John M. Fox “The new Hudson” 1948

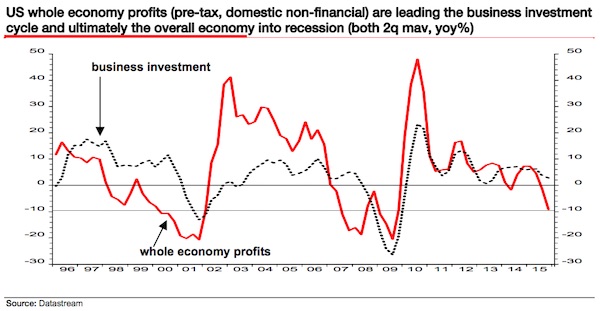

Ambrose sees inflation?!

• Time To Stop Dancing With Equities On A Live Volcano (AEP)

Be very careful. The US economic expansion is long in the tooth and starting to hit the time-honoured constraints that mark the last phase of the business cycle. Wall Street equities are more stretched by a host of measures than they were at the peak of sub-prime bubble just before the Lehman crisis. All it will take to bring the S&P 500 index back to earth is a catalyst, and that is exactly what is coming into view on the macro-economic horizon. This does not mean we are on the cusp of recession or racing headlong towards some imminent reckoning, but we are probably in the final innings of this epic asset boom. Didier Saint-Georges, from fund manager Carmignac, says the “massive and indiscriminate equity market rally” since February’s panic-lows is a false dawn driven by short-covering, telling us little about the world’s deformed economic, financial, and political landscape.

Corporate earnings peaked at $1.845 trillion (£1.3 trillion) in the second quarter of 2015, and recessions typically start five to seven quarters after the peak. “We will not be dancing on the volcano like so many others,” said Saint-Georges. If we are lucky it will be a slow denouement with a choppy sideways market going nowhere for another year as the US labour market tightens, and workers at last start to claw back a greater share of the economic pie. The owners of capital have had it their way for much of the post-Lehman era, exorbitant beneficiaries of central bank largesse. Now they may have to give a little back to society. Yet this welcome “rotation” spells financial trouble. Strategists Mislav Matejka and Emmanuel Cau, from JP Morgan, have told clients to prepare for the end of the seven-year bull run, advising them to trim equities gradually and build up a safety buffer in cash.

“This is not the stage of the US cycle when one should be buying stocks with a six to 12-month horizon. We recommend using any strength as a selling opportunity,” they said. Their recent 165-page report on the subject is a sobering read. The price-to-sales ratio (P/S) of US stocks is higher than any time in the sub-prime boom. Share buy-backs are at an historic high in relation to earnings (EBIT). Net debt-to-equity ratios have blown through their historical range. This is happening despite two quarters of tighter lending by US banks. Spreads on high-yield debt have doubled since 2014, jumping by 300 basis points even after stripping out the energy bust. The list goes on; the message is clear. “One should be cutting equity weight before the weakness becomes obvious,” they said.

Read more …

Hillary equals more of the same. The same disaster.

• Hillary Clinton’s Corporate Cash and Corporate Worldview (Naomi Klein)

There aren’t a lot of certainties left in the US presidential race, but here’s one thing about which we can be absolutely sure: The Clinton camp really doesn’t like talking about fossil-fuel money. Last week, when a young Greenpeace campaigner challenged Hillary Clinton about taking money from fossil-fuel companies, the candidate accused the Bernie Sanders campaign of “lying” and declared herself “so sick” of it. As the exchange went viral, a succession of high-powered Clinton supporters pronounced that there was nothing to see here and that everyone should move along. The very suggestion that taking this money could impact Clinton’s actions is “baseless and should stop,” according to California Senator Barbara Boxer. It’s “flat-out false,” “inappropriate,” and doesn’t “hold water,” declared New York Mayor Bill de Blasio.

New York Times columnist Paul Krugman went so far as to issue “guidelines for good and bad behavior” for the Sanders camp. The first guideline? Cut out the “innuendo suggesting, without evidence, that Clinton is corrupt.” That’s a whole lot of firepower to slap down a non-issue. So is it an issue or not? First, some facts. Hillary Clinton’s campaign, including her Super PAC, has received a lot of money from the employees and registered lobbyists of fossil-fuel companies. There’s the much-cited $4.5 million that Greenpeace calculated, which includes bundling by lobbyists. One of Clinton’s most active financial backers is Warren Buffett, who is up to his eyeballs in coal. But that’s not all. There is also a lot more money from sources not included in those calculations. For instance, one of Clinton’s most prominent and active financial backers is Warren Buffett.

While he owns a large mix of assets, Buffett is up to his eyeballs in coal, including coal transportation and some of the dirtiest coal-fired power plants in the country. Then there’s all the cash that fossil-fuel companies have directly pumped into the Clinton Foundation. In recent years, Exxon, Shell, ConocoPhillips, and Chevron have all contributed to the foundation. An investigation in the International Business Times just revealed that at least two of these oil companies were part of an effort to lobby Clinton’s State Department about the Alberta tar sands, a massive deposit of extra-dirty oil. Leading climate scientists like James Hansen have explained that if we don’t keep the vast majority of that carbon in the ground, we will unleash catastrophic levels of warming.

During this period, the investigation found, Clinton’s State Department approved the Alberta Clipper, a controversial pipeline carrying large amounts of tar-sands bitumen from Alberta to Wisconsin. “According to federal lobbying records reviewed by the IBT,” write David Sirota and Ned Resnikoff, “Chevron and ConocoPhillips both lobbied the State Department specifically on the issue of ‘oil sands’ in the immediate months prior to the department’s approval, as did a trade association funded by ExxonMobil.”

Read more …

“All this leads one to think that the government doesn’t recognize the severity of the problem.”

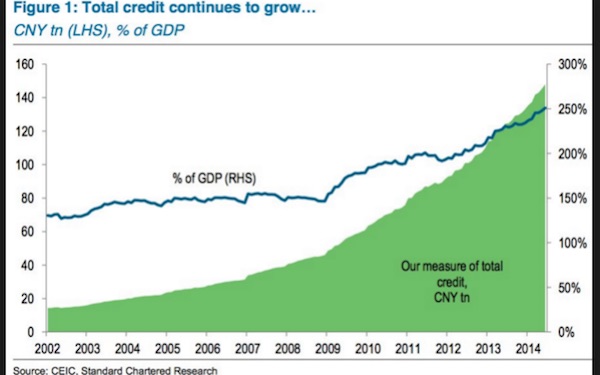

• How Bad Is China’s Debt Problem, Really? (Balding)

For months now, China’s regulators have been warning about the dangers of rapidly expanding credit and the need to deleverage. With new plans to clean up bad loans at the country’s banks, you might conclude that the government is getting serious about the risks it faces. But there’s reason to doubt the effectiveness of China’s approach. In fact, it’s running a serious risk of making its debt problems worse. After the financial crisis, China embarked on a credit binge of historical proportions. In 2009, new loans grew by 95%. The government offered cheap credit to build apartments for urban migrants, airports for the newly affluent and roads to accommodate a fleet of new cars. Yet as lending grew at twice the rate of GDP, problems started bubbling up. Companies gained billion-dollar valuations, then collapsed when they couldn’t profit.

Enormous surplus capacity drove down prices. Excessive real-estate lending led to the construction of “ghost cities.” Asset bubbles popped and bad loans mounted. China’s policy makers say they recognize these problems. The government’s most recent 5-year plan, released in December, notes the need for deleveraging. The PBOC has talked up the party line about slowing credit growth and making high-quality loans. Yet officials still say that only about 1.6% of commercial-banking loans are nonperforming. Some analysts put the real figure closer to 20%. And Beijing’s primary plan to address the problem – allowing companies to swap their debt with banks in exchange for equity – actually creates new risks. For one thing, while a debt-for-equity swap may help excessively indebted firms, it will wreak havoc with banks.

Directly, a given bank will no longer receive the cash flow from interest and principal payments. Indirectly, it won’t be able to sell equity to the PBOC or to other banks as it could with a loan. Valuing the equity could present a bigger problem. In China, banks must count 100% of loans made to non-financial companies against their reserve requirements. When they invest in equity, however, they must set aside 400% of the value of the investment. If the debt isn’t worth face value to the bank, it seems unlikely that the equity is worth far more – suggesting that large write-downs will be required. The swaps program also creates a number of big-picture problems. Consider the tight relationship between banks and large government-linked companies.

If banks were under pressure to roll over loans when they were creditors hoping to get repaid, what will their incentive be when they own the firm and have essentially unlimited lending capacity? Another problem is that Chinese industry exists in a deflationary debt spiral: Prices have been falling for years, raising the real cost of repaying loans. If companies are relieved of their debt, they’ll have an incentive to reduce prices to gain market share, thus worsening one of the primary causes of the current malaise. All this leads one to think that the government doesn’t recognize the severity of the problem. Debt-for-equity swaps and loan rollovers simply aren’t long-term solutions for ailing companies on the scale China faces.

Read more …

All that monopoly money behaves like liquid gas.

• China Traders Flee to Hong Kong in Record Stock-Buying Streak (BBG)

Cash is pouring into Hong Kong stocks from across the mainland border. Chinese investors have been net buyers of the city’s shares for 104 consecutive trading days, sinking 43.8 billion yuan ($6.8 billion) into equities from October through Tuesday, according to data compiled by Bloomberg tracking investments via the exchange link with Shanghai. Mainland traders have now put more money into Hong Kong than global asset managers have invested in Shanghai, a reversal of flows in the link’s first year, the data show. As concern persists about a further slide in the yuan, Chinese investors are piling into cheaper shares across the border that have lagged behind mainland counterparts for years.

While the flows are small relative to estimates of the record capital flight from China in 2015, they’re another sign of what’s at stake for policy makers seeking to stabilize the currency and stem outflows by providing credible investment options at home. “In China, there is talk of an asset drought – people don’t find domestic assets particularly attractive,” said Tai Hui at JPMorgan. “They are investing overseas in any way possible including via the southbound stock connect.” Buying mainland Chinese stocks has been a losing proposition this year, with the benchmark Shanghai Composite Index down 14%. Other investment alternatives such as property are coming under scrutiny as authorities impose fresh curbs after home prices jumped in the biggest cities such as Shanghai and Shenzhen.

Read more …

What’s next? Compete with OPEC?

• China Set To Shake Up World Copper Market With Exports (Reuters)

China may be about to shock the global copper market by unleashing some of its stockpiles of the metal, which are near record highs, onto the global market. Four traders of copper, including two from state-owned Chinese smelters, said they expect China to raise its copper exports – which are usually tiny – in the next few months. China’s refined copper exports averaged less than 10,000 tonnes a month in the first two months of 2016, and around 17,000 a month in 2015. If higher exports materialize, they will be a major jolt to producers and investors in the metal across the world – in particular because it would come during what is traditionally the strongest period of demand for copper from China, the world’s largest consumer of the metal. It will also be a further sign that the Chinese economy is still struggling against headwinds. Some sectors that buy copper – such as construction and manufacturing – have been hit especially hard in the past couple of years.

Traders and analysts in China say slowing building construction and electronics manufacturing has stifled demand for refined copper from the nation’s massive smelting sector at a time when the country is already swimming in the metal. China’s copper consumption has been a crucial measure of the country’s economic growth as the metal forms the essential network of its infrastructure, carrying water, conducting electricity and comprising the circuits in its machines. “The situation for copper smelters in China is probably the worst it has been in 20 years. But they won’t admit it. It wouldn’t surprise me in the least (if they start exporting),” said a source at an Asian copper producer, who declined to be named because he is not authorized to speak to the media. Increasing Chinese exports would mark an abrupt turnaround in global copper trade flows as China’s refined copper imports hit a record in 2015.

Read more …

Looking at China, it’s hard not to think of 1789, Robespierre, Marie-Antoinette, Bastille. Napoleon next?

• Panama Papers Reveal Offshore Secrets Of China’s Red Nobility (G.)

The eight members of China’s Communist party elite whose family members used offshore companies are revealed in the Panama Papers. The documents show the granddaughter of a powerful Chinese leader became the sole shareholder in two British Virgin Islands companies while still a teenager. Jasmine Li had just begun studying at Stanford University in the US when the companies were registered in her name in December 2010. Her grandfather Jia Qinglin was at that time the fourth-ranked politician in China. Other prominent figures who have taken advantage of offshore companies include the brother-in-law of the president, Xi Jinping, and the son-in-law of Zhang Gaoli, another member of China’s top political body, the politburo standing committee.

They are part of the “red nobility”, whose influence extends well beyond politics. Others include the daughter of Li Peng, who oversaw the brutal retaliation against Tiananmen Square protestors; and Gu Kailai, wife of Bo Xilai, the ex-politburo member jailed for life for corruption and power abuses. The relatives had companies that were clients of the offshore law firm Mossack Fonseca. There is nothing in the documents to suggest that the politicians in question had any beneficial interest in the companies connected to their family members. Since Monday, China’s censors have been blocking access to the unfolding revelations about its most senior political families. There are now reports of censors deleting hundreds of posts on the social networks Sina Weibo and Wechat, and some media organisations including CNN say parts of their websites have been blocked.

The disclosures come amid Xi Jinping’s crackdown on behaviour that could embarrass the Communist party. Two more well-connected figures – the brother of former vice-president Zeng Qinghong and the son of former politburo member Tian Jiyun – are directors of a single offshore company. They have previously been linked in a court case that highlighted how some Chinese “princelings” have used political connections for financial gain. They have emerged from the internal data of the offshore law firm Mossack Fonseca. [..] China and Hong Kong were Mossack Fonseca’s biggest sources of business, with clients from these jurisdictions linked to a total of 40,000 companies past and present. About a quarter of these are thought to be live: in 2015, records show the firm was collecting fees for nearly 10,000 companies linked to Hong Kong and China. The Mossack Fonseca franchise now has offices in eight Chinese cities, according to its website

Read more …

How much pressure will he get?

• David Cameron’s EU Intervention On Trusts Set Up Tax Loophole (FT)

David Cameron personally intervened in 2013 to weaken an EU drive to reveal the beneficiaries of trusts, creating a possible loophole that other European nations warned could be exploited by tax evaders. The disclosure of the prime minister’s resistance to opening up trusts to full scrutiny comes as he faces intense pressure to make clear whether his family stands to benefit from offshore assets linked to his late father. Although Mr Cameron championed corporate tax transparency, he wrote in November 2013 to Herman Van Rompuy, president of the European Council at the time, to argue that trusts widely used for inheritance planning in Britain should win special treatment in an EU law to tackle money laundering.

In the letter, seen by the Financial Times, Mr Cameron said: “It is clearly important we recognise the important differences between companies and trusts. This means that the solution for addressing the potential misuse of companies, such as central public registries, may well not be appropriate generally.” Britain has emerged as the strongest European rival to Switzerland for private banking and wealth management, administering £1.2tn of assets, according to Deloitte. The sector contributed £3.2bn to the economy, according to 2014 estimates from the British Bankers’ Association. A senior government source said that Mr Cameron’s letter reflected official advice that creating a central registry for trusts would have been complex and would have distracted from the main objective of shining a light on the ownership of shell companies.

“It would have slowed down the process because of the different types of trust involved,” the official said. “They are sometimes used to protect vulnerable people, so that would have been an extra complication. “As the directive went through we reached a position where trusts which generate tax consequences had to demonstrate their ownership to HM Revenue & Customs.” According to officials, the UK stance in 2013 prompted clashes with France and Austria as well as with members of the European Parliament, who accused Britain of double standards in the fight against tax avoidance. Maria Fekter, the Austrian finance minister at the time, had attacked Britain earlier that year as “the island of the blessed for tax evasion and money laundering”. She cited trusts as a specific problem.

Read more …

“London is the epicentre of so much of the sleaze that happens in the world..”

• Panama Papers Reveal London As Centre Of ‘Spider’s Web’ (AFP)

As-well as shining a spotlight on the secret financial arrangements of the rich and powerful, the so-called Panama Papers have laid bare London’s role as a vital organ of the world’s tax-haven network. The files leaked from Panama law firm Mossack Fonseca exposed Britain’s link to thousands of firms based in tax havens and how secret money is invested in British assets, particularly London property. Critics accuse British authorities of turning a blind eye to the inflow of suspect money and of being too close to the financial sector to clamp down on the use of its overseas territories as havens, with the British Virgin Islands alone hosting 110,000 of the Mossack Fonseca’s clients. “London is the epicentre of so much of the sleaze that happens in the world,” Nicholas Shaxson, author of the book “Treasure Islands”, which examines the role of offshore banks and tax havens, told AFP.

The political analyst said that Britain itself was relatively transparent and clean, but that companies used the country’s territories abroad – relics of the days of empire – to “farm out the seedier stuff”, often under the guise of shell companies with anonymous owners. “Tax evasion and stuff like that will be done in the external parts of the network. Usually there will be links to the City of London, UK law firms, UK accountancy firms and to UK banks,” he said, calling London the centre of a “spider’s web”. “They’re all agents of the City of London – that is where the whole exercise is controlled from,” Richard Murphy, professor at London’s City University, said of the offshore havens. The files showed that Britain had the third highest number of Mossack Fonseca’s middlemen operating within its borders, with 32,682 advisers.

Although not illegal in themselves, shell companies can be used for illegal activities such as laundering the proceeds of criminal activities or to conceal misappropriated or politically-inconvenient wealth. Around 310,000 tax haven companies own an estimated £170 billion (210 billion euros, $240 billion) of British real estate, 10% of which were linked to Mossack Fonseca. The files appeared to show that the United Arab Emirates President Sheikh Khalifa bin Zayed Al-Nahyan owned London properties worth more than £1.2 billion and that Mariam Safdar, daughter of Pakistani prime minister Nawaz Sharif, was the beneficial owner of two offshore companies that owned flats on the exclusive Park Lane.

Read more …

“..the London property market has been skewed by laundered money. Prices are being artificially driven up by overseas criminals who want to sequester their assets here in the UK”

• How Laundered Money Shapes London’s Property Market (FT)

For three-quarters of Londoners under 35, owning a home in the capital remains out of reach. But according to the leaked Panama Papers, buying property in London presented little problem for associates of Bashar al-Assad, the Syrian president; for a convicted embezzler who is also the son of a former Egyptian president; or for a Nigerian senator facing corruption charges. The leaks from the Panamanian law firm Mossack Fonseca have brought back into focus the ownership of London property via offshore companies by people suspected of corruption overseas — a phenomenon that has helped to shape the capital’s housing market, where prices are up 50% since 2007. “We think it very likely that the influx of corrupt money into the housing market has pushed up prices,” said Rachel Davies, senior advocacy manager at Transparency International.

Donald Toon, head of the National Crime Agency, has gone further, saying last year that “the London property market has been skewed by laundered money. Prices are being artificially driven up by overseas criminals who want to sequester their assets here in the UK”. Since 2004 £180m of UK property has been subject to criminal investigation as suspected proceeds of corruption, according to Transparency International data from 2015. Yet this probably represented “only a small proportion of the total”, added the campaign group. Most of these properties were bought using anonymous shell companies based in offshore tax havens such as the British Virgin Islands. Overseas companies own 100,000 properties in England and Wales, Land Registry data show. Owning property through a company can present tax advantages but, depending where that company is based, it can also offer anonymity.

According to Transparency International figures, almost one in 10 properties in the London borough of Kensington & Chelsea is owned through a “secrecy jurisdiction” such as the British Virgin Islands, Jersey or the Isle of Man. “UK property can be acquired anonymously, anti-money-laundering checks can be bypassed with relative ease, and if you invest in luxury property in London you know your investment is safe. All that comes from the flaws in the UK anti-money-laundering system,” said Ms Davies. According to the documents leaked to the International Consortium of Investigative Journalists, Soulieman Marouf, an al-Assad associate whose assets in Europe were frozen for two years from 2012, holds luxury flats in London worth almost £6m through British Virgin Islands companies.

The family of a deceased former Syrian intelligence chief owns a £1.2m Battersea home, the Guardian reported. The documents also link Alaa Mubarak — a son of Hosni Mubarak, the former Egyptian president — who was jailed and released last year for corruption, to an £8m Knightsbridge property. Bukola Saraki, the president of the Nigerian senate who faces charges in his home country of failing to declare assets, owns a Belgravia property, while a second is held by companies in which his wife and former special assistant are shareholders. Mr Saraki denies any wrongdoing and says he declared his assets in accordance with the law.

Read more …

This bubble too will burst.

• London Luxury-Apartment Sales Slump Triggers 20% Bulk Discounts (BBG)

Developers in central London are offering institutional investors discounts of as much as 20% on bulk purchases of luxury apartments as demand from international buyers slumps amid higher taxes and low commodity prices. Concessions of about that magnitude are being offered to investors willing to take 100 homes or more, according to Killian Hurley, chief executive officer of London developer Mount Anvil. Broker CBRE is negotiating discounts of as much as 15% for bulk purchases on the fringes of the capital’s best districts, said Chris Lacey, head of U.K. residential investment. A record number of high-end homes are planned in London districts such as Nine Elms and Earls Court even as demand wanes.

Sales of properties under construction in the U.K. capital slumped 19% in the fourth quarter of 2015, according to researcher Molior, while the percentage of overseas buyers fell to 20% from about 33% a year earlier, broker Hamptons International data show. “We will see distress in prime central London and in Nine Elms, where there has been a lot of international investment,” Andrew Stanford at LaSalle Investment said in an interview. “There have been a number of house builders who have approached us directly with schemes as a direct result of off-plan sales falling, particularly in central London.” Bulk buyers may be hard to find because the apartments being built aren’t designed for the rental market, lacking features such as equal-size bedrooms, said Stanford, whose company has invested more than $457 million in U.K. multifamily housing on behalf of clients.

Many developers traveled to Asia to sell homes in advance of construction and secure cheaper development loans because the down payments made projects less risky. The imposition of higher purchase taxes has now reduced the appeal of the costliest properties, leaving developers wondering how they will secure funding, said Dominic Grace, head of London residential development at broker Savills. “It is a question everyone is asking, and the truth is no one really knows,” Grace said.

Read more …

Sure..

• US Readies Bank Rule On Shell Companies Amid ‘Panama Papers’ Fury (Reuters)

The U.S. Treasury Department intends to soon issue a long-delayed rule forcing banks to seek the identities of people behind shell-company account holders, after the “Panama Papers” leak provoked a global uproar over the hiding of wealth via offshore banking devices. A department spokesman said on Wednesday the rule would “soon” be turned over to the White House for review and issuance, but did not confirm any timetable for the initiative, which has taken years. Governments around the globe have launched probes into possible financial wrongdoing after 11.5 million documents from the Panamanian law firm Mossack Fonseca, nicknamed the “Panama Papers,” were leaked to the media and reports emerged Sunday. Mossack Fonseca has said it was the victim of a computer hack, and that it has consistently acted appropriately.

The papers offer “validation for those who have been screaming for a decade” about the need for financial institutions in the United States and elsewhere to address risks of money laundering, terror finance and other crime by identifying people who clandestinely control legal entities, former Treasury official Chip Poncy told Reuters. The leaked documents may give banks a glimpse into the kind of information on true, or “beneficial” owners, that they regularly should be obtaining to better understand the cross-border money flows they facilitate, said Poncy, one of the architects of the Treasury rule, which has been in the works since 2012.

But simply having a client who is linked to the offshore shell companies highlighted in the Panama papers “doesn’t necessarily mean much,” said a former FinCEN official who asked not to be named due to his role in the private sector. What would be significant is “inconsistent information or payment flows that now connect” in ways that suggest possible illicit activity, he said.

Read more …

“We have innuendo, we have a complete lack of standards on the part of the western media, and the major mistake made by the leaker was to give these documents to the corporate media..”

• US Government, Soros Funded Panama Papers To Attack Putin: WikiLeaks (RT)

Washington is behind the recently released offshore revelations known as the Panama Papers, WikiLeaks has claimed, saying that the attack was “produced” to target Russia and President Putin. On Wednesday, the international whistleblowing organization said on Twitter that the Panama Papers data leak was produced by the Organized Crime and Corruption Reporting Project (OCCRP), “which targets Russia and [the] former USSR.” The “Putin attack” was funded by the US Agency for International Development (USAID) and American hedge fund billionaire George Soros, WikiLeaks added, saying that the US government’s funding of such an attack is a serious blow to its integrity. Organizations belonging to Soros have been proclaimed to be “undesirable” in Russia.

Last year, the Russian Prosecutor General’s Office recognized Soros’s Open Society Foundations and the Open Society Institute Assistance Foundation as undesirable groups, banning Russian citizens and organizations from participation in any of their projects. Prosecutors then said the activities of the institute and its assistance foundation were a threat to the basis of Russia’s constitutional order and national security. Earlier this year, the billionaire US investor alleged that Putin is “no ally” to US and EU leaders, and that he aims “to gain considerable economic benefits from dividing Europe.” “The American government is pursuing a policy of destabilization all over the world, and this [leak] also serves this purpose of destabilization. They are causing a lot of people all over the world and also a lot of money to find its way into the [new] tax havens in America. The US is preparing for a super big financial crisis, and they want all that money in their own vaults and not in the vaults of other countries,” German journalist and author Ernst Wolff told RT.

Earlier this week, the head of the International Consortium of Investigative Journalists (ICIJ), which worked on the Panama Papers, said that Putin is not the target of the leak, but rather that the revelations aimed to shed light on murky offshore practices internationally. “It wasn’t a story about Russia. It was a story about the offshore world,” ICIJ head Gerard Ryle told TASS. His statement came in stark contrast to international media coverage of the “largest leak in offshore history.” Although neither Vladimir Putin nor any members of his family are directly mentioned in the papers, many mainstream media outlets chose the Russian president’s photo when breaking the story.

“We have innuendo, we have a complete lack of standards on the part of the western media, and the major mistake made by the leaker was to give these documents to the corporate media,” former CIA officer Ray McGovern told RT. “This would be humorous if it weren’t so serious,” he added. “The degree of Putinophobia has reached a point where to speak well about Russia, or about some of its actions and successes, is impossible. One needs to speak [about Russia] in negative terms, the more the better, and when there’s nothing to say, you need to make things up,” Kremlin spokesman Dmitry Peskov has said, commenting on anti-Russian sentiment triggered by the publications. WikiLeaks spokesman and Icelandic investigative journalist Kristinn Hrafnsson has called for the leaked data to be put online so that everybody could search through the papers. He said withholding of the documents could hardly be viewed as “responsible journalism.”

Read more …

Almost funny.

• Bookmakers Set Odds For Next Leader To Resign After Panama Papers (MW)

Whose scalp will the Panama Papers scandal claim next? Irish bookmaker Paddy Power has opened betting lines on which head of state could be the next to go. “Who needs the Grand National when you’ve got the Panama Papers to punt on?” the betting line boasted in a press release on Wednesday. Icelandic Prime Minister Sigmundur Gunnlaugsson, announced yesterday he was stepping down after Panama Papers revelations that he and his wife sought to hide their claims on Icelandic banks that were bailed out by his administration during the financial crisis. Paddy Power puts the odds of British Prime Minister David Cameron resigning next at 20-1. The leaked documents outed Cameron’s father Ian Cameron as a client of the Panamanian law firm, Mossack Fonseca, at the center of the scandal.

Cameron’s father used a secret but legal offshore structure to set up a fund for investors. After saying all day Monday that his tax affairs were a “private matter”, media questions about his family’s remaining interest in the fund forced Cameron’s office, according to BBC reports, to issue a statement affirming that his family “[does] not benefit from any offshore trusts.” A surer bet according to the bookmaker is Argentina’s President Mauricio Macri at 8-1 odds. Macri won last year’s general election campaigning on a platform promising to fight corruption but the leaked documents say he was a director of Fleg Trading Ltd, founded in 1998 by his father Franco Macri, one of the richest men in Argentina. The company was dissolved in January 2009. “It was an offshore company to invest in Brazil, an investment that ultimately wasn’t completed, and where I was director,” he said in a television interview with a local program.

A Paddy Power spokesman told MarketWatch that to pay off, the leader has to leave “after being implicated specifically in the Panama Papers.” There have already been a few bets made that Macri and Cameron are next, he said. Paddy Power also has laid odds that the President of Pakistan Nawaz Sharif will leave at 10-to-1 and Ukraine’s President Petro Poroshenko almost as good at 12-1. Sharif is mentioned in the leak as the result of a £7 million loan from Deutsche Bank backed up by four London apartments owned by offshore companies established by Mossack Fonseca. Poroshenko – nicknamed the ‘chocolate king’ – hid his ongoing interest in his candy company, Roshen, in a blind trust offshore when he became president in 2014. He had promised to sell it after being elected. Longshots to leave include President Xi Jinping of China, Russia’s Putin and France’s Francois Hollande, all set at 33-1.

Read more …

Coming closer.

• Brexit May Force Europe’s Banks To Dump $123 Billion Of Securities (BBG)

If Britain decides to leave the EU, a corner of the credit market may depart with it and European banks could be left having to replace as much as €108 billion ($123 billion) of securities. Lenders from the EU that bought bonds backed by U.K. mortgages, bank loans and credit-card debt may find themselves caught up in the fallout of a “Brexit” because the debt might no longer count toward their emergency cash reserves. While a settlement with the bloc would take years to reach, lawyers and analysts are beginning to flag concerns about holdings of the asset-backed securities, a market that’s already been hammered since the financial crisis.

“Banks could find themselves having a liquidity issue if these assets no longer count,” said Vincent Keaveny at law firm DLA Piper, who specializes in structured credit. “There are big risks out there, but there aren’t any easy fixes.” Under the Basel Accords, a set of agreements by global regulators, banks must meet minimum standards meant to make them more resilient to shocks after the financial crisis highlighted their weaknesses. One standard, known as the Liquidity Coverage Ratio, requires banks maintain an adequate amount of high-quality assets that can be quickly converted to cash to meet liquidity needs for 30 days.

Certain securitized notes are counted, but their underlying assets must originate from a member state, according to the European Commission’s Delegated Act for the standard. That means some bonds backed by collateral from a newly go-it-alone Britain may be excluded. “‘Brexit’ could result in certain U.K. ABS no longer qualifying as eligible assets for current LCR purposes,” Angela Clist and Nicole Rhodes, London-based lawyers specializing in securitization at Allen & Overy LLP, wrote in a note to clients in February.

Read more …

“When economists say “equilibrium,” what they really mean is “any solution to any equations I decide to write down.”

• Economics Builds a Tower of Babel (BBG)

In Lewis Carroll’s “Through the Looking Glass,” Humpty Dumpty proudly declares: “When I use a word, it means just what I choose it to mean – neither more nor less.” To which Alice replies: “The question is whether you can make words mean so many different things.” Humpty Dumpty could have been an economist. The modern economics profession made a collective decision, long ago, to develop a system of jargon in which words have multiple, sometimes contradictory meanings. Unfortunately, the general public’s reaction tends to be similar to that of poor Alice. Want some examples? There’s no shortage. Let’s take the word “investment.” Most people think this means buying some financial assets, such as stocks or bonds. That’s basically a form of lending – you give someone money today, and you hope they’ll give you back more money tomorrow.

Economists call that “financial investment,” but the kind of investment they usually talk about is business investment, meaning a company’s purchase of capital goods. Since companies use debt to buy capital goods (or use their own cash, which is essentially the same thing), this kind of “investment” is actually a type of borrowing. So economists use the same word to mean both borrowing and lending! That couldn’t possibly result in any confusion, right? Two similar examples are “capital” and “equity.” “Equity” can mean stock – partial ownership of a company – or it can refer to “shareholders’ equity,” which is a measure of the value of a business. “Capital” in econ can mean financial capital, i.e. money in the bank. More commonly, it refers to capital goods – productive stuff such as buildings or machines that help you create more stuff.

Though economists usually use the term in the second way, many people outside the profession refer to financial capital as “economic capital.” Confused yet? We’re just getting started. Everyone knows that economists love models where rational agents interact in an efficient market that reaches equilibrium, right? Except that almost every word in that sentence is complete nonsense, thanks to econ’s Humpty Dumpty-like tendency to redefine words without telling anyone. So how about “equilibrium”? The word used to refer to a situation where prices adjust in order to clear markets, so that supply matches demand. Later, game theorists came up with “Nash equilibrium,” named after mathematician John Nash, which refers to a situation where everyone is responding optimally to everyone else in a strategic situation. Other concepts proliferated, and so by now the word has lost all meaning entirely. When economists say “equilibrium,” what they really mean is “any solution to any equations I decide to write down.”

Read more …

Will the EU survive?

• Dutch ‘No’ Vote On Ukraine Pact Forces Government Rethink (Reuters)

The Dutch government said on Wednesday it could not ignore the resounding “No” in a non-binding referendum on the EU’s association treaty with Ukraine, but that it may take weeks to decide how to respond. Although the results were preliminary, they exposed dissatisfaction with the Dutch government and policy-making in Brussels – signalling a anti-establishment mood in a founding EU member weeks before Britain votes on membership. There could also be far-reaching consequences for the fragile Dutch coalition government, which currently holds the rotating EU presidency and which has lost popularity amid a wave of anti-immigrant sentiment. Exit polls indicated roughly 64% of Dutch voters voted “No” and 36% said “Yes”. Although turnout was too close to call, early tallies indicated it was just ahead of a turnout minimum of 30% required for the vote to be valid.

“It’s clear that ‘No’ have won by an overwhelming margin, the question is only if turnout is sufficient,” Dutch Prime Minister Mark Rutte said in a televised reaction. “If the turnout is above 30% with such a large margin of victory for the ‘No’ camp, then my sense is that ratification can’t simply go ahead,” Rutte added. That sentiment was shared by Diederik Samsom, leader of the Labour Party, the junior partner the governing coalition. “We can’t ratify the treaty in this fashion,” he said. A person familiar with internal EU discussions on how leaders in Brussels would respond said EU officials had been hoping for very low turnout that would disqualify or diminish the impact of a “No” vote. The European Commission, the bloc’s executive, will play for time, waiting for the Dutch government to suggest a way forward, the official said. The political, trade and defence treaty is already provisionally in place, but has to be ratified by all 28 EU member countries for every part of it to have full legal force. The Netherlands is the only country that has not done so.

Read more …

Monday there was a lot of media and brouhaha, and then they have a 17-day hiatus? EU-Assclowns.

• Greece Sees Two-Week Lag In Migrant Returns To Turkey (AFP)

A last-minute flurry of asylum applications by migrants desperate to avoid expulsion from Greece to Turkey will likely cause a two-week “lag” in an EU deportation plan slammed by rights groups, a Greek official said Wednesday. Nikos Xydakis, junior foreign minister for European affairs, indicated there would likely be few migrants sent back to Turkey over the next two weeks, following the first deportation of around 200 people on Monday. “We knew there would be a lag, an intermediate period before the program takes off, of at least two weeks to get through the first batch of (asylum) applications,” Xydakis told reporters. He nevertheless said the next set of expulsions would likely take place “from Friday onwards”, without going into further detail.

Athens stressed that the people shipped back to Turkey on Monday were migrants who had not claimed asylum. But the UN’s refugee agency has expressed concern that 13 of them, mostly Afghans, had expressed a wish to claim asylum but were not registered in time. Xydakis said some two dozen EU legal experts had arrived so far to assist the asylum process, compared to hundreds of security agents from EU border agency Frontex. “This is the weakness of the whole procedure. It is easier to deploy police officers than experts in refugee law, interpreters, debriefers,” he said. But he added: “They are coming.” Once the system is fully up and running, Greece has said it can process asylum claims in two weeks. “In two weeks (authorities) can get through 400 to 500 applications,” Xydakis said.

Under the terms of the EU-Turkey deal, all “irregular migrants” arriving on the Greek islands from Turkey since March 20 face being sent back, although the accord calls for each case to be examined individually. And for every Syrian refugee returned, another Syrian refugee will be resettled from Turkey to the EU, with numbers capped at 72,000. “It was overestimated that in five days everything would begin, it was crazy. We told them many times in Brussels, we knew,” Xydakis said. “Things must be done by the book, we cannot bundle people together, they have to be certified and checked,” the minister said. Out of around 6,000 migrants who have arrived on the islands of Chios and Lesvos after the March 20 deadline, more than 2,300 have now applied for asylum. And many others had previously complained of not having had access to the asylum procedure.

Read more …