Esther Bubley Greyhound bus at Washington Court House, Ohio Sep 1943

You know they’re desperate when they play the royal card and announce a new baby on the way. Britain, and especially Downing Street 10, got a huge scare last week when a poll showed the Scottish independence movement is now favorite to win the September 18 referendum. It’s not entirely clear, but I don’t think Cameron and his crew would be able to stay on if Scotland secedes from the UK.

So who would do the negotiations for what remains united under the Queen? That’s the first bit of confusion and mayhem I very much hope will turn into an absolute mess that will break the EU and the eurozone as they presently exist. Simply because something needs to be the catalyst that makes it happen.

Brussels has turned into a convoluted monstrosity that makes far too many victims just to allow a few handfuls of people with extreme and contorted power dreams to ejaculate. The EU is way past its best before date, and the rot and decay can only possibly lead to more victims if it isn’t halted.

It was a nice idea 60-odd years ago, but it’s fallen into the hands of the wrong cabal, and when you look at how things have evolved during that time, it’s not that hard to recognize the entire set-up was doomed to lead where it has. There was never any positive feedback built into the system, i.e. Brussels was handed more power all the time as time went by, until it became more powerful than its member states (with the possible exception of Bonn/Berlin).

It has become self-propelling, for the simple reason that it was built that way. An ideal opportunity for psychopathic schemers to live out the fantasies such people have, and which they will live to the fullest unless they’re kept in check. The same thing that’s painfully evident in places like Washington or Beijing.

Only with even less democracy. Voters in European nations may still have a token influence through their national ballot boxes, but the big decisions are made in Brussels. And all the politicians they get to choose from, at least those in the parties that matter, all support the EU project, more often than not because they too dream of centralized power.

There is no longer a choice available to reject Brussels, or reject the Euro, or reject what either the ECB or the European Commission – both of which are extremely ‘light’ on democracy – dictate. That’s the heart of the European problem, and that’s what will finish it off. Only, if that last bit takes too long, it will cause a lot of additional damage throughout the EU.

It’s a project with its own demise built in. A good idea with a fatally defective architecture. As always, nobody notices in times of plenty and abundance. But when those proverbial ‘seven years’ have gone, people won’t want to belong to some larger block anymore; when the alleged advantage of the bigger unity has evaporated, people don’t want their decisions to be made by someone they don’t know and who doesn’t speak their language or know their culture.

But according to Brussels, and to all the national politicians who support the EU project, there is now no longer a way back. The euro can’t be undone, and neither can the EU. The narrative is that Brussels must, of necessity, absorb ever more power from national governments, and hence ever more power from the people they represent, and that’s exactly the way the entire monstrous project was constructed. Perhaps not intentionally, but still.

Point in case: the EU is set to announce new sanctions against Russia, still based on zero evidence about anything at all, and the best part is they seek to hurt the oil industry but not the gas industry, because they need the latter. And what’s going to keep Russia from saying if you want one you must take both? What would keep Moscow from closing its airspace to EU airlines and bankrupting a whole series of them? In Brussels, arrogance, hubris and stupidity are in a fierce battle for first place.

Scotland is the first EU region to try and break free from a larger entity, and, oh sweet irony, many of the pro-independence Scots will vote Yes because they like the EU so much (or at least more than the UK presently does). But let’s not let a bit of irony get in the way, shall we?

If only because a win for the Yes side has the potential to cause so much disruption it won’t matter what caused the disruption. The Yes side wants to be part of the CTA, which allows free flow of people between England and Scotland, no passports etc. But whether that’s acceptable to the EU, or the UK, is doubtful.

The Yes side wants to keep using the British pound, in a scheme they call sterlingization, and there are tons of questions there as well. Will the UK allow it, will the EU, can you be an EU member when you use someone else’s currency, can you be without having your own central bank, plenty of delightful conundrums that so far nobody has provided a conclusive answer for.

If and when Scotland votes for independence 10 days from now, the confusion and mayhem and anger and bitterness will be the only things deemed worth talking about in Albion. Royal baby or not. But the whole thing will be resolved at some point, not to everybody’s whole content, and not with every politician still in the seats they occupy today, but one thing’s for sure: it will be a breath of fresh air that Europe desperately needs.

Because if Scotland can do it, so can Catalunya, and the Basque, and Venice, and so many other regions that would rather decide about their own future than have some ‘higher power’ do it for them. As is their right as per the UN charter on self-determination.

The EU has become a straight-jacket that restricts the freedom of far too many people, and they’re going to break free. It’s only a matter of time. Of course it more likely that the UK will opt to leave the EU than for Scotland to be put out on the curb, but that’s fine by me: what’s important right now is that somebody starts rattling the cage, and starts calling out for freedom. It’s inevitable that it will take place, and the sooner that happens the better, because we don’t want violent unrest to erupt.

In yet another twist of irony, I am most likely to see my wish of an EU break-up fulfilled by someone I have grave doubts about: Marine Le Pen of the Front National in France. She called yesterday on President Hollande – and his 13% approval rating – to dissolve parliament, and she leads in all the polls. Le Pen would take France out of the EU in only a few simple steps, and that would be the end, since without France there is no EU.

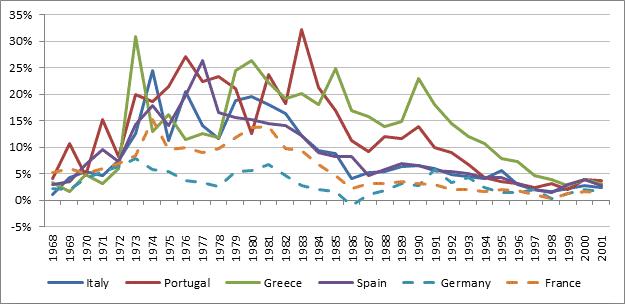

It’s for the people in Greece, Italy, Spain etc. that this is the most crucial. Until the moment that their countries break free of the Brussels shackles, their economies will continue to suffer, and so will they.

Unemployment numbers are still at insane levels there, debt levels are, if possible, even crazier, and there’s no way out because they are forced to live in a sort of Germany by the olive trees. All their ‘leaders’ since the crisis hit have been EU happy technocrats, who talk of reforms until the cows come home but do thing to alleviate unemployment numbers, undoubtedly the biggest problem around.

My point is, we need something that will lead to the dissolution of the EU as it exists today. And then all parties involved can go back to the drawing board. Some form of European cooperation is of course fine, and can be very beneficial, but not the one there is today.

So come on Scotland, help make it happen. We’re counting on you guys.

• New EU Sanctions to Stop Fundraising by 3 Russian Oil Giants (WSJ)

New European Union sanctions on Russia will expand the number of Russian companies unable to raise money in the bloc’s capital markets to include three major state-owned oil companies, according to documents seen by The Wall Street Journal. Under a modest expansion of sanctions introduced in late July, the three oil companies— Gazpromneft, the oil-production and refining subsidiary of OAO Gazprom, oil transportation company Transneft, and oil giant Rosneft—will be forbidden from raising funds of longer than 30 days’ maturity. Five state-controlled banks, including Sberbank and VTB Bank, already barred from raising funds for longer than 90 days under the July sanctions, will also have the maximum maturity cut to 30 days. The new sanctions are expected to be implemented Tuesday. They include for the first time a measure preventing the named companies from raising new bank loans in the EU of longer than 30 days’ maturity.

Three companies involved in military production—Oboronprom, United Aircraft Corp. and Uralvagonzavod—will also be barred from future EU fundraising. The sanctions will also bar new contracts for services needed for oil exploration and production in deep water, the Arctic or shale-oil projects. The restrictions will bar sales from the EU of so-called dual-use technologies—meaning they have both civil and military applications—to nine Russian companies providing services to the Russian military. The list includes electronic-optics company JSC Sirius, mechanical engineering company OJSC Stankoinstrument, and the small-arms manufacturer JSC Kalashnikov.

European leaders said late last week the new measures could be lifted if there were clear evidence that Moscow was helping forge a genuine political solution in Ukraine. According to an EU spokeswoman, that evidence would need to include permanent monitoring of the Russia-Ukrainian border, the withdrawal of illegal armed groups from Ukraine and of Russian forces illegally operating on Ukrainian territory. On Sunday, fighting in two Ukrainian cities called into question a cease-fire agreed to on Friday. The documents show the EU seeking to hit Russian oil companies, but leaving unscathed those involved in gas production and export, which are critical to many European countries’ energy supplies. They also make some exceptions for exports destined for the Russian space and civilian nuclear industries.

Read more …

Russia may close its airspace. Goodbye EU airlines.

• Medvedev: New Sanctions Against Russia May Provoke ‘Asymmetric Response’ (RIA)

New Sanctions against Russia in energy or finance sectors could trigger an asymmetric response from Moscow, such as closing its airspace, Russia’s Prime Minister Dmitry Medvedev told the Vedomosti newspaper in an interview released Monday. “It is them [the West], who should be asked whether there will be new sanctions. But if there are sanctions, linked with energy, [or] further restrictions on our finance sector, we will have to respond asymmetrically. For instance, [with] restrictions in transport area. We act on the premise of friendly relations with our partners, and this is why the sky above Russia is open for flights. But if we are restricted, we will have to answer,” Medvedev added.

The prime minister argued that certain Western airlines could go bankrupt in case they are banned to use Russia’s airspace. “But this is a bad option. I just would like our partners to realize it at a certain moment. Especially, [considering the fact] that the sanctions do not help to establish peace in Ukraine. They miss [beside the mark], and an absolute majority of the politicians understand it. There are just an inertness of thinking and, unfortunately, the will to use force in international affairs,” Medvedev stressed. Earlier, a number of European politicians told RIA Novosti that Brussels would introduce a new wave of sectoral sanctions against Russia on Monday. Late July, the European Union and the United States imposed restrictions against Russia’s oil and banking sector over Moscow’s stance in the Ukrainian internal conflict. In response, Russia banned certain food products importation from the Western nations, which introduced anti-Russian sanctions.

Read more …

• Four NATO Allies Deny Ukraine Statement On Providing Arms (Reuters)

A senior aide to Ukraine’s President Petro Poroshenko said on Sunday that Kiev had agreed at the NATO summit in Wales on the provision of weapons and military advisers from five NATO member states, but four of the five swiftly denied any such deal had been reached. NATO officials have previously said the alliance will not send arms to non-member Ukraine, but have also said individual allies may do so if they wish. A NATO official contacted by Reuters on Sunday on the Lytsenko comment reiterated this policy. “At the NATO summit agreements were reached on the provision of military advisers and supplies of modern armaments from the United States, France, Italy, Poland and Norway,” Poroshenko aide Yuri Lytsenko said on his Facebook page. Lytsenko gave no further details. He may have made his comment for domestic political reasons to highlight the degree of NATO commitment to Ukraine and to its pro-Western president.

A senior U.S. official, speaking on condition of anonymity, denied that the United States had made such a pledge. The official told Reuters, “No U.S. offer of lethal assistance has been made to Ukraine.” Asked about Lytsenko’s comments, defence ministry officials in Italy, Poland and Norway also denied plans to provide arms. In France, an aide at the Elysee palace declined to comment. “This news is incorrect. Italy, along with other EU and NATO countries, is preparing a package of non-lethal military aid such as bullet-proof vests and helmets for Ukraine,” an Italian defence ministry official told Reuters. Norwegian Defence Ministry spokesman Lars Gjemble, speaking to the NTB news agency, said, “We’re participating with staff officers in two military exercises in Ukraine, but it’s not correct that we’re delivering weapons to Ukraine.”

Read more …

Fools.

• US, Ukraine Start Black Sea Naval Exercises (Eurasianet)

United States-led, Ukraine-hosted naval exercises will start this week in the Black Sea, ahead of NATO exercises in Western Ukraine later this month. While both exercises are iterations of annual drills and so not directly in response to the events in Crimea and eastern Ukraine, the fact that they’re going ahead is nevertheless a signal of U.S. support for Kiev. The naval exercises, Sea Breeze, are usually held in July but were put off until September this year. They’ll be led by the U.S. destroyer USS Ross and also include ships from Ukraine, Georgia, Romania, Turkey, Canada, and Spain.

One apparent concession to the heightened tension in the region this year: unlike in previous years, no U.S. or NATO ships will dock in Ukraine this time. “Much of the exercise will focus on maritime interdiction operations as a primary means to enhance maritime security,” announced U.S. European Command in a statement. “The other key components of the exercise focus on communications, search and rescue, force protection and navigation.” Ukraine’s navy was in a woeful state before the current crisis; since then its main base at Sevastopol was annexed by Russia, its commander defected to Russia, and many of its ships were seized by Russia. In that context, this sentence from the U.S. statement could be interpreted in various ways: “Leaders from Ukraine and the U.S., co-hosts for the 13th iteration of the exercise, share sentiments about the progress of both the exercise and maritime security in the Black Sea that have occurred since the exercise’s inception.”

One wonders about Ukrainian leaders’ sentiments about “progress” in Black Sea maritime security… No Russian official appears to have commented directly on the exercise, but RIA Novosti writes: “Sea Breeze exercises by NATO forces began in 1997, and have often been met with hostility by anti-NATO political forces in Ukraine. NATO has been flexing its muscles near the Russian border since Crimea’s reunification with Russia in March. Moscow has repeatedly expressed concern over Western pressure on Russia.” The exercises are scheduled for September 8-10

Read more …

Sheehan’s piece is as well-documented as it is frightening.

• Sell Financial Stocks and Bonds: The Fed’s Illegal Seizure Of AIG (Sheehan)

Reserve Your Seats: On August 26, 2014, for what seems the fiftieth time, the U.S. Court of Federal Claims rejected the U.S. government’s attempt to extinguish Starr International Co. v. United States. Judge Thomas Wheeler said the case brought by Hank Greenberg’s AIG (specifically, Starr International Co., which owned 12.5% of the shares on September 15, 2008) will go to trial on September 29, 2014. Wheeler stated: “The complexity of the submissions and the factual disagreements strongly point to the need for a trial.” According to Reuters, “a U.S. Department of Justice spokeswoman declined to comment.” On the other hand, David Boies, the Attorney of Record from Boies, Schiller & Flexner, LLP, representing Starr International, did comment: “The decision speaks for itself.” Former AIG Chairman Hank Greenberg has sued the U.S. government for $25 billion as compensation for the shares owned by Starr International. According to Reuters, “The trial is expected to last six weeks.”)

The news sounds reassuring: “U.S. bank regulators plan to adopt rules on [September 3, 2014] forcing big banks to hold more assets that they could sell easily in a credit crunch, a requirement that is closely linked to the experience of the 2007-2009 financial crisis.” It is possible the rules will work. However, no formula will capture rising or falling confidence in a financial company at some future date. We are vectoring towards another 2008. Confidence, on the part government and Federal Reserve officials, financial institutions, and the public, are intertwined. When financial institutions are afraid to lend to each other liquid assets will be held for dear life.

There are two topics in store. First, changes to financial institution bankruptcy law may prompt a bank run. Second, depositions in Starr International Company, Inc. v. United States should awaken investors to our “policy makers” disintegration when we needed a leader. (It is significant when the bureaucratic meritocracy rose to positions of leadership, it changed its role to that of “policymakers.” That it did not and does not want to lead is the reason it is spent.) In the discussion about financial institution bankruptcy (topic number one), it is well to keep in mind consequences are magnified by topic number two. As a footnote, it is inconceivable the government and Fed models, such as those used to calculate the September 3, 2014, bank liquidity rules, include an exponential factor that kicks in when the combined worries of a Dodd-Frank “call” and a heavy-handed government rescue mission hit simultaneously. [..]

Given the cleavage from reason by our policy makers (one last, irresistible Fact: no one from AIG was allowed in the room during its nationalization), consider: (1) interests you may hold in financial institutions and (2) Paul Singer’s description of the now legal means to redistribute those interests. Financial firms are more leveraged than is generally understood. Sell their securities.

Read more …

And this is why.

• Fed Seeks to Calm Congress Demand for More Oversight (Bloomberg)

Federal Reserve Chair Janet Yellen has tried to repair damaged relations with Congress during her first seven months in office. The fix-up isn’t going very well. Republicans on the House Financial Services Committee started the year promising a series of inquiries into the nation’s central bank. New legislation aimed at reducing the Fed’s discretion on monetary policy and bank supervision has been proposed. A bipartisan group of 15 House and Senate members sent a letter to the Fed, asking it to clarify how it would use its emergency lending authority in another crisis. The efforts signal growing discomfort with policy makers’ unusual reach in financial markets and their expanding regulatory powers.

The Fed is “moving into new territory,” said Representative William Huizenga, a Michigan Republican, whose exchange with Yellen at a July 16 hearing turned tense, as each briefly spoke over the other. “They don’t feel like they need to explain it to us.” Yellen has worked hard at reconciliation after relations soured under her predecessor, Ben Bernanke. His unprecedented actions during the financial crisis – including an $85 billion rescue of insurer AIG — raised concerns the central bank was growing too powerful while resisting scrutiny of its actions. She sat for more than five hours of testimony at her first semi-annual appearance before the House committee and has supported changes, at the request of Democrats, in the way the Fed handles enforcement actions.

Still, interviews with members of Congress and their current and former staff show the distrust that sprouted during the crisis has taken deep root, especially among Republicans, who could have a Senate majority after November’s mid-term elections. Some legislators say the Fed has confused its independence on monetary policy with independence from their oversight, an attitude they resent. Huizenga’s office said the Fed recently took six months to respond to questions on the Volcker Rule, which limits risky trading by banks. “Getting ignored on the legislative side and then being beaten about the head any time you want to question what they are doing – it’s an arrogance that comes out there that is stunning,” he said.

Read more …

• Eurozone Faces Another Recession As Investor Confidence Plunges (Telegraph)

A key gauge of euro area confidence saw a “collapse” this month, as efforts to revive the currency bloc failed to excite investors. Falling to its lowest level in over a year, both components of the Sentix Investor Confidence index – assessing the current situation and investors’ six-month expectations – were both in negative territory. The headline reading dropped to 2.7 to -9.8 in September, while analysts had expected to see just a slip in confidence, to 2.0. Sebastian Wanke, senior analyst at Sentix, said that “this constellation signals a renewed recession for the eurozone”. Last Thursday the European Central Bank (ECB) slashed three of its key interest rates, and announced plans to deploy a new stimulus package.

Mario Draghi, president of the ECB, unveiled a scheme to purchase asset-backed securities (ABS), including mortgage bonds, in an attempt to revive the flagging economy. Mr Wanke said that the reading “is all the more noteworthy as during Mr Draghi’s presidency the ECB has managed on several occasions to turn round investors’ economic expectations. Now, this does not seem to work”. Eurozone growth ground to a halt in the second quarter, statiscians confirmed on Friday. Meanwhile annual inflation remains well below the ECB’s target of just under 2pc, falling to a five-year low of 0.3pc in August. Frederik Ducrozet, of Crédit Agricole, questioned whether the Sentix reading pointed to a recession. He tweeted that the gauge was “a market-based indicator with little macro content”.

Read more …

• What Would Independence Really Mean For Scotland’s Economy? (Guardian)

Alistair Darling seems to be a sucker for punishment. He was chancellor of the exchequer on the blackest day of the global financial crisis in the autumn of 2008, when the Royal Bank of Scotland was forced to tell the government that its cash machines would run out of money within three hours. Six years on, Darling has another exceptionally tough job: fronting the campaign seeking to prevent Scotland voting for independence on 18 September as the polls show support for his side slipping. In a faint echo of those turbulent days after the collapse of Lehman Brothers, the City has woken up to the possibility that the Scots will decide to go it alone. Sunday’s YouGov poll for the Sunday Times showing the first ever lead for yes – albeit at 51% to 49% – should clarify thinking further. The Bank of England has begun to draw up contingency plans to cope with the potential fallout from the end of a union that has lasted for more than 300 years.

On the estates of Glasgow, where Iain Duncan Smith once came to outline his vision for welfare reform, supporters of independence are telling people who haven’t voted since Margaret Thatcher used them as guinea pigs for the poll tax that they have the chance to be rid of the Tories for ever. The narrowing polls raise the prospect of a divorce that could be long, complex and bitter. The pound has been coming under pressure as it has become clear that the race is rapidly becoming a far closer call than anyone but diehard Scottish nationalists had ever envisaged. “In some ways it is a bigger challenge than 2008,” Darling says during a visit to Aberdeen. “This is about the future of the country in which I live. I don’t want to take a leap into the unknown.”

Clearly not all Scots see it that way. Many say they are taking the leap with their eyes wide open. They have been told by George Osborne and Ed Balls that there is no possibility that an independent Scotland could forge a monetary union with the rest of the UK. They have been told by the country’s acknowledged oil expert, Sir Ian Wood, that the reserves of oil may not be as plentiful as previously thought. They have been served notice by some big employers that they will up sticks and leave in the event of a yes vote. But Dave Moxham, deputy general secretary of the Scottish TUC, says: “The direction is only one way. And that is from undecided voters to yes. Whether it will be enough to win I am not sure, but it is a noticeable trend.” John Swinney is the Scottish National party’s answer to Darling: calm, cautious, a safe pair of hands. Sitting in Yes Scotland’s HQ in Hope Street, Glasgow, he puts the case for independence in one short sentence. “I think we will make a better job of running the country ourselves rather than having decisions made by the UK government.”

Read more …

• London Press Reflects Panic At Scottish Poll (Guardian)

Suddenly, Scottish independence is front page news for the London-based national press. The narrowing of the polls has concentrated editors’ attention as never before. The splash headlines of the Daily Telegraph (“Ten days to save the Union”), the Independent (“Ten days to save the United Kingdom”) and the Guardian (“Last stand to keep the union”) convey the mounting sense of panic about the possibility of the Yes side winning the vote on 18 September. The Times’s splash, “Parties unite in last-ditch bid to save the Union”, reports that “David Cameron and Ed Miliband will unite this week” in order to back “a government paper that commits to handing more powers to Scotland within days of a ‘no’ vote.” Three tabloids play the royal card: “Queen’s fear over break up of Britain” (Daily Mail); “Don’t let me be last Queen of Scotland” (Daily Mirror); and “Queen’s fears for Britain’s break-up” (Daily Express). Metro reminds its readers of a central bone of contention between the two sides: “No, we will NOT share the pound”.

And the Sun? Well, as you might expect, it manages to find a pun: “Jocky horror show”. (But it must take the subject seriously because it has not run its usual topless page 3 girl). The panic page 1 headlines are echoed in leading articles. The Telegraph’s full-length editorial concedes that “it is now at least conceivable that a fortnight from today negotiations will be under way to administer the break-up of the United Kingdom.” It believes Alex Salmond’s “appeal to national sentiment has superseded the anxieties many Scots felt when confronted with concerns about their ability to make their way in the world economically… with 10 days to go, the final appeal – as Mr Salmond intended it should be – is to the heart and not the head.” The Telegraph attacks Labour for “a desperate 11th-hour attempt to shore up the house they helped undermine” and contends that it is “incumbent upon Labour, who have run the Better Together campaign often to the deliberate exclusion of the Tories, to get their supporters to the polls next Thursday to save the Union.”

Read more …

• Scottish Independence Looms as Iceberg Moves Toward UK (Bloomberg)

Scottish independence increasingly looks like an iceberg that could sink Prime Minister David Cameron’s government and the opposition Labour Party. And like the passengers on the Titanic, they never saw it coming. Yesterday’s YouGov Plc (YOU) poll putting the Yes vote on 51% sparked a fresh effort from supporters of the union to urge Scots to come back from the brink. About 100 Labour lawmakers will travel to Scotland this week to campaign for a No vote, while Conservative Chancellor of the Exchequer George Osborne offered more powers over taxes and spending to the Scottish Parliament — if voters opt to stay part of the U.K. Cameron was staying with Queen Elizabeth II at Balmoral Castle in northeast Scotland when he learned that the independence campaign had moved into the lead.

“These polls can and must serve as a wake-up call to anyone who thought the referendum result was a foregone conclusion,” Alistair Darling, the leader of the Better Together campaign, which opposes independence, said in a statement. “It never was. It will go down to the wire.” Scottish independence would bring the curtain down on a 307-year-old union that created one of the most influential countries in the world. It would also constitute the biggest crisis of Cameron’s premiership. The prospect of the U.K.’s demise raises as yet unresolved questions over the future of the country’s nuclear deterrent, currently based on Scotland’s west coast, and so its diplomatic standing. Yet Cameron was so unconcerned that his office said he didn’t watch either of the televised debates between Darling and Scottish nationalist leader Alex Salmond. After challenging the economic viability of an independent Scotland, the prime minister has mixed that message with an appeal to the shared history of the nations in the U.K.

It was a Scot, William Paterson, who founded the Bank of England.

Read more …

Only?

• Japan Q2 GDP Revised Down To A 7.1% Contraction (Reuters)

Japan’s economy shrank an annualised 7.1% in April-June from the previous quarter, revised down from a preliminary 6.8% contraction due to weaker-than-expected capital spending, Cabinet Office data showed on Monday. The revised contraction was the biggest since a 15.0% decline marked in January-March 2009. The result compared with a median forecast for a 7.0% contraction in a Reuters poll of economists. On a quarter-on-quarter basis, the economy shrank 1.8% in the second quarter, compared with a preliminary reading of a 1.7% contraction. The result matched the median market forecast.

Read more …

• Economists Point To Emerging ‘Draghinomics’ (FT)

Eurozone officials attending the Ambrosetti forum over the weekend welcomed the European Central Bank’s moves to cut interest rates and signal forthcoming purchases of asset-backed securities, with some private-sector economists suggesting this could herald a new policy mix. Even though the ECB’s long-term forecasts of moderate recovery remain unchanged, the bank’s board members have grown increasingly worried about the recent downward pressure on prices and the softening of consumer confidence. Its latest moves are designed to stave off deflation and jolt the sluggish eurozone economy back to life. Nouriel Roubini, professor of economics at New York University, said ECB president Mario Draghi’s remarks at the Jackson Hole meeting of central bankers signalled an important evolution of thinking. Mr Draghi said at the symposium that monetary policy should be supported by increased spending by countries with strong fiscal positions and structural reforms in economies such as France and Italy.

Mr Roubini labelled the emerging policy mix “Draghinomics” because of its similarity to the three arrows of Abenomics in Japan. “Abenomics has three arrows: monetary and fiscal easing and structural reforms. The eurozone is in near deflation and the recovery is not happening. Monetary and fiscal easing cannot resolve the problem on their own. The ECB has recognised that structural and supply-side reforms are fundamental,” Mr Roubini told the Financial Times. Jyrki Katainen, the European Commission’s vice-president for economic and monetary affairs, said that member states needed to stick to the fiscal discipline that had helped stabilise the currency bloc. But in an interview with the Financial Times, he suggested there was some “fiscal space” in the eurozone as a whole to increase public investment spending. The commission would put renewed emphasis on structural reforms.

“I very much agree with Mario Draghi and what he said that there is a huge need for pursuing structural reforms to improve competitiveness in Europe,” Mr Katainen said, highlighting labour and product market reforms, pension reforms, and liberalising some professional services in various countries. He also said that public spending across the eurozone should be adapted to encourage investment. One other senior eurozone official attending the Italian forum which gathers together policy makers, business people and academics said: “Structural reforms are key. Those countries that have made these efforts are performing better: Ireland, Spain and Portugal. Italy and France should think a little bit about this.” Members of the ECB’s governing council applauded Mr Draghi’s performance to the press on Thursday, saying his remarks accurately characterised the debate between policy makers. It was during the press conference following the rate cut announcement that the ECB president acknowledged the council was split for the first time since last November.

Read more …

China is one big udder for Oz.

• China’s Housing Market Nears Collapse. Should Australia Worry? (Guardian)

After a decade of riding on the back of China with little concern about falling off, recent data has many economists worried that the ride is about to get much bumpier. It’s perhaps not surprising that China is important not just to Australia’s economy, but the whole world’s. But just how important it has become is surprising. Back at the start of this century the Chinese economy was around 11% the size of the US; now it is nearly 60% the size of the US. But despite that massive growth, it wasn’t until 2007 that China became more important than the US to world economic growth. Before 2007, the US was easily the biggest contributor to the growth of the world’s economy. In 2004, for example, the world economy grew by 12.8% (nominal terms) to which the US contributed two percentage points.

By way of context, the UK and Japan that year contributed 0.9 percentage points, France 0.7 and Germany 0.8. China also contributed 0.8 percentage points. In 2007, the world’s GDP grew by a similar 12.7%, but this time China was the biggest contributor with 1.6 percentage points worth, and the US contributing just 1.2. And since then, China has remained the biggest driver of the world’s economic growth: To put it in even more stark terms, from 2007 to 2013, the world’s economy grew by 31% and China contributed nearly a third of that, with 10.1 percentage points worth. Plucky little Australia with 1 percentage point chipped in for 3.2% of the world’s growth in the period – not bad given that we only account for around 2% of the size of world’s economy:

Read more …

• China Posts Record Surplus as Exports-Imports Diverge (Bloomberg)

China’s trade surplus climbed to a record in August as exports rose on the back of increased shipments to the U.S. and Europe, while imports fell for a second month as a property slump hurt domestic demand. Exports increased 9.4% from a year earlier, the Beijing-based customs administration said today, compared with the 9% median estimate in a Bloomberg survey. Imports unexpectedly dropped 2.4%, leaving a trade surplus of $49.8 billion. Divergent directions for exports and imports show China is some way from providing the global growth boost that IHS Inc. this month forecast will see it eclipse the U.S. economy in 2024. Languishing domestic demand underscores risks to the government’s economic-growth target this year of about 7.5% as home prices and construction fall, boosting chances of additional stimulus.

“A targeted cut in mortgage rates is more and more likely,” said Shen Jianguang, chief Asia economist at Mizuho Securities Asia Ltd. in Hong Kong. “If the weakness in the property market can’t be reversed, it’s difficult for the government to reach its annual growth target of 7.5%.” Sustaining export gains may also be challenging because geopolitical risks are weighing on Europe’s economic outlook, said Shen, who formerly worked at the European Central Bank. The increase in exports follows a previously reported 14.5% jump in July and compares with analysts’ estimates for gains ranging from 4.9% to 17%. The median projection for imports was a 3% increase, after a 1.6% drop in July, and the trade surplus was forecast at $40 billion, following a previous record of $47.3 billion in July.

Read more …

China is doing much worse than reported.

• China Commodity Imports Flashing Warning Signs (Reuters)

If you were trying to distil China’s commodity imports for August into a single word, that word may be cautious. Crude oil imports rose 6% from a month earlier, but China was a net fuel exporter for a fourth month this year, meaning that some of the additional crude imports were shipped out as refined products. In assessing the state of Chinese oil demand, the impact of the trade in refined products is becoming increasingly important, as the trend is now clearly toward rising net exports, particularly of diesel. Crude imports were 5.93 million barrels per day (bpd) in August, slightly below the average of 6.03 million bpd for the first eight months of the year. This represents a gain of 450,000 bpd over the 5.58 million bpd imported in the first eight months of 2013.

However, net fuel imports in the first eight months of last year amounted to about 246,000 bpd, while this year there are a paltry 17,000 bpd. If the net fuel imports are added to crude imports, it takes year to date imports for 2014 to 6.047 million bpd, and to 5.826 million bpd for the same period last year, a difference of just 221,000 bpd. This is probably a more accurate reflection of the true state of Chinese fuel demand, and even this picture may be overstated, given the likelihood that strategic storages were being filled in the first half of 2014. What this means is that the International Energy Agency’s forecast for Chinese oil demand to rise 2.9% in 2014 may be too optimistic, and a figure closer to 2% is more likely.

Other commodity imports are also sending warning signals, with unwrought copper flat on month, iron ore dropping 9.3% and coal slumping 18.1%. Unwrought copper imports were 340,000 tonnes in August, bringing the year-to-date total to 3.2 million tonnes, a gain of 14.3% from the same period last year. This is still a relatively strong outcome, and given concern over the strength of manufacturing and housing construction, it would seem that imports are likely running ahead of actual consumption, meaning that stockpiling for financing purposes is still boosting demand.

Read more …

• Weak China Iron Ore Imports Weigh On Prices (FT)

China’s iron ore imports dipped in August, contributing to a $10 a tonne drop over the past month in seaborne prices for the key ingredient in steel to the lowest level since October 2009. Reduced imports of iron ore and coal, plus lower prices for other bulk commodities, helped push China’s August import data into negative territory. China’s total imports shrank 2.4% last month, while a 9.4% growth in exports reflected strong demand from the US and Europe. Weak Chinese manufacturing data for August have raised expectations for further domestic stimulus measures, following gradual easing of local housing policies. A slowdown in construction combined with overcapacity has helped pressure markets for steel and other metals.

China imported 74.9m tonnes of iron ore in August – down 9% from July and roughly equivalent to June – as steel mills cut operating rates to their lowest level since March. However, iron ore imports are still up nearly 17% for the year to date, illustrating how falling prices have helped imported ore maintain market share at the expense of more expensive domestic iron ore mines. In spite of the drop in prices, an official at the central planning agency, the National Development and Reform Commission, lectured BHP Billiton’s China head on the need for a “new model” in pricing, according to a transcript of the meeting last week released by the agency. Her remarks raised concern that international iron ore miners could join the ranks of foreign industries targeted for “monopoly” pricing practices.

Read more …

• Marine Le Pen Calls To Dissolve France’s Lower House (RT)

France is in a “catastrophic situation” and the newly reshuffled cabinet is a “circus,” National Front party leader Marine Le Pen said on Sunday, urging President Hollande to dissolve the National Assembly. Speaking to French media, the head of France’s right-wing National Front likened the recent reshuffle of Prime Minister Manuel Valls’ cabinet to an “illusionist performance,” calling it a “circus.” Le Pen suggested that French President Francois Hollande should dissolve the National Assembly, France’s lower house of parliament. She added that it was “more than necessary” and “the only responsible decision” Hollande would make since he became head of state five years ago. “Francois Hollande tries to save time, but the damage is too deep,” Le Pen argued. In August, Hollande asked Valls to form a new government following tensions within his cabinet over the country’s economic policy. The decision came after strong criticism of the country’s economic direction – which the outgoing economy minister, Arnaud Montebourg, voiced as he called for a “major shift.”

“My responsibility as economy minister is to tell the truth, and observe…that not only are these austerity policies not working but they are also unfair,” Montebourg said in a statement at a media conference on August 25. He frontally attacked German Chancellor Angela Merkel for imposing “austerity police” across Europe. Hollande appointed a new government composed of core allies, casting aside high-profile, left-wing critics – including Montebourg, Culture Minister Aurélie Filippetti, and Minister for Education Benoît Hamon. The move was the second government reshuffle in less than six months. The latest polls have indicated that Le Pen’s popularity is on the rise. A survey released on Friday estimates that the nationalist leader would beat Hollande in the second round of the 2017 elections after grabbing over 30% of the vote in the first round.

Read more …

• EU Banks Sidestepping Bonus Limits Face Regulatory Crackdown (Bloomberg)

Banks in the European Union that attempt to evade new bonus rules face a “coordinated policy response” from the bloc’s regulators. Michel Barnier, the EU’s financial-services chief, called for action on the “politically very important matter” of lenders that have turned to so-called allowances to get around an EU ban on bonuses worth more than twice fixed pay. “I would like to underline my strong concerns with regard to the continuing reports of the use of these allowances,” Barnier wrote in a Sept. 4 letter to Andrea Enria, chairperson of the European Banking Authority. “It is important to show a collective proactive stance on this important matter and address the claims made that the spirit, if not the letter, of union law is being disregarded.”

Barclays, HSBC, Lloyds and Royal Bank of Scotland are among banks that have introduced allowances in response to the bonus limit. Lenders have warned that the cap will harm their competitiveness and force them to increase fixed pay. Allowances, also known as role-based pay, are a regularly adjustable part of employees’ pay packets. They are considered by the banks to be part of salary unaffected by the bonus cap. Barnier asked Enria to share the results of the EBA’s investigation into bonus-cap evasion by the end of the month “in order to ensure that we can address any concerns in a timely manner through a coordinated policy response.” The European Commission provided a copy of the letter.

Read more …

And then?

• Snowden ‘To Get Swiss Asylum If He Testifies On NSA’ (RT)

Switzerland has reportedly decided it will not extradite National Security Agency whistleblower Edward Snowden to the US if he comes to testify against the NSA’s spying activities, Swiss media said. In the document, titled “What rules are to be followed if Edward Snowden is brought to Switzerland and then the United States makes an extradition request,” Switzerland’s Attorney General stated that Snowden should be guaranteed safety if he arrives to the country to testify, Sonntags Zeitung reported. In particular, the report proposes to ensure the whistleblower’s safety by inviting him as a witness to a parliamentary hearing focusing on the NSA’s surveillance practices. In the document, the authority said that Switzerland does not extradite a US citizen, if the individual’s “actions constitute a political offense, or if the request has been politically motivated,” Swiss ATS news agency reported.

Snowden’s safety can thus be guaranteed if it is ruled that the charges against him have a “predominantly political character,” the document concluded. The only obstacle for that could be “higher-level government commitments,” the Office of the Attorney General said, adding that it must be verified if such obligations do, in fact, exist. The document was reportedly requested last November. Snowden’s Swiss lawyer, Marcel Bosonnet, said he is pleased with the Attorney General’s conclusions. “The legal requirements for safety are met,” he assured, adding that Snowden has already showed interest in testifying. Immigration rights activist Sarah Progin-Theuerkauf hinted that Snowden might even have a shot at Swiss asylum following the proposed testimony. “There is evidence that Edward Snowden meets the criteria of refugee status under the Geneva Convention and therefore should be granted asylum,” she told Sonntags Zeitung. Swiss politicians meanwhile are calling to welcome Snowden to Switzerland as soon as possible.

Read more …

Interesting.

• Venezuelan Default Suggested by Harvard Economist (Bloomberg)

As Venezuela racks up billions of dollars of arrears with importers that are fueling the worst shortages on record, one of the nation’s top economists is questioning the government’s decision to keep servicing its foreign bonds. A “massive default on the country’s import chain” is part of what has allowed the nation to keep paying its foreign bonds, Ricardo Hausmann, a former Venezuelan planning minister who is now director of the Center for International Development at Harvard University in Cambridge, Massachusetts, said by phone from Boston. “I find the moral choice odd. Normally governments declare that they have an inability to pay way before this point.” While Hausmann declined to say if he’s specifically recommending a default, he said he found “no moral grounds” for the government and state-owned oil company Petroleos de Venezuela SA to make $5.3 billion of bond payments due in October.

With foreign reserves at an 11-year low and arrears to importers growing, Venezuelans are struggling to find everything from basic medicines to toilet paper. And prices are surging on the goods that they can buy, saddling the country with the world’s highest inflation rate. The nation’s bonds are sinking as President Nicolas Maduro fails to stem the crisis. The extra yield investors demand to own Venezuelan sovereign bonds instead of U.S. Treasuries has jumped 1.92 percentage point in the past month to 12.3 percentage points, the highest since March, according to data compiled by JPMorgan Chase & Co. The spread is the highest in emerging markets. Bonds slumped last week after Maduro removed Rafael Ramirez, the country’s main economic policy maker, fueling concern the government may delay or scrap measures to ease the hemorrhaging of dollars, including a currency devaluation and increase in gasoline prices.

Marcos Torres, the head of economy and finance at the central bank, didn’t reply to an e-mail seeking comment on Hausmann’s statements. An official at the Information Ministry declined to comment when reached over the weekend. Hausmann has been a public figure in Venezuela for more than two decades, having served as planning minister in the government that the late Hugo Chavez, Maduro’s predecessor and mentor, tried to topple in a 1992 coup attempt. Hausmann then joined the Inter-American Development Bank, where he was chief economist, before leaving for Harvard in 2000. In a Sept. 5 piece published in Project Syndicate that was titled “Should Venezuela Default?”, Hausmann and Miguel Angel Santos, a Harvard research fellow, highlighted how the import arrears and shortages are imposing hardship on Venezuelans. “The fact that his administration has chosen to default on 30 million Venezuelans, rather than on Wall Street, is not a sign of its moral rectitude,” they wrote. “It is a signal of its moral bankruptcy.”

Read more …