Louise Dahl-Wolfe Looking at Matisse, Museum of Modern Art 1939

Oh, that’s what the tax cuts are for?!

• S&P 500 Companies Return $1 Trillion To Shareholders In Tax-Cut Surge (R.)

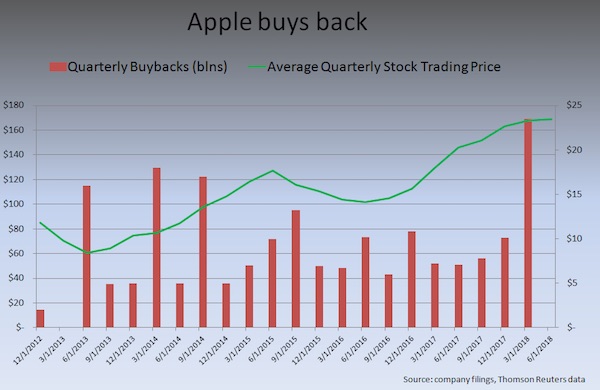

S&P 500 companies have returned a record $1 trillion to shareholders over the past year, helped by a recent surge in dividends and stock buybacks following sweeping corporate tax cuts introduced by Republicans, a report on Friday showed. In the 12 months through March, S&P 500 companies paid out $428 billion in dividends and bought up $573 billion of their own shares, according to S&P Dow Jones Indices analyst Howard Silverblatt. That compares to combined dividends and buybacks worth $939 billion during the year through March 2017, Silverblatt said in a research note. Earnings per share of S&P 500 companies surged 26 percent in the March quarter, boosted by the Tax Cuts and Jobs Act passed by Republican lawmakers in December.

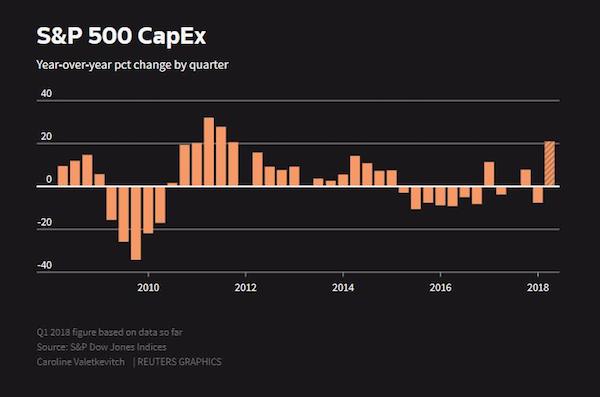

Companies have been returning much of that profit windfall to shareholders via share buybacks and increased dividends at never before seen amounts, highlighted by Apple’s record $23.5 billion worth of shares repurchased in the first quarter. S&P 500 companies have also plowed some of the windfall from lower taxes into investments toward growth or becoming more efficient. First-quarter capital expenditures totaled at least $159 billion, up more than 21 percent from the year before, according to S&P Dow Jones Indices. The biggest overhaul of the U.S. tax code in over 30 years, the new law slashes the corporate income tax rate to 21 percent from 35 percent, and charges multinationals a one-time tax on profits held overseas.

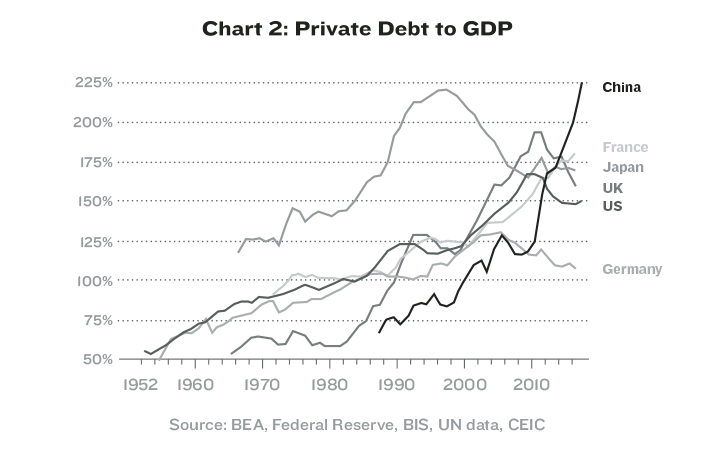

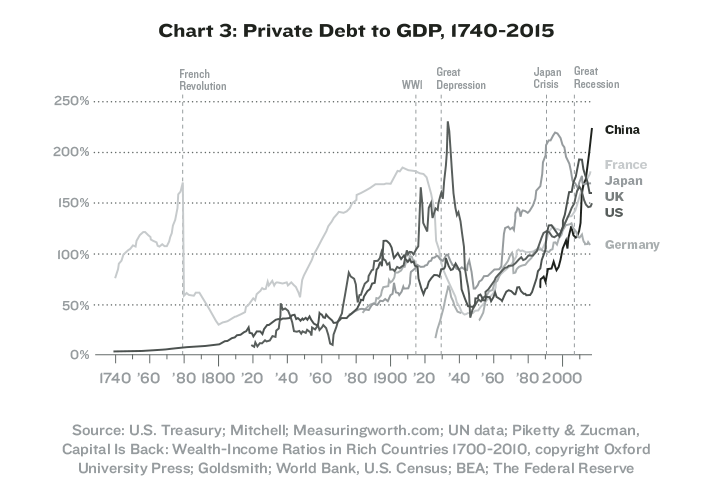

Mauldin turns dark side.

• The 2020s Might Be The Worst Decade In US History (Mauldin)

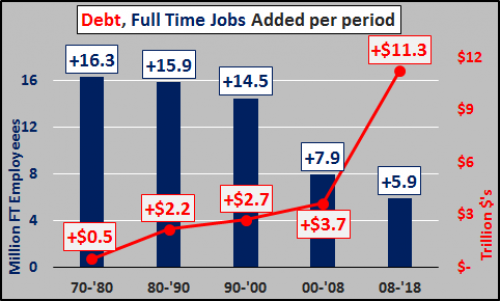

I recently wrote about a looming credit crisis that’s stemming from high-yield junk bonds. The crisis itself will have massive consequences for investors. But that’s not the worst part. The crisis will create a domino effect and trigger global financial contagion, which I usually refer to as “The Great Reset.” The collapse of high-yield bonds will hit stocks and bonds. Rising defaults will force banks to reduce their lending exposure, drying up capital for previously creditworthy businesses. This will put pressure on earnings and reduce economic activity. A recession will follow. This will not be just a U.S. headache, either. It will surely spill over into Europe (and may even start there) and then into the rest of the world.

The U.S. and/or European recession will become a global recession, as happened in 2008. Europe has its own set of economic woes and multiple potential triggers. It is quite possible Europe will be in recession before the ECB finishes this tightening cycle. As always, a U.S. recession will spark higher federal spending and reduce tax revenue. So I expect the on-budget deficit to quickly reach $2 trillion or more. Within four years of the recession’s onset, total government debt will be at least $30 trillion. This will further constrain the private capital markets and likely raise tax burdens for everyone—not just the rich.

Meanwhile, job automation will intensify, with businesses desperate to cut costs. The effect we already see on labor markets will double or triple. Worse, it will start reaching deep into the service sector. The technology is improving fast. The working-class population will not like this and it has the power to vote. “Safety net” programs and unemployment benefit expenditures will skyrocket. Studies show that the ratio of workers covered by unemployment insurance is at its lowest level in 45 years. What happens when millions of freelancers lose their incomes?

We’re talking trillions. Poof!

• Moody’s Warns Of ‘Particularly Large’ Wave Of Junk Bond Defaults Ahead (CNBC)

With corporate debt hitting its highest levels since before the financial crisis, Moody’s is warning that substantial trouble is ahead for junk bonds when the next downturn hits. The ratings agency said low interest rates and investor appetite for yield has pushed companies into issuing mounds of debt that offer comparatively low levels of protection for investors. While the near-term outlook for credit is “benign,” that won’t be the case when economic conditions worsen. The “prolonged environment of low growth and low interest rates has been a catalyst for striking changes in nonfinancial corporate credit quality,” Mariarosa Verde, Moody’s senior credit officer, said in a report.

“The record number of highly leveraged companies has set the stage for a particularly large wave of defaults when the next period of broad economic stress eventually arrives.” Though the current default rate is just 3 percent for speculative-grade credit, that has been predicated on favorable conditions that may not last. Since 2009, the level of global nonfinancial companies rated as speculative, or junk, has surged by 58 percent, to the highest ever, with 40 percent rated B1 or lower, the point that Moody’s considers “highly speculative,” as opposed to “non-investment grade speculative.” In dollar terms, that translates to $3.7 trillion in total junk debt outstanding, $2 trillion of which is in the B1 or lower category.

“Strong investor demand for higher yields continues to allow all but the weakest issuers to avoid default by refinancing maturing debt,” Verde wrote. “A number of very weak issuers are living on borrowed time while benign conditions last.” The level of speculative-grade issuance peaked in the U.S. in 2013, at $334.5 billion, according to the Securities Industry and Financial Markets Association. American companies have $8.8 trillion in total outstanding debt, a 49 percent increase since the Great Recession ended in 2009.

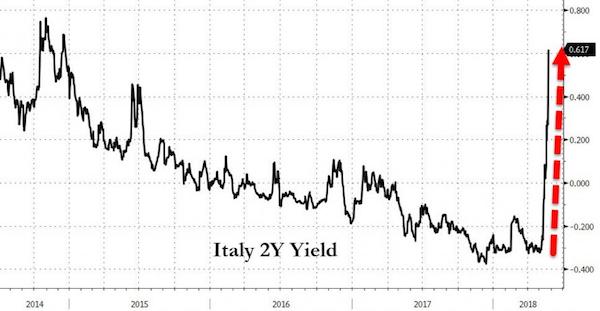

President Mattarella has refused to accept the nominee for finance minister, Savona. He’s a euroskeptic.

Meanwhile, if Italian bonds are downgraded further, Europe has a massive problem.

• Moody’s Puts Italy On Downgrade Review, Junk Rating Possible (ZH)

In a quite direct ‘threat’ to the newly formed Italian coalition, Moody’s warned that Italy will face a downgrade from its current Baa2 rating (potentially more than one notch to junk status) due to the lack of fiscal restraint in the new “contract” and the potential for delays to Italy’s structural reforms. While Italy’s current rating is Baa2, and a downgrade would leave it at Baa3 (still investment grade), one look at Italian debt markets this week and one can be forgiven for thinking it is pricing in a multiple-notch downgrade to junk… and thus potentially making things awkward for its ECB bond-buying-benefactor and its banking system’s massive holdings of sovereign bonds.

Full Moody’s Report: Moody’s Investors Service has today placed the Government of Italy’s ratings on review for possible downgrade. Ratings placed under review are the Baa2 long-term issuer and senior unsecured bond ratings as well as the (P) Baa2 medium-term MTN programme, the (P)Baa2 senior unsecured shelf, the Commercial Paper and other short-term ratings of Prime-2/(P) Prime-2 respectively. The key drivers for today’s initiation of the review for downgrade are as follows: 1. The significant risk of a material weakening in Italy’s fiscal strength, given the fiscal plans of the new coalition government; and 2. The risk that the structural reform effort stalls, and that past reforms such as the pension reforms implemented in 2011 are reversed.

Moody’s will use the review period to assess the impact of the fiscal and economic policy platform of the new government on Italy’s credit profile, with a particular focus on the effect on the deficit and debt trajectories in the coming years. The review will also allow Moody’s to assess further whether the new government intends to continue to pursue growth-enhancing structural reforms, or conversely to reverse earlier reforms, such as the 2011 pension reform, as well as other economic policy initiatives in the coming months that may have an incidence on the country’s growth potential over the coming years.

What do you mean we can’t blame the weather?

• UK Economy Posts Worst Quarterly GDP Figures For Five Years (G.)

The weakest household spending for three years and falling levels of business investment dragged the economy to the worst quarter for five years, official statisticians have said. The Office for National Statistics confirmed its previous estimate that GDP growth slumped to 0.1% in the first quarter, while sticking to its view that the “beast from the east” had little impact. The latest figures will further stoke concerns over the strength of the UK economy, amid increasing signals for deteriorating growth as Britain prepares to leave the EU next year. Some economists, including officials at the Bank of England, thought the growth rate would be revised higher as more data became available.

Threadneedle Street delayed raising interest rates earlier this month after the weak first GDP estimate, despite arguing that the negative hit to the economy from heavy snowfall in late February and early March had probably been overblown. Instead the ONS said it had seen a longer-term pattern of slowing growth in the first three months of the year. Rob Kent-Smith of the ONS said: “Overall, the economy performed poorly in the first quarter, with manufacturing growth slowing and weak consumer-facing services.” While admitting bad weather will have had some impact, particularly for firms in the construction industry and some areas of the retail business, statisticians said the overall effect was limited, with increased online sales and heightened energy production during the cold snap.

The figures show the services industries contributed the most to GDP growth, with an increase of 0.3% in the first quarter, while household spending grew at a meagre 0.2%. The construction industry declined by 2.7% and business investment fell by 0.2%.

“..an advance team of 30 White House and State Department officials was preparing to leave for Singapore later this weekend..”

• Prospects of US-North Korea Summit Brighten (R.)

Prospects that the United States and North Korea would hold a summit brightened after U.S. President Donald Trump said late on Friday Washington was having “productive talks” with Pyongyang about reinstating the June 12 meeting in Singapore. Politico magazine reported that an advance team of 30 White House and State Department officials was preparing to leave for Singapore later this weekend. Reuters reported earlier this week the team was scheduled to discuss the agenda and logistics for the summit with North Korean officials. The delegation was to include White House Deputy Chief of Staff Joseph Hagin and deputy national security adviser Mira Ricardel, U.S. officials said, speaking on condition of anonymity.

Trump said in a Twitter post late on Friday: “We are having very productive talks about reinstating the Summit which, if it does happen, will likely remain in Singapore on the same date, June 12th., and, if necessary, will be extended beyond that date.” Trump had earlier indicated the summit could be salvaged after welcoming a conciliatory statement from North Korea saying it remained open to talks. “It was a very nice statement they put out,” Trump told reporters at the White House. “We’ll see what happens – it could even be the 12th.” “We’re talking to them now. They very much want to do it. We’d like to do it,” he said.

Through Kimberley Strassel, the Wall Street Journal distances itself ever more from the MSM.

• The Real ‘Constitutional Crisis’ (Strassel)

Democrats and their media allies are again shouting “constitutional crisis,” this time claiming President Trump has waded too far into the Russia investigation. The howls are a diversion from the actual crisis: the Justice Department’s unprecedented contempt for duly elected representatives, and the lasting harm it is doing to law enforcement and to the department’s relationship with Congress. The conceit of those claiming Mr. Trump has crossed some line in ordering the Justice Department to comply with oversight is that “investigators” are beyond question. We are meant to take them at their word that they did everything appropriately. Never mind that the revelations of warrants and spies and dirty dossiers and biased text messages already show otherwise.

We are told that Mr. Trump cannot be allowed to have any say over the Justice Department’s actions, since this might make him privy to sensitive details about an investigation into himself. We are also told that Congress – a separate branch of government, a primary duty of which is oversight – cannot be allowed to access Justice Department material. House Intelligence Committee Chairman Devin Nunes can’t be trusted to view classified information – something every intelligence chairman has done – since he might blow a source or method, or tip off the president. That’s a political judgment, but it holds no authority. The Constitution set up Congress to act as a check on the executive branch—and it’s got more than enough cause to do some checking here.

Yet the Justice Department and Federal Bureau of Investigation have spent a year disrespecting Congress—flouting subpoenas, ignoring requests, hiding witnesses, blacking out information, and leaking accusations. Senate Judiciary Chairman Chuck Grassley has not been allowed to question a single current or former Justice or FBI official involved in this affair. Not one. He’s also more than a year into his demand for the transcript of former national security adviser Mike Flynn’s infamous call with the Russian ambassador, as well as reports from the FBI agents who interviewed Mr. Flynn. And still nothing.

[..] Mr. Trump has an even quicker way to bring the hostility to an end. He can – and should – declassify everything possible, letting Congress and the public see the truth. That would put an end to the daily spin and conspiracy theories. It would puncture Democratic arguments that the administration is seeking to gain this information only for itself, to “undermine” an investigation. And it would end the Justice Department’s campaign of secrecy, which has done such harm to its reputation with the public and with Congress.

“..a malevolent secret police operation..”

• A Mendacious Exercise In Manufacturing Paranoia (Jim Kunstler)

After many months, the gaslight is losing its mojo and a clearer picture has emerged of just what happened during and after the 2016 election: the FBI, CIA, and the Obama White House colluded and meddled to tilt the outcome and, having failed spectacularly, then labored frantically to cover up their misdeeds with further misdeeds. The real election year crimes for which there is actual evidence point to American officials not Russian gremlins. Having attempted to incriminate Trump at all costs, these tragic figures now scramble to keep their asses out of jail.

I say “tragic” because they — McCabe, Comey, Rosenstein, Strzok, Page, Ohr, et al — probably think they were acting heroically and patriotically to save the country from a monster, and I predict that is exactly how they will throw themselves to the mercy of the jury when they are called to answer for these activities in a court of law. Of course, they have stained the institutional honor of the FBI and its parent Department of Justice, but it is probably a healthier thing for the US public to maintain an extremely skeptical attitude about what has evolved into a malevolent secret police operation.

The more pressing question is how all this huggermugger gets adjudicated in a timely manner. Congress has the right to impeach agency executives like Rod Rosenstein and remove them from office. That would take a lot of time and ceremony. They can also charge them with contempt-of-congress and jail them until they comply with committee requests for documents. Mr. Trump is entitled to fire the whole lot of the ones who remain. But, finally, all this has to be sorted out in federal court, with referrals made to the very Department of Justice that has been a main actor in this tale.

The most mysterious figure in the cast is the MIA Attorney General, Jeff Sessions, who has become the amazing invisible man. It’s hard to see how his recusal in the Russia matter prevents him from acting in any way whatsoever to clean the DOJ house and restore something like operational norms — e.g. complying with congressional oversight — especially as the Russia matter itself resolves as a completely fabricated dodge. The story is moving very fast now. The Pequod is whirling around in the maelstrom, awaiting the final blow from the white whale’s mighty flukes.

Gullible?

• Tesla Seeks To Dismiss Securities Fraud Lawsuit (R.)

Tesla Inc on Friday asked a court to dismiss a securities fraud lawsuit by shareholders who said the electric vehicle maker gave false public statements about the progress of producing its new Model 3 sedan. In a filing in federal court in San Francisco, Tesla said that its statements about the challenges the company faced with Model 3 were “frank and in plain language,” including repeated disclosures by Chief Executive Elon Musk of “production hell.” Tesla did not seek to hide the truth, its motion to dismiss said. The company says its Model 3 has experienced numerous “bottlenecks” from problems with Tesla’s battery module process at its Nevada Gigafactory to general assembly at its Fremont plant.

Tesla is under pressure to deliver the Model 3 to reap revenue and stem massive spending that has put Tesla’s finances in the red. The ramp of the Model 3, Tesla said in the court filing, was “the first of its kind,” with difficulties likely to crop up after it got underway. The lawsuit filed last October seeks class action status for shareholders who bought Tesla stock between May 4, 2016 through October 6, 2017, inclusive. It said shareholders bought “artificially inflated” shares because Musk and other executives misled them with their statements. Tesla made such statements during the lead-up to, and early production of, its Model 3 sedan and failed to disclose that the company was “woefully unprepared” for the vehicle’s production, the lawsuit said.

Good on ’em! Cars don’t belong in cities.

• Madrid Takes Its Car Ban to the Next Level (CityLab)

The days when cars could drive unhindered through central Madrid are coming to a close. Following an announcement this week, the Spanish capital confirmed that, starting in November, all non-resident vehicles will be barred from a zone that covers the entirety of Madrid’s center. The only vehicles that will be allowed in this zone are cars that belong to residents who live there, zero-emissions delivery vehicles, taxis, and public transit. Even on a continent where many cities are scaling back car access, the plan is drastic. While much of central Madrid consists of narrow streets that were never suitable to motor vehicles in the first place, this central zone also includes broad avenues such as Gran Via, and wide squares that have been islands in a sea of surging traffic for decades.

The plan is thus not just about making busy central streets more pleasant, but about creating a situation where people simply no longer think of bringing their cars downtown. This might come as a shock to some drivers, but the wind has been blowing this way for more than a decade. Madrid set up the first of what it calls Residential Priority Zones in 2005, in the historic, densely packed Las Letras neighborhood. Since then, a modest checkerboard of three other similar zones have been installed across central Madrid. The new area will be a sort of all-encompassing zone that abolishes once and for all the role of downtown streets as through-routes across the city.

To get people used to the idea, implementation of the non-local car ban will be staggered. In November, manual controls by police around the zone’s edge will begin. Cars that are breaching the new rules will be warned of the fine they face in the future—€90 per occurrence—without actually being charged then. In January, a fully automated system with cameras will be put in place, and from February, the €90 will be actively enforced against any cars found breaking the rules.