Pablo Picasso Bather � 1908

— Donald J. Trump Posts From His Truth Social (@TrumpDailyPosts) September 10, 2024

RFK Trump

RFK Jr. says Trump admitted to him he didn’t drain the swamp his first term and has asked him to help him drain the swamp moving forward:

“He said, I didn't know anything about governing and he said, we won this election, and then all of a sudden, you got to fill 60,000 jobs.”… pic.twitter.com/GH19wOsYvX

— End Tribalism in Politics (@EndTribalism) September 9, 2024

Numbers

https://twitter.com/i/status/1827669780880302308

RFK unify

Bottom line: No matter what state you live in, VOTE TRUMP. A Trump victory is a Kennedy victory. pic.twitter.com/GBn2p2RLnX

— Robert F. Kennedy Jr (@RobertKennedyJr) September 10, 2024

Mail-in

REPORT: 20% of mail-in ballots were fraudulent in the 2020 election according to a study conducted by the Heartland Institute.

The study was referenced by Donald Trump over the weekend who received backlash for making the claim.

According to the Heartland Institute’s Justin… pic.twitter.com/KBBgHAn40U

— Collin Rugg (@CollinRugg) September 9, 2024

judge Joe Brown

KAMALA SOROS CORRUPTION: Kamala Harris as Attorney General refused to prosecute the George Soros owned OneWest Bank for over 1,000 violations of federal law. A one year investigation had uncovered evidence of widespread misconduct, but she refused to prosecute Soros and Mnuchin.… pic.twitter.com/mRA5ij93ju

— Truth Justice ™ (@SpartaJustice) September 9, 2024

Lara

Lara Trump – 700 trained Republican poll watchers applied in Detroit … only 50 were accepted.

OVER 2300 Democrats were accepted?!

The @RNC filed a lawsuit in Wayne County to STOP THIS.

I’ll post an update when I have more info.

Repost!

— Sheri™ (@FFT1776) September 9, 2024

Elon SNL

https://twitter.com/i/status/1833306523553984680

Don’t see much commentary on the debate yet. But predictably, both sides will have seen their candidate win.

What’s remarkable is that the Dems all of a sudden want another debate, something they strongly opposed before. That would seem to indicate that they don’t think Kamala won this one.

• Trump Says Debate Performance Against Harris His Best Ever (Sp.)

Former US President Donald Trump said following his debate with Vice President Kamala Harris that he had his best debate performance ever, despite Trump believing that the moderators were aiding Harris. “I thought that was my best Debate, EVER, especially since it was THREE ON ONE,” Trump said on Tuesday via Truth Social. People are calling Trump’s performance a “big win,” the former president also said. The Harris campaign likewise praised her debate performance and suggested a second debate in October. Donald Trump criticized President Joe Biden for not making an effort to talk to Russian President Vladimir Putin in two years to try to resolve the conflict in Ukraine. “He [Biden] hasn’t even made a phone call in two years to Putin, hasn’t spoken to anybody. They don’t even try and get it. That is a war that’s dying to be settled,” Trump said on Tuesday night in his debate against his Democratic rival Kamala Harris.

Trump said in a presidential debate that he wants the Ukraine conflict to come to an end immediately and claims he will be able to immediately broker a peace plan if reelected. “I want the war to stop, I want to save lives,” Trump said on Tuesday night in the debate against Democratic nominee Kamala Harris. Trump said he would speak with Russian President Vladimir Putin and Ukraine’s Volodymyr Zelensky, adding that he would also be able to get both leaders to negotiate and end the conflict. It is in the United States’ best interest to get the Ukraine conflict resolved quickly, Trump added. The campaign of Democratic nominee Kamala Harris said that the second debate with Republican nominee Donald Trump should take place next month, Harris-Walz campaign Chair Jen O’Malley Dillon said in a statement.

“Under the bright lights, the American people got to see the choice they will face this fall at the ballot box: between moving forward with Kamala Harris or going backwards with Trump,” O’Malley said after the first presidential debate concluded on Tuesday night. “That’s what they saw tonight and what they should see at a second debate in October. O’Malley also said that Harris is ready for a second debate but questioned whether Trump is ready. Kamala Harris said during a debate with former US President Donald Trump that the United States does not have troops in any conflict zone around the world.

“As of today, there is not one member of the US military who is in active duty in a combat zone, in any war zone around the world – the first time this century,” Harris said on Tuesday evening. The US military has had forces deployed in countries around the world under the Biden administration, including Syria, Iraq and Jordan. During the June debate between Trump and US President Joe Biden, Biden falsely claimed that he was the only president to not have any troops die anywhere in the world. In August 2021, 13 US military servicemembers died during the withdrawal from Afghanistan, due to a suicide bombing at the airport in Kabul. Moreover, in January 2024, three US troops were killed by a drone attack in Jordan.

“Trump also claimed Harris wants to do a second debate because she “got beaten.”

• Harris Tried to ‘Hide Her Imposter Syndrome’ in Debate – Psychiatrist (Sp.)

Less than two months away from the US presidential election, former POTUS Donald Trump faced off against current Vice President Kamala Harris in a highly anticipated debate on Tuesday night. Donald Trump “made some good points” during the presidential debate, while vice president Kamala Harris got through by “skirting the issues,” board-certified psychiatrist Dr. Carole Lieberman told Sputnik. Overall, the face-off was described as “extremely disturbing” by the best-selling author based in Beverly Hills, California. She noted that former California Attorney General Kamala Harris had prepared for the debate “more than for anything else in her life. Even the law boards.”

“In order to hide her imposter syndrome, she memorized lines that she hoped would derail Trump. Imposter syndrome is where someone knows they don’t have the qualifications for the position they are in, so they feel like an imposter.Kamala doesn’t have the qualifications to be vice president, no less president. She has to know Biden picked her to be vice president because she is a ‘woman of color.’ He picked her to get votes from these demographics, not because she was the most qualified,” the pundit remarked. As for Trump, he was “overly concerned with not wanting to seem out of control” if he took Harris’ bait, the psychiatrist said. She remarked that one of Trump’s “best lines” was when he called out the VP over her father, Donald J. Harris, “for being a Marxist, which we all know is true.” “He knew where the bones were buried and he should have exposed more of them. At times, Kamala exposed her weakness by grimacing and trying to get at Trump more strongly, such as when she resorted to accusing him of being a criminal. His retorts to that were to call it what it was – lawfare,” noted the writer.

Looking ahead, Dr. Lieberman voiced hope that there would be a second debate between Trump and Harris and the former president would have a chance “to expose more of her sinister plans for America.” VP Kamala Harris and former POTUS Donald Trump faced off on Tuesday for their first presidential debate in Philadelphia on Tuesday. After the 90-minute event, hosted by ABC News, Trump told the media that he believed it was his “best debate ever.” Trump also claimed Harris wants to do a second debate because she “got beaten.” The Republican presidential contender has not yet committed to another one-on-one later this month.

https://twitter.com/i/status/1833450191552451008

jim tells me his host server is/was down, but his articles are also on Substack…

• The Votes and Who Counts Them (Jim Kunstler)

“The world is a dangerous place to live — not because of the people who are evil but because of the people who don’t do anything about it.” —Albert Einstein. When The New York Times tells you that the United States Constitution is a threat to democracy — As it did on the front page of its August 31 edition — you know that you are in thrall to exceedingly subtle minds. The Times only employs persons, both birthing and other, of the subtlest minds. You can tell because they are credentialed by our country’s finest institutions of educational credentialing. They come to The Times fully equipped with the armamentarium of advanced, progressive, innovative, nuanced, cutting-edge modes of understanding our world — which, you’ll agree, is a pretty goshdurned complex place, and rather niggardly in yielding its secret workings. Hence, The Times has concluded that the Constitution is flawed, perhaps fatally, because it allowed for the election of Donald Trump once, and now, possibly, a second time:

“It’s no surprise, then, that liberals charge Trump with being a menace to the Constitution. But his presidency and the prospect of his re-election have also generated another, very different, argument: that Trump owes his political ascent to the Constitution, making him a beneficiary of a document that is essentially antidemocratic and, in this day and age, increasingly dysfunctional.” The Constitution does not stipulate a particular election day, but subsequent US law established the first Tuesday after the first Monday in November as the day for federal elections (the states can establish their own election dates for state and local offices). This changed beginning in the year 2000, when Oregon legislated to conduct all elections by mail-in ballot and other states followed with alterations to voting methods beyond a single election day.

The Covid-19 pandemic prompted states to permanently relax rules on absentee ballots and expand mail-in voting, under guidance from the federal agencies such as the CDC, while the CARES Act of 2020 provided emergency funding to implement procedures for mail-in voting in order to reduce in-person voting that might enable the spread of Covid-19. All of that followed orderly legislative procedure. The result was widespread ballot fraud, especially in crucial swing voting districts, much of it arrant. Contrary to official narratives out of the “Joe Biden” administration and the salient organs of corporate news, the allegations of widespread fraud were not “baseless” nor were they “conspiracy theories.” Subtle minds schooled in nuanced, cutting-age modes of analysis agreed to ignore documentary evidence of ballot fraud because it disfavored their preferred candidate, “Joe Biden.” Subtler judicial minds subsequently dismissed challenges to official tallies.

Other shenanigans such as the $400-million that Mark Zuckerberg (Meta and Facebook) injected into swing districts for “election administration and voter turn-out,” via his Center for Tech and Civic Life (CTCL), was not adjudicated in any court. The upshot of the “Zuckerbucks” prank was that polling offiicials in many precincts were replaced by Democratic Party activists who ended up counting the votes. The Federal Election Commission (after “Joe Biden” became president) decided that under federal campaign finance law, the contributions were not seen as illegal — though the “Zuckerbucks” scandal did lead to legislative reform in several states.

You might suppose in the years since the 2020 election that opportunity would be seized to materially correct the weaknesses of mail-in ballots, early voting, ballot “harvesting” practices, giant “balloting centers,” and the use of vote-tallying machines (Dominion, etc.) with modems allowing for Internet hackery. The best and simplest reform would be a return to paper ballots cast only on one election day, with voter ID and proof of citizenship (accomplished prior in voter registration), conducted in smaller, distributed precinct polling places that make hand-counting of ballots practical. Alas, this was too difficult for Congress, while the subtle, nuanced, cutting-edge minds working in news media were not interested in such straightforward reform and did not advocate for it.

”There is definitely more to this story, and we need to uncover the truth..”

• Melania Trump Demands ‘Truth’ About Shooting of Husband (RT)

Former First Lady Melania Trump has called for answers to “uncover the truth” behind the attempted assassination of her husband, former President Donald Trump, nearly two months ago. Trump narrowly escaped death when Thomas Matthew Crooks, 20, opened fire on him during a rally in Butler, Pennsylvania on July 13. The incident was a “horrible, distressing experience” for the family, Melania said in a video posted on X on Tuesday. ”Now, the silence around it feels heavy. I can’t help but wonder: Why didn’t law enforcement officials arrest the shooter before the speech?” The would-be assassin positioned himself on a nearby rooftop that provided an unobstructed view of the Republican candidate. One bullet grazed the former president’s right ear, resulting in one attendee’s death and injuries to two others. The shooter was subsequently killed by Secret Service agents.

https://t.co/ZCTwZSqZND pic.twitter.com/KKA6anTEYC

— MELANIA TRUMP (@MELANIATRUMP) September 10, 2024

The House of Representatives unanimously voted to create a bipartisan task force to investigate the attempted assassination. Comprised of seven Republicans and six Democrats, the task force aims to examine potential security lapses at the federal, state, and local levels of law enforcement that preceded the incident. In an interview last month, Trump accused President Joe Biden and his Democratic rival, Kamala Harris, of being partly responsible for the assassination attempt. “I think to a certain extent it’s Biden’s fault and Harris’ fault,” he said, claiming they “were making it very difficult to have proper staffing in terms of Secret Service” and “weren’t too interested in my health and safety,” while promoting rhetoric that could have encouraged the shooter. ”There is definitely more to this story, and we need to uncover the truth,” Melania said in the video, which appears to promote her upcoming memoir.

“..a significant cost to the integrity of the election: the voters will be improperly denied a choice between persons who are actually candidates, and who are willing to serve if elected..”

• Michigan Supreme Court Blocks RFK Jr.’s Bid to Remove Name From Ballot (ET)

The Michigan Supreme Court has denied Robert F. Kennedy’s request to have his name removed from the state’s general election ballot, reversing a lower court ruling and closing the last legal avenue available to Kennedy in the case. In a split 5–2 ruling issued on Sept. 9, the Michigan Supreme Court reinstated the original ruling by the Michigan Court of Claims, which denied Kennedy’s motion for mandamus relief, an extraordinary legal remedy that requires a plaintiff to demonstrate a clear legal right and that the defendant, in this case the Michigan Secretary of State, has a clear duty to act. The high court ruled that Kennedy did not provide a clear legal basis requiring the removal of his name from the November ballot and failed to identify a law that would leave no room for discretion in this matter on the part of election officials.

“Plaintiff has neither pointed to any source of law that prescribes and defines a duty to withdraw a candidate’s name from the ballot nor demonstrated his clear legal right to performance of this specific duty, let alone identified a source of law written with ‘such precision and certainty as to leave nothing to the exercise of discretion or judgment,’” reads the majority opinion, which reversed an appeals court’s decision that sided with Kennedy and reinstated the lower court’s decision that dismissed his request with prejudice. Michigan Supreme Court Justices Brian K. Zahra and David F. Viviano dissented. They argued that there was no statute prohibiting Kennedy from withdrawing from the election and no practical reason to deny Kennedy’s request to remove his name from the ballot before ballots were printed. Their dissent focused on harm to voters, contending that keeping Kennedy on the ballot would confuse voters and distort the true electoral choice.

“There is, however, a significant cost to the integrity of the election: the voters will be improperly denied a choice between persons who are actually candidates, and who are willing to serve if elected,” the dissenting justices wrote. “The ballots printed as a result of the Court’s decision will have the potential to confuse the voters, distort their choices, and pervert the true popular will and affect the outcome of the election.” Days before the Supreme Court decision, the Michigan Court of Appeals argued that Kennedy had a “clear legal right” to withdraw, emphasizing that no specific statute prevented a presidential candidate from stepping down, even one nominated by a minor party. Kennedy, who had been nominated by the Natural Law Party, withdrew from the presidential race on Aug. 23 and endorsed former President Donald Trump. At the time, Kennedy said he wanted his name removed in key swing states so as not to draw votes away from the former president.

“..57% of the public wanted dialogue with Russia to begin..”

• More Ukrainians Want Talks With Russia – WSJ (RT)

An increasing number of Ukrainians want Kiev to find a diplomatic solution to the conflict with Moscow, the Wall Street Journal has reported. In its article on Tuesday, the US outlet acknowledged that “some Ukrainians are asking a question that had until recently been taboo: Is it time to try to negotiate?” According to the article, opinion polls show that support for talks with Russia has been “creeping upward” in Ukraine since the failure of Kiev’s much-hyped counteroffensive last year. While it contended that a majority of Ukrainians still want their country to keep fighting to retake all territories captured by Russia, it did not provide exact figures. Another poll, published by the Kiev International Institute of Sociology (KIIS) in early August, suggested that 57% of the public wanted dialogue with Russia to begin.

The outlet cited a 33-year-old school teacher from the southeastern city of Zaporozhye, who said that she is willing to give up any part of territory in exchange for peace so that her husband could return home from the front line. “Where can we go with this war?” she wondered. The group that is most skeptical about a peace deal with Russia is the Ukrainian military, with one recent survey showing that only 18% of active-duty troops and veterans are in favor of the talks, the article read. According to the same poll, 15% of soldiers and veterans said they would join an armed protest if Kiev signs an unfavorable agreement with Moscow. The members of the military who spoke to the WSJ said that they were concerned that Russia could use a pause in the fighting to prepare for a new attack on Ukraine and that seeking peace with concessions would mean that the sacrifice of their fallen comrades had been in vain.

During his meeting with US Defense Secretary Lloyd Austin at Ramstein Air Base in Germany on Friday, Ukrainian leader Vladimir Zelensky suggested that the conflict between Russia and Ukraine should end “this fall.” According to Zelensky, in order for this happen, NATO must keep arming Kiev and increase pressure on Moscow to agree to the Ukrainian peace plan, which calls for the withdrawal of Russian forces from all territories that Kiev considers its own, including Crimea, and for Moscow to pay reparations and submit its officials to war tribunals.

Last week, Russian President Vladimir Putin reiterated that Moscow had “never refused” negotiations with Kiev, but stressed that they should take place “not on the basis of some ephemeral demands but on the basis of the documents that were agreed to and actually initialized in Istanbul” in late March 2022, when the sides last sat at the negotiating table. During the talks in Türkiye, Ukraine was willing to declare military neutrality, limit its armed forces, and vow not to discriminate against ethnic Russians. In return, Moscow would have joined other leading powers in offering Ukraine security guarantees, Putin said.

“Don’t kid yourself… We are playing with WWIII, and we have a president that… Where is our president?”

• Ukraine Conflict ‘Much Worse’ Than Americans Are Being Told – Trump (RT)

Donald Trump has claimed that President Joe Biden’s Ukraine policy – now fully adopted by his Democratic rival Kamala Harris – is dragging the US into a third world war. He reiterated that he would settle the conflict “in 24 hours” if elected president this November, even before being sworn in. During a debate with Harris on Tuesday, Trump asserted that the conflict would never have occurred had he still been in the White House in early 2022. When asked if he wanted Kiev to win, the Republican replied that he wanted “the war to stop.” “I want the war to stop. I want to save lives that are being wasted… People are being killed by the millions…. It’s so much worse than the numbers you’re getting, which are fake,” he claimed, without clarifying the source of those estimates.

The moderator pressed for a direct answer, inquiring whether Trump believes “it’s in the US’s best interest for Ukraine to win this war.” “I think it’s in the US’s best interest to get this war finished and just get it done. We need to negotiate a deal because we have to stop all these human lives from being destroyed,” Trump insisted. The former president then claimed he had a “good relationship” with Russian President Vladimir Putin and that everything has “gone to hell” since he left office. “When I saw Putin building up soldiers on Ukraine’s border, I thought: ‘Oh, he must be negotiating; it must be a strong point of negotiation,’” Trump stated. ”Well, it wasn’t, because Biden had no idea how to talk to him. He had no idea how to stop it… And it is only getting worse; it could lead to World War III,” he added. “Don’t kid yourself… We are playing with WWIII, and we have a president that… Where is our president?”

“They threw him out of the campaign like a dog… We have a president that doesn’t even know he’s alive.” “I will get it settled before I even become president,” Trump promised. “If I win, when I’m president-elect… I’ll get them together.” Harris countered by claiming that the only reason Trump says “this war would be over within 24 hours” is that he would simply give it up. “And that’s not who we are as Americans,” she added. The Vice President went on to tout her role in consolidating Western support for Ukraine, claiming that because of “the work that I and others did,” along with the provision of “air defense, ammunition, artillery, javelins, and Abrams tanks,” Ukraine remains an “independent and free” country.

“The international community should recognize that troops using Nazi insignia, who often appear to act as such, cannot fight in Ukraine.”

• Slovakia PM Fico Accuses World Of Ignoring Ukraine’s ‘Nazi Troops’ (RT)

People eager to condemn the atrocities committed by the Third Reich are at the same time turning a blind eye to Ukrainian troops wearing Nazi symbols today, Slovakian Prime Minister Robert Fico has lamented. The head of the government gave a speech at the holocaust museum located at the former site of the Sered concentration camp on Monday in western Slovakia, in which he highlighted the need to educate new generations about the crimes committed by Nazis during World War II before bringing up the Ukraine conflict. “We all talk about fascism, Nazism, while silently tolerating units moving across Ukraine that have a very clear label and are connected to movements that we consider dangerous and forbidden today. Since it is a geopolitical fight, nobody cares,” Fico said.

“I want to pay tribute to the victims, not with pathetic speech, but I want to call for action,” he added. “The international community should recognize that troops using Nazi insignia, who often appear to act as such, cannot fight in Ukraine.” Kiev has embraced as heroes Ukrainian nationalists who collaborated with Nazi Germany while the symbols and ideology of the Third Reich have been popular among growing right-wing forces in the country for decades. The Azov battalion, accused of war crimes and atrocities, is infamous for its open embrace of bigotry and white supremacism, although its successor unit claims to have mostly eradicated such people from its ranks. Ukrainian troops have repeatedly been filmed brandishing Nazi iconography on their uniforms and weapons, including during the ongoing incursion into Russia’s Kursk Region.

In a widely publicized incident, two Ukrainian soldiers filmed themselves imitating invading Wehrmacht troops while harassing an elderly Russian civilian. The man went missing after the encounter. Thousands of Ukrainian Nazi collaborators made their way to Western nations, such as Canada, when the Axis powers were defeated in 1945. Some of them were later used by the CIA in attempts to destabilize the USSR during the Cold War. Just last week, Library and Archives Canada in Ottawa expressed reservations against releasing the list of some 900 alleged Nazi criminals who fled to the country after the war. Making the names public may embarrass the country’s Ukrainian community, officials told the media. The Slovakian prime minister is a vocal critic of Western support for Kiev against Moscow. The Ukrainian Nazi link is one of the reasons he has cited in explaining his position.

“India refused, stating publicly that Zelensky’s plan was not the only one to be considered, as other peace plans were also on the table..”

• Modi’s Peace Plan: How India Is Navigating The Ukraine Conflict (RT)

Prime Minister Narendra Modi has sought to play a role in promoting a negotiated resolution of the conflict in Ukraine. He has India’s national interest in mind, as the nation of 1.4 billion people needs a peaceful international environment in which to grow, especially when it is at a critical stage in its development process and aims to become the third largest economy before the end of the decade. India has historical ties of friendship and trust with Russia; its defense ties with Moscow are crucial for its security. It is also strengthening its ties with the US and EU, which are its major economic and technology partners, and with whom people-to-people ties are very strong. While Russia does not interfere in New Delhi’s ties with its Western partners, the US and the EU have wanted India to dilute its ties with Moscow. American sanctions, especially on its financial sector, are, in any case, interfering in India’s ties with Russia.

India has a philosophy of ‘vishwabandhu’- “friendship with all in the world”- which cannot be practiced in a revived Cold War-type global situation that has seen the virtual collapse of multilateralism. It would want to preserve its ties with Russia and build them further, even as it seeks to expand its ties with the US and Europe. This presents an increasingly difficult diplomatic challenge. India is not unaware of the complexities of the Ukraine conflict and the challenge of finding common ground between the diametrically opposed Ukrainian and Russian positions on issues of territory, Ukraine’s NATO membership, etc. The Ukrainian position has the support of the US, NATO and the EU, who continue to arm and fund Kiev. They remain determined that Russia must not be allowed to win the war as that would threaten the security of Europe. The issue goes well beyond Ukraine; it is one of a future security architecture of Europe that rejects Russia as a partner.

India is party to several UN resolutions, and formally subscribes to the rhetoric that sovereignty and territorial integrity, as well as international law and the UN Charter, should be respected; however, this does not offer a pathway to a resolution of the conflict in Ukraine. In any eventual resolution, some territorial adjustments will be inevitable, as will the security-related aspects inherent in the issue of Ukrainian membership in NATO. A security formula will have to be found outside the NATO framework. Modi has made it known on more than one occasion that he is ready to contribute to a peace process in Ukraine in whatever possible way. He reiterated that message at his summit meeting with Putin in July this year. In August, he visited Kiev with a view to closing the circle and pressing for the peace option.

That visit ended in some controversy. Zelensky pushed his 10 point peace plan,(add comma) and for establishing its peace credentials(remove semi-colon) Ukraine pressed India to join the communiqué issued at the end of the Peace Summit in Switzerland in June. India refused, stating publicly that Zelensky’s plan was not the only one to be considered, as other peace plans were also on the table, that all stakeholders had to be involved, and innovative solutions needed to be explored. India’s readiness to promote peace on consensual terms was reiterated. Be that as it may, by making a most uncomfortable trip to Ukraine, Modi created more diplomatic space for India, allowing it to manage Western pressures and shift from a perceived pro-Russian stance to a position of greater neutrality.

Modi has spoken to Biden about his Ukraine visit and has also briefed Putin. Talk of some form of Indian mediatory role in Ukraine gained attention after Putin said at the Eastern Economic Forum at Vladivostok last week that he and Modi had exchanged perspectives on the Ukraine conflict and insights from his visit to Kiev. Contrary to some commentary in India suggesting that Modi’s visit to Ukraine signaled a shift in India’s ties with Russia, Putin acknowledged these peace initiatives. He stated that he respected Russia’s friends and partners — especially China, Brazil, and India —which have genuinely sought to resolve the conflict and that he was in constant communication with them on this issue.

“..the premise that a person cannot be held criminally liable for third-party acts, is a naïve and utterly misguided approach.”

“..on another level he is just a computer nerd and his incoherent actions and statements are proof of that..”

• Durov Still Does Not Get It (Karganovic)

After being released on bail from a French prison, Russian entrepreneur Pavel Durov made several statements which indicate that he is labouring under grave illusions about the nature of his predicament. He described the action of the French authorities, which resulted in his arrest and detention on French territory, as “surprising and misguided.” He then went on to question the legal premise of his detention and subsequent indictment, which is that he could be held “personally responsible for other people’s illegal use of Telegram.”) It is disappointing to see a thirty-nine years old sophisticated cosmopolitan adult, traumatised as he must be by his recent experiences, reasoning like a child. One should have expected a person of Durov’s wealth to secure competent legal assistance to help him understand the legal “facts of life” pertaining to his case.

There are two basic facts that the lawyer selected by Durov to represent him should have explained to his client. Incidentally, that lawyer is extremely well wired into the French establishment and the judicial system which is persecuting his bewildered protégé. It would not be uncharitable to say that his loyalties are dubious. The first and most fundamental of these facts is the political nature of the case. Durov’s predicament cannot be properly understood apart from that reality. Recognition of that fact does not exclude entirely the effective use of legal arguments and remedies but it marginalises their practical impact. The second important fact that a conscientious legal professional already in the first interview would have made clear to his client is that in the real world in which Durov is facing grave criminal charges, indulging intuitive notions of justice, including the premise that a person cannot be held criminally liable for third-party acts, is a naïve and utterly misguided approach.

Pavel Durov is a highly intelligent and, in his field, very accomplished individual. But on another level he is just a computer nerd and his incoherent actions and statements are proof of that. Contrary to what he seems to think possible, and as incompatible as that may appear to be with the concept of natural justice, under specific circumstances an individual can be criminally charged for the acts of third parties. Mechanisms that make that possible already are firmly in place. We would not necessarily be wrong to characterise those mechanisms as repugnant to the natural sense of justice, or even as quasi-legal. But formally they are well established and are integral components of criminal law. Tyrannical political systems are free to invoke those instruments whenever they decide to target a bothersome non-conformist such as Pavel Durov.

Whilst on the one track relentless pressure is undoubtedly being applied to the conditionally released but still closely supervised Durov to accede to the demands of deep state structures and turn Telegram’s encryption keys over to security agencies, on a parallel track the legal case against him is being constructed. It will be based on some variant or derivative of the theory of strict liability. The exact contours of that variant are yet to be defined as the case proceeds, and everything will depend on how the defendant responds to the combination of carrots and sticks that are now being put in front of him.

Since no evidence is being offered to prove that acting personally in his capacity as Telegram CEO Durov was complicit in any of the incriminating activities listed in the charge sheet, the only conclusion that can be drawn is that some version of strict liability will be the vehicle of choice to make the accusations stick. Unless he capitulates, the objective is to put him away for a long time, or at least to threaten him credibly with such an outcome in order to exact his cooperation. Strict liability is a convenient tool because it offers many shortcuts to the Prosecution. It achieves the desired effect in the absence of proof of specific intent and regardless of the defendant’s mental state, thus eliminating for the prosecution major evidentiary hurdles.

“..in 1994 then-President Boris Yeltsin told his US counterpart, Bill Clinton, that “Russia has to be the first country to join NATO.”

• Russian Security Chief Explains West’s Key ‘Mistake’ (RT)

The US and its allies missed an opportunity to neutralize Russia by fully embracing it in the 1990s, Security Council Secretary Sergey Shoigu believes. In an interview with Rossiya-24 channel aired on Tuesday, the former defense minister recalled how in 1994 then-President Boris Yeltsin told his US counterpart, Bill Clinton, that “Russia has to be the first country to join NATO.” “If at that point they fast-tracked us into the European Union… I believe we would have lost our sovereignty by today. The resources and natural deposits that our country has would have been largely redistributed and snatched,” Shoigu said. Russia was in a deep financial hole in the mid 1990s and relied on foreign aid to remain afloat, so it would have willingly gone into the Western fold, if offered, the official argued.

Clinton Yeltsin 1996

Shoigu recalled that, at the time, he was monitoring the arrival of tranches of foreign subsidies to rush to the government and get some funding to pay salaries to workers at the Emergencies Ministry, which he headed. ”They’ve made a mistake. They should have gotten us into the EU as soon as possible. And we would be like the EU members: just a command from across the ocean, we would be folding our paws and getting ready to jump through a hoop,” Shoigu mused in this week’s interview. As an example of European compliance with US whims, Shoigu cited the scandal involving French helicopter carriers of the Mistral class, which Russia ordered in 2011 for its Navy.

The deal was called off after the 2014 armed coup in Kiev, an attempt to punish Moscow for accepting breakaway Crimea as a new Russian region. Washington pressured Paris into tearing up the contract with Russia by leveraging the size of a pending fine on a French bank, Shoigu claimed. He was apparently referring to the Paris-listed BNP Paribas, which in June 2014 agreed to enter a guilty plea with the Americans in a case of sanctions avoidance and to pay a $9 billion penalty to close the case. According to the French authorities, scrapping the Mistral deal at the last minute and selling the ships to Egypt instead came at a net loss of €409 million ($450 mn).

“The US is a country that doesn’t fulfill its obligations as a host country of the UN headquarters in the best way. So, it’s probably not the best place to travel right now..”

• Kremlin Explains Putin’s Decision on UN General Assembly (RT)

Russian President Vladimir Putin will not attend this year’s high-level session of the United Nations General Assembly in New York because the US is not a suitable host for such events, Kremlin spokesman Dmitry Peskov has said. The UN General Assembly opens on Tuesday and will end on September 30. It will culminate with a week of high-level events between September 23 and 27, which will feature speeches by numerous world leaders, including US President Joe Biden, British Prime Minister Keir Starmer, and French President Emmanuel Macron. Ukraine’s Vladimir Zelensky is also expected to attend and deliver a speech on September 25. Commenting on Moscow’s participation, Peskov signaled that Putin has no plans to fly to New York.

“He hasn’t gone there in recent years. The US is a country that doesn’t fulfill its obligations as a host country of the UN headquarters in the best way. So, it’s probably not the best place to travel right now,” the spokesman said. The last time Putin personally addressed a UN General Assembly session was in 2015, while in 2020 he delivered a pre-recorded speech at the event. After the start of the Ukraine conflict in February 2022, the US imposed sanctions on numerous top Russian officials, including Putin and Foreign Minister Sergey Lavrov. However, under the 1947 Headquarters Agreement between the US and the UN, Washington is obliged to grant diplomats and representatives of member states immunity and unimpeded access to UN headquarters.

Against this background, the Russian delegation to the UN General Assembly will be headed by Lavrov. Russian officials have on numerous occasions accused the US of failing in its UN obligations, pointing to long delays in issuing visas to Russian diplomatic personnel. In April 2023, the US also declined to grant entry to Russian journalists accompanying Lavrov to UN headquarters, with officials in Washington accusing them of spreading “propaganda.” Lavrov denounced the decision, claiming that the US “had done something stupid.” Washington, he added, “showed what its sworn assurances about protecting freedom of speech, access to information, and so on are really worth.”

“If an official summons is ignored, MPs may consider it a lack of respect for parliament, but this sanction is only symbolic..”

• Elon Musk May Be Summoned to UK Parliament for Questioning on X Activities (Sp.)

The British parliament may summon US entrepreneur Elon Musk to testify about the activities of his social network X, in particular on the issue of moderation and the fight against hateful content, Financial Times reported on Monday. Ruling Labour Party parliamentarian Dawn Butler told the newspaper that the American entrepreneur would be invited as a witness. Butler is running to head the parliamentary science and technology committee, the publication said. Such committees examine the activities of ministers, civil servants and leading figures in a particular field within the framework of a certain issue. “It is vital for the committee to formally examine the use of algorithms in pushing hateful material — and the moderation of such content — on X and other social media platforms,” Butler said.

The British lawmakers can summon someone to answer questions from the committee, but they cannot force them to attend. If an official summons is ignored, MPs may consider it a lack of respect for parliament, but this sanction is only symbolic, the publication says. In August, British officials complained that X did not cooperate with the authorities in removing posts that posed a threat to national security during the wave of unrest. Musk himself, against the backdrop of mass protests in Britain, predicted a civil war in the country, a statement that caused discontent in London.

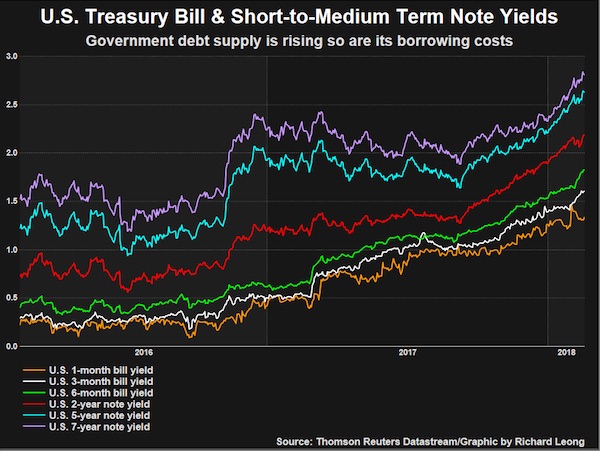

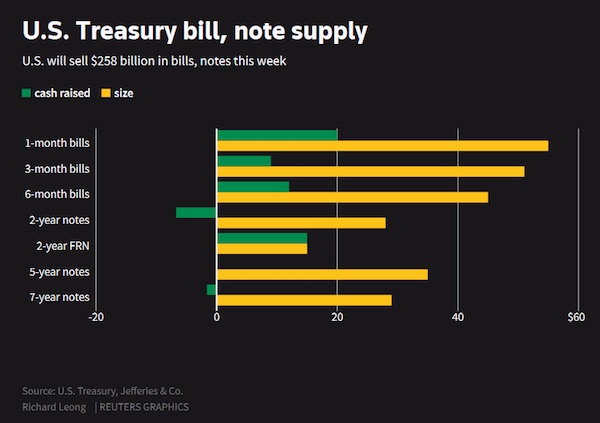

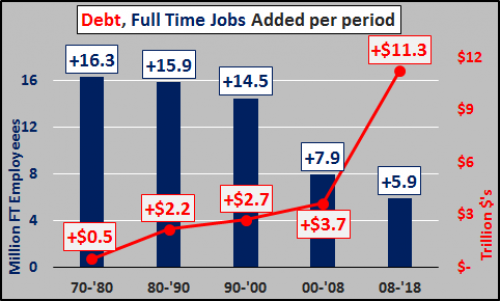

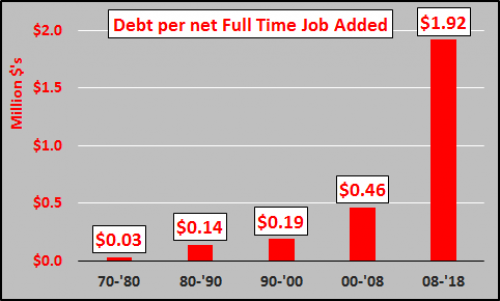

“..the US would have to pay over $1.2 trillion in interest on the debt in the coming 12 months, which is reportedly equal to about 25% of government revenue..”

• US ‘Going Bankrupt Extremely Quickly’ – Musk (RT)

The cost of servicing the vast US federal debt now outstrips the defense budget, Tesla and SpaceX CEO Elon Musk has claimed in an interview with the All-In podcast. He added that the country is “going bankrupt extremely quickly.” The US Treasury announced in late July that the national debt had surpassed $35 trillion, having soared by a trillion in a six-month period. In June, the US House Of Representatives passed its version of the annual defense policy bill that authorizes a record $895 billion in spending, marking an increase of 1% compared to the previous fiscal year. “Interest payments on the national debt are now higher than the entire Defense Department budget and rising,” Musk said, warning that the US is “going bankrupt extremely quickly.”

The tycoon stressed that every trillion dollars of debt added is money that “our kids and grandkids are going to have to pay somehow.” Earlier this week, the tech billionaire shared a post on his X platform (formerly Twitter) by an account focused on finance and economics, stating that the US would have to pay over $1.2 trillion in interest on the debt in the coming 12 months, which is reportedly equal to about 25% of government revenue. Earlier this month, Musk warned that the current rate of government spending was putting the US in the fast lane to bankruptcy, and that government overspending was stoking inflation. In August, the US Labor Department reported that annual inflation had dipped below 3% in the previous month for the first time since 2021. Prices of goods and services went up by 2.9%, while core inflation, which excludes the food and energy industries, rose by 3.2% over the previous 12 months.

Barry Soetoro

Former FBI agent, John D'Souza, explains who Barack Obama really is.

Barry Soetoro was an asset for many intelligence agencies at the same time before being installed as the President of the United States. pic.twitter.com/x1SchLHgCu

— SULLY (@SULLY10X) September 9, 2024

Vaxx

https://twitter.com/i/status/1833228842967679054

Swan

swan landing on water pic.twitter.com/MdGMD6NrcO

— Nature is Amazing ☘️ (@AMAZlNGNATURE) September 10, 2024

Horse

Leadership between a human and horse crosses the prey/predatory barrier.

Horses are natural followers; they're looking for a natural leader.

And the size of the leader really doesn't mean anything.https://t.co/x9TcjHI8JH

— Massimo (@Rainmaker1973) September 10, 2024

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.