Pennsylvania, and Arizona. Trump has maintained that all allegations against him are part of a politically motivated smear campaign. He dismissed the ‘Russiagate’ accusations as a hoax and witch hunt that aimed to sabotage his presidency and block him from forging better US relations with Russia.

NEW: Hillary Clinton unironically says that Donald Trump wants to "kill his opposition" as she rants about how compassionate Joe Biden is and how evil Trump is.

Remarkable.

The twice-failed presidential candidate, who failed to mention how her party is weaponizing the… pic.twitter.com/O2nNHbyHuL

— Collin Rugg (@CollinRugg) April 20, 2024

“Where there is no vision, the people are lost..”

• Texas Is a Fading Conservative State (Paul Craig Roberts)

Americans regard Texas as a Conservative state. It is not. The conservatism is only skin deep. The conservatism is limited to a small majority of the people. Professional organizations, such as the Bar Association, many city governments, the universities, and the public schools have been infiltrated and taken over by woke liberals. Texas universities are as crazed, corrupt, and anti-American as those in the Northeast and on the West coast. They serve the same agendas, such as indoctrinating white people that they are racist, legitimizing sexual perversity, redefining American patriots as Nazis and Trump Deplorables. The public schools teach that white people are racists and confuse kids about their gender. The Bar Association uses law as a weapon against Republicans, such as attorney Sidney Powell.

The Texas Bar Association disciplined Sidney Powell, first convicting her of misconduct and fraud for filing lawsuits challenging fraudulent vote counts in the 2020 presidential election, and revoking her license as punishment. The state appeals court found that the bar association had convicted her on the basis of zero evidence. It was just a vendetta by woke liberals devoid al all integrity against a Republican.This is America today. In the hands of blue cities and states and in the US Department of Justice (sic) law as law no longer exists. Neither does the US Constitution. What exists is a weapon to be used against Trump Republicans and dissenters from official narratives.

In America there are two systems of law. One system located in red states is a rule of law. The other in blue states is a system of law as a weapon to destroy opponents. We see this clearly in blue NY and blue Atlanta where show trials devoid of any evidence are being conducted against President Trump. We see it in the Justice (sic) Department’s continuing misuse of law to force attendees at the January 6 rally to incriminate themselves by pleading guilty in order to avoid a 20-year prison sentence for exercising their constitutional right to protest.

The totally corrupt Biden Regime has an open border policy for the explicit purpose of turning red states into blue ones by filling them with millions of immigrant-invaders in order to overload the voting rolls with Democrat voters. The Democrats assume that they have purchased the loyalty of the immigrant-invaders by allowing them in and supporting them on public welfare while giving them work permits so that they can underbid the employment of American citizens. Evidence was recently provided that Biden has flown at public expense 360,000 immigrant-invaders into Florida, and evidence was provided that the Biden regime has funded the Jewish NGO that is recruiting world-wide immigrant-invaders with $300,000,000. American citizens are helpless, because almost half of them are so utterly stupid that they vote for their own self-destruction by voting Democrat.

“..Harari deserves credit for blood-curdling honesty, if not for the morality of his and his masters’ “visions.”

• A Collective “Common Enemy” Now Stalks Mankind (Karganovic)

Yuval Hariri, Klaus Schwab’s spokesman, recently made a statement that should send chills up everyone’s spine. “If bad comes to worse and the Flood comes,” Harari said, he and the likeminded cabal of shadowy world masters will “build an Ark and leave the rest to drown.” Elsewhere, Harari elaborates on the reasons for his fellow elitists’ cold-hearted indifference to the fate of the vast majority of Earth’s inhabitants: “If you go back to the middle of the 20th century …and you think about building the future, then your building materials are those millions of people who are working hard in the factories, in the farms, the soldiers. You need them. You don’t have any kind of future without them.” What he means is that you – referring to the dominant social and financial elites of that era – still “needed” the labour of millions in the various fields of economic endeavour in order to turn a profit.

Since then, how have things changed according to “futurologist” Harari? “Now, fast forward to the early 21st century when we just don’t need the vast majority of the population, because the future is about developing more and more sophisticated technology, like artificial intelligence [and] bioengineering, most people don’t contribute anything to that, except perhaps for their data, and whatever people are still doing something useful, these technologies increasingly will make them redundant and will make it possible to replace those people.” Elitist mouthpiece Harari deserves credit for blood-curdling honesty, if not for the morality of his and his masters’ “visions.” He is plainly signalling the view that this writer, the editors of this portal, its readers and the rest of mankind are expendable and apart from whatever economic utility they still might possess are bereft of any inherent dignity or value.

Harari and his immediate superior in the elitist nomenklatura, Klaus Schwab, technically are private individuals. Their organisational vehicle, the World Economic Forum, is a private NGO registered in Switzerland. Formally, they neither represent nor do they speak for any government or official structure with a proper claim to legitimacy. They have no licence to plan or arrange the future of humanity, beside the self-authorisation to do so which they and the oligarchical globalist power centres they commune and mingle with have arrogated to themselves. No one elected or empowered them to plan anybody’s future, other than their own, and even that strictly in their private capacity.= Yet disposing of the future of mankind is precisely what they presume to do, in Davos in plenary session once a year and the rest of the time in conspiratorial confabulation amongst themselves.

Catfish

https://twitter.com/i/status/1781592640623886517

Horses dolphins

https://twitter.com/i/status/1781559109487124859

King

Elephant shows Lions who the real king of the jungle is. pic.twitter.com/80PpaADOSn

— Nature is Amazing ☘️ (@AMAZlNGNATURE) April 19, 2024

Octopus

https://twitter.com/i/status/1781604985345606000

Resting sharks

https://twitter.com/i/status/1781720652241846625

Reflex

The incredible reflexes of this deer pic.twitter.com/8wHpWxNyPc

— Nature is Amazing ☘️ (@AMAZlNGNATURE) April 20, 2024

Piggy bank

"Give me a piggy bank ride please!"

"Dude you're an elephant…" pic.twitter.com/Z0FV78g7FA

— Nature is Amazing ☘️ (@AMAZlNGNATURE) April 19, 2024

Great white

This is when Ocean Ramsey and her team encountered what is possibly the largest great white shark ever recorded, approximately 6 meters long (~ 20 feet).https://t.co/qkA1XqqqiG

— Massimo (@Rainmaker1973) April 20, 2024

Rhino

Rhino: you okay?

Dog: sir this is the most terrifying moment of my life pic.twitter.com/DFpB14m3PS

— Nature is Amazing ☘️ (@AMAZlNGNATURE) April 20, 2024

Aquarium

https://twitter.com/i/status/1781745912303251759

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.