G.G. Bain Three-ton electric sign blown into Broadway, New York. 1912

All of the money, none of the prospects. Will he be the first to spend a full billion? Don’t change your station.

• ‘I’m Spending All My Money To Get Rid Of Trump’: Michael Bloomberg (R.)

U.S. presidential candidate Michael Bloomberg told Reuters he is ready to spend much of his vast fortune to oust Republican President Donald Trump from the White House in 2020, rejecting criticism from rivals for the Democratic nomination that the billionaire is trying to buy the U.S. election. Ranked by Forbes as the eighth-richest American, Bloomberg has flooded U.S. airwaves and social media feeds with messages that he stands the best chance to beat Trump, spending more on campaign ads since he launched his campaign in November than his main Democratic rivals have over the last year.

“Number one priority is to get rid of Donald Trump. I’m spending all my money to get rid of Trump,” Bloomberg told Reuters aboard his campaign bus on Saturday, during a nearly 300-mile (483-km) drive across Texas, one of the 14 states that will vote on Super Tuesday on March 3. “Do you want me to spend more or less? End of story.” U.S. Senator Elizabeth Warren, one of the leading Democratic presidential contenders who has vowed to get money out of politics, blasted Bloomberg when he launched his campaign with a $37-million TV advertising blitz, accusing the former New York City mayor of trying to buy American democracy. “These are just political things they say, hoping they catch on and they don’t like me doing it, because it competes with them, not because it’s bad policy,” Bloomberg said.

After entering the race late and missing the first six Democratic debates, Bloomberg generally sits fifth in national public opinion polls behind Joe Biden, Bernie Sanders, Warren and Pete Buttigieg. But not just the two liberal standard-bearers of Warren and Sanders, all of the four are too liberal to beat Trump, Bloomberg said. “One of the reasons I’m reasonably confident I could beat Trump is I would be acceptable to the moderate Republicans you have to have,” said Bloomberg, a former Republican who made his fortune selling financial information to Wall Street firms. “Whether you like it or not, you can’t win the election unless you get moderate Republicans to cross the line. The others are much too liberal for them and they would certainly vote for Donald Trump.”

Presidential candidate Michael Bloomberg says his Democratic rivals are 'too liberal' to beat Donald Trump. Ranked by Forbes as the eighth-richest American, Bloomberg is planning to air a 60-second commercial during during the Super Bowl. So is Trump https://t.co/Z0LIqJYgM1 pic.twitter.com/RegPO1rS9n

— Reuters (@Reuters) January 13, 2020

No, I don’t think Trump is brilliant, thank you. Just funny to see this coming from Greece.

• What If @realDonaldTrump Is Brilliant? (Papachelas)

History is often written by those who don’t follow the rules or, rather, by those who ostentatiously throw them onto the trash heap of history. Donald Trump is one of those people, whether we like it or not. In an era where political correctness and slick public relations are the norm in politics and beyond, Trump came along with his own unique style and turned everything on its head. This started during his candidacy for president. A one-time close associate of his described how his team tried to convince him to start using prepared speeches, reading from a teleprompter. He didn’t like the idea at all but he agreed to give it a go.

When the moment came for his first public speech, he started reading from the teleprompter, darting looks to his left and right, clearly uncomfortable with the whole process. At one point, his patience at an end, he petulantly threw down the screen and blamed his awkwardness on his team, declaring that he preferred making speeches without teleprompters. His associates were aghast for a few minutes. But after seeing the rave reception of the move by Trump’s supporters, they realized that his instinct and political brilliance was probably beyond them.

He pulled it off in domestic politics; could he also do it in foreign policy? All the relevant literature, handbooks and collected wisdom of experts far and near suggest that such a feat is impossible. What is essentially a negotiating tactic from the Manhattan real estate world cannot work in the forum of international politics. The art of pushing someone to the end of their tether and then making a deal at the last minute would be rejected as unenforceable. But that’s exactly what Trump is testing now. The assassination of Iranian General Qasem Soleimani in Iraq by American forces was a very extreme act which all Trump’s predecessors had avoided, as had even successive Israeli governments. Trump did it.

And by doing so he simultaneously sent a clear message to the Middle East that the USA is no longer dependent on its oil and natural gas reserves. Iran responded in a relatively reasonable fashion. In a few weeks, it will become clear whether those who believe that Iran will hit back harder – albeit under or over the radar – are right, or whether a new balance of power will finally emerge that puts it “in its place” and possibly leads to a new deal. That’s when a lot of so-called experts will be banging their heads against the wall.

Prepare for 11 months of this, getting uglier as we go along.

• Warren, Sanders Campaigns Spar In Rare Show Of Discord (R.)

A rare sign of discord emerged on Sunday between progressive Democratic presidential contenders Elizabeth Warren and Bernie Sanders over a report that Sanders’ campaign volunteers had called her a candidate of the elite in conversations with voters. “I was disappointed to hear that Bernie is sending his volunteers out to trash me,” Warren told reporters after a campaign event in Marshalltown, Iowa, which will hold the nation’s first nominating contest on Feb. 3. “I hope Bernie reconsiders and turns his campaign in a different direction.” Warren and Sanders, who are friends, fellow U.S. senators and their party’s progressive standard-bearers, agreed early in the nominating contest to an informal non-aggression pact and have largely avoided criticizing each other.

Politico reported late on Saturday that Sanders’ campaign had distributed talking points for volunteers on what to say to voters who are thinking of supporting his main rivals – former Vice President Joe Biden, Pete Buttigieg, the former mayor of South Bend, Indiana, and Warren. The guidance suggested that volunteers argue Warren was supported by “highly-educated, more affluent people who are going to show up and vote Democratic no matter what,” rather than motivating people who do not normally vote, Politico reported. Sanders said on Sunday he did not approve the negative talking points about other candidates. “We have over 500 people on our campaign. People do certain things. I’m sure that on Elizabeth’s campaign people do certain things as well,” Sanders told reporters after a rally in Iowa.

Blaming Trump for a process that has taken centuries to develop is as silly as it is lazy. There is no government anywhere that is willing to commit anything other than lip service to this.

• How Bad Can The Climate Crisis Get If Trump Wins Again? (G.)

Climate pollution in the US is up under Donald Trump and threatens to undermine international efforts to stall the crisis, especially if he wins re-election this year and secures a second term in the White House. While US climate emissions fell 2.1% in 2019, they rose significantly in 2018, according to estimates from the economic analysis firm Rhodium Group. On net, emissions are slightly higher than in the beginning of 2017, when Trump’s administration began enacting dozens of environment rollbacks aimed at helping the oil and gas industry. Trump is still working to further weaken bedrock standards. This week he proposed to allow major projects like pipelines and highways to bypass reviews of how they will contribute to global warming.

The draft rule is unlikely to become final before the November election, but it is yet another reason industries weighing climate choices might delay significant action. “What they have done is created confusion within the business community and the environmental world as to what are going to be the standards,” said Christine Todd Whitman, who led the Environmental Protection Agency under the Republican president George W Bush. “Essentially every regulation the agency promulgates gets a lawsuit that goes with it, almost inevitably … that’s the only good thing you can say about it.” Whitman called the approach “mindless” and said “whoever is a bigger donor gets to tell them what the environmental policy should be, it seems”.

In the absence of any federal climate action, states, cities and businesses have pledged their own efforts, seeking to encourage other big emitters like China and India to continue to slow their growing climate pollution. Andrew Light, a climate negotiator for President Barack Obama’s state department, said the world is taking note of those efforts, but if Trump is re-elected “you are going to see a lot of people who are worried anew about what the US can do.” Americans choosing Trump would send the signal that they don’t care about the climate, Light said.

America’s Pledge, a project to quantify ongoing US emissions reductions, estimates that non-federal actors – like states and cities – could cut climate pollution 37% below 2005 levels by 2030. A Democrat in the White House could increase that to 49% with what Light described as modest, politically achievable policy changes. Experts are increasingly calling for the US to halve its emissions by 2030 and neutralize them by 2050.

Next up: $50 trillion. You’re being had.

• Avoid UK Recession By Kickstarting Green Economy, Says Thinktank (G.)

The government fightback against the next recession should include pumping as much as £50bn into green projects, in a move that would help reboot the economy and tackle the climate emergency, according to a left-leaning thinktank. Against a backdrop of concern among economists that Britain is ill-equipped to combat another downturn on the scale of the 2008 financial crisis, the New Economics Foundation thinktank said a green plan to beat a future slump was required. In the event of a recession, it said the government should spend at least 2% of GDP, or around £30bn, to decarbonise the economy, by investing in renewable energy projects, planting trees, transport infrastructure, electric vehicles, and retrofitting homes with new insulation.

For a larger economic shock, as much as 3% of GDP, or around £50bn, could be spent. Leading economists including former US Treasury secretary Larry Summers and the former chief economist at the International Monetary Fund, Olivier Blanchard, have called on governments around the globe to prepare for future economic shocks with readily available blueprints to raise government spending. It comes as central banks, including the Bank of England, have limited capacity to provide support because interest rates remain close to the lowest levels on record more than a decade after the financial crisis. Mark Carney, the Bank’s governor, has hinted that Threadneedle Street could cut rates soon, while warning that it is running out of ways to combat recessions.

The foundation said that raising investment in green infrastructure was required regardless of whether Britain was facing a recession or not. However, it said that a plan for fighting a future downturn should have decarbonisation at its core. [..] It said that spending around £10.5bn on a mass insulation programme for homes – equivalent to only a third of the coalition government’s tax cuts between 2010 and 2013 – would have enabled residential emissions to fall by around 30% by 2018.

Why would CNN run a piece like this, at this point in time?

• China Is Really Worried About Unemployment, Social Unrest (CNN)

The Chinese government wants to do whatever it can to protect the economy in 2020. It’s got an enormous task ahead of it. Beijing has made clear that the world’s second largest economy cannot spiral into a slump and risk mass layoffs as it tangles with rising debt, cooling domestic demand and an ongoing trade war with the United States. That’s particularly important this year because it marks the conclusion of the government’s 13th Five-Year Plan, during which it promised to establish a “moderately prosperous society” and end poverty. Senior members of the Communist Party’s Politburo — the seven most powerful men in China — said last week that all efforts must be taken to achieve those goals in 2020.

In recent weeks, the government has bombarded the economy with a wave of stimulus measures, from tariff reductions that could help soothe the pain from rising prices, to rate cuts that could fuel more bank lending. Authorities are also amping up the language they’re using to describe the situation. China’s State Council last month called on local governments to “go to all lengths” to prevent massive job losses this year — what it characterized as the country’s top policy priority. The chief administrative office even warned that the country could face “massive unexpected incidents” if unemployment balloons — a euphemism in China widely understood to refer to social unrest and riots, and one that is rare in public government documents.

In recent years, the government has said it has to create 11 million new jobs annually to keep employment on track. While China’s official unemployment data has barely budged over the last several years, hovering between 4% and 5%, Beijing’s messaging suggests that it is unusually worried about the slowing economy and the challenges that the year could bring. “Beijing is much more worried about social unrest than about ballooning local debt, which at one point seemed to be a priority, ” said David Zweig, director of Transnational China Consulting Limited and a professor emeritus at the Hong Kong University of Science and Technology. Huge protests, after all, have for months consumed Hong Kong, which local officials said last November would sink into its first annual recession in a decade.

The protests have focused on calls for greater democracy, but economic factors such as the soaring cost of housing and an increasingly competitive labor market have been fueling a growing sense of dissatisfaction, particularly among the city’s young people. Social unrest might be the “black swan” risk facing the country, Zweig added, using a phrase that Chinese President Xi Jinping himself uttered last year to describe an improbable but chaotic event. “2020 is going to be very difficult, and mass unemployment may be the most feared problem,” said Frank Ching, a China political commentator and adjunct associate professor at the Hong Kong University of Science and Technology. “It’s not just an economic issue — it could develop into a political one. “

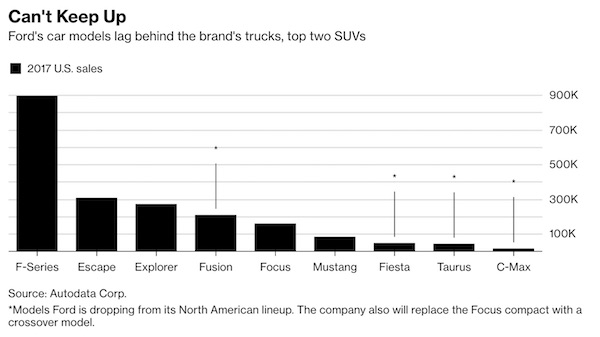

And 15% for GM. Who’s taking over? Reuters doesn’t say.

• Ford’s China Vehicle Sales Drop 26% In Third Straight Year Of Decline (R.)

Ford Motor Co’s China vehicle sales fell for a third consecutive year, by 26.1%, as it battles a prolonged overall sales decline in its second-biggest market that has hit demand for its mass-market Ford brand and sports utility vehicles. The U.S. automaker delivered 146,473 vehicles in China in the fourth quarter, down 14.7% year-on-year, Ford said in a statement. In total, it sold 567,854 vehicles over 2019. Ford has been trying to revive sales in China after its business began slumping in late 2017. Sales sank 37% in 2018, after a 6% decline in 2017. Anning Chen, president and chief executive of Ford Greater China, said that while 2019 was a “challenging” year for the automaker, it saw its market share in the high-to-premium segment stabilize and its sales decline in the value segment start to narrow in the second-half of the year.

“The pressure from the external environment and downward trend of the industry volume will continue in 2020, and we will put more efforts into strengthening our product lineup with more customer-centric products and customer experiences to mitigate the external pressure and improve dealers’ profitability.” The automaker plans to launch more than 30 new models in China over the next three years of which over a third will be electric vehicles. It has also said it would localize management teams by hiring more Chinese staff and aimed to improve relationships with joint venture partners. [..] Its larger U.S. rival General Motors last week said its sales in China fell 15% from a year earlier to 3.09 million vehicles in 2019, its second year of decline.

Waiting for the Belingcat “analysis”.

• Downing of PS-752 Already Being Used To Smear MH-17 Skeptics (OffG)

Many have noted that Iran’s honorable decision to take responsibility for the catastrophe is in sharp contrast with Washington’s response in 1988 when the U.S. Navy shot down Iran Air Flight 655 scheduled from Tehran to Dubai over the Strait of Hormuz in the Persian Gulf, killing all 290 occupants, after failing to cover it up. Just a month later, Vice President George H.W. Bush would notoriously state he would “never apologize for the United States of America. Ever. I don’t care what the facts are.” Although he was not directly referring to the incident, one can only imagine what the reaction would be if Iranian President Hassan Rouhani were to say the same weeks after shooting down the Ukrainian plane, let alone an American one.

Predictably, Tehran’s transparency has gone mostly unappreciated while the Trump administration is already trying to use the disaster to further demonize Iran. Oddly enough, Ukrainian International Airlines is partly owned by the infamous Ukrainian-Israeli oligarch, politician and energy tycoon Igor Kolomoisky, who was notably one of the biggest financiers of the anti-Russian, pro-EU coup d’etat which overthrew the democratically elected government of Viktor Yanukovych in 2014. Kolomoisky is also a principal backer of current Ukrainian President Volodymyr Zelensky whose dubious phone call with Trump resulted in the 45th U.S. president’s impeachment last month.

In another astounding coincidence, Kolomoisky’s Privat Group is believed to control Burisma Holdings, the Cypress-based company whose executive board 2020 presidential candidate Joe Biden’s son Hunter was appointed to following the Maidan junta. The former Vice President admitted that he bribed Ukraine into firing its top prosecutor who was looking into his son’s corruption by threatening to withhold $1 billion in loan guarantees. Kolomoisky, AKA “the Chameleon”, is one of the wealthiest people in the ex-Soviet country and was formerly appointed as governor of an administrative region bordering Donbass in eastern Ukraine following the 2014 putsch.

He has also funded a battalion of volunteer neo-Nazi mercenaries fighting alongside the Ukrainian army in the War in Donbass against Russian-speaking separatists which the military aid temporarily withheld by the Trump administration that was disputably contingent upon an investigation of Biden and his son goes to. In 2014, another infamous plane shootdown made international headlines when Malaysian Airlines Flight 17 (MH17) scheduled from Amsterdam to Kuala Lumpur was shot down over the breakaway Donetsk People’s Republic (DPR) in eastern Ukraine, killing all 298 passengers and crew.

Can Evo make a come-back?

• Bolivia Exiled Ex-President Morales Calls On Radio For Armed Militias (R.)

Bolivia’s exiled former president Evo Morales on Sunday defended a call he made for the formation of armed groups, a recording of which was leaked on public radio. Speaking exclusively to Reuters on Sunday night in Argentina where he is in exile, the defiant former president confirmed his was the voice in a recording played on Bolivian radio calling for creation of armed militias “as in Venezuela”. He said people have a right to defend themselves if the new government was attacking them. He said he had not meant armed with guns and was referring to citizen defense groups that had always loosely existed. “In Bolivia, if the armed forces are shooting the people, killing the people, the people have the right to organize their security,” he said in the interview with Reuters.

“We´re not talking arms, more like slingshots,” he said. “In some times (these groups) were called militias, in other times they were called union security or union police and in some places it is called communal guard. It is not new.” In the recording released by radio station Kawsachun Coca Tropico, Morales said he and his supporters had been “too trusting” ahead of last year´s presidential election, and should have had a “Plan B.” “If between now and in a little while… I were to return (to Bolivia) or someone else goes back, we must organize as in Venezuela armed militias of the people,” Morales said in the recording. “We were too trusting. The blunder: we did not have a ‘Plan B’.”

Is all innovation positive? Given how it’s promoted, one might think so. But that’s just because of the money involved.

• Somebody Snuck A Potato Into CES 2020 (F.)

I almost walked right by it. But then I realized the object the young man was holding up, apparently thrilling the small crowd gathered around his tiny CES 2020 booth, was a potato. The vegetable in question looked like an ordinary, chunky Idaho spud, although protruding out of one side was some kind of antenna, a black plastic appendage bent upward. Close to the potato’s surface, the exterior of the antenna became a thin, blade-like electrode that pierced the skin, clearly doing… something. The man was regaling the crowd with his incredible smart product, which he said was finally unlocking the awesome decision-making power of the potato. The antenna, which he called the NeuraSpud, tapped into the potato’s “artificial intelligence.”

Once you connected your smartphone over Bluetooth to the device and launched the accompanying app, you could ask the potato anything — with your voice, no less — and it would spout an answer on the screen, the digital-vegetable equivalent of a Magic Eight Ball. If the smart potato sounds like a big, stupid stunt, that’s because it is. The man behind the idea, Nicholas Baldeck from France, told me he brought his admittedly ridiculous “invention” to CES to make a point about the torrent of smart gadgets at the show, many of which don’t really solve problems at all. “This product has way more chance of success than 60% of the startups here,” Baldeck says. “I am skeptical of this idea of ‘connected everything.’

Now it looks like innovation is about putting a chip into any object. I’m not sure the word ‘smart’ makes more sense before the word toothbrush than the word potato.” Baldeck went to a lot of trouble to make his point. His booth cost $1,000, and he spent about $4,000 in travel, equipment and marketing. Plus the electrode-driven antenna he brought really works, he says — though “works” in this context is somewhat fungible, since what the electrode is “reading” from the juices inside the potato to create the answers is probably just random junk. He also had to buy a bunch of potatoes.

Include the Automatic Earth in your 2020 charity list. Support us on Paypal and Patreon.