Pablo Picasso Portrait of Dora with bun 1937

Conservative journalist/editor Peter Oborne says the exact same thing I said a few days ago in A Tale of Two Cummings. Boris Johnson is just a figurehead.

Nigel Farage is complaining that the Tories want him and his Brexit party to step aside, but that’s Cummings and his polls that show Farage is too unpopular.

• The Future Of Britain Is In The Hands Of Unelected Svengali Cummings (Oborne)

Cummings is no longer in the shadows, operating behind the scenes — this Svengali is out in the open. Indeed, he seems to relish being seen in public, striding ostentatiously into Downing Street every morning. Now, we are all familiar with his shaven head, scruffy T-shirts, crumpled appearance and contemptuous and appraising eyes, his newspapers and bundles of documents carried in a Vote Leave bag. According to some papers, and many ministers and civil servants I have spoken to recently, this is the man who is truly running Britain. It’s Cummings who oversees the No 10 grid which controls the timing of announcements and public events. It’s in this capacity that he dispatches the PM up and down Britain, photographed in hospitals, sharing selfies with nurses, and on construction sites wearing a hard hat.

It is also Cummings, not Johnson, who determines political strategy — hence the huge public spending announcements on health, extra police and other issues. Indeed, it looks very much as if Johnson has become the public face of Cummings. And this, I am afraid, is profoundly disturbing. No one ever voted for Cummings, he has little experience of life outside politicking yet he has been given unprecedented power at a moment of immense crisis in the national fortunes. Within hours of Johnson becoming Tory leader two weeks ago, newly anointed special adviser Cummings called ‘his’ staff together in the magnificent Downing Street first-floor state room. He told them that he plans to deliver Brexit ‘by any means necessary’.

Quoting Michael Jordan: “Some people want it to happen. Some wish it to happen. Others make it happen.”

• No-Deal Brexiteers Are Winning Because They Want It More (Sky)

Consider this: we now have a prime minister and a government, buttressed by a not inconsiderable rump of the Conservative party, who have made it clear that there is not a convention they are not willing to break, an institution they are not willing to smash, a precedent they are not willing to burn, in the pursuit of their goal. The PM and his coterie have said that they would prorogue parliament because it might stand in their way; that they are willing to schedule an election far in excess of the usual time limits because it would ensure our exit on the 31 October. In so doing they would therefore go against yet more precedent in pursuing a highly tendentious policy during an election period (where normally a caretaker administration would do little of controversy).

And now, we have news that the prime minister would squat in Number 10 after he loses a confidence vote in the House of Commons. He is even willing to do so, apparently, if the Commons coalesces around an alternative prime minister, despite the fact the Cabinet Manual (the closest we have to a constitution) makes it clear that this is quite unacceptable and that it would risk the neutrality of the Queen. All of this would be constitutional vandalism. Brexit then, “whatever the cost”, as Dominic Cummings has said. It is a nihilistic vision of politics and indeed, a most unusual one for self-described “Conservatives” but it is, relentless and clear-sighted. Indeed, its recklessness has imbued this administration with a strange purpose and energy.

Larry craves attention.

• UK Too Desperate To Secure US Trade Deal – Larry Summers (G.)

The former US treasury secretary Larry Summers has said he does not believe that a “desperate” UK would manage to secure a post-Brexit trade deal with Washington, as Dominic Raab, the new foreign secretary, heads to the US to scope out the potential for such an agreement. Summers, who was a senior official under Bill Clinton and Barack Obama, said the UK was in a weak position when it came to negotiating with trade partners. He told BBC Radio 4’s Today programme on Tuesday: “Britain has no leverage, Britain is desperate … it needs an agreement very soon. When you have a desperate partner, that’s when you strike the hardest bargain.”

Despite warm words from Donald Trump about a trade deal, Summers said: “We have economic conflict with China and, even on top of that, the deterioration of the pound is going to further complicate the negotiating picture. “We will see it as giving Britain an artificial comparative advantage and make us think about the need to retaliate against Britain, not to welcome Britain with new trade agreements.” Even if the two countries could come to an agreement, Summers said, the UK was in a weak negotiating position. “Britain has much less to give than Europe as a whole did, therefore less reason for the United States to make concessions,” he said. “You make more concessions dealing with a wealthy man than you do dealing with a poor man.”

The UK says the EU doesn’t want to talk, and vice versa. The demand to take the backstop out is a perfect dealbreaker. It can only lead to a no-deal Brexit. Re: Cummings.

• Brexit: Michael Gove Accuses ‘Wrong And Sad’ EU Of Intransigence (G.)

Michael Gove has accused the European Union of intransigence over Brexit talks, calling it “wrong and sad”, as divisions between the UK and Brussels became further entrenched with the government seemingly intent on a no-deal departure. Gove, who is in charge of no-deal preparations, reiterated Boris Johnson’s position that the only route to progress would be the EU starting again with withdrawal negotiations, something Brussels has repeatedly and consistently ruled out. Adding to the impression of Johnson’s hardening position, newly released government read-outs of the prime minister’s phone calls with a series of EU leaders over recent days showed he delivered the same uncompromising message to them.

While the Irish prime minister, Leo Varadkar, insisted on Tuesday that a no-deal departure was not inevitable, both he and the country’s finance minister, Paschal Donohoe, warned of a significant and long-term change to relations between the countries if it did happen. Downing Street has increasingly pushed the message that Brexit will happen on 31 October under any circumstances – even intimating that No 10 believes the mandate of the 2016 Brexit referendum would overrule even a blocking vote in parliament.

There is increasing worry among some MPs that Johnson could try to force through a no-deal Brexit against the will of the Commons, with his de facto chief of staff, Dominic Cummings, reportedly threatening No 10 staff with the sack if they dissent. The government’s official position is still that it is seeking a formalised departure, albeit only if Brussels ditches the Irish backstop border insurance policy and reopens the withdrawal agreement.

And of course Britain is anxious to keep the Skripal narrative going. In reality, all it would take is to present the man.

• Met Police Examine Vladimir Putin’s Role In Salisbury Attack (G.)

Scotland Yard has examined the role of the Russian president, Vladimir Putin, in the novichok nerve agent attack in Salisbury, it has been revealed. Putin is assessed by UK intelligence agencies as having been “likely” to have approved of the attack in March 2018 on Sergei Skripal, a former Russian military officer, and his daughter, both of whom were left seriously ill but survived. Dawn Sturgess later died after coming across a discarded perfume bottle used by two Russian intelligence agents to carry the military grade nerve agent. Two Russian agents have been charged over the attack, and Britain wants them extradited and has issued a European arrest warrant (EAW) and Interpol red notice for their detention.

The Metropolitan police assistant commissioner Neil Basu, the head of UK counter-terrorism policing, said the investigation into the attack was continuing. Basu said the issues involved in bringing charges over the attack were complex. “You’d have to prove he [Putin] was directly involved,” he said. “In order to get an EAW, you have to have a case capable of being charged in this country. We haven’t got a case capable of being charged. “We’re police officers, so we have to go for evidence. There has been a huge amount of speculation about who is responsible, who gave the orders, all based on people’s expert knowledge of Russia. I have to go with evidence.”

“The movement in forward points may reflect a tightening in USD (dollar) liquidity..”

• China State Banks Seen Supporting Yuan In Forwards Market (R.)

China’s state banks have been active in the onshore yuan forwards market this week, using swaps to tighten dollar supply and support the Chinese currency, four sources with knowledge of the matter told Reuters. The spot value of the yuan has fallen sharply this week against the dollar as tensions between China and the United States escalated and prompted fears that their trade war could shift into a currency war. The sources said banks had conducted significant amounts of buy-sell swaps in the onshore market on Tuesday. Buy-sell swaps help to reduce the supply of dollars that the market can access to short-sell the yuan. “Yesterday big banks were all selling one-year onshore forward swaps, then in the afternoon the spot dollar-yuan fell,” said a trader at a foreign bank in Shanghai.

One state bank also was seen active in offshore forward swaps, two traders at foreign banks with knowledge of the matter said. On Wednesday, one-year onshore dollar-yuan forwards were at 175 points, down from 321 points on Monday, according to Refinitiv data. One-year offshore dollar-yuan forwards were at 459 points, down from 640 points on Monday. “The movement in forward points may reflect a tightening in USD (dollar) liquidity when some market participants need to buy spot dollars and sell them back in forwards. Meanwhile, the spot and outright moves were also partly due to a stabilization in RMB (yuan) sentiment on Tuesday,” said Frances Cheung, head of macro strategy for Asia at Westpac in Singapore.

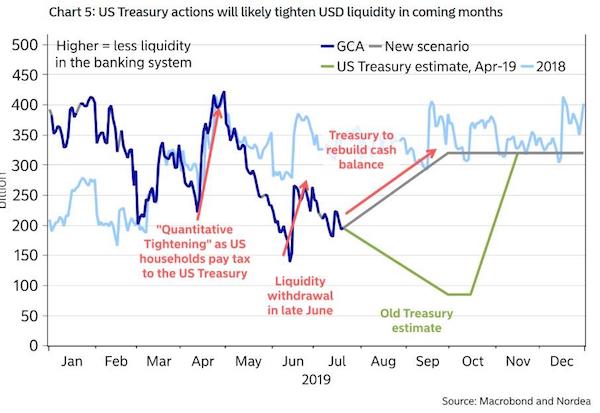

Liquidity.

• Forget China, The Fed Has A Much Bigger Problem On Its Hands (ZH)

The Fed may have launched its first easing cycle since 2007 and liquidity-sapping quantitative tightening may finally be over, but Powell may have a much bigger problem on his hands – one which has nothing to do with China, and everything to do with a dramatic drain of liquidity in the market over the next two months.

We first hinted at this last week when we noted that as part of the recently completed debt ceiling deal, instead of taking its time in replenishing the cash balance (green line in the chart below), the US Treasury will scramble to rebuild its cash balance up to $350 billion, from today’s level of $133 billion (gray line), a process which as we said last Wednesday will “significantly tighten up liquidity in the banking system and potentially result in turmoil in funding and money markets as the world is flooded with an issuance of T-Bills” as the Treasury seeks to fill the $217 billion cash hole, which will lead to a substantial liquidity withdrawal from the broader financial system as shown in the following Nordea chart.

The problem, in a nutshell, is that traditionally such a rapid liquidity withdrawal leads to weaker risk appetite, a far stronger USD and lower treasury yields, while widening the LIBOR/OIS spread and further depressing the already negative EURUSD cross-currency basis. While we cautioned about all this last week (even before the FOMC announcement), it appears that our appreciation of just how severe this problem may be for the Fed and capital markets was overly optimistic, because according to a new analysis by Bank of America’s Mark Cabana, the Fed may have no choice but to resume Quantitative Easing and start expanding its balance sheet again – potentially as early as 4Q – in order to ease funding pressures expected during the coming wave of Treasury supply.

Debt denominated in dollars by any chance?

• Papua New Guinea Asks China To Refinance Its National Debt (G.)

Papua New Guinea has asked China to refinance its entire government debt in a blow to Australia’s attempts to counter China’s influence in the region. The request marks a “significant shift” in regional politics and PNG’s allegiances, according to Pacific experts. Australia has traditionally been the largest aid donor and most important ally of PNG, but in recent years ties between China and PNG have strengthened. PNG’s prime minister, James Marape, visited Australia two weeks ago at the invitation of his counterpart, Scott Morrison, in his first international visit since becoming the Pacific nation’s leader at the end of May.

In a speech during his visit, Marape said he wanted PNG to move away from an “aid-donor” relationship with Australia within 10 years, and step up alongside its neighbour as a leader in the Pacific region. However, on Tuesday, after a meeting with Xue Bing, the Chinese ambassador in Port Moresby, Marape requested that China refinance its debts of A$11.8bn (27bn kina, or US$7.95bn). PNG’s debt sits at around 32.8% of its GDP. “[The prime minister] requested the ambassador to inform Beijing on a bid to assist the government of PNG refinance its existing country’s K27bn debt,” said Marape’s office in a statement seen by the Guardian.

“He suggested that both the Bank of PNG and [China’s] People’s Bank will take the lead with the department of treasury in ensuring that consultations are under way,” the statement continued. “It suggest a significant shift in the relationship between Australia and Papua New Guinea and Papua New Guinea and China,” says Matthew Clarke, professor of international development at Deakin University. “In the past Australia would have been the natural country to turn to for this sort of refinancing, but now we see China’s place in the region shift and it becomes potentially a much more dominant player in the donor relationship.”

“The United States, and allies including Japan, Australia and New Zealand, are actively expanding their diplomatic postings in the Pacific to counter China’s influence..”

• Chinese Port Plans Put Pacific Back In Play (R.)

Early in the morning, before sunrise, low tide on the Samoan island of Savai’i reveals the remnants of an old American airstrip, washed away by decades of erosion, cyclones and tsunamis. The World War II site in Asau, which also hosts a 1960s-era concrete wharf in its well-protected natural harbor, is being considered for a new port to be developed by China, according to the Samoan government and the area’s highest ranking chief, Masoe Serota Tufaga. The proposed construction of a facility that could be turned into a military asset in hostile times has worried the United States and its regional allies, which have dominated international influence in the vast waters of the South Pacific since 1945.

Sitting at his coconut and cocoa plantation on the hills above the port site, Tufaga told Reuters he would abide by any government deal for a Chinese-developed port even though he was concerned about Beijing’s growing influence. “The government and China came here to look at it – they offered it,” said 71-year-old Tufaga, who has the final say over land-use agreements affecting Asau. “If China wants to operate this, it’s too hard for us to say to the government, no, we can not allow China here. The people are looking for some jobs. “That’s right – it’s money. It’s money.”

The United States, and allies including Japan, Australia and New Zealand, are actively expanding their diplomatic postings in the Pacific to counter China’s influence, and warning island nations that Beijing-funded projects needed to make financial sense. China is using “predatory economics” to destabilize the Indo-Pacific and the United States is working with its partners to address the region’s pressing security needs, U.S. Defence Secretary Mark Esper said in Sydney on Sunday.

Erdogan bluff. I hope.

• Pentagon Set to Prevent “Unacceptable” Turkish Invasion Of Northern Syria (ZH)

Turkey has for days been poised to unilaterally invade northern Syria over US objections, which Ankara officials say is to establish a 32 kilometer (20 mile) zone inside the war torn country, giving Turkey complete control of a region where the Syrian Kurdish YPG operates (People’s Protection Units). Turkey has long considered the US-backed group, which forms the core of the Syrian Democratic Forces (SDF), to be a terrorist extension of the outlawed PKK. The Pentagon has condemned the impending Turkish unilateral move, with US Defense Secretary Mark Esper telling reporters early Tuesday that it would be unacceptable and thwarted by Washington, though it’s unclear how far the Pentagon would be willing to go.

“What we’re going to do is prevent unilateral incursions that would upset, again, these mutual interests that the United States, Turkey and the SDF share with regard to northern Syria,” Esper said. Crucially, according to ABC News, US officials “have made clear that an invasion is an extremely risky venture that could threaten the safety of U.S. forces working with the SDF…”. On Sunday Turkish President Recep Tayyip Erdogan said that his forces would launch an operation in Syria east of the Euphrates River at an unspecified start date, and noted that the US and Russia had been notified. In ongoing negotiations this summer the US and Turkey have clashed over just such a “safe zone,” given Turkey wants the area completely clear of Kurdish armed groups, which the Pentagon simultaneously backs.

Turkish defense officials have lately threatened their “patience is limited” as the army builds up its forces along the border. The Foreign Ministry on Friday warned, “We won’t let this process be dragged out. If our expectations aren’t met, we are fully capable of taking whatever measures [are needed] to ensure our national security.”

If Mifsud is an FBI asset, there are zero Russians left in the story.

• The Mainstream Media Wants the Mifsud Story to Just Go Away (ET)

John Solomon of The Hill is reporting that an audiotape containing professor Joseph Mifsud’s deposition has been given to both U.S. Attorney John Durham’s investigators and to the Senate Judiciary Committee. “I can report absolutely that the Durham investigators have now obtained an audiotape deposition of Joseph Mifsud, where he describes his work, why he targeted George Papadopoulos, who directed him to do that, what directions he was given, and why he set that entire process of introducing Papadopoulos to Russia in motion in March of 2016, which is really the flashpoint the starting point of this whole Russia collusion narrative,” Solomon told Fox News’ Sean Hannity.

“I can also confirm that the Senate Judiciary Committee has also obtained the same deposition,” he said. Mifsud, who I have written about extensively in previous columns, is the key that turns the lock to the lid of this Pandora’s box that we refer to as “Spygate.” So I’m wondering why Solomon appears to be the only mainstream reporter pursuing this Mifsud story. I suspect it’s because many DNC Media outlets, after having fallen deeply and passionately in love with the Trump-Russia collusion hoax, are reluctant to call attention to something that would be the final nail in its coffin. The last thing the mainstream media wants right now would be for Mifsud to go on the record with both Durham’s investigative team and with Congress to say he was working for the FBI and was only pretending to be a Russian agent.

If Mifsud was an FBI asset sent to entrap Papadopoulos, then there are no real Russian agents anywhere in this entire Trump-Russia collusion story. Ponder what that means for a minute. You can’t save the Russian collusion narrative, if you can’t find any real Russians anywhere in the story. The FBI under James Comey will then be seen as having engaged in an operation to entrap people, and “Russian agents” turn out to be fakes working for the FBI and who were making fake offers of Russian help to the Trump campaign.

But nobody knew a thing.

• Epstein’s Mysterious Manhattan Apartment Building On East 66th Street (BI)

Before his extended stay in New York’s Metropolitan Correctional Center began in July, disgraced sex offender Jeffrey Epstein dwelled in some of the city’s most exclusive real estate, laying his head in a palatial Upper East Side townhouse and conducting his mysterious business out of a landmarked mansion on Madison Avenue. But it hasn’t been all private islands and 7,000-acre ranches for the half-billionaire. For decades Epstein has run some of his operations quietly out of a squat Second Avenue residential building owned by his brother, Mark Epstein, and frequently visited by the former Israeli Prime Minister Ehud Barak. According to property records and court filings, Jeffrey Epstein has long housed girlfriends, associates, employees, and businesses in a handful of units at 301 East 66th St.

There are 200 units at the address, and the majority of them are owned on paper by his brother’s development firm, Ossa Properties. While Ossa nominally owns the units connected to Jeffrey Epstein, the aforementioned records and filings show that Epstein effectively controls them. The postwar white-brick high-rise sits atop a nail salon, a coffee shop, and an Italian restaurant along a traffic-choked stretch of Second Avenue. Topped by a green canopy, the front door opens to a doorman guarding a hallway that leads to a light-filled lobby decorated with two couches and an armchair. Though the building shares a ZIP code with Epstein’s townhouse, its share of the neighborhood east of Park Avenue is less upscale, catering more to families and young professionals than foreign heads of state.