Alfred Sisley Snow at Louveciennes 1878

Alina

Habba: We have billionaires who have created companies now helping to clean up a bad economy, clean up a government where we don't have efficient spending and run the country like they run their businesses much like Donald Trump. That's why he is a billionaire. pic.twitter.com/CSOH4dfGgr

— Acyn (@Acyn) December 7, 2024

https://twitter.com/i/status/1865244916961726923

Leavitt

.@karolineleavitt: "President Trump won this election by utilizing non-traditional, non-legacy media voices outside the beltway. That's clearly who the American people are listening to … It would be irresponsible of us not to include some of those voices in the briefing room." pic.twitter.com/1Yntl9eT7n

— Trump War Room (@TrumpWarRoom) December 6, 2024

"There has NEVER been a wavering in the optimism and the confidence from President Trump in @PeteHegseth," says incoming Press Secretary @karolineleavitt.

"President Trump stands by him 100%." pic.twitter.com/Bmt9Fo7931

— Trump War Room (@TrumpWarRoom) December 6, 2024

Tulsi

KEEP TULSI GABBARD FAR AWAY FROM NATIONAL INTELLIGENCE‼️

NEW: Nearly 100 former national security officials slammed Trump’s pick of Tulsi Gabbard for director of national intelligence, calling for closed Senate hearings to assess her qualifications. The letter, obtained by NBC… pic.twitter.com/9rVUFgUYIl

— Christopher Webb (@cwebbonline) December 7, 2024

McEnany

The Judge dropped count 1 against Daniel Penny, but this is far from a victory.

It is a travesty.

A Good Samaritan was made into a bad actor.

A hero turned into a villain.

Only in Manhattan (and maybe LA and DC) would a case like this have even been brought.

This… pic.twitter.com/wPpbgQoE8C

— Kayleigh McEnany (@kayleighmcenany) December 6, 2024

https://twitter.com/i/status/1865102720698364085

The speed at which the Assad regime unraveled provokes a whole new additional set of questions. Where were Russia, Iran, China? Were they ever going to help? There was hardly any resistance from Syrian troops, no fighting.

• Syrian Army Informs Officers Of Regime Change – Reuters (RT)

The Syrian Army command announced on Sunday that President Bashar Assad’s 24-year rule has come to an end, according to a Syrian officer who spoke to Reuters. The announcement follows a rapid offensive by jihadist forces in the capital. The jihadists claim that Damascus is “now free of Assad” and are expected to make their first public statement via state TV, Reuters reports, citing two anti-government sources. In response to the political uncertainty, Prime Minister Mohammad al-Jalali stated that he is “ready to cooperate with any leadership chosen by the people,” as quoted by Al Jazeera. He added that he remains at home and is inclined to support the continuity of government.

Ahmed Al-Sharaa, a prominent commander for the jihadist group Hayat Tahrir al-Sham (HTS), has issued orders prohibiting all militant forces in Damascus from approaching public institutions or firing weapons into the air. He went on to say that government institutions will remain under the supervision of the “former prime minister” until they are officially transferred to the new authorities. Over the weekend, HTS fighters and other anti-government militias entered Damascus, effectively taking control of the capital. Flight tracking websites indicate that Assad’s plane has left the city.

“There is no doubt that the rebels in Syria are creations of the CIA and Israel.”

“It’s an attempt by the US, Israel, and Turkey to overthrow the government in Damascus in order to block assistance flowing through Syria to Lebanon.”

—Former UK Diplomat pic.twitter.com/pk3MB3Nvzn

— sarah (@sahouraxo) December 7, 2024

“HTS, the group backed by NATO member Turkey and leading this anti-Assad onslaught, is a US-designated terror organization..”

• ‘Not Our Fight!’: Trump Weighs In On Syria’s Unraveling (ZH)

President-elect Donald Trump has weighed in on the rapid-moving events in Syria, where jihadist groups backed by Turkey are entering the outside environs of the capital of Damascus. The embattled President Bashar al-Assad still appears to be in residence, but his future is far from certain. “Opposition fighters in Syria, in an unprecedented move, have totally taken over numerous cities, in a highly coordinated offensive, and are now on the outskirts of Damascus, obviously preparing to make a very big move toward taking out Assad,” he began the statement on Truth Social.Trump emphasized that Washington should stay completely out, calling the situation a “mess” and that it is “not our fight”. He posted the same message on X.

It alludes to Russia’s inability to continue protecting Syria, given it is bogged down in the nearly three year long Ukraine war, while also blasting former President Obama’s past Syria policies and that he laid down ‘red lines’. Below is the full statement: “Russia, because they are so tied up in Ukraine, and with the loss there of over 600,000 soldiers, seems incapable of stopping this literal march through Syria, a country they have protected for years. This is where former President Obama refused to honor his commitment of protecting the RED LINE IN THE SAND, and all hell broke out, with Russia stepping in. But now they are, like possibly Assad himself, being forced out, and it may actually be the best thing that can happen to them. There was never much of a benefit in Syria for Russia, other than to make Obama look really stupid.”Syria is a mess, but is not our friend, & THE UNITED STATES SHOULD HAVE NOTHING TO DO WITH IT. THIS IS NOT OUR FIGHT. LET IT PLAY OUT. DO NOT GET INVOLVED!”

It must be remembered that Hayat Tahrir al-Sham (HTS), the group backed by NATO member Turkey and leading this anti-Assad onslaught, is a US-designated terror organization. A big question is: what comes next? While HTS has morphed from Syrian Al-Qaeda, it is trying to present to the West a softer image, claiming that it will protect minorities including Christians. However, its recent past clearly demonstrates that it rules territories under its control with Taliban-style force and brutality. Much of the nation’s population until now has stuck with Assad given the alternative is Somalia-style fracturing and rule by competing jihadist warlords. One thing is for sure: Trump will inherent dealing with an absolute tragic mess in Syria, the heartland of the Middle East, upon his opening days in office. Currently, US forces still occupy one-third of Syria, in the oil and gas areas of the northeast. During Trump’s first term he expressed an effort to “bring the troops home” but it’s widely reported he was stymied by his generals and national security officials.

Yesterday CNN call HTS 'moderate' Today: Churches smashed, women veiled by force, Christmas erased. HTS, an Al-Qaeda offshoot, is no moderate force. Coordinated media lies show the chilling power of Western security services to control the narrative. #Syria pic.twitter.com/S6uukSW20U

— Craig Murray (@CraigMurrayOrg) December 7, 2024

600,000 Russian soldiers vs 400,000 Ukrainian soldiers?

• Ukraine ‘Would Like To Make A Deal’ With Russia – Trump (RT)

Ukraine “would like to” make a peace deal with Russia, US President-elect Donald Trump has signaled after meeting with Vladimir Zelensky in Paris. In a post on his Truth Social platform on Sunday, Trump called for an immediate ceasefire and negotiations between Moscow and Kiev. Trump’s remarks came after reports emerged of a regime change in Syria, Russia’s ally in the Middle East, where jihadists claimed to have taken over the Syrian capital Damascus and toppled President Bashar Assad’s 24-year rule. Trump speculated that this happened because Assad’s “protector,” Russia, “was not interested in protecting him any longer.”

“[Russia] lost all interest in Syria because of Ukraine, where close to 600,000 Russian soldiers lay wounded or dead, in a war that should never have started, and could go on forever, Trump stated, claiming that Russia is currently “in a weakened state… because of Ukraine and a bad economy.” “Likewise, Zelensky and Ukraine would like to make a deal and stop the madness. They have ridiculously lost 400,000 soldiers, and many more civilians. There should be an immediate ceasefire and negotiations should begin,” the President-elect said, adding that if the conflict is not resolved, “it can turn into something much bigger, and far worse.”

Notre Dame

The world leaders at Notre Dame welcome President-elect Trump who commands respect unlike any head of state of our time.pic.twitter.com/Gpuk4MM8xw

— Greg Price (@greg_price11) December 7, 2024

It was suggested Trump shook Macron’s hand so hard, the latter needed a chiropractor.

• Meeting With Trump And Macron Was ‘Productive’ – Zelensky (RT)

US President-elect Donald Trump has met briefly with French President Emmanuel Macron and Ukrainian leader Vladimir Zelensky in Paris. No joint statement was released after the trilateral talks, but Zelensky hailed the conversation as “good and productive.” Trump arrived in Paris on Saturday to attend the reopening of Notre Dame Cathedral, extensively damaged in a fire in 2019. The trip was Trump’s first foreign visit since he defeated Kamala Harris in last month’s presidential election, but he nevertheless arrived at the Elysee Palace 40 minutes late, French media reported. Trump and Macron shared a warm embrace outside the palace, and speaking to reporters inside, Macron said that it was a “great honor” to host the incoming US president. Trump returned the compliment, before declaring that “the world seems to be going a little crazy right now.”

Zelensky, who was originally due to hold a one-on-one meeting with Macron, arrived nearly an hour later, before the three met for roughly 35 minutes, according to BFMTV. The three men did not speak to the press afterwards, and left for Notre Dame separately after posing for pictures. In a post on X, Macron said that the meeting was focused on “common action for peace and security.” Zelensky, also posting on X, described the talks as “good and productive.” “President Trump is, as always, resolute. I thank him,” Zelensky wrote. “We all want this war to end as soon as possible and in a just way,” he continued. “We spoke about our people, the situation on the ground, and a just peace.” “We agreed to continue working together and keep in contact. Peace through strength is possible,” he concluded, using a catchphrase regularly deployed by Trump to describe his foreign policy.

Throughout his campaign, Trump repeatedly promised that he would end the Ukraine conflict within “24 hours” of taking office, without offering any specifics on how he would achieve this beyond pushing Zelensky and Russian President Vladimir Putin into negotiations. Recent media reports suggest that he intends to ‘freeze’ the conflict along the current line of contact, using the threat of a reduction in US aid to force Zelensky to negotiate, and the threat of increased aid to Kiev to pressure Putin into talks. Zelensky insists that his ten-point ‘peace formula’ is the only viable path to what he calls a “just peace” with Russia. However, the Kremlin has dismissed this document as “delusional,” with its demands that Russia restore Ukraine’s 1991 borders, pay reparations, and surrender its own officials to war-crimes tribunals.

Moscow maintains that any settlement must begin with Ukraine ceasing military operations and acknowledging the “territorial reality” that it will never regain control of the Russian regions of Donetsk, Lugansk, Kherson, and Zaporozhye, as well as Crimea. In addition, the Kremlin insists that the goals of its military operation – which include Ukrainian neutrality, demilitarization, and denazification – will be achieved.

“If you don’t think they’re going to do this to RFK Jr., you haven’t been paying attention,” Kelly urged.

• Megyn Kelly Warns Deep State Is Coming For Hegseth, Gabbard, RFK Jr (ZH)

As Pete Hegseth – president-elect Trump’s pick for SecDef – runs the gauntlet of the nomination process, amid a cornucopia of media amplified unsubstantiated accusations against him, Sirius XM host Megyn Kelly has warned that the political establishment, both Democrats and Republicans, are attempting to derail Trump’s second term before it has even begun by targeting his cabinet picks. As Steve Watson writes at Modernity.news, Kelly pointed to Pete Hegseth, who who is fighting to stay in the running for Secretary of Defense amid a cornucopia of media amplified unsubstantiated accusations against him. Kelly warned that if Hegseth falls like Matt Gaetz did, then RFK Jr., Tulsi Gabbard and anyone else Trump picks will likely be next. “If you don’t think they’re going to do this to RFK Jr., you haven’t been paying attention,” Kelly urged.

“I realize that Pete has his belly exposed. He has not led a perfect life, and there’s plenty if you want to start attacking his character in terms of his marital history and so on,” Kelly noted. “But as he said to me yesterday, he found around 20, I think it was 18 or so, he found his two J’s: his wife, Jen and Jesus, and started changing his life in a profound way,” she further explained. The host continued, “Let’s say they get Pete’s scalp like they got Matt Gates’s scalp, Bobby Kennedy’s history makes Pete look like the consummate Boy Scout. He looks like he’s ready to enter the priesthood.” “He’s a lot older, with a lot more of a checkered past… It’s not going to be pretty at all. So we are really at a crossroads here about whether we are going to sacrifice these nominees because of checkered personal pasts or not. It’s not going to get easier after Pete,” Kelly emphasized.

But, as Gery Berntsen writes at American Greatness, when Pete Hegseth is confirmed as Secretary of Defense, he will be a forceful agent of change for the betterment of the United States of America. The abridged version of a famous Machiavelli quote, “Nothing is more difficult or dangerous than to attempt to change the order of things,” is in full view as we watch the process of confirming President Trump’s Secretary of Defense. When Pete Hegseth is confirmed as Secretary of Defense, he will be a forceful agent of change for the betterment of the United States of America. President-elect Trump’s nominee, retired Army National Guard Major and Fox News host Peter Hegseth, is receiving considerable fire amid allegations of misconduct while CEO of Concerned Veterans for America (CVA).

I am writing this article because I was one of the founding members of CVA. I am an Air Force veteran and retired senior operations officer and chief of station in the Central Intelligence Agency. While at the CIA, I held major field command positions and was a senior manager in the CIA’s Counter-Terrorism Center (CTC). I led the CIA’s largest paramilitary element on the ground during the invasion of Afghanistan in 2001, seizing Kabul, initiating the battle of Tora Bora, and leading teams around the globe in several dangerous crises. I worked hand in glove with the most important elements of the National Security Council, the Department of Defense, the Department of Justice, and the FBI to secure and safeguard American interests. Based on 30 years of this experience and my personal knowledge of Pete Hegseth, I have no doubt that he will excel as Secretary of Defense.

Megyn Kelly is joined by The Daily Wire’s Michael Knowles

“The Trump administration, working with Chris Rufo, a new IRS chief, and [attorney general nominee] Pam Bondi, could raise hundreds of billions of dollars merely by enforcing the strict rules and laws pertaining to nonprofit organizations..”

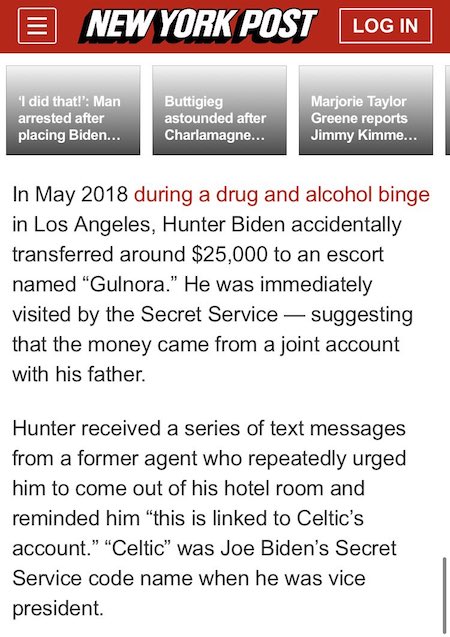

• The Clintons Need Biden’s ‘Blanket Pardons’ More Than Other Democrats (Sp.)

After President Joe Biden issued an unusual blanket pardon for his son, Hunter, Democratic Congressman Ed Markey has urged the president to extend “preemptive pardons” to other top Democrats whom Donald Trump believes “harmed him” and might otherwise be treated by him in a “fascistic way.” “After nearly four years of weaponizing US government resources against perceived enemies of certain dynastic political families, Markey and Biden have some nerve suggesting that the Trump administration will be engaging in ‘fascist’ retaliation starting January 20, 2025,” Wall Street analyst Charles Ortel tells Sputnik, referencing Biden’s prosecution of January 6 protestors and labeling MAGA supporters as “extremists.” US journalist Jonathan Martin reported on December 4 that Biden’s senior aides are debating the issue, and the alleged pardon list might include Sen.-elect Adam Schiff (D-Calif.), former GOP Rep. Liz Cheney, former COVID czar Anthony Fauci.

“The public has yet to learn how deep the rot became across America ever since 1988, when elites embraced unregulated globalism and a turbocharged spoils system where trillions of dollars in spending that is not audited (by design) can be pilfered or diverted to fund political campaigns and multiple-mansion lifestyles,” Ortel says.According to the analyst, the political trajectories of the Biden, Clinton, Bush, Obama, Pelosi, and Cheney dynasty families warrant close scrutiny for alleged influence-peddling and other questionable conduct. “Those who howl loudest now anticipating Trump’s return likely include many with guilty knowledge of their own roles perpetrating a raft of crimes, believing the system will remain rigged to protect them,” he notes. As Joe Biden’s White House reportedly considers “preemptive pardons” for some top Democrats, Ortel suggests that the Clintons might be on the list.

“‘The Clinton Foundation’ (in quotes because I challenge an informed lawyer to demonstrate that it validly and lawfully exists as a public charity) has yet again issued false and materially misleading public filings as it continues to solicit donations in various ways across state lines and national boundaries,” says Ortel, who has conducted a private investigation into the charity’s alleged fraud for several years. In 2018, two forensic investigators-turned-whistleblowers, John Moynihan and Larry Doyle, testified before the US Congress that the Clinton Foundation does not operate as a tax-exempt 501(c)(3) organization but acts as a foreign agent and owes the US government between $400 million and $2.5 billion in taxes. Additionally, Special Counsel John Durham’s probe indicated that Hillary Clinton and her team played a significant role in shaping and promoting the Trump-Russia collusion narrative.

According to Ortel, this hoax was used to prevent Trump from investigating the Clintons’ apparent pay-to-play schemes, mishandling of classified information, and alleged money laundering. “The Trump administration, working with Chris Rufo, a new IRS chief, and [attorney general nominee] Pam Bondi, could raise hundreds of billions of dollars merely by enforcing the strict rules and laws pertaining to nonprofit organizations. Many of these ‘elite’ entities have brazenly abused the law in countless ways, especially the Clintons since October 23, 1997,” Ortel says. “[One] report notes that the Biden family may now have greater exposure since Hunter can no longer readily invoke the Fifth Amendment,” Ortel points out. The Washington Free Beacon reported on December 3 that Hunter will no longer be able to rely on his Fifth Amendment right to silence regarding any potential federal crimes for which he’s been pardoned, according to two former House general counsels.

The Fifth Amendment protects against self-incrimination; however, with Hunter no longer at risk of federal prosecution for the period between January 2014 and December 2024, he appears to be ineligible for this protection. The newspaper alleges that Republican lawmakers should jump at the opportunity to subpoena Hunter Biden for new information about his family’s knowledge or involvement in his apparent influence-peddling schemes. There are a lot of questions concerning the Biden family’s conduct in post-coup Ukraine where Hunter helped secure millions of dollars of funding for Metabiota, a Pentagon bio-reseach contractor, and where he got a hefty salary from Bursima gas firm. “Finally, offering Hunter pardons for federal crimes back to January 1, 2014 raises suspicions that Joe may know of illegal activities in which Hunter engaged, years before crimes alleged in the indictments in the gun (2018) and tax (2019) cases,” Ortel stresses.

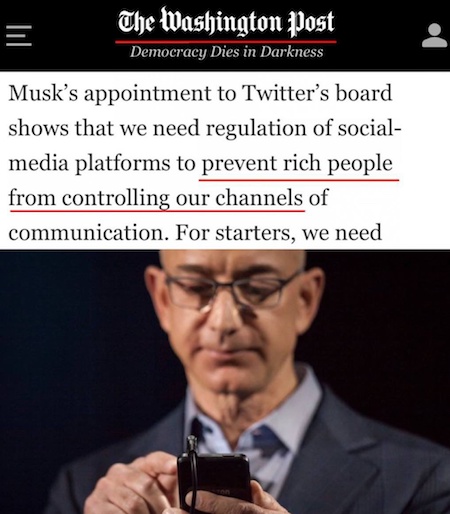

“The value of shares in his electric vehicle company, Tesla, rose by 80% in the past month.”

• Musk Spent $260 Million On Trump (RT)

The world’s richest person, entrepreneur Elon Musk, spent at least $260 million to get Donald Trump re-elected as US president, various media outlets have reported, citing Thursday’s filings with the Federal Election Commission. The Tesla and SpaceX CEO has emerged as a top Republican donor and one of the most prominent members of Trump’s inner circle, noted the Washington Post. Some $238 million of the donations went to a political action committee (PAC) that Musk founded this year, America PAC, CNN said, citing the filings. Other groups backing Trump benefitted as well, with the entrepreneur giving $20.5 million to RBG PAC, and $3 million to the MAHA Alliance.

According to the Washington Post, Musk spent $232 million supporting Trump and other Republican candidates before the election. After the vote and through November 25, he gave nearly $45 million more to America PAC, taking his total political spending to at least $277 million. Following the election victory, Trump appointed Musk as his government efficiency adviser. The entrepreneur will oversee a new Department of Government Efficiency, or DOGE, aimed at cutting government spending. The billionaire has pledged to audit the entire US government, aiming to cut up to $2 trillion in spending.

The entrepreneur’s influence has led to the media and some conservatives dubbing him the “co-president of the United States” and “the Soros of the right,” referring to billionaire investor and prolific liberal donor George Soros. Musk is the world’s richest person, according to the Bloomberg Billionaires Index, with an estimated total net worth of $362 billion as of December 6. The value of shares in his electric vehicle company, Tesla, rose by 80% in the past month. The world’s most valuable carmaker is expected to benefit from streamlined regulation on self-driving cars during the new Trump administration.

This is how rotten the EU is. Secret deals for €35+ billion kept secret. Zero accountability.

“The prosecutor secretly contested the case, arguing that von der Leyen should be immune from prosecution due to her official duties..”

• Prosecutor Blocks Lawsuit Against Ursula von der Leyen Over Pfizergate (Sp.)

A Belgian court was unable to review the charges against European Commission President Ursula von der Leyen due to the intervention of the European Prosecutor’s Office, according to activist and prosecution representative Frédéric Baldan. A lawsuit against European Commission President Ursula von der Leyen has been postponed indefinitely by a Belgian judge. The postponement follows a hearing that took place on Friday at the Liège Palace of Justice, focusing on potential violations in the procurement of coronavirus vaccines by von der Leyen. The hearing was closed to the public and von der Leyen is currently abroad. “The European Prosecutor’s Office made a move that effectively blocked the court proceedings,” Baldan told Sputnik. The prosecutor secretly contested the case, arguing that von der Leyen should be immune from prosecution due to her official duties. As a result, the judge postponed the hearings indefinitely.

The issue of whether von der Leyen’s immunity applies to the charges will be addressed on January 6. Baldan believes the European Prosecutor’s Office acted in her favor. In 2021, The New York Times reported that von der Leyen and Pfizer CEO Albert Bourla exchanged SMS messages discussing a massive vaccine procurement contract. The deal, which could be worth up to €35 billion, raised suspicions about von der Leyen’s direct influence on negotiations, sparking a media scandal dubbed “Pfizergate.” Despite calls to release the text messages, the European Commission refused to make them public in June 2022. In October the same year, the EU’s Public Prosecutor’s Office announced it was investigating the centralized procurement of vaccines on behalf of EU member states, though details remain confidential. Additionally, a separate investigation was launched in Belgium after Baldan filed a lawsuit against von der Leyen, claiming her actions caused economic harm to the country.

In March 2024, it was reported that the case had been transferred to the European Public Prosecutor’s Office, which confirmed it is continuing its investigation, though it refused to disclose further details. The European Court of Justice in Luxembourg is also reviewing a complaint filed by The New York Times, which had requested von der Leyen’s communications with Pfizer but was denied access. The European Commission argued that these messages were not official documents and could not be retrieved. A ruling is expected in the coming months. During the pandemic, the European Union mainly purchased vaccines from the BioNTech-Pfizer consortium, along with other pharmaceutical companies. These procurements, involving billions of euros, have been the subject of ongoing scrutiny and legal disputes due to delays in supply and lack of transparency.

Oreshnik = no nukes needed.

• How Russia Plans To Win In Ukraine (Dmitry Trenin)

The Ukrainian crisis exposed a troubling reality for Russia: its concept of strategic deterrence proved incapable of preventing enemy aggression. While it has successfully deterred a massive nuclear attack by the United States or large-scale conventional aggression by NATO, it has failed to address a new and insidious form of conflict. Washington and its allies have gambled on inflicting a strategic defeat on Russia through a client state—one they control, arm, and direct. Moscow’s nuclear doctrine, designed for a very different set of circumstances, proved inadequate. It failed to prevent Western intervention at the outset and allowed its escalation. In response, the Kremlin has recognized the need to adapt. In the third year of the operation, a long-overdue update to the doctrine has been announced. This summer, President Vladimir Putin outlined the necessary changes.

By November, the new document—entitled Fundamentals of the State Policy of the Russian Federation in the Field of Nuclear Deterrence—was in place. The updated doctrine represents a profound shift in Russia’s nuclear policy, transforming it into a proactive deterrent. Previously, nuclear weapons could only be used in conventional conflicts when the very existence of the state was at risk. The threshold was set so high that it effectively allowed adversaries to exploit it. Now, the conditions have been broadened significantly. One key addition is the recognition of “joint aggression.” If a non-nuclear state at war with Russia operates with the direct support of a nuclear power, Moscow reserves the right to respond, including with nuclear weapons. This sends a clear and unmistakable message to the United States, Britain, and France: their facilities and territories are no longer immune to retaliation.

The doctrine also explicitly accounts for scenarios involving massive aerospace attacks, including drones and cruise missiles, as well as aggression against Belarus. Another important change is the expanded list of threats deemed unacceptable to Russia’s security. These changes collectively signal a more assertive posture, reflecting the reality of today’s conflict and deterring potential Western miscalculations. Western reactions to these updates were predictable. Media hysteria painted Putin as reckless, while politicians feigned calm, claiming they would “not be intimidated.” The military and intelligence communities have remained largely silent, quietly drawing their own conclusions. These updates come against an increasingly grim backdrop for the West. Realists within NATO understand the war in Ukraine is effectively lost. The Russian army holds the initiative across the front and is advancing steadily in the Donbass.

The Ukrainian armed forces are unlikely to turn the tide in the foreseeable future, if ever. Consequently, Western strategists are now eyeing a ceasefire along the battle lines as the only viable option. Notably, there has been a subtle shift in the narrative. Articles in Reuters and other Western outlets suggest that Moscow, too, may consider freezing the conflict. However, such a scenario would need to align with Russian interests. For Moscow, anything less than full victory equates to defeat, and such an outcome is simply not an option. The administration of US President Joe Biden, despite the Democrats crushing election defeat, has apparently decided to ‘help’ Donald Trump stay on course. The authorization to use US and British long-range missiles to hit targets in the Kursk and Bryansk regions is both a defiant challenge to Putin, and a ‘gift’ to the president-elect.

Likewise the transfer to Kiev of anti-personnel mines banned by the Ottawa Convention, a new batch of anti-Russian sanctions (including against Gazprombank) and an attempt to ‘push’ the latest Biden aid package for Zelensky through Congress. Russia’s response to the escalation has not been limited to updating its doctrine. The recent test of the ‘Oreshnik’ intermediate-range hypersonic missile under combat conditions marked a pivotal moment. By striking the Yuzhmash missile factory in Dnepropetrovsk, Moscow signaled to NATO that the vast majority of its European capitals are within range of this new weapon. ‘Oreshnik’ carries both conventional and nuclear warheads, and its speed — reportedly reaching up to Mach 10 — renders existing missile defense systems ineffective. Although still experimental, its successful deployment paves the way for mass production. The message is clear: Moscow is not bluffing. This shift from verbal warnings to decisive actions underscores the seriousness of the Kremlin’s resolve.

The West has long convinced itself that Putin would never strike NATO countries. With the advent of ‘Oreshnik,’ that belief has been shattered. The United States and its allies continue to escalate recklessly, betting on provoking a Russian overreaction. The authorization of long-range missile strikes on Russian territories like Kursk and Bryansk, combined with the transfer of banned weapons and the constant drumbeat of sanctions, reflects their desperation. More dangerously, there are whispers of Ukraine’s potential NATO membership or even the transfer of nuclear weapons to Kiev. While the latter remains unlikely, the risk of a “dirty bomb” cannot be ruled out. The West’s hope, however, is that Russia might strike first with atomic weapons, handing NATO the moral high ground. Such an outcome would allow Washington to isolate Moscow globally, undermining its relationships with key players like China, India, and Brazil. Yet Moscow has countered these provocations with calculated precision, refusing to take the bait.

Blinken: “Getting younger people into the fight, we think, many of us think, is necessary..”

Putin: [Zelensky] has “no right to push people to their death and drive them into battle.” The orders that Zelensky gives are “criminal..”

• Teenagers Preparing To Flee Ukraine – The Times (RT)

Many Ukrainian teenagers are planning to leave the country and never return as the US increases pressure on Kiev to lower the mobilization age, the Times has reported. Earlier this week, outgoing US Secretary of State Anthony Blinken said it was not right that “18 to 25-year-olds are not in the fight” against Russia. “Getting younger people into the fight, we think, many of us think, is necessary,” he stressed.In an article on Thursday, the British paper quoted a teenager from the city of Kharkov, who said that “many” of his friends are now choosing to study abroad because “it is safer there.”“There is no risk of being taken into the army at a foreign university,” he explained, adding that he plans to study in Poland, and may not return after graduation.

“When I have finished, I will decide whether to return to Ukraine or stay there. It will be safer there, there are no bombs falling and there is no danger that I will be mobilized for the war without my consent,” he said. Another teenager who spoke to The Times said he also wants to attend higher education in a foreign country. Ukrainian lawmaker Aleksandra Ustinova told the paper that a decision to lower the mobilization age to 18 would be met with “huge opposition inside Ukraine and we would not get the results [on the battlefield] that we want because this is not such a large amount of people.”“It would also be a clear signal for families to get their children out. So, if we want to lose our future generation, then, yeah, this is the thing to do,” Ustinova stressed.

The number of men aged between 18 and 25 in Ukraine is estimated to be at least 300,000.According to UN data, at least 6.8 million Ukrainians have fled the country and become refugees since the escalation between Moscow and Kiev in February 2022. Most of them are women and children, as men of fighting age are banned from travelling abroad.Since the start of the conflict, officials in Moscow have repeatedly accused the US and its allies of wanting “to fight to the last Ukrainian” in their effort to inflict a strategic defeat on Russia. Russian President Vladimir Putin said last week that Ukrainian leader Vladimir Zelensky, who canceled a presidential election earlier this year, has “no right to push people to their death and drive them into battle.” The orders that Zelensky gives are “criminal,” Putin stressed.

“..a Final Confrontation – with several overtones ranging from expanding lebensraum to provoking the Apocalypse.”

• The Syria Tragedy and the New Omni-War (Pepe Escobar)

Until recently, a serious geopolitical working hypothesis was that West Asia and Ukraine were two vectors of the standard Hegemon modus operandi, which is to incite and unleash Forever Wars. Now both wars are united in an Omni-War. A coalition of Straussian neo-cons in the US, hardcore revisionist Zionists in Tel Aviv and Ukrainian neo-nazi shades of grey is now betting on a Final Confrontation – with several overtones ranging from expanding lebensraum to provoking the Apocalypse. What stands in their way is essentially two of the top BRICS: Russia and Iran. China, self-protected by their collective lofty dream of “community of a shared future for mankind”, warily watches on the sidelines, as they know that at the end of the road, the true “existential” war by the Hegemon will be against them. Meanwhile, Russia and Iran need to mobilize for Totalen Krieg. Because that’s what the enemy is launching.

The total destabilisation of Syria, with heavy CIA-MI6 input, now proceeding in real time, is a carefully engineered gambit to undermine BRICS and beyond. It proceeds in parallel to Pashinyan removing Armenia from the CSTO – based on a US promise to support Yerevan in a possible new clash with Baku; India being encouraged to ramp up a weapons race with Pakistan; and across-the-board intimidation of Iran. So this is also a war to destabilize the International North South Transportation Corridor (INSTC), of which the three major protagonists are BRICS members Russia, Iran and India. As it stands, the INSTC is totally geopolitical risk-free. As a top BRICS corridor-in-the-making, it carries the potential to become even more effective than several of China’s cross-Heartland corridors of the Belt and Road Initiative (BRI).

The INSTC would be a key lifeline for a great deal of the global economy in case of a direct confrontation between the US/Israel combo and Iran – with the possible shutdown of the Strait of Hormuz leading to the collapse of a multi-quadrillion pile of financial derivatives, economically imploding the collective West. Turkiye under Erdogan, as usual, is playing a double game. Rhetorically, Ankara stands by a genocide-free and sovereign Palestine. In practice, the Turkiye supports and funds a motley crew of Greater Idlibistan jihadis – trained by Ukrainian Neo-nazis in drone warfare and with weapons financed by Qatar – who have just marched on and conquered Aleppo, Hama, and possibly beyond. If this army of mercenaries were real followers of Islam, they would be marching in defense of Palestine.

At the same time, the real picture inside the corridors of power in Tehran is extremely murky. There are factions favoring getting closer to the West, which clearly would have ramifications for the Axis of Resistance’s ability to fight Tel Aviv. On Lebanon, Syria never wavered. History explains why: from the point of view of Damascus, Lebanon historically remains a governorate, so Damascus is responsible for the security of Beirut. And that’s one of Tel Aviv’s key motives to propel the current Salafi-jihadi offensive on Syria – after smashing virtually every communication corridor between Syria and Lebanon. What Tel Aviv could not accomplish on the ground – a victory over Hezbollah in southern Lebanon – has been replaced by isolating Hezbollah from the Axis of Resistance.

Wars in West Asia are a complex mix of national, sectarian, tribal and religious vectors. In a sense, they are endless wars; controllable to an extent, but then back again. The Russian strategy in Syria seemed to be very precise. As it was impossible to normalize a completely fragmented nation, Moscow opted to free the Syria that really matters – the capital, the most important cities, and the Eastern Mediterranean coast – from the Salafi-jihadi mobs. The problem is that freezing the war in 2020, with direct implication by Russia, Iran and (reluctantly) Turkiye, did not solve the “moderate rebel” problem. Now they’re back – in full force, supported by a vast Rent-a-Jihadi mob, with NATOstan Intel behind them. Some things never change.

Too late now?!

• Russia Warns Against Geopolitical Use of Terrorists in Syria’s Conflict (Sp.)

The offensive by the Hayat Tahrir al-Sham (HTS)* terrorist group in Syria has been long in the making, and Russia will oppose attempts by the militants to alter the situation in the Syrian Arab Republic (SAR), Russian Foreign Minister Sergey Lavrov said. Moscow has called for restraint from all parties in the unraveling conflict in Syria. “The situation has sharply escalated in recent days due to the clearly premeditated aggressive offensive on government forces by Hayat Tahrir al-Sham (former Al-Nusra Front*), an organization designated by the UN Security Council as a terrorist group, which has been joined by several smaller factions,” Lavrov said during a press conference following his visit to Doha. He emphasized the urgent need to stop the hostilities and said that Russia would actively oppose any attempts by HTS militants to change the situation on the ground in Syria.

“We are absolutely convinced of the inadmissibility of using terrorists like Hayat Tahrir al-Sham to achieve geopolitical goals, as is happening now with the organization of this offensive from the Idlib de-escalation zone,” Lavrov explained during a session at the Doha Forum. The main task now in the situation surrounding Syria, according to Lavrov, is to halt the clashes. UN Special Envoy for Syria Geir Pedersen has promised to involve influential external actors to stop the fighting and resume negotiations between the government and opposition, Lavrov added. The top Russian diplomat also reiterated Moscow’s efforts to counteract terrorism in Syria: “We are doing everything to prevent terrorists from gaining the upper hand, even if they claim that they are no longer terrorists.” “On the military front, Russia is helping the Syrian army with support from the [Russian Aerospace Forces], based in Khmeimim, and we assist the Syrian army in repelling terrorist attacks,” he added.

Additionally, Lavrov stated that Russia, along with Iran and Turkiye, will take steps to ensure that calls for de-escalation in Syria are heard. The terrorist group Hayat Tahrir al-Sham, along with several armed factions from the so-called Syrian armed opposition, launched a large-scale operation on November 29, advancing from northern Idlib towards the cities of Aleppo and Hama. By the following day, November 30, the second-largest city in Syria, Aleppo, along with its surroundings, including the international airport and the Kuweires military airbase, came under the control of the terrorists. This marked the first time that the militants had fully taken over Aleppo since the beginning of the Syrian crisis in 2011. Until late 2016, the armed opposition controlled only the eastern part of the city, which was recaptured by the Syrian army with Russian air support.

After the capture of Aleppo, the terrorist units attempted to advance towards the city of Hama, capturing the town of Maaret al-Numan. The Syrian army fought off heavy terrorist attacks in the Hama province from three directions for several days, preparing for a counteroffensive. However, on December 5, the SAR military command officially announced the redeployment of its units from the city of Hama. The city of Hama, located in central Syria, has been under the control of the Syrian army throughout the conflict, which began in the spring of 2011. Hama holds strategic geographic importance, lying between the provinces of Homs and Damascus and connecting through mountain ranges to the Latakia province. The last attempt at an armed insurgency by radical Islamist underground forces, supported by the Muslim Brotherhood*, in Syria’s fourth-largest city took place in 1982. At that time, thanks to prompt action by the Syrian military command, the city was freed from terrorist groups, and control was restored to official authorities.

They must have known what would happen.

• Russia, Iran Call For ‘Internal Dialogue’ To Resolve Crisis In Syria (Cradle)

The Foreign Ministers of Russia, Turkiye, and Iran on 7 December called for an immediate end to hostilities in Syria and for ‘”internal dialogue” between the Syrian government and the “legitimate opposition.” “We called for an immediate end to hostile activities … and for this purpose called for the dialogue between the government and legitimate opposition,” Russian Foreign Minister Sergei Lavrov stated during talks in the Qatari capital, Doha. “We stated, all of us, that we want the [United Nations] Resolution 2254 to be fully implemented,” Lavrov added. Resolution 2254 calls for a commitment to the “sovereignty, independence, unity and territorial integrity” of Syria and an end to the conflict through “an inclusive and Syrian-led political process.” Lavrov did not specify which opposition forces Russia regarded as legitimate but made clear it considered Hayat Tahrir al-Sham (HTS) a terrorist group.

HTS is led by Abu Mohammad al-Julani, a former deputy of the notorious ISIS leader Abu Bakr al-Baghdadi. Formerly known as the Nusra Front, HTS now claims it is no longer a sectarian Salafi-Jihadi group and welcomes ethnic and religious diversity in Syria. Western media is now promoting HTS, which includes many foreign fighters and remains on the US terror list, as moderates that will protect Syria’s religious minorities. During the US-led covert war on Syria that began in 2011, the Nusra Front and ISIS carried out large numbers of massacres of Christians, Shiites, Alawites, Yezidis, and even Sunnis who were supportive of the governments of Iraq and Syria. HTS and the Turkish-backed Syrian National Army (SNA) launched an invasion of the Aleppo countryside on 27 November. In the past ten days, they have captured two of Syria’s largest cities, Aleppo and Hama.

HTS and SNA militants are now gathering their forces at the edge of Homs City in preparation for an assault. In Doha, Foreign Minister Lavrov stated further, “It’s inadmissible to allow the terrorist group to take control of territory in violation of agreements.” Asked how the situation in Syria would develop and what would happen to Russian military bases there, Lavrov said he was “not in the business of guessing.”

Russia has an airbase in Latakia and a key naval base in Tartous. Iranian Foreign Minister Abbas Araghchi similarly called for “political dialogue” between the Syrian government and the “opposition groups” that are now threatening Damascus. Araghchi said that the parties in Doha agreed to initiate “political dialogue between the Syrian government and the legitimate opposition groups.” For its part, a Turkish foreign ministry source emphasized the importance of restarting the Syrian political process during the talks with Russia and Iran in Doha. The source added that the talks were constructive.

He’s right. Exposing the real EU.

• Romanian Presidential Frontrunner Claims He’s Victim Of Coup D’état (RT)

The invalidation of Romania’s presidential election results by the country’s top court is a formalized coup d’etat, according to independent candidate Calin Georgescu, who clinched a surprise win in the first round last month. Georgescu outperformed the other candidates in the first round of the election with 22.94%, beating out liberal leftist candidate Elena Lasconi, who received 19.18%, and the country’s Social Democrat Prime Minister Marcel Ciolacu, who finished third with 19.15%. On Friday, Romania’s Constitutional Court dismissed Georgescu’s victory, citing a clause in the nation’s laws that emphasizes the need to ensure the correctness and legality of the election. The judiciary body announced that the whole process would be resumed later.

“Essentially, this is a formalized coup d’etat. The rule of law is in an induced coma, and justice subordinated to political orders has practically lost its essence. It is no longer justice, it obeys the orders,” Georgescu, a known critic of Romania’s pro-NATO and pro-Ukraine policy, said on Friday, as cited by Realitatea TV. The politician also stressed that the court’s decision represents more than a legal controversy, adding that “the corrupt system in Romania showed its true face by making a pact with the devil.” Georgescu also said that the power of the people is the basis for a democratic state, and the authorities are obliged to respect the results of the national vote. He stated that the current Romanian government is afraid of losing power and facing revelations.

Earlier this week, Western media outlets reported that declassified information from Romania’s intelligence agencies had revealed that the sudden rise of Georgescu in the first round of the election was “not a natural outcome.” According to the claims, his win emerged thanks to a coordinated social media effort, most likely orchestrated by a “state actor” meddling in the candidate’s mostly Tik-Tok-based campaign, helping to get his message out to the voters. The annulment came amid accusations that Moscow had assisted Georgescu’s campaign, which Russian Foreign Ministry spokeswoman Maria Zakharova has dismissed as “absolutely groundless.” She said that Romanian elections are carried out in a climate of “an unprecedented surge of anti-Russian hysteria” that is set “to influence the consciousness and will of the country’s citizens.” Washington, meanwhile, has praised the move. On Friday, State Department spokesman Matthew Miller said that the US reaffirms its “confidence in Romania’s democratic institutions and processes, including investigations into foreign malign influence.”

Calin

Calin Georgescu opposes the satanic elites in Europe with tremendous bravery. He was overwhelmingly winning in the presidential elections of Romania. Then the corrupt regime cancelled the elections and surrounded his home with police, threatening to arrest him. When international… pic.twitter.com/Y3q45BUQ3j

— StopWorldControl.com (@davidjsorensen) December 6, 2024

“It’s an epic battle of light and darkness, Hobbits and Orcs, almost as if lifted straight from a fantasy novel..”

• France Is A Perfect Example Of Centrist Elites Wrecking The West (Amar)

In the most immediate terms, Macron’s reckless early-election gamble in the summer and his devious and undemocratic maneuvering to keep out the victorious Left after his party’s predictable trouncing, has left France, in effect, ungovernable. Barnier’s predictable failure makes no difference to that fact. Fresh parliamentary elections, once again, would probably not help either. And anyhow, they are ruled out by the constitution before next summer. Macron will now try out yet another prime minister, number six since he became president. That is a high attrition rate: In 7 years, the would-be embodiment of “institutional stability” has gone through as many heads of government as De Gaulle in 19 years. It’s also an accelerating attrition rate: Macron’s prime ministers get used up ever faster. The future will show if this trend can be broken. If so, then not because of but despite the president’s baneful influence.

As a French commentator noted, he won’t provide a solution, but he can still cause a lot of problems. There are good reasons for declaring this moment the death of Macronism. Its core project of leaving behind the politics of left and right and replacing them with a combination of Centrism and a “Jupiterian” (Macron’s own, early term) personality cult now lies in tatters. Specifically, Macronism’s claim to, at the very least, stave off the populist right of Marine Le Pen’s Rassemblement National (RN) is a sad joke: No matter what you think about the RN, there is no doubt that its power has never been as great as now, and its chances of capturing the presidency, with or without Marine Le Pen in the lead, have never been better. Macron has become the Biden of France: in both cases, while building their rule on a promise to keep out right-populist challengers, the two presidents’ incompetence and egotism has facilitated the rise of those challengers.

And how do the French feel in the midst of all of this? Spoiler alert: Not grand. According to French newspaper Le Monde’s summary of comprehensive polling by Ipsos, France is a “country anxious and discontent, hit by a political crisis,” and bereft of trust in its “political personnel and institutions.” In terms of their individual experiences, only 50% are content, 70% believe that the conditions of their life are “less and less favorable,” and 55% say they find it hard to make ends meet. Regarding their country as a whole, a whopping 87% consider it in decline, which is 18% worse than when Macron was elected for the first time in 2017: National slow claps for “Jupiter.” But the rest of the political elites don’t look much better: Solid, even preponderant majorities consider them “corrupt” (63%), “not representative” (78%), and out for their own, personal good (83%).

In principle, there’s a difference between being miserable and being afraid. But the two states of mind go together really well, too: Almost all of the French (92%) have a bad feeling they are living in a “violent society”, and almost a third think “very violent” is the more precise term. You may say things could hardly get worse. Yet the French firmly believe they can: 89% see violence on the rise, and the majority of those respondents (61%) think it is rising “a lot.” In sum: A selfish boss from hell (who could fire himself but swears he won’t), no functioning government, a tanking economy, and a mood like there’s no tomorrow. How did that happen to the “Grande Nation”? This is where we get back to the third factor mentioned above: the overarching historic trend. Let’s zoom out from unhappy France and small-minded, selfish Macron, and what we are seeing is an exemplary case of Centrism ruining a country.

True, you would never guess that if you relied on, for instance, The Economist. There, the same old, tired, and dim story is relentlessly told: How a heroic “center” and its stalwart defenders are resisting (or not so much) dastardly attacks from the “populists” and “extremists.” It’s an epic battle of light and darkness, Hobbits and Orcs, almost as if lifted straight from a fantasy novel. It even features glorious last stands: For the New York Times, Britain’s Keir Starmer, “one of the last centrist leaders on the global stage” is “trying to fight populism from the lonely center.” “Remember the Alamo,” I guess.

And yet, look at the real world: Clinton, Biden, Harris, Scholz, Macron, to name only a few – What do they all have in common? They stand for the failed, rejected project of elitist Centrism, dragging down their countries. For a stubborn, snobbish, and manipulative style of politics, complete with lawfare, mass media campaigns of calumny and disinformation, incipient authoritarianism and police-state methods, a dead-end foreign policy of blaming others (Russia and China most of all) for their countries’ problems and decline, and a resolute surrender to the forces of “the market,” which, here, is simply code for globalized capitalist interests.

1/ Pop=Joe.

2/ Pop goes the value.

• Pop Art: The Value of Hunter Biden’s Art Expected to Collapse (Turley)

We have previously discussed the controversy surrounding Hunter Biden’s art sales. Many viewed the art as another avenue for political allies to funnel money to the Bidens. That was reinforced when it was discovered that the lucrative sales heralded by Hunter’s allies were found to have been largely the results of purchases by his “sugar bro” Kevin Morris. Now, experts say that whatever value is left in Hunter’s art will likely collapse with his father’s departure — the clearest indicator of the actual value of the art for “investors.” Hunter’s art appears to be moving from an impressionistic to a harsh realism period. Georges Bergès, Hunter Biden’s art gallerist, contradicted claims of the White House on the handling of the art. Hunter reportedly knew who purchased roughly 70% of the value of his art, including Democrat donors Morris and Elizabeth Hirsh Naftali.

While Biden allies hyped the sales to show that Hunter was a legitimate artist, Bergès admitted that Morris actually purchased most of the art. Morris has reportedly given Hunter millions to cover unpaid taxes and expenses. Hunter only sold paintings to ten people for $1.5 million, according to congressional testimony from 2024. Morris bought 11 works for $875,000 in total. The drop in the value of art reflects not the volatile art market but the fluctuating influence peddling market. The Bidens are finally cashing out of Washington. In the meantime, Hunter is facing a bizarre claim from one of his debt holders that, in return for allegedly walking out on over a year of rent, Hunter sent him art made with his own feces to sell. Shaun Maguire claims that Hunter rented his $4.25 million home in California in 2019. When Hunter’s lawyers denied the story, he posted pictures on social media.

Without getting into the merits of this claim, the question is whether Hunter will sue for defamation. I was previously threatened with a defamation lawsuit for discussing the scandal involving Morris. I continued to write about the allegations (and the threat of a lawsuit) but was never sued. It was an example of the scorched Earth approach of the Hunter team. This is such a bizarre story that it is hard to imagine that it could be true. Conversely, Maguire must have known of the litigious reputation of the Biden team when he decided to go public with this claim. If this story is untrue, it could constitute defamation per se as a statement that impugns his professional and business reputation. A simple testing of the art would tend to establish the truth of the matter. However, there is no indication of any demand for a retraction or notice to sue. Hunter generally has two years for such a lawsuit, but California has a shorter one-year period.

In the meantime, Hunter has pledged to continue to do his art after his father granted him a sweeping pardon for any crimes committed in the last ten years. Given his past excessive spending on a lavish lifestyle, the art alone does not appear to be a viable source of income. However, Morris has helped create a new movie based on his life. Hunter reportedly celebrated the pardon by watching an early showing of the film. In the end, Hunter’s work may be the ultimate Pop art, work that only holds value so long as Pop is in power. Of course, if Nietzsche was right that “the essence of all beautiful art…is gratitude,” Hunter has much to be grateful for. For past and prospective buyers, perhaps less so.

Regretting his French passport more than ever…

• Durov Subjected To First Detailed Questioning In Court (RT)

Telegram founder Pavel Durov has been questioned by a Paris court for the first time on the charges against him, more than three months after his arrest, AFP news agency reported on Friday, citing an unnamed source. Previous court hearings had focused on procedural issues relating to the terms of the tech billionaire’s detention. The charges against Durov relate to the alleged involvement of the messaging platform in a wide range of criminal activities. Durov reportedly arrived at the court accompanied by two lawyers, David-Olivier Kaminski and Christophe Ingrain. The entrepreneur said he “trusts French justice,” but refused to comment on the progress of the case or the charges against him. The Russian national, who is also a citizen of France, the UAE and Saint Kitts and Nevis, was arrested after landing in Paris on August 24.

Durov was charged with multiple offenses, including complicity in distributing child pornography, and enabling drug dealing and money laundering. The charges stem from accusations that Telegram’s lax moderation rules allow for the widespread misuse of the messenger service. The billionaire was later released on bail of €5 million ($5.5 million), but has been barred from leaving France while his case is ongoing. Some of the charges against him could carry sentences of up to ten years. Durov has vehemently denied the allegations. In October, the entrepreneur revealed that the messenger service had been complying with privacy policies in several countries, and had been disclosing information about criminals to authorities for the past six years.

According to one of Durov’s lawyers, as cited by the French news agency, it was “absurd” to think that his client was “involved” in crimes committed via the messaging platform. An unnamed source close to the investigation told AFP that the entire legal procedure was having a positive effect in France and elsewhere, as Telegram has begun responding to legal requisitions more actively. Commenting in August on Durov’s detention, Kremlin spokesman Dmitry Peskov highlighted the absurdity of holding the entrepreneur accountable for crimes committed using his network. Peskov quipped that Paris could use the same grounds to arrest the CEOs of Renault or Citroën, as terrorists use cars.

McCullough RFK

Senate Confirmation Hearings on Robert F. Kennedy, Jr, for Secretary of Health and Human Services will be Like David versus Goliath

Corrupt BIG FOOD, BIG PHARMA, former @US_FDA Commissioner @pfizer Gottlieb all lobbying to senators to sink the nomination. Dr. McCullough on… pic.twitter.com/JY92v7i3O4

— Peter A. McCullough, MD, MPH® (@P_McCulloughMD) December 7, 2024

Cancer

https://twitter.com/i/status/1865082844680175821

AOC

https://twitter.com/i/status/1865215257943146917

Sand cat

Meet the sand cat (Felis margarita), a small wild cat that inhabits sandy and stony deserts far from water sources.pic.twitter.com/EBB5Sfgdfi

— Massimo (@Rainmaker1973) December 7, 2024

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.