Arthur Rothstein Interior of migratory fruit worker’s tent, Yakima, Washington Jul 1936

The Fed will never be able to get out. That was clear the moment they stepped in.

• The Market Will Need The Fed Again In 2020 (Axios)

The No.1 risk to the stock market continuing its outperformance next year is not President Trump or consistently weak U.S. economic data or even China, senior analysts at John Hancock Investment Management say, but whether or not the Fed continues to stimulate the economy through what they call “not QE.” What it means: Fed chair Jerome Powell has insisted the central bank’s bond buying program — initiated after rates in the systemically important repo market spiked to five times their normal level in September — is not quantitative easing. But “it walks and talks” like QE, analysts say, and has injected close to $1 trillion of liquidity into the repo market and added more than $260 billion to the Fed’s balance sheet.

The intrigue: The new “not QE” program was “like a fourth rate cut this year,” John Hancock co-chief investment strategist Matthew Miskin said during a media briefing Tuesday in New York. And it has given a boost to the stock market. The big picture: “The equity market has benefited from a super aggressive Fed,” Ethan Harris, head of global economics at Bank of America Merrill Lynch, told Axios during a separate event Tuesday at BAML headquarters. “I mean the Fed basically anesthetized the markets to the trade war escalation this summer.”

Because the Fed was able to mask the economy’s pain from the market, a strong sell-off may be needed to motivate the Trump administration to secure what Harris calls a “skinny” trade deal with China and avert the Dec. 15 tariffs that will hit billions of dollars worth of consumer goods. The converse is also true, Miskin argued. “If things turn more sour because we’re not getting a trade deal or the tariffs go on Dec. 15, the stress underpinning … the market will re-emerge and the Fed’s definitely going to have to be there,” he told Axios.

End the Fed.

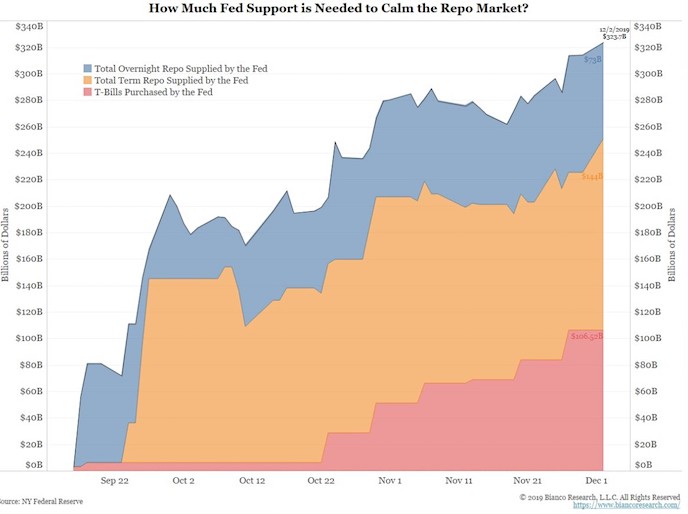

• The Repo Market Is Broken And Fed Injections Are Not A Lasting Solution (MW)

The Federal Reserve’s ongoing efforts to shore up the short-term “repo” lending markets have begun to rattle some market experts. The New York Federal Reserve has spent hundreds of billions of dollars to keep credit flowing through short term money markets since mid-September when a shortage of liquidity caused a spike in overnight borrowing rates. But as the Fed’s interventions have entered a third month, concerns about the market’s dependence on its daily doses of liquidity have grown. “The big picture answer is that the repo market is broken,” said James Bianco, founder of Bianco Research in Chicago, in an interview with MarketWatch. “They are essentially medicating the market into submission,” he said. “But this is not a long-term solution.”

This chart shows the more than $320 billion of total repo market support from the Fed since Sept. 17, when for the central bank began pumping in daily liquidity after overnight lending rates jumped to almost 10% from nearly 2%. Initially, the central bank rolled out roughly $75 billion in daily lending facilities to arm Wall Street’s core set of primary dealers with low-cost overnight loans to keep the roughly $1 trillion daily U.S. Treasury repo market running. The facilities allow banks to snap up loans by pledging safe-haven U.S. Treasurys or agency mortgage-backed securities with the New York Fed, but crucially without the typical risk-based pricing that lenders regularly charge when funding each other.

“..the answer is yes: the market is broken, and you can thank central banks for that.”

• Is Something Broken? Quants Running “Scared” As Nothing Makes Sense (ZH)

It was a year where the S&P put the mini bear market of December 2018 in the dust, and after a dramatic reversal which saw most central banks flip from hawkish to dovish throughout the year…

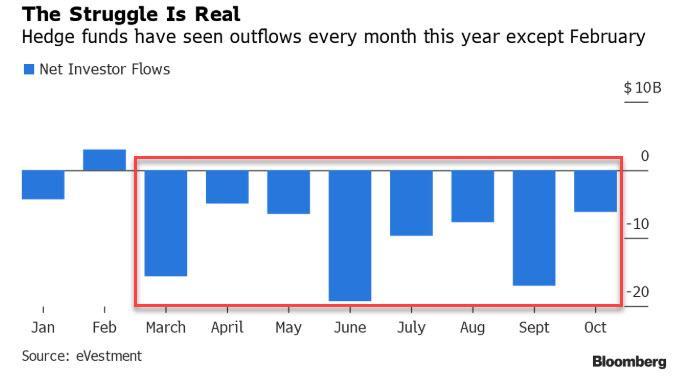

… the MSCI World index is just shy of its January 2018 highs, and the S&P has returned an impressive 24% (despite the jittery start to December), and stands at all time record highs, despite, paradoxically, a year of record equity fund outflow. On paper, this should have been a great year for investors after a dismal 2018. In reality, however, 2019 has been just as painful for not just for hedge funds, which have substantially underperformed the S&P again and in October saw a record 8 consecutive months of outflows, the most since the financial crisis…

… but especially for quants, which after a relatively solid year, suffered the September quant crash that destroyed most of their YTD gains, and have generally been unable to find their bearings in a year in which nothing seemed to work. It’s also Georg Elsaesser, a Frankfurt-based fund manager at Invesco, is trying to calm down his newbie quant clients as choppy stock moves make life difficult for anyone trading factors, which wire up all those systematic portfolios on Wall Street. “Some of them are kind of scared,” Elsaesser told Bloomberg. “They’re asking the questions: Is something going wrong? Is something broken?” Well actually, the answer is yes: the market is broken, and you can thank central banks for that.

All three are Democrat donors who have a deep dislike of Trump. They couldn’t hide that, didn’t even try, instead went on RussiaRussia rants.

But this was supposed to be about the Constitution, not about their opinions. Turley was the only one who stuck to what was on the table.

• Legal Experts Called By Democrats Say Trump’s Actions Are Impeachable (R.)

The hearing on Wednesday was the committee’s first to examine whether Trump’s actions qualify as “high crimes and misdemeanors” punishable by impeachment under the U.S. Constitution. Three law professors chosen by the Democrats made clear during the lengthy session that they believed Trump’s actions constituted impeachable offenses. “If what we’re talking about is not impeachable, then nothing is impeachable,” said University of North Carolina law professor Michael Gerhardt. But George Washington University law professor Jonathan Turley, who was invited by the Republicans, said he did not see clear evidence of illegal conduct. He said the inquiry was moving too quickly and lacked testimony from people with direct knowledge of the relevant events.

“One can oppose President Trump’s policies or actions but still conclude that the current legal case for impeachment is not just woefully inadequate, but in some respects, dangerous, as the basis for the impeachment of an American president,” said Turley, who added that he did not vote for Trump. [..] Republicans focused their questions on Turley, who largely backed up their view that Democrats had not made the case for impeachment – although he did say that leveraging U.S. military aid to investigate a political opponent “if proven, can be an impeachable offense.” Democrats sought to buttress their case by focusing their questions on the other three experts – Gerhardt, Harvard University law professor Noah Feldman and Stanford University law professor Pam Karlan – who said impeachment was justified.

Karlan drew a sharp response from Republicans for a remark about how Trump did not enjoy the unlimited power of a king. “While the president can name his son Barron, he can’t make him a baron,” she said. White House spokeswoman Stephanie Grisham on Twitter called Karlan “classless,” and first lady Melania Trump said Karlan should be “ashamed of your very angry and obviously biased public pandering” for mentioning her 13-year-old son.

Jonathan Turley: "The problem is not that abuse of power can never be an impeachable offense, you just have to prove it, and you haven’t." pic.twitter.com/EXxkHfAXmN

— The Hill (@thehill) December 5, 2019

Thanks to Pamela Karlan for so aptly capturing Democratic elites’ delusional, Reaganite, jingoistic Cold Warrior mindset in your claim that we need to arm Ukraine “so they fight the Russians there and we don’t have to fight them here” & we remain “that shining city on the hill.” pic.twitter.com/C78aNThnUk

— Aaron Maté (@aaronjmate) December 4, 2019

Matt Taibbi: “We laughed at this logic when George W. Bush used it to justify his Mideast wars: “We will fight them over there so we do not have to face them in the United States of America.”

Michael Tracey: “This woman was ostensibly called to testify about the legal and Constitutional questions around impeachment and instead ends up going on a bizarre Cold Warrior rant implying that Russia plans to invade the United States”

• Gaetz Grills Impeachment Witnesses Over Democratic Donations (Fox)

Turning to the professors, he asked UNC-Chapel Hill Professor Michael Gerhardt to confirm that he donated to President Barack Obama. “My family did, yes,” Gerhardt responded. Shifting his attention to Harvard Law Professor Noah Feldman, Gaetz noted the educator has written several articles that portray Trump in a negative light. “Mar-a-Lago ad belongs in impeachment file,” Gaetz said, repeating the title of an April 2017 piece Feldman wrote for Bloomberg Opinion. Gaetz further pressed Feldman, asking him: “Do you believe you’re outside of the political mainstream on the question of impeachment?” Responding to Gaetz, Feldman said impeachment is warranted whenever a president abuses their power for personal gain or when they “corrupt the democratic process.”

The professor added he was an “impeachment skeptic” until the July 25 call between Trump and Ukrainian leader Volodymyr Zelensky. After the exchange, Gaetz turned to Stanford Law Professor Pamela Karlan and challenged her on reported four-figure donations to Clinton, Obama and Sen. Elizabeth Warren, D-Mass. “Why so much more for Hillary than the other two?” he added, smiling. The Florida lawmaker went on to criticize Karlan for a remark she made while answering an earlier question by Rep. Sheila Jackson Lee, D-Texas. Karlan had told Jackson Lee that there is a difference between what Trump can do as president and the powers of a medieval king. “The Constitution says there can be no titles of nobility, so while the president can name his son ‘Barron’, he can’t make him a baron.”

Gaetz fumed at the remark, saying it does not lend “credibility” to her argument. “When you invoke the president’s son’s name here, when you try to make a little joke out of referencing Barron Trump… it makes you look mean, it makes you look like you are attacking someone’s family: the minor child of the president of the United States.”

"America is not just 'the last best hope,' as Mr. Jefferies said, but it's also the shining city on a hill. We can't be the shining city on a hill and promote democracy around the world if we're not promoting it here at home."

— Prof. Pamela S. Karlan #ImpeachmentPBS pic.twitter.com/75l6fcRcWR

— PBS NewsHour (@NewsHour) December 4, 2019

Professor Turley, who voted against Trump in 2016, confirmed under oath today from a legal perspective that there was no bribery, no extortion, no obstruction of justice and no abuse of power. What false charge can Democrats possibly pursue next? pic.twitter.com/pxSazjKFyA

— John Ratcliffe (@RepRatcliffe) December 4, 2019

Rep. Debbie Lesko, R-Ariz., serves on the House Judiciary Committee.

• Judiciary Committee Member: Unfair, Politically Biased Ordeal (USAT)

By now we have all heard the news that President Donald Trump’s counsel will not be participating in the House Judiciary Committee’s first impeachment hearing Wednesday. As a member of the committee, I believe President Trump has made the right decision. In their obsession and rush to impeach the president by the end of the year, Democrats have rigged the process from the start. I wouldn’t blame anyone, let alone the president, for being skeptical about this unfair process. Closed door secret meetings, selectively leaked details, refusing to allow Republican witnesses, and releasing the Schiff report and witness list right before the hearing all indicate an unfair, politically biased ordeal.

With little to no information provided by Judiciary Chairman Jerry Nadler, right now it appears anything goes. The president was provided little notice and no indication of who would be the witnesses or if there would be additional hearings. This leaves more questions than answers as we head into the next phase of an already tainted process. House Democrats do not seem to grasp that they cannot legitimize such an illegitimate process halfway through. This process has been unfair for the president and the Republicans from the start, with Democrats ignoring the historical precedents outlined in the Clinton and Nixon impeachments. When it comes to Trump, Democrats have created a whole new set of rules. For them, the end justifies the means, no matter how devoid of due process and fairness those means are.

I don’t have space for all 10, but Solomon is a must read.

• The 10 Most Important Revelations From The Russia Probe FISA Report (Solomon)

Derogatory information about informant Christopher Steele The FBI stated to the court in a footnote that it was unaware of any derogatory information about the former MI6 agent it was using as “confidential human source 1” in the Russia case. This claim could face a withering analysis in the report. Congressional sources have reported to me that during a recent unclassified meeting they were told the British government flagged concerns about Steele and his reliance on “sub-sources” of intelligence as early as 2015. Bruce Ohr testified he told FBI and DOJ officials early on that he suspected Steele’s intelligence was mostly raw and needed vetting, that Steele was working with Hillary Clinton’s campaign in some capacity and appeared desperate to defeat Trump in the 2016 election.

And documents show State Department official Kathleen Kavalec alerted the FBI eight days before the first FISA warrant was obtained that Steele may have been peddling a now-debunked rumor that Trump and Vladimir Putin were secretly communicating through a Russian bank’s computer server. Most experts I talked with say each of these revelations might constitute derogatory information that should be disclosed to the court. On a related note, Horowitz just released a separate report that concluded the FBI is doing a poor job of vetting informants like Steele, suggesting there was a culture of withholding derogatory information from informants’ reliability and credibility validation reports.

News leaks as evidence One of Horowitz’s earlier investigative reports that recommended fired FBI Deputy Director Andrew McCabe for possible prosecution put an uncomfortable spotlight on the bureau’s culture of news leaks. Since then, a handful of other cases unrelated to Russia have raised additional questions about whether the FBI uses news leaks to create or cite evidence in courts. One key to watch in the Horowitz report is the analysis of whether it was appropriate for the FBI to use a Yahoo News article as validating evidence to support Steele’s dossier. We now know from testimony and court filings that Steele, his dossier and Fusion GPS founder Glenn Simpson played a role in that Yahoo News story.

It’s not just the Fed, but they haven’t exactly helped.

• Illinois’ Unfunded Pension Liability Rises To $137.3 Billion (R.)

Illinois’ growing unfunded pension liability, which increased by $3.8 billion to $137.3 billion at the end of fiscal 2019, underscores the need for state action to boost funding or cut costs, analysts said on Wednesday. The increase was fueled by actuarially insufficient state contributions and lower-than-expected investment returns, according to a new state legislative report. Illinois has the lowest credit ratings among U.S. states at a notch or two above the junk level due to its huge unfunded pension liability and chronic structural budget deficit.

Eric Kim, a Fitch Ratings analyst, said growth in the unfunded liability is expected to continue as long as contributions lag actuarial requirements and pension benefits are protected under the Illinois Constitution. “For us, what this all speaks to is the state addressing fundamental structural budget challenges,” he said. Earlier this year, Governor J.B. Pritzker created pension task forces, including one to explore asset sales to boost pension funding. Laurence Msall, president of Chicago-based government finance watchdog the Civic Federation, said the state has not effectively attacked core pension problems, including unsustainable costs. “At best Illinois is running in place, while trying to avoid sliding downhill,” he said.

A normal market phenomenon?

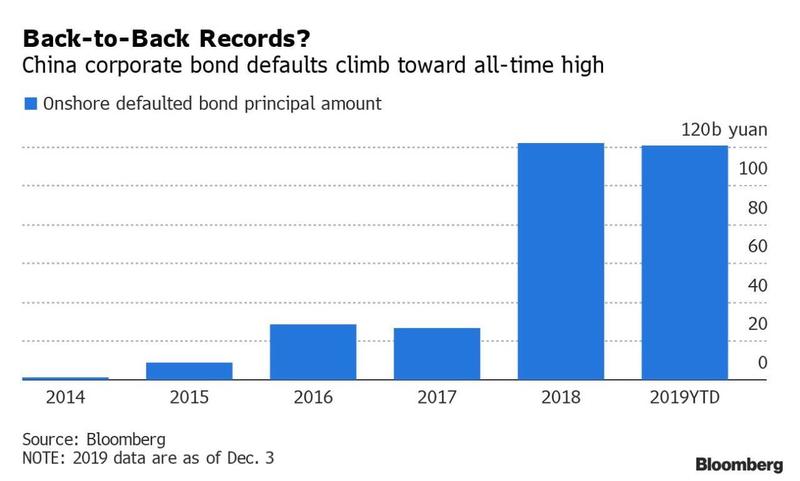

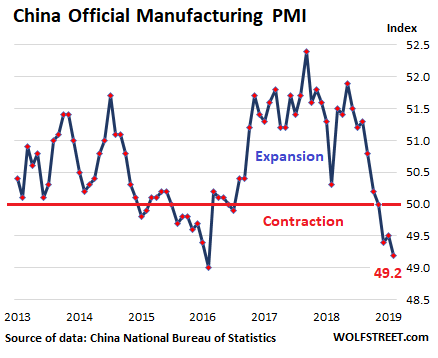

• China Set To Make History With Record Number Of Bond Defaults In 2019 (ZH)

While China is bracing for what may be a historic D-Day event on December 9, when the “unprecedented” default of state-owned, commodity-trading conglomerate Tewoo with $38 billion in assets may take place, it has already been a banner year for Chinese bankruptcies. According to Bloomberg data, China is set to hit another dismal milestone in 2019 when a record amount of onshore bonds are set to default, confirming that something is indeed cracking in China’s financial system and “testing the government’s ability to keep financial markets stable as the economy slows and companies struggle to cope with unprecedented levels of debt.”

After a brief lull in the third quarter, a burst of at least 15 new defaults since the start of November have sent the year’s total to 120.4 billion yuan ($17.1 billion), and set to eclipse the 121.9 billion yuan annual record in 2018. The good news is that this number still represents a tiny fraction of China’s $4.4 trillion onshore corporate bond market; the bad news is that the rapidly rising number is approaching a tipping point that could unleash a default cascade, and in the process fueling concerns of potential contagion as investors struggle to gauge which companies have Beijing’s support. As Bloomberg notes, policy makers have been walking a tightrope as they try to roll back the implicit guarantees that have long distorted Chinese debt markets, without dragging down an economy already weakened by the trade war and tepid global growth.

The French know how to strike.

• France Braces For Biggest Strikes Of Macron’s Presidency (G.)

Emmanuel Macron is braced for the biggest strikes of his presidency as French rail workers, air-traffic controllers, teachers and public sector staff take to the streets on Thursday against proposed changes to the pension system. French rail transport is expected to almost completely grind to a halt with 82% of drivers on strike and at least 90% of regional trains cancelled, amid fears that the transport disruption could continue for days. In Paris, 11 out of 16 metro lines will shut completely, with commuters scrambling to hire bikes and scooters. Many schools will close and even some police unions have even warned of “symbolic” closures of certain police stations. Shops along the route of a march in Paris have been advised to close in case of violence on the edges of the demonstration. About half of the scheduled Eurostar trains between Paris and London have been cancelled.

The standoff is a crucial test for the centrist French president, whose planned overhaul of the pensions system was a key election promise. The government argues that unifying the pensions system – and getting rid of the 42 “special” regimes for sectors ranging from rail and energy workers to lawyers and Paris Opera staff – is crucial to keep the system financially viable as the French population ages. But unions say introducing a “universal” system for all will mean millions of workers in both the public and private sectors must work beyond the legal retirement age of 62 or face a severe drop in the value of their pensions. The row cuts to the heart of Macron’s presidential project and his promise to deliver the biggest transformation of the French social model and welfare system since the postwar era.

Does Uber have more lawyers than drivers?

• Uber Faces £1,500,000,000 Bill For Unpaid VAT (Metro)

Car-sharing giant Uber is a step closer to being liable for an estimated £1.5 billion in unpaid UK tax. Campaigners have won an important legal step that could pave the way for the taxman to come knocking on the beleaguered firm’s door. The move is on top of another legal challenge to stop Uber operating in London. Uber has long-argued that it is a platform that brings drivers and riders together, rather than a transport business. This means that it falls to individual drivers to pay VAT on any rides instead of the company itself. But as the threshold for VAT is only for individuals earning more than £85,000 a year, none of the drivers need to charge it. Campaigners from the Good Law Project calculates this has cost the public £1.5 billion in lost revenue so far.

The law team initially attempted to take Uber to court to force them to disclose their tax affairs but the case looked like being too expensive. Instead, they challenged HM Revenues and Customs and demanded the taxman assess Uber for VAT liabilities. HMRC objected, saying its dealings with Uber were commercially sensitive and it should not have to disclose whether or not it is investigating. Today the Court of Appeal rejected HMRC’s arguments and Mrs Justice Lieven said HMRC now had to disclose whether or not they had made an assessment over Uber’s payment of VAT. The case for the Good Law Project is being led by anti-Brexit campaigner Jolyon Maugham QC who said: ‘The more time passes without an assessment being raised the more VAT is lost – forever.’

Again, Assange -with his aides- is the only person who has abided by the law. All other parties involved have not. That should have a huge bearing on the case.

• Julian Assange in Videoconference: The Spanish Case Takes a Turn (IPD)

The UK Central Authority has had a change of heart. On December 20, Assange is set to be transferred from his current maximum-security abode, Belmarsh, to Westminster Magistrates Court to answer questions that will be posed by De la Mata. To date, the evidence on Morales and the conduct of his organisation is bulking and burgeoning. It is said that the company refurbished the security equipment of the London Ecuadorean embassy in 2017, during which Morales installed surveillance cameras equipped with microphone facilities. While Ecuadorean embassy officials sought to reassure Assange that no recordings of his private conversations with journalists or legal officials were taking place, the opposite proved true.

An unconvinced Assange sought to counter such measures with his own methods. He spoke to guests in the women’s bathroom. He deployed a “squelch box” designed to emit sounds of disruption. These were treated as the measures of a crank rather than those of justifiable concern. The stance taken by Ecuador has not shifted, despite claims by Morales that any recordings of Assange were done at the behest of the Ecuadorean secret service. Instead, Ecuador’s President Lenín Moreno has used the unconvincing argument that Assange, not Ecuador, posed the espionage threat. “It is unfortunate that, from our territory and with the permission of authorities of the previous government, facilities have been provided within the Ecuadorean embassy in London to interfere in the processes of other states.” The embassy, he argued, had been converted into a makeshift “centre for spying.”

German broadcasters NDR and WDR have also viewed documents discussing a boastful Morales keen to praise his employees for playing “in the first league…We are now working for the dark side.” The dark side, it transpires, were those “American friends,” members of the “US Secret Service” that Morales was more than happy to feed samples to. NDR has added its name to those filing charges against UC Global for allegations that its own journalists were spied upon in visiting the Ecuadorean embassy in London.

The allegations have the potential to furnish a case Assange’s lawyers are hoping to make: that attaining a fair trial in the United States should he be extradited to face 18 charges mostly relating to espionage would be nigh impossible. The link between UC Global, the US intelligence services, and the breach of attorney-client privilege, is the sort of heady mix bound to sabotage any quaint notions of due process. The publisher is well and truly damned.

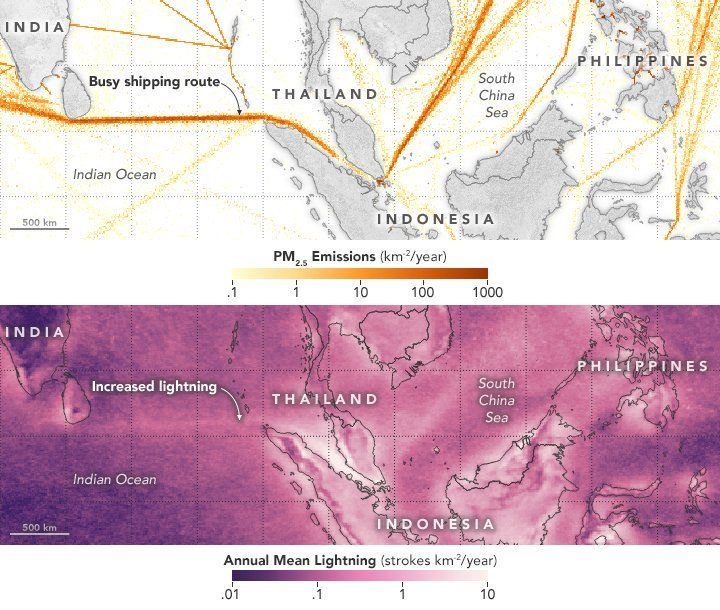

Simon Kuestenmacher: Map shows that #lightning follows shipping lanes: As it turns out particles in ship exhaust increase the likelihood and intensity of thunderstorms. Really cool fact that I had never considered! Source: https://buff.ly/2B0tcOV

Please support the Automatic Earth on Paypal and Patreon so we can continue to publish.

Top of the page, left and right sidebars. Thank you.

.jpg)