Pablo Picasso Rooster 1938

The cavalry.

• Art Cashin: Once the 10-Year Yield Hits 3% ‘All Hell’ Could Break Loose (CNBC)

It could be a bad day for the markets once the yield on the benchmark 10-year Treasury hits 3%, closely followed trader Art Cashin told CNBC on Thursday. “That 3% level is both a target and a kind of resistance. Everybody knows it’s like touching the third rail,” said Cashin, UBS director of floor operations at the New York Stock Exchange. “The assumption is once they do it, all hell will break loose. So we’ll wait and see.” As of early Thursday, the 10-year yield was slightly lower, around 2.91%, down from Wednesday’s four-year high of 2.95%. Wall Street fears returned Wednesday afternoon after minutes from the Federal Reserve’s latest meeting sent bond yields rising and stocks into a tailspin. The last time the 10-year yield traded above 3% was in January 2014.

“Initially, yields moved down, stocks rallied like crazy,” Cashin recalled about Wednesday, moments after the Fed minutes were released. “Then about eight minutes into that move, stocks looked back and noticed bonds had changed their mind.” The sharp moves seen Wednesday were probably due to “our friends, the long-lost ‘bond vigilantes,'” Cashin told “Squawk on the Street.” The term “bond vigilantes” was coined by market historian Ed Yardeni during the 1980s, referring to traders who sell their holdings in an effort to enforce what they consider fiscal discipline. Selling bonds sends yields higher due to the inverse relationship between bond prices and bond yields. “We’re going to need a couple weeks to see if the bond vigilantes really are back or not,” Cashin said. “Or whether it was simply a fluke. But remembering what bond vigilantes look like, it certainly had fingerprints on them.”

Before it burns down the entire financial sector.

• China Regulators Take Control Of Insurance Giant Anbang (AFP)

China took over Anbang Insurance for a year on Friday and said its former chairman faces prosecution for “economic crimes”, in the government’s most drastic move yet to rein in politically connected companies whose splashy overseas investments have fuelled fears of a financial collapse. The highly unusual commandeering of Anbang signalled deep official concern over the Beijing-based company’s financial situation and comes as the government looks to address spiralling debt in the world’s second-largest economy. The China Insurance Regulatory Commission said Anbang, which has made a series of high-profile foreign acquisitions in recent years, had violated insurance regulations and operated in a way that may “severely” affect its solvency. The announcement also clarified the fate of Anbang’s chairman Wu Xiaohui, who was reported by Chinese media to have been detained last June.

The insurance regulator confirmed Wu was being “prosecuted for economic crimes”, a startling fall from grace for a man who reportedly married a granddaughter of late Chinese leader Deng Xiaoping. A statement by government prosecutors in Shanghai said Wu was suspected of fraudulent fundraising and “infringement of duties”. Acquisitive private companies such as Anbang, HNA, Fosun and Wanda have increasingly loomed in the government’s cross-hairs as it conducts a sweeping crackdown on potential financial risks. The four firms were in the vanguard of an officially-encouraged surge in multi-billion-dollar overseas deals by Chinese firms to snatch up everything from European football clubs to hotel chains and movie studios, and were until recently considered untouchable because of their political connections.

China needs to keep its reserves at home.

• Xi’s Debt Crackdown Goes Into Hyperdrive (BBG)

If you needed confirmation about China’s determination to rein in surging corporate debt, the dramatic government takeover of Anbang Insurance is pretty much it. The unprecedented seizure of a private insurer underscores President Xi Jinping’s policy drive to cut back on the debt-fueled excesses that have accompanied China’s growth miracle. It’s a direct hit to corporate binge spending that authorities want to stem; it energizes a long running anti-corruption campaign; and it demonstrates that short-term economic pain will be tolerated for the longer-term goal of a more sustainable expansion. For the rest of the world, the intervention offers up a useful reminder: When you do business with China, you do business with the Communist Party.

“It’s a new example of the seriousness of Xi Jinping’s government to insert the party and the state at all levels of business,” said Fraser Howie, co-author of the book “Red Capitalism” who has two decades of experience in China’s financial markets. “They have no qualms about coming in over the top and saying ‘we are going to take this over.’” He likened the takeover to the U.S. Federal Reserve, the Financial Industry Regulatory Authority and the Securities and Exchange Commission coming together to restructure a company. [..] The backdrop to the pincer move on Anbang and its founder Wu Xiaohui, who is to be prosecuted for alleged fraud, is a robust economy that’s giving officials the running room to crack down on debt excesses without depressing growth.

Overseas investment by Chinese companies has been strictly curtailed since last year as part of the broader ambition to shift the economy onto a more sustainable footing after years of debt-fueled expansion. Because China is self financed and credit is steered by state-owned lenders to state-controlled or linked companies, authorities have the luxury of intervening at their whim to shuffle money from one section of the economy to another. That’s one of the key reasons why regulators are able to tackle Anbang and other high profile conglomerates without lawyers, shareholder activists or opposition politicians getting in the way.

I don’t believe this is the whole story. Shadow banking in China is so lucrative there’s no way foreigners are not heavily involved.

• BIS Suggests Beijing Is Behind China Shadow Banking Sector (F.)

Concerns about the scale of shadow banking in China have now risen alongside concerns about the ever-rising debt load across the economy. The IMF, for example, has been consistently warning about this issue, along with Western credit ratings agencies. But the biggest hawk on China’s credit risks has for some time been the Bank for International Settlements (BIS), known as the central banker’s bank. The BIS produced a comprehensive assessment of the “shadow banking” sector last week. The report itself is not very surprising, but it does suggest much coverage of the issue adopts a misplaced tone. The most important insight the report generates is simply that the shadow banking sector in China is almost entirely driven by the traditional, state-dominated banks ; the SOE banks, the Joint Stock banks and the City commercial banks, all of which have significant levels of state involvement.

Indeed it was estimated in 2014 that the Chinese banking system was capitalized by only about 12% private capital, the rest linking back to the Chinese state, either centrally or regionally. In other words, although the phrase “shadow banking” is used in China, in Western economies this usually refers to activity that is quite distinct from the state, where private investors knowingly operate outside of the many regulatory safeguards offered by traditional banking. Whereas in China the state is either the key mediator or even the guarantor of the unregulated activity. In other words, the state in China is freely engaging in unregulated activity, precisely in order to avoid the burdens of their own regulations. This is perhaps why “shadow banking” in China is often–and more accurately–referred to as “banking in the shadows” as it is a substitute for traditional banking, but it takes place out of sight.

This may be well understood by banking professionals, but it is an example of the kind of difference of emphasis that leads to misunderstanding in the markets and the press. The impression that China is somehow slowly getting to grips with a poorly regulated sector, or at least announcing its intention to do so, is quite simply at variance with what is actually going on, which is that the state itself is the source of the problem. The “shadow banking” sector in China has expanded enormously, not in spite of the state but because of it. It both applies the regulations in the formal banking sector, and avoids them in the “shadow banking” sector. None of this changes the fact that the overarching problem is China’s rapidly rising overall debt pile, but we shouldn’t be under any illusions over what exactly is hiding in the shadows. More to the point, if the activities of the Chinese state are hiding in the shadows, it is worth considering what exactly they are hiding from?

Short term gains. Halt outflows. But a strong yuan wreaks hovoc on exports.

• China Is Letting The Yuan Crush The Dollar To Appease Trump (CNBC)

The Chinese yuan has appreciated 10% against the dollar since the start of 2017, quelling some criticism that the export giant has been deliberately suppressing its currency to gain economic advantage over its trading partners. This is all going according to China’s plan, experts said. Although the strength of the yuan against the dollar is in part due to the greenback’s weakness, experts said the world’s second-largest economy is also propping up its currency to appease President Donald Trump. China has “reversed the rise” of the dollar against the yuan, and there’s now “meaningful” strength against the greenback, Bilal Hafeez, global head of G-10 foreign-exchange strategy at Nomura, wrote in a recent note. “Part of this was likely a response to the election of President Trump and the need to avoid being labelled a currency manipulator,” Hafeez added.

On the 2016 campaign trail, Trump repeatedly said he would name China a currency manipulator from his first day in office. That has not happened. [..] China will probably continue to manage its currency in the background even if it keeps its value against the dollar relatively high, analysts said. Morgan Stanley analysts said in a note this week that the trade-weighted yuan should remain “largely stable” around current levels as Beijing’s capital control efforts have worked. “If [the yuan] continues to appreciate rapidly, policy-makers may seek to stem the rise in order to maintain stability in the trade-weighted [yuan], which would likely be achieved by verbal communication and a relaxation of some outbound capital restrictions,” Morgan Stanley added.

Beijing is walking a tricky tightrope as the Communist regime seeks to balance political concerns with economic reforms and the demands that come with a market-based system. In the second half of 2015, the Chinese government shocked markets by devaluing the yuan. That spurred capital flight due to concerns over the health of the world’s second-largest economy — which further depressed the Chinese currency. Beijing has been trying to reverse that damage. “I think they ultimately want a weaker currency, they just don’t know how to achieve it. They tried in 2015, it didn’t work, turned into a vicious cycle and they’re kind of stuck right now with always trying to control everything but not knowing how to get a weaker currency through a structural slowdown in a way that does not cause a lot of disturbances to domestic financial markets for instance,” said Jason Daw at Societe Generale.

The Russians did it.

• Bond Villain in the World Economy: Latvia’s Offshore Banking Sector (CP)

If the world economy were a Bond movie, Latvia’s offshore banking economy would be its Bond villain. Presently, this plucky state of 1.8 million people on Russia’s border is leading the world’s financial press with two major scandals. First, there is their long-standing Central Bank Governor, Mr. Ilmars Rimsevics. While Latvia’s population (disproportionally aged, as many of the young have left to find work abroad) only rivals that of Hamburg, but with a much smaller economy, Mr. Rimsevics nonetheless commands a salary bigger than Central Bank heads of most similar sized countries and in 2016 saw the largest%age salary increase of any EU Central bank head. Regardless of his super-sized income, Mr. Rimsevics has been accused of using his post as a sinecure to increase his pay by several multiples. His ‘victims’ being the banks in Latvia that he oversees, of which one, Norvik, the provenance of a Russian oligarch in London, protested.

[..] The other scandal, more serious, but lacking a face and bereft of central casting’s villainous imagery (e.g., oligarchs at the hunting lodge), is that of ABLV. ABLV is the largest Latvian owned bank. Latvia is a small country with lots of ‘banks.’ ABLV is largely a correspondent bank, or a bank holding deposits of foreigners along with providing them with ‘services’ that conceal the identity of their owners. Correspondent banking, euphemistically in the ‘industry’ called “wealth management” and “tax optimization.” [..] Just as Mr. Rimsevics has seemingly been caught with Russian oligarchs, ABLV has been linked to handling money for North Korea’s weapons program. This crossed the line for the United States, which in the main has vacillated between support and tolerance of offshore banking, but who since 9/11 has become wary of its ‘downsides,’ such as terrorists and ‘axis of evil’ states availing themselves of their helpful services.

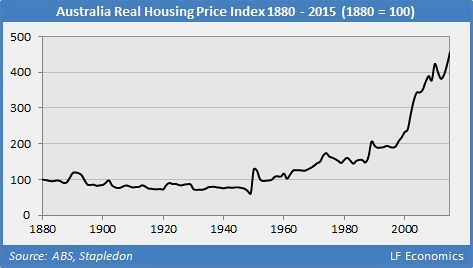

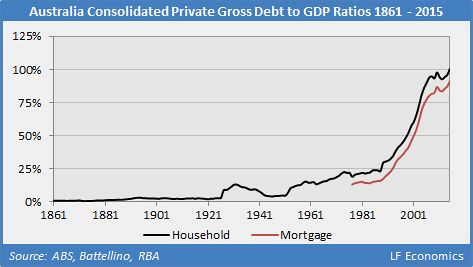

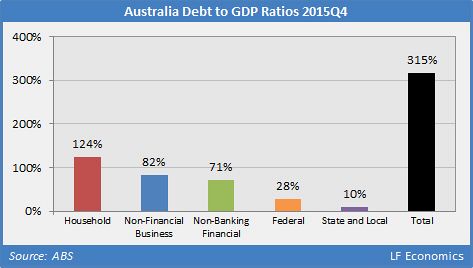

“Yes RBA, you did inflate housing bubble…”

• Reserve Bank Of Australia Accused Of Causing Ponzi Mortgage Market (AFR)

For years the Reserve Bank of Australia dismissed our warnings that excessively stimulatory interest rate cuts – which bequeathed borrowers with never-before-seen 3.4% mortgage rates that fuelled double-digit house price inflation – had blown a bubble that presented genuine financial stability risks. This manifested via record increases in speculative investor activity, interest-only loans and, more broadly, Australia’s household debt-to-income and house price-to-income ratios, which leapt into unchartered territory (notably above pre-global financial crisis peaks). The RBA narrative was very different. “Our concern was not that developments in household balance sheets posed a risk to the stability of the banking system,” governor Philip Lowe recently explained.

“Rather, it was more that…the day might come, when faced with bad economic news, households feel they have borrowed too much and respond by cutting their spending sharply, damaging the overall economy.” Nothing to see here when it comes to financial stability, if you believe the weasel words. It turns out Lowe was privately “packing his dacks” after unleashing the mother-of-all-booms powered by the cheapest credit in history. After the sudden deceleration in national house price growth – as documented here – from an 11.5% annualised rate in May 2017 to just 1.9% today, the governor revealed to parliamentarians that he’s now “much more comfortable…than I have been in recent years when I have been appearing before this committee, when I was quite worried”. That’s central speak for petrified.

Lowe conceded that “housing prices were rising very, very quickly – much faster than people’s income – and the level of debt was rising much faster than people’s income”. Yet according to the RBA’s interpretation, the 50% explosion in house prices between 2012 and 2018 was propelled not by the 11 interest rate cuts it bestowed on borrowers over the same period, but by a lack of new housing supply. You have to ignore the record building boom to believe this BS.

Pay me Ponzi!

• US Shale Investors Still Waiting On Payoff From Oil Boom (R.)

U.S. oil production has topped 10 million barrels per day, approaching a record set in 1970, but many investors in the companies driving the shale oil revolution are still waiting for their payday. Shale producers have raised and spent billions of dollars to produce more oil and gas, ending decades of declining output and redrawing the global energy trade map. But most U.S. shale producers have failed for years to turn a profit with the increased output, frustrating their financial backers. Wall Street’s patience ran out late last year as investors called for producers to shift more cash to dividends and share buybacks. “‘Give me some cash, please.’ That’s what investors have said,” said Anoop Poddar, a partner at private equity firm Energy Ventures.

And yet such calls for payouts remain a debate in the industry as oil prices have recently creeped up to four-year highs. Investors demanding immediate returns could risk forcing firms to curb expansion that could have a higher long-term payoff if oil prices continue to rise. For now, share prices of shale producers have yet to fully recover from the 2014 oil price collapse, when many investors took losses as hundreds of firms went bankrupt and those that survived struggled. The energy sector has lagged the rally that took the broader stock market to record highs. The S&P 500 Energy Index remains nearly a third off its peak in mid-2014, when oil prices topped $100 a barrel. The broader S&P 500 index is up 39% during the same period.

This year, five of the 15 largest U.S. independent shale firms have started paying or raised quarterly dividends, the documents show. But six of the firms have never offered a dividend or have not restored cuts implemented since the 2014 oil price collapse. Anadarko Petroleum earlier this month added $500 million to an existing buyback program and raised its dividend by 20%, sending its shares up 4.5% the next trading day. Buybacks reduce the number of shares outstanding, boosting the value of stock that remains.

This could turn ugly. Very ugly.

• EU Leaders Go to Battle Over Post-Brexit Budget Gap (BBG)

Hashing out the European Union’s multiannual budget is a political slugfest at the best of times. Throw in Brexit and the contest looks even more bruising. The U.K.’s scheduled withdrawal from the EU next year will leave a 10 billion-euro ($12.3 billion) annual hole in the bloc’s spending program, the main topic when leaders meet on Friday to map out Europe’s 2021-2027 budget. A Bloomberg survey of government positions reveals splits over how to cover the gap, with at least three net contributors – Sweden, the Netherlands and Austria – saying they won’t pay more. While amounting to only 1 percent of EU economic output, the European budget of 140 billion euros a year provides key funds for farmers, poorer regions and researchers in everything from energy to space technologies.

It’s also a barometer of the political mood in European capitals, signaling the risk of fissures as the EU seeks to maintain unity in the Brexit talks, confront new security challenges and curb democratic backsliding in countries such as Poland. “I expect it to be quite a fight,” said Guntram Wolff, director of the Bruegel think tank in Brussels. “The EU budget hole is quite substantial. You actually have a double challenge: you have to cut some spending and increase money for new priority areas.” [..] Britain’s absence from the next multiannual European spending program is conspicuous because the country is the No. 2 net contributor. Germany, which is the largest, and Italy, the fourth biggest, both say they are open to increasing their payments into the financial framework, the survey shows. Portugal and Estonia, both net recipients of funds, are prepared to raise their contributions, while France and Belgium are still undecided.

So what’s he going to do about it?

• Irish President Criticises EU Treatment Of Greece (IT)

Those responsible for mistaken economic policies that have had such a negative effect on the Greek people need to take responsibility for their actions, President Michael D Higgins has said, on the first day of his state visit. “It is a moral test of all actions that the person who initiates an action must take responsibility for its consequences,” Mr Higgins told his Greek counterpart, Prokopis Pavlopoulos. “It is little less than outrageous that the social consequences of decisions that are taken are not in fact understood and offered to people as choices,” Mr Higgins said, in remarks at a bilateral meeting at the presidential mansion.

Referring to the speech made by Emmanuel Macron on his recent state visit to Athens, Mr Higgins said he had to “say something much stronger” than the French president, who, he noted had acknowledged “that great mistakes, with great effect on the Greek people, have been made and that these were mistakes of the European Union”. “Cohesion, social cohesion, social Europe, must be placed on the top of the agenda that we all now share on the future of the union.” This meant that “we cannot continue adjusting out populations to economics models that not only have failed but have not submitted themselves to empirical tests in relation to their social consequences. “If parliaments and the mediating institutions continue to leach influence because they no longer have any power, because influences are coming from those who have no accountability, then we have a crisis.”

Note: the whole thing is based on an FBI report, with probes of Novartis going back to at least 2014.

“..bribery scandal [..] the worst since the creation of the modern Greek state almost 200 years ago..”

• Greek MPs Vote To Investigate Top Politicians In Novartis Bribery Claims (G.)

The Greek parliament is to investigate 10 of the country’s top politicians over in return for patronage that resulted in huge losses for Greece. After a raucous 20-hour debate, MPs voted early on Thursday to form a parliamentary committee tasked solely with investigating two former prime ministers and eight other ministers in connection with the allegations. The governor of the Bank of Greece, Yannis Stournaras; Europe’s migration commissioner, Dimitris Avramopoulos and the country’s former prime minister Antonis Samaras are among those accused of giving Novartis preferential market treatment. “We will not cover up,” Samaras’s successor, Alexis Tsipras, told parliament. “The Greek people must learn who turned pain and illness into a means of enrichment.”

Officials in Tsipras’ leftist-led administration have described the alleged bribery scandal as the worst since the creation of the modern Greek state almost 200 years ago. It has raised fears of political instability at a time when many had hoped the country was finally returning to normality after years of tumult. All 10 of those implicated vehemently rebutted the charges in often angry and emotional speeches during the debate. Stournaras, a former finance minister who helped steer Greece through some of its darkest days of the debt crisis after the country’s near-economic collapse, described the allegations as “disgusting fabrications”. Panagiotis Pikrammenos, who headed a one-month caretaker administration at the height of the crisis in 2012, came close to tears as he described the allegations against him “as lies and unacceptable slander”.

The cross-party committee, made up of 21 MPs, is expected to be established imminently. It will have the power to decide whether accusations of bribery, breach of duty and money-laundering apply, under a strict statute of limitation, to each of the accused. Under Greek law, parliament must investigate politicians for alleged infractions before they can face judicial prosecution. Few question that wrongdoing was committed. A confidential report by prosecutors originally tipped off by US authorities alleged that bribes of as much as €50m (£44m) were paid to politicians between 2006 to 2015 to promote Novartis’s products. More than 4,500 doctors are accused of malpractice as well. [..] With losses of around €4 billion for the country’s health system, the scandal will have played a significant role in Greece’s financial meltdown.

How to make sure an economy won’t recover.

• Greece Is The European Champion In Corporate Taxes (K.)

Corporate taxation in Greece is burdensome and anti-competitive, the Hellenic Federation of Enterprises (SEV) says in a report published on Thursday, stressing that Greek taxes also fail to draw revenues above the average rate of other European countries that as a rule have lower corporate taxation. According to SEV, the real tax load on corporations has increased considerably, with income tax reverting to the 2006 level plus the income on revenues from dividends: Today income tax comes to 29%, the tax on dividends to 15%, the solidarity levy to 10% and social security contributions for board members to 26.7%. This amounts to 81% of profit distribution, SEV said.

The federation’s analysts argue that profit taxation is above the European Union average and definitely higher than neighboring states that are Greece’s direct rivals within the bloc. If one adds board members’ social security contributions, then Greece has the highest corporate taxes by far, being the only country to have increased its tax sum since 2000, at a time when other states have been reducing the burden. SEV goes on to note that the tax rates are the just tip of the iceberg. The report focuses on the overall framework of corporate taxation that does not allow enterprises to grow and improve their competitiveness in international markets.

The federation highlights six specific problems in the corporate tax framework:

– The option of offsetting losses against future profits in Greece is for just five years, against at least 10 years in most EU states;

– Other countries have special incentives through tax exemption on expenditure, which in Greece are particularly limited;

– There is no framework for favorable regulations and incentives for mergers and acquisitions, which would encourage the streamlining and expansion of companies and reduce bad loans;

– There are no incentives such as accelerated amortization for new investments on equipment, which SEV calculates would have been fiscally neutral;

– Greek amortization rates are noncompetitive, particularly concerning investments in machinery and other equipment, forcing Greek firms to amortize their equipment slowly;

– Finally, Greece retains anachronistic levies such as stamp duty.

Ignores the role of social media-induced echo chambers.

• The Gun-Control Debate Could Break America (French)

Last night, the nation witnessed what looked a lot like an extended version of the famous “two minutes hate” from George Orwell’s novel 1984. During a CNN town hall on gun control, a furious crowd of Americans jeered at two conservatives, Marco Rubio and Dana Loesch, who stood in defense of the Second Amendment. They mocked the notion that rape victims might want to arm themselves for protection. There were calls of “murderer.” Rubio was compared to a mass killer. There were wild cheers for the idea of banning every single semiautomatic rifle in America. The discourse was vicious. It was also slanderous. There were millions of Americans who watched all or part of the town hall and came away with a clear message: These people aren’t just angry at what happened in their town, to their friends and family members; they hate me.

They really believe I’m the kind of person who doesn’t care if kids die, and they want to deprive me of the ability to defend myself. The CNN town hall might in other circumstances have been easy to write off as an outlier, a result of the still-raw grief and pain left in the wake of the Parkland shooting. But it was no less vitriolic than the “discourse” online, where progressives who hadn’t lost anyone in the attack were using many of the same words as the angry crowd that confronted Rubio and Loesch. The NRA has blood on its hands, they said. It’s a terrorist organization. Gun-rights supporters — especially those who oppose an assault-weapons ban — are lunatics at best, evil at worst. This progressive rage isn’t fake. It comes from a place of fierce conviction and sincere belief. Unfortunately, so does the angry response from too many conservatives.

[..] Unlike the stupid hysterics over net neutrality, tax policy, or regulatory reform, the gun debate really is — at its heart — about life and death. It’s about different ways of life, different ways of perceiving your role in a nation and a community. Given these immense stakes, extra degrees of charity and empathy are necessary in public discussion and debate. At the moment, what we have instead are extra degrees of anger and contempt. The stakes are high. Emotions are high. Ignorance abounds. Why bother to learn anything new when you know the other side is evil?

Major cold spell on the doorstep.

• 50,000 Die In UK ‘Cold Homes Public Health Crisis’ (Ind.)

Thousands of people are “needlessly” dying each year because they cannot afford to properly heat their homes, new research has revealed. The UK has the second-worst rate of excess winter deaths in Europe, a study by National Energy Action and climate-change charity E3G found. The organisations called for urgent action to end to the devastating but “entirely preventable” tragedy that they say amounts to a “cold homes public health crisis”. The death toll looks set to rise next week as the UK braces for an imminent “polar vortex” predicted to bring harsh frost, snow showers and freezing temperatures. Almost 17,000 people in the UK are estimated to have died in the last five years as a direct result of fuel poverty and a further 36,000 deaths are attributable to conditions relating to living in a cold home, the research found.

The number dying each year is similar to the amount who die from prostate cancer or breast cancer. A total of 168,000 excess winter deaths from all causes have been recorded in the UK over the latest five-year period. Of 30 countries studied, only Ireland has a higher proportion of people dying due to cold weather. The research was published to coincide with Fuel Poverty Awareness Day on Friday which aims to highlight the problems faced by those struggling to keep warm in their homes. It comes just 24 hours after Centrica, which owns British Gas, announced plans to cut 4,000 jobs after a “weak” year in which it made £1.25bn profit. The company’s chief executive, Ian Conn, said the Government’s energy price cap – designed to prevent loyal and vulnerable customers being ripped off – was partly to blame for the layoffs. Pedro Guertler, of E3G, who co-authored the research, said the winter death figures were not only a tragedy but a “national embarrassment”.