Hannah Höch Cut with the Dada Kitchen Knife through the Last Weimar Beer-Belly Cultural Epoch in Germany 1919

SNL

When SNL is doing skits like this, you know that they think Kamala’s cooked. Mood shifted. I see zero on the ground excitement for her. The whole administration is a joke to normal people. A sick, sad, long joke that we’re ready to be done with!pic.twitter.com/jDShu4A6Mg

— Robby Starbuck (@robbystarbuck) October 13, 2024

Mechazilla has caught the Super Heavy booster! pic.twitter.com/6R5YatSVJX

— SpaceX (@SpaceX) October 13, 2024

Tesla

Dan Ives: “I've covered tech for almost 25 years – What I saw yesterday in LA, I think was a game-changer. This is the new chapter, the new book for @Tesla – Tesla is front and center of the 4th Industrial Revolution.” pic.twitter.com/fMRUEolZYA

— ALEX (@ajtourville) October 12, 2024

Trump water

Trump's solution for solving the California water crisis is so detailed & GENIUS. He wants to prevent water from the Klamath River from being dumped into the Pacific Ocean and re-route it back into the cities

"We'll say, Gavin, if you don't do it, we're not giving you any of… pic.twitter.com/6EziTWFTGf

— George (@BehizyTweets) October 13, 2024

Letitia

https://twitter.com/i/status/1845175071771590960

Walz

FINALLY a journalist asks the logical question:

How can you "turn the page" on an administration Kamala is PART OF and says she wouldn't change anything about?

A panicked Tim Walz replies that she's not Trump.

He's got nothing. pic.twitter.com/Ih0K2jjGbR

— Tim Young (@TimRunsHisMouth) October 12, 2024

Hand counting

WATCH: Since when did it become “nerve racking” for ballots to be counted in front of poll watchers?

This election official in GA said that his senior citizen ballot counters will need rest to perform any audits.

Somethings up in GA.

— Gunther Eagleman™ (@GuntherEagleman) October 12, 2024

Cardone

https://twitter.com/i/status/1845247125116027096

Zakharova

https://twitter.com/i/status/1845109011533955482

”We got a problem. I actually worry about the next three months..”

If he leads the polls, they can throw a war in his lap. Probably Iran.

• Trump Warns of World War III Because of Biden Administration (RT)

The US is dangerously close to sliding into World War III within months due to the policies of the administration of President Joe Biden, Republican presidential candidate Donald Trump has said. Speaking at a campaign rally on Saturday in California, a Democratic Party stronghold, Trump claimed that an overwhelming majority of Americans believe the country is on the wrong track. The former president said, however, that he has an even more pressing concern. ”We got a problem. I actually worry about the next three months… I worry we’ll end up in a world war because of the people that we have [in the administration],” he said. Trump promised that if he is elected president in November, he would “act with urgency and speed to save America and to rescue the people of California from [Democratic nominee] Kamala Harris’ atrocious failures.”

He added that during his time in office, he “kept… [the] country safe, we had no wars.” “I’ll keep you out of wars… I will end [the] war in Ukraine, stop the chaos in the Middle East, and I will prevent very definitely World War III,” he said. The Republican has repeatedly promised to end the Ukraine conflict within 24 hours of being elected, before even being sworn into office, although the details of the plan remain largely unknown. According to his running mate, J.D. Vance, Trump could start talks with Russia, Ukraine, and European stakeholders to establish a demilitarized zone along the current front line, with Kiev agreeing to stay out of NATO. Harris, who has been a staunch supporter of Ukraine, has criticized Trump’s approach, claiming that he would essentially force Kiev to surrender.

The Kremlin has also expressed skepticism about the Republican’s promises of peace, with spokesman Dmitry Peskov suggesting that he does not “think there is a magic wand” that can stop the fighting overnight. In June, Russian President Vladimir Putin said that Moscow would immediately agree to a ceasefire and start peace talks if Kiev began withdrawing troops from the Russian regions of Donetsk, Lugansk, Kherson, and Zaporozhye, and committed to neutrality. Later, he also signaled that a precondition for talks also includes the complete withdrawal of Ukrainian troops from Russia’s Kursk Region.

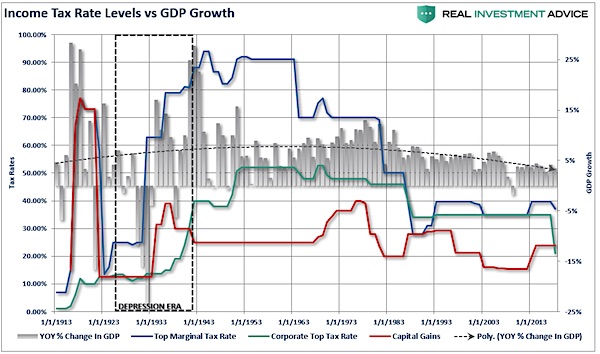

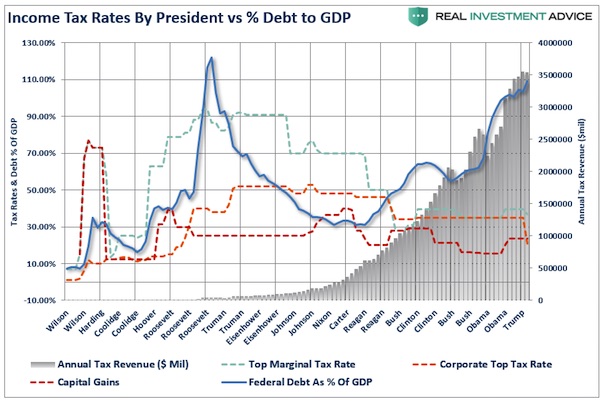

Trying to simplify taxes?!

• The Tax Cut Tour: Trump Targets Voters With More Breaks (RCW)

In Michigan, during remarks before the Detroit Economic Club, former President Trump vowed to make interest on car loans fully tax deductible, a proposal that would be a boon to the automobile industry in Michigan and elsewhere – and which is merely the latest promise in what has become a pattern. Trump told voters in Nevada that he would eliminate taxes on tips earlier this summer. The Republican nominee followed that up this fall by promising to restore the state and local tax deduction, a key tax deduction that he and congressional Republicans eliminated while president and which, if restored, would be a benefit to suburban voters in states like New York, New Jersey, and California. Trump has also called for making Social Security benefits tax-free. Seniors, who would benefit from that last proposal, live, well, everywhere. While Americans over 50 are the largest voting bloc, the beneficiaries of the latest tax slash are much smaller: Citizens living abroad.

“I support ending the double taxation of overseas Americans,” Trump told The Wall Street Journal Thursday, a reference to his plan to lower the tax burden of the small number of citizens who pay both federal taxes and taxes to the foreign government where they reside. As the Journal reported, it was a play to win support from an often-overlooked group of voters. All the proposed tax slashing has left some heads reeling. “Trump’s just throwing darts at the populist-pandering dart board. Economic coherence be damned,” said Brian Riedl, senior fellow at the Manhattan Institute, a center-right think tank. The politics, meanwhile, are undeniable. Vice President Kamala Harris found herself playing catch up when she unveiled a similar “no tax on tips” proposal. Republicans complain that Harris is playing “copy-cat.” Her proposal does differ from that of Trump, however, in that she supports eliminating taxes on tips only for those making under $75,000 and would pair that reform with legislation boosting the minimum wage for tipped workers from $2.13 an hour to $7.25.

She has also slammed Trump’s tariff proposal as “a sales tax on the American people.” From the call to make auto loans tax-deductible to the tipping proposals, Indiana Rep. Jim Banks sees a through line: a focus on blue-collar voters. “President Trump understands the importance of working-class voters to our party,” Banks, a Trump ally and candidate for Senate, told RealClearPolitics. He said Republicans on Capitol Hill ought to follow the former president’s lead “and give middle-class families a tax break by making the TCJA’s individual rate cut permanent before the end of next year.” Promises come easy during election season. Actual strategies to get them into law are rare on the campaign trail. The question for all politicians: How will they deliver once in office? Asked how the former president would replace revenue lost to tax cuts, Trump spokeswoman Karoline Leavitt cited his track record rather than any specific legislative strategy.

“President Trump delivered on his promise to cut taxes in his first term,” she said. “He can be trusted to deliver on these promises in his second term.” Trump has already vowed that income from new tariffs would make up the federal revenue lost by tax cuts. Harris, meanwhile, has long argued, like most Democrats, that the rich ought to pay “their fair share.” Critics looking for technical specifics will find those broad answers unsatisfying, too. “If you demand all your current federal spending – or more – but also believe all taxes are illegitimate, Trump is your guy,” Riedl said before noting how Trump once described himself as “the King of Debt.” An estimate released by the Committee for a Responsible Federal Budget found that Trump’s plans could add as much as $15 trillion to the national debt over a decade, while Harris’ proposals would add nearly $8 trillion. No president from either party since Bill Clinton was in the Oval Office has taken the national debt and annual budget deficits seriously.

Paul Winfree, who served as Trump’s deputy director of the Domestic Policy Council, told RCP that the former president “understands something important that all the tax nerds do not.” While wonks in the Washington beltway have often criticized Trump’s instinct to slash taxes left and right, Winfree, now the president and CEO of the Economic Policy Innovation Center, said the candidate realizes “that you will pay a price for taking away benefits that people currently have, but that you’re not rewarded for allowing people to keep what they have either.” “So he’s looking to build on the Trump tax cuts,” Winfree said of his old boss, “which will be essential to maintaining a political coalition necessary to their success.” The election, meanwhile, is in less than a month. Tax Day, more than six.

“..Miller had presented fake VIP and press passes at the checkpoint. “They were different enough to cause the deputies alarm..”

• Third Trump Assassination Attempt Foiled – Law Enforcement (RT)

A third attempt on the life of Donald Trump was prevented on Saturday when law enforcement officers arrested an armed man with fake press passes outside the former US president’s rally in Coachella, California, a local sheriff has said. Vem Miller, a 49-year-old Las Vegas resident, was arrested at a checkpoint outside the rally venue on Saturday with an illegally owned shotgun, a loaded handgun, and a high-capacity magazine, the Riverside County Sheriff’s Office said in a statement on Sunday. Riverside County Sheriff Chad Bianco told local media that Miller had presented fake VIP and press passes at the checkpoint. “They were different enough to cause the deputies alarm,” Bianco told the Press-Enterprise. “We probably stopped another assassination attempt.”

Bianco described Miller as a “sovereign citizen,” referring to a loose collective of extreme libertarians who believe that the government cannot legally exercise authority over them. Miller is a registered Republican who holds a master’s degree from the University of California, Los Angeles, and ran for state assembly in Nevada in 2022, Bianco added. Miller has not confirmed or denied that he intended to assassinate Trump, Bianco stated. The 49-year-old suspect was released on $5,000 bail and will appear before a court in January charged with illegal firearms possession. Trump has survived two assassination attempts over the last three months. The former president and Republican presidential candidate narrowly avoided death at a campaign rally in Pennsylvania in July, when a bullet fired from around 150m away grazed his ear.

The gunman fired from a rooftop that had inexplicably been left unprotected by the Secret Service, and managed to kill one rally goer and injure two others before he was shot dead by a sniper. The second attempt took place at Trump’s golf course in West Palm Beach, Florida, in September. A gunman aiming at Trump from behind bushes was spooked by Secret Service agents and arrested after he fled the scene. The suspect, identified as Ryan Wesley Routh, had unsuccessfully attempted to join the Ukrainian military in 2022, and afterwards embarked on a scheme to recruit former Afghan commandos to fight for Kiev. American intelligence agents have claimed that Iran is seeking to assassinate Trump, and President Joe Biden has warned Tehran that he would treat an attack on his former political rival as an act of war.

“..no nominee in recent history has been ferried around in military planes ahead of an election.”

• Trump Campaign Requests Military Aircraft With Antimissile Capabilities (ZH)

Donald Trump has survived two assassination attempts within a very short period of time, but now with less than a month to go till the November election, his campaign is reportedly requesting the use of military aircraft and vehicles to protect him. Sources who spoke to the New York Times and Washington Post in Friday stories indicate the former president has requested much greater protections than US Secret Service agents currently provide him. There are also new reports saying he’s unlikely to play golf again until new expanded protocols are in place, as the Secret Service would have trouble protecting him on a golf course. The Washington Post reports based on emails it reviewed: “Donald Trump’s campaign requested military aircraft for Trump to fly in during the final weeks of the campaign, expanded flight restrictions over his residences and rallies, ballistic glass pre-positioned in seven battleground states for the campaign’s use and an array of military vehicles to transport Trump.”

The report further calls the requests “extraordinary and unprecedented” given that “no nominee in recent history has been ferried around in military planes ahead of an election.” The campaign has reportedly cited the Iran threat directed against Trump. Late last month he was given a special briefing by top US intelligence officials about alleged efforts of Tehran to assassinate him. A Sept. 24th statement from the campaign said, “President Trump was briefed earlier today by the Office of the Director of National Intelligence regarding real and specific threats from Iran to assassinate him in an effort to destabilize and sow chaos in the United States.” These new efforts to get military-level protections, which are typically only afforded to the sitting Commander-in-Chief, are based precisely on the belief that Iran is still trying to kill him.

The WaPo report says “Trump advisers have grown concerned about drones and missiles, according to the people.” Republican congressional leaders have also urged the necessity of greatly heightened protocols to protect the former president, to include protective military assets, such as when his plane goes from state to state in these final days leading up to the election: She [Susie Wiles, co-campaign manager for Trump] also wrote that the U.S. government has not been able to provide what the campaign views as an extensive enough plan to protect Trump. Rep. Michael Waltz (R-Fla.), a Trump ally who is on the House Intelligence Committee and the Butler assassination inquiry, wrote a letter to the Secret Service asking for military aircraft or additional protection for Trump’s private plane, according to a copy of the letter reviewed by The Post. CNN late Friday provided some further details on what exactly the Trump campaign is requesting:

“Trump’s campaign wants to use these resources – including access to military aircraft with deterrent systems to protect against surface-to-air missiles – as the former president crisscrosses the US during the final weeks of the presidential campaign.” President Joe Biden, when asked about Trump’s requests on Friday, said they should be fulfilled – “as long as he doesn’t ask for F-15s.” While mainstream media is likely to scoff at these requests, calling them “unprecedented”, it remains that it is also unprecedented that a former president who is running for the top office again should face two assassination attempts within just two months of each other, and with massive Secret Service failures to boot. Recently a foreign leader was ferried about the eastern US in a military plane: Zelensky. And Democrats didn’t bat an eye over a foreign leader getting such protections at the taxpayers’ dime, ironically enough.

“It’s pure McCarthyism. And unethical. And it’s scaring some lawyers away.”

• Group Threatening Lawyers’ Licenses If They Work For Trump (JTN)

While lawfare frequently has targeted GOP politicians, the tactic is spreading to the legal profession as a group called “The 65 Project” has taken to social media vowing to go after the licenses of attorneys who chose to work for former President Donald Trump. The 65 Project, which launched earlier this year as a “bipartisan” watchdog with both prominent Democrats and Republicans, announced it had launched digital and print advertisements in swing states such as Wisconsin and Michigan with the stark warning, “Don’t lose your law license because of Trump.” The managing director of the project said that 86 bar complaints have already been filed against attorneys who have filed election lawsuits on behalf of Trump following the 2020 election. “Across the country, lawyers who lent their credibility as officers of the court to Donald Trump to file factually and legally baseless claims to overturn legitimate election results have been investigated by state bar associations, been fined, had their licenses suspended, and even disbarred,” managing director Michael Teter said.

Following the 2020 election, Trump claimed that the election was stolen and there were multiple lawsuits filed in different states such as Georgia and Pennsylvania. While many of the lawsuits were unsuccessful, the lawfare against attorneys working for Trump or working on other election integrity cases was successful. Former New York City Mayor Rudy Giuliani who represented Trump in a Georgia election lawsuit, was disbarred in Washington, D.C. last month. This occurred just months after he lost his law license in New York. The panel that decided his license should be suspended wrote that Giuliani “claimed massive election fraud but had no evidence.” The 65 Project has a list of lawyers that it has filed ethics complaints against, including former Trump lawyer Jenna Ellis who worked on an Arizona election subversion case, Kurt Olsen who represented Arizona gubernatorial candidate Kari Lake in her 2022 election fraud case and Harvard Law School Professor Emeritus Alan Dershowitz.

Dershowitz told Just the News in a statement that what the group is doing is “pure McCarthyism.” “They already filed a complaint against me,” he said. “It’s pure McCarthyism. And unethical. And it’s scaring some lawyers away.” “The 65 Project is a bipartisan effort to protect democracy and preserve the rule of law by deterring future attacks on our electoral system,” The 65 Project said in a statement. “We are holding accountable Big Lie Lawyers who bring fraudulent and malicious lawsuits to overturn legitimate election results, and working with bar associations to revitalize the disciplinary process so that lawyers, including public officials, who subvert democracy will be punished.” Trump has argued that he has face lawfare at the federal level with lawsuits not related to election integrity, but involving his personal life and business.

Dershowitz said earlier this year on an episode of the Just the News, No Noise TV show that lawyers have been advised not to work for Trump or they would face consequences. “I know lawyers who have been asked to defend Donald Trump on First Amendment grounds,” Dershowitz said. “They would normally take the case, but they say, ‘we can’t afford it for our family because they’re coming after our bar license.'”Dershowitz said that he was seeing the return of “McCarthyism” and it is being pushed by the younger generation. Last month, Trump was found guilty on 34 counts of falsifying business records in the first degree for his reimbursement of a $130,000 payment his then-lawyer Michael Cohen made to porn star Stormy Daniels ahead of the 2016 presidential election. Trump had argued that this lawsuit and lawsuits on other states were part of a political witch hunt, which other GOP politicians and even some on the left have echoed.

“So President Biden would violate the Constitution, refuse to yield to the courts, and pursue his “bucket list” of priorities without any legal restraints. All would be done in defense of democracy..”

• Dems Call on Biden to Commit Unconstitutional Acts in his Final Days (Turley)

With the end of the Biden Administration in sight, liberal pundits seem to be striving to prove that the only difference between a lawbreaker and a law-abiding citizen is the ability to get away with the crime. Popular figures on the left from Michael Moore to Keith Olbermann are calling on President Joe Biden to commit overtly unlawful acts in his final 100 days in office, including targeting his political opponents. In one of the few statements of Moore with which I agree, he stated that this is “no joke.” It certainly is not. It is the same logic used by looters that they have a license for illegality. However, this constitutional looting would endanger not just the Constitution but the country as a whole if Biden were to heed this advice. In a posting on Substack, Moore told Biden that it was time to yield to temptation and check off a liberal 13-item “bucket list” of demands, tossing aside questions of legality or constitutionality in the process.

“You’re not done. You’ve still got 100 days left in office! And the Supreme Court has just granted you super powers — AND immunity! You don’t answer to anyone. For the first time in over 50 years, you don’t have to campaign for anything…“You have full immunity! No kidding! No joke! That’s not hyperbole! You can get away with anything! And what if anything means everything to the people?” The list includes emptying death row, canceling all student and medical debt, halting weapons shipments to Israel, ending the death penalty, declaring the Equal Rights Amendment a constitutional amendment, and granting clemency to nonviolent drug offenders. Many of these items could only be fulfilled by knowingly gutting the Constitution and assuming the powers of a monarch. That includes just canceling all student and medical debt in defiance of both the courts and Congress. As discussed in my most recent column, others have added to that bucket list.

Take Olbermann who, while insisting that he is fighting to “save democracy,” has called upon Biden to target political opponents like Elon Musk with deportation: “If we can’t do that by conventional means, President Biden, you have presidential immunity. Get Elon Musk the F out of our country and do it now.” These calls come in the midst of a counter-constitutional movement led by law professors. Moreover, the disregard for such legal authority has been voiced by liberal academics like Harvard Professor Lawrence Tribe. Indeed, his past “just do it” approach was not dissimilar in advice to Biden. For example, the Biden administration was found to have violated the Constitution in its imposition of a nationwide eviction moratorium through the Centers for Disease Control and Prevention (CDC). Biden admitted that his White House counsel and most legal experts told him the move was unconstitutional. But he ignored their advice and went with that of Harvard University Professor Laurence Tribe, the one person who would tell him what he wanted to hear. It was, of course, then quickly found to be unconstitutional.

The false premise of the recent calls is that the Court removed all limits on the presidency in its recent ruling on presidential immunity. The fact that law professors are repeating this clearly erroneous claim is a measure of the triumph of rage over reason today. As I have previously written, I am not someone who has favored expansive presidential powers. As a Madisonian scholar, I favor Congress in most disputes with presidents. However, I saw good-faith arguments on both sides of this case and the Court adopted a middle road on immunity — rejecting the extreme positions of both the Trump team and the lower court. As I previously wrote, the Court followed a familiar approach: The Court found that there was absolute immunity for actions that fall within their “exclusive sphere of constitutional authority” while they enjoy presumptive immunity for other official acts. They do not enjoy immunity for unofficial, or private, actions.

[..] So President Biden would violate the Constitution, refuse to yield to the courts, and pursue his “bucket list” of priorities without any legal restraints. All would be done in defense of democracy. It shows how the line between tyranny and democracy can be lost in an age of rage.

Brzezinski.

• If Israel Attacks Iran, Russia Is Not Going to Stay on the Sideline (Whitney)

“I don’t think there is an implicit obligation for the United States to follow like a stupid mule whatever the Israelis do. If they decide to start a war, simply on the assumption that we’ll automatically be drawn into it, I think it is the obligation of friendship to say, ‘you’re not going to be making a national decision for us.’ I think that the United States has the right to have its own national security policy.” -Zbigniew Brzezinski. The US foreign policy establishment used to include men who were capable of strategic thinking. No more. What passes for strategic thinking now is the endless reiteration of Israeli talking points uttered by retired generals who are owned by the weapons industry and the Israeli lobby. These men—who represent the views of an infinitesimal percentage of the overall population—are an essential part of the larger machine that prepares the public for intervention, escalation and war.

Their current assignment is to convince the American people that Israel’s impending attack on Iran serves America’s national security interests which, of course, it doesn’t. In fact, the country is being boondoggled into a bloody conflagration that will, in all probability, precipitate a sharp decline in US global power followed by a swift end to the so-called American Century. All of this was forecast by one of America’s most scholarly foreign policy analysts, Zbigniew Brzezinski, who delievered a warning on the topic of Iran more than a decade ago in an op-ed in the Los Angeles Times. Here’s what he said: “….an attack on Iran would be an act of political folly, setting in motion a progressive upheaval in world affairs. With the U.S. increasingly the object of widespread hostility, the era of American preponderance could even come to a premature end. Although the United States is clearly dominant in the world at the moment, it has neither the power nor the domestic inclination to impose and then to sustain its will in the face of protracted and costly resistance….”

It is therefore high time for the administration to sober up and think strategically, with a historic perspective and the U.S…. It’s time to cool the rhetoric. The United States should not be guided by emotions or a sense of a religiously inspired mission… our choice is either to be stampeded into a reckless adventure profoundly damaging to long-term U.S. national interests or to become serious about giving negotiations with Iran a genuine chance….. Treating Iran with respect and within a historical perspective would help to advance that objective. American policy should not be swayed by the current contrived atmosphere of urgency ominously reminiscent of what preceded the misguided intervention in Iraq.” Been there, done that, Zbigniew Brzezinski, LA Times. Well said. One can only wish that the lamebrain pundits on cable news would circulate the article among themselves.

Like him or hate him, Brzezinski provided a coherent, well-researched analysis that dispassionately evaluated whether the costs of a particular operation were greater than the benefits. In this case, there is simply no comparison. The US is rushing towards a conflict that serves no national interest, that it can’t win, and that will have a catastrophic impact on the nation’s future. Here’s Brzezinski again: “We do not need to increase the scale of the conflict in the region because an increase in that conflict involving the Iranians …would likely reignite the conflict in Iraq, would set the Persian Gulf ablaze, would increase the price of oil 2-fold, 3-fold, 4-fold…Europe would become even more dependent on Russia for its energy…. So, what is the benefit to us?

All I know as an analyst of international politics is (a war with Iran) this would be a disaster. And, frankly, I think it will be a disaster for us more than for Israel because, as a result of the war…. we will be forced out of the region… because of the dynamic hatred that develops. And, have no illusions about it, if the conflict spreads, we’re going to be alone… And if we are driven out, how much would you bet on the survival of Israel for more than five or ten years?” Zbigniew Brzezinski, Real News Network, 2:15 min. So, it would not just be disastrous for the United States, but disastrous for Israel as well, which—absent Washington’s “unconditional” support—would wither on the vine in 5 or 10 years. Perhaps, there are some who would disagree with this analysis? Perhaps there are some who think that a tiny belligerent colony at the heart of the Arab world—that has made every effort to make itself a damned nuisance for the last 75 years—could survive without US assistance?

Oh, great..

• US Troops Will Deploy To Israel – Pentagon (RT)

The US has ordered the deployment of a THAAD air defense system to Israel, along with a crew of American service members to operate it, Pentagon Press Secretary Maj. Gen. Pat Ryder announced on Sunday. The move marks the first deployment of US combat troops on Israeli soil since the Israel-Hamas war began last year. According to Ryder, the THAAD battery “and associated crew of US military personnel” will be stationed in Israel “to help bolster Israel’s air defenses following Iran’s unprecedented attacks against Israel on April 13 and again on October 1.” US President Joe Biden, who the White House previously said had “no plans or intentions to put US boots on the ground in combat,” ordered the deployment, Ryder stated. The THAAD, or Terminal High Altitude Area Defense system, is a mobile anti-ballistic missile system designed to detect and intercept ballistic missiles during their descent stage.

It fires a non-explosive projectile at eight times the speed of sound, relying on kinetic energy to destroy incoming missiles. A THAAD battery consists of 95 soldiers and six truck-mounted launchers capable of firing a total of 48 interceptors. The US deployed a THAAD battery to Saudi Arabia after the Israel-Hamas war began last October, and to Israel on a training exercise in 2019. However, neither the system nor the American troops who operate it have been sent to Israel since the current conflict began. While American soldiers took part in a brief aid mission off the coast of Gaza earlier this year, they did not set foot in the Palestinian enclave. The deployment comes as Israel prepares its response to an Iranian missile attack on October 1, in which around 200 ballistic missiles were fired at Israeli military targets. Tehran maintains that the strike was a “legitimate” response to Israel’s assassination of Hamas leader Ismail Haniyeh in Tehran and Hezbollah leader Hassan Nasrallah and a senior Iranian general in Beirut.

Israel is widely expected to target Iran’s oil or nuclear infrastructure, although the US has advised West Jerusalem against either choice. Whatever form the Israeli response takes, Iran has vowed to retaliate. Earlier this week, a source in Tehran told RT that this retaliation would be “proportionate.” Should West Jerusalem target Iran’s oil infrastructure, Tehran will respond by striking Israel’s oil refineries. Attacks on other infrastructure, such as power plants or nuclear facilities, will likewise prompt retaliatory strikes on corresponding installations in Israel, the source explained. Hours before Ryder’s announcement, Iranian Foreign Minister Seyed Abbas Araghchi warned that the US is putting the “lives of its troops at risk by deploying them to operate US missile systems in Israel.” “While we have made tremendous efforts in recent days to contain an all-out war in our region, I say it clearly that we have no red lines in defending our people and interests,” Araghchi added.

UNIFIL has been there since 1978.

• Netanyahu Orders UN To Evacuate Lebanon Peacekeepers (RT)

Israeli Prime Minister Benjamin Netanyahu has demanded that UN Secretary-General Antonio Guterres withdraw UNIFIL peacekeepers from southern Lebanon, adding that by remaining there they are “providing a human shield to Hezbollah terrorists.” In a Hebrew-language video message posted to social media on Sunday, Netanyahu told Guterres “it is time for you to withdraw UNIFIL from Hezbollah strongholds and from the areas of combat.” “The IDF has repeatedly asked for this, and has been met with repeated refusals, all aimed at providing a human shield to Hezbollah terrorists,” he continued. UNIFIL, or the United Nations Interim Force in Lebanon, was formed in 1978 to oversee the withdrawal of Israeli forces to below the so-called ‘blue line’, which separates Lebanon from Israel and the occupied Golan Heights.

Headquartered in the town of Naqoura, UNIFIL is currently composed of around 10,000 troops from around 50 countries, who are tasked with monitoring the demilitarization of southern Lebanon between the blue line and the Litani River. Israel maintains that UNIFIL has done nothing to prevent Hezbollah entrenching itself in this region, while preventing its own forces from responding to the threat. In the weeks since the Israel Defense Forces (IDF) crossed the blue line and entered southern Lebanon, UNIFIL has claimed that Israeli forces have repeatedly hit its bases and outposts. Four Sri Lankan and Indonesian peacekeepers were injured on Thursday and Friday when Israeli tanks fired on their watchtowers, UNIFIL said. Another was hit by gunfire at Naqoura later on Friday, although UNIFIL said that it could not identify the origin of the fire.

IDF bulldozers have demolished UNIFIL walls and bunkers, while a contingent of Irish peacekeepers found themselves surrounded by Israeli tanks earlier this week when they refused the IDF’s demand that they leave their outpost. Switching to English, Netanyahu told Guterres to “get the UNIFIL forces out of harm’s way. It should be done right now, immediately.” “Your refusal to evacuate the UNIFIL soldiers makes them hostages of Hezbollah,” he continued, warning that “this endangers both them and the lives of our soldiers.” UNIFIL has refused to withdraw from its positions, and in a joint statement on Saturday, 40 countries contributing to the mission called on Israel to investigate the attacks on peacekeepers. One day earlier, the leaders of France, Italy, and Spain expressed “outrage” at the attacks, and accused Israel of violating UN Security Council resolution 1701, which states that its forces cannot operate in southern Lebanon.

Netanyahu said that Israel “regrets” injuring the peacekeepers, but added that the “simple and obvious” way to prevent further bloodshed is “just get them out of the danger zone.” Israel escalated its military campaign against Hezbollah last month, pounding Beirut with a wave of airstrikes including one that killed the group’s leader, Hassan Nasrallah. A ground invasion followed, and the death toll in Lebanon currently stands at over 2,100, according to the country’s Health Ministry. The IDF has acknowledged the deaths of two dozen of its soldiers in Lebanon, although Hezbollah insists that the true scale of Israel’s losses is far higher.

“..Israel would expand “little by little” and eventually encompass all Palestinian territories as well as Jordan, Lebanon, Egypt, Syria, Iraq, and Saudi Arabia..”

• Israel Finance Minister Calls For Borders To Extend To Damascus (MEE)

Far-right Israeli Minister of Finance Bezalel Smotrich has drawn criticism for calling for Israel to expand its borders to Damascus in a recent documentary. In an interview for the documentary, In Israel: Ministers of Chaos, produced by European public service channel, Arte, Smotrich claimed that Israel would expand “little by little” and eventually encompass all Palestinian territories as well as Jordan, Lebanon, Egypt, Syria, Iraq, and Saudi Arabia. “It is written that the future of Jerusalem is to expand to Damascus,” he said, citing the “greater Israel” ideology, which envisions the expansion of the state across the Middle East. Jordan’s Ministry of Foreign Affairs condemned the incendiary remarks saying that they highlighted Smotrich’s dangerous and “racist” ideology. Smotrich previously cited the concept at a memorial service for a Likud activist in Paris.

When speaking from a podium decorated with a map of Israel that included Jordan, he claimed that there was “no such thing” as the Palestinian people. The French foreign ministry subsequently announced that government representatives in Paris did not intend to meet with Smotrich during his visit to the country. Aside from being the finance minister, Smotrich now holds significant powers over the occupied West Bank. In August, Smotrich expressed support for blocking aid to Gaza, saying that: “Nobody will let us cause two million civilians to die of hunger even though it might be justified and moral until our hostages are returned.” At the end of February, the minister said that the state of Israel should “wipe out” the Palestinian village of Huwwara, after it was subjected to a violent rampage by Israeli settlers.

“..the World War II-era massacre of tens of thousands of ethnic Poles by Ukrainian ultranationalists lionized by the post-2014 regime in Kiev..”

• Zelensky ‘Left Seething’ After Meeting With Polish Minister (Sp.)

Poland’s political class has generally been at the forefront of powers cheerleading Ukraine’s entry into Western institutions including NATO and the European Union, notwithstanding underlying tensions over the World War II-era massacre of tens of thousands of ethnic Poles by Ukrainian ultranationalists lionized by the post-2014 regime in Kiev. Volodymyr Zelensky was reportedly “left seething” after last month’s meeting with Polish Foreign Minister Radoslaw Sikorski, who impeded the Kiev regime’s aspirations to join the EU by tying the issue to demands that ethnic Poles killed by Ukrainian fascists during WWII be exhumed from their final resting places in what is now western Ukraine. Sources told Bloomberg about the tensions, which are said to have coincided “with mounting war fatigue” among Kiev’s Western sponsors, and growing uncertainty over post-2014 Ukraine’s constitutionally-mandated pursuit of membership in the EU and NATO.

As many as 100,000 ethnic Polish civilians and tens of thousands of Russians, Jews, anti-fascist Ukrainians were murdered en masse by members of the Ukrainian Insurgent Army (Ukrainian acronym UPA) – an ultranationalist militia operating in Nazi-occupied western Ukraine during the second World War. Killings and terrorism largely took place between 1943-1944, but continued into the early 1950s. Between 100,000 and 200,000 Ukrainians would fight in the UPA, compared to over six million who served in the Red Army. In post-2005 Orange Revolution Ukraine and especially after 2014, UPA leaders Stepan Bandera and Roman Shukhevych have been idolized as heroes and fighters for Ukraine’s independence, with monuments erected in their honor and streets renamed to carry their names in cities across the country.

Former Ukrainian President Viktor Yanukovich revoked his predecessor’s decision to posthumously award Bandera and Shukhevych ‘hero of Ukraine’ titles in 2011 prior to his ouster in a coup three years later. Polish Minister of Defense and Deputy Prime Minister Wladyslaw Kosiniak-Kamysz announced publicly last week that Kiev “will not join the EU if it does not address the Volyn issue, if there is no accord, no exhumations and no remembrance.” Polish Prime Minister Donald Tusk hinted as much at a press conference in August, saying “there is a need to dig into this history [of the WWII-era massacres, ed.] if we are about to build a good future,” and warning that “as long as there is no respect for those standards from the Ukrainian side, then Ukraine will certainly not become part of the European family.”

“If there is a direct conflict with NATO, it will immediately go nuclear, and everybody knows this.”

• West Sacrificing Economy, Military Readiness to Back Ukraine (Sp.)

The United States and its European allies are destroying their own militaries and economies to fight an increasingly futile crusade against Russia, according to Serbian-American journalist Nebojsa Malic. The analyst joined Sputnik’s The Backstory program recently to comment on the ongoing Ukraine proxy war as voters in Western countries increasingly turn against the quixotic effort. “The enthusiasm for Ukraine in America is just about tapped out after these two hurricanes and the disastrous damage they’ve inflicted, and the fact that it took a week for anybody to even notice that North Carolina and Tennessee are facing biblical floods,” said Malic. “That’s basically the vibe in America that I can see from here: no more, not a penny more to Ukraine.” “The Pentagon is drawing on its [weapons] stockpiles as much as they can,” the analyst claimed. “It’s not the issue of, ‘oh, send everything.’ They are sending everything. This is everything they can spare.”

“Ten days ago when the Iranians fired all of those missiles at Israel apparently the US ships that were stationed there fired off 12 interceptors, not to very much effect from what I could see. And it turns out that’s the entire annual production. They’re making 12 missiles a year. So, it’s not like they have something to send. They’re already raiding the US armory as it is.” The Ukraine proxy war has shed light on the weaknesses of Western militaries as the US and its allies have struggled to continue to arm Kiev. A report earlier this year revealed that Russia is producing three times more artillery than the United States and its European partners combined. The conflict has brought the two competing models of defense production into stark relief, with privatized Western military contractors unable to produce arms in the same quantities as Moscow’s state-owned production industry.

Western military planners are also not accustomed to waging a large-scale war against a formidable opponent like Russia, a fact tacitly admitted as the US military began a massive restructuring this year to prepare for a possible war against China in the Pacific theater. Western armed forces have most recently focused on counterinsurgency strategies against resistance forces in the Middle East. Russia has meanwhile proven itself capable of quickly adapting amid its special military operation, even as the US and European countries like the UK and Germany send Kiev their top-of-the-line equipment. “Most people in the West can’t even conceive of this scale and intensity of warfare,” Malic claimed. “Western militaries aren’t built for it.” The Ukraine proxy war has shed light on the weaknesses of Western militaries as the US and its allies have struggled to continue to arm Kiev.

A report earlier this year revealed that Russia is producing three times more artillery than the United States and its European partners combined. The conflict has brought the two competing models of defense production into stark relief, with privatized Western military contractors unable to produce arms in the same quantities as Moscow’s state-owned production industry. Western military planners are also not accustomed to waging a large-scale war against a formidable opponent like Russia, a fact tacitly admitted as the US military began a massive restructuring this year to prepare for a possible war against China in the Pacific theater. Western armed forces have most recently focused on counterinsurgency strategies against resistance forces in the Middle East. Russia has meanwhile proven itself capable of quickly adapting amid its special military operation, even as the US and European countries like the UK and Germany send Kiev their top-of-the-line equipment.

“Most people in the West can’t even conceive of this scale and intensity of warfare,” Malic claimed. “Western militaries aren’t built for it.” “I remember reputable military experts warning five, six, ten years ago when they were trying to ramp up military spending in the West that NATO has the capability to fight for maybe two weeks,” he continued, noting the resources required to build costly Western equipment like Abrams tanks. “That was two and a half years ago, and now they’ve depleted all of their armories and all of their ammunition stocks, and now you have to wonder whether they still have the ability to fight for two weeks.” “If there is a direct conflict with NATO, it will immediately go nuclear, and everybody knows this.”

“..it was under Stoltenberg that NATO, pursuing irrational “expansion to the East,” reached its current stage of weakness, demoralization, and disunity..”

• Stoltenberg Stupidly Celebrates His Own Failure To Achieve Security (SCF)

Jens Stoltenberg is finally no longer the leader. This is not necessarily good news, as the new secretary general appears to be even more bellicose than the previous one and promises policies that could easily lead to strategic disaster in the current tensions between the Atlantic alliance and the Russian Federation. However, it is undeniable that one of the worst administrations in NATO’s history – and the one that came closest to an open confrontation with Moscow – has now ended. Stoltenberg has recently made a number of statements praising his supposed “achievements” as NATO leader. He claims that under his leadership the alliance has achieved its highest numbers of troops on the eastern flank. Stoltenberg has also acclaimed himself for his success in allowing countries such as Finland and Sweden to join NATO as well as significantly expanding the number of troops on combat readiness for the event of a war.

In fact, Stoltenberg seems to be delighting over his own failure. It was under him that NATO saw the start of the continent’s biggest conflict since the World Wars in Europe, reaching a critical point in the regional security architecture. These tensions, which could at any moment escalate to the level of an open war with direct Western involvement, are precisely the consequence of the irresponsible policies implemented during Stoltenberg’s disastrous administration. NATO’s expansion into Eastern Europe, both in terms of new members and available troops, is not something to be celebrated, but rather lamented. It was precisely this expansion that led to the current conflict. If Stoltenberg were indeed a rational, prudent leader with a strong strategic sense, he would have been able to use diplomacy with the member countries and negotiate a de-escalation of the suicidal policy of “containment” against Russia.

But, on the contrary, Stoltenberg endorsed all this and was active in worsening the Ukraine crisis, contributing significantly to the escalation of tensions and the beginning of the current war. More than that, he failed to stop the warmongering of the member states, allowing NATO to begin full support for the Kiev regime. This support is now at its most critical point, as the alliance’s countries are close to authorizing the use of long-range weapons against Russian civilian targets – which could lead to a nuclear world war. Stoltenberg, even now out of office, is partly to blame for this, as it was under his administration that this anti-Russian madness was launched by NATO.

Furthermore, it must be emphasized that the alliance has never been so fragile. Contrary to what Western war propaganda claims, anti-Russian policies are not strategically beneficial for NATO. On the contrary, in addition to threatening global peace, these measures put the very stability of the alliance at risk. NATO is not “stronger and more united than ever,” as the former secretary general says, but at its most fragile and delicate phase in history. On the battlefield, Russian forces destroy NATO equipment – and troops disguised as “mercenaries” – every day. The U.S. and Europe no longer have the capacity to continue supporting Kiev continuously, given the large number of losses on the front lines, but at the same time, the alliance is unable to end this support, falling into a vicious cycle of violence and defeats.

In addition, countries dissatisfied with the situation, such as Hungary and Slovakia, are already beginning to create a dissident position within NATO itself, threatening the bloc’s long-term stability. In the end, it was under Stoltenberg that NATO, pursuing irrational “expansion to the East,” reached its current stage of weakness, demoralization, and disunity. And, to make matters even more catastrophic, an open world war could yet emerge as a belated consequence of NATO’s actions over the past ten years. Instead of celebrating his own failure as a leader, Stoltenberg should simply be grateful that he had the opportunity to leave office before the worst-case scenario arose.

For 17 days last December… And they did nothing.

• US Failed To Stop Mystery Drones Over Military Sites – WSJ (RT)

An unidentified fleet of drones potentially spied on a US military airbase in Virginia after intruding into restricted airspace for 17 days last December, with the Pentagon powerless to stop them, the Wall Street Journal has revealed. Swarms of drones were detected flying over Langley Air Force Base on Virginia’s shoreline – one of the select US bases hosting F-22 Raptor stealth fighters – the WSJ reported on Saturday, citing dozens of US officials, police reports, and court documents. Former US Air Force General Mark Kelly, who was made aware of the incursions in December, estimated the lead unmanned aerial vehicle (UAV) to be “roughly 20 feet long, flying at more than 100 miles an hour, at an altitude of approximately 3,000 to 4,000 feet,” with other drones following. The drones flew in a pattern of one or two fixed-wing units accompanied by smaller quadcopters, roughly the size of 20-pound commercial drones, often operating at a lower altitude, the report said.

The dozens of drones moved south across Chesapeake Bay toward Norfolk and the base housing the US Navy’s SEAL Team Six special operations unit, as well as Naval Station Norfolk – a large naval port, Kelly noted. When news reached the White House, officials reportedly attempted to brainstorm a response. Military radars – tuned to detect larger military aircraft and to ignore anything resembling a bird –often failed to pick up the drones and needed recalibration. The offending quadcopters were also controlled on a radio frequency unavailable to off-the-shelf drones. Police attempted to pursue the drones, tracking their movements, but ultimately failed to identify their owners. Authorities were skeptical about bringing the UAVs down. Federal law bars the military from shooting down drones near military bases unless they pose an immediate threat – which does not include aerial spying, the WSJ wrote.

Jamming the drones was considered risky to local 911 emergency systems and Wi-Fi networks. Using directed energy weapons to shoot them down was viewed as too much of a risk to commercial aircraft. The flights ceased on December 23 and the perpetrators remain a mystery, according to the report. Authorities failed to determine who was responsible for the flights but were reportedly convinced that the unprecedented incursion was too complex to have been orchestrated by hobbyists. It is not the only case of unidentified drones being spotted over critical US infrastructure. Two months prior, five drones were reportedly detected over the Nevada National Security Site, a US nuclear testing facility outside Las Vegas. Officials have yet to identify those behind the incursion.

Yes, there are some curious links.

• Unholy Coincidences Between The Security State And Lone Wolf Assassins (Carman)

Polybius, one of the earliest historians to write about the cyclical nature of politics and history, once stated, “Since the masses of the people are inconstant, full of unruly desires, passionate, and reckless of consequences, they must be filled with fears to keep them in order. The ancients did well, therefore, to invent gods and the belief in punishment after death.” Just look at the modern news cycle for proof of how this tactic persists today. The relevance of Polybius’ insight becomes even more pertinent when you consider that he wrote it during the decline of the Hellenistic empire—just as it was collapsing into the black hole of history—and holy sh*t that’s eerily applicable as we watch the fall of U.S. hegemony in real time. Western society’s fixation on the self and the use of scare tactics by institutions to maintain control inevitably leads to deceptions surrounding the conspiratorial and collaborative causes of events designed to induce fear. The narrative often attributes the cause of disruptive events to a “disturbed” individual, to wholly deflect from the all-encompassing truth, which, on the whole, is often far more disturbing.

Take, for example, the first assassination attempt on former President Donald Trump. The official narrative of Crooks, a lone teenage gunman—disturbed, of course—crumbles under scrutiny. The behaviour of the security detail that day, the delayed response after the threat was identified, and the gunman’s ability to get into position, firearm and ladder in hand, are all deeply suspicious. That he appeared in a Blackrock promo video only raises further questions. We’ll get to the role of “banksters” soon enough, but citizen journalists have uncovered links between the gunman and phone calls to an FBI office, both months and days before Trump’s Pennsylvania rally. Only a conspiracy nut could conjure such nonsense that the security state may have been involved because, of course, it’s highly regular for most teenagers to be involved in some capacity with Blackrock and the FBI, and only a wholly rabbitholed kook could see the cyclical pattern of this narrative.

Consider Lee Harvey Oswald, perhaps the most famous “disturbed” lonewolf of all. We’re asked to believe that this unhinged man somehow outsmarted an entire Secret Service detail to assassinate a president he claimed to admire. Oddly, Oswald’s little green address book notes that Kennedy wasn’t even his intended target, suggesting that the death of arguably the most popular president in U.S. history might have been accidental. Coincidentally, Oswald, a former Marine, allegedly defected to the USSR after becoming disillusioned with American propaganda. His own writings suggest he was on a secret mission for the CIA, working as an informant within Russia. Whether or not this is true, Oswald’s links to the military-industrial complex should be a glaring red flag to anyone with critical faculties. How many people have even minor connections to the security state? Probably less than 0.01%, yet these ties keep emerging in case after case involving infamous, high-profile assassins.

The connections between Charles Manson, MKUltra, and the security state were long dismissed as conspiracy theory. But documents now confirm Manson’s involvement in MKUltra, as well as his curious meetings with his parole officer—who, it turns out, shared office space with one of the program’s leaders. Despite multiple parole violations, Manson was never returned to prison. Why? The security state’s best-case motive seems to be that they allowed Manson to cultivate a murderous cult to sow fear. The establishment feared that groups like the Black Panthers, along with the anti-war movement in Hollywood, posed a threat to the old institutions of power. So, they induced a climate of fear within the people to prevent unity, utilising identity politics and racial baiting to create division and distrust, destroying any mounting threat to the old hegemony. Does this tactic sound familiar?

Similarly, the cycle of disturbed young men committing atrocities to terrify the public remains a powerful tool of control. Look at Timothy McVeigh and the Oklahoma City bombing. The official narrative paints McVeigh as a white supremacist and anti-government extremist. Yet, paradoxically, his actions seemed to do the government a favour. Some sources claim crucial documents tied to the Whitewater scandal—which could have led to the indictment of the Clintons—were conveniently lost in the explosion. Unsurprisingly, the bombing also served as a pretext for the government to crack down on anti-establishment groups, which had grown in response to events like Waco and Ruby Ridge. If we subscribe to the theory that the cause is manufactured to justify the “consequence,” which usually relates to tighter government control, it’s easy to question the official version of events.

The key point, however, as with Oswald and Manson, is that yet again McVeigh had ties to the military-industrial complex and the CIA. In a letter to his sister, McVeigh claimed he was recruited into a secret black-ops team involved in smuggling drugs into the United States to fund covert activities and was “to work hand-in-hand with civilian police agencies to quiet anyone whom was deemed a security risk.” His co-conspirator, Terry Nichols, backed up the claims, alleging that an FBI agent, Larry A. Potts, oversaw these activities. While there’s no definitive proof, the coincidence is striking: yet another “disturbed” man with connections to the security state. What are the chances?

“The mandate for Trudeau’s government expires at the end of October 2025..”

• Canada’s Dissenting Liberal MPs Seek to Topple Trudeau (Sp.)

A faction of disgruntled lawmakers from Canadian Prime Minister Justin Trudeau’s own governing Liberal Party is coordinating efforts to oust him as their leader, reported CBC News. “At least 20″ dissenting MPs have reportedly signed the document urging leadership change, with others voicing their support, in a joint call for Trudeau to resign, according to the outlet. Trudeau has been teetering on the ropes since the humiliating by-election loss of two strongholds in Toronto (to the Conservatives) and Montreal (to Bloc Québécois). Pressure to relinquish his hold on the Liberal Party has also grown amid his government’s free fall in the polls. At 41.6%, Pierre Poilievre and his Conservative Party are more than 20 points ahead of the Liberal Party, as reflected in numbers released by Nanos Research earlier in the month.

The top issues of concern for Canadians remain the soaring cost of living, housing affordability, skyrocketing prices and immigration. Last month, the New Democratic Party (NDP) pulled the plug on its support for Trudeau, exiting a 2022 “supply and confidence” deal. The arrangement had offered confidence votes to the PM’s minority government, in exchange for support on key issues. Despite being decimated in the polls, Trudeau has dug in, saying he is “not going anywhere.” The Liberal government has already survived two non-confidence votes. The Liberals, NDP and Bloc Quebecois voted against a Conservative motion that called for MPs to declare they have lost faith in Prime Minister Justin Trudeau and his nine-year-old government several weeks ago. The mandate for Trudeau’s government expires at the end of October 2025, and media reports have made no bones about the Liberals’ defeat at the next general election.

Enjoyed reading this.

• Titan of Business, Friend of Strays: The legendary Ratan Tata (Chowdhury)

It’s rare – and rather beautiful – when an industrialist is remembered not for his net worth or assets left behind, but for his empathy and big heart. Such was the life led by Indian business tycoon and philanthropist Ratan Tata, who passed away late on October 9. With his death, India lost a visionary industrialist. Budding entrepreneurs lost their biggest source of inspiration. Humanity lost a beacon of selfless compassion. The stray dogs of the country lost their biggest champion. “I’d like to be remembered as a person who made a difference. Not anything more, not anything else.” These were among the many wise words he often regaled the world with. And what a difference he made. He’s left behind a wake of mourners, shaken by the loss of a kind soul who loved humans and animals alike.

Most of India didn’t have the good fortune to have met him, yet his death feels like a devastating personal loss to all who knew of him. His impact was felt not only in the companies he nurtured, but also in the values of integrity, ethics and nation-building he championed. Besides playing the role of one of India’s greatest nation-builders, Mr Tata was instrumental in raising Indian industry to the heights it commands today. He joined the Tata Group – founded by his great-grandfather Jamsetji Tata – as an intern in 1962 and made his way to the top, gradually establishing himself as a visionary industrialist who transformed the Indian conglomerate into a global powerhouse. “Take the stones people throw at you and use them to build a monument,” said the man who spearheaded a series of bold international acquisitions like Jaguar Land Rover, Tetley Tea, General Chemical, Corus Steel, Brunner Mond and Daewoo. What were considered the heydays of Air India were under Mr Tata’s chairmanship.

From the launch of Tata Nano, the world’s most affordable car, to investments in a number of startups to kickstart their contribution towards the Indian job market, his contributions towards pushing the country forward were unparalleled. And in a world of loud, limelight-hogging CEOs, Mr Tata was a quiet, transformative force who redefined leadership. Reinforcing this statement was a way of life he believed in: “The best leaders are those most interested in surrounding themselves with assistants and associates smarter than they are.” Beyond the boardroom, Mr. Tata’s legacy is shaped by his myriad philanthropic endeavours. He transformed millions of lives in India through his commitment to social causes, rooted in his family’s long-standing tradition of promoting societal progress. And through Tata Trusts – one of India’s oldest charitable institutions – he championed healthcare, education, sanitation, rural development, animal welfare and skill development.

Despite the Tata Group boasting a market cap of over US$400 billion, Mr Tata is never named on any list of the world’s top billionaires. This is because he has donated over US$110 billion of his wealth, and his family contributes 65% of their income to various causes. One of his many defining moments came during the Covid-19 pandemic when, in 2020, Tata Sons and Tata Trusts together pledged Rs 15 billion ($178 million) towards efforts to fight the virus, including the donation of personal protective equipment, testing kits and healthcare infrastructure. In 2021, Tata Trusts – managed by Mr Tata then as an active member of the family – emerged the global leader on the charitable front, according to the EdelGive Hurun Philanthropists of the Century report. Moreover, in the 2023 financial year, the total disbursals made by the organisation stood at Rs 4.56 billion ($54 million), the latest annual report of Tata Trusts shows.

Mechazilla

— Elon Musk (@elonmusk) October 13, 2024

https://twitter.com/i/status/1845446512584626586

Elon mistake

Elon Musk: The most common error of a smart engineer is to optimize a thing that should not exist.

“The most common error of a smart engineer is to optimize a thing that should not exist. Why would people do that?

Everyone's been trained in high school and college to answer… pic.twitter.com/5YdnBWQbA7

— ELON DOCS (@elon_docs) October 12, 2024

Crane

A self-folding cranepic.twitter.com/hw7fkiTPpA

— Massimo (@Rainmaker1973) October 13, 2024

Penguin

https://twitter.com/i/status/1845084459357569290

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.