Rembrandt van Rijn The artist’s son Titus 1657

Still puzzled by this.

Tucker midterms

Tucker knows. pic.twitter.com/zjtQNOnCUh

— Rep. Matt Gaetz (@RepMattGaetz) November 10, 2022

A single word

Remember our President's inspiring

words about our nation pic.twitter.com/vIIEVEKSi9— Historic Vids (@historyinmemes) November 9, 2022

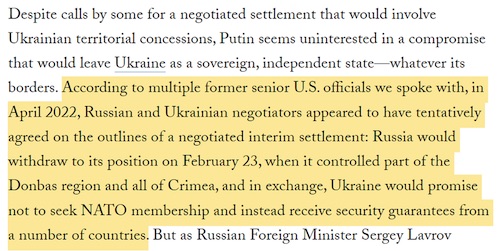

“U.S. officials reportedly told Zelensky that Kiev “must show its willingness to end the war reasonably and peacefully.”

• Will A Russian Kherson Exit Create The Right ‘Facts On The Ground’? (Snider)

Will the Russian withdrawal from the key city of Kherson this week continue what appears to be momentum toward a diplomatic end to the war in Ukraine? The signs may be pointing in that direction. In late September, Russia declared its annexation of the Donbas republics of Donetsk and Luhansk as well as the eastern regions of Kherson and Zaporizhzhia. Ukrainian President Volodymyr Zelensky responded by signing a decree banning any negotiations with Putin. Zelensky said that Ukraine is “ready for dialogue with Russia, but with another president of Russia.” That decree posed a problem, particularly for the United States, which is trying to maintain a coalition assembled to support Ukraine militarily, financially, and through sanctions on Russia.

Since imminent regime change in Moscow has appeared unlikely, waiting for another president might mean a potentially endless war. And that’s a hard sell for weary European allies — who are heading toward a cold winter — no matter their commitment to the cause of defending Ukraine. So, in a shift from its position that it had “ruled out the idea of pushing or even nudging Ukraine to the negotiating table,” the Biden administration reportedly began urging Zelensky to “signal an openness to negotiate with Russia and drop his government’s public refusal to engage in peace talks unless President Vladimir Putin is removed from power,” according to the Washington Post.

At first, Ukraine publicly rejected the pressure. Zelensky adviser Mykhailo Podolyak reiterated the promise that Ukraine will only “talk with the next leader” of Russia, and told the Italian newspaper La Repubblica that talks could only resume once the Kremlin relinquishes all Ukrainian territory and that Kyiv would fight on even if it is “stabbed in the back” by its allies. But the pressure may have been strong. Several days of talks between Kiev and Washington culminated in a visit by National Security Adviser Jake Sullivan with Zelensky. Perhaps coincidentally, Sullivan has also reportedly “been in contact with Yuri Ushakov, a foreign-policy adviser to Mr. Putin” and with Russia’s Security Council Secretary Nikolai Patrushev. U.S. officials reportedly told Zelensky that Kiev “must show its willingness to end the war reasonably and peacefully.”

On November 8, the messaging from Ukraine suddenly changed dramatically. Zelensky announced that he is now open to diplomacy with Putin and urged the international community to “force Russia into real peace talks.” Zelensky insisted that his preconditions for talks are “restoration of (Ukraine’s) territorial integrity … compensation for all war damage, punishment for every war criminal and guarantees that it will not happen again.” Washington insists that its message was not an attempt to push Ukraine to the negotiating table, but rather an attempt to manage international perceptions. The plan was to “reinforce to the world that it’s Ukraine, not Russia, that wants to resolve the conflict.” One official said, “That doesn’t mean they need to go to the negotiating table right now. We don’t even think right now is the right time based on what Russia is doing.

“Morale requires that the next Russian move has to be [a] big push with strategic significance.”

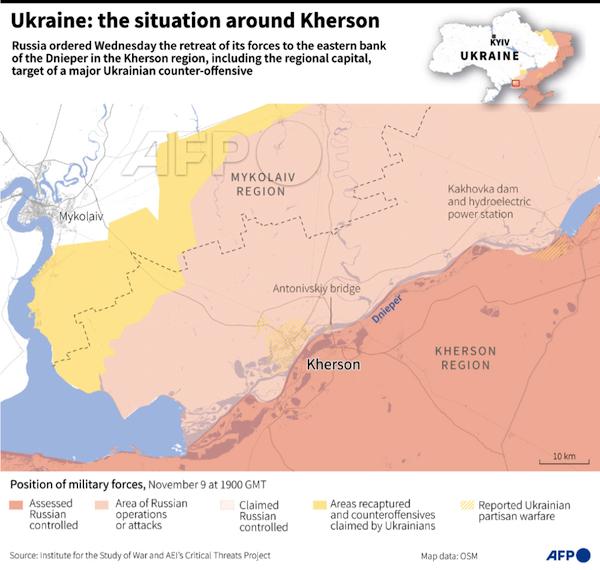

• The Pullout From Kherson (MoA)

The Russian command decided to remove its troops in the Kherson region from the left bank of the Dnieper. Defense Minister Sergei Shoigu did not look happy when he gave the order. He knows that another such setback will cost him his job. This move looks bad. That alone will have consequences. The Ukrainians, the Biden administration and the European supporter of Ukraine will be emboldened by this. The support in Russia for the war will shrink. Some people in Russia will start to call for President Putin’s head. There is no danger though that they will get it. This move is operationally sound. From the military point of view there is little chance to withstand a serious attack in the region as the resupply across the Dnieper river is very difficult and can not be guaranteed.

Moreover the possible breach of the Dnieper river dams would make any resupply impossible for at least a week or even longer. That would be enough time for the Ukrainians to slaughter whatever number of Russian troops were left behind. Strategically the move is bad. It closes for now the possibility of moving into Nikolaev (Mykolaiv) and further towards Odessa. This could have and should have been done earlier. But the Russian command did not commit sufficient forces for that fight. There were also sound reason for not doing that. Now it is too late to criticize those decisions. It is quite possible that, behind the scene, a deal has been made over this. If one was made we are unlikely to learn of it anytime soon. The priorities now should be to get the soldiers and equipment out of the area. It will require intense air defense coverage to prevent the close down of ferry points by Ukrainian artillery.

There is no reason to make it easy for the Ukraine to regain the area. Until the evacuation is done any significant Ukrainian move into the area should be responded to with effective artillery fire. Soon the Ukrainian army will start to move troops prepared for an attack in Kherson to other front lines. Russia must likewise move its troops to reinforce its positions elsewhere. Morale requires that the next Russian move has to be [a] big push with strategic significance. The concept of deep battle and deep operations should be reapplied. Historically it has nearly always worked to Russia’s advantage. But the big push does not need to be solely militarily. A further significant damage of Ukraine’s economy via its electricity network is an additional option. To severely interdict its supply lines from the west is another one.

“Apparently, the EU needs to undermine its economy completely before calls to start the dialogue will be accompanied by concrete steps..”

• Moscow Sets Out Conditions For Talks With EU (RT)

Russia is open to any negotiations with the EU to find a way out of the current crisis, Foreign Ministry spokeswoman Maria Zakharova told local media on Thursday. However, she voiced concerns that any meaningful discussions may start only after the bloc has “completely destroyed” its own economy. Speaking to the Russian newspaper Argumenty i Fakty, Zakharova addressed a recent NBC report alleging that some Western officials believe that the upcoming winter may spell an opportunity for talks between Moscow and Kiev. However, she noted that Western calls to seek a diplomatic solution to the Ukraine conflict, “unfortunately are just rhetoric,” adding that all EU policies, including military support for Ukraine, “are aimed at escalation.”

The shift in narrative has been spurred by an emerging rift between ordinary European citizens and policymakers, she believes. The former “are getting tired of permanent confrontation rhetoric and endless baseless accusations against Russia,” the spokeswoman said, adding that “there is a growing demand for putting an end to the Ukraine conflict.” These concerns are also underpinned by Europe’s economic woes, Zakharova continued. “News about new sanctions or regular calls to ‘punish’ Russia economically scare Europeans themselves,” she noted. “Apparently, the EU needs to undermine its economy completely before calls to start the dialogue will be accompanied by concrete steps,” the official remarked, adding the bloc is pursuing these policies to please the US. According to Zakharova, Moscow is open to “discussing ways out of the current crisis,” but any peace settlement must be of some benefit to Russia.

“It is important that any proposals take into account the real situation ‘on the ground’ and have an added value for our country,” she noted.In recent months, top EU officials have been sending conflicting signals about their stance on possible engagement with Moscow. While EU foreign policy chief Josep Borrell claimed in April that the conflict in Ukraine “will be won on the battlefield,” last month he said that Brussels is ready to seek a “diplomatic solution” while vowing to continue to support Kiev militarily. Russian officials have repeatedly stated they are ready to conduct negotiations with Kiev to end the conflict. Meanwhile, Ukrainian President Vladimir Zelensky has set out conditions for any diplomatic engagement, which include the “restoration of [Ukraine’s] territorial integrity,” “compensation for all war damage” and “punishment of every war criminal.”

“..the Europeans still constituted a new and serious – although declining – rival for God’s own People..”

• The Collective West Might Be Losing The War With Eurasia (Lee)

[..] of all people, Leon Trotsky writing in, (War – In the International 1933) – opined … ‘’That prior to WW2 the US was Europe’s debtor but now Europe was relegated to the background. The United States is the principal factory, the principal depot and the Central Bank of the world.’’ America’s hegemony over Europe long pre-dated WW2 and actually later grew larger with the addition of ex Eastern European states which had been formerly part of the Soviet sphere of influence. Western Europe had willy-nilly long since been subordinated to the USA. A while later (1946) the Americans gave the British short shrift reminding them that they would have to adjust to the post-war realities and take the medicine – the American loan, as Michael Hudson explains:

‘’In effect the Sterling Area was to be absorbed into the Dollar Area, which would be extended throughout the world. Britain was to remain in a weak position in which it found itself at the end of WW2, with barely any free monetary reserves and dependent on dollar borrowings to meet its current obligations. The United States would gain access to Britain’s pre-war markets in Latin America, Africa, the Middle East and Far East. This first loan on the post-war agenda – which President Truman announced in forwarding it to Congress would set the course of American and British economic relations for many years to come. Truman was well aware of the change of fortunes for the UK, for the Anglo-American Loan Agreement spelled the end of Britain as a great power.’’(1)

Sometime later and under the changed geopolitical and economic conditions President Richard Nixon and his economist acolytes placed their chief diplomat, Henry Kissinger, in charge of arrangements to put in place a policy to keep the Europeans subordinate and while they were at it to simultaneously endeavor to put a limit on Japanese expansion. Then came the big game-changer: Gold was officially delinked from the US$ in August 1971. Nixon’s currency reforms – were designed among various other decisions and also generally aimed at European and Japanese interests. It should be noted that Japan did not play any political role at all but simply followed in America’s wake, as she invariably did in economic and even political matters since.

This unilateral decision by the Americans to deprive paper money from convertibility into gold was enough to tip the Europeans into disorder and turbulence. For all their protestations of loyalty in Europe, the leaders of each country feverishly groped for an outcome that answered their own interests. However still licking their wounds, and for all their weakness, the Europeans still constituted a new and serious – although declining – rival for God’s own People, American capitalism-imperialism, which says a lot about how far the former had slid down the slippery-slope.

“..those loans would have long maturities of up to 35 years and require no repayment of the principal before 2033..”

• Zelensky Says EU’s €18 Billion Aid Is What “True Solidarity” Looks Like (ZH)

What’s not to like about a massive interest-free loan that won’t have to be paid back for decades, or maybe never? Ukraine’s President Volodymyr Zelensky says it shows “true solidarity”… “Grateful to the European Commission and President Ursula von der Leyen for announcing 18 billion-euro financial aid package for 2023,” Zelensky announced on social media Wednesday. “This shows true solidarity of the EU.” The EU Commission President explained in a statement that the whopping €18 billion support package for 2023 is being mulled to prepare the ground for the reconstruction of Ukraine as it continues on the path toward EU membership, after it was granted candidate status on June 23 of this year.

As Politico reported earlier, “Commissioners meeting today for their weekly College meeting will propose a new EU instrument to finance €18 billion (around €1.5 billion a month) in subsidized loans for Ukraine for 2023, according to a draft regulation also obtained by Paola.” The draft regulation reads as follows: “In order to finance the support under the Instrument in the form of loans, the Commission shall be empowered, on behalf of the Union, to borrow the necessary funds on the capital markets or from financial institutions.” The Commission would reportedly link interval disbursement of the funds based on commitments from Kyiv upholding ‘rule of law’ requirements and making democratic reforms, again as preparation for potential future EU admission.

According to further details, “Though the funds would officially be in the form of loans (aside from additional voluntary contributions by EU governments), those loans would have long maturities of up to 35 years and require no repayment of the principal before 2033. Interest would be subsidized by EU member countries.” The proposed package comes after last Thursday Ukrainian parliament approved a draft so-called “victory budget” for 2023, with a “record deficit” of $38 billion, including a little over $27 billion for the nation’s armed forces. Naturally the bulk of this is expected to be filled by donors, the IMF, United States and European Union.

Only one man can raise the billions required to save FTX pic.twitter.com/Y4wSuYlf3f

— . (@SundownerCrypto) November 9, 2022

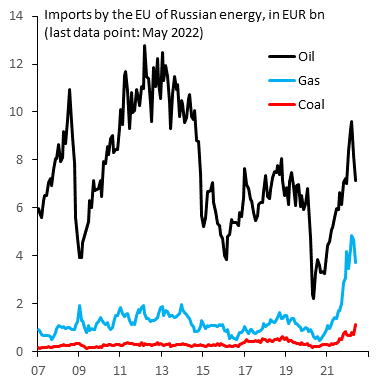

Europeans pay twice: billions for “True Solidarity” and double energy prices.

• Energy Bills In Europe Are 90% Higher Than Last Year (OP)

Electricity and gas prices are soaring across Europe, with bills close to double from last year in most European capitals, according to new data from the Household Energy Price Index – a monthly tracker of energy prices for households across 33 European capitals, including the 27 EU member states and several non-members. According to the data collected for the HEPI, natural gas bills in Europe have gone up by as much as 111 percent over the past year, with electricity prices up by an average of 69 percent. Taken together, Euronews calculates these two make for a total 90-percent increase in household energy bills over the past year.

“Significantly higher [energy prices] compared to one year ago … can be attributed to a combination of factors, such as increased demand connected to post-pandemic economic recovery and extraordinary weather conditions, the record-high prices for natural gas, and high CO2 emissions allowances,” the authors of the latest HEPI report noted. The high energy bills are creating headaches for European governments: strikes and protests are multiplying and disgruntlement with energy policies is growing. The cost of living in most of Europe is already exorbitant because of the energy crisis and this crisis is only going to get worse after the EU embargoes on Russian oil and then fuels come into effect.

In some parts of Europe, according to the latest HEPI report, energy prices have reached record highs but in others, prices have actually fallen, at least in October. The news is not as good as it looks at first glance: the decline was a result of government intervention, i.e. energy subsidies. There have been a lot of subsidies as European governments try to alleviate the financial pain on households and businesses to avoid further disgruntlement. Germany alone will be spending some $200 billion on such coping measures, including a cap on energy prices up to a certain level of consumption.

“Basically, we are the only ones in Europe who are arguing in favor of peace..”

• Hungary Explains ‘Total Failure’ Of Sanctions On Russia (RT)

The sanctions on Russia have not achieved any of the EU’s stated goals and only backfired by hurting the economies of member states, Hungarian Foreign Minister Peter Szijjarto has said.The EU, along with the US and several other countries, imposed sweeping restrictions on Moscow in response to its military operation in Ukraine, which was launched in February. “The sanctions which have been introduced by the European Union [against] Russia have failed. It’s a total failure,” Szijjarto told Jordan’s Roya News on Sunday. It was said by the European Commission that the sanctions will help us to conclude this war as soon as possible and that it will bring Russia’s economy to its knees. What’s the outcome? It’s totally the opposite.

“The war is becoming more and more brutal … And, in the meantime, the European economy is suffering very badly,” Szijjarto stated, adding that the continent has been hit by a “tremendous energy crisis,” as well as high inflation and rising food prices. The minister said that Hungary paid €7 billion ($6.9 billion) for energy imports in 2021, but has to pay €19 billion ($18.9 billion) this year. “That’s huge. And this is the outcome of a failed sanctions policy.” Szijjarto said that, instead of economic restrictions, the EU should focus on achieving peace in the region. He argued that a settlement in Ukraine could come as a result of negotiations between Russia and the US.

“Basically, we are the only ones in Europe who are arguing in favor of peace,” he said. The foreign minister defended Hungary’s decision to reject Kiev’s calls to send weapons and not to participate in the training of Ukrainian troops. These measures “contribute to escalation” rather than helping to end the conflict, he said.Hungary’s economy heavily relies on Russian energy, and the government has resisted Brussels’ plans to completely ban oil and gas imports from Moscow. After tense negotiations, Budapest received several exemptions from the bloc-wide restrictions on purchases of Russian fossil fuels. Hungary said this week that it will not support the EU’s joint loan package, which would secure €18 billion ($17.9 billion) in aid for Kiev.

Ursula vs Michel. The failure of the EU personified.

• The Dysfunctional Relationship At The Heart Of The EU (Pol.eu)

When the leaders of the world’s most powerful countries meet at the G20 summit in Bali next week, don’t expect the European Union to present a united front. Rather than coordinate, the bloc’s top two officials — European Commission President Ursula von der Leyen and European Council President Charles Michel — are more likely to avoid each other, with staffers involved in organizing the trip under strict instructions to avoid any overlap in itineraries. In the nearly three years since their tenures began, relations between Michel and von der Leyen have undergone an extraordinary breakdown, with staff from the two institutions discouraged from communicating and the two leaders locking each other out from meetings with foreign dignitaries.

The dysfunctional partnership is not only impacting the EU’s legislative and political agenda, which depends on a delicate inter-institutional balancing act. It’s also threatening to undermine the EU’s standing in the world. One of the centerpieces of the G20 will be a meeting between Michel and Chinese leader Xi Jinping scheduled to take place on the fringes of the summit. Given the divisions within the EU about how to deal with Beijing, it’s shaping up to be a crucial meeting. But von der Leyen hasn’t been invited. The reason? Her refusal to allow Michel to attend a meeting with Indian Prime Minister Narendra Modi at the G7 in Germany in June. Rivalry between the Commission and the Council has long been a challenge due to an inherent structural tension within the EU’s byzantine system.

The Commission is the bloc’s executive arm, with the ability to propose legislation, putting its president at the heart of nearly every EU initiative. But the Council is where heads of state or government meet to turn proposals into law. Though its president plays a coordinating role, moderating the debate between the real decision-makers, the position is arguably closer to where the bloc’s real power lies. One of the centerpieces of the G20 will be a meeting between Michel and Chinese leader Xi Jinping scheduled to take place on the fringes of the summit. Given the divisions within the EU about how to deal with Beijing, it’s shaping up to be a crucial meeting. But von der Leyen hasn’t been invited. The reason? Her refusal to allow Michel to attend a meeting with Indian Prime Minister Narendra Modi at the G7 in Germany in June.

“.. it’s worth being looked at.”

• Biden Supports National Security Review of Elon Musk Twitter Purchase (Turley)

President Joe Biden said on Wednesday that “I’m not going to change anything” after the midterm elections even with the possible loss of one or both houses of Congress. One thing that did not change is Biden’s continued suggestion that his political opponents are fascists or national security threats. Biden is now supporting an investigation into whether Elon Musk’s taking over of Twitter is a national security threat. Biden’s statement comes just a couple days after Musk’s call for supporters to vote for Republican control of Congress and the President attacking him for his plan to restore free speech protections on Twitter. During a press conference at the White House, a reporter asked Biden if he thought Musk was a national security threat because of his business ties to Saudi Arabia. Biden responded:

“I think that Elon Musk’s cooperation, and/or technical relationships with other countries, uh, is worthy of being looked at. Whether or not he is doing anything inappropriate, I’m not suggesting that. I’m suggesting that … it’s worth being looked at.” This followed Biden’s tirade against Twitter for moving toward less censorship. The President seriously asked “how do people know the truth” if social media companies did not control what they could read or hear on these platforms. Biden could have simply demurred and said that he would leave such matters to the responsible agencies to consider. Instead, he added his call to those of Democratic politicians and pundits to initiate a national security review.

The call to unleash a national security review on Musk’s takeover is being pushed by various liberal legal experts and pundits without any sense of concern over the use of such powers for political ends. Among those calling for an investigation is Sen. Chris Murphy, D-Conn., who asked the Committee on Foreign Investment in the United States (CFIUS) to review the deal. Of course, many of these Democratic leaders and pundits supported Twitter silencing those with opposing views for years. In previous hearings, Democratic senators demanded greater censorship from Twitter in areas ranging from Covid to climate change. However, according to Murphy, they are now worried about “the potential influence of the Government of Saudi Arabia” and “[a]ny potential that Twitter’s foreign ownership will result in increased censorship, misinformation, or political violence is a grave national security concern.”

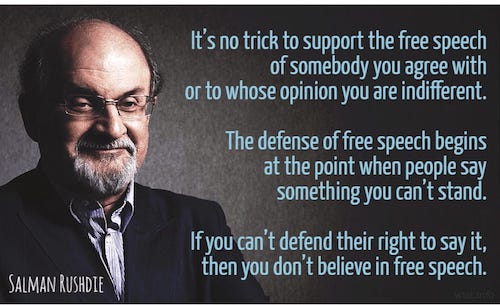

But this is not “.. worth being looked at.”

• Biden: GOP Vow To Investigate Son Hunter’s Business Deals ‘Almost Comedy’ (JTN)

In his post-election press conference, President Biden derided the House GOP’s pledge to investigate his son Hunter’s foreign business dealings as “almost comedy.” GOP Congressman James Comer, the potential chair of the House Oversight Committee, has said Hunter’s business deals in China, Russia and Ukraine pose a national security risk and might have “compromised” the president himself. Biden was asked on Wednesday for his message to Republicans who are considering investigating his family and, particularly, his son Hunter’s business dealings. “‘Lots of luck in your senior year,’ as my coach used to say,” Biden retorted. “Look, I think the American public want us to move on and get things done for them.

“It was reported — whether it’s accurate or not, I’m not sure — but it was reported many times that Republicans were saying, and the former president said, ‘How many times are you going to impeach Biden?’ You know, impeachment proceedings against, I mean, I think the American people will look at all of that for what it is. It’s just almost comedy. I mean, it’s — but, you know, look, I can’t control what they’re going to do. All I can do is continue to try to make life better for the American people.” Comer said in September that the U.S. Treasury Department has refused to provide Biden family members’ “suspicious foreign business transactions” that were flagged by U.S. banks. “We’re not investigating Hunter Biden for political reasons,” Comer said. “We’re investigating Hunter Biden because we believe he’s a national security threat, who we fear has compromised Joe Biden.”

If Trump next week wants to announce running, he will do it without the momentum.

• Gingrich Suspects Trump Rethinking 2024 (JTN)

Former House Speaker Newt Gingrich told Just the News that former President Donald Trump is likely “rethinking and reappraising” running for president again in 2024, adding that he personally doesn’t see a scenario where Florida Republican Gov. Ron DeSantis decides not to run for president in 2024. “I mean, just in my own emails today, the number of people who want somebody other than Trump who have decided, literally overnight, that person is going to be DeSantis, he’s going to find it almost impossible to avoid running,” Gingrich said on Wednesday. “I think Trump’s got to look at the results and be troubled,” he added. “I can tell you, for me, this was not the result I expected. I thought we’d win a lot more seats.”

Gingrich added that Republicans have to look at the results and ask themselves what they did wrong and where they go from here. Gingrich was asked if he thinks Trump is going to announce a 2024 run or decide that it’s no longer his time. “I think he’s a very, very smart man,” he said. “And I’m sure that he is very disappointed. He worked very hard. He did a whole array of rallies with thousands of people. And I know, because I have the same feeling, I know that he went into Election Day thinking it was going to be a huge success. And I suspect that he’s going through the same kind of rethinking and reappraising that I’m going through.

“He is a very smart guy, and he’s got asked two questions: Can he in fact beat DeSantis? He probably would say yes. Coming out of that fight, would he be able to win a general election? I don’t think he wants to run and, you know, have that kind of situation.” Gingrich elaborated on his personal reaction to the results of the midterm election so far. “I was pretty shaken because that was not the election I expected,” he admitted. “And I don’t have as much confidence in my own judgment as I would have had yesterday morning.”

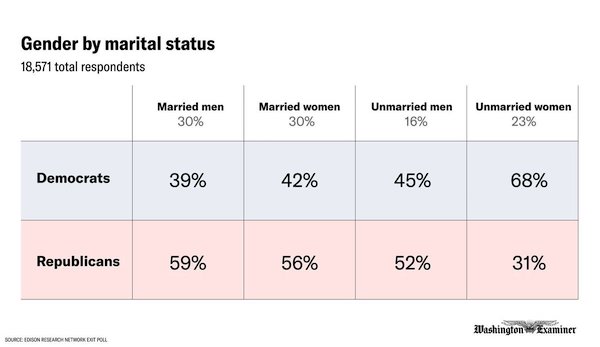

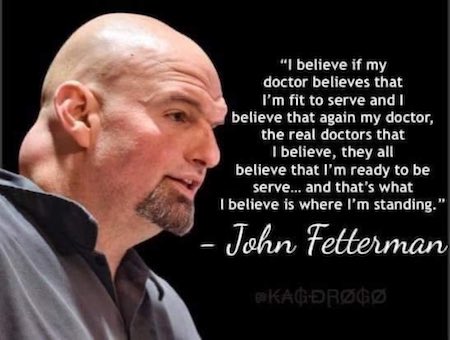

“Democrat party officials and political activist groups knew how to exploit the opportunities within the new system of ballot distribution and collection..”

• 2022 Midterms Highlight the Distinct Difference Between Ballots and Votes (CTH)

As the political discussion centers on the 2022 wins and losses from the midterm election, one thing that stands out in similarity to the 2020 general election is the difference between ballots and votes. It appears in some states this is the ‘new normal.’ Where votes were the focus, the Biden administration suffered losses. Where ballots were the focus, the Biden administration won. Perhaps the two states most reflective of ‘ballots’ being more important than ‘votes’ are Michigan and Pennsylvania. Despite negative polling and public opinion toward two specific candidates in those states, Michigan Governor Gretchen Whitmer and Pennsylvania Senate candidate John Fetterman achieved victories. Whitmer and Fetterman were not campaigning for votes, that is old school.

Instead, the machinery behind both candidates focused on the modern path. The Democrat machines in both states focused on ballot collection and ignored the irrelevant votes as cast. Since the advent of ballot centric focus through mail-in and collection drop-off processes, votes have become increasingly less valuable amid the organizers who wish to control election outcomes. As a direct and specific result, ballot collection has become the key to Democrat party success. The effort to attain votes for candidates is less important than the strategy of collecting ballots. It should be emphasized; these are two distinctly different election systems. The system of ballot distribution and collection is far more susceptible to control than the traditional system of votes cast at precincts.

A vote cannot be cast by a person who is no longer alive, or no longer lives in the area. However, a ballot can be sent, completed and returned regardless of the status of the initially attributed and/or registered individual. While ballots and votes originate in two totally different processes, the end result of both “ballots” and “votes,” weighing on the presented election outcome, is identical. While initially the ballot form of election control was tested in Deep Blue states, through the process of mail-in returns under the guise and justification of “expanding democracy,” a useful tool for those who are vested in the distinction, I think we are now starting to see what happens on a national level when the process is expanded.

The controversial 2020 election showed the result of making ‘ballots’ the strategy for electoral success. Under the justification of COVID-19 mitigation, mail-in ballots took center stage. Ballot harvesting by Democrat operations was one term for the outcome. Democrat party officials and political activist groups knew how to exploit the opportunities within the new system of ballot distribution and collection, and when you combine that with a massive legal pressure campaign to accept any and all forms of ballots, well, you can see how they are dependent.

“On Thursday, he tweeted that the platform’s usage continued to rise: “One thing is for sure: it isn’t boring!”

• Executives Flee Twitter As Musk Mentions ‘Bankruptcy’ (RT)

At least six executives have reportedly resigned from Twitter this week. The social media platform’s new owner Elon Musk has called an all-hands meeting on Thursday, announcing a return to office hours and mentioning the possibility of bankruptcy unless the company can find a way to become profitable. Among the departures was the head of safety and moderation Yoel Roth, Bloomberg reported citing insider sources. Musk had kept Roth on despite the complaints from conservatives that he had been responsible for much of the political censorship on the platform – one of the reasons the Tesla and SpaceX billionaire cited for buying the company. “The economic picture ahead is dire,” Musk wrote in an email calling the meeting, according to the New York Times.

“Without significant subscription revenue, there is a good chance Twitter will not survive the upcoming economic downturn.” Unless Twitter can generate profits from its $8 monthly Blue program, bankruptcy is a very real possibility, Musk reportedly said, adding that the platform is currently too dependent on advertising.A number of companies have pulled their ads from Twitter in recent weeks, due to a pressure campaign by activists angry at Musk’s buyout of the company – and endorsement of Republicans in the US midterm elections.Musk also told staff that the days of free food, teleworking and other perks were over, according to multiple outlets. “If you can physically make it to an office and you don’t show up, resignation accepted,” he reportedly said.

Along with Roth, five other executives quit this week. The heads of privacy, information security and compliance resigned just before the deadline to submit a report to the US government, required under a 2011 settlement with the Federal Trade Commission.The FTC is “tracking recent developments at Twitter with deep concern,” said spokesman Douglas Farrar, adding that “no CEO or company is above the law.” On Wednesday, US President Joe Biden told reporters “there’s a lot of ways” to investigate Musk’s acquisition of Twitter as a potential national security risk. Musk has warned the public that Twitter “will do lots of dumb things in coming months.” On Thursday, he tweeted that the platform’s usage continued to rise: “One thing is for sure: it isn’t boring!”

Interesting take by Stefano Scoglio. “And that also explains why this material is so toxic without needing to introduce any spike protein.”

• mRNA “Vaccines” Causing Cells To Produce Spike Proteins Is A Fairy Tale (OffG)

“Why, then, is it impossible for mRNA to enter the cell and cause it to produce spike proteins?” The first thing the researchers in the field state is that the living cell is a “formidable barrier”, very difficult if not impossible to penetrate. And then they list 5 factors that prevent the mRNA to enter cells, getting into the ribosomes where the spike protein is supposed to be produced: First: As soon as the genic material is injected, it is attacked by specific enzymes called extra-cellular ribonucleases, which degrade any foreign genetic material. Pharmaceutical companies claim that the lipid nanoparticles are supposed to protect the mRNA from the enzymatic attack: But nobody knows how much protection is offered. As the Pfizer “vaccine” injects 30 micrograms of mRNA, let’s say that about half, 15 micrograms, survive.

Second: At this point, the mRNA/lipids blend has to enter the cell, supposedly through endocytosis, i.e. the cell is forming an external pouch that brings in the material. But, the researchers state, often instead of endocytosis the cell produces exocytosis, that is the pouch is used to keep the foreign material outside: Let’s say that half enters and so we now have 7.5 micrograms inside the cell. Third: At this point enters the endosomes/lysosome system: all scientists in the field know that this enzymatic endocellular system attacks, degrades and eliminate at least 98 percent of any foreign material entering the cells. We are now down to 0.15 micrograms, that 150 nanograms, an infinitesimal quantity.

Fourth: If this were the end, you could at least claim that a very minuscule dose would enter the ribosomes. But alas, the ribonuclease enzymes are also inside the cell, they are called endocellular ribonucleases, and they would dispose very quickly of the minuscule amount of mRNA. Finally, the researchers mention a fifth element, the most important, the one that makes all the processes described so far completely useless and unnecessary. And that also explains why this material is so toxic without needing to introduce any spike protein. They indicate that these “vaccines” are so highly immunogenic. Indeed, they use this word immunogenic.

Quality Issues With mRNA Covid Vaccine Production

Dark.

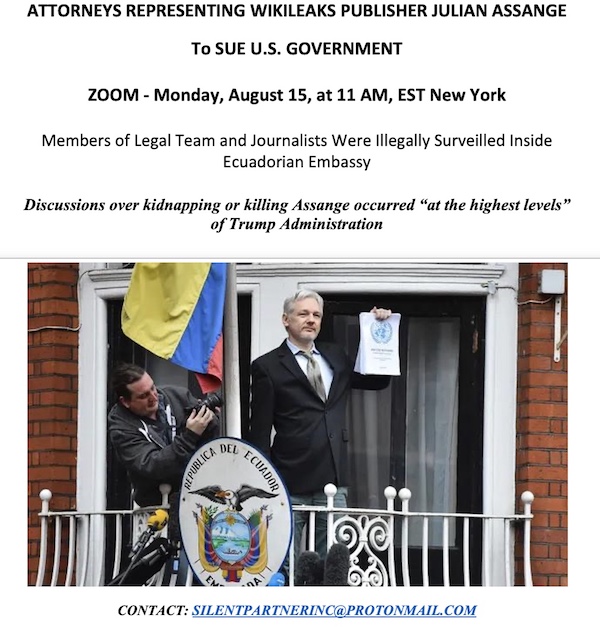

• UK Exec Wining, Dining With People Plotting To Kill My Husband – Stella (DecUK)

Assange’s treatment in the US would be much worse. In 2020, UK District Judge Vanessa Baraitser blocked Assange’s extradition to the US because of the risk of suicide under the onerous conditions he would face. Baraitser’s decision was based on the fact that, if convicted, Assange would likely be moved to the ‘Supermax’ Administrative Maximum Facility (ADX) in Florence, Colorado, home to convicted terrorist Abu Hamza and Mexican druglord El Chapo. A former warden of the prison has said: “There’s no other way to say it — it’s worse than death.” Pre-trial, Assange could also be held under Special Administrative Measures, or SAMs, where inmates spend 23 or 24 hours a day in their cells with no contact with other prisoners.

The US then appealed Baraitser’s ruling, saying it would promise that Assange would not be subject to SAMs or housed in ADX. Crucially, though, the US reserved the right to reverse these promises in case of further violations by Assange, which can be easily invented. In December 2021, the UK High Court agreed with the US appeal and reversed the lower court decision not to extradite Assange. Many believe Assange would commit suicide before being put on a plane to the US. “I’m convinced that Julian cannot survive under the conditions the US will put him in,” says Stella. “I have no doubt they will put him in a regime of isolation. The only reason he’s surviving now is because he’s able to see me, to see the children. He has a hope of fighting extradition to the US.”

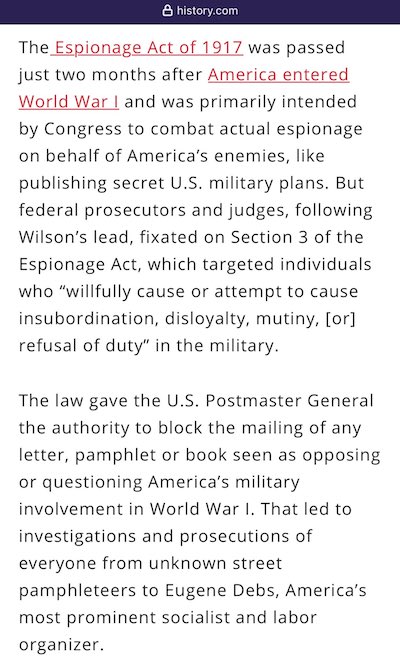

She adds: “He’s facing trial in the Eastern District of Virginia with a jury that will be composed of people who are either working for or somehow linked to the national security sector, because that is what that area is. That is the jury pool. He faces 175 years under the Espionage Act, under which there is no defence. He cannot explain, he cannot justify, he cannot defend himself from the accusation.” She pauses. “Under the indictment, Julian is accused of conspiring with a source to publish information: receiving that information from the source, possessing that information, and communicating it to the public. That is journalism. And if you define journalism as a crime, then Julian is guilty and he has no defence.”

Saylor

My discussion this morning on the virtues of #Bitcoin, the vices of #Crypto, the wisdom of Satoshi, and the future of Digital Assets with @MorganLBrennan, @davidfaber, & @carlquintanilla.pic.twitter.com/LcidKLpfGg

— Michael Saylor⚡️ (@saylor) November 10, 2022

Cow

https://twitter.com/i/status/1590775125049081856

Moon

The video is shot inside the Arctic Circle right between the border of Canada, Alaska and Russia. It lasts only a few seconds, but it is worth admiring the spectacular view.

Th can be seen for 36 seconds only once a year; the moon appears in all its splendor and then disappears. pic.twitter.com/wKclPu9Nbx— Vishwanath Prabhu (@VishwaPrabhu61) November 7, 2022

Support the Automatic Earth in virustime with Paypal, Bitcoin and Patreon.