An article on Jim Quinn’s Burning Platform gave me hope. Hope that the madness will be forced to end, though I have no hope this will be an easy process. The article, by “Hardscrabble Farmer”, describes what happens in France now the even stricter Health Pass measures have come into force. Much of the country is grinding to a halt.

We’ll have to wait and see how it plays out, and sure, the French are out for the summer, so empty terraces and restaurants are not that exceptional. The writer is probably not native French, and doesn’t know the intricacies of the health care system which is not entirely state run, there are indeed private clinics, “elite” is a French word after all, but much of what he says is undoubtedly true. And not only in France.

I think most countries that now cajole and threaten their citizens into being vaccinated will find, and have to admit at some point, that they just don’t have the numbers. But first France:

Here in France it has gone to the extreme with the “Health” Pass. Last week on the 21st ALL restaurants, bars, coffee shops, and any leisure activities like sporting events, theaters, cinemas, museums, were closed to anyone without “the pass” and all staff at these places are mandated to get the jab to keep their job. It is now a 6 Month prison sentence if you are caught inside any of these places without the pass (the man who slapped the president in the face got only 3 months prison time).

Business owners will get a fine of 45,000 euros and 1 year prison sentence if they do not comply with the use of “the pass” and force all their employees to get the jab. (If you know France, you can commit murder and have less of a sentence) So the result? All the low paid employees quit, they can make more on welfare here (for now). We can still technically “get take out food” but I just tried last night and every restaurant in our town (that is dine in with take out) has closed their doors due to the lack of staff.

As of last week ALL doctors, nurses and health industry workers have been mandated to get the jab or lose their license, practice, job, business etc. [..] Since the Health care system is state run and funded, it has been run into the ground. All the good doctors left France 5 Years ago, all the hospitals look like they are 3rd world hospitals since there is no money to repair them, half of the equipment doesn’t work and not every hospital is stocked with supplies needed for daily needs (masks, gels, disposable gowns etc).

For 5 years Nurses have been understaffed and doing double the work because the Health care system is nearly bankrupt…. So add to this the mandatory jab. So the result? Well they took to the streets by the millions and now all the hospitals just lost another 50% of staff capacity. My doctor just went into early retirement (a.k.a. he quit) and I have yet to find a replacement.

As of Aug 1st ALL large malls, retail stores and grocery store owners and their staff need to be jabbed and the health pass is required to enter for employees and customers. This would be the equivalent to closing ALL Targets, Walmarts, Costcos, Home Depots, and all major grocery stores [..] to those without “the pass”.

[..] As of Sept 15th All public areas and access will be off limits. No farmers markets, no parks, no national parks, lakes, rivers, beaches, recreation areas, campsites etc. and no gathering over 100 people, no churches, no weddings, etc. As of Oct 1st ALL small vendors such as, delis, pizza trucks, sandwich shops, butchers, bakers, vegetable stands etc.

So as of Oct 1st I will only be able to purchase food by internet and pick up (if allowed). Food shortages, Truckers strike, hospitals and airports shutting down unemployment going through the roof. Its going to be a bumpy ride folks. Is it me or does all this seem a bit extreme for a “pass” that isn’t exactly working?

About those numbers: according to Our World in Data, France has 52% fully vaccinated people, and 68% who’ve had at least a single dose. I don’t believe that for a second, just as I don’t believe any country’s official numbers. Because they are used to push more people into getting vaccines, the idea being that high numbers will make them think it’s time to be with the group.

70% of U.S. adults have had at least one shot of a Covid vaccine, according to data published Monday by the CDC, about a month behind President Joe Biden’s Fourth of July goal.

[..] “We need to have at least 80% of the population vaccinated to truly have some form of herd immunity,” Dr. Paul Offit, a voting member of the Food and Drug Administration’s Vaccines and Related Biological Products Advisory Committee, said in a recent interview. “This is a fairly contagious virus.”

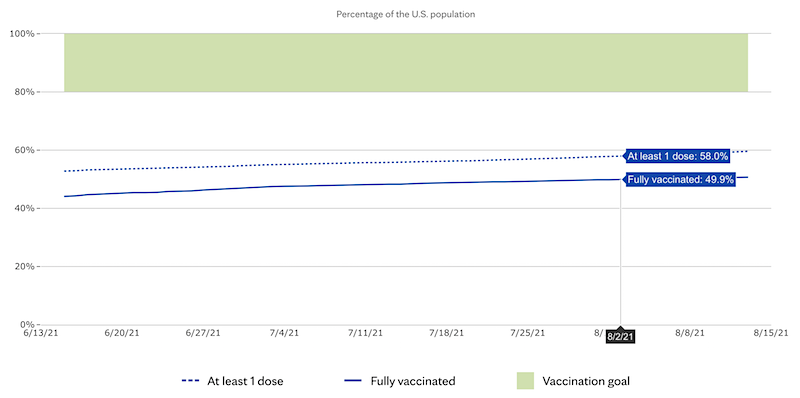

But also on August 2, the Mayo Clinic had the US at 58% single dose vaccinated, which Our World in Data appears to confirm, and 49.9% fully vaccinated. But that doesn’t look too great a whole month after Biden’s July 4 70% goal ran out, dies it?

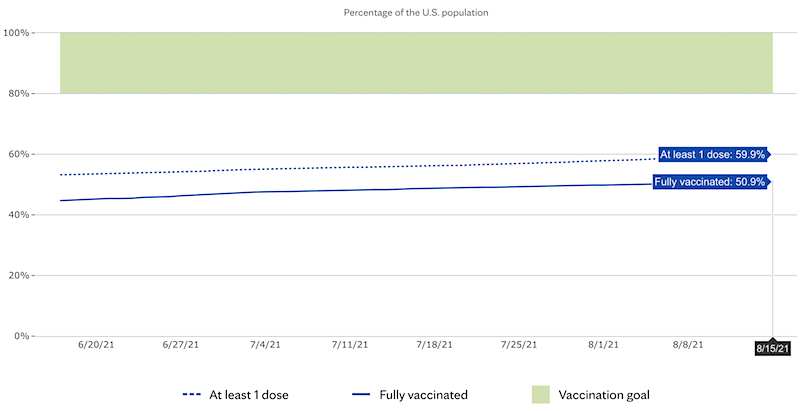

Two weeks later, on August 15, the number of fully vaccinated is up by just 1%, at 50.9%.

At that rate it will take a while. Or rather, that rate means they might as well give up. Because it’s an uphill battle in which the low hanging fruit has been picked. Vaccination centers are closing, demand is drying up. Just getting to 70% would be a miracle. But then the “experts” say that is not enough either, you need 80%. Forget about it. You will kill your economy first. Even at 70%, you have almost a third of your population not working, not shopping, living outside of the economy.

Bill H.R. 4980, posted on Congress.gov., says:

To direct the Secretary of Homeland Security to ensure that any individual traveling on a flight that departs from or arrives to an airport inside the United States or a territory of the United States is fully vaccinated against COVID-19, and for other purposes.

This means half of Americans won’t be allowed to fly. Happy Americans! Happy airlines! And of course these measures will subsequently at some point be applied to all the fields they already are in France. Hospitality, stores, hospitals, etc. Which will lose a lot of their staff. and a huge chunk of their customers. As the fully vaccinated go up by 1% per two weeks.

Oh, and wait, I haven’t even mentioned the 3rd, 4th and so on, booster shots. Think everyone will get them all? If these people have their way, we’re going to live in a world where one week you can dine out and fly, but the next you first need to get the umpteenth shot to do it. And you may get real sick if you don’t to boot.

In Greece, the government last week announced that 65.1% of the total population have one dose, and 61.1% “of adults have completed their inoculation.” That would mean they are way ahead of the US, even though they started much later, had supply problems and so on. No, they’re lying too, all governments massage the numbers.

With the US at 50%, I’d say Greece is at 30%, 40% max. And resistance here is high, so the numbers will only climb very slowly. But of course, threats. A friend who works in a restaurant told me today that they’re threatening to fire him in October. He’s trying, with 5 others at the same place, to hire a lawyer to take their case, but the lawyers have so many of these cases that their fees have skyrocketed.

They base their claim on the idea that the Greek parliament have said you can’t fire people for not taking the vaccine. I simply don’t know enough about that. But it’s clear which way the wind is blowing. Here and in so many other places. Some people are docile, some governments have better propaganda, but it’s still all moving in the same direction.

What may break this downhill, and dangerous, trend, is reports about severe adverse effects, such as antibody-dependent enhancement, breaking through the near perfect wall of silence built around “alternative” views and other things that don’t fit the narrative. You can’t fool all of the people all of the time. But you can obviously try. And you can try and set one half of your population against the other. That’s a lovely idea too. The Land of the Free, but only for those who follow orders.

Note: I know, I know, they’re all betting on boosting their numbers by inoculating every new born child, even the unborn. Problem is, people tend to love their children even more than themselves. And no-one can assure them it’s safe to jab their kids, even if they claim it: there’s no evidence of it, none.

We try to run the Automatic Earth on donations. Since ad revenue has collapsed, you are now not just a reader, but an integral part of the process that builds this site. Thank you for your support.

Support the Automatic Earth in virustime. Click at the top of the sidebars to donate with Paypal and Patreon.

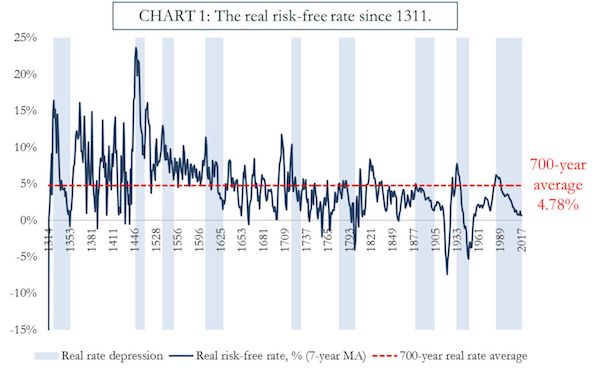

Forget secular stagnation. One historian says the world is actually in its ninth “real rate depression” and 700 years of data show that – when it comes – the turnaround could be sudden. In research published on the Bank of England’s staff blog, Harvard University’s Paul Schmelzing says most work pointing to a period of permanently lower equilibrium real interest rates is too short term. Instead, he tracked the risk-free rate since 1311 by identifying the dominant asset of each period – starting with sovereign rates in the Italian city states in the 14th and 15th centuries and moving to long-term rates in Spain, then the Province of Holland, the U.K., Germany, and finally the U.S. Real rates, or the benchmark interest rates minus inflation, have averaged 4.78% while the 200-year real-rate average is 2.6%.

That makes the current market environment “severely depressed,” Schmelzing wrote. However, it’s simply following a five-century downward trend, in which there have been nine periods of secular decline followed by reversals. The current period – since the 1980s – is the second-longest recorded and its closest historical analogy is the global “Long Depression” of the 1880s and 1890s which saw low productivity growth, deflationary price dynamics, and the rise of global populism and protectionism. This spell seems to have ended without a push from policy makers. That could be good news for those struggling to find a fix for the current low-rate environment. “There is strong evidence suggesting that the last ‘secular stagnation cycle’ started fading relatively autonomously after just over two decades following the key financial shock, not requiring the aid of decisive fiscal or monetary stimulus.”

Saudi Arabian banks have frozen more than 1,200 accounts belonging to individuals and companies in the kingdom as part of the government’s anti-corruption purge, bankers and lawyers said on Tuesday. They added that the number is continuing to rise. Dozens of royal family members, officials and business executives have been detained in the crackdown and are facing allegations of money laundering, bribery, extorting officials and taking advantage of public office for personal gain. Since Sunday, the central bank has been expanding the list of accounts it is requiring lenders to freeze on an almost hourly basis, one regional banker said, declining to be named because he was not authorised to speak to media.

The banker did not name the companies affected but said they included listed and unlisted firms across many sectors. He added that if the freezes stayed in place for long, they could start to hurt day-to-day business activities such as paying staff and creditors or making other transactions. A second banker said, however, that most of the frozen accounts belonged to individuals rather than companies, and that banks were being allowed by the regulator to continue to fund existing commitments. Among top business executives detained in the probe are billionaire Prince Alwaleed bin Talal, chairman of investment firm Kingdom Holding; Nasser bin Aqeel al-Tayyar, founder of Al Tayyar Travel; and Amr al-Dabbagh, chairman of builder Red Sea International.

The stocks of all three companies, which have issued statements saying they continue to operate as normal, plunged between 9 and 10% on Tuesday. One of the bankers speaking to Reuters said the central bank had met with some foreign banks this week to reassure them that the freezing of accounts targeted individuals, and that firms linked to those people would not be damaged.

The Saudi government is aiming to confiscate cash and other assets worth as much as $800 billion in its broadening crackdown on alleged corruption among the kingdom’s elite, according to people familiar with the matter. Several prominent businessmen are among those who have been arrested in the days since Saudi authorities launched the crackdown on Saturday, by detaining more than 60 princes, officials and other prominent Saudis, according to those people and others. The country’s central bank, the Saudi Arabian Monetary Authority, said late Tuesday that it has frozen the bank accounts of “persons of interest” and said the move is “in response to the Attorney General’s request pending the legal cases against them.”

The purge is the most extensive of the kingdom’s elite in recent history. Crown Prince Mohammed bin Salman, the son of King Salman, was named heir to the throne in June and has moved to consolidate power. He has said that tackling corruption at the highest level is necessary to overhaul what has long been an oil-dependent economy. The crackdown could also help replenish state coffers. The government has said that assets accumulated through corruption will become state property, and people familiar with the matter say the government estimates the value of assets it can reclaim at up to 3 trillion Saudi riyal, or $800 billion.

Early this morning, Israeli Channel 10 news published a leaked diplomatic cable which had been sent to all Israeli ambassadors throughout the world concerning the chaotic events that unfolded over the weekend in Lebanon and Saudi Arabia, which began with Lebanese Prime Minister Saad Hariri’s unexpected resignation after he was summoned to Riyadh by his Saudi-backers, and led to the Saudis announcing that Lebanon had “declared war” against the kingdom. The classified embassy cable, written in Hebrew, constitutes the first formal evidence proving that the Saudis and Israelis are deliberately coordinating to escalate the situation in the Middle East. The explosive classified Israeli cable reveals the following:

• On Sunday, just after Lebanese PM Hariri’s shocking resignation, Israel sent a cable to all of its embassies with the request that its diplomats do everything possible to ramp up diplomatic pressure against Hezbollah and Iran.

• The cable urged support for Saudi Arabia’s war against Iran-backed Houthis in Yemen.

• The cable stressed that Iran was engaged in “regional subversion”.

• Israeli diplomats were urged to appeal to the “highest officials” within their host countries to attempt to expel Hezbollah from Lebanese government and politics.

As is already well-known, the Saudi and Israeli common cause against perceived Iranian influence and expansion in places like Syria, Lebanon and Iraq of late has led the historic bitter enemies down a pragmatic path of unspoken cooperation as both seem to have placed the break up of the so-called “Shia crescent” as their primary policy goal in the region. For Israel, Hezbollah has long been its greatest foe, which Israeli leaders see as an extension of Iran’s territorial presence right up against the Jewish state’s northern border.

“Having failed to liberate the Syrians, Saudi, the West, its Sunni Gulf allies and Israel will now see if they can succeed in blocking any Iranian gas ambitions by liberating the Lebanese from their own government.”

The Great Gas War has already two distinct fronts: The now relatively quiet Northern Front in Ukraine and the Southern Front in Syria in which the Western empire has been losing. It looks to me that Lebanon is being targeted as the next front, where the West hopes its loses might be recouped. Yesterday, November 6th, Reuters reported, “Saudi Arabia said on Monday that Lebanon had declared war against it because of attacks against the Kingdom by the Lebanese Shi‘ite group Hezbollah.” This comes after Israel, Saudi’s long time though largely un-offical best friend in the region, has been very publicly preparing to renew its own war with Lebanon – or more accurately with Hezbollah. As the American news journal Newsweek put it recently, “ISRAEL PREPARES FOR ANOTHER WAR WITH HEZBOLLAH AS IDF PRACTICES LEBANON INVASION.”

Why now and why Lebanon? Well the rulers of Saudi, a Sunni dominated country, will tell us that it is because Hezbollah is a Shia terrorist organisation. “Hezbollah” literally means the “Party of Allah” or “Party of God”. Saudi Gulf affairs minister Thamer al-Sabhan yesterday pointedly referred to Hezbollah as, “the Lebanese Party of the Devil”. Saudi is not alone of course, Hezbollah has also been listed as a terrorist organisation by America, Israel, the Arab League, the UK and the EU. It is also, however, part of the popular government of Lebanon having seats in its parliament. I suggest, however, a powerful reason that a new war with Hezbollah may be in the offing is because Lebanon is the next link in any gas pipeline that could potentially bring Iranian Gas to Europe.

That was the reason the West decided to “liberate” the Syrian people and it will be why they decide to enforce the same salvation upon the people of Lebanon. Having failed to liberate the Syrians, Saudi, the West, its Sunni Gulf allies and Israel will now see if they can succeed in blocking any Iranian gas ambitions by liberating the Lebanese from their own government. I would not be surprised to hear quite soon from opposition groups vocally denouncing the government or at least Hezbollah. I expect spokes people from those groups to suddenly get a global platform along-side American and regional supporters such as Saudi.

The number of British-made bombs and missiles sold to Saudi Arabia since the start of its bloody campaign in Yemen has risen by almost 500%, The Independent can reveal. More than £4.6bn of arms were sold in the first two years of bombings, with the Government grant increasing numbers of export licences despite mounting evidence of war crimes and massacres at hospitals, schools and weddings. The United Nations says air strikes by the Saudi-led coalition are the main cause of almost 5,295 civilian deaths and 8,873 casualties confirmed so far, warning that the real figure is “likely to be far higher”. It has condemned the “entirely man-made catastrophe” leaving millions more on the brink of famine and sparking the world’s worst cholera epidemic, while blacklisting Saudi Arabia for killing and maiming children.

There is also fresh concern over the Kingdom’s attempt to shut all air, land and sea ports into Yemen, which it said was to stop the flow of weapons but will also halt aid imports. British-made bombs have been found at the scene of bombings deemed to violate international law but the UK has continued its political and material support for Riyadh’s campaign. Figures from the Department for International Trade (DIT) show that in the two years leading up to the Yemen war, £33m of ML4 licences covering bombs, missiles and countermeasures were approved. But in the two years since the start of Saudi bombing in March 2015, the figure increased by 457% to £1.9bn, according to calculations by Campaign Against the Arms Trade (CAAT). Licences covering aircraft including Eurofighter jets have also risen by 70% to £2.6bn in the same period.

Prime Minister Theresa May is weighing whether to fire a member of her cabinet only seven days after her defense secretary quit in a sexual harassment scandal, as the U.K. government faces fresh turmoil in the midst of Brexit talks. May is likely to dismiss her International Development Secretary Priti Patel in a row over a succession of unauthorized meetings she held with Israeli officials behind the prime minister’s back, according to reports from the BBC and The Sun Tuesday, which the U.K. government declined to deny. The premier has not yet had the chance to speak to Patel – who is on an official trip to Africa – about the latest revelations. A conversation would be expected before a decision is made about the minister’s future. If she is forced out, Patel will be the second minister to depart May’s cabinet in one week, after Michael Fallon resigned from the defense ministry amid allegations over his past behavior toward women.

For some, May’s latest headache is yet another demonstration of her weakness, which draws repeated questions over how her government can last long enough to see Brexit to the finish line. If more dominoes drop – in the shape of senior ministers – the last one to fall could ultimately be the prime minister herself. “The destabilizing effect on an already weak administration has prompted another burst of speculation that May could soon be forced to resign,” Mujtaba Rahman of Eurasia Group said in a note to clients. He thought one likely scenario is for May to be toppled if she fails to get a grip on the latest crisis and is ousted because her MPs judge that the government cannot go on like this – and is incapable of recovering the authority a prime minister needs.

Make no mistake, last week’s increase in interest rates was a big deal. Painful as it might be for a good share of the population, the real point is that the Bank is signalling the end of a particular phase of monetary policy. Since 2010 the counterpart to self-defeating austerity policies has been expansionary monetary policies. These have inflated assets – enriching the already-rich, while failing to stimulate wider economic recovery. Yesterday the Bank of England’s Monetary Policy Committee signalled an end of this dangerous game. But this technocratic realignment makes no difference to the fact that ‘the Guardians of the nation’s finances’ – Bank and Treasury economists – have failed absolutely to revive the economy.

You need look no further than the (ongoing) decline in real wages, to continuing low levels of private investment, and to the dangers of rising household debt. A small interest rate rise is hardly likely to improve these conditions. Bank and Treasury economists (aided and abetted by the OBR) are guilty of defeatism. They argue that despite their powers, THERE IS NOTHING TO BE DONE. It is assumed that somehow ‘the invisible hand’ or ‘the markets’ will, without intervention by the authorities, correct the weakness, insecurity and failures of the British economy. The prolonged and painfully weak recovery is regularly blamed on something defined as “productivity”. By shifting responsibility for economic failure on to productivity, the Bank, Treasury and OBR economists are saying that somehow economic failure is inherent to the economy – to businesses and especially to workers.

“Nothing to do with us, guv” they mutter. They add that the situation has been exacerbated by the vote to leave the EU. This is a handy way of denying that the ongoing economic failure of the British economy (and the Brexit vote) can be explained by austerity policies, and the failures of the financial system. By taking this approach, economists at the Bank have – conveniently – set the scene for endorsing further inaction by the Chancellor later this month. Yesterday the Governor of the Bank was flanked by Ben Broadbent and Dave Ramsden. Ben Broadbent, as a Goldman Sachs economist, was among the earliest to call for austerity policies. Dave Ramsden (who did not vote for the rate rise) implemented these policies as top economist at the Treasury.

But both Broadbent and Ramsden were senior figures in economic policy-making throughout the debt inflation that preceded the crisis, and (we presume) supporters of financial globalisation. It is obvious to anyone with an ounce of common sense that austerity policies have hurt the most vulnerable, and damaged Britain’s economic potential, by forcing a brutal adjustment to lower quality and lower paid work. Labour has been forced to bear the brunt of the Global Financial Crisis. The weakness in productivity is just the outcome of these policies, not the cause.

The German economy is at risk of overheating, according to a leaked advisory council report that follows pressure from the Bundesbank for a swifter end to the ECB’s expansive monetary policy. In their annual report, seen by Handelsblatt newspaper, the five “wise men” who advise the German government on economic policy said the economy, which they expected to expand strongly this year and next, was moving gradually into a “boom phase”. “There are clear signs that economic capacity is over-utilised,” read the report, which is due to be published on Wednesday. Germans have been among the foremost critics of the ECB’s bond-buying program, which was introduced three years ago to depress borrowing costs and reignite growth in the euro zone’s heavily indebted southern periphery.

The wise men expected Germany’s economy to expand by 2% this year and by 2.2% in 2018, Handelsblatt said. With unemployment at its lowest level since the early 1990s, Germany’s circumstances are very different from Italy’s or Spain‘s, straining the ECB’s ‘one-size-fits-all’ monetary policy. ECB President Mario Draghi last month announced a halving n the size of its 2 trillion euro bond-buying program, but this is far from the return to conventional monetary policy many Germans, including Bundesbank president Jens Weidmann, demand. Without an intervention to cool the economy, Germany’s hawks fear the buoyant economy could tip over into an inflationary cycle. Last week, a senior official from Chancellor Angela Merkel’s conservatives warned that German savers would not tolerate continued low interest rates for much longer.

“The phrase ‘Set a thief to catch a thief’ is common parlance,” says Professor Atul K. Shah. “‘Set a global brand of professional accountants to rob society and pilfer its taxes, bleeding governments’, is not, but it should be.’ Professor Bill Black says internal controls are absolutely critical in reducing fraud by insiders in particular, but not just insiders, as the Paradise Papers have repeatedly demonstrated. Emile Woolf says there is no way to remove control fraud and dodgy accounting practices from the economy without first prosecuting the culprits. “The devils that committed this criminal negligence – with the exception of the Royal Bank of Scotland (RBS) – have never been fined or prosecuted” he said. “What you can then do is create a ring fenced fund inside those institutions, earmarked to save them from going under. But the company has to recognise it has to be paid back.

“RBS is incapable of paying back the billions of fines it still owes for misconduct,” he says. “Where does that money come from and where does it go? Without the fines RBS would have made £100 million profit this year, but because of the reserve for fines in the USA and UK, all those fines are far too great to allow for payment of a dividend.” Of course calculating a true profit figure is difficult when a significant portion of that profit is fraudulent, because it doesn’t take into account the result of the inequities of ten years ago. “The worrying thing for all of us is if it happens again,” he says. “My hope is that three years from now, banks will be forced to recognise their loans that will never be repaid. But my worry is that this is going to be after the next financial crisis, because it’s happening again. There is no redeeming features in the present. The only difference is the next crisis is going to be bigger.”

Joel Benjamin told Renegade Inc that accounting is as much about *what* you count or don’t count as it is *how* you count it. “This is evidenced through the practice of ‘base erosion and profit shifting’ – shifting profits to offshore low or no tax jurisdictions, ” he said. In the space of 50 years, Britain’s economy has transformed from an industrial power house, to that of a finance-led extractive parasite, where the cash starved productive economy receives less than 10% of bank credit. “Until the Big Four accountancy firms are accurately viewed as enablers of corporate offshore dealing, regulatory arbitrage and ardent defenders of the neoliberal order, not the ‘reputable’ objective independent arbiters of the public interest as they claim, society will continue to be taken for a ride, and public services and social cohesion will continue their long decline,” he said.

Mitchell tried to tell me that governments do not spend by ‘printing money’ but rather just adjust bank accounts with numbers. But I know as anyone in the street knows that they just want to print more and more. That is at the core of MMT – they want the government to go on a spending spree and just ignore the inflationary consequences. They hide that by saying that “public spending cannot be unlimited and must be commensurate to the capacity of the economy” which is just a smokescreen that I can see through. And everybody will see through it. It is code for spend like a drunken’ sailor – throw money at lazy people who cannot be bothered finding a job. Throw money at public schools that teach socialist doctrines – you know about inequality and stuff like that.

Throw money at public hospitals so that people can receive unlimited health care without having to pay for it – that is the quickest way to encourage waste and bad behaviour. People know that they can just get sick and no matter what their income is they will get some care. Where is the incentive to stay healthy in that sort of system. The article also shows how stupid Mitchell is when it says he: “… debunks the idea that governments borrow money from international markets and with it the notion that they are hostage to the market.” Well where the hell else do they get the cash from? Does he really think we are that stupid? How come China has all those US government debt bonds or whatever they are called and the US government is spending the Chinese cash? How does he explain that obvious point?

Well he tried to claim the Chinese doesn’t issue US dollars and that only the US government issues US dollars so that it cannot possibly be funded by the Chinese. I don’t buy that, not that I understood anything he said about this – all this talk about trade surpluses accumulating financial claims in the currency that the deficit country issues, and then allowing the surplus nation to use those claims (say, US dollars in the first instance) to purchase US dollar financial assets etc ad nauseum. As if that tells us anything. How come the Chinese can loan the US government money that is what I want to know? Mitchell told the journalist that Jeremy Corbyn should not worry about international capital markets because Britain could impose capital controls if it wanted to. That gets to the nub of my worries – socialist governments stealing hard-earned cash from investors who actually have some get up and go.

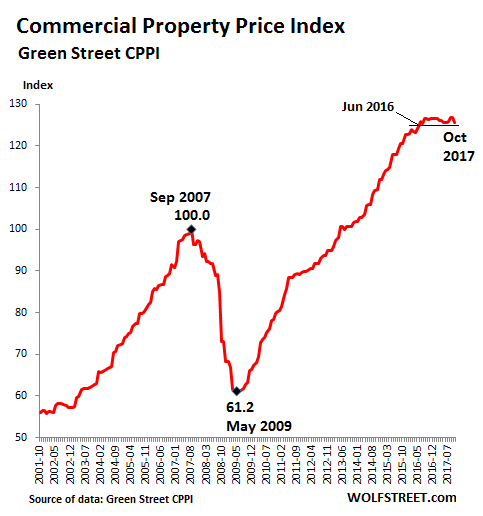

Commercial real estate prices soared relentlessly for years after the Financial Crisis, to such a degree that the Fed has been publicly fretting about them. Why? Because US financial institutions hold nearly $4 trillion of commercial real estate loans. But the boom in most CRE sectors is over. The Green Street Property Price Index – which measures values across five major property sectors – had soared 107% from May 2009 to the plateau that began late last year, and 27% from the peak of the totally crazy prior bubble that ended with such spectacular fireworks. But it has now turned around, dragged down by a plunge in prices for retail space. The CPPI by Green Street Advisors dropped 1.1% in October from September. In terms of points, the 1.4-point decline was the largest monthly decline since March 2009. The index is now below where it had been in June 2016:

This phenomenal bubble, as depicted by the chart above, has even worried the Fed because US financial institutions hold nearly $4 trillion of CRE loans, according to Boston Fed governor Eric Rosengren earlier this year. Of them, $1.2 trillion are held by smaller banks (less than $50 billion in assets). These smaller banks tends to have a loan book that is heavily concentrated on CRE loans, and these banks are less able to withstand shocks to collateral values. Rosengren found that among the root causes of the Financial Crisis “was a significant decline in collateral values of residential and commercial real estate.” But the CRE bubble isn’t unraveling as gently as the chart suggests. Some sectors are still surging, while others are plunging. According to the report, the index, which captures the prices at which CRE transactions are currently being negotiated and contracted, “was pushed down by falling mall valuations.”

Catalan secessionist parties on Tuesday failed to agree on a united ticket to contest a December snap regional election, making it more difficult to rule the region after the vote and press ahead with their collective bid to split from Spain. Catalonia’s secessionist push has plunged Spain into its worst political crisis in four decades, triggered a business exodus, forced Madrid to cut its economic forecast and reopened old wounds from Spain’s civil war in the 1930s. Pro-independence groups have called for a general strike in the restive region on Wednesday. Catalan political parties had until midnight on Tuesday to register coalitions ahead of the Dec. 21 vote, but the two main forces which formed an alliance to rule the region for the last two years did not manage to agree on a new pact in time.

While they could still find an agreement after the vote, political analysts say the lack of a deal on a joint campaign may also trigger a leadership fight at the top of the movement. This is because center-right PdeCat (Catalan Democratic Party) of sacked Catalan president Carles Puigdemont is expected to be overtaken by leftist Esquerra Republicana de Catalunya (ERC) of former regional vice president Oriol Junqueras. Puigdemont and Junqueras are the two main leaders behind the current secession bid that last month led to a unilateral declaration of independence which Spain thwarted by imposing direct rule on the region. Junqueras is currently in custody pending a potential trial on charges of sedition, rebellion and misuse of public funds. Puigdemont, who faces the same charges, is currently in self-imposed exile in Belgium and has said he would oppose extradition.

An opinion poll released on Sunday by Barcelona-based newspaper La Vanguardia showed Junqueras’ ERC could garner between 45 and 46 seats in the 135-strong regional assembly while Puigdemont’s PdeCat would win between 14 and 15 seats. In order to reach the 68-seat threshold for a majority, they would then have to form a parliamentary alliance with anti-capitalist CUP, which is expected to get seven or eight seats. Such an alliance previously existed between 2015 and 2017.

More than 300,000 people in Britain – equivalent to one in every 200 – are officially recorded as homeless or living in inadequate homes, according to figures released by the charity Shelter. Using official government data and freedom of information returns from local authorities, it estimates that 307,000 people are sleeping rough, or accommodated in temporary housing, bed and breakfast rooms, or hostels – an increase of 13,000 over the past year. Shelter said the figures were an underestimate as they did not include people trapped in so-called “hidden homelessness”, who have nowhere to live but are not recorded as needing housing assistance, and end up “sofa surfing”. London, where one in every 59 people are homeless, remains Britain’s homelessness centre. Of the top 50 local authority homelessness “hotspots”, 18 were in Greater London, with Newham, where one in 27 residents are homeless, worst hit.

However, while London’s homeless rates have remained largely stable over the past year, the figures show the problem is becoming worse in leafier commuter areas bordering the capital, such as Broxbourne, Luton, and Chelmsford. Big regional cities have also seen substantial year-on-year increases in the rate of homelessness. In Manchester, one in 154 people are homeless (compared with one in 266 in 2016); in Birmingham one in 88 are homeless (119); in Bristol one in 170 are affected (199). Polly Neate, chief executive of Shelter, said: “It’s shocking to think that today, more than 300,000 people in Britain are waking up homeless. Some will have spent the night shivering on a cold pavement, others crammed into a dingy hostel room with their children. And what is worse, many are simply unaccounted for.

It’s done. Bannon 1 – 0 Kushner. President Donald Trump announced the U.S. would withdraw from the Paris climate pact and that he will seek to renegotiate the international agreement in a way that treats American workers better. “So we are getting out, but we will start to negotiate and we will see if we can make a deal, and if we can, that’s great. And if we can’t, that’s fine,” Trump said Thursday, citing terms that he says benefit China’s economy at the expense of the U.S. “In order to fulfill my solemn duty to protect America and its citizens, the United States will withdraw from the Paris climate accord, but begin negotiations to re-enter either the Paris accord or really an entirely new transaction on terms that are fair to the United States, its businesses” and its taxpayers, Trump said.

As Bloomberg reports, Trump’s announcement, delivered to cabinet members, supporters and conservative activists in the White House Rose Garden, spurns pleas from corporate executives, world leaders and even Pope Francis who warned the move imperils a global fight against climate change. As we noted earlier, we should prepare for the establishment to begin its mourning and fearmongering of the disaster about to befall the world. Pulling out means the U.S. joins Russia, Iran, North Korea and a string of Third World countries in not putting the agreement into action. Just two countries are not in the deal at all – one of them war-torn Syria, the other Nicaragua. The Hill notes that many Republicans on Capitol Hill are likely to support pulling out of the Paris deal – 20 leading Senate Republicans, including Majority Leader Mitch McConnell (R-Ky.) asked Trump to do just that last week.

Withdrawing from Paris would greatly please conservative groups, which have orchestrated an all-out push in opposition to the pact. “Without any impact on global temperatures, Paris is the open door for egregious regulation, cronyism, and government spending that would be disastrous for the American economy as it is proving to be for those in Europe,” said Nick Loris, a fellow at the Heritage Foundation. “It is time for the U.S. to say ‘au revoir’ to the Paris agreement,” he said.

And use to NOT have their leader appear on TV. I’m thinking a decision by the new (American?!) campaign team installed after the Snap announcement. “Stay away from the camera, it can only do you harm!” Boris PM by July 1?

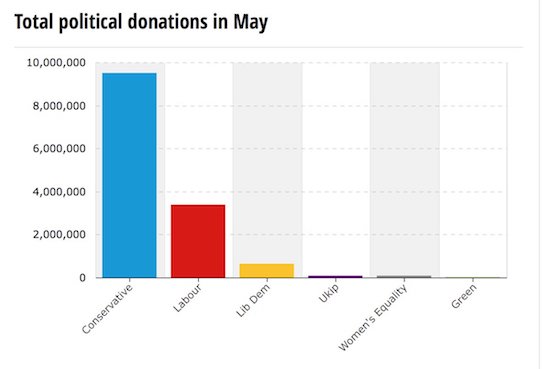

The Conservatives raised more than 10 times as much as Labour last week, partly thanks to a donation of over £1m from the theatre producer behind The Book of Mormon and The Phantom of the Opera. John Gore, whose company has produced a string of hit musicals, gave £1.05m as part of the £3.77m received by the Conservatives in the third week of the election campaign. In the same time, Labour received only £331,499. The Electoral Commission only publishes details of donations over £7,500, so the smaller donors who make up most of Labour’s fundraising are not identified. Almost all Labour’s larger donations came from unions, including £159,500 from Unite. The new figures show the Conservatives have received £15.2m since the start of 2017, while Labour has received £8.1m.

The large donations came as the poll lead held by the Conservatives and Theresa May appeared to fall following controversies around her social care policy. In the week starting 17 May, the Liberal Democrats received £310,500, of which £230,000 came from the Joseph Rowntree Reform Trust and £25,000 came from the former BBC director general Greg Dyke. The Women’s Equality party received £71,552, with Edwina Snow, the Duke of Westminster’s sister who is married to the historian Dan Snow, giving £50,000. Ukip’s donations fell dramatically to £16,300 from £35,000 the previous week. Political parties can spend £30,000 for every seat they contest during the regulated period. There are 650 seats around the country, meaning that parties can spend up to £19.5m during the regulated period in the run-up to the election.

Befitting a surprise election, the manifestos from the main parties contained surprises. Labour is shaking off decades of shyness about nationalisation and tax increases for the rich and for the first time in decades has a policy agenda that is not Tory-lite. The Conservatives, meanwhile, say they are rejecting “the cult of selfish individualism” and “belief in untrammelled free markets”, while adopting the quasi-Marxist idea of an energy price cap. Despite these significant shifts, myths about the economy refuse to go away and hamper a more productive debate. They concern how the government manages public finances – “tax and spend”, if you will.

The first is that there is an inherent virtue in balancing the books. Conservatives still cling to the idea of eliminating the budget deficit, even if it is with a 10-year delay (2025, as opposed to George Osborne’s original goal of 2015). The budget-balancing myth is so powerful that Labour feels it has to cost its new spending pledges down to the last penny, lest it be accused of fiscal irresponsibility. However, as Keynes and his followers told us, whether a balanced budget is a good or a bad thing depends on the circumstances. In an overheating economy, deficit spending would be a serious folly. However, in today’s UK economy, whose underlying stagnation has been masked only by the release of excess liquidity on an oceanic scale, some deficit spending may be good – necessary, even.

The second myth is that the UK welfare state is especially large. Conservatives believe that it is bloated out of all proportion and needs to be drastically cut. Even the Labour party partly buys into this idea. Its extra spending pledge on this front is presented as an attempt to reverse the worst of the Tory cuts, rather than as an attempt to expand provision to rebuild the foundation for a decent society. The reality is the UK welfare state is not large at all. As of 2016, the British welfare state (measured by public social spending) was, at 21.5% of GDP, barely three-quarters of welfare spending in comparably rich countries in Europe – France’s is 31.5% and Denmark’s is 28.7%, for example. The UK welfare state is barely larger than the OECD average (21%), which includes a dozen or so countries such as Mexico, Chile, Turkey and Estonia, which are much poorer and/or have less need for public welfare provision. They have younger populations and stronger extended family networks.

The third myth is that welfare spending is consumption – that it is a drain on the nation’s productive resources and thus has to be minimised. This myth is what Conservative supporters subscribe to when they say that, despite their negative impact, we have to accept cuts in such things as disability benefit, unemployment benefit, child care and free school meals, because we “can’t afford them”. This myth even tints, although doesn’t define, Labour’s view on the welfare state. For example, Labour argues for an expansion of welfare spending, but promises to finance it with current revenue, thereby implicitly admitting that the money that goes into it is consumption that does not add to future output.

The banker at the other end of the phone line was furious, recalled Shanghai lawyer Wang Chaoyu. A pile of steel pledged as collateral for a loan of almost $3 million from his bank, China CITIC, had vanished from a warehouse on the outskirts of the city. Just several months earlier, in mid-2013, Wang and the banker had visited the warehouse and verified that the steel was there. “The first time I went, I saw the steel,” recalled Wang, an attorney at Beijing DHH Law Firm, which represents the Shanghai branch of CITIC. “Afterwards, the banker got in contact with me and said, ‘The pledged assets are no longer there.’” The trouble had begun in 2012, after CITIC loaned the money to Shanghai Hanning Iron and Steel, a privately held steel trader. Hanning failed to meet payments, according to a mediation agreement reviewed by Reuters, and CITIC took ownership of the steel.

It was when CITIC moved to retrieve the collateral that the banker visited the warehouse and discovered that the 291-tonne pile of steel was no longer there, Wang said. The bank is still in court trying to recoup its losses. The missing collateral is a setback for CITIC. But it is indicative of a much wider problem that could endanger the health of China’s financial system – fraudulent or “ghost” collateral. When bank auditors in China go looking, they too often find that collateral recorded on the books simply isn’t there. In some cases, collateral that has been pledged simply doesn’t exist. In others, it disappears as borrowers in financial distress sell the assets. There are also instances in which the same collateral has been pledged to multiple lenders. One lawyer said he discovered that the same pile of steel was used to secure loans from 10 different lenders.

With the mainland facing its slowest growth in over a quarter of a century, defaults are mounting as borrowers struggle to repay their loans. The danger of fraudulent collateral in this situation, say economists, is that it exacerbates the problem of bad debt for China’s banks, increasing the risk of financial turmoil. As growth slows, lenders can expect more nasty surprises, said Xin Qingquan at Chongqing University. More instances of fake collateral will arise, he said. [..] There are no official statistics or estimates of the problem. But fraudulent collateral is “a huge issue,” said Violet Ho, co-head of Greater China Investigations and Disputes Practice at Kroll, which conducts corporate investigations on the mainland. “Often you also see that the paperwork around collateral may be dodgy, and the bank loan officer knows, the intermediary knows, and the goods owner knows – so it’s essentially a Ponzi scheme.”

[..]Bad loans are mounting fast. Officially, just 1.74% of commercial bank loans were classified as non-performing at the end of March. But some analysts say lenders often mask the true level of bad debt and so the figure is likely much higher. Fitch Ratings said in a report last September that it had estimated non-performing loans in China’s financial system could be as high as 15% to 21%. This in a banking sector that has undergone a massive credit expansion. The value of outstanding bank loans ballooned to $17.2 trillion at the end of April from $5.8 trillion at the end of 2009, according to data from China’s central bank. In September last year, the Bank for International Settlements warned that excessive credit growth in China meant there was a growing risk of a banking crisis in the next three years.

The Bank of Japan’s assets apparently exceeded 500 trillion yen ($4.49 trillion) as of the end of May, growing to rival the country’s economy as the central bank continues its debt purchases under an ultraeasy monetary policy. The bank’s total assets stood at 498.15 trillion yen as of May 20. By the time the month ended Wednesday, its holdings of Japanese government bonds had increased by another 2.24 trillion yen. Assuming that the BOJ had not significantly reduced its non-JGB assets, its balance sheet almost certainly crossed over the 500 trillion yen mark into uncharted territory. The BOJ’s balance sheet began expanding at a rapid clip after Governor Haruhiko Kuroda launched unprecedented quantitative and qualitative easing in April 2013. At around 93%, the scale of the Japanese central bank’s assets in proportion to GDP has no close match. Latest data shows that the U.S. Fed held roughly $4.5 trillion in assets, which is equivalent to 23% of the country’s GDP.

The ECB’s balance sheet, at about €4.2 trillion ($4.71 trillion) is larger than the BOJ’s, but it still sits at around 28% of the eurozone GDP. The BOJ in September shifted its policy focus from QE to controlling the yield curve, but the bank is still snapping up JGBs to keep long-term rates at around zero. The central bank has stood firm on its pledge to continue expanding its balance sheet to boost currency supply until Japan’s consumer price inflation is steadily above 2%. This suggests that the BOJ’s balance sheet will continue expanding past the 500 trillion yen mark. This prospect makes some financial experts uneasy. Once the inflation target is finally met, and the BOJ starts raising interest rates, the bank will have to pay more in interest to financial institutions’ reserve deposits than it will earn from its low-yielding JGB holdings.

Between 20% and 25% of the nation’s shopping malls will close in the next five years, according to a new report from Credit Suisse that predicts e-commerce will continue to pull shoppers away from bricks-and-mortar retailers. For many, the Wall Street firm’s finding may come as no surprise. Long-standing retailers are dying off as shoppers’ habits shift online. Credit Suisse expects apparel sales to represent 35% of all e-commerce by 2030, up from 17% today. Traditional mall anchors, such as Macy’s, J.C. Penney and Sears, have announced numerous store closings in recent months. Clothiers including American Apparel and BCBG Max Azria have filed for bankruptcy. Bebe has closed all of its stores.

The report estimates that around 8,640 stores will close by the end of the year. Retail industry experts say Credit Suisse may have underestimated the scope of the upheaval. “It’s more in the 30% range,” Ron Friedman, a retail expert at accounting and advisory firm Marcum said of the share of malls that he predicts will close in the next five years. “There are a lot of malls that know they’re in big trouble.” By ignoring new shopping centers being built, the research note took an overly simplistic view of the changing landscape of shopping centers, said analyst David Marcotte, senior vice president with Kantar Retail. “There are still malls being built,” Marcotte said. “Predominantly outlet malls and lifestyle malls.”

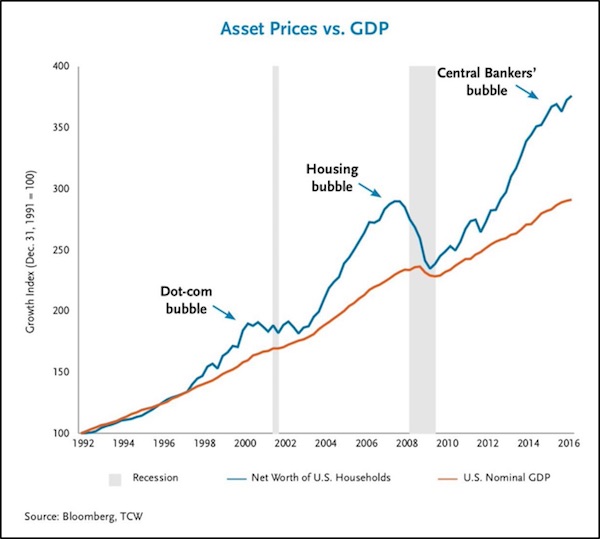

Now don’t get me wrong. Do I think Emmanuel Macron, a former Rothschild investment banker whose “ambition was always two steps ahead of his experience”, is the second coming of Charles de Gaulle? Do I think Donald freakin’ Trump is a modern day Andrew Jackson? Bwa-ha-ha-ha-ha-ha … good one! But here’s what I do think: • Something old and powerful is happening in the real world to crush the status quo political systems of every Western democracy. • Something predictably sad is happening in the political world to replace the old guard candidates with self-absorbed plutocrats like Trump and pretty boy bankers like Macron. • Something new and powerful is happening in the investment world to divorce political risk and volatility from market risk and volatility. The old force repeating itself in the real world is nicely summed up by these two charts, the most important charts I know. They’re specific to the U.S., but applicable everywhere in the West.

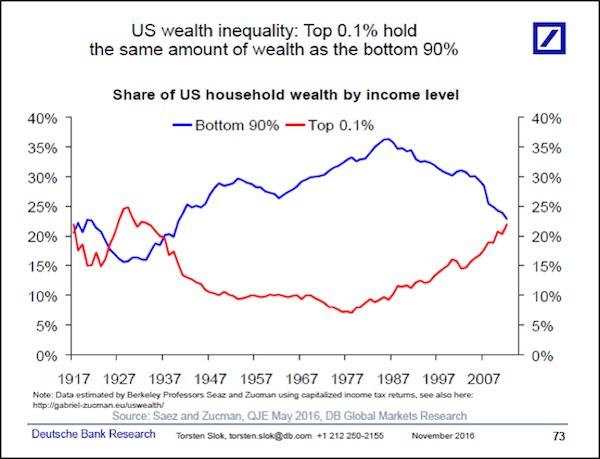

First, the Central Banker’s Bubble since March 2009 and the launch of QE1 has inflated U.S. household wealth far beyond what the nominal growth rate of the U.S. economy would otherwise support. This is a classic bubble in every sense of the word, with the primary difference from prior vast bubbles being its concentration and focus in financial assets — stocks and bonds — which are held primarily by the rich. Who wins the Academy Award for creation of wealth inequality in a supporting role? Ladies and gentlemen, I give you the U.S. Federal Reserve.

And as the second chart shows, this central bank largesse has sharply accelerated the massive shift in wealth to the Rich from the Rest, a shift which began in the 1980s with the Reagan Revolution. We are now back to where we were in the 1930s, where the household wealth of the bottom 90% of U.S. wage earners is equal to the household wealth of the top one-tenth of 1% of U.S. wage earners.

So look … I’m not saying that the current level or dynamics of wealth inequality is a good thing or a bad thing. I’m just saying that it IS. And I understand that there are insurance programs today, like social security and pension funds, which are not reflected in this chart and didn’t exist in the 1930s, the last time you saw this sort of wealth inequality. I understand that there are a lot more people in the United States today than in the 1930s. I understand that there are all sorts of important differences in the nature of wealth distribution between today and the 1930s. I get all that. What I’m saying, though, is that just like in the 1930s, there is a political price to be paid for this level of wealth inequality. That price is political polarization and electoral rejection of status quo parties.

[..] downgrades of bonds issued by local governments raise the interest rates those governments must pay on holders of its debt, thereby costing those communities up to hundreds of millions of dollars annually, according to the report, which was released Wednesday by the non-profit Roosevelt Institute’s ReFund America Project and focused on recent downgrades by Moody’s in relatively impoverished, predominantly-black localities. The more recent report [..] took a granular look at a few communities whose budgets were impacted by downgrades, which drive the prices of bonds down while raising the interest rate at which the government has to pay its bondholders. New Jersey was set to lose $258 million annually as a result of a Moody’s ratings drop, the report calculated, using the spread between interest rates on bonds with different Moody’s credit ratings and the amount of debt affected by the downgrade.

Moody’s announced a downgrade of the New Jersey’s $37 billion in publicly-issued debt to A3, six levels below the agency’s top rating of Aaa, in late March. The agency attributed the downgrade to “significant pension underfunding, including growth in the state’s large long-term liabilities, a persistent structural imbalance and weak fund balances,” as well as a tax cut that would decrease revenues by $1.1 billion over the next four years. New Jersey’s city of Newark — which is 52.4% African American and 33.8% Hispanic, compared to 12.6% and 16.3%, respectively, on the national level, according to U.S. Census data — was slated to lose an estimated $10 million annually as a result of a Moody’s downgrade, the report calculated. Newark’s median household income was just over $33,000, compared to nearly $54,000 nationwide, as of 2015.

That year, Moody’s downgraded Newark’s $374 million in general obligation unlimited tax bonds to Baa3, one level above junk bond status. The rating change, Moody’s said in the press release, reflected “the city’s further weakened financial position since last year,” along with its “reliance on market access for cash flow, history of aggressively structured budgets typically adopted late in the year and uncertainty around continued financial support from the state of New Jersey.” Further west, Chicago Public Schools (CPS) also stood to suffer tremendously from a Moody’s rating drop. The report authors calculated that the school system would lose out on $290 million annually from a September 2016 Moody’s downgrade to B3, five ranks below the highest junk bond rating. Nearly 40% of students are African American, 46.5% are Hispanic and 80.2% are considered “economically disadvantaged,” according to October 2016 CPS data.

Illinois had its bond rating downgraded to one step above junk by Moody’s Investors Service and S&P Global Ratings, the lowest ranking on record for a U.S. state, as the long-running political stalemate over the budget shows no signs of ending. S&P warned that Illinois will likely lose its investment-grade status, an unprecedented step for a state, around July 1 if leaders haven’t agreed on a budget that chips away at the government’s chronic deficits. Moody’s followed S&P’s downgrade Thursday, citing Illinois’s underfunded pensions and the record backlog of bills that are equivalent to about 40% of its operating budget. “Legislative gridlock has sidetracked efforts not only to address pension needs but also to achieve fiscal balance,” Ted Hampton, Moody’s analyst, said in a statement.

“During the past year of fruitless negotiations and partisan wrangling, fundamental credit challenges have intensified enough to warrant a downgrade, regardless of whether a fiscal compromise is reached.” Illinois hasn’t had a full year budget in place for the past two years amid a clash between the Democrat-run legislature and Republican Governor Bruce Rauner. That’s left the fifth most-populous state with a record $14.5 billion of unpaid bills, ravaged entities like universities and social service providers that rely on state aid and undermined Illinois’s standing in the bond market, where investors have demanded higher premiums for the risk of owning its debt. Moody’s called Illinois “an outlier among states” after suffering eight downgrades in as many years.

“The rating actions largely reflect the severe deterioration of Illinois’ fiscal condition, a byproduct of its stalemated budget negotiations,” S&P analyst Gabriel Petek said in a statement. “The unrelenting political brinkmanship now poses a threat to the timely payment of the state’s core priority payments.” Illinois’s 10-year bonds yield 4.4%, 2.5 percentage points more than those on top-rated debt. That spread – a measure of the perceived risk – is the highest since at least January 2013 and more than any of the other 19 states tracked by Bloomberg.

Uber reported yesterday that its NET LOSS totaled more than $700 million last quarter, despite pulling in a whopping $3.4 billion in revenue. (This means they spent at least $4.1 billion!) That’s the latest in a string of massive, 9-figure quarterly losses for the company. The only question I have is– how much cocaine are these people buying? Seriously, it’s REALLY HARD to spend so many billions of dollars. You could have over 100,000 employees (‘real’ employees, not Uber drivers) and pay them $150,000 EACH and still not blow through that much money in a single quarter. Even if you think about Research & Development, Uber still managed to burn through almost as much cash as NASA’s $4.8 billion budget last quarter. The real irony is that this company is worth $70 BILLION. And Uber is far from alone. Netflix is also worth $70 billion; and like Uber, they can’t make money.

Over the last twelve months Netflix burned through over $1.7 billion in cash, and they made up for it by going deeper into debt. The list goes on and on– Snapchat debuted with a $30 billion valuation after its IPO, only to subsequently report that they had lost $2.2 billion in the previous quarter. Telecom company Sprint is still somehow worth more than $30 billion despite having over $40 billion in debt and burning through more than $6 billion over the last three years. And then there’s Twitter, a rudderless, profitless company that is still worth over $13 billion. This is pure insanity. If companies that burn through obscene piles of cash and have no clear path to profitability are worth tens of billions of dollars, it seems like any business that’s cashflow positive should be worth TRILLIONS. None of this makes any sense, and investing in this environment is nothing more than gambling. Sure, it’s always possible these companies’ stock prices increase even more. Maybe Netflix and Twitter quadruple despite continuing losses and debt accumulation. Maybe Bitcoin surges to $50,000 next month. And maybe the Dallas Cowboys finally offer me the starting quarterback position next season.

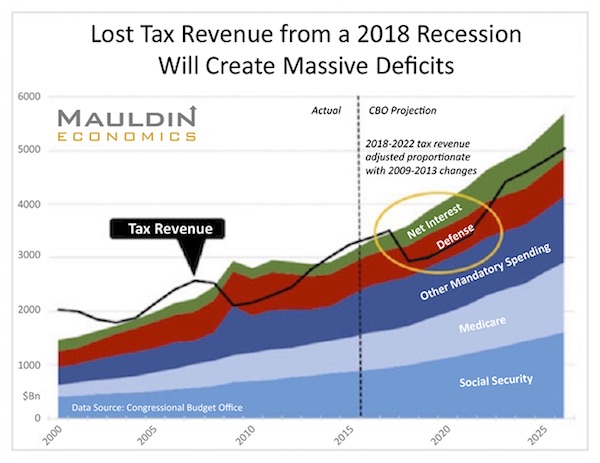

Sometime this year, world public and private plus unfunded pensions will surpass $300 trillion. That is not even counting the $100 trillion in US government unfunded liabilities. Oops. These obligations cannot be paid. A time is coming when the market and voters will realize this. Will voters decide to tax “the rich” more? Will they increase their VAT rates and further slow growth? Will they reduce benefits? No matter what they decide, hard choices will bring political turmoil. And that, of course, will mean market turmoil. We are coming to a period I call “the Great Reset.” As it hits, we will have to deal, one way or another, with the largest twin bubbles in the history of the world. One of those bubbles is global debt, especially government debt. The other is the even larger bubble of government promises.

The other is the even larger bubble of government promises. History shows it is more than likely that the US will have a recession in the next few years. When it does come, it will likely blow the US government deficit up to $2 trillion a year. Obama took eight years to run up a $10 trillion debt after the 2008 recession. It might take just five years after the next recession to run up the next $10 trillion. Here is a chart my staff at Mauldin Economics created in late 2016 using Congressional Budget Office data. It shows what will happen in the next recession if revenues drop by the same percentage as they did in the last recession (without even counting likely higher expenditures this time).

And you can add the $1.3 trillion deficit in this chart to the more than $500 billion in off-budget debt—and add a higher interest rate expense as interest rates rise. The catalyst could be a European recession that spills over into the US. Or it might be one triggered by US monetary and fiscal mistakes. Or a funding crisis in China, or an emerging-market meltdown. Whatever the cause, the next recession will be just as global as the last one. And there will be more buildup of debt and more political and economic chaos.

The price of raw ivory in Asia has fallen dramatically since the Chinese government announced plans to ban its domestic legal ivory trade, according to new research seen by the Guardian. Poaching, however, is not dropping in parallel. Undercover investigators from the Wildlife Justice Commission (WJC) have been visiting traders in Hanoi over the last three years. In 2015 they were being offered raw ivory for an average of US$1322/kg in 2015, but by October 2016 that price had dropped to $750/kg, and by February this year prices were as much as 50% lower overall, at $660/kg. Traders complain that the ivory business has become very “difficult and unprofitable”, and are saying they want to get rid of their stock, according to the unpublished report seen by the Guardian. Worryingly, however, others are stockpiling waiting for prices to go up again.

Of all the ivory industries across Asia, it is Vietnam that has increased its production of illegal ivory items the fastest in the last decade, according to Save the Elephants. Vietnam now has one of the largest illegal ivory markets in the world, with the majority of tusks being brought in from Africa. Although historically ivory carving is not considered a prestigious art form in Vietnam, as it is in China, the number of carvers has increased greatly. The demand for the worked pieces comes mostly from mainland China. Until recently, the chances of being arrested at the border slim due to inefficient law enforcement. But the prices for raw ivory are now declining as the Chinese market slows; this is partly due to China’s economic slowdown, and also to the announcement that the country will close down its domestic ivory trade.

China’s ivory factories were officially shut down by 31 March 2017, and all the retail outlets will be closed by the end of the year. Other countries have been taking similarly positive action on ivory, although the UK lags behind. Theresa May quietly dropped the conservative commitment to ban ivory from her manifesto, but voters have picked it up and there has been fury across social media. “All the traders we are speaking to are talking about what’s going on in China. It’s definitely having a significant impact on the trade,” said Sarah Stoner, senior intel analyst at the WJC. “A trader in one of the neighbouring countries who talked to our undercover investigators said he didn’t want to go to China anymore – it was so difficult in China now, and friends of his were arrested and sitting in jail. He seemed quite concerned about the situation,” said Pauline Verheji, WJC’S senior legal investigator.

Audi’s emissions scandal flared up again on Thursday after the German government accused the carmaker of cheating emissions tests with its top-end models, the first time Audi has been accused of such wrongdoing in its home country. The German Transport Ministry said it has asked Volkswagen’s luxury division to recall around 24,000 A7 and A8 models built between 2009 and 2013, about half of which were sold in Germany. VW Chief Executive Matthias Mueller was summoned to the Berlin-based ministry on Thursday, a ministry spokesman said, without elaborating. The affected Audi models with so-called Euro-5 emission standards emit about twice the legal limit of nitrogen oxides when the steering wheel is turned more than 15 degrees, the ministry said.

It is also the first time that Audi’s top-of-the-line A8 saloon has been implicated in emissions cheating. VW has said to date that the emissions-control software found in its rigged EA 189 diesel engine does not violate European law. The 80,000 3.0-liter vehicles affected by VW’s emissions cheating scandal in the United States included Audi A6, A7 and Q7 models as well as Porsche and VW brand cars. The ministry said it has issued a June 12 deadline for Audi to come up with a comprehensive plan to refit the cars. Ingolstadt-based Audi issued a recall for the 24,000 affected models late on Thursday, some 14,000 of which are registered in Germany, and said software updates will start in July. It will continue to cooperate with Germany’s KBA motor vehicle authority, Audi said.

Just a few hours after Megyn Kelly announced on NBC’s Today show that she would be interviewing Vladimir Putin in St Petersburg tomorrow at the International Economic Forum, Showtime released the first trailer and extended clip for The Putin Interviews, a sit-down with the Russian president conducted by the film-maker Oliver Stone for a four-part special that premieres on 12 June. Promoted as “the most detailed portrait of Putin ever granted to a Western interviewer”, The Putin Interviews spawned from several encounters over two years between Stone, director of politically oriented films including JFK and Nixon, and Putin. The interviews are to air as four one-hour installments, landing just a week after Kelly’s discussion with Putin, the centerpiece of her news magazine show on NBC, which premieres on Sunday night.

In the extended clip released on Thursday, Stone and Putin can be seen driving in a car with an English translator in the backseat, discussing topics such as Edward Snowden’s whistleblowing and Russian intelligence. “As an ex-KGB agent, you must have hated what Snowden did with every fiber of your being,” Stone asks in the clip. “Snowden is not a traitor,” Putin replies. “He did not betray the interests of his country. Nor did he transfer any information to any other country which would have been pernicious to his own country or to his own people. The only thing Snowden does, he does publicly.”

Two weeks before a critical Eurogroup summit, German Finance Minister Wolfgang Schaeuble launched a broadside at Prime Minister Alexis Tsipras, claiming that the leftist premier has not shifted the burden of austerity away from poorer Greeks as he had pledged. In his comments, Schaeuble also maintained that party influence on the Greek public administration has increased rather than decreased during Tsipras’s time in power, noting that ruling party officials have been appointed to the country’s privatization fund. Greek government sources responded tersely to Schaeuble’s criticism. “The responsibility of Schaeuble in managing the Greek crisis has been recorded historically,” one source said. “There is no point in his ascribing it to others.”

Meanwhike Germany’s Die Welt reported that the ECB had similar views on the need for Greek debt relief to the IMF, and indicated that Schaeuble might be facing pressure to make unpopular decisions ahead of elections scheduled to take place in Germany in September. Tsipras, for his part, apparently sought to lower expectations in comments on Thursday. During a visit to the Interior Ministry, he said the government’s goal was “fulfilling the country’s commitments” linked to Greece’s third international bailout. He dodged reporters’ questions about whether he expected to leave a European Union leaders’ summit on June 22 wearing a tie – something he has pledged to do only when Greece secures debt relief. “The important thing is that I don’t leave with further burdens,” Tsipras said.

Aides close to Tsipras will be closely following a Euro Working Group meeting scheduled for June 8 for indications about what kind of deal creditors are likely to put on the table at the Eurogroup summit planned for June 15. If the solution that is in the works is deemed to be too politically toxic, it is likely that Tsipras will undertake another round of telephone diplomacy with key EU leaders such as German Chancellor Angela Merkel and French President Emmanuel Macron. He spoke to several prominent EU leaders earlier this week to underline the Greek government’s conviction that it has honored its promises to creditors and it is their turn to reciprocate with debt relief.

Doctors may soon have a new weapon in the long-running war between antibiotics and bacteria. It’s a Swiss Army knife of a drug that’s tens of thousands of times more effective in lab tests against dangerous antibiotic-resistant bacteria. Starting with the discovery of penicillin in 1928, scientists and doctors have been finding and making molecules that weaken or kill bacteria in a range of different ways to help humans survive infections. And as soon as humans started employing these antibiotics, bacteria began evolving to beat those attacks. That has started to become a huge problem. So-called superbugs like methicillin-resistant Staphylococcus aureus (MRSA) can ward off some of our most potent antibiotics, making infections by these bacteria extremely hard to treat.

Not only that, but their existence poses a strategic challenge as well, forcing doctors to think hard about when and where they use certain antibiotics, lest bacteria develop resistance to them and render them less effective. Vancomycin is one antibiotic that has stayed effective even as others have been been brought down by resistant bacteria. That’s because of the way vancomycin works: by latching onto one of the building blocks bacteria use to build their cell walls, like the microscopic equivalent of a bully stealing your shovel in the sandbox and not giving it back. (In this analogy, we’re on the bully’s side.) By interfering with such a critical cellular process in such a fundamental way, vancomycin makes it hard for bacteria to develop a simple mutation to defeat the antibiotic. That makes vancomycin one of our last lines of defense for treating infections like MRSA that others can’t.

It’s why the World Health Organization (WHO) added the drug to its list of essential medicines. Naturally, some bacteria have found ways to fight vancomycin, the most common being to substitute a different cell wall building block that the antibiotic can’t latch onto. Taking vancomycin out of doctors’ quivers would be a big blow. Which is why the WHO also lists vancomycin-resistant bacteria at number four and five on its list of the most threatening antibiotic-resistant microbes. So. To try to make sure vancomycin can beat those resistant bacteria, and stay effective for the next few decades—a reasonable lifetime for an antibiotic—chemists Dale Boger, Nicholas Isley and Akinori Okano at the Scripps Research Institute in California opened up the hood to make a few adjustments to the molecule.

After swapping out one part and bolting on a couple others, the group’s souped-up vancomycin was about 25,000 times more potent against resistant bacteria, and it had better endurance. They describe their work in the Proceedings of the National Academy of Sciences. The major change was to the region of the molecule that grabs those cell wall building blocks, which are called D-alanyl-D-alanine. Resistant bacteria have learned to substitute the very similar D-alanyl-D-lactate, which your standard vancomycin can’t bind to very well, limiting its effectiveness. The researchers changed an oxygen atom for two atoms of hydrogen, making a new version of vancomycin that could hang onto either building block.

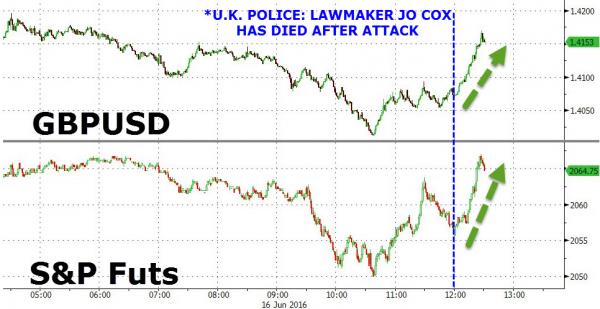

The devastating news that British MP Jo Cox has died following the shooting incident earlier today by a mentally unstable man…

“U.K. Labour Party lawmaker Jo Cox died after being attacked as she met constituents in her electoral district in West Yorkshire in the north of England. Campaigning ahead of next week’s referendum on Britain’s membership of the European Union was suspended for the rest of Thursday by both sides after the attack, which happened just before 1 p.m. Jo was attacked by a man who inflicted serious and, sadly, ultimately fatal injuries,” West Yorkshire Police Temporary Chief Constable Dee Collins said in a televised press conference in Wakefield.

…has sparked a bullish buying binge in stocks as Sterling rallies on the market’s “hope” that the Brexit vote will be delayed. This evening’s major speech at Mansion House by Bank of England Governor Carney has been cancelled due to her death…

Bank of England says Governor Mark Carney will no longer deliver planned speech in London. BOE cites “dreadful attack today on Jo Cox MP” Governor will attend event and deliver a “short speech reflecting on today’s events”

No further comment. Perhaps complete silence would be the most appropriate answer, but all we’ll hear all day and then some is comments and opinions. Spin doctors and conspiracies work overtime.

Labour MP Jo Cox, who died on Thursday after being attacked in her constituency of Batley and Spen in West Yorkshire by an armed man, makes a speech in parliament about the need for the UK to help child migrants stranded unaccompanied in Europe. The speech was part of a debate on the issue which took place in April 2016.

America has a housing crisis, and most Americans want policy action to address it. That’s the conclusion of an annual survey released Thursday by the MacArthur Foundation. The “crisis” is no longer defined by the layers of distress left behind after the subprime bubble burst, but about access to stable, affordable housing. A vast majority of respondents – 81% – said housing affordability is a problem, and one-third said they or someone they know has been evicted, foreclosed on, or lost their housing in the past five years. Over half the respondents, 53%, said they’d had to make sacrifices over the past three years to be able to pay their mortgage or rent. Yet most respondents believe the housing problem is solvable, and want policymakers to address it.

Nearly two-thirds of survey respondents from both parties say housing hasn’t received enough attention in the 2016 campaign. Most people supported a range of proposed policies to support affordable housing, both rentals and purchase. But people increasingly believe that owning a home is a “an excellent long-term investment.” Some 60% agreed with that statement, up from 56% a year ago and 50% in 2014. Access to stable, affordable housing – whether to rent or buy – is “about more than shelter,” the MacArthur Foundation noted in a release. “It is at the core of strong, vibrant, and healthy families and communities.”

“If 2006 was a known bubble with housing prices at “X”, affordability never better, easy availability of credit, unemployment in the 4%’s, total workforce at record highs, and growing wages, then what do you call today with house prices at X+ 5% to 20%, worse affordability and credit, higher unemployment, weakening total workforce, and shrinking wages? Whatever you call it, it’s a greater thing than “X”.

[..] if everybody always had to purchase owner-occupied properties using the same down payment amount and a market rate, fixed-rate mortgage then house prices would always reflect the employment, income, and macro-economic conditions of the surrounding area. But, when ‘Shadow Demand’ cohorts enter the market using cheap and easy credit and liquidity prices can detach from local-area economics, especially if the Shadow Demand continues to gain market share. Heck, in the greater Phoenix region, over 50% of all households can’t afford the going rate on a two-bedroom apartment, yet house prices are some of the strongest in the nation. Obviously, this isn’t due to strong end-user, shelter-buyer fundamentals.

As Shadow Demand continues to gain share over end-user buyers, they settle for lower respective returns on their housing investments and prices continue to rise. Then, when appraisers use properties purchased by Shadow buyers — for unconventional purposes with cheap and easy credit and liquidity — as comparable sales, all property values rise. Sure, there are end-user, shelter-buyers who will be able to chase the market all the way up. But, the larger the bubble blows the more the end-user, shelter-buyer demand will get crowded out and/or turn into increased supply as they liquidate. We are seeing this happen all over the nation.

In Bubble 1.0, Shadow Demand continued to gain market share until it blew up. And we know that beginning in 2011 the four pillars of unorthodox, Shadow Demand — beginning with the distressed market — controlled housing demand and still does. The implosion of the mortgage securitization market in 2007 didn’t crash housing. Rather, when the Shadow Demand – reliant on cheap and easy credit and liquidity largely driven by securitization — left the market, housing “reset to end-user, shelter-buyer fundamentals”. In other words, the pendulum swung back to the fundamental, end-user, shelter-buyer with 20% down and a market-rate 30-year fixed mortgage, which was 30% lower. Again, this isn’t a housing crash per se, rather a demand-shift and a reset, or reattachment, to real fundamentals.