G. G. Bain Goose Creek, houses on the water, Jamaica Bay, Long Island 1910

“As a reserve currency, the euro is falling apart..”

• Euro’s Reserve Status Jeopardized As Central Banks Dump Holdings (Blooomberg)

Quantitative easing may be helping Europe achieve its economic targets, but it’s also undermining the long-term viability of the euro by tarnishing its allure as a global reserve currency. Central banks cut their euro holdings by the most on record last year in anticipation of losses tied to unprecedented stimulus. The euro now accounts for just 22% of worldwide reserves, down from 28% before the region’s debt crisis five years ago, while dollar and yen holdings have both climbed, the latest data from the IMF show. “As a reserve currency, the euro is falling apart,” said Daniel Fermon, a strategist at SocGen. “As long as you have full quantitative easing, there’s no need to invest. The problem for the moment is we don’t see a floor for the currency. Money’s flowing out.”

ECB President Mario Draghi has in the past welcomed the drop-off in reserve managers’ holdings because a weaker exchange rate makes the continent more competitive. Yet firms including Mizuho Bank Ltd. warn the currency’s waning popularity reflects a more lasting loss of confidence in an economy that shrank in two of the past three years. “Global reserve managers may be thinking the euro is going to sink economically if it continues this way,” said Daisuke Karakama, the Tokyo-based chief market economist at Mizuho and a former European Commission official. With yen allocations rising, “they may be expecting Japan’s positive economic growth to continue as a result of” that nation’s record stimulus, Karakama said.

The decline in euro reserves suggests other central banks consider the ECB’s €1.1 trillion of QE bond purchases, which started a month ago, to be the biggest threat to the currency’s global status since its 1999 debut. Greece’s debt woes aren’t helping, either. The ECB ramped up the emergency funding available to Greek banks Thursday to alleviate the country’s worsening liquidity issues amid drawn- out negotiations over its bailout. All this is prompting banks from Citigroup, the world’s biggest foreign-exchange trader, to Goldman Sachs to predict the euro will fall below parity with the dollar this year, from a 12-year low of $1.0458 last month and $1.0617 Friday.

Plenty reasons.

• Why The Euro Could Fall Even Further (CNBC)

It’s been a one-way euro trip lower. The common currency has fallen every day this week, and is now near the lowest levels in 12 years. Now, currency traders are keenly watching American economic data, as better news about the economy could lead the euro drop to intensify. It all comes down to expectations about the Federal Reserve’s next move. Most market participants believe the Fed will raise short-term rate targets this year. That should help the U.S. dollar and hurt the euro, as it means that holding dollars will produce greater returns than holding euros, increasing demand for the greenback.

Expectations about a June Fed move have been tamped down due to a bevy of soft economic readings, most conspicuously the March jobs number. But this week, the Fed minutes and hawkish words from William Dudley have told investors that a June hike is still on the table, according to Boris Schlossberg of BK Asset Management. Dudley, the generally dovish New York Fed president, told Reuters on Wednesday that depending on how the data develops, a June move could be “still in play.” In the week ahead, Schlossberg says the biggest data point he will watch is Tuesday’s retail sales report. If it indicates that “the U.S. consumer finally started to spend, then dollar bulls run wild, and we may see 1.0500 break” on the euro, which is currently a bit below 1.0600 per dollar.

That’s because better data could serve to convince traders that the much-awaited Fed move will come sooner than previously anticipated. However, some traders say the move is overdone. “This short-term move is technical, so I expect to see the euro bounce and the dollar pull back off of the recent move,” said David Seaburg at Cowen.

Not that big a problem. It allows for the interest rate to come down further.

• Putin’s New Problem Is The Strong Ruble (Bloomberg)

Vladimir Putin is facing a problem few could have anticipated: The ruble is becoming too strong. Last year’s worst-performing major currency is this year’s best and while that’s buoying the nation’s bonds, driving yields to the lowest in four months, it’s also crimping Russia’s export revenue. Even though oil is little changed in dollars this year, the price when converted to rubles has plunged to the lowest since 2011. The currency rout in 2014 helped Russia to keep its budget deficit within 1% of GDP as the ruble weakened in lockstep with a 50% slump in oil. Now, with the cease-fire in Ukraine and the allure of higher-yielding assets attracting investors to ruble debt, the government is seeing the opposite effect.

“The current ruble level is already uncomfortable for the budget considering the oil price in rubles is already low,” Vladimir Bragin, head of research at Alfa Capital in Moscow, said by phone on Thursday. “In order to reach macroeconomic stability, Russia needs to limit its budget deficit and a weaker ruble is an easy way to do that.” The ruble’s 14% gain this month is making it easier for central bank Governor Elvira Nabiullina to push ahead with rate cuts this year after she hoisted the benchmark to 17% in December to stem the currency’s slide. Nabiullina lowered the rate by 3 percentage points so far in 2015.

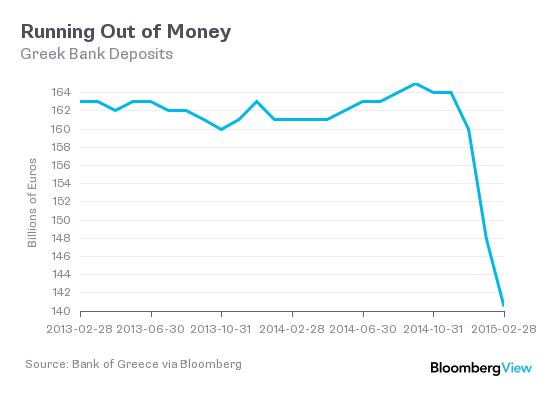

“The prospect of a negotiated exit within a month is now close to 40%..”

• Greece: The Next Deadline Approaches (CNBC)

Greece repaid one of its key loans on Thursday, but with the country’s coffers still close to empty, the government may merely have earned short-term respite. As the holiday of the Orthodox Easter Weekend approaches, newly minted Prime Minister Alexis Tsipras and Finance Minister Yanis Varoufakis are unlikely to be unwinding for the long weekend. Greece has been given six working days by the euro zone technical staff of the Euro Working Group to come up with proposals for a reform agenda—on which further financial aid is conditional—ahead of a key meeting of euro zone finance ministers on April 24 in Riga, Latvia. The struggling Greek economy still needs financial support. It faces two redemptions of bills for a total of €2.4 billion as soon as April 14 and 17.

“Euro area finance ministers are probably at the end of their tether, after ten weeks of the new government’s foot-dragging and game-playing, and any sympathy for the Greek position has long disappeared,” the economic research team at Daiwa wrote in a research note. Tsipras is barely off the plane from a trip to Russia, which seemed on the surface to have achieved little in terms of concrete promises from Russia to assist Greece in the event of it defaulting on its debt repayments, leaving the euro or losing financial support from its creditors.

Economists are now increasingly taking the possibility of a “Grexit”, deemed incredibly unlikely by many just a couple of years ago. The risk of Greece defaulting on its debt repayments is now 50-50%, according to UBS, although its analysts argue that default does not necessarily mean euro zone exit. The prospect of a negotiated exit within a month is now close to 40%, according to Gabriel Sterne, head of global macro research at Oxford Economics. And capital controls – limits on the amount of money that can be taken out of the country—usually a sign of severe economic distress—are just “one more turn of the financial screw away” he added.

“After five years of austerity imposed by creditors, “the word ‘reform’ resonates in Greece like the word ‘democracy’ in Iraq,” he said. “It’s a dirty word.”

• Greek Finance Minister Steers Debt Talk His Way (NY Times)

You would never know from his demeanor that Yanis Varoufakis, the celebrity Greek finance minister, was carrying the weight of a nation on his shoulders. In fact, you could be forgiven for thinking that it was his country’s uncompromising creditors who were on the defensive. On Thursday, at a conference of economic luminaries, Mr. Varoufakis was working hard to divert the discussion from Greece’s shrinking financial freedom and fears that it might default. (He had a bit of wind at his back with news that Greece on this same day had just met its deadline for repaying a €460 million, or $491 million, loan installment to the IMF. Rather than concede any Greek missteps, Mr. Varoufakis wanted to assess the flaws of the eurozone that he said had been revealed by the 2008 global meltdown and its aftermath.

“There is no doubt that if we had a federal republic, if we had a United States of Europe, we would not be here discussing the Greek crisis, the eurozone crisis, banking union or anything of the sort,” he said in an onstage conversation with the Nobel laureate Joseph E. Stiglitz, at a conference of the Institute for New Economic Thinking. “Unfortunately,” he added, “the way we designed the eurozone, it was crying out for a crisis.” Mr. Varoufakis, as is now well known, became finance minister in January as part of the Syriza-led leftist government of Prime Minister Alexis Tsipras, which came to power promising voters to renegotiate the €240 billion international bailout, whose terms Athens blames for sending the economy into a tailspin and leaving more than 50% of Greek youth jobless.

When Mr. Stiglitz asked him how Greece’s creditors could have repeatedly overestimated the country’s ability to grow under the terms of the bailout, Mr. Varoufakis replied, “I think it’s the politics of denial.” Even making Thursday’s payment to the I.M.F. required scraping together money from the government’s dwindling resources. It staved off a default for now, but did nothing to solve the bigger problem: that the government is running out of cash to meet obligations like paying pensions and the wages of public employees. To obtain another tranche of desperately needed bailout funds, Greece still has to persuade its highly skeptical creditors — which also include the ECB and the European Commission — that Athens has a credible economic overhaul plan. [..]

Mr. Varoufakis, 54, comes across as a sort of debonair Mr. Spock, a financial Vulcan of the eurozone. Dressed in a dark jacket with his trademark casual, open-collared shirt, he speaks clearly about the currency bloc’s awkward truths, avoiding the jargon and evasiveness that normally characterizes the region’s dreary politics. Appearing on a separate panel with Mr. Varoufakis on Thursday, the Irish central bank chief, Patrick Honohan, referred to the “glass being half full” after Ireland’s bailout and tentative recovery. “I don’t like the metaphor,” Mr. Varoufakis said. “In the case of my country, the glass is broken.”

“..Italy’s debt increased dramatically after the introduction of the euro..”

• 100,000 Italians Sign Petition For Eurozone Exit Referendum (RT)

Italy’s Five Star Movement (M5S) party has collected more than 100,000 signatures on a petition calling for a law that would allow a referendum on withdrawal from the eurozone. M5S MP Carlo Sibila says he expects a referendum to take place at the start of next year. Though the petition has already surpassed the required amount of signatures needed for the initiative, Sibila said that he hopes it will gather another 50,000 by early May in order to highlight the issue. “Who wants to stay in euro? This is the main question,” Sibila told RT. “But we don’t want to get out just like this – we want a program and a discussion, and then let the citizens decide. It’s really necessary today as the situation in Italy is going from bad to worse where jobs and economy are concerned.” The Italian constitution, however, does not provide for the cancellation of international agreements through referenda.

According to Sibila, Italy’s debt increased dramatically after the introduction of the euro. He also noted that Italy’s unemployment rate hovers around 12.7%, the sixth highest in the EU. “We can’t have our own fiscal policy, but without the euro it is possible in Italy,” Sibila said. The Five Star Movement, formed in 2009 by comedian and activist Beppe Grillo, finished second in the 2014 European Parliament election with 21% of the vote. Sibila stressed that M5S does not seek to leave the European Union, but merely to leave the currency union. “Italian citizens need to have the right to decide if they want to stay inside or outside the monetary union,” Sibila told RT. “We are not questioning the EU, it is only the monetary union.” Italy joined the Eurozone in 1999, and the currency was introduced into circulation three years later.

“..the Chinese company’s Class-A shares have gained 61% since last April..”

• PetroChina Overtakes Exxon Mobil To Become World’s Biggest Energy Company (RT)

The capitalization of China’s biggest oil producer PetroChina reached $352.8 billion during Thursday trading in Shanghai, surpassing ExxonMobil as the world’s most valuable energy company for the first time since 2010. The market cap of America’s Exxon reached $352.6 billion in Shanghai Thursday trading, Bloomberg reports. PetroChina’s market cap has gone up 13.81% in the last 12 months while Exxon’s market value has fallen by 14%, following the slump in oil prices. Moreover, the Chinese company’s Class-A shares have gained 61% since last April. The last time PetroChina was more valuable than Exxon was at the close of trading on June 25, 2010, according to Bloomberg.

“PetroChina has multiple positives at the moment: it’s got a reform story, it’s also listed in Hong Kong, and China has more freedom for mainland fund managers in the works,” said Mark Matthews head of Asia research at Bank Julius Baer & Co. in Singapore. “China is also planning to transfer stakes in state-owned enterprises away from their regulator, which will on the whole be positive for SOEs,” he added. Oil companies across the world have been facing difficult times since crude prices started to plunge last summer. ExxonMobil’s adjusted net income of $6.3 billion in the fourth quarter was the lowest since a loss in the final three months of 2009, according to Bloomberg data. PetroChina’s net profit was $1.8 billion in the same period.

The Shanghai Composite closed at its highest level in seven years on Thursday gaining about 88% over the past year as the best performer among major indexes. Meanwhile, the Chinese yuan has declined 0.1% versus the dollar in the past year. PetroChina is the listed arm of state-owned China National Petroleum Corporation (CNPC), with almost all of its operating profit coming from the exploration and production sector along with a small contribution from its natural gas and pipeline unit.

Some bubbles these days take on grotesque proportions.

• China Bears on Wrong End of $4 Trillion Rally Refuse to Go Away (Bloomberg)

Bull markets are always tough on short sellers. This one in China right now, though, is proving downright brutal. Bearish wagers on the Shanghai Stock Exchange have climbed threefold in the past nine months and reached a record 6.09 billion yuan ($981 million) on Wednesday, a period in which the benchmark equity index jumped 94%. Across the border in Hong Kong, where the Hang Seng Composite Index has surged 7.6% in just the past two days, the gauge’s 20 most-shorted stocks surged 18% on average. The gains show the dangers of betting against a Chinese market where new investors are flocking to stocks at a record pace and traders have taken out an unprecedented 1.06 trillion yuan of debt in Shanghai to amplify their buying power.

While technical indicators show shares in both the mainland and Hong Kong are more vulnerable to a reversal than any other market, Marco Polo Pure Asset Management says bears may be setting themselves up for more losses if China’s stimulus efforts produce an economic recovery later this year. “It’s not a market you want to bet against,” said Aaron Boesky, who oversees about $125 million as the chief executive officer of Marco Polo in Hong Kong. The firm’s Pure China fund was the top performer in the second half of 2014 among China-focused hedge funds tracked by AsiaHedge Intelligence. “I can respect people who might want to stay out of it, because it is a very volatile market, even for local Chinese,” he said. “Staying out is respectable. Shorting it could be suicidal.”

“Greece lost 13% of its population during WWII..”

• WWII Reparations: Rare Footage From Greece’s Occupation By The Nazis (KTG)

Greek Defense Ministry has published a video with rare footage from the occupation of Greece by the Nazis during the World War II. Among others, the footage shows children suffering from malnutrition and emaciated adults, victims of the Great Famine during the Nazi occupation. The video should be seen in the context of the Greek claim of €278.7 billion in WWII reparations from Germany. According to the video voice-over, the Enforced Loan by the Nazis was to blame for the mass starvation of estimated 300,000 people in Athens alone. “The agreement of 14 March 1942 foresaw that Greece paid to its occupiers 1.5 billion drachmas per month, a total of 3.5 billion USD, according to the Dollar value of 1938.

The current value of the enforced loan is 54 billion euro without the interest. The agreement had to be implemented retrospectively as of 1.1. 1942. The agreement was signed by Germany and Italy and Greece was notified later. Two agreement modifications were added on 2. December 1942, with the effect that Germany had to start repaying the loan by April 1943. Germany paid back two installments only. In the Peace Paris Treaties (1947) Greece claimed 14 billion USD in war reparations, but the allies reduced the Greek claim down to 7.1 billion USD.” According to the video “Greece lost 13% of its population during the WWII. One part was lost in the battlefield, but the largest part due to Famine and the Nazis’ atrocities.”

The Great Famine, the period of mass starvation during the occupation of Greece by the powers of Axis – the fascist Italy and the Nazi Germany – hit especially the urban areas and some islands. The Great Famine was initiated by a large scale plunder by the Axis forces and as soon as the German army entered Athens 0n 27. April 1941. The Nazis confiscated fuel and all means of transportation, including fishing boats, preventing any transfer of food and other supplies and seized strategic industries. They proceeded with the wholesale and food looting , unemployment and hyperinflation skyrocketed, the black market flourished. The price of bread was increased 89-fold from April 1941 to June 1942.

“Since it was declared an official holiday in 1965, May 9, with its spontaneous gatherings of veterans in the streets, public festivals and gun salutes in the evening, has in fact become Russia’s most moving holiday..”

• EU Leaders Snub Moscow World War II Commemorations (Spiegel)

This Monday, Russia President Vladimir Putin visited the cemetery in the village of Marfino, not far from the old western Russian city of Staraya Russa, where he placed a bouquet of red roses. Then he met with veterans of the “Great Patriotic War,” the term Russians use to describe their battle against Hitler. It would be hard to find another part of Russia that is as saturated with the blood of that war than the earth around Staraya Russa. Officially, 850,000 soldiers died there during the two-and-a-half-year German occupation. The real figure is probably higher, because the Red Army long attempted, albeit unsuccessfully, to fend off repeated attacks by the enemy along the northwestern front.

The encounter near Marfino was one of the events with which the Russian president is preparing his country for May 9, which marks the anniversary of the end of the war with Hitler’s Germany. It is “our country’s most important and most honest holiday,” Putin said in Staraya Russa. “It is the day of the great victory.” The end of the war will be commemorated in Russia for the 70th time this year. Since it was declared an official holiday in 1965, May 9, with its spontaneous gatherings of veterans in the streets, public festivals and gun salutes in the evening, has in fact become Russia’s most moving holiday — and perhaps the only one that has truly united the people. The victory over Hitler happened three generations ago.

Still, during Putin’s visit to Staraya Russa, the veterans reminded him of the words of military commander Alexander Suvorov, who said that a war is not over “until the last soldier has been buried.” Last year, search teams recovered the remains of 12,900 fallen soldiers from swamps near Novgorod, the forests of Smolensk and the region around St. Petersburg.

Right. Sure.

• Obama Says ‘Days Of Meddling’ In Latin America Are Past (BBC)

US President Barack Obama has told Latin American leaders that the days when his country could freely interfere in regional affairs are past. He was speaking just before the seventh Summit of the Americas was due to kick off in Panama City. Mr Obama and Cuban leader Raul Castro will meet face-to-face for the first time since a December detente. But their much-anticipated meeting could be overshadowed by tensions between the US and Venezuela. Mr Obama told a forum of civil society leaders in Panama City that “the days in which our agenda in this hemisphere presumed that the United States could meddle with impunity, those days are past”.

At past Summits of the Americas, which bring together the leaders of North, Central and South America, the US has come in for criticism for its embargo against Cuba and its objection to having Cuba participate in the gatherings. This seventh summit is the first which Cuba will attend and much of the attention will be focussed on the body language between the former foes. The meeting will the be first formal encounter between the leaders of the US and Communist-run Cuba in more than five decades. Mr Obama stressed that he hoped the thaw in relations would improve the lives of the Cuban people. “Not because it’s imposed by us, the United States, but through the talent and ingenuity and aspiration and the conversation among Cubans, among all walks of life. So they can decide what is the best course of prosperity.”

“If we destroy Creation … Creation will destroy us..”

• Sneak Peek At Pope’s Crusade (Paul B. Farrell)

Here’s a sneak peak of Pope Francis’s historic “Climate Change Encyclical,” soon to be released, complete with talking points for his upcoming address to the joint session of Congress. We’ll analyze them: The encyclical’s likely headline: “Safeguard Creation … We are the custodians of Creation … If we destroy Creation … Creation will destroy us,” a public warning often repeated by the pontiff this past year, a message certain to intensify the anger of GOP climate-science deniers, Big Oil, Koch Bros, Exxon Mobil and most fossil-fuel firms, as well as their banks, investors owning their stocks and capitalists everywhere. Here’s why: Pope Francis’s much-anticipated encyclical will be broadcast worldwide to billions, including 5,000 bishops, 400,000 priests and 1.2 billion members of the Roman Catholic Church.

He will be encouraging his army of the faithful to take strong action, fight climate change and global warming threats to the environment. The encyclical will also be translated into hundreds of languages and broadcast worldwide. At the same time, Pope Francis will be lobbying heads of state and religious leaders, and inspiring billions of people worldwide, encouraging them to join this revolution. This historic encyclical will also set the stage for everything else Pope Francis has planned in 2015. He’s a man with a mission to save the world from the accelerating threats to the planet’s natural resources. More immediate, the encyclical will serve as major talking points for his address to the joint session of Congress in September, his address to the United Nations General Assembly in New York and his December message to the historic UN Climate Conference in Paris. Many of his points on the environment are already well known.

“.. instead of realising initial plans to stop and reverse the trend of species loss by 2010, more and more species are disappearing from the agrarian landscape..”

• Agriculture Poses Immense Threat To Environment (EurActiv)

Conventional agriculture is causing enormous environmental damage in Germany, warns a study by the country’s Federal Environment Agency, saying a transition to organic farming and stricter regulation is urgently needed. EurActiv Germany reports. Spanning over 50% of the country, agriculture takes up by far the biggest amount of land in the country, and is one of its most important economic sectors. But intensive farming still harms the environment to an alarming extent, according to a study conducted by the Federal Environment Agency (UBA). The use of pesticides and fertilisers as well as intensive animal husbandry, have a negative impact on humans and nature, the 40-page document indicates. “Over the last 30 years, innovation and technical progress in most sectors has led to great successes in reducing the amount of substance that reaches the environment.

But agriculture emissions show only marginal improvements,” the study’s authors write. One of the most controversial issues concerns greenhouse gas emissions. According to the researchers, the use of moors and clear-cutting for agriculture, as well as fertilisers, soil cultivation and animal husbandry produce a high level of emissions that impact the climate. In 2012, agriculture-related emissions were around 70 million tonnes of CO2 equivalent – about 7.5% of the year’s total greenhouse gas emissions. This means that after industry, which made up 84%, agriculture was the second largest emitter in Germany. Biodiversity is also threatened by intensive farming. Agriculture burdens the environment with nitrogen, phosphorus and heavy metals. Broad-spectrum pesticides not only wipe out parasites, but also kill other beneficial insects.

As a result, this has adverse effects on birds and other mammals, who lose their food resources. The unfortunate result is that instead of realising initial plans to stop and reverse the trend of species loss by 2010, more and more species are disappearing from the agrarian landscape. The authors write that excessive nitrogen emissions are still alarmingly high, with 60% of nitrogen emissions originating from agriculture. Still, the country’s nitrogen surplus has been stagnating at a high level for years. At an average of 97 kg per hectare, it exceeds the German government’s target value within the sustainability strategy by almost 20 kg per hectare. As a result, agriculture, with a share of 57%, is the nation’s largest source of nitrogen emissions into the environment.

A lot more serious than people seem to think.

• California’s New Era of Heat Destroys All Previous Records (Bloomberg)

The California heat of the past 12 months is like nothing ever seen in records going back to 1895. The 12 months before that were similarly without precedent. And the 12 months before that? A freakishly hot year, too. What’s happening in California right now is shattering modern temperature measurements—as well as tree-ring records that stretch back more than 1,000 years. It’s no longer just a record-hot month or a record-hot year that California faces. It’s a stack of broken records leading to the worst drought that’s ever beset the Golden State. The last 12 months were a full 4.5 degrees Fahrenheit (2.5 Celsius) above the 20th century average. Doesn’t sound like much? When measuring average temperatures, day and night, over extended periods of time, it’s extraordinary.

On a planetary scale, just 2.2 degrees Fahrenheit is what separates the hottest year ever recorded (2014) from the coldest (1911). California’s drought has already withered pastures and forced farmers to uproot orchards and fallow farmland. It’s costing the state billions each year that it goes on. Governor Jerry Brown issued an executive order this month for the first mandatory statewide water restrictions in U.S. history, with $10,000-a-day penalties against water agencies that fail to reduce water use by 25%. California has seen droughts before with less rainfall, but it’s the heat that sets this one apart. Higher temperatures increase evaporation from the soil and help deplete reservoirs and groundwater. The reservoirs are already almost half empty this year, and gone is the snowpack that would normally replenish lakes and farmlands well into June.