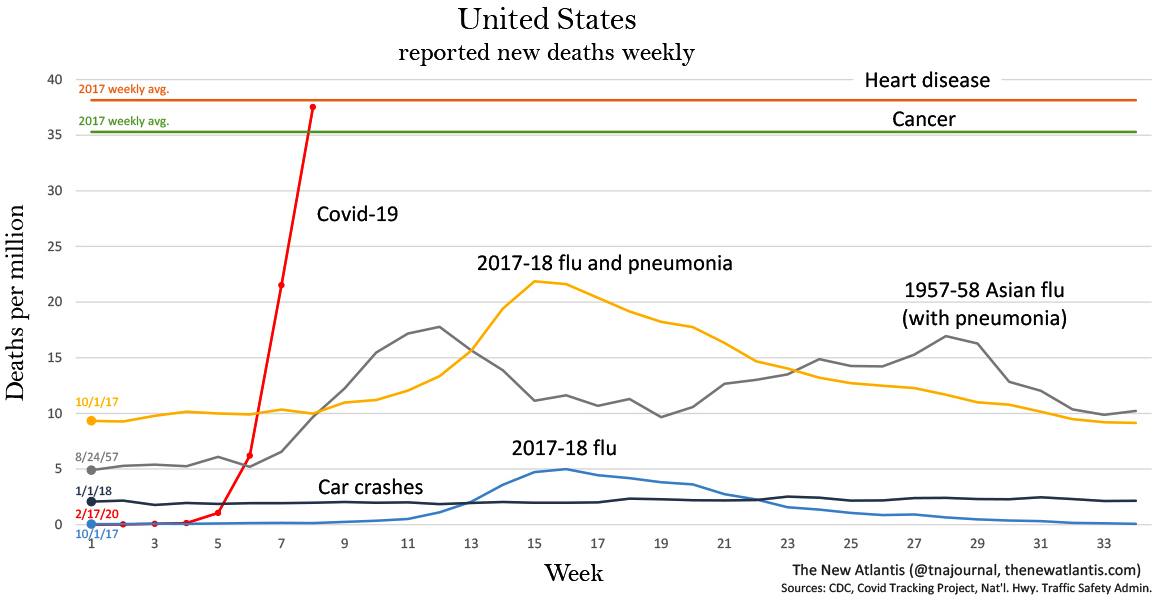

There are times when you think: now things must be easy to comprehend, but as it turns out, they are still not. Let me try once more. See, I was thinking it must have become much easier to gauge the impact in the US of COVID19 when I published the graph below from TheNewAtlantis.com a few days ago. That the stories about seasonal flu etc. at least should be dead and buried, because, well, just look at the graph.

No such “luck”. That warped comparison keeps on rearing its head. The graph is plenty clear about it, however. In a period of about 3 weeks, COVID19 obliterated all other causes of death far behind.

click to enlarge in new tab

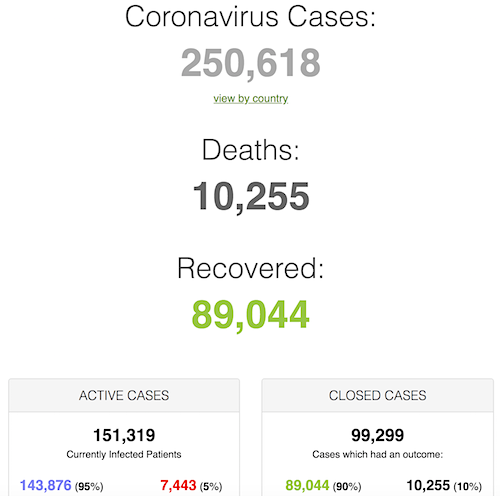

I have followed the progress of the virus since early January, so plenty of graphs are available. Below are those from Worldometer and SCMP, starting February 20.

On February 2, the US had 5 cases and zero deaths. Then we get to the graphs.

On February 20, there were 75,750 global cases, 74,500 of which were in China. There were 2,130 deaths, of which just maybe 10 were outside China.

The US had fewer than 15 cases and zero deaths.

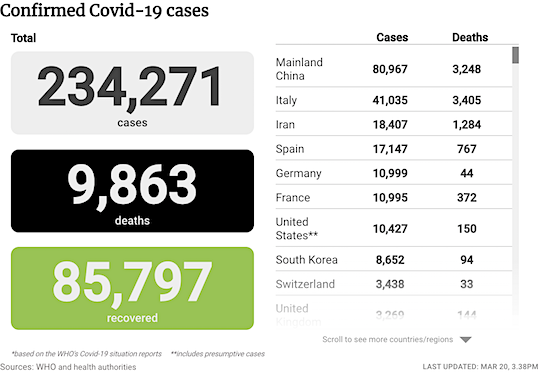

One month later, things had changed quite dramatically, or so it seemed.

On March 20, there were 250,000 global cases and over 10,000 deaths. Cases had tripled, deaths had almost quintupled. Italy had overtaken China in most fatalities, from zero a month earlier.

The US had emerged “on the forefront”. It now had 10,400 cases and 150 deaths. Yes, that is just one month ago, 32 days to be exact.

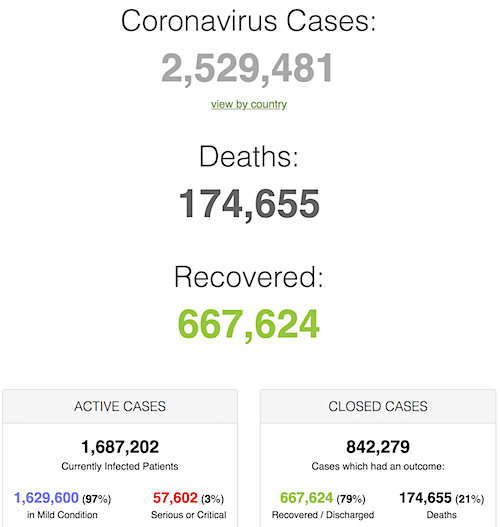

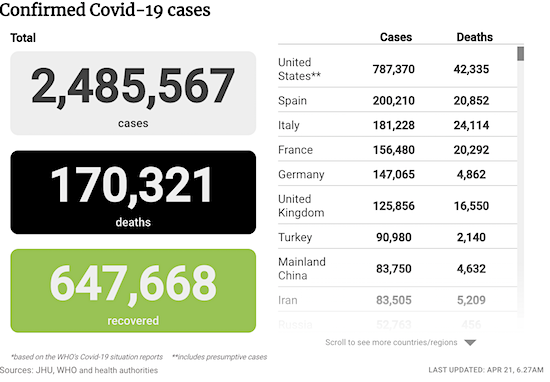

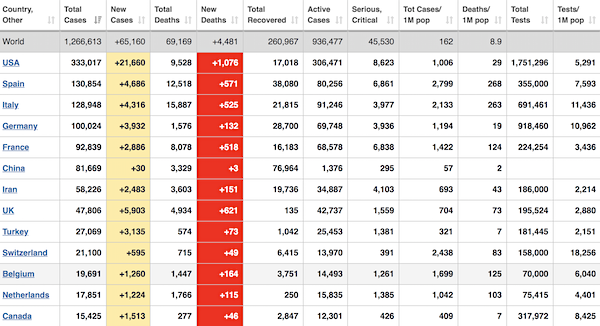

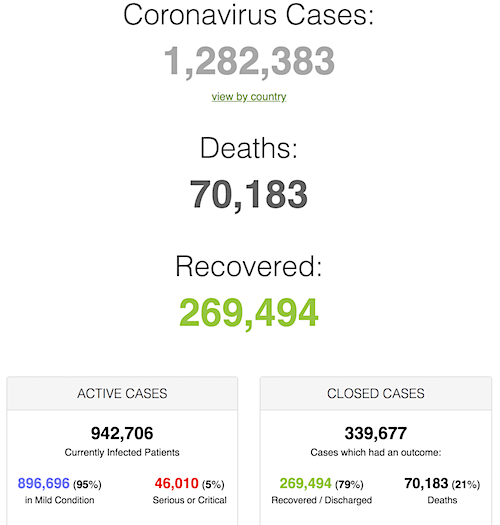

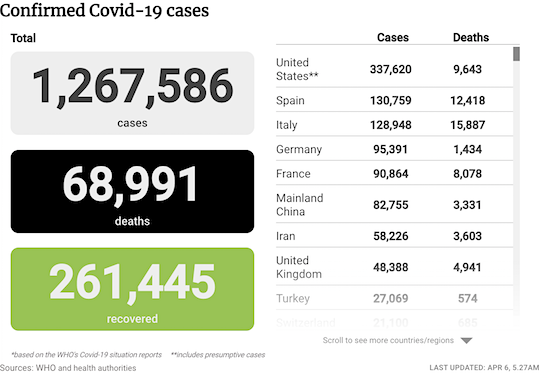

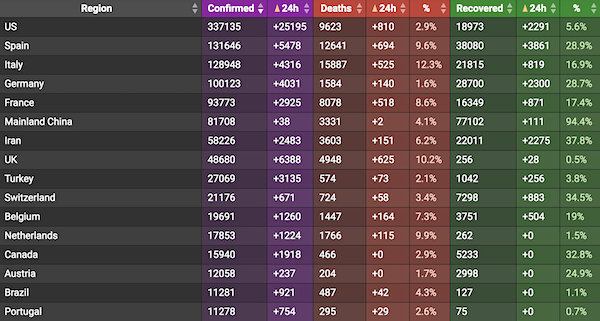

Today, on April 21 2020, you would hardly recognize the situation as it was on February 20 or March 20.

There are now over 2,500,000 cases and over 172,000 deaths.

The US has become the frontrunner, and by a very large margin. It has over 800,000 cases and over 43,000 deaths.

From those 10,400 cases and 150 deaths 32 days ago.

Moreover, of those 43,000 deaths, almost half, 20,000, died in just the past 7 days.

And it’s at this point that people want to call the peak.

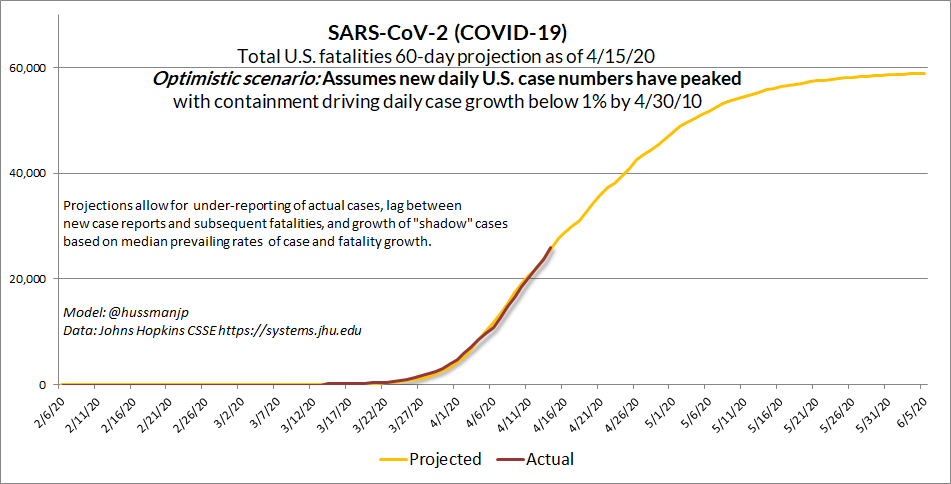

Investor John Hussman developed a model from early February which he’s been updating ever since. His model followed (or actually, predicted) actual numbers quite well:

Apr 15 (637,716 cases, 30,826 deaths): Assuming sustained containment efforts, the “optimistic” projection (my adaptive model) suggests that U.S. daily new cases may have peaked. This does NOT mean these efforts can now be abandoned. Most U.S. fatalities are still ahead, and we still lack capacity to test/track/trace.

But 5 days ago, John started getting worried:

Apr 16 (667,801, 32,917): This isn’t good. U.S. fatalities just jumped off book. We shouldn’t see 31,000 yet.

Apr 18 (735,076, 38,903): So much for the optimistic scenario. We’re way off book. I had hoped this was just a one-time adjustment. Understand this:

PEAK daily new cases in a containment scenario is also PEAK infectivity if containment is abandoned at that moment.

I’ve long said that people are social animals, and you cannot -and shouldn’t- keep them apart for too long. But at the same time, containment measures in case of epidemics go back a very long way in history. And it’s very well for people to develop models that appear to show that the virus will do whatever it can until it no longer does, and it will soon disappear even if we didn’t do anything to prevent it from spreading.

But those are still just models, just like the one John Hussman developed. And until they are proven, which takes time, the actual numbers we have now speak loudly. Globally, we went from 250,000 to 2,500,000 cases in one month, and from 10,000 fatalities to 172.000. In the US in that same month we went from 10,400 cases to over 800,000 and from 150 deaths to 43,000.

“PEAK daily new cases in a containment scenario is also PEAK infectivity if containment is abandoned at that moment”, says Hussman. Of course everybody wants their freedom back. But at what price? If you don’t, because you can’t, know what the price will be, are you still willing to pay that price?

What I mean is, everyone’s trying to call a peak, but for most that’s merely because they want there to be a peak. The numbers don’t really say that; they may seem to do, but that’s just over 1,2 or 3 days at best. While half of all US fatalities have been over the past 7 days.

If the peak has really already occurred, we will not know it until about 10-14 days from now. So the only thing we can do is to wait that long. Perhaps it would be a good idea to listen to what those have to say who are so enthusiastically labeled “heroes” all over the globe, the doctors, nurses and other frontline caretakers.

If they are indeed your heroes, and that’s not just some empty phrase, listen to what they have to say about the pressure on them, on the system they work in, on the numbers of cases and deaths they see themselves confronted with.

But also listen when they say things you may not like to hear. If anybody deserves a relaxation of a lockdown, and of pressure overall, surely it must be them, before you.

Guess it’s too much to ask that perhaps you may have learned some lessons lately, about things that you don’t need to do but that you always did. Or to ask you if you heard the birds singing louder in the bluer skies this morning.

Just out of curiosity: Did you know that Anne Frank spent 2 whole years locked down behind a wall?

We would like to run the Automatic Earth on people’s kind donations. Since their revenue has collapsed, ads no longer pay for all you read, and your support has become an integral part of the process. You can donate on Paypal or Patreon, which you find at the top of the right- and left sidebars on this page.

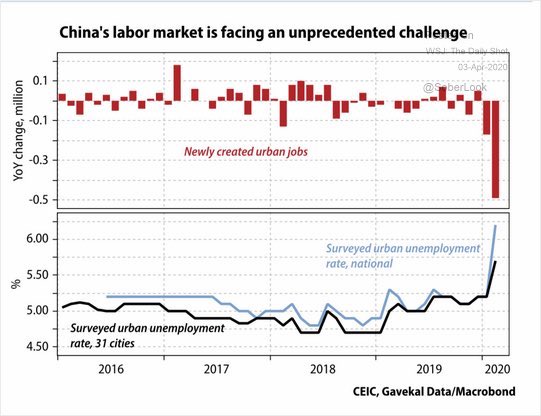

The coronavirus outbreak has already taken a great toll on the Chinese economy, with all headline readings pointing towards a record slowdown in growth during the first two months of the year. But there is an even greater danger for what was once the world’s fastest-growing major economy: that Covid-19 will become the catalyst that will bring its many long-simmering problems to the boil. At the centre of these problems is a rising systemic risk in its banking and financial systems caused by a high level of debt accrued over the past decade. The outbreak could not have occurred at a worse time. The past 10 years have not only seen the economy saddled with this debt, but it has also involved a steady structural slowdown that last year saw the growth rate fall to 6.1 per cent, the lowest in decades.

Now, just at the very time the country might consider spending more to prop up that growth rate, a raging pandemic means it will be making much less money than usual. The latest data from the Chinese Ministry of Finance shows fiscal revenue plunged by 9.9 per cent in the January-February period, the steepest drop since 2009. Overall tax revenue fell 11.2 per cent, driven by a 19 per cent slump in value-added tax (VAT) revenue, the main source of fiscal income. These drops come just as the government has offered a handsome tax cut in response to the pandemic. Meanwhile, the escalation of the pandemic in the rest of the world will only further weigh on China’s economic growth, corporate profits and personal income. In turn, this will inevitably drag down government revenue in months to come.

Beijing’s proposed stimulus spending will only exacerbate China’s already-massive debt pile, which had reached 310 per cent of gross domestic product by the end of last year, according to the Institute of International Finance. Many economies that have experienced such levels of debt have gone on to suffer a financial crash or economic crisis. China now accounts for about 60 per cent of the US$72.5 trillion emerging market debt. A deleveraging campaign had reduced Beijing’s debt mountain in 2018. But it has since returned to credit-driven stimulus to support growth and combat the effects of its trade war with the United States. About 80 per cent of China’s debt stock was accumulated over the past decade as the country strived to achieve the politically significant milestone of doubling its economic sizefrom 2010 to 2020. The milestone was a key goal in President Xi Jinping’s Chinese dream of “national rejuvenation”.

While the coronavirus threat has receded in China itself, any hope of an early recovery is forlorn as Covid-19 is still ripping through the major developed economies – essentially, China’s customers and trade partners. Plunging demand from abroad will create a second shock wave that will hit China’s export-oriented economy just as it is recovering from the first shock of having to lock down its cities. China’s balance sheet will be hit by both dwindling revenue and a spiralling demand for spending. Rising corporate debt, surging local government borrowings, and soaring non-performing loans for commercial banks are three areas that could wreck its fragile financial and banking systems. The non-financial corporate debt-to-GDP ratio jumped from 93 per cent in 2009 to 153 per cent last year [..]

China, America’s most powerful rival, has played a particularly harmful role in the current crisis, which began on its soil. Initially, that country’s lack of transparency prevented prompt action that might have contained the virus. In Wuhan, the epicenter of the outbreak, Chinese officials initially punished citizens for “spreading rumors” about the disease. The lab in Shanghai that first published the genome of the virus on open platforms was shut down the next day for “rectification,” as the Hong Kong-based South China Morning Post reported in February. Apparently at the behest of officials at the Wuhan health commission, news reports indicate, visiting teams of experts from elsewhere in China were prevented from speaking freely to doctors in the infectious-disease wards.

Some experts had suspected human-to-human transmission, but their inquiries were rebuffed. “They didn’t tell us the truth,” one team member said of the local authorities, “and from what we now know of the real situation then, they were lying” to us. Now China’s propagandists are competing to create a narrative that obscures the origins of the crisis and that blames the United States for the virus.

This irresponsible behavior and lack of transparency revealed what Trump’s National Security Strategy had identified early on: that “contrary to our hopes, China expanded its power at the expense of others.” Instead of becoming a “responsible stakeholder”—a term George W. Bush’s administration used to describe the role it hoped Beijing would play following China’s entry into the World Trade Organization in 2001—the Chinese Communist Party used the advantages of WTO membership to advance a political and economic system at odds with America’s free and open society. Previous National Security Strategy documents had tiptoed around China’s adversarial conduct, as if calling out that country as a competitor—as the 2017 document unequivocally did—was somehow impolite.

[..] Dependence on China for crucial medical equipment throughout the pandemic has illuminated the dangers of a hyper-globalized economy. Experts had warned of American dependence on key drug ingredients from China. The Wall Street Journal has reported that China is the only maker of key ingredients for certain classes of drugs, including established antibiotics that treat a range of bacterial infections such as pneumonia. American reliance on Chinese suppliers for other pharmaceuticals and medical supplies is also worrisome. Americans should not depend on an authoritarian rival state for its citizens’ health—any more than the United States and other free and open societies should give Chinese companies, and by extension the Chinese Communist Party, control over communications infrastructure and sensitive personal data.

It seems the new virus first began appearing in Wuhan last November to the bafflement of local doctors. On December 31, China reported a cluster of pneumonia-like cases to the WHO. On the same day, Taiwan tipped off the Geneva-based body that it had learned of medical staff in China falling ill – a clear sign of human-to-human transmission. Yet it said the information was not shared since the nation is excluded from a key WHO platform. Chen Chien-jen, Taiwan’s vice-president and an epidemiologist, said the WHO’s failure to obtain first-hand information on human transmission led to crucial delay. ‘An opportunity to raise the alert level both in China and the wider world was lost.’

The WHO confirms receiving an email mentioning ‘news reports of atypical pneumonia reported in Wuhan, and that Wuhan authorities said they believed it was not SARS’ but denies there was any mention of medical staff falling ill. There are suggestions Chinese authorities knew of human-to-human transmissions early in January, even as they detained doctors desperately trying to warn about a potential epidemic and accused them of spreading false ‘rumours’. Taiwan sent its own team to Wuhan in mid-January after failing to obtain clarification through official channels, which confirmed human transmission. There have also been credible claims on Chinese social media, repeated by online news reports, that an infected disease specialist in Wuhan alerted a senior WHO official in Asia because they had trained together and remained friends.

On January 11, a Chinese government respiratory expert who initially said the virus was ‘under control’ admitted he might have been infected in Wuhan. Media reports show medical staff were being treated in hospital for symptoms by January 15. Yet on January 14, the WHO confidently told the world that ‘the Chinese authorities have found no clear evidence of human-to-human transmission of the novel coronavirus identified in Wuhan’. It seems the new virus first began appearing in Wuhan last November to the bafflement of local doctors. On December 31, China reported a cluster of pneumonia-like cases to the WHO. On the same day, Taiwan tipped off the Geneva-based body that it had learned of medical staff in China falling ill – a clear sign of human-to-human transmission.

Yet it said the information was not shared since the nation is excluded from a key WHO platform. Chen Chien-jen, Taiwan’s vice-president and an epidemiologist, said the WHO’s failure to obtain first-hand information on human transmission led to crucial delay. ‘An opportunity to raise the alert level both in China and the wider world was lost.’ The WHO confirms receiving an email mentioning ‘news reports of atypical pneumonia reported in Wuhan, and that Wuhan authorities said they believed it was not SARS’ but denies there was any mention of medical staff falling ill. There are suggestions Chinese authorities knew of human-to-human transmissions early in January, even as they detained doctors desperately trying to warn about a potential epidemic and accused them of spreading false ‘rumours’.

Taiwan sent its own team to Wuhan in mid-January after failing to obtain clarification through official channels, which confirmed human transmission. There have also been credible claims on Chinese social media, repeated by online news reports, that an infected disease specialist in Wuhan alerted a senior WHO official in Asia because they had trained together and remained friends. On January 11, a Chinese government respiratory expert who initially said the virus was ‘under control’ admitted he might have been infected in Wuhan. Media reports show medical staff were being treated in hospital for symptoms by January 15. Yet on January 14, the WHO confidently told the world that ‘the Chinese authorities have found no clear evidence of human-to-human transmission of the novel coronavirus identified in Wuhan’.

A thread on the election of China's handpicked Director-General, Tedros Ghebreyesus (the first non-physician to ever lead the organization, FWIW), and how he came to lead the organization tasked with out global health. (Spoiler: he was supported by many current armchair QBs) 1/

Britain should pursue the Chinese government through international courts for £351 billion in coronavirus compensation, a major study into the crisis has concluded. It comes as 15 senior Tories led by former Deputy Prime Minister Damian Green write to Boris Johnson to demand a ‘rethink and a reset’ in relations with Beijing. The first comprehensive investigation into the global economic impact of the outbreak concludes that the G7 group of the world’s leading economies have been hit by a £3.2 trillion bill that could have been avoided if the Chinese Communist Party had been open and honest about the outbreak late last year.

Britain’s slice of the compensation sum includes the full cost of Chancellor Rishi Sunak’s economic bailout and hike in NHS spending in response to the crisis. The landmark study also directly highlights crunch British policy decisions made earlier this year – such as not cancelling flights from London to Wuhan in January – that were hampered or directly affected by misinformation from China and the acquiescent World Health Organisation. The report, to be published tomorrow by the Henry Jackson Society, a British foreign policy think-tank, says there is evidence that China directly breached international healthcare treaty responsibilities, and outlines ten legal avenues major nations could take to pursue damages from them.

It is titled ‘Coronavirus Compensation: Assessing China’s potential culpability and avenues of legal response’ and concludes: ‘The CCP (Chinese Communist Party) sought to conceal bad news at the top, and to conceal bad news from the outside world. Now China has responded by deploying an advanced and sophisticated disinformation campaign to convince the world that it is not to blame for the crisis, and that instead the world should be grateful for all that China is doing. ‘The truth is that China is responsible for Covid-19 – and if legal claims were brought against Beijing they could amount to trillions of pounds.’ Legal avenues include bringing a case at the Permanent Court of Arbitration at The Hague against China for breaking sanitary commitments, going to the UN and International Court of Justice, or the WTO.

When the coronavirus began to spread, Mongolia took sensible precautions. It halted border crossings from China, with which it shares a 2,877-mile border. Mongolia also imposed travel bans on people from South Korea and Japan, the other epicenters of the pandemic at the time. Yet the virus nonetheless found its way to Mongolia, where the first infected person — known as the “index case” — was a Frenchman who had come to the country from France via Moscow. The story is the same for many other countries that became part of the pandemic due to infected people carrying it from Europe. South Africa’s first coronavirus cases had gone to northern Italy for a skiing trip. South America’s first case was a Brazilian who had traveled to Italy’s Lombardy region, and Bangladesh’s first cases were Bangladeshis who had also come from Italy.

Panama’s index case was imported from Spain, and Nigeria’s first experience with coronavirus was an Italian business traveler. Jordan’s was imported from Italy. As Covid-19 cripples the U.S. and ravages many countries in the world, politicians are battling to craft a narrative of who is to blame for its damage. The virus started in China, of course, but narratives of how it went from epidemic to global pandemic often leave out a crucial element: the role of Europe. European countries have been hit much harder than Asian nations and have spread the virus significantly more than other regions. The Intercept went through news reports of Covid-19 index cases across the world, and the results were startling. Travel from and within Europe preceded the first coronavirus cases in at least 93 countries across all five continents, accounting for more than half of the world’s index cases.

Travel from Italy alone preceded index cases in at least 46 countries, compared to 27 countries associated with travel from China. One of the reasons European travel facilitated the spread of the coronavirus was because those countries were late to close air links. Italy closed one terminal of Milan’s main airport on March 16, when the northern region of Lombardy already had 3,760 cases in a population of 10 million people. By contrast, China had shut down flights out of Hubei province on January 23, when there were 500 reported cases worldwide and 17 deaths in Hubei among a population of 58 million. London’s Heathrow and Paris’s Charles De Gaulle airports are still open as cases soar in both of those cities, while Spain’s air operators only closed major terminals in Madrid and Barcelona when air traffic had ground to a halt anyway.

Japan’s Prime Minister Shinzo Abe has decided to declare a coronavirus emergency, according to the Nikkei, as new cases in the capital surged at a record pace. And while the Japanese publication notes that the government will hold an unofficial meeting of a panel of experts and start preparing for the declaration, Kyodo reported moments ago that Japan will declare a state of emergency on April 7, which would take effect on April 8. An emergency declaration gives governors in the areas covered formal powers, such as issuing requests that people stay home; Tokyo and surrounding areas, as well as Osaka, are expected to be affected by the declaration.

Abe has been criticized for not having already declared an emergency – a hesitance thought by many to stem from a strong desire to hold the Olympics this summer in Tokyo as originally planned. The International Olympic Committee decided in late March to postpone the games to 2021 after consulting with the prime minister and others. And yet, a conflict is set to emerge almost instantly because Japan’s constitution does not permit the government to demand that individuals stay home, owing to civil liberties concerns. Is Japan – which already buys billions in stocks just to avoid a market crash and preserve social order – about to also have a constituational crisis?

In any case, we find it strange that there were almost “no cases” in the weeks leading up to Japan’s reluctant decision to postpone this year’s Olympics, only to see a sudden record surge afterwards as Japan’s cases “mysteriously” soared, demonstrating once again that the coronavirus – or rather the tracking of its case and death toll – is first and foremost a political priority. Abe met with parties including Health Minister Katsunobu Kato and Yasutoshi Nishimura, the economic and fiscal policy minister, on Sunday to discuss the spread of infections. “If necessary, we will decide [to declare an emergency] without hesitation,” said Nishimura, who heads the government’s coronavirus response, on a show of public broadcaster NHK on Sunday. “We are looking for signs of an overshoot,” he said, referring to an explosion in cases, and noted that the atmosphere has grown extremely tense.

After going through model after model to make accouncements and set policy, Fauci says: “disease models “don’t tell you anything. You can’t really rely upon models..”

A web site that tracks actual hospital beds in use suggests the model used by top White House health officials to project the trajectory of the coronavirus has so far overestimated the number of Americans hospitalized by the disease by tens of thousands. Those projections, popularly known as the “Murray” model after the model’s lead author, University of Washington professor Christopher Murray, were explicitly cited by Dr. Deborah Birx, the response coordinator for the White House’s Coronavirus Task Force, at a press conference in the last week. Birx told reporters that Murray’s model, which predicts a shortage of tens of thousands of hospital beds throughout the country by the middle of April, underscored the task force’s “concern that we had with the growing number of potential fatalities” based on the model’s projections.

Yet a comparison of actual hospitalized patients by state and nationally suggests the model has so far overestimated the number of beds needed to treat pandemic patients. The forecast predicted, for example, that the United States would need around 164,750 hospital beds for COVID-19 patients on Saturday. Yet the COVID Tracking Project, a team of journalists and data analysts who collect and tabulate coronavirus data from state tallies around the country, reported only around 22,158 currently hospitalized coronavirus patients nationwide on Saturday. The discrepancies are also stark when looked at on a state-by-state basis. The model estimated that 65,434 patients would need hospital beds in New York State on Friday. In reality, there were 15,905 hospitalizations in that state by Sunday morning, according to the COVID Tracking Project.

Notably, the model touts its predictions as occurring under “full social distancing” through May of this year, meaning the projected hospitalizations are meant to occur even with significant quarantine measures. It is unclear why the model’s numbers are so significantly higher than the actual numbers observed in hospitals across the country. Officials have offered explanations for various model fluctuations ranging from data assumptions to the impact of stay-at-home orders. [..] at a White House press conference on Saturday, Birx said that coronavirus modelers are “re-evaluating all of their models in light of the level of the impact of the mitigation.” “Just to be clear, we won’t know how valid the models are until we move all the way through the epidemic,” she said.

Dr. Anthony Fauci, meanwhile, reportedly said during a recent meeting that disease models “don’t tell you anything. You can’t really rely upon models.” Fauci has elsewhere indicated a preference for overestimating the possible effect of the coronavirus pandemic in the United States, telling reporters in March: “I think we should be overly aggressive and get criticized for overreacting.”

In a state where the government usually operates on the basis of buy now, pay later (often much, much later), the emergency of the coronavirus pandemic has required a decidedly different approach. About two weeks ago, Illinois officials tracked down a supply of 1.5 million potentially life-saving N95 respirator masks in China through a middleman in the Chicago area and negotiated a deal to buy them. One day before they were expecting to complete the purchase, they got a call in the morning from the supplier informing them he had to get a check to the bank by 2 p.m. that day, or the deal was off. Other bidders had surfaced.

Realizing there was no way the supplier could get to Springfield and back by the deadline, Illinois assistant comptroller Ellen Andres jumped in her car and raced north on I-55 with a check for $3,469,600. From the other end, Jeffrey Polen, president of The Moving Concierge in Lemont, drove south. Polen isn’t in the medical supply business, but he “knows a guy,” an old friend who specializes in working with China’s factories. As they drove, Andres and Polen arranged to meet in the parking lot of a McDonald’s restaurant just off the interstate in Dwight. They made the handoff there. Polen made it back to his bank with 20 minutes to spare. Illinois already has received part of the mask shipment. There’s more on the way.

That’s just a taste of the “Wild West” world of emergency procurement taking place over the past several weeks as the state fights for equipment and supplies to protect frontline workers and patients in the battle against COVID-19. Most of that work is being performed by Gov. J.B. Pritzker’s administration through a rapid-procurement strike team, pulling together procurement specialists from around state government under the auspices of the Illinois Emergency Management Agency. [..] They’re all looking for what we have come to know as PPE or personal protective equipment — masks, gloves, gowns and face shields — plus coronavirus testing kits and swabs and, most prized of all, ventilators to help those most seriously ill keep breathing.

There’s a separate team working just on ventilators, said Deputy Governor Christian Mitchell, who is overseeing the procurement efforts for Pritzker. When they find what they need, they have to move immediately to complete the purchase before losing out to another bidder — even as the competition causes prices to jump to levels that would have been ridiculous just a month ago.

Mexico’s president unveiled a plan on Sunday to lift the economy out of the coronavirus crisis, vowing to help the poor and create jobs, but his promise of fiscal discipline sparked criticism that the measures fell far short of what was needed. President Andres Manuel Lopez Obrador pledged Mexico would create 2 million new jobs in the next nine months and boost small business and housing loans. He also vowed to tighten public sector austerity to avoid debt. Governments worldwide have unleashed unprecedented spending pledges to minimise damage to their economies from the coronavirus, including a $2-trillion package by Mexico’s top trading partner, the United States.

But Mexico’s leftist leader, targeting measures for the “most vulnerable”, said he would use a budget stabilization fund and cash from public trusts to fund plans to shield the poor from a slump economists expect to be severe. “This crisis is temporary, transitory,” Lopez Obrador said in a televised speech. “Normality will return soon. We will defeat the coronavirus, we will reactivate the economy.” Last week, Lopez Obrador said about $10 billion was available from various rainy day funds, while the finance ministry said “buffers” for the economy included a stabilization fund of about $6.6 billion available from the end of 2019.

Known by his initials “AMLO”, the president said Mexico would announced next week investments in the energy sector worth 339 billion pesos ($13.5 billion) to boost the economy, which some private analysts forecast to contract by up to 10% in 2020. That sum is far less than $92 billion in energy investments the private sector has proposed to the president.

Congress needed a year of intense infighting to approve a $4.7 trillion budget, but just a single week to draft this $2 trillion deal. Although members quibbled over numbers before the vote — Bernie Sanders insisted on more unemployment insurance, while others worried about creating a “slush fund” for airlines and other industries — the bill ultimately cruised through, passing in a voice vote in the House and 96-0 in the Senate. The Emergency Economic Stabilization Act of 2008, the only comparable “We need a gazillion dollars in 10 minutes” legislation in recent history, passed after a bitter battle, with 63 House Democrats and 91 House Republicans opposing. Analysts and politicians insisted the new bailout, in the broad strokes, was uncontroversial, a fire hose of money for virus-ravaged hospitals, workers, and small businesses.

Even critics of Wall Street agreed that this one isn’t a complete washout compared with the last disaster, when the taxpayer was asked to bail out the very people who’d caused the crisis. “At least this bailout has a Main Street component,” says Dennis Kelleher of Better Markets, a financial watchdog group. There are serious logistical questions about how money is supposed to get to Main Street — like, for instance, the use of the tiny Small Business Administration to push $377 billion in emergency loans out the door — but the larger problem has to do with the meat of the bill: the backstopping of the financial sector. As happened in the run-up to September 2008, Wall Street in recent weeks warned of Armageddon if the Fed did not immediately start spending billions per minute to buy every conceivable kind of financial product.

The Fed responded by dusting off emergency lending facilities like the Term Asset-Backed Securities Loan Facility, the Commercial Paper Funding Facility, the Money Market Mutual Fund Liquidity Facility, the Primary Dealer Credit Facility, the Secondary Market Corporate Credit Facility, and the Primary Market Corporate Credit Facility, all of which saw action after the crash of 2008. Each would be used to step in and buy financial products in the various markets frozen due to virus panic.The Fed furthermore announced that on March 23rd it would begin buying $50 billion in government-backed mortgage securities, in addition to $75 billion in Treasury bills, every day.

They’ve since lowered those numbers, but the scale of these interventions dwarfs any of the Fed’s actions post-2008. A $50 billion buying spree roughly represents as much Fed support of mortgage markets in one day as was done across a month at the peak of the last round of Quantitative Easing. Taken in conjunction with the CARES Act, the Fed and the Treasury were now positioned to become a major ongoing buyer of everything from mortgages to U.S. government debt to exchange-traded funds to corporate bonds to money-market funds.

[..] The Fed “balance sheet” as of Friday was already at $5.3 trillion, nearly $800 billion higher than its previous peak in May 2016. Wall Street analysts are predicting this number will eventually reach $10 trillion, and why not? Fed chief Jerome Powell signaled that assistance would be unlimited when he said the central bank “would not run out of ammunition.” As with 2008, the emergency support is supposed to be temporary, but there’s less belief that this is even ostensibly true this time around. There will be a lot of howling over the irony: Trump when he ran for president in 2016 said then-Fed chief Janet Yellen should be “ashamed” of creating a “false stock market” for Barack Obama. Our future will be a parody of the Yellen economy. Short-term loans to make payroll and keep tenants in storefronts are only a part of the rescue. The coronavirus emergency is probably temporary. The bailout looks like forever.

UK Prime Minister Boris Johnson will remain in hospital on Monday after being admitted for “persistent symptoms of coronavirus,” ten days after first testing positive for it. The prime minister was admitted to St Thomas’ Hospital in Westminster at 8pm on Sunday on the advice of his doctor after continuing to exhibit a high temperature. A spokesperson insisted on Sunday that Johnson’s hospital admission was not an “emergency” measure but had merely been for precautionary reasons in order to carry out tests. However the Times of London newspaper reported that the prime minister was treated with oxygen on arrival. Downing Street has repeatedly insisted that Johnson was only experiencing “mild symptoms” of the virus.

However, aides have reportedly become “increasingly worried” about the prime minister’s health in recent days, according to multiple reports, with Johnson heard “coughing and spluttering” his way through conference calls. Johnson was “more seriously ill than either he or his officials were prepared to admit,” according to the Guardian, which reported a source suggesting that Johnson “was being seen by doctors who were concerned about his breathing.” The Sun newspaper reported a Downing Street source suggesting that Johnson would remain in hospital “as long as necessary.” Asked about the prime minister’s condition on Monday the Housing Secretary Robert Jenrick told the BBC that Johnson was “still very much in charge of the government.”

IMHO #property#landlords#prs#btl#housing Sectors will mirror Great Depression 1929/30's (Chart Below). Pandemics of 1918 & 1969 show DOW bottomed at 33% prior to true recovery, thus can we use this to find #FTSE & #property bottom Post COVID-19 will see Paradigm shift for ALL pic.twitter.com/dEzhhYkjmc

Last Wednesday, we published the success story from Dr. Vladimir Zelenko, a board-certified family practitioner in New York, after he successfully treated 350 coronavirus patients with 100 percent success using a cocktail of drugs: hydroxychloroquine, in combination with azithromycin (Z-Pak), an antibiotic to treat secondary infections, and zinc sulfate. Dr. Zelenko said he saw the symptom of shortness of breath resolved within four to six hours after treatment. Hydroxychloroquine is now being used worldwide, according to a map from French Dr. Didier Raoult. In the meantime, scientists at University of Pittsburgh School of Medicine believe they’ve found potential vaccine for coronavirus.

Now, Dr. Zelenko provides updates on the treatment after he successfully treated 699 COVID-19 patients in New York. In an exclusive interview with former New York Mayor, Rudy Giuliani, Dr. Vladmir Zelenko shares the results of his latest study, which showed that out of his 699 patients treated, zero patients died, zero patients intubated, and four hospitalizations. Dr. Zelenko said the whole treatment costs only $20 over a period of 5 days with 100% success. He defines success as “Not to die.” Dr. Zelenko first posted his Facebook video message last week calling on President Trump to “advise the country that they should be taking this medication.”

There are many other success stories about hydroxychloroquine across the country. Last week, Dr. William Grace, an oncologist at Lenox Hill Hospital in New York City, said they’ve not had a single death in their hospital because of hydroxychloroquine. “Thanks to hydroxychloroquine, we have not had a death in our hospital,’ Dr. Grace said.

Also, in a study conducted by the National Institute of Health (NIH) also confirmed some of Dr. Dr. Zelenko’s findings. The study by NIH showed that Zinc supplementation decreases the morbidity of lower respiratory tract infection in pediatric patients in the developing world. A second study also conducted by NIH titled: “In Vitro Antiviral Activity and Projection of Optimized Dosing Design of Hydroxychloroquine for the Treatment of Severe Acute Respiratory Syndrome Coronavirus 2 (SARS-CoV-2),” also showed hydroxychloroquine to be more potent in killing the virus off in vitro (in the test tube and not in the body).

One for our medical commenters. A Chinese study that suggests the virus in first instance attacks blood cells, not lungs. This could also explain why chloroquine is effective. By the way, word has it that doctors are taking hydroxychloroquine on a regular basis to protect themselves. Note: It is no use when taken either too early or too late.

@yishan on Twitter: “Virus is disrupting the hemoglobin’s oxygen capacity. It is attacking our BLOOD first, not the lungs. It is NOT a respiratory ailment (primarily), lung breakdown symptoms are a consequence of the attack on blood hemoglobins. Hypoxia is happening BEFORE lungs are affected.”

The novel coronavirus pneumonia (COVID-19) is an infectious acute respiratory infection caused by the novel coronavirus. The virus is a positive-strand RNA virus with high homology to bat coronavirus. In this study, conserved domain analysis, homology modeling, and molecular docking were used to compare the biological roles of certain proteins of the novel coronavirus. The results showed the ORF8 and surface glycoprotein could bind to the porphyrin, respectively. At the same time, orf1ab, ORF10, and ORF3a proteins could coordinate attack the heme on the 1-beta chain of hemoglobin to dissociate the iron to form the porphyrin. The attack will cause less and less hemoglobin that can carry oxygen and carbon dioxide.

The lung cells have extremely intense poisoning and inflammatory due to the inability to exchange carbon dioxide and oxygen frequently, which eventually results in ground-glass-like lung images. The mechanism also interfered with the normal heme anabolic pathway of the human body, is expected to result in human disease. According to the validation analysis of these finds, chloroquine could prevent orf1ab, ORF3a, and ORF10 to attack the heme to form the porphyrin, and inhibit the binding of ORF8 and surface glycoproteins to porphyrins to a certain extent, effectively relieve the symptoms of respiratory distress. Favipiravir could inhibit the envelope protein and ORF7a protein bind to porphyrin, prevent the virus from entering host cells, and catching free porphyrins. Because the novel coronavirus is dependent on porphyrins, it may originate from an ancient virus.

It must be possible to run the Automatic Earth on people’s kind donations. These are no longer the times when ads pay for all you read, your donations have become an integral part of it. It has become a two-way street; and isn’t that liberating, when you think about it?

Thanks everyone for your wonderfully generous donations over the past days.

Joe Biden: “We cannot let this, we’ve never allowed any crisis from the Civil War straight through to the pandemic of 17, all the way around, 16, we have never, never let our democracy sakes second fiddle, way they, we can both have a democracy and … correct the public health.” pic.twitter.com/Ymz8JtQvjH

— Trump War Room – Text TRUMP to 88022 (@TrumpWarRoom) April 6, 2020

Remember this? Musicians from the Rotterdam Philharmonic Orchestra virtually came together to play Beethoven’s ‘Ode to Joy’ from their homes pic.twitter.com/I3s1YqUVkU

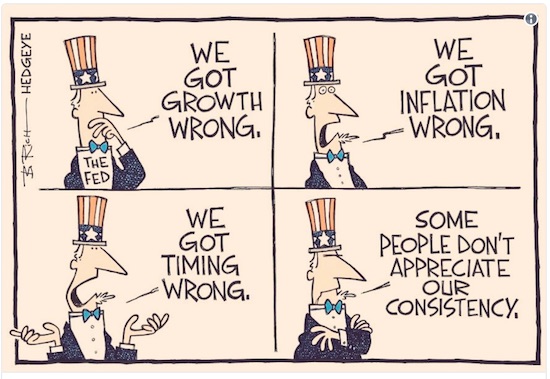

You would think, certainly if you were as naive and innocent as I am, that when you get offered the job of Chair of the Federal Reserve, you must be sure, before accepting, that you have the credentials and the knowledge required. If you don’t, it looks as if you don’t take the job seriously. Janet Yellen, who’s been Chair since January 2014, doesn’t seem to agree.

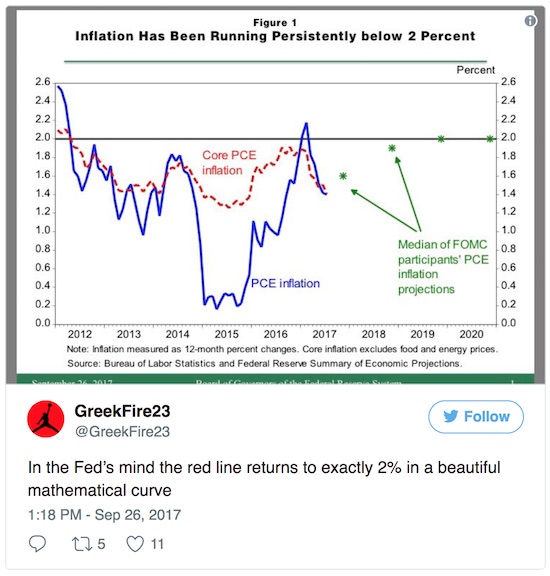

In a speech Tuesday for the National Association for Business Economics Yellen ‘honestly’ admitted that she doesn’t understand inflation, control of which is the Fed’s no.1 task (it’s debatable whether that’s a good idea). She doesn’t understand a bunch of other issues either. Those are her own words, not mine. Here are these own words:

“My colleagues and I may have misjudged the strength of the labor market, the degree to which longer-run inflation expectations are consistent with our inflation objective, or even the fundamental forces driving inflation..”

Clear enough, you would think. But she didn’t offer her resignation. And for an important post like Fed chair, that is a major problem. As she undoubtedly does. So why is she keeping her job? Doesn’t she realize that when you don’t understand the issues you deal with, you’re prone to make disastrous mistakes?

Yellen and her colleagues work with models, and the models are wrong. The Fed’s predictions for things like inflation are ridiculously off, all the time. That may be news to her, but it’s old hash for many people in her field. So that she’s surrounded solely by people who don’t understand these things either is not an excuse.

So what does she expect now? That she will start to understand them all of a sudden, after years and years of not being able to? That reality will change to comply with her models? We can discount the option that she will suddenly begin using entirely different models, they’re all she has. But what then?

Under her predecessor Ben Bernanke, who never conceded he had no idea either but still didn’t, the Fed lowered interest rates to near zero Kelvin and bought trillions of dollars in bonds and securities. Now Yellen for some reason thinks it’s time to get rid of the stuff.

But on what basis does she make such a decision, if she self-admittedly doesn’t even understand the fundamental forces in play? How is that different from handing a box of matches to a 3-year old? Isn’t she really simply an academic dropped in a casino? From CNBC:

Yellen said a regular pace of rate hikes ahead is likely still warranted, though Fed officials are looking closely at the assumptions underlying those projections. While conceding that the Fed may need to slow the removal of accommodation, she also said the central bank “should also be wary of moving too gradually.”

There comes a point when naive innocent me starts asking: what does that even mean? Rate hikes are warranted but we don’t know why? Accommodative policies have been going too fast but they shouldn’t be too slow? Based on what? It can only be based on models that have proven faulty, can’t it, because they have no others.

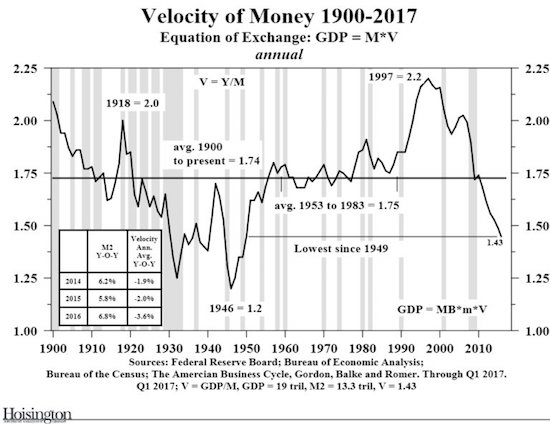

Here are a few pointers for the occupants of the Marriner S. Eccles Federal Reserve Board Building. Inflation is money velocity multiplied by money and credit supply. MV = PY. M is money supply, V is velocity, P is price level and real GDP is Y.

Velocity of money means consumer spending. 70% of US GDP is consumer spending. But American consumers are neck deep in debt and have very little money left to spend. Much of what they spend, they must borrow.78% of Americans live paycheck to paycheck. So forget about money velocity.

Moreover, as for the Fed’s second mandate after inflation, full employment, they don’t get that one either. They seem to act on the presumption that any one job is just like the other. And then bleat: “My colleagues and I may have misjudged the strength of the labor market”.

But America has turned into a nation where the gig economy (the natural successor to first the knowledge economy, then the service economy), waiters, greeters and people working 3 jobs just to make ends meet have become the norm. When in the present circumstances you claim to have almost ‘achieved’ full employment, as Yellen and the Fed do, you must really be blind as a bat.

The other side of the equation is money supply. Interestingly, the Fed has issued tons of it, but handed it all to its owner banks. If they had spent it inside the economy itself, we could have been looking at a whole other picture. If those trillions would have gone to investment, manufacturing etc., instead of propping up banks and companies buying their own shares, Yellen might have actually seen some inflation.

If Americans have no money to spend, there can not be inflation. Simple. But the same stupid faulty predictions just keep coming:

So why is anybody still paying attention to Janet Yellen? Well, because she has her finger on the biggest financial trigger on the planet. No matter how shaky and uneducated that finger may be. Or do we pay attention exactly because we know what’s behind that shaky finger? Do we all put everything on red just because grandma does it too?

The craziest thing of all is that in reactions in the media to Yellen’s speech, she’s praised for admitting she has no clue what she’s doing. That takes the cake. And eats it too. Praised for admitting you’re terribly unfit for your job. That’s just great. That’s Bizarro world.

It’s well past best before time to get rid of Janet Yellen, and all the intellectual but idiots who work at the Fed. What is it, 1,000 PhDs, or was that 10,000? But the only thing that makes any real sense of course, the only thing that can save the nation, is to get rid of the Fed and its braindead mandates, interests and occupants altogether.

Hedgeye got this one painfully right:

And yeah, I know Yellen could be fired too if she doesn’t resign, but with Goldman Sachs all over the White House, what are the odds? And who would come in when she goes? She’s ideal, who’s going to get angry at a barely 5′ grandmother even is she clearly out of her depth and league?

There’s so much negative real bad economic and financial news out there that it’s hard to choose a ‘favorite’, but I guess I’m going to have to go with what underlies and ‘structures’ it all, the IIF stating that for the first time since 1988 and the Reagan presidency, there’s more money flowing out of emerging markets than there’s flowing in. That is for sure a watershed moment.

And no, that trend is not going to be reversed either anytime soon. Emerging economies, even if they wouldn’t include China -but they do-, have relied exclusively on selling ‘stuff’ to the rich world which combined cheap commodities with cheap labor, and now they see their customer base shrink rapidly just as they were preparing to harvest the big loot.

Now, I hope I can be forgiven for thinking from the get-go that this was always a really dumb model. That emerging nations would provide the cheap labor, and the west would kill of its manufacturing base and turn into a service economy.

This goes very predictably wrong if and when we figure out that A) economies that don’t manufacture anything can’t buy much of anything, and B) that we can sell those services our economies are ‘producing’ only to ourselves, as long as the emerging nations maintain a low enough pay model to make their products worth our while to import.

It makes one wonder how many 6 year-olds would NOT be able to figure this out. In the same vein, how many of them would be hard put to understand that our economies, overwhelmed by, and drowning in, debt, cannot be rescued by more debt? Here’s thinking the sole reason so many of us don’t get it is that we’ve been told it’s terribly hard to grasp, and you need a 10-year university course to ‘get it’.

I see a bad US jobs report coming in as we speak, and that’s not really saying much of anything. The damage not only runs far deeper than those massaged reports, it’s also already been done ages ago. Non-farm employment reports are Brooklyn Bridge-for-sale territory.

We’d all be much better off looking at the $11-13 trillion in ‘value’ lost from global equity markets in Q3. Or, for that matter, at Goldman’s statement that, and I’m only slightly paraphrasing here, only companies buying up their own stocks could save the S&P 500 for 2015.

Think about it: we don’t make much of anything anymore, and what we do make hardly anybody wants to buy, so we issue debt and buy it up ourselves. This may well be presented as a clever ‘investment’ model, but I aks of you: how much closer to eating our own excrements are we comfortable getting?

Stock buybacks can have strategic advantages in specific circumstances in healthy economies, but massive buybacks on the back of too-cheap credit/debt is not one of those circumstances. It’s desperation writ very large.

One other article that stuck out, because it brings into the bright shining limelight the longtime Automatic Earth assertion that we are headed for a disastrous “multiple claims to underlying real wealth”, is Paul Brodsky’s piece served by Tyler Durden. It has far more value than any alleged jobs article, because it describes the real world, not some distorted fantasy:

[..] the data show plainly there are five times as many claims for US dollars as US dollars in existence. Does this matter to investors? Well, yes, it matters a lot. Not only is there not enough money to repay outstanding debt; the widening gap between credit and money is making it more difficult to service the debt and more difficult for nominal US GDP to grow through further credit extension and debt assumption.

Remember, only a dollar can service and repay dollar-denominated debt. Principal and interest payments cannot be made with widgets or labor, only dollars. This means that future demand and output growth generated through more credit issuance and debt assumption is self-defeating. In fact, it adds to the problem.

[..] the value of dollar-denominated assets is not supported by the money with which it is ostensibly valued. This has not been a problem historically because the proportion of un-reserved credit has been low relative to asset values and cash flow. As we are seeing today, however, it is becoming a significant problem because balance sheets are already highly levered and zero-bound interest rates chokes off the incentive to refinance asset prices higher.

If the total value of US denominated assets is, say, $100 trillion, and the US dollar money stock is somewhere around $12 trillion, then the inescapable implication is that the market’s expects either: a) $88 trillion more US dollars will be created in the future to fund the purchase of the gross asset pool at current valuations; b) there has to be a decline in the nominal value of aggregate assets, or; c) both.

The US is not going to ‘create’ $88 trillion. More debt cannot solve this. And so the only option available is a huge decline in asset ‘values’. ‘Values’ that have been grossly distorted for years now, and which we all could have known can’t be kept from falling back to earth indefinitely.

Just this morning, we saw 3 other key indicators all point way down. That’s not in itself peculiar or anything, what’s peculiar is that it’s taken so long for people to figure out which way the wind blows. And I betcha, most still won’t get it. Because they’re all exclusively looking for signs of a recovery.

They’ve been looking for 8 years or so now, and there’s always some piece of data that can be found to feed the blinders, but it’s all been nonsense for 8 years running. Your economy, my economy, and the global economy, can and will not recover, and certainly not as long as more debt is injected in our already insanely overindebted financial systems.

I don’t want to make this another of those endless articles, but do click the links, and do read up on each of them. And then shiver. Have a stiff drink. Unless you’re still looking for a recovery. And let’s not forget, yes, it’s true that massive stock buybacks in the US, Europe, perhaps even China, as well as more QE to infinity and beyond, may save a bunch of numbers and you might be sitting pretty yet under the yuletide tree.

But the simplest of principles stands no matter what: there’s no way out of this that doesn’t lead through the exact kind of massive debt deleveraging that all governments and central banks are ostensibly trying desperately to prevent. And which will make the debt deflation, certainly after 8 years of trying to push the 180º opposite way, epic and monumental.

On the bright side: at least if you would have read the Automatic Earth through those past 8 years, you would have known and hopefully been prepared for that debt deflation. It’s not as if it’s something new or unexpected, not around here.

$13 trillion in market losses in just one quarter would be very hard to make up for even in very favorable circumstances. We have no such circumstances. We’ve built our very lives on squeezing China et al for 27 years, and issuing more debt as if there’s no tomorrow -sort of a self-fulfilling prophecy-, and now we’ve belatedly realized that there’s a time limit on that model.

But hey, by all means, it’s your money, and it’s your life, so do keep on betting on that recovery, and the return to ‘normal’, whatever that once was. Put it all on red. Go crazy! You do risk becoming a lonely crowd though. Meanwhile, those of us down here with our feet planted in the real earth have just this one question: “How bad can this get, and how fast?”.