Vincent van Gogh Gypsy Camp near Arles 1888

Dershowitz+

https://twitter.com/i/status/1691291110717390848

Weiss Maria

.@MariaBartiromo: "David Weiss was the one behind the botched plea deal which was intended to shield Hunter Biden from all future charges. The plea agreement blew up after a federal judge raised concern that Hunter would recieve immunity from any future criminal charges…

The… pic.twitter.com/ZErqldL2ZP

— KanekoaTheGreat (@KanekoaTheGreat) August 13, 2023

Biden rally

MSNBC Contributor: “As soon as they start impeaching [ Joe Biden] with no evidence just based on innuendos and this Hunter stuff, I believe the American people are going to rally around the President.”

— The Post Millennial (@TPostMillennial) August 14, 2023

“If Trump returns to the White House in 2024, he will not be able to pardon himself in [cases handled by state courts].

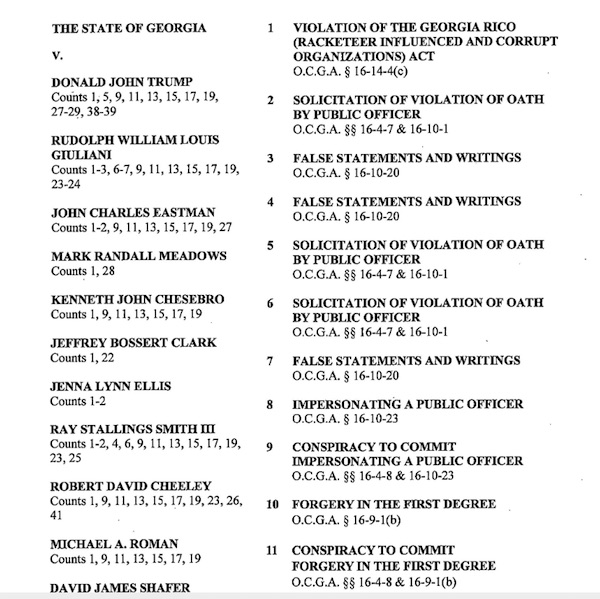

• Trump Indicted for 4th Time in Georgia Election Interference Case (DeMartino)

The former US president has already been hit with a total of three indictment, two of which are federal cases. To date, the Trump camp has repeatedly rejected all charges, underscoring that legal proceedings are intended to block the ex-commander-in-chief’s 2024 reelection campaign. Former US President Donald Trump was indicted for a fourth time late Monday, this time for his and his allies alleged actions to overturn the 2020 presidential election results in the state of Georgia. The grand jury indictment in Georgia stretched far into the night on Monday, with the indictment only becoming public just before 11 p.m. The 98-page indictment list charges a total of 19 individuals including Trump, and fellow associates Rudy Giuliani, John Eastman, Mark Meadows, Jeffrey Clark, among other figures.

Over 40 charges are listed in the filing, which also notes there are 30 co-conspirators who have yet to be officially indicted. Trump was specifically hit with 13 charges, including: Violation of the Georgia RICO Act, solicitation of violation of oath by public officer, conspiracy to commit impersonating a public officer and conspiracy to commit forgery in the first degree, among others. Among the charges listed in the filing against Trump, violations of the Georgia RICO (racketeering) Act is considered the most serious. RICO cases are typically used to clamp down on drug cartels or larger criminal organizations. It’s specifically used in cases where an alleged offender engaged in a minimum of two predicated crimes that were in connection to an enterprise that is either considered legal or illegal.

Shortly after the indictment was released, Fulton County District Attorney Fani T. Willis told reporters that the defendants must surrender voluntarily no later than 12 p.m. local time on August 25. “[Trump and his allies] constituted a criminal organization whose members and associates engaged in various related criminal activities,” Willis said at a news conference just before midnight Monday. “They knowingly and willfully joined conspiracy to unlawfully change the outcome of the election in favor of Trump.” Willis did state that she will seek to try the case within six months’ time, and that she wanted to try all defendants together, a task that insiders have already noted may pose several difficulties.

[..] Trump has also been indicted on federal charges related to his alleged mishandling of classified documents and in a New York state case over money he paid to an adult film actress to keep her from speaking about an affair she alleged to have with Trump years before the start of the 2016 US election cycle. In that case, investigators claim the payments were illegally classified as legal expenses. The cases in Georgia and New York are particularly significant because the US president does not have authority over state courts. While legal experts have debated if a president could pardon themselves in a federal case, there is no doubt they cannot in cases handled by state courts. If Trump returns to the White House in 2024, he will not be able to pardon himself in those cases.

President Trump’s attorney @AlinaHabba is outraged that they are allowing cameras & the press in the courtroom right now.

“It is part of the show. This is a show. It’s a political show. Fani… it is not okay what you are doing. This is unacceptable. The fact that we have… pic.twitter.com/w9NPRKep3a

— TheStormHasArrived (@TheStormRedux) August 15, 2023

They have no case, so they gather everything they can think of and hope something sticks to the wall. But that’s nothing to do with justice.

• Georgia DA Charges Trump, Others With New RICO Indictment (ZH)

It’s been quite a day in Atlanta (and for scrambling Democrats) as former President Trump was indicted for the 4th time. Before the Grand Jury’s verdict, Reuters reported that a document was leaked earlier in the day on the Fulton County, Georgia court’s website showing former president Trump being indicted on RICO charges (among many others). The Georgia DA released a statement calling the document “fictitious”. Trump’s team (and the entire internet) mocked this farcical comment: “This was not a simple administrative mistake.” The Grand Jury then handed down a 98-page indictment, against the former president (the jurors’ names were unredacted)… …claiming that he – and 18 of his allies – orchestrated a sweeping criminal enterprise, committing more than a dozen felonies, as he tried and failed to overturn his defeat in Georgia’s 2020 election.

Defendants include Rudy Giuliani, Mark Leadows, Sidney Powell, and John Eastman. The charging documents also list 30 unindicted co-conspirators. Trump faces 13 counts in the indictment. Here is the full list: •One count in violation of the Georgia Racketeer Influenced and Corrupt Organizations Act •Three counts of solicitation of violation of oath by public officer •One count of conspiracy to commit impersonating a public officer •Two counts of conspiracy to commit forgery in the first degree •Two counts of conspiracy to commit false statements and writings •One count of conspiracy to commit filing false documents •One count of filing a false document •Two counts of false statements and writings All of these charges were exactly as per the leaked “fictitious” document that was found on the courthouse website hours before the Grand Jury’s decision.

Statement from the Trump Campaign: “Like Manhattan DA Alvin Bragg, Deranged Jack Smith, and New York AG Letitia James, Fulton County, GA’s radical Democrat District Attorney Fani Willis is a rabid partisan who is campaigning and fundraising on a platform of prosecuting President Trump through these bogus indictments. Ripping a page from Crooked Joe Biden’s playbook, Willis has strategically stalled her investigation to try and maximally interfere with the 2024 presidential race and damage the dominant Trump campaign. All of these corrupt Democrat attempts will fail. Combined with the intentionally slow-walked investigations by the Biden-Smith goon squads and the false charges in New York, the timing of this latest coordinated strike by a biased prosecutor in an overwhelmingly Democrat jurisdiction not only betrays the trust of the American people, but also exposes true motivation driving their fabricated accusations.

They could have brought this two and half years ago, yet they chose to do this for election interference reasons in the middle of President Trump’s successful campaign. He is not only leading all Republicans by a lot but he is leading against Joe Biden in almost every poll. President Trump represents the greatest threat to these Democrats’ political futures (and the greatest hope for America). The legal double-standard set against President Trump must end. Under the Crooked Biden Cartel, there are no rules for Democrats, while Republicans face criminal charges for exercising their First Amendment rights.

These activities by Democrat leaders constitute a grave threat to American democracy and are direct attempts to deprive the American people of their rightful choice to cast their vote for President. Call it election interference or election manipulation—it is a dangerous effort by the ruling class to suppress the choice of the people. It is un-American and wrong. They are taking away President Trump’s First Amendment right to free speech, and the right to challenge a rigged and stolen election that the Democrats do all the time. The ones who should be prosecuted are the ones who created the corruption. President Trump will never give up and will never stop fighting for you, as we all work to Make America Great Again in 2024.”

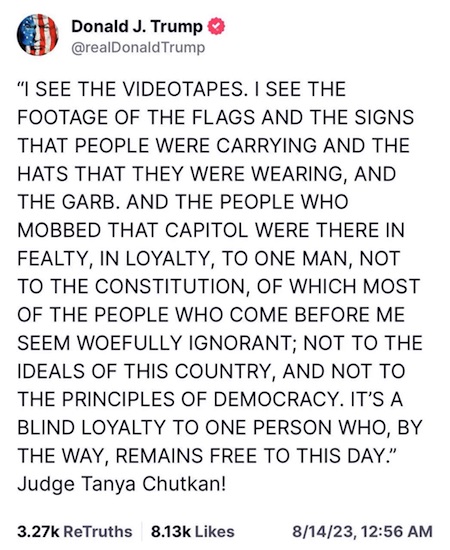

“The very client that was in front of her in federal court was one of her former clients. That is rule #1 for disqualification.”

• Judge In Trump J6 Trial Worked At Law Firm that Repped Fusion GPS (ZH)

U.S. District Judge Tanya S. Chutkan, who is overseeing the Trump J6 trial being prosecuted by the Biden Justice Department, previously worked at a law firm that represented Fusion GPS, the company that helped orchestrate the Russia collusion hoax targeting former President Donald Trump. During Chutkan’s stint with Boies Schiller Flexner, the Democrat-friendly law firm also reportedly represented Clinton Cabal foot soldier Huma Abedin, the former wife of disgraced Democrat Anthony Weiner. The stunning revelations came in the wake of reports that the Obama-appointed judge worked at the same Boies Schiller Flexner law firm with President Joe Biden’s embattled son, Hunter. The same law firm that employed Chutkan also reportedly represented Burisma.

Trump blasted the apparently gross conflicts of interest and bias saddling Chutkan, writing on Truth Social that, “The Obama appointed Judge in the FREE SPEECH Indictment of me by my political opponent, Crooked Joe Biden’s Department of InJustice, shared professional ties at the law firm that worked for Energy Company Burisma, based in Ukraine, of which Hunter Biden and his associate were “proud” MEMBERS OF THE BOARD, and were paid Millions of Dollars, even though Hunter knew almost NOTHING about Energy. How much was the law firm paid? So Horrible. This is a CLASSIC Conflict of Interest!” The J6 free speech trial won’t be the first time Chutkan has been entangled by court conflicts stemming from her legal workings with outfits targeting Trump.

Chutkan was forced to recuse herself from the bench when she was overseeing Fusion GPS’s attempt to block former congressman Devin Nunes and Kash Patel from outing the source of payments that funded the infamous Steele dossier. “Fusion GPS, the DNC, and the Hillary Clinton campaign paid Christopher Steele millions of dollars and they laundered it through the FBI and the FISA court to unlawfully surveil Donald Trump. That’s big-time stuff,” Patel, who served in the Trump administration, noted during an interview with America First’s Sebastian Gorka. After months of litigation before Chutkan, when it became apparent that Nunes and Patel would be successful, “she recused -on her own- from that case. Why?” Patel asked rhetorically.

“We found out her law firm, Boies Schiller, represented Fusion GPS,” Patel answered. “The very client that was in front of her in federal court was one of her former clients. That is rule #1 for disqualification.” It also sets a sterling precedent for Chutkan’s removal from the Trump J6 trial, Patel said. “She set the precedent. She cannot neutrally and arbitrarily preside over Donald Trump’s criminal trial when she recused herself from the very representation of the Democratic entrenchment: the DNC, the Hillary Clinton campaign, Fusion GPS, because she was so biased because of her prior representation from Boies Schiller,” he argued.

“The same David Weiss who cooked up a wrist-slap plea agreement on all this, with a hidden Get-Out-Of-Jail-Free clause inserted slyly in the fine print of the so-called “diversion agreement”..

Karma is God’s hickory switch, and almost always applied with a cosmic chortle. Things come around when a certain excess cargo of cognitive dissonance breaks the brains of those just struggling to carry on. The country has had enough — enough walking-talking hypocrisies, enough trips laid on it, enough Tik-tok lectures from the nose-rings-for-lunch-bunch. We’re at the end of something and the beginning of something new. As in: an ass-beating is coming down. Cue one Oliver Anthony, southern country boy with a flaming red beard and a new anthem for millions sore-beset by the relentless effronteries of the ruling elites. Rolling Stone Magazine, a ruling elites house organ, played the phenomenon this way:

These things listed above are…what? Things that Rolling Stone is in favor of? Pet causes? High taxes and obese people on welfare? And Mr. Anthony’s song is dissing them? You mean Right-Wing influencers shouldn’t mention Jeffrey Epstein’s name? Is it just plain rude… or does it stir up unappetizing questions that are better off not being asked (in polite company)? Kind of shows you where the battle lines are drawn now, doesn’t it? Perhaps the final insult galvanizing all this sentiment in a song was Merrick Garland’s devious Friday afternoon announcement — when, theoretically, no one was paying attention — that he appointed US Attorney David Weiss as Special Counsel in the Hunter Biden matter.

This is the same David Weiss, you understand, who oversaw the Hunter Biden investigation for the past five years before ascertaining anything that might be chargeable from a vast inventory of financial crimes with an overlay of documented sex and drug transgressions. The same David Weiss who let the statute of limitations run out on many of those crimes while he dawdled and frittered in Wilmington. The same David Weiss who cooked up a wrist-slap plea agreement on all this, with a hidden Get-Out-Of-Jail-Free clause inserted slyly in the fine print of the so-called “diversion agreement” that would have immunized Hunter B against any further inquiries — which Judge Maryellen Noreika discovered only by chance at the last moment, scotching the deal. (And yet, the government now claims that the diversion agreement — and Hunter B’s immunity from further charges — “stands alone,” is “in effect” and “still binding.” Hmmmm….)

Great interview.

• Tucker And RFK Jr. Talk Ukraine, Biolabs, And Who Killed His Uncle (ZH)

RFK Jr. and Tucker Carlson sat down for a lengthy interview published on X (formerly Twitter) on Monday, in which the two discuss Ukraine, bio-labs, and who killed his uncle, JFK. Carlson made clear that he wasn’t going to badger Kennedy with questions about his stance on vaccines, which the MSM has made a central focus for obvious reasons. The interview begins by discussing the Biden administration denying RFK Jr. Secret Service protection. Despite the fact that his uncle and his father were both assassinated, the Biden administration denied SS protection “We applied for Secret Service protection in May,” said Kennedy, adding “The President has discretion to give Secret Service protection to any candidate, for any reason.” Kennedy noted that former President Barack Obama was given Secret Service protection more than 500 days before the election, and that his uncle Ted Kennedy received protection more than 450 days before an election. “I think the DNC is playing hardball,” Kennedy added.

https://twitter.com/i/status/1691239726190100481

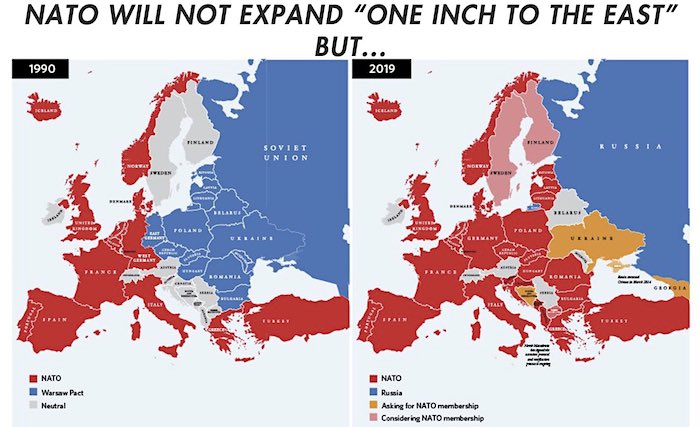

On the topic of Ukraine (12 minutes in), Kennedy says Americans are being lied to, and were sold on a “comic book pitch, which we see in every war. There’s a bad guy who’s like, you know, unspeakably evil, who’s planning world conquest or a terrorist attack on America. And we have to be the good guys and go in and stop it.” Kennedy then explained that “a group of people who are known as Neocons, since 2001, have been talking about putting NATO in Ukraine. Now, I’ll give you some background. In 1992 the walls came down and the Soviet Union collapsed. Gorbachev went to Tony Blair and President Bush and said ‘I’m going to withdraw 400,000 Soviet troops from East Germany. I’m going to allow you to reunify Germany under NATO troops – so you’re gonna move NATO troops, a hostile force, into our barracks and our bases – and the only commitment I want from you, is that once I allow Germany top become part of NATO, that you will never move NATO further to the East.'” “James Baker, who was the Secretary of State at that time, famously said: ‘we promise that we will not move NATO one inch to the East.'” “Then, in 1996, 1997, five years later, Zbigniew Brzezinski … says ‘ok, we should start moving NATO to all the former (USSR) satellite states.'”

US Biolabs in Ukraine: At around 35 minutes into the interview, Carlson and Kennedy begin discussing the US bioweapons program. Meanwhile back home, RFK Jr. said that there are “36,000 ‘death scientists’ who are now employed full time in developing microbes that can be used to kill people.”

Tucker RFK

Ep. 16 RFK Jr. explains Ukraine, bio-labs, and who killed his uncle pic.twitter.com/RMr5VZVqSM

— Tucker Carlson (@TuckerCarlson) August 14, 2023

As long as it keeps going, US/NATO don’t have to admit defeat…

• US Expects Ukrainian Conflict To Drag On For A While – Envoy (TASS)

The United States is sinking deeper into the confrontation with Russia and expects the Ukrainian conflict to drag on for a long time, Russian Ambassador to Washington Anatoly Antonov said, commenting on the next package of US military aid to Kiev. “With persistence, worthy of a better use, Washington is sinking deeper and deeper into the confrontation with Russia, while using Ukrainians as proxies. Sends new batches of weapons and money to the Zelensky regime. It looks like the administration cannot figure out how to get out of the bloody project and save its face at the same time. The White House obviously does not care about the rapid decline in the level of support for such a strategy in the American society. Instead it hopes that the conflict will drag on for a long time.

“What is missed here is that the deadly products of the US defense corporations are used by Kiev criminals against peaceful citizens and civilian facilities,” Antonov said in a statement published on the Russian embassy’s Telegram channel. The diplomat pointed out that Washington does not want to learn from its mistakes and continues to provide military aid to Ukraine, although “such irresponsibility is already too costly for both parties involved in the conflict, as well as for a local taxpayer.” “We emphasize that it will not be possible to achieve victory over the Russian Armed Forces ‘on the battlefield’. One cannot break the stamina of a Russian soldier defending his land. All goals and objectives of the special military operation will be achieved,” Antonov pointed out.

Earlier, the US allocated Ukraine a new package of weapons and military equipment worth $200 million. US Secretary of State Antony Blinken said that the package includes, in particular, interceptors for Patriot air defense systems, shells for HIMARS multiple rocket launchers, TOW and Javelin anti-tank missile systems, 37 tractors, artillery shells of 155 and 105 mm caliber, tank shells of 120 mm caliber, over 12 million rounds of small arms ammunition and grenades, spare parts and accessories.

Bolton doesn’t understand “checkmate”.

• John Bolton Blames Biden For Kiev’s ‘Stalling’ Counteroffensive (RT)

Failures in Ukraine’s much-touted counteroffensive against Russia stem from the West’s inability to provide Kiev with the necessary military equipment within a reasonable timeframe, former US National Security Advisor John Bolton has said. In an op-ed for the Wall Street Journal published on Sunday, Bolton lamented that Kiev’s long-anticipated push, which started in early June, “isn’t making the headway some proponents had forecast,” adding that the disappointing results must become a “wake-up” call for Washington. The former White House official – widely regarded as a foreign-policy hawk and who has advocated regime changes in Iran, Syria, Libya, and Cuba – insisted in his article that Kiev’s “inability to achieve major advances is the natural result of a US strategy aimed only at staving off Russian conquest,” while he also urged US President Joe Biden to start “vigorously working toward Ukrainian victory.”

“Ukraine’s offensive failures and Russia’s defensive successes share a common cause: the slow, faltering, non-strategic supply of military assistance by the West,” Bolton claimed, adding that the US-led support for Kiev has been hampered further by speculation that Moscow might escalate the conflict. Bolton, who served in the Trump administration up to 2019, sought to allay those concerns, insisting that “there’s no evidence” that Russia has conventional military capability to threaten NATO or a desire to launch a nuclear strike. Moscow has repeatedly stated that it adheres to the policy that nuclear war should never be fought, and that it might resort to its atomic arsenal only if the very existence of the state is threatened.

The former national security adviser also dismissed the need for talks between Kiev and Moscow, arguing that these would only benefit Russia. Instead, he suggested that the West and Washington should radically tighten the sanctions regime. In addition, he called on Washington to slap restrictions directly on China, citing its “enormous support” for Moscow. While Beijing remains Russia’s key trade partner, it has repeatedly denied that it was providing Moscow with military support.

Ukrainian forces went on a large-scale offensive against Russian lines over two months ago, after being reinforced by hundreds of Western-supplied tanks and armored vehicles. However, according to the Russian Defense Ministry, Kiev has so far failed to gain any ground and has lost more than 43,000 service members since the start of the push. Bolton’s view on the reasons for Ukraine’s difficulties is shared by a number of Ukrainian officials, including President Vladimir Zelensky, who has suggested that without long-range weapons, it’s difficult for Kiev not only to carry out its offensive, but also to hold the frontline. Moscow has repeatedly warned Western countries against sending military assistance to Kiev, arguing that by doing so, they become engaged in a “proxy war” against Russia.

A once proud(ly) neutral nation.

• New Defense Agreement Would See US Troops Deployed in Finland (Antiwar)

Washington and Helsinki are working on a new deal to govern the military relationship between the two nations. Finland recently became the thirty-first member of NATO, doubling the alliance’s border with Russia. According to YLE News, Finnish state media, Helsinki and Washington are negotiating a new Defense Cooperation Agreement (DCA). YLE said the new deal would be a “significant departure from its previous” DCA with the US. Finland held a prolonged policy of official neutrality prior to joining NATO earlier this year. However, Helsinki established deep ties with the bloc over recent decades. The new DCA will expand America’s military presence to several Finnish bases, including ports and airports.

The outlet reports the new DCA will “permit the presence of foreign troops for extended periods, specifically for conventional military exercises…[and] grant US military personnel access to facilities and areas within Finland for training, weapons storage, and equipment maintenance.” The war games and NATO soldiers will be viewed as a provocation by Russia, which shares an 800 miles border with Finland. Helsinki already hosts NATO troops for military drills near the Russian border.

When Helsinki announced its intention to join the North Atlantic bloc last year, the Kremlin warned about additional international troop deployments in Finland. Last week, Moscow announced it would deploy additional military assets to its border with NATO members. Finnish negotiations have expressed some reservations about expanding the DCA with the US. YLE explains, “noting that the agreement excludes nuclear weapons,” and Helsinki wants all integration troops deployments to be labeled as temporary.

“..the nuances of a West teetering at the cusp of radical metamorphosis..”

• The Black Sea, Out-of-View ‘War’ (Alastair Crooke)

There are signals in the American MSM that lately, U.S. policy is shifting (but is not finally settled). One thing, however, is clear: the blame for the failed offensive is being squarely laid by the U.S. on the shoulders of Ukraine – and now, for the first time, Kiev is reciprocating the jibes by ridiculing western inability to supply what it promised. Relations plainly are souring. However, in step with the West disowning and distancing itself from the military tactics deployed by Ukraine to attack the ‘Surovikin Lines’, NATO powers seemingly are backing off too from entering negotiations (in spite of a MSM lobby pressing for them). Perhaps western policy-makers now view a ‘negotiated’ outcome as potentially humiliating for Biden.

Put plainly: Does this western despairing of Ukrainian military prospects imply a coming, draw-down on the war, or alternatively, a western strategic shift towards a different mode of attritional war against Russia? In short, do the attacks at Novorossiysk presage a move to ‘real war’ – where Russia’s transport infrastructure is a priority target for attack? Or simply, were the Novorossiysk attacks merely a crude nudge to Russia, saying: ‘Re-start the export of Ukrainian grain!’? The wider issue which this Novorossiysk attack ‘opens’ is whether or not Russia might assess that it has been too cautious and incrementalist in pursuit of its strategic aims? The missile strikes on Reni and Izmail can be seen as very tentative initiatives by Russia to probe the ground and the appetite in NATO for ‘real war’ – where the enemy’s transport infrastructure would be a priority target for attacks.

Is this the moment that Russia might feel it should move to ‘real war’ – firstly, because the ground in the Ukraine suggests the moment is ripe? And secondly, because at another level, there is the need to address the perennial dilemma of all conflicts: Any military approach (i.e. such as Sun Tzu’s dictum: “It is the unemotional, reserved, calm, detached warrior who wins, not the hothead”) and one that recognises the weakness of its opponents’ psyche and the need to nudge it delicately towards acceptance of a new, unfamiliar reality, is always vulnerable to be misconstrued as signalling weakness. Starkly put: Is a Russian show of strength now needed to correct western misperceptions which continue to fantasise about weakness, unrest and the coming political collapse of Russia? Sun Tzu would retort: “Engage people with what they expect. It is what they are able to discern, and confirms their projections.

It settles them into predictable patterns of response, occupying their minds – whilst you wait for the extraordinary moment — that which they cannot anticipate.” Well, maybe some answers can be given: The western war hawks (to employ an old metaphor) may be ‘big talk, but NATO has no trouser’ for real war. The West, even now, is struggling at the cusp of economic crisis with supply-line disruption: A tanker war would be fatal (oil skywards and inflation too). The exit from delusion is always slow – as Sun Tzu hints. The rather tired adage is that war is the ‘extension of politics by other means’, but especially today ‘other means’ can – and often is – the extension of politics. Today, Russia is acting as ‘pathfinder’ towards a new global multi-polar bloc. In this capacity, Russia needs to act politically with its eye cocked towards the Global South, as well as to the nuances of a West teetering at the cusp of radical metamorphosis.

Military commands may chaff at it, but the Global South admires Russia precisely because it does not ape the Colonial Powers. The world respects power, yes, but is tired of just ‘fire-power’. Russia has a leading role to play now, and many are the constituencies that must be taken into account. This will be underlined in the coming days as events in Niger unfold, and as the BRICS summit proceeds with new arrangements for trading mechanisms high on the agenda. The effective use of ‘other means of asymmetric power’ is contingent upon timing above all else. (Sun Tzu for the last time): “Occupy their minds while you wait for the right moment”. It would seem that President Putin is very familiar with The Art of War.

They’re afraid of religion. They want to be the only organization. Even the mob left religion alone.

• Zelensky Regime’s Police Raid Kiev-Pechersk Lavra Orthodox Church (Sp.)

Police officers have cordoned off three buildings that are part of the Kiev-Pechersk Lavra, and are storming the premises, the canonical Ukrainian Orthodox Church (UOC) said on Tuesday. “Right now, the police are storming the Lavra’s 54th, 57th and 58th buildings, where both pilgrims and some monks reside,” the UOC said in a message published on its Telegram account. According to the UOC, police officers “have already cut the locks and broke into the [Lavra’s] 57th building.” The reported developments come after Gennady Askaldovich, the Russian Foreign Ministry’s special representative for Cooperation to Promote Respect for the Right to Freedom of Religion, slammed the eviction of the monks from the Kiev-Pechersk Lavra, branding the move as more lawlessness and despotism by the Zelensky regime.

“If this decision [on the eviction] is carried out, the schismatics will have a direct path to seize and close the great Orthodox shrine. Another act of lawlessness and arbitrariness has taken place on the part of the Kiev regime, which fabricated a lawsuit and got the verdict it needed,” Askaldovich said in a statement. On Thursday, a Kiev court upheld a claim against the Kiev-Pechersk Lavra to remove all obstacles to the use of property. The monks can now be evicted, sources familiar with the court decision told Sputnik. Ukrainian media reported, in turn, that a commission from the Ukrainian Ministry of Culture and Information Policy had sealed off four buildings that are part of the Kiev-Pechersk Lavra.

Nikita Chekman, a Kiev-Pechersk Lavra attorney and UOC archpriest, castigated the court’s decision as “one of the most shameful in Ukrainian history.”

Over the past 12 months, the Zelensky regime has orchestrated a full-blown crackdown against the Ukrainian Orthodox Church. Asserting its connection with Russia, local authorities in various regions of Ukraine have prohibited the church’s activities, and a bill seeking a nationwide ban on the UOC was submitted to the Ukrainian parliament. Kiev also slapped sanctions on some of the church’s clerics. The Security Service of Ukraine, in turn, began to lodge criminal cases against the church’s clergy, and also launched a “counterintelligence” crusade against UOC bishops and priests, as well as against its churches and monasteries in search of evidence of “anti-Ukrainian activities.”

Yes, yes, Victoria Nuland…

• Washington Accused Of Betraying Allies Over Niger (RT)

Washington got in the way of its own NATO ally, France, when it decided to send Deputy Secretary of State Victoria Nuland to talk to [Niger’s] new military government, Le Figaro reported over the weekend, citing a source within the French Foreign Ministry. The US “did the exact opposite of what we thought they would do,” a French diplomatic source told the paper, adding that “with allies like these, we do not need enemies.” Paris has been insisting on the reinstatement of ousted President Mohamed Bazoum ever since a new military government came to power in Niger in a coup in late July. The French government was also ready to support the use of force by West African nations for that purpose, as it upheld the Economic Community of West African States (ECOWAS) in its decision to mobilize reserve forces in the wake of the ousting.

By sending Nuland to Niger, the US demonstrated it was ready to talk to the coup leaders instead, Le Figaro said. “For [French President] Emmanuel Macron, the credibility of France, particularly in terms of discourse on democracy, was at stake. For the Americans, even if they are also concerned about a rapid return to constitutional order, the priority is the stability of the region,” the paper’s source within the foreign ministry said. Americans simply want “to keep their bases” in the region above all else, the diplomat said, adding that Washington “will not hesitate” to drop a demand for what he called “constitutional legality” to achieve this goal. Now, Paris fears that Washington could reach an agreement with Niger’s military government behind France’s back.

The US has a sizable force on the ground in Niger, amounting to some 1,300 soldiers and almost equaling that of France, which has around 1,500 servicemen in the country. American troops are divided between two bases, located in the Niger capital of Niamey and the northern city of Agadez.Agadez is reportedly of particular importance for Washington as it houses a landing strip for drones and serves as a surveillance hub for a large area stretching from West Africa to Libya in the north. According to Le Figaro, Paris is also displeased by the fact that, despite both France and the US having troops in Niger, it is only the French presence that provokes resentment among the locals. “The United States, like our other allies for that matter, has a habit of letting us take the hits,” the French diplomat told the paper.

The coup in Niger took place on July 26, when the presidential guard headed by Tchiani detained Bazoum and his family, citing a “deteriorating security situation and bad governance.” The move sparked condemnation from global powers, while ECOWAS imposed harsh sanctions on Niger and issued an ultimatum to the coup leaders to release Bazoum or face military intervention. On Monday, Niger’s military government agreed to hold talks with ECOWAS in a bid to defuse tensions in the region. Nuland visited Niger last Monday. During the talks, she warned the new military government against striking any deals with the Russian private military company Wagner and urged them to restore the Washington-friendly status quo.

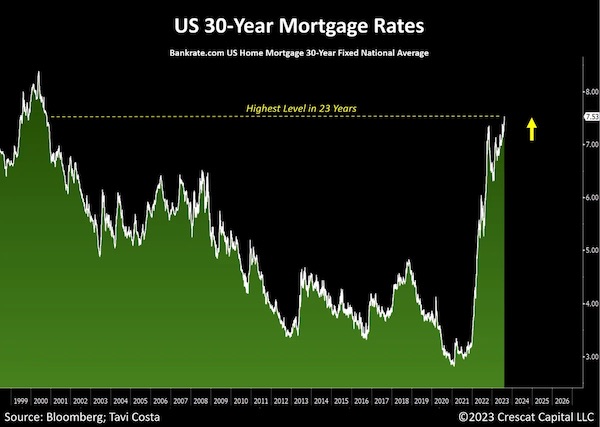

“..we are in the weeds because interest rates are at a point that nothing can be refinanced and rolled over.”

• Full Faith & Credit of a Bankrupt Insolvent Government – Bill Holter (USAW)

Precious metals expert and financial writer Bill Holter says there is a long list of financial trouble coming to America sooner than later. There is the commercial real estate implosion, rising interest rates, an exploding federal budget, banana republic political problems, but the at the top of the list is the monster unpayable debt problem and the soon-to-be failing U.S. dollar. Holter says, “You can’t have a third of the federal taxes paid out in interest, and that number is only going to grow over time. . . . If the markets would not collapse ahead of time, which they certainly will, but if they did not, we would get to the point where the interest would eat up all the tax receipts. That is a mathematical impossibility.

We’re broke. On the other side of it, we have two rules of law. We have one rule of law if you are a liar from the left and another rule of law if you are a conservative and you don’t support the bull crap rules they are putting out there. . . . This is an illustration that this country has already become a banana republic. The problem with that is the dollar issued by this country is the world’s reserve currency. It’s a huge problem.” Holter says the dollar is going to take a big hit in the next financial crisis that has already started. When it hits, Holter predicts, “The actual bottom line is dollars are just pieces of paper backed by our government. The dollar is backed by the full faith and credit of a bankrupt insolvent government, and people will figure that out very quickly.

When it comes to survival, people are not going to give up something real for nothing. . . . We are in the weeds right now because of interest rates . . . look at mortgage rates, they are well over 7% for a 30-year mortgage. So, that’s going to hurt housing. Commercial real estate has already been destroyed. . . . I think we are in the weeds because interest rates are at a point that nothing can be refinanced and rolled over.” In closing, Holter says, “This is not my opinion, it’s a mathematical equation. The debt cannot be paid back. It’s not possible. We will default one way or another. We will print the crap out of the dollar and devalue it, or outright nonpayment.” Holter predicted years ago we would end up in a “Mad Max” scenario when credit dries up and store shelves empty. Holter contends that credit is drying up with the money supply shrinking for eight straight months. The “Mad Max” world Holter is still predicting is now looking like it’s going to come true sooner than later.

It’s a trap, he’d have to “first travel to the United States to formally admit guilt in court proceedings.”

Don’t.

• US Hints At Assange Plea Deal (RT)

Caroline Kennedy, the United States’ ambassador to Australia, has indicated that the US Justice Department may consider seeking a plea deal with WikiLeaks founder Julian Assange that could downgrade his charges and allow him to return to his homeland. Assange, 52, faces a potential life sentence in a US prison on espionage charges linked to the 2010 release on his WikiLeaks platform of highly sensitive US Army intelligence information provided to him by former analyst Chelsea Manning. But speaking to the Sydney Morning Herald in comments published on Sunday, Kennedy said that a diplomatic remedy to the long-running Assange saga might be forthcoming, telling the newspaper, “There absolutely could be a resolution.”

When asked if the United States could arrange for a plea deal involving Assange, Kennedy said that this was “up to the Justice Department.” While there has been no official comment on the issue from the relevant US authorities, a plea deal could theoretically be sought, which would see Australian native Assange agreeing to plead guilty to lesser charges in return for being permitted to return home to serve any remaining prison time. Assange has been held in London’s Belmarsh Prison since 2019 as he fights extradition to the United States. Previously, Assange had been granted political asylum by Ecuador’s embassy in London since 2012, before his arrest seven years later. “Caroline Kennedy wouldn’t be saying these things if they didn’t want a way out,” Assange’s brother, Gabriel Shipton, told the Sydney Morning Herald. “The Americans want this off their plate.”

According to international law expert Donald Rothwell, the terms of any Assange plea deal would likely require him to first travel to the United States to formally admit guilt in court proceedings. “Everything we know about Julian Assange suggests this would be a significant sticking point for him,” Rothwell told the newspaper. “It’s not possible to strike a plea deal outside the relevant jurisdiction except in the most exceptional circumstances.” However, a successful plea deal would likely require authorization from US Secretary of State Antony Blinken, who said last month that Assange’s actions “risked very serious harm to our national security, to the benefit of our adversaries, and put named human sources at grave risk of physical harm, grave risk of detention.”

Bosco Verticale

https://twitter.com/i/status/1691133402408275978

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.