Russell Lee Saloon, Craigville, Minnesota Aug 1937

PM Abe and the BOJ are panicking big time. Japan debt is already well over 400% of GDP, and nothing they have done has had any positive effect other than those they’ve made up. It’s a matter of when, not if. Expect ugly.

• Kuroda Jolts Markets With Assault on Deflation Mindset (Bloomberg)

Today’s decision to expand Japan’s monetary stimulus may be regarded as shock treatment in the central bank’s effort to affect confidence levels. Bank of Japan Governor Haruhiko Kuroda’s remedy to reflate the world’s third-largest economy through influencing expectations saw the yen sliding and stocks climbing. Kuroda led a divided board in Tokyo in a surprise decision to expand unprecedented monetary stimulus. Bank officials hadn’t provided any hints in recent weeks that additional easing was on the cards to help reach the BOJ’s inflation goal. Kuroda, 70, repeatedly indicated confidence this month that Japan was on a path to reaching his 2% target in the coming fiscal year. Just three of 32 economists surveyed by Bloomberg News predicted extra easing. “We have to admit that this is sort of a second shock – after we had the first shock in April last year,” said Masaaki Kanno, chief Japan economist at JPMorgan Chase, referring to the first round of stimulus rolled out by Kuroda in 2013.

Kanno, who used to work at the BOJ, said “this is very effective,” especially because it comes the same day as the government pension fund said it will buy more of the nation’s stocks. The BOJ chief, a former Finance Ministry bureaucrat who at one time was in charge of currency affairs, had repeatedly said that the central bank wouldn’t hesitate to expand asset buying if necessary. At the same time, his public confidence in Japan being on a path to reach the inflation target left the idea that no stimulus was coming today, Kanno said. “Kuroda loves a surprise – Kuroda doesn’t care about common sense, all he cares about is meeting the price target,” said Naomi Muguruma, a Tokyo-based economist at Mitsubishi UFJ Morgan Stanley Securities Co., who correctly forecast more stimulus today. “Kuroda knows that when he moves it must be big and surprising.” The BOJ is aiming to pre-empt any risk of a delay in ending Japan’s “deflationary mindset,” it said in today’s policy statement. Kuroda later told reporters that surprising the markets wasn’t his intention.

Read more …

And the Japanese are still not spending, so inflation can’t and won’t rise. The Nikkei may have gained 5%, but the people in the street only got even more scared and prudent.

• Kuroda Surprises Again With Stimulus Boost as Japan Struggles (Bloomberg)

Bank of Japan Governor Haruhiko Kuroda led a divided board to expand what was already an unprecedentedly large monetary-stimulus program, boosting stocks and sending the yen tumbling. Kuroda, 70, and four of his eight fellow board members voted to raise the BOJ’s annual target for enlarging the monetary base to 80 trillion yen ($724 billion), up from 60 to 70 trillion yen, the central bank said in Tokyo. An increase was foreseen by just three of 32 analysts surveyed by Bloomberg News. The BOJ also cut its forecasts for consumer prices. Facing projections for failure to reach the BOJ’s 2% inflation target in about two years, and with the economy under pressure from a higher sales tax, enlarging the stimulus at some point had been anticipated by analysts for months. Kuroda opted not to telegraph his intentions in recent weeks, leaving today’s move a surprise – sending the Nikkei 225 Stock Average to the highest level since 2007.

“It was great timing for Kuroda,” said Takeshi Minami, Tokyo-based chief economist at Norinchukin Research Institute, one of two who correctly forecast today’s easing. Minami noted that it follows the Federal Reserve’s ending of quantitative easing, helping highlight the differing paths for the U.S. and Japan. Today’s decision comes almost 19 months after Kuroda unleashed his initial asset-purchase plan, with the intention of doubling the monetary base. That move similarly drove up stocks and undercut the yen. Since then, a more competitive exchange rate has triggered higher corporate earnings, and asset-price gains have expanded Japanese households’ net worth. The bank will purchase exchange-traded funds so their amounts outstanding increase by about 3 trillion yen a year, it said. Japanese real estate investment trusts will be purchased with a view to raising their amounts outstanding by about 90 billion yen annually, according to the bank.

Read more …

Down 5% again on Monday?

• Japan Stocks Soar To 7-Year High On BOJ, Pension Fund Boost (Bloomberg)

Japanese stocks soared, with the Nikkei 225 Stock Average closing at a seven-year high, as the Bank of Japan unexpectedly boosted easing and the nation’s pension fund prepared to unveil new asset allocations. The Nikkei 225 jumped 4.8% to 16,413.76 at the close in Tokyo, the highest since Nov. 2, 2007. The Topix index surged 4.3% to 1,333.64, bringing its gain for the week to 7.4%, the most since April 2013. The measure erased its losses for the year and is now up 2.4%. Volume on both gauges was more than 75% higher than their 30-day averages. The yen tumbled 1.5% to 110.83 per dollar.

Shares rose in the morning session after a Nikkei newspaper report that the $1.2 trillion Government Pension Investment Fund would announce new portfolio targets today, more than doubling its goal for domestic shares to 25% of assets. They surged in the afternoon after BOJ policy makers voted 5-4 to target an 80 trillion yen ($726 billion) annual expansion in the central bank’s monetary base. “Today you’re getting a double boost with talk of the GPIF increasing its shares allocation and the BOJ pumping more cash in at a faster rate,” Shane Oliver, head of investment strategy at AMP Capital Investors, which manages about $125 billion, said by phone. “It had become increasingly apparent that what the BOJ was doing wasn’t enough and they needed to do more, and it’s always been a question of when they would do that. It’s an excellent outcome.”

Read more …

” … the “Euroglut”, the largest surplus in the history of financial markets.”

• US And China Tighten In Unison, And Damn The Torpedoes (AEP)

Mind the monetary gap as the world’s two superpowers turn off the liquidity spigot at the same time. The US Federal Reserve and the People’s Bank of China have both withdrawn from the global bond markets, each for their own entirely different reasons. The combined effect is a shock of sorts for the international financial system. The Fed’s message on Wednesday night was hawkish. It did not invoke the excuse of a stronger dollar or global market jitters to extened bond purchases. It no longer sees “significant” constraints to the labour market. Instead it spoke of “solid job gains” and a “gradual diminishing” of under-employment. This a tightening shift, and seen as such by the markets. The euro dropped 1.5 cents against a resurgent dollar within minutes of the release, falling back below $1.26. Rate rises are on track for mid-2015 after all. The Fed is no longer printing any more money to buy Treasuries, and therefore is not injecting further dollars into an interlinked global system that has racked up $7 trillion of cross-border bank debt in dollars and a further $2 trillion in emerging market bonds.

The stock of QE remains the same. The flow has changed. Flow matters. The Fed has ended QE3 more gently than QE1 or QE2. This helps but it may also have given people a false sense of security. The hard fact is that the Fed has tapered net stimulus from $85bn a month to zero since the start of the year. The FOMC tried to soften the blow in its statement with pledges to keep interest rates low for a very long time. This assurance has value only if you think QE works by holding down interest rates, as the Yellen Fed professes to believe. It cuts no ice if you are a classical monetarist and think that QE works its magic through the quantity of money effect, most potently by boosting broad M3/M4 money through purchases of assets outside the banking system. Pessimists argue that the world economy is so weak that it needs a minimum of $85bn a month of Fed money creation (not to be confused with zero interest rates) just to avoid stalling again.

Or put another way, there is nagging worry that tapering itself may amount to an entire tightening cycle, equivalent to a series of rate rises in the old days. If they are right, rates may never in fact rise above zero in the US or the G10 states before the global economy slides into the next downturn. It is no great mystery why the world is caught in this “liquidity trap”, or “secular stagnation” if you prefer. Fixed capital investment in China is still running at $5 trillion a year, and still overloading the world with excess capacity in everything from solar panels to steel and ships, even after Xi Jinping’s Third Plenum reforms. Europe has been starving the world of demand by tightening fiscal policy into a depression, running a $400bn current account surplus that is now big enough to distort the global system as a whole. George Saravelos, at Deutsche Bank, dubs it the “Euroglut”, the largest surplus in the history of financial markets.

Read more …

Scary situation.

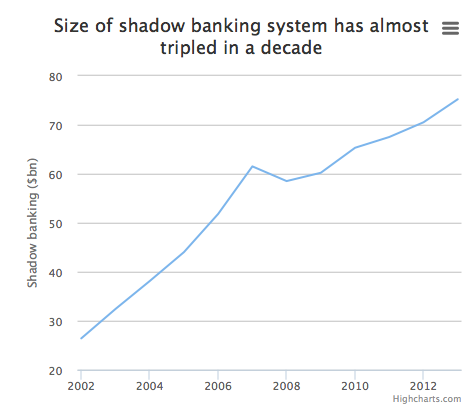

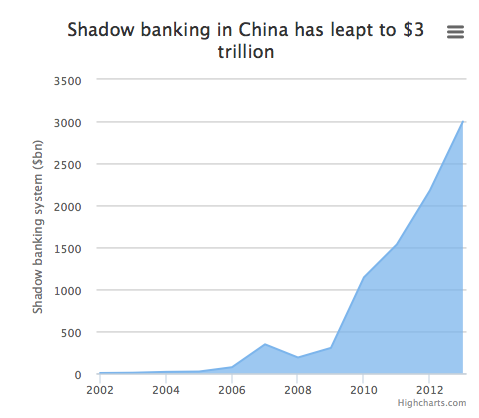

• Shadow Banking Grows to $75 Trillion Industry (Bloomberg)

The shadow banking industry grew by $5 trillion to about $75 trillion worldwide last year, driven by lenders seeking to skirt regulations and investors searching for yield amid record low interest rates. The size of the shadow banking system, which includes hedge funds, real estate investment trusts and off-balance sheet investment vehicles, is about 120% of global gross domestic product, or a quarter of total financial assets, according to a report published by the Financial Stability Board today. Shadow banking “tends to take off when strict banking regulations are in place, when real interest rates and yield spreads are low and investors search for higher returns, and when there is a large institutional demand for assets,” according to the report. “The current environment in advanced economies seems conducive to further growth of shadow banking.”

While watchdogs have reined in excessive risk-taking by banks in the wake of the collapse of Lehman Brothers Holdings Inc. in 2008, they are concerned that lenders might use shadow banking to evade the clampdown and cause risks to build up out of sight of regulators. The FSB published guidelines for supervisors last year to keep track of the industry. “Risks can migrate outside of the core and as a result, the FSB’s shadow banking monitoring exercise is of the utmost importance,” Agustin Carstens, who heads up the FSB’s risk assessment committee, said in the statement. The FSB, a global financial policy group comprised of regulators and central bankers, found that shadow banking increased most rapidly in Argentina, which saw a 50% jump, and China, where growth was more than 30%. The global share of activity based in the U.S. declined to 33% last year from 41% in 2007, according to the report, while the proportion of shadow banking based in China rose to 4% from 1%.

Read more …

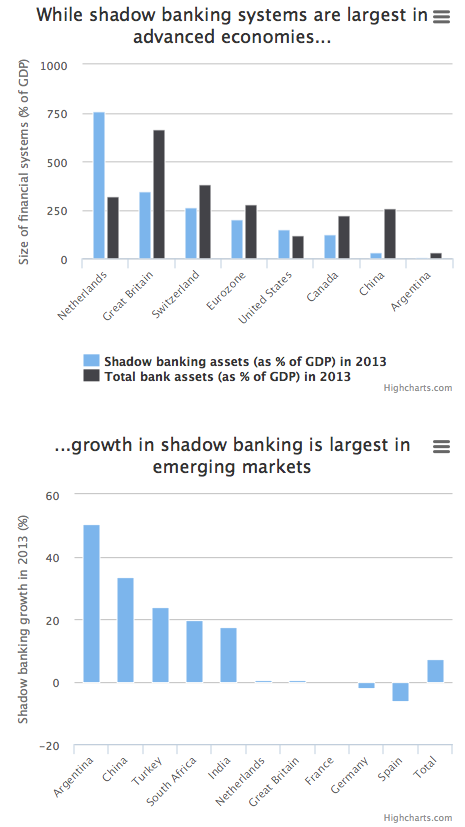

Same, with graphs.

• The $75 Trillion Shadow Hanging Over The World (Telegraph)

Global shadow banking assets rose to a record $75 trillion (£46.5 trillion) last year, new analysis shows. The value of risky investment products, mortgage-backed securities and other non-bank entities increased by $5 trillion to $75 trillion in 2013, according to the Financial Stability Board (FSB). Shadow banking, which is not constrained by bank regulation, now represents about 25pc of total financial assets – or roughly half of the global banking system. It is also equivalent to 120pc of global gross domestic product (GDP). The FSB, which monitors and makes recommendations on financial stability issues, said that while non-bank lending complemented traditional channels by expanding access to credit, data inconsistencies together with the size of the system meant closer monitoring was warranted.

“Intermediating credit through non-bank channels can have important advantages and contributes to the financing of the real economy; but such channels can also become a source of systemic risk, especially when they are structured to perform bank-like functions and when their interconnectedness with the regular banking system is strong,” the FSB said in its annual shadow banking report. While regulators have highlighted that the size of the shadow banking system does not pose a systemic risk on its own, many non-bank lenders obtain short-term funds to invest in longer-term assets, which can trigger fire sales if nervous investors decide to withdraw their money at once.

During the financial crisis, the rapid sell-off reduced asset values and spread the stress to traditional banks, some of which controlled shadow lenders. “The system-wide monitoring of shadow banking is a core element of the FSB’s work to strengthen the oversight and regulation of shadow banking in order to transform it into a transparent, resilient, sustainable source of market-based financing for real economies,” said Mark Carney, chairman of the FSB and Governor of the Bank of England.

Read more …

Yes, it’s Ambrose.

• QE Central Bankers Deserve A Medal For Saving Society (AEP)

The final word on quantitative easing will have to wait for historians. As the US Federal Reserve winds down QE3 we can at least conclude that the experiment was a huge success for those countries that acted quickly and with decisive force. Yet that is not the ultimate test. The sophisticated critique – to be distinguished from hyperinflation warnings and “hard money” bluster – is that QE contaminated the rest of the world in complicated ways and may have stored up a greater crisis for the future. What we can conclude is that extreme QE enabled the US to weather the most drastic fiscal tightening since demobilisation after the Korean War, without falling back into recession. Much the same was true for Britain. The Fed’s $3.7 trillion of bond purchases did not drive up debt ratios, as often claimed. It reduced them.

Flow of Funds data show that total non-financial debt has dropped from a peak near 260pc of GDP in 2009 and since stabilised at 237pc of GDP. Public debt did jump, matched by falls in household and corporate debt ratios. On cue, federal debt is now falling as well. The deficit is down to 2.8pc of GDP, low enough to erode the debt ratio in a growing economy through the magic of the denominator effect. This is not a “pure” economic experiment, of course. There are other variables: the shale boom and the manufacturing renaissance in chemicals and plastics that it has spawned; quick action by the US authorities to clean up the banking system. Yet it is indicative. By contrast, the eurozone carried out its fiscal austerity without monetary stimulus to cushion the shock, lurching from crisis to crisis as a result. The region has yet to reclaim it former levels of output, a worse outcome than during the Great Depression by a wide margin. Not even the 1840s were this bad. You have to go back to the Thirty Years War in the 17th century to trump the economic devastation of EMU.

Read more …

“Beijing-based ICBC reported its biggest jump in soured credit since at least 2006 in the third quarter. Smaller rival Bank of China more than doubled its provisions for bad loans”.

• Falling Bank Deposits Add to China Economy Warning Sign (Bloomberg)

Chinese bank deposits dropped following a crackdown on lenders manipulating their numbers and “illicit” means of attracting money, threatening to weigh on credit growth and hinder efforts to reignite the economy. Four of the five biggest banks, led by Industrial & Commercial Bank of China, posted a drop in deposits as they reported third-quarter earnings this week. Central bank data showed it was the first quarterly decline for the nation’s banking industry since at least 1999. The lower deposit levels are likely to curtail credit as banks are prohibited from lending more than 75% of their quarter-end holdings, while a sustained drop could hamper government efforts to rejuvenate an economy forecast to expand this year at the weakest pace since 1990. The lenders may also come under pressure to tap more expensive financing.

“With banks now less able to window-dress their deposit figures, some will be forced to scale back lending to meet loan-to-deposit requirements,” Julian Evans-Pritchard, China economist for Capital Economics said. “Regulatory controls are getting harder for banks and that’s weighing on credit growth.” ICBC, the world’s largest lender by assets, posted the biggest decline in funds during the third quarter, with its deposits dropping by 388 billion yuan ($63 billion) from June to 15.3 trillion yuan. Bank of China, Agricultural Bank of China and Bank of Communications also reported declines. Only China Construction Bank, the nation’s second-largest, had an increase. As a housing-market slump drags on the nation’s growth, bad loans are piling up. Beijing-based ICBC reported its biggest jump in soured credit since at least 2006 in the third quarter. Smaller rival Bank of China more than doubled its provisions for bad loans, while the combined profit growth of the five biggest banks slowed to 6% from 10% a year earlier.

Read more …

Reminds me of the IRS, for some reason. Australia in joint operation with China …

• China Snares 180 Fugitives Abroad in Global Anti-Graft Sweep (Bloomberg)

China said it has now captured 180 economic fugitives from 40 countries as part of a campaign started in July to recover billions of dollars of illicit gains. The suspects were apprehended under Operation Fox Hunt 2014, the official Xinhua News Agency reported yesterday. Authorities arrested 104 suspects and the rest turned themselves in, Xinhua said. The number of those apprehended is up from 128 announced earlier this month. The Communist Party under President Xi Jinping has mounted a crackdown on corruption that has netted thousands of cadres in the country and is targeting Chinese abroad. Between 2002 and 2011, $1.08 trillion of illicit funds were spirited out of China, estimates Washington-based Global Financial Integrity.

China has sent 20 teams of investigators to Thailand, the Philippines, Malaysia, Cambodia and other neighboring countries, Xinhua reported. The government estimates the number of corrupt officials who have moved abroad at anywhere from 4,000 to 18,000 people, according to China’s chief prosecutor Cao Jianming. The two top destinations for economic fugitives are the U.S. and Canada, in part because China doesn’t have extradition treaties with them, the official China Daily reported last month. The Australian Federal Police will take part in a joint operation with Chinese counterparts to seize assets of fugitive officials, the Sydney Morning Herald reported Oct. 20.

Read more …

Right. That time goes back decades.

• Time To Take A Zero-Tolerance Approach To The Banks (Guardian)

It’s been a wretched week for Britain’s banks. On Tuesday, Lloyds Banking Group announced it was setting aside an additional £900m for the mis-selling of payment protection insurance. On Thursday, Barclays made a £500m provision for the fine it can expect for rigging the foreign exchange market. The banking list of shame will no doubt be added to when Royal Bank of Scotland reports on Friday. Patience with the banks is wearing thin. As Minouche Shafik, the deputy governor of the Bank of England, said in a speech earlier this week, it is no longer credible to put the wrongdoing down to a few bad apples. The language used by Shafik was instructive. She talked of “appalling cases of misconduct”, and of a long tail of “outrageous conduct cases”. Unless banks have a tin ear, they must surely have got the message: Threadneedle Street has had enough.

What was a bit strange about Shafik’s speech was her comment that she found some of the behaviour in the City “truly shocking”. There is no longer anything remotely shocking in the unearthing of financial malfeasance. It is only shocking in the way that the gambling going on in Rick’s night club in Casablanca was shocking to Captain Renault. There are many explanations for why the rigging of markets and the rooking of customers happened. In the end, though, the simplest explanation is the best. It happened because the banks thought they could get away with it. The culture was one in which self-enrichment was seen as serving the greater good; regulation was so light-touch as to be non-existent; and the chances of being punished were slim. It’s not just the banks, of course. Why did newspapers hack phones? Because they could get away with it. Why do multinational companies pay so little tax on their UK activities? Because they can. Public trust in business generally, not just the banks, has rarely been lower and it’s not hard to see why.

Read more …

PIMCO owns dangerously large amounts of certain companies’ bonds.

• New Junk Bond Risk: It Matters Who Owns What (CNBC)

Add a new concern to the stable of high-yield bond risks: ownership of some companies’ issuance has become concentrated in the hands of just a few fund managers. “A reduced number of asset managers hold a significant amount of the debt of large corporate issuers across advanced and emerging market economies,” the IMF said in a report issued earlier this month, noting the top-five fund families hold at least 50% of reported bond ownership filings by many large non-resource companies in the JPMorgan Corporate Emerging Markets Bond Index. Some managers hold large chunks of a company’s debt, with the report highlighting that Pimco holds more than 20% of Ally Financial’s total bonds outstanding and around 15% of Navient’s, while in emerging markets, the top-five hold around 30% of Digicel’s bond issuance and more than 20% of Melco’s.

Pimco didn’t immediately return an emailed request for comment But while the IMF is concerned about how dependence on just a few funds may affect issuers’ access to markets in “times of stress,” others believe the risk may be to the fund manager. “If you own 20% of a company’s debt – and that’s something we would never do, because we don’t think that’s prudent – you’re almost duty bound to support the company in its next financing,” said Tim Jagger, portfolio manager at Aviva Investors, which has around $371 billion under management. “It’s going be very difficult if you’re not involved, to think other investors will get involved.” Jagger also noted that the concentration of ownership highlights what may be one of the biggest risks in the fixed income market generally: liquidity may suffer as changes in regulations since the Global Financial Crisis mean banks can’t warehouse an inventory of bonds like they used to.

Read more …

Must read.

• Putin To Western Elites: Play-Time Is Over (Dmitry Orlov)

Most people in the English-speaking parts of the world missed Putin’s speech at the Valdai conference in Sochi a few days ago, and, chances are, those of you who have heard of the speech didn’t get a chance to read it, and missed its importance. (For your convenience, I am pasting in the full transcript of his speech below.) Western media did their best to ignore it or to twist its meaning. Regardless of what you think or don’t think of Putin (like the sun and the moon, he does not exist for you to cultivate an opinion) this is probably the most important political speech since Churchill’s “Iron Curtain” speech of March 5, 1946.

In this speech, Putin abruptly changed the rules of the game. Previously, the game of international politics was played as follows: politicians made public pronouncements, for the sake of maintaining a pleasant fiction of national sovereignty, but they were strictly for show and had nothing to do with the substance of international politics; in the meantime, they engaged in secret back-room negotiations, in which the actual deals were hammered out. Previously, Putin tried to play this game, expecting only that Russia be treated as an equal. But these hopes have been dashed, and at this conference he declared the game to be over, explicitly violating Western taboo by speaking directly to the people over the heads of elite clans and political leaders. The Russian blogger chipstone summarized the most salient points from Putin speech as follows:

1. Russia will no longer play games and engage in back-room negotiations over trifles. But Russia is prepared for serious conversations and agreements, if these are conducive to collective security, are based on fairness and take into account the interests of each side.

2. All systems of global collective security now lie in ruins. There are no longer any international security guarantees at all. And the entity that destroyed them has a name: The United States of America.

3. The builders of the New World Order have failed, having built a sand castle. Whether or not a new world order of any sort is to be built is not just Russia’s decision, but it is a decision that will not be made without Russia.

4. Russia favors a conservative approach to introducing innovations into the social order, but is not opposed to investigating and discussing such innovations, to see if introducing any of them might be justified.

5. Russia has no intention of going fishing in the murky waters created by America’s ever-expanding “empire of chaos,” and has no interest in building a new empire of her own (this is unnecessary; Russia’s challenges lie in developing her already vast territory). Neither is Russia willing to act as a savior of the world, as she had in the past.

6. Russia will not attempt to reformat the world in her own image, but neither will she allow anyone to reformat her in their image. Russia will not close herself off from the world, but anyone who tries to close her off from the world will be sure to reap a whirlwind.

7. Russia does not wish for the chaos to spread, does not want war, and has no intention of starting one. However, today Russia sees the outbreak of global war as almost inevitable, is prepared for it, and is continuing to prepare for it. Russia does not war—nor does she fear it.

8. Russia does not intend to take an active role in thwarting those who are still attempting to construct their New World Order—until their efforts start to impinge on Russia’s key interests. Russia would prefer to stand by and watch them give themselves as many lumps as their poor heads can take. But those who manage to drag Russia into this process, through disregard for her interests, will be taught the true meaning of pain.

9. In her external, and, even more so, internal politics, Russia’s power will rely not on the elites and their back-room dealing, but on the will of the people.

To these nine points I would like to add a tenth:

10. There is still a chance to construct a new world order that will avoid a world war. This new world order must of necessity include the United States—but can only do so on the same terms as everyone else: subject to international law and international agreements; refraining from all unilateral action; in full respect of the sovereignty of other nations.

Read more …

On off on off.

• Russia Agrees to Terms With Ukraine Over Gas Supply (Bloomberg)

Russia agreed to terms for restoring natural-gas exports to Ukraine, laying the groundwork to prevent residents going without heat as temperatures drop. The gas negotiations, brokered by the European Union, came as pro-Russian rebels stepped up attacks on Kiev government forces. They violated the wobbly truce 45 times in the past 24 hours, the Defense Ministry said on Facebook today. One civilian was killed by shelling, the Donetsk city council said on its website. European leaders said they hoped the agreement would help mend ties between the two countries. “This breakthrough will not only make sure that Ukraine will have sufficient heating in the dead of the winter,” European Energy Commissioner Guenther Oettinger told a news conference in Brussels last night. “It is also a contribution to the de-escalation between Russia and Ukraine.”

The 28-nation EU sought to avoid a repeat of 2006 and 2009, when disputes between the former Soviet republics over gas debts and prices led to fuel transit disruptions and shortages across Europe amid freezing temperatures. Tensions remained even as the sides made progress on fuel supplies. The EU yesterday rebuked Russia for an announcement by Foreign Minister Sergei Lavrov that the country would recognize separatist elections planned for Nov. 2 in Ukraine’s rebel-held territories. The conflict in east Ukraine has killed at least 3,700 people, the United Nations estimates. [..] Under yesterday’s agreement, Russia said it would resume sending natural-gas to Ukraine – halted since June – after receiving the first tranche of debt repayment and upfront payments for future deliveries. Ukraine agreed to pay $3.1 billion to Russia by the end of this year to partially cover what Russia estimates is $5.3 billion owed by Naftogaz Ukrainy to Gazprom. The first tranche, $1.45 billion, will be paid “in the coming days,” Russian Energy Minister Alexander Novak said.

Read more …

Large scale (would-be) LNG exporters, US, Australia, Qatar, risk a lot.

• Oil Rout Seen Diluting Price Appeal of US LNG Exports (Bloomberg)

Oil’s collapse is eroding the appeal of potential U.S. LNG exports to Asia as it cuts the cost of competing supplies linked to the price of crude. Brent’s 22% drop this year outpaced the 8.9% decline in natural gas at Henry Hub, the benchmark for U.S. liquefied natural gas shipments that are scheduled to begin in 2015. When the cost of processing and shipping American supplies to Asia is taken into account, the price advantage over oil-linked cargoes from producers such as Qatar has more than halved, according to data compiled by Bloomberg. While the U.S. shale boom prompts the world’s biggest natural gas producer to plan exports of the fuel, it’s also boosting the country’s crude output to the most in 30 years, helping drive down global oil prices.

“The U.S. will not sell cheap gas,” Umar Jehangir, the deputy secretary of development and joint ventures at Pakistan’s Petroleum and Natural Resources Ministry, said in Singapore on Oct. 29, adding that the opinion was his own. “U.S. LNG will be exactly the same price as gas coming out of Qatar to Asia.” Cheniere Energy Inc., which is set to become the first natural gas exporter from the U.S. shale boom when its Sabine Pass terminal in Cameron Parish, Louisiana, starts next year, says the economics still make sense. Even after crude’s slump, there’s a 15% gap between Henry Hub-indexed prices and oil-linked supplies, Jean Abiteboul, the president of Cheniere Supply & Marketing, said in London on Oct. 29.

Read more …

” … a victim of its own success”?!

• Oil Price Declines Have Small-Cap Shale Investors Scrambling (Reuters)

Plummeting oil prices are pushing some of the small-cap companies which flourished as part of the U.S. shale energy boom close to their breaking point, while also prompting some well-known fund managers to aggressively buy energy stocks. Concerns about slowing growth in Europe and a stronger dollar have helped push the price of light crude oil down about 25% since June to about $82 a barrel, creeping closer to the average marginal cost of crude production of about $73 a barrel for U.S. onshore work, according to a research note from Baird Equity Research. Those declines have sent the SIG Oil Exploration and Production index down 21.2% over the last three months. “The market is selling all of these companies, even if it’s clear that $75 a barrel oil is not going to affect every company the same,” said Mike Breard, an analyst who works on the Hodges Small-Cap fund, part of Hodges Capital.

It’s a sudden turnabout for an industry that appears to be a victim of its own success. The high price of oil over the last decade was largely behind the push to mine shale oil through fracking, a controversial technique that uses high pressure to capture gas and oil trapped in deep rock. Fracking has helped the U.S. become among the world’s largest oil producers and led to concern that there is now an oversupply of crude. Production in the U.S. is on pace to add a record 1.1 million barrels a day in 2014, and another 963,000 in 2015, according to the U.S. Energy Information Administration. Already, the share price of small-cap shale oil companies such as Forest Oil has fallen below $1 as a result of high debt levels. Analysts now say that with the price of oil now close to the point where it’s no longer profitable to drill, small-cap energy stocks laden with high costs and little cash on their balance sheets could prove vulnerable to further price declines and may become acquisition targets if oil stays below $75 a barrel for six months or more.

Read more …

“If Iran walks away from the negotiation table over the proliferation of nuclear weapons technology in the country, markets could easily be spooked over the region’s stability”.

• Iran A ‘Time Bomb’ For Oil Prices (CNBC)

Markets should look for “a significant additional political risk premium on the price of Brent” if nuclear arms talks between Iran and major world powers break down, Nomura has warned. If Iran walks away from the negotiation table over the proliferation of nuclear weapons technology in the country, markets could easily be spooked over the region’s stability and that could affect the price of Brent, which has tumbled since June, Nomura’s senior political analyst Alastair Newton said in a note Thursday. “Iran could bring politics very much to the fore again in determining the price of Brent crude before year-end,” Newton warned.

Brent crude for December delivery fell below $86 a barrel on Friday to $85.41 as a stronger dollar and over-supply combined to put pressure on the benchmark. The price has slipped more than 9% so far in October, its biggest monthly drop since May 2012, and a quarter since June. The deadline for the completion of negotiations between Tehran and the so-called P5+1 group which comprises the five permanent members of the UN Security Council (China, Russia, France, the U.K. and the U.S.) plus Germany is on November 24. “In the event of no agreement by the 24th, I think that the U.S. Congress would impose fresh sanctions anyway,” Newton said. He added there were grounds for caution that the likelihood of agreement was less than 50%.

Read more …

Curious. Mysterious.

• Drones Spotted Over Seven French Nuclear Sites (AFP)

France’s state-run power firm Électricité de France (EDF) on Wednesday said unidentified drones had flown over seven nuclear plants this month, leading it to file a complaint with the police. The unmanned aircraft did not harm “the safety or the operation” of the power plants, EDF said, adding that the first drone was spotted on 5 October above a plant in deconstruction in eastern Creys-Malville. More drone activity followed at other nuclear power sites across the country between 13 October and 20 October, usually at night or early in the morning, EDF said, adding that it had notified the police each time. Greenpeace, whose activists have in the past staged protests at nuclear plants in France, denied any involvement in the mysterious pilotless flight activity.

But the environmental group expressed concern at the apparent evidence of “a large-scale operation”, noting that drone activity was detected at four sites on the same day in 19 October – at Bugey in the east, Gravelines and Chooz in the north and Nogent-sur-Seine in north-central France. Neither EDF nor the security forces had given any explanation about the overflights, the group said, urging the authorities to investigate. “We are very worried about the occurrence and the repetition of these suspicious overflights,” said Yannick Rousselet, head of Greenpeace’s anti-nuclear campaign, in a statement.

Read more …

“These are people who want to live in a dream world.”

• US Fracking Advocates Urged to Win Ugly by Discrediting Foes (Bloomberg)

As he took the floor at the tony Broadmoor resort in Colorado Springs, the veteran Washington public relations guru had an uncompromising message for oil and gas drillers facing an anti-fracking backlash. “You can either win ugly or lose pretty. You figure out where you want to be,” Rick Berman told the Western Energy Alliance, according to a recording. “Hardball is something that I’m a big fan of, applied appropriately.” Berman has gained prominence, including a “60 Minutes” profile, for playing hardball with animal activists, labor unions and even Mothers Against Drunk Driving. In Colorado, he was offering to take on environmentalists pushing restrictions on hydraulic fracturing, or fracking. The fight over fracking in the state has been viewed as a bellwether for similar debates brewing from New York to Sacramento. Energy companies are lobbying against a slew of regulations, including ones setting safety rules for fracking on public lands and another capping carbon emissions from power plants.

That partly explains why energy and resources companies, including Koch Industries, Exxon Mobil and Murray Energy are spending lavishly on political campaigns this year. The Center for Responsive Politics data shows the industry will contribute an amount second only to its record $143 million leading up to the 2012 election. So far they have given $95.5 million to candidates and political committees. Industry supporters say they have no choice. They face a well-funded environmental campaign from groups such as the Sierra Club that threaten to endanger the boom in production and domestic manufacturing that followed the shale revolution. “There is an anti-fossil fuel movement, and a very well-funded lobbying campaign is behind it,” said Michael Krancer, Pennsylvania’s former top natural-gas regulator and an energy attorney at Blank Rome LLP in Philadelphia. “These are people who want to live in a dream world.”

Read more …