John French Sloan South Beach Bathers 1908

“The only door left open is door number 3.”

• Capital Flight to Germany in Full Swing (Mish)

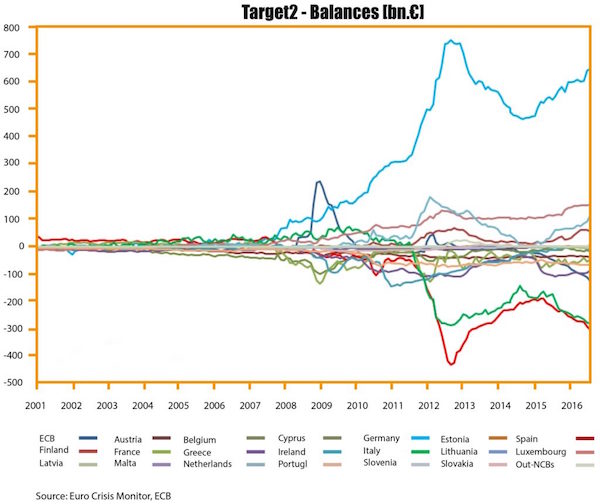

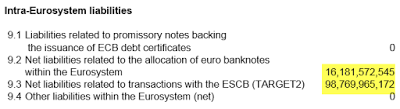

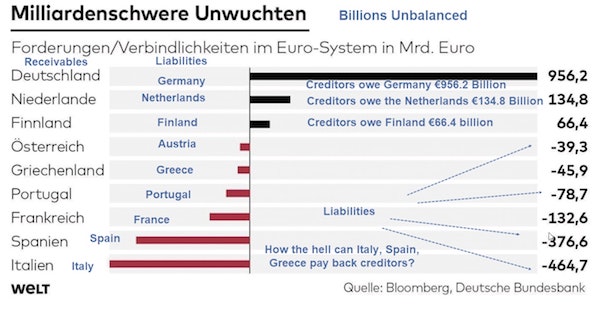

I have commented on Target2 liabilities before. Perhaps a Mish-modified translation from the Welt article Imbalance in the Euro System Reaches a New Record will ring a bell. The central banks of Germany’s euro partners Italy, Spain and France owe the Bundesbank almost a trillion euros . This is a new high. – more than ever before. Tendency continues to rise. There is no security for this money. Read that last line again and again until it sinks in. Italy is €464.7 billion in the hole. Spain is €376.6 billion in the hole. Creditors owe Germany, the Netherlands, and Finland over €1.157 trillion. In May, Italian liabilities increased by almost 40 billion euros.

“Capital flight to Germany is in full swing,” says Hans-Werner Sinn, longtime head of the Ifo Institute and one of the most prominent economists in the Federal Republic. Originally, Target2 was designed to facilitate cross-border transactions within the eurozone. The system achieved this goal. From the point of view of critics, this means that the Deutsche Bundesbank provides long-term unsecured and non-interest-bearing loans to the central banks of other eurozone countries , especially the central banks of southern countries Italy, Spain and Portugal.

Target2 is a fundamental problem of the Eurozone. • The ECB guarantees these loans. • As long as they are guaranteed, then hells bells, why not make more loans? Germany will pay one way or another. Here are the possibilities. 1) Germany and the creditor nations forgive enough debt for Europe to grow. This is the transfer union solution. 2) Permanently high unemployment and slow growth in Spain, Greece, Italy, with stagnation elsewhere in Europe 3) Breakup of the eurozone. Those are the alternatives. Germany will not allow number 1. It is unreasonable to expect number 2 to last forever. The only door left open is door number 3.

Nothing about this needs to be invented.

• The Big Italy Short Was Hiding In Plain Sight (R.)

The marriage of politics and finance in Italy regularly produces strange offspring. But a suggestion, floated over the weekend in the country’s most-respected newspaper, of a James Bond-style plot by some big investors to sink Italian financial markets added a new twist. More curious was the theory’s abrupt disappearance by Monday. The episode highlights the degree to which Europe’s most chaos-resilient economy has entered a risky new paradigm with the arrival of the most populist government since the Italian Republic’s founding in 1946. On Saturday, Corriere della Sera, the Milanese voice of the establishment, published an article which speculated that some investors betting against Italian assets might have helped engineer a market crisis.

The trigger for the Italian panic was the May 15 publication by Huffington Post’s Italian website of a draft version of the new government’s “contract”, which included language pertaining to a possible exit from the single European currency. That document, HuffPo has said, arrived in an unmarked envelope. Markets went haywire over the prospect that the government cobbled together by the two parties who gained the most seats in the March election – the right-wing League and hard-to-label 5-Star Movement – would adopt an explicitly anti-euro platform. The difference between the yields on 10-year German and Italian government bonds surged to almost 320 basis points from just around 130 basis points before the draft appeared. Any bets against Italian sovereign credit would have produced a tidy profit.

Corriere has substantially revised the story. It no longer includes language that one hedge fund, Brevan Howard, considered defamatory. That firm’s AH Master Fund, run by Alan Howard, gained 37 percent in May, thanks in part to bets on the direction of Italian assets. On Tuesday, the newspaper appended an author’s note to the piece in which it said: “We never intended to accuse or suggest that there were any kind of offenses or improper conduct by Howard in trading or in his involvement in the case of documents filtered to the Huffington Post.” In a statement to Reuters Breakingviews, the author, Federico Fubini, defended the piece. “We have run a fact-based article whose substance remains.” The paper decided “to amend the text to avert a potentially time-consuming case in foreign courts.”

EU, China protectionism.

• G7 Summit Highlights Western Leaders Hypocrisy (Lacalle)

The G7 failure to come to terms on trade highlights the problem of governments trying to macromanage trade. And no, the failure to even agree to disagree cannot be blamed on President Trump and his new-found economic nationalism. The list of countries with the largest trade surplus with the United States is led by China, which exports $375 billion more than it imports. It is followed, very far away, by Mexico ($71 billion), Japan (69 billion), Germany (65 billion), Vietnam (38 billion), Ireland (38 billion) and Italy ($31 billion). Not surprisingly, the markets with most protectionist measures against the United States are China, the European Union, Japan, Mexico and India.

These facts explain much more about the failure of the G7 summit than any Manichean analysis on Trump, Trudeau, Macron, or any of the leaders gathered there. During the last twenty years, the world has carried out a widespread practice in governments’ disastrous idea of “sustaining” GDP with demand-side policies. Build excess capacity, subsidize it, and hope to export that excess to the United States. Especially China, Germany, and Japan have economies with high state interventionism and therefore very high excess capacity, in part due to a high personal savings rate. Steel and aluminum, like the automobile industry, are examples of building unnecessary capacity and subsidizing it, country by country, hoping it will be somebody else who closes its inefficient factories to be able to export more to that country.

In Germany, the influence of the automobile industry over the government is legendary. What isn’t are the relatively high tariffs American manufacturers face when exporting to Europe and the low tariffs America itself imposes on automobile imports. What is also ironic is that modern-day protectionism didn’t start with Trump. Barriers against global trade increased between 2009 and 2016. The World Trade Organization warned, year after year, since 2010, about the increase in protectionism. The Obama administration, faced with the exponential increase in its trade deficit, was the one that introduced the highest number of protectionist measures between 2009 and 2016. The only difference between Trump and Obama was that Obama didn’t publicize this much and the mainstream media didn’t complain.

True, these deals need a sunset clause.

• Donald Trump Was Right. The Rest Of The G7 Were Wrong (Monbiot)

He gets almost everything wrong. But last weekend Donald Trump got something right. To the horror of the other leaders of the rich world, he defended democracy against its detractors. Perhaps predictably, he has been universally condemned for it. His crime was to insist that the North American Free Trade Agreement (Nafta) should have a sunset clause. In other words, it should not remain valid indefinitely, but expire after five years, allowing its members either to renegotiate it or to walk away. To howls of execration from the world’s media, his insistence has torpedoed efforts to update the treaty.

In Rights of Man, published in 1791, Thomas Paine argued that: “Every age and generation must be as free to act for itself, in all cases, as the ages and generations which preceded it. The vanity and presumption of governing beyond the grave is the most ridiculous and insolent of all tyrannies.” This is widely accepted – in theory if not in practice – as a basic democratic principle. Even if the people of the US, Canada and Mexico had explicitly consented to Nafta in 1994, the idea that a decision made then should bind everyone in North America for all time is repulsive. So is the notion, championed by the Canadian and Mexican governments, that any slightly modified version of the deal agreed now should bind all future governments.

But the people of North America did not explicitly consent to Nafta. They were never asked to vote on the deal, and its bipartisan support ensured that there was little scope for dissent. The huge grassroots resistance in all three nations was ignored or maligned. The deal was fixed between political and commercial elites, and granted immortality. In seeking to update the treaty, governments in the three countries have candidly sought to thwart the will of the people. Their stated intention was to finish the job before Mexico’s presidential election in July. The leading candidate, Andrés Lopez Obrador, has expressed hostility to Nafta, so it had to be done before the people cast their vote. They might wonder why so many have lost faith in democracy.

[..] Trump was right to spike the Trans-Pacific Partnership. He is right to demand a sunset clause for Nafta. When this devious, hollow, self-interested man offers a better approximation of the people’s champion than any other leader, you know democracy is in trouble.

Caitlin again.

• Centrists Very Concerned That Donald Fucking Trump Isn’t Hawkish Enough (CJ)

[..] by far the most common concerns being expressed about the Singapore summit are based not on a fear of this administration making insufficiently aggressive demands of Pyongyang, but on pure ridiculous nonsense. “President Trump seems to have given away two or three of the major things that Kim Jong-Un wanted,” Schumer complained at the aforementioned press conference. “A meeting. The flags next to each other. Now a delay of exercises with South Korea, without getting anything in return.” Huh? A meeting? Flags next to each other? I can kinda-sorta-almost see into Schumer’s twisted reality tunnel when it comes to temporarily suspending military drills along the DPRK’s border as an act of good faith, but on what planet is having a meeting or putting two flags next to each other a win of any kind?

Well, going by the outcry I’m seeing from Twitter pundits, the concern appears to be that it “legitimizes” Kim Jong-Un. What exactly that means is hard to fathom in terms of actual, tangible reality, but for years that term has been passed around like it has as much relevance as war or starvation sanctions. This imaginary product of “legitimacy” is, according to influential mainstream political commentators, meant to be withheld from Kim until he gives up everything he has and grovels on his belly begging for it. This just shows you the power of narrative, where repeating some meaningless placeholder syllables over and over again can create the illusion that a purely mental construct is as relevant in peace negotiations as nuclear warheads.

It isn’t hard to see through for anyone who doesn’t have a vested interest in subscribing to that narrative, though, and Pyongyang certainly has no such interest. [..] There are many, many perfectly valid things to criticize the Trump administration for. Opening up peace talks with North Korea is not one of them, and anyone who says it is is not a friend of humanity. The fact that nobody on either side of the aisle seems to have their foot anywhere near the brake pedal when it comes to war should concern us all, and we need to do something about it.

Might as well stop the whole process right now.

• May Heads Off Major Defeat After Last-Minute Climbdown To Rebels (Ind.)

Rebel Conservatives have forced Theresa May into a climbdown, handing parliament greater control of Brexit if she fails to seal a deal. After the prime minister was threatened with what could have been a damaging commons defeat, she promised key concessions in dramatic last minute talks with pro-EU rebels. It is likely to mean her accepting a deadline by which she must secure a deal with Brussels, if she wants to stay in the driving seat for negotiations. Her ministers must now spell out the detail of her compromises within days, with Tory rebels warning a failure to do so would reignite the prospect of a major commons loss destabilising her leadership.

It followed a day which started with the resignation of a minister and passed into febrile commons debate that saw ministers bargaining openly with rebels in the chamber. Rebel MP Nicky Morgan told The Independent: “The whole point of what has come about is that we are going to have a process to this, something which does not simply allow us to drift into a hard Brexit.” The row was precipitated by the Lords last month passing a plan that would have given parliament the power to direct Ms May’s actions if she failed to seal a Brexit deal later this year. Ministers were demanding Tory MPs vote it out of existence in the Commons on Tuesday, but had also refused to consider a more palatable compromise proposed by the former Conservative attorney general Dominic Grieve.

It would have instead seen Ms May being tied into a strict timetable of having to set out her own proposals if she failed to seal a deal by November, and then gain parliamentary approval for them – the stronger powers for MPs to direct her action would only come into play if a deal had still not been reached by February.

What, no new loans?

• Tesla To Cut 9% Of Staff In Profitability Drive (G.)

Tesla is slashing thousands of jobs, its chief executive, Elon Musk, announced Tuesday, as the electronic car company attempts to hit production targets and reach profitability. Musk called the job cuts, which will affect about 9% of the company’s more than 40,000 employees, “difficult, but necessary” in a tweet that contained the email he had sent to employees announcing the layoffs. “What drives us is our mission to accelerate the world’s transition to sustainable, clean energy, but we will never achieve that mission unless we eventually demonstrate that we can be sustainably profitable,” the billionaire entrepreneur wrote in the email.

The job cuts will be centered on salaried employees, not factory workers, Musk said, writing, “This will not affect our ability to reach Model 3 production targets in the coming months.” Tesla has been under intense pressure to prove that it can achieve mass production of the Model 3, its first mass market vehicle. The company has yet to reach Musk’s goal of producing 5,000 cars a week – originally promised for the end of 2017. At Tesla’s annual shareholder meeting on 5 June, Musk said he believed the company would hit the 5,000 cars-a-week goal by the end of June, and that he thought the company could be profitable later this year.

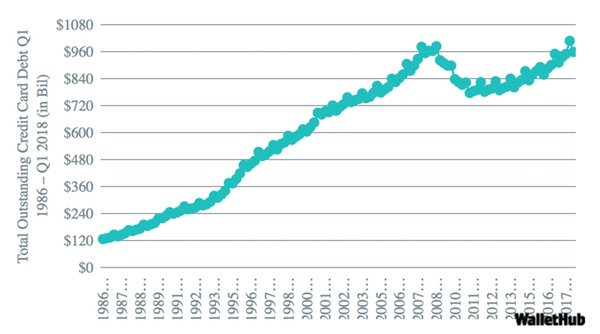

They paid off so much because they owe so much.

• Americans Just Paid Off A Ton Of Credit-Card Debt—But Here’s The Bad News (MW)

A lot of Americans paid big credit-card bills in the first quarter of 2018. And they still have a long way to go. Americans repaid $40.3 billion in credit card debt during the first quarter of 2018, according to a new analysis of data from the U.S. Census Bureau, Federal Reserve and credit agency TransUnion by the personal-finance website WalletHub. That’s the second-highest amount paid off in one quarter since the first quarter of 2009, when consumers paid off more than $44 billion. Now, the bad news: That doesn’t mean their debts are getting that much smaller. Americans ended 2017 with $91.6 billion in new credit-card debt, the largest annual amount since 2007 and 104% above the post-recession average.

Outstanding credit card debt is at the second-highest point since the end of 2008, the report said. In 2017, Americans hit a record high of $1.021 trillion in outstanding revolving debt (often categorized as credit-card debt). In April 2018, they still had more $1.030 trillion to pay off, according to the Federal Reserve. Consumers’ recent debt payoff “is not as dramatic as the dollar amount makes it seem,” said Nick Clements, the co-founder of personal finance company MagnifyMoney, who previously worked in the credit industry. The reason: The total amount of credit-card debt Americans have has also been growing.

How Monsanto sneaks in illegal seeds.

• India Farmers Sow Unapproved Monsanto Cotton Seeds, Risking Arrest (R.)

Many Indian farmers are openly sowing an unapproved variety of genetically modified (GM) cotton seeds developed by Monsanto, as the government sits on the sidelines for fear of antagonizing a big voting bloc ahead of an election next year. India approved the first GM cotton seed trait in 2002 and an upgraded variety in 2006, helping transform the country into the world’s top producer and second-largest exporter of the fiber. But newer traits are not available after Monsanto in 2016 withdrew an application seeking approval for the latest variety due to a royalty dispute with the government. The herbicide-tolerant variety, lab-altered to help farmers save costs on weed management, has, however, seeped into the country’s farms since then. Authorities say they are still investigating how that happened.

“I will only use these seeds or nothing at all,” said Rambhau Shinde, a farmer who has been cultivating cotton for nearly four decades in the western state of Maharashtra. The federal environment ministry said last year planting the seeds violated the Environment Protection Act, and farmers who did so were risking potential jail terms. But many farmers are desperate to boost their incomes after poor yields over the past few years and are willing to ignore the warnings. A government official in New Delhi, who deals with matters related to GM crops, said it was difficult to keep farmers away from something that they saw benefit in. “If you don’t allow them to plant legally, illegal planting will happen,” the official said, requesting anonymity, adding that Monsanto had yet to reapply for an approval to sell its latest variety of GM cotton in India.

Bats and cats and rats.

• One in Three British Mammal Species Could Be Gone Within A Decade (Ind.)

Populations of much-loved British mammals including hedgehogs and water voles have dropped by up to two-thirds over the past 20 years, and many more are threatened with imminent extinction. Even some apparently common creatures such as rabbits have been driven into decline by human pressures such as harmful farming activities and climate change. These findings come from a review carried out by the Mammal Society and Natural England, the first of its kind to be conducted in more than two decades. The country has undergone significant changes since the last analysis in 1995, and some of the species at risk then – including badgers and otters – have since made considerable recoveries.

However, pesticide use, invasive species and road deaths have all taken their toll, and the scientists behind the study have warned Britain is on “a precipice” and must take urgent action to save its mammals. “This is happening on our own doorstep so it falls upon all of us to try and do what we can to ensure that our threatened species do not go the way of the lynx, wolf and elk and disappear from our shores forever,” said Professor Fiona Mathews, chair of the Mammal Society. The review, which made use of data collected by members of the public as well as scientists over the course of decades, covered all 58 of the country’s land mammal species.

The scientists constructed the first ever “red list” for British mammals, and found 12 are threatened with extinction. This means animals like the wildcat, greater mouse-eared bat and even the black rat are likely to be gone forever from Britain’s shores within the next 10 years. However, they noted this is likely to be an underestimate, and the real number could be as high as one in three.