René Magritte The Pleasure Principle (Portrait of Edward James) 1937

50 days to Brexit. Don’t be surprised if that whole country dissolves before our eyes.

Perfect name, good actions.

At 5.55am, Talgarth Road, one of the major arteries into west London, is just beginning to clog up with early rush-hour traffic. A man named Dave, his white van pulled over into a loading bay, is putting up a billboard poster by the side of the carriageway. The previous one was an advert for Calvin Klein featuring the model Lara Stone. Over the course of 20 minutes, Dave covers Stone up, expertly pasting rectangles of paper over her, using a ladder for the high ones, then sweeping over with his brush. The first rectangle, in the top left corner, contains a headshot of Jacob Rees-Mogg and the beginning of his Twitter handle. As Dave lines up edges, pastes and brushes, and Stone disappears, a quote emerges from Rees-Mogg.

This one wasn’t a tweet; he said it in parliament. “We could have two referendums. As it happens, it might make more sense to have a second referendum after the renegotiation is completed.” There are three other men here, dressed in hoodies, lumberjack shirts and beanies, lurking around and admiring the work. Their work – because Richard, Adam and Chris are three of the four key people behind Led By Donkeys, the remainer guerrilla activists highlighting the hypocrisy and lies of politicians by posting their damning quotes on billboards around the country. Less guerrilla now, actually: they’ve gone legit, this hoarding is paid for. Before, they just took them over.

[..] It all began, as most good ideas do, in the pub. They were talking about the infamous David Cameron tweet – “Britain faces a simple and inescapable choice – stability and strong government with me or chaos with Ed Miliband” – which was doing the rounds again after Theresa May cancelled the vote on her deal in December. And someone said: why don’t they slap it on a billboard, make it the tweet you can’t delete? The next day, on the WhatsApp group, one of them said they had found someone who would print it out for them. They all agreed: “Let’s just fucking do it.” It was cheaper to do five, so they cobbled together four more tweets – from Michael Gove, David Davies, John Redwood and Liam Fox – not really thinking they’d ever put them up. Initial outlay was about 200 quid, plus £90 on a ladder from B&Q.

Tusk is an idiot, but he was right when he said thet as both May and Corbyn want to Leave, there is no political leadership for Remain. But the majority of Britons by now want to Remain. Don’t underestimate the danger of this.

• Tusk: Special Place In Hell For Brexiteers Without Even Sketch Of A Plan (Ind.)

A war of words has further undermined Theresa May’s mission to Brussels to rescue her Brexit deal, after the EU warned of a “special place in hell” for politicians who botched the project. Downing Street and Tory politicians hit back angrily after the extraordinary attack by Donald Tusk on those who triumphed in the referendum “without even a sketch of a plan how to carry it safely”. The prime minister’s spokesman urged people to ask whether such language was “helpful” – before noting, sarcastically, that was impossible “because he didn’t take any questions”. Andrea Leadsom, the Commons leader, condemned the comments by Mr Tusk, the European Council president, as “disgraceful” and “spiteful”, saying such behaviour “demeans him”.

Sammy Wilson, Brexit spokesman of the Democratic Unionist Party (DUP), which props up the Tories in power, went further – branding him a “devilish, trident-wielding, Euro maniac”. But pro-EU Tory Anna Soubry backed him and named Boris Johnson, David Davis and Nigel Farage as among his likely targets, for having “abdicated all responsibility”. The fury overshadowed the tough message for Ms May before she lands in Brussels on Thursday morning – that the EU will never agree to reopening the divorce deal, as she has vowed to do. The prime minister will again demand either an end date for the Irish backstop or an exit mechanism from it for there to be any hope of the Commons passing the deal. Ms May appeared to drop her third option – replacing the backstop with ill-defined “alternative arrangements”, based on unproven technology – to the anger of some Brexiteer Tories.

Vote Corbyn, get May.

• Corbyn Lays Out Labour’s Terms For Backing May On Brexit (G.)

Jeremy Corbyn has written to the prime minister, offering to throw Labour’s support behind her Brexit deal if she makes five legally binding commitments – including joining a customs union. The Labour leader held private talks with Theresa May last week for the first time since her deal was rejected by a historic margin of 230 votes in January. In a follow-up letter sent on Wednesday, he laid out in the clearest terms yet what commitments he is seeking in exchange for offering Labour support. His intervention will dismay backbench Labour MPs and grassroots activists still hoping he will switch the party’s policy towards demanding a second Brexit referendum – which is not mentioned in the letter.

And it comes as No 10 prepares to publish legislation underpinning workers’ rights, perhaps as early as next week, in an attempt to win support from Labour backbenchers. In his letter, Corbyn calls for the government to rework the political declaration setting the framework for Britain’s future relationship with the EU – and then enshrine these new negotiating objectives in UK law, so that a future Tory leader could not sweep them away after Brexit. He says the changes to the political declaration must include:

• A “permanent and comprehensive UK-wide customs union”, including a say in future trade deals.

• Close alignment with the single market, underpinned by “shared institutions”.

• “Dynamic alignment on rights and protections”, so that UK standards do not fall behind those of the EU.

• Clear commitments on future UK participation in EU agencies and funding programmes.

• Unambiguous agreements on future security arrangements, such as use of the European arrest warrant.

Britain can no longer manage with two parties. Same as so many countries.

• Not Opposing Brexit Could Lose Labour 45 Seats (G.)

A trade union affiliated with the Labour party has claimed that Jeremy Corbyn’s party could lose an additional 45 seats in a snap election if it fails to take an anti-Brexit position, in a leaked report. The report, drawn up by the transport union TSSA and including extensive polling, was sent to the leftwing pressure group Momentum. It appears to be an attempt to pile pressure on the Labour leader over Brexit. It claims that “Brexit energises Labour remain voters” disproportionately, and warns: “There is no middle way policy which gets support from both sides of the debate.” The Guardian understands that while the report was sent to Momentum, it was not commissioned or requested by the group.

Sources inside the party stressed that there were risks from turning either way on Brexit – and other polls showed a different picture. The document – marked strictly confidential – says: “There can be no disguising the sense of disappointment and disillusionment with Labour if it fails to oppose Brexit and there is every indication that it will be far more damaging to the party’s electoral fortunes than the Iraq war. “Labour would especially lose the support of people below the age of 35, which could make this issue comparable to the impact the tuition fees and involvement in the coalition had on Lib Dem support.” The document starts by pointing out that the TSSA has “supported Jeremy Corbyn’s leadership from the very beginning”.

It says that the party’s supporters view Brexit as a “Tory project”. It adds that four-fifths of them believe the current deal will hurt the British economy and 91.4% of Labour voters do not trust the government to deliver a good Brexit for people such as them.

Only in hindsight will Americans see the damage done by these people.

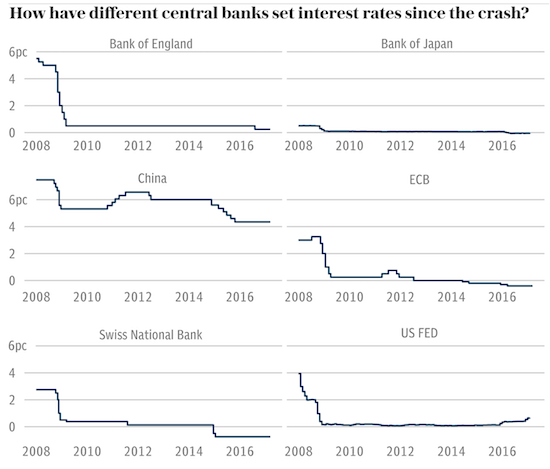

• Yellen: Next Fed Move May Be A Rate Cut (CNBC)

The Federal Reserve’s next move may well be an interest rate cut if weakening growth around the world starts infecting the U.S. economy, former central bank Chair Janet Yellen said Wednesday. Weakening economies in China and Europe are posing danger to an otherwise strong U.S. economy, Yellen told CNBC’s Steve Liesman during a “Power Lunch” interview. “Of course it’s possible. If global growth really weakens and that spills over to the United States where financial conditions tighten more and we do see a weakening in the U.S. economy, it’s certainly possible that the next move is a cut,” she said. “But both outcomes are possible.” The former central bank head cited “slowing global growth” as the biggest threat to the economy she once watched over. “The data from China has been recently weak, the European data has also come in weaker than expected,” she said.

The very last people who should conduct such tests.

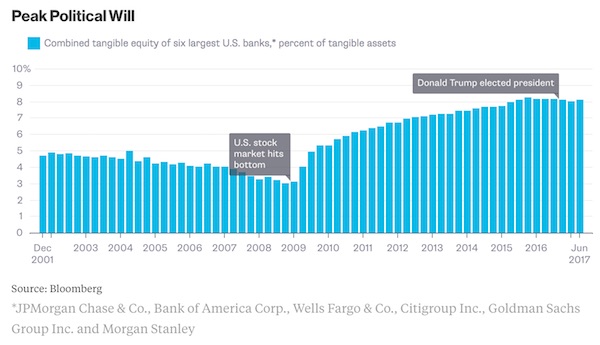

• Fed’s Quarles Sees 2019 As An ‘Interim’ Year For Bank Stress Tests (R.)

U.S. bank stress tests conducted during an “interim” period this year will help the Federal Reserve decide what permanent changes to make to the closely followed examinations, the Fed’s point person on financial supervision Randal Quarles said on Wednesday. On Tuesday the Fed said it would make its stress testing of large banks more transparent in 2019, providing financial firms significantly more information about how their portfolios would perform under potential economic shocks. The changes respond to long-running bank complaints that the current stress-testing process is cumbersome and opaque. Less complex banks with assets between $100 billion and $250 billion, such as SunTrust Banks and Fifth Third Bancorp, do not have to face 2019 stress tests, as the Fed is moving to a two-year cycle for testing those firms.

“Our challenge now is to preserve the strength of the test, while improving its efficiency, transparency, and integration into the post-crisis regulatory framework,” Federal Reserve Vice Chairman of Supervision Randal Quarles said in remarks prepared for delivery at a Council for Economic Education event in New York. “Our experience with this ‘interim’ year will inform the move to a permanently longer testing cycle – a change that would, of course, be subject to a full notice and comment process.” The 2019 tests also include factoring in a jump to 10 percent unemployment from the current 4 percent rate, as well as elevated stress in corporate loan and commercial real estate markets in the most severe scenario.

The press, including WaPo, have changed tactics. They no longer try for a larger audience, they make their existing readers more faithful. More subscribers, much ‘better’ targeted ads.

• Press Needs More Than Super Bowl Ad To Fix Its Plunging Credibility (ZH)

Media Bias: While journalists are getting pink slips across the country, the Washington Post decided to dump a boatload of cash for a Super Bowl image ad that tried to portray the news media as national heroes. Here’s a better, and much cheaper, idea to restore the industry’s shattered reputation: Be less blatantly partisan. In the 60-second ad, Tom Hanks intones about the importance of journalists against the backdrop of historic events. Thankfully, during these times, the ad says, “There’s someone to gather the facts. To bring you the story. No matter the cost. Because knowing empowers us. Knowing helps us decide. Knowing keeps us free.” The problem with journalists today, however, is that they aren’t interested in gathering facts or empowering the public with knowledge.

Instead, they are interested mainly in pushing their agenda — a basic failing of the profession brought into high relief over the past two years. The latest IBD/TIPP Poll makes this abundantly clear. The poll asked several questions to gauge the public’s perception of the mainstream news media. What did it find? First, that fully half the country says its trust in the media decreased over the past two years. A tiny 8% say it’s increased. That includes a plurality of independents (49%). Even among Republicans, who’ve long grown accustomed to media bias, 81% say their trust in the press has dropped over the past two years. Geographically, those in the Midwest and the South are mostly likely to say their trust in the press has declined (52% and 57%, respectively) since Trump took office.

Men are far more likely than women (54% vs. 47%). And those with incomes over $75,000 (51% of home distrust the media more) more than lower-income households. These findings alone should be alarming. After all, as any corporate executive knows, you can’t run a successful business when a vast and increasing share of your customer base doesn’t trust the product you are selling. It gets worse. The poll found that more than two-thirds of the public (69%) think the news media “is more concerned with advancing its points of view rather than reporting all the facts.” Only 29% of the public disagrees with that statement. In other words, nearly seven out of 10 adults in the country think the Post ad’s blather about “gathering the facts” is bull. That includes 72% of independents, 95% of Republicans, and — surprisingly enough — 43% of Democrats.

And how can the press pull off its tricks? Easy as pie. Edward Bernays and Goebbels.

Given the right circumstances… a little programing… and enough time for it all to marinate in his soft, mammalian brain… there is almost nothing Homo Credulus will not learn to embrace. Don’t believe us? Take a look at the historical record; you’ll soon wonder how we ever got this far. Sure, you’ll discover gizmos and flying contraptions… art and agriculture… music and mathematics. You’ll witness spectacular scientific breakthroughs, the number “0” and a man’s footprint on the moon. You’ll also find automobiles with so many cup holders, you won’t know where to holster your oversized 7/11 Big Gulp. But you’ll also scratch you head. Perhaps you’ll even weep. And if you think hard enough, you’ll put a few things to serious question…

“Central banks?” “Modern democracy?” “The Rosie O’Donnell Show?” How has mankind survived such atrocities? Self inflicted, no less! And why, moreover, does he rush so earnestly to repeat and replay his worst mistakes? Don’t be too hard on yourself, Dear Reader. After all, repetition is nothing new… You’ll recall that it was the Greeks who first gave the world democracy – from the Greek, demokratia, literally “Rule by ‘People’”. (And yes, it was those very same Greeks who put their own beloved Socrates to death… by a majority vote of 140-361.) Today, democracy is a cherished tenet of “the West.” It is woven into the civic religion, sewn into the social fabric. Men march off eagerly to fight for it, to proselytize it … and to die in forgotten ditches defending it. At least, that’s what they believe they’re doing. As usual, the poor saps have been duped.

The phrase “Making the world safe for democracy” was actually a marketing slogan, coined back in the 1910s, as a way to sell “The Great War” to America. Weary from their own disastrous Civil War just a few decades earlier, in which hundreds of thousands gave up the ghost, Americans were mostly inward looking at the time. That is to say, they wanted little to do with what they largely saw as a “European affair.” Polls might have indicated no appetite for battle… but the nation’s politicians were nonetheless starved for military misadventure. They sensed big profits abroad, both in manufacturing armaments and making onerous bank loans to foreign lands. Sure, “the nation” would have to fill tank and trench with warm young bodies… but very few soldiers would carry senatorial surnames along with their rifles.

Too late already. A deliberate Monsanto policy.

• French, German Farmers Must Destroy Crops After GMOs Found In Monsanto Seeds (RT)

French and German farmers have been forced to dig up thousands of hectares of rapeseed fields after authorities found an illegal GMO strain mixed in with the natural seeds they’d bought from Bayer-Monsanto. Authorities discovered the illicit seeds in three separate batches of rapeseed seeds last fall, but the public has only just been notified. While Bayer issued a recall, by the time the farmers learned of it some of the seeds had already been planted, covering 8,000 ha in France and 3,000 ha in Germany. Bayer-Monsanto estimated the number of rogue seeds at just about .005 percent of the total volume of rapeseed seeds sold to both nations under the brand name Dekalb, but each country has a ban on GMO cultivation, with strict penalties for “accidental” contamination of standard crops.

The agrochemical giant refused to estimate the total cost of the GMO contamination, which knocks out not only this season’s crop but also the next season’s, as farmers will be barred from growing rapeseed next year “to avoid re-emergence of the GMO strain,” according to Bayer-Monsanto’s French COO Catherine Lamboley. They offered to compensate farmers €2,000 per hectare, which would work out to about €20 million between both countries. The cause of the contamination is unknown, Lamboley said, claiming the seeds were produced in Argentina “in a GMO-free area” and declaring that the company “has decided to immediately stop all rapeseed production in Argentina.” The rogue GMO seeds were of a variety grown in Canada that is banned in Europe, although imported food made with the modified rapeseed is permitted for human and animal consumption as long as it is adequately labeled.

Except those farmed.

• The Killing Of Large Species Is Pushing Them Towards Extinction (G.)

The vast majority of the world’s largest species are being pushed towards extinction, with the killing of the heftiest animals for meat and body parts the leading cause of decline, according to a new study. While habitat loss, pollution and other threats pose a significant menace to large species, also known as megafauna, intentional and unintentional trapping, poaching and slaughter is the single biggest factor in their decline, researchers found. An analysis of 362 megafauna species found that 70% of them are in decline, with 59% classed as threatened by the International Union for Conservation of Nature. Direct killing by humans is the leading cause across all classes of animals, the study states.

A range of maladies including intensive agriculture, toxins and invasive competitors are also helping to trigger these declines. This situation adds to the “mounting evidence that humans are poised to cause a sixth mass extinction event”, according to the research, published in Conservation Letters. It adds that “minimizing the direct killing of the world’s largest vertebrates is a priority conservation strategy that might save many of these iconic species and the functions and services they provide.” Humans cause the deaths of large creatures in a variety of ways, from snares that entangle mountain gorillas and the poaching of elephants for ivory to the killing of the Chinese giant salamander, which can grow up to 6ft long and is considered a delicacy in Asia.

So what are you going to do about it? Appeal to your politicians?

• Global Warming Could Exceed 1.5ºC Within Five Years (G.)

Global warming could temporarily hit 1.5C above pre-industrial levels for the first time between now and 2023, according to a long-term forecast by the Met Office. Meteorologists said there was a 10% chance of a year in which the average temperature rise exceeds 1.5C, which is the lowest of the two Paris agreement targets set for the end of the century. Until now, the hottest year on record was 2016, when the planet warmed 1.11C above pre-industrial levels, but the long-term trend is upward. Man-made greenhouse gases in the atmosphere are adding 0.2C of warming each decade but the incline of temperature charts is jagged due to natural variation: hotter El Niño years zig above the average, while cooler La Ninã years zag below.

In the five-year forecast released on Wednesday, the Met Office highlights the first possibility of a natural El Niño combining with global warming to exceed the 1.5C mark. Dr Doug Smith, Met Office research fellow, said: “A run of temperatures of 1C or above would increase the risk of a temporary excursion above the threshold of 1.5C above pre-industrial levels. Predictions now suggest around a 10% chance of at least one year between 2019 and 2023 temporarily exceeding 1.5C.” Climatologists stressed this did not mean the world had broken the Paris agreement 80 years ahead of schedule because international temperature targets are based on 30-year averages.

“Exceeding 1.5C in one given year does not mean that the 1.5C goal has been breached and can be redirected towards the bin,” said Joeri Rogelj, a lecturer at the Grantham Institute. “The noise in the annual temperatures should not distract from the long-term trend.”