Charlie Kirk with his family 2025

At 31 years old, Charlie Kirk has passed away after being shot at a campus event in Utah.

Please join us in prayer for him and his family.

His dedication to his God, his family, and his country will continue to inspire countless Americans, and his legacy will live on forever.… pic.twitter.com/6SIMYiF2uc

— Townhall.com (@townhallcom) September 10, 2025

I am offering $500k in $10k grants to paint murals of the face of Iryna Zarutska in prominent US city locations

Please contact katie@eoghan.com for more details

Please also share this message

If you would like to contribute to this fund, please contact Katie also pic.twitter.com/M8OyqfcZlm

— Eoghan McCabe (@eoghan) September 10, 2025

Leavitt

https://twitter.com/GuntherEagleman/status/1965471159274672129

https://twitter.com/DerrickEvans4WV/status/1965484112183214339

Walsh

Time for MASSIVE change in America

pic.twitter.com/IyUpNRHB2e— Elon Musk (@elonmusk) September 10, 2025

Matt Walsh: "As a society, we have two choices. Either we inflict severe, merciless suffering on violent criminals, or we allow severe, merciless suffering to be inflicted on the innocent. One group or the other will endure brutality and violence."pic.twitter.com/MmapO05yjD

— Joe Rogan Podcast News (@joeroganhq) September 9, 2025

11

"The average homicide suspect has been arrested ELEVEN times prior to them committing a homicide. That is a problem. That is a problem!"

"WE NEED TO KEEP VIOLENT PEOPLE IN JAIL"

– Former DC Police Chief Robert Contee, in 2023 pic.twitter.com/DVBTiEFTBV

— Vince Coglianese (@VinceCoglianese) September 9, 2025

Bessent

https://twitter.com/EricLDaugh/status/1965553818399044053

America has seen two violent murders in the span of one week, Iryna Zarutska and Charlie Kirk. What appears to tie the two together is the influence of what passes for a leftish world view these days. A view that made it possible for Zarutska’s killer to roam free despite countless arrests, as well as requests for psychological treatment. That guy should never have been on that train, and just about everyone who’s been in contact with him knows why. Woke society decided to set him free.

Charlie Kirk became a victim of his association with Donald Trump. If you can’t get to the boss, look at those around him. It’s very painfully ironic that Charlie lived by the word, not the sword. His favoite terrain was the dialogue, the exchange of ideas, but that’s not everyone’s favorite. Still, he wasn’t a far right wing activist or anything like it.

Violence in America comes from the left, they just about have secured a monopoly on it, while maintaining the illusion that it’s the right that is the real threat. That’s one false idea that needs urgent correction.

We’re going to let it all sink in, and read about it, and have the dialogue that Charlie loved so much, but what remains more than anything right now is the pain. As for Iryna: you’re beautiful. It breaks our hearts that we couldn’t save you.

“”I don’t know why this is affecting me so personally.” Its because in Charlie you see yourself, the most polite version of yourself, the most articulate, the most charitable to your enemies. And even that wouldn’t be enough to save you from them.”

• “Dark Moment For America” – Trump Addresses The Nation (ZH) /span>

Update (2114ET) President Trump addressed the nation from the Oval Office on the senseless political assassination of Charlie Kirk at a Turning Point event at Utah Valley University, calling it a “dark moment for America.” Trump called Kirk a “martyr for truth” and vowed to crack down on the radical left… The president continued:

“My administration will find each and every one of those who contributed to this atrocity and to other political violence, including the organizations that fund it and support it, as well as those who go after our judges, law enforcement officials, and everyone else who brings order to our country. I am filled with grief and anger at the heinous assassination of Charlie Kirk on a college campus in Utah. Charlie inspired millions, tonight all who knew him and loved him are united in shock and horror.

From the attack on my life in Butler, Pennsylvania last year, which killed a husband and father, to the attacks on ICE agents, to the vicious murder of a healthcare executive in the streets of New York, to the shooting of House Majority Leader Steve Scalise and three others. Radical left political violence has hurt too many innocent people and taken too many lives. Tonight, I ask all Americans to commit themselves to the American values for which Charlie Kirk lived and died, the values of free speech, citizenship, the rule of law. His legacy will live on for countless generations to come. Today, because of this heinous act, Charlie’s voice has become bigger and grander than ever before, and it’s not even close. May God bless his memory. May God watch over his family.”

Our takeaway is that the radical left, which has been funding chaos through dark-money NGOs and other groups, is about to get a major wake-up call from the Trump administration. A move to counter these rogue NGOs could be just one executive order away. Stay tuned.

— Karoline Leavitt (@PressSec) September 11, 2025

Kirk made a name for himself about winning debates in “proper democratic fashion” …

https://twitter.com/Sargon_of_Akkad/status/1965869904130945521?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E1965869904130945521%7Ctwgr%5E9ceb77cf7b8d03814b551d89085043857317275d%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fwww.zerohedge.com%2Fpolitical%2Fshots-reportedly-fired-charlie-kirk-event-utah-valley-university

Civil terrorism expert Jason Curtis Anderson of One City Rising states:

“The assassination of Charlie Kirk marks a dangerous escalation in America’s culture war—where the battle of ideas is now escalating into political violence against those who run organizations devoted to debate and civil discourse. Very few people grasp the gravity of this moment . Incidents like this don’t exist in isolation; they risk triggering a chain of events that can further destabilize the country. Whether it’s the anti-ICE movement, pro-Palestinian agitators, anarchist networks, or NGO-backed permanent protest groups like Indivisible, we are watching the rise of something new and deeply alarming. As Tal Fortgang wrote in City Journal, America is entering a new era of civil terrorism—where the goal is no longer peaceful protest, but intimidation, silencing, and destabilization of our democratic order.”

Like us, many are struggling to find the words to discuss this but @Merovingianus offered some useful insight:

“Among all the justifiable outrage over the years, Charlie Kirk has consistently been one the calmest and most polite among us. Someone shot him and the entire scope of the Left is celebrating. If we do not act accordingly we might as well surrender now. I’ve seen several people saying something along the lines of “I don’t know why this is affecting me so personally.” Its because in Charlie you see yourself, the most polite version of yourself, the most articulate, the most charitable to your enemies. And even that wouldn’t be enough to save you from them. It is because you are seeing that the marketplace of ideas you grew up believing as sacred is now a war zone that will get you killed and you’re struggling to reconcile the world you live in with the world you grew up in.

You are struggling to comprehend and incorporate the irrefutable evidence that this political divide isn’t one solved by polite exchange of ideas and that we are in a nation at war with itself.”

RIP Charlie.

Let’s have 1,000 murals each all over the country for Iryna Zarutska and Charlie Kirk.

• Elon Musk Jumps In On Iryna Zarutska Mural Project (Tim O’Brien)

After George Floyd died and in the mayhem over the Black Lives Matter and Antifa riots, a cottage industry of artistic murals erupted, transforming Floyd from a common street thug into a saintly martyr. Within days of his death, a mural was painted on the site where Floyd died at the Cup Foods convenience store at 38th Street and Chicago Avenue. Shortly thereafter, a second mural was painted nearby. This sparked artists across the country and around the world to add to the contrived mythology of Floyd, creating murals in places as far away as Idlib, Syria, Barcelona, Spain, Dublin, and Berlin. The murals were one of the few purely peaceful ways Floyd was honored at the time.

Fast forward to this week, when news of the murder of Iryna Zarutska broke, and conservatives and everyday people were outraged, while the legacy media and the Left remained silent. No riots, no looting from the right, but plenty of anger. That anger, and a respect for Zarutska, appears to have inspired the CEO and founder of Intercom, Eoghan McCabe, to post on X that he’s “offering $500k in $10k grants to paint murals of the face of Iryna Zarutska in prominent US city locations.” He then provided an email address to learn more about this impromptu memorial project.

This morning, Elon Musk posted on X: “I will contribute $1M.” With momentum like this, expect to start seeing the face of Zarutska in a city near you. Who is McCabe? He’s a Berkeley-based entrepreneur who is prominent in the AI customer service sector. Earlier this week, like millions of Americans, he was outraged by the cold-blooded killing of Zarutska. He called for quick consequences for the person convicted of this crime, “I do think that rapid, public executions for crimes like this are a spiritual goal that we should point ourselves towards. I worry about Western society if we can’t react in proportion to how evil this is.” In another post on X, McCabe said, “It’s an objective fact that leftism is responsible for this[.] The leftist politicians who kept this monster free are evil, and must be very severely punished[.]”

Zarutska’s murder has outraged Americans for a number of reasons this week. The killing itself was so sudden and so gruesome on public transportation in a relatively safe city like Charlotte, that anyone who spends any time in public spaces can easily imagine something like this happening to them. The fact that the killing happened on August 22, but it only emerged in the public consciousness over a week later, and only on social media at first, is unsettling. How can such an inhuman act not make national news. Related to this is the reaction on the right. The cultural dilemma for everyone is based on trust in the news media. If the news media willfully ignores or even buries a story like this to advance its narratives, then what good is it?

Matt Margolis detailed how wretched the legacy media behaved once conservatives shamed it into covering the story. A healthy media landscape would shout this news early and often as a warning to America that something needs to be done about crime and the people who commit it. Now. Instead, through its silence and even worse, for blaming conservatives for noticing the murder, the news media has decidedly taken a stance in favor of more crime, more murder, more killings of people like Zarutska at the hands of hardened criminals like Decarlos Brown, Jr.

A story that tells itself.

• “Art Must Always Tell The Truth” (CTH)

Popular artist Banksy created a graffiti mural in London depicting the current state of the UK censorship system using the courts to trample the rights of British citizens:

It did not take long for the authorities to cover the mural and eventually attempt to remove it.

A good illustration of modern Britain. Masked man removes artistic dissent against a Tyrannical State, under the guard of Foreign State Security.pic.twitter.com/Ley9jAIYUW

— Paul Weston (@PWestoff) September 10, 2025

However, what remained of the artwork was the essential core of the truth.

I particularly like the fact the govt turned the CCTV camera, so they can monitor who might visit the scene of the criminal dissent.

Apparently, the British government doesn’t quite see the irony.

Intriguing take: “..some drones used by Ukrainian and Russian forces for mutual attacks “lost their track as a result of the impact of the parties’ electronic warfare assets.”

• Kremlin Responds To Polish ‘Drone Attack’ Claims (RT)

Moscow has dismissed Poland’s latest claim that Russian drones breached the country’s air space. Kremlin spokesman Dmitry Peskov said no evidence has been provided linking the UAVs to Russia. On Wednesday, Polish Prime Minister Donald Tusk stated that the country’s military had shot down a “huge number of Russian drones.” Warsaw has described the incident as an “unprecedented violation of Polish airspace” and an “act of aggression.” However, Peskov has dismissed the accusations, pointing out that “The EU and NATO leadership accuse Russia of provocation on a daily basis. Most often, without even trying to provide any arguments.”

He further noted that, to his knowledge, the Kremlin has not yet received any request for contact from the Polish leadership over the incident. Meanwhile, Russia’s charge d’affaires in Warsaw, Andrey Ordash, told RIA Novosti that when he was summoned to the Polish Foreign Ministry on Wednesday, the Polish authorities did not provide any evidence that the downed UAVs belonged to Russia. He noted that the drones had flown into Poland from Ukraine. Tusk has claimed, however, that the aircraft came from Belarus rather than Ukraine, and characterized the incident as a Russian “provocation.” The Belarusian military had previously reported giving Poland early warning that some drones used by Ukrainian and Russian forces for mutual attacks “lost their track as a result of the impact of the parties’ electronic warfare assets.”

After announcing the alleged airspace violation, Tusk formally invoked Article 4 of NATO’s founding treaty, which provides for consultations in case one of the bloc’s members believes its security is threatened. Last week, former Polish President Andzej Duda referenced a November 2022 incident in which a Ukrainian missile landed on Polish territory. Kiev insisted it was an intentional Russian attack and called for NATO-level retaliation. Duda said that Ukrainian authorities were trying to get the US-led bloc into a direct confrontation with Russia, describing such a scenario as a “dream” for Kiev, but unacceptable for Poland.

“.. once we get this peace settled, we could have a very productive economic relationship with both Russia and Ukraine..”

• Trump Against Economic Isolation of Russia – Vance (RT)

US President Donald Trump does not view attempts to isolate Russia economically as a sustainable strategy and believes trilateral cooperation involving Moscow, Kiev, and Washington could ensure lasting peace in Eastern Europe, Vice President J.D. Vance said on Tuesday. In an interview with One America News Network, Vance described joint ventures with Russia as “one of the carrots” the Trump administration is offering in efforts to broker an end to the Ukraine conflict. The approach contrasts with Western European leaders who have sought to dismantle Russian trade ties, arguing that past decades of energy reliance on Moscow were a strategic mistake, but in doing so they have significantly worsened their own economic situation.

“The president’s been very open with both the Europeans and the Russians that he doesn’t see any reason why we should economically isolate Russia except for the continuation of the conflict,” Vance said. He stressed that Russia possessed vast natural resources whether other parties liked it or not, and that “once we get this peace settled, we could have a very productive economic relationship with both Russia and Ukraine.” Shared economic growth, he added, could be “the best guarantee of a long-term peace.”

Vance contrasted Trump’s stance with that of the previous administration, which he said poured American resources into Ukraine without any real exit plan. He was responding to host Matt Gaetz’s claims that behind closed doors Moscow was offering to increase use of the US dollar in energy trade to help ease American domestic prices. Last week, EU foreign policy chief Kaja Kallas accused Trump of “weakening” allies with trade tariffs and undermining Western unity. Russian officials have highlighted the benefits of renewed cooperation with the US. President Vladimir Putin said Russian businesses had both capital and technology to pursue lucrative joint projects, including gas extraction ventures in Alaska and the Arctic, if Washington is willing to give political approval.

Like the spring 2022 Bucha false flag before it, the Yarovaya provocation looks like a fresh push to break off the peace process, and blame Russia.”

• ‘Russian Strike on Pension Queue’ Claims Debunked (Sp.)

Ukrainian officials have accused Russia of killing 24 people on line to collect pensions in the village of Yarovaya in the Ukrainian-occupied area of the Donetsk People’s Republic. Here’s why the claims don’t hold up. “The world must not remain silent,” Zelensky urged after publicizing the incident, demanding a “response” from the US and Europe. There’s just one problem: the incident bears all the hallmarks of a false flag. Here’s evidence. A Russian MoD source told Sputnik that Russian forces did not carry out any attacks in the vicinity of Yarovaya on September 9, with the last strike in the area carried out on the night of September 7, and targeting an area near the neighboring settlement of Novosyolovka on the line of contact. No reports on casualties were issues before Zelensky made his claims.

Info about the ‘Russian strike’ was immediately disseminated by Zelensky-aligned social media and immediately picked up by Ukrainian and Western media. Footage presented by the Ukrainian side shows landmarks that can be easily be determined on satellite maps, including the post office building, a local memorial and trees surrounding both. The destruction in the footage doesn’t even come close to matching the shape and size of a Russian aerial bomb (Russian 100 kg FAB-250 and 200 kg FAB-500 bombs’ destructive radius and power is incomparably greater than that shown in the video). Instead, the destruction looks more like the result of the detonation of an explosive device with the equivalent of just a few kg of TNT.

Yarovaya is one of the increasingly few areas of the DPR still under Ukraine’s control, signifying Kiev’s rejection of Russia’s negotiating position for ending the conflict, which includes full Ukrainian withdrawal from the Donbass. The provocation comes on the heels of last month’s summit meeting between Putin and Trump, during which Trump backed off on US sanctions threats. Like the spring 2022 Bucha false flag before it, the Yarovaya provocation looks like a fresh push to break off the peace process, and blame Russia.

“..an amateurish and dim top diplomat becomes a disgrace to be ashamed of before the world, even among embarrassed friends.”

The word diplomat is losing its meaning, if it’s not already gone. A diplomat must engage in diplomacy, be diplomatic. Kallas obviously doesn’t fit that notion.

• Wondering Why The EU Is So Screwed? Just Look At Its Top Diplomat (Amar)

Kaja Kallas, the European Union’s de facto foreign minister (and former prime minister of Estonia), is unusually, grotesquely incompetent, even for an unelected EU apparatchik. Like former German Foreign Minister Annalena “360 Degrees” Baerbock – now instagraming like an excited upper-class teenager from her ill-begotten UN sinecure in New York – Kallas also displays an enormous capacity for being pleased with herself. She appears never happier than when holding a mic to her own platitudes, presented in a mortifyingly basic form of very labored English, while being obsequiously soft-balled by a fawning interviewer. In both cases, the contrast between the self-image and reality is jarring: Kallas and Baerbock’s obvious, glaring lack of intellectual ability, elementary education, and basic professional know-how should have ended their misguided career ambitions long ago.

Yet, instead, Kallas, like Baerbock, has not only rapidly fallen up the slippery ladder of career and privilege. She has done so in a particularly visible area. High officials responsible for the economy, for instance, can do – and do – enormous damage. But those in charge of foreign policy are no less dangerous, while, literally, publicly representing tens or hundreds of millions of people. A professional and intelligent foreign minister – such as, for instance, China’s Wang Yi, India’s S. Jaishankar, or Russia’s Sergey Lavrov – can enhance respect for a country or bloc even among its critics or opponents. However, an amateurish and dim top diplomat becomes a disgrace to be ashamed of before the world, even among embarrassed friends. They’re perhaps worse: a laughingstock, signaling that whoever chooses to be represented by a fool must be foolish as well.

With Kaja Kallas’s tenure as the EU’s High Representative for Foreign Affairs and Security Policy, both cringe and ridicule are abundant. Her recent peak performances have included a truly inane take on the history of the Second World War, silly and rather racist musings on the general abilities of “the Russians” and “the Chinese,” and, of course, a preposterous attempt to blame them – plus Iran and North Korea – for disrupting our brave old world of a rules-bound order that includes the Gaza genocide, compliments of Israel and the West. Regarding what Kallas mistakes for history, the high-flyer from Estonia has opined that she was surprised by claims that Russia and China fought together in and won World War II. Of course, that’s simply a fact: Both countries were and are widely recognized as prominent members of the alliance that defeated global fascism in Europe and Asia.

Indeed, if Kallas were capable of telling an intern to Google the matter or consult the online version of the Encyclopedia Britannica, she’d find out quickly that China and Russia (then the core of the Soviet Union) are counted among the “Big Four” core of the alliance (alongside Great Britain and the US). This place was earned with rivers of blood: China and the Soviet Union were the two most brutally devastated countries in World War Two. China fought massive Japanese forces, and Russia broke the spine of Nazi Germany’s Wehrmacht. Even busy Estonian collaborators could not save the day for the Führer.

“..using the Ukraine conflict to financially chain its member nations so that it can subjugate them and strip them of their sovereignty..”

• EU Uses Ukraine Conflict To Create ‘United States Of Europe’ – Orban (TASS)

The leadership of the European Union is using the Ukraine conflict to financially chain its member nations so that it can subjugate them and strip them of their sovereignty, Hungarian Prime Minister Viktor Orban believes. “The Brusselian elite are pushing joint indebtedness to strip nations of their sovereignty and drag us toward a United States of Europe. They want to use the war in Ukraine as the pretext to shackle us all financially. We must look beyond the battlefield to the future of the Union itself: free nations or submission to unelected bureaucrats?” he wrote on the X social network. The Hungarian Prime Minister noted that by doing this, the EU is making a last-ditch effort to preserve itself as currently formulated. Earlier, Orban said that the EU bureaucratic center had ceased to play the role of coordinator of the bloc and has turned into a “Frankenstein pursuing its own interests.”

He stressed that when the EU was created, it was agreed that power would be concentrated in the hands of individual nations, but now Brussels is trying to centralize that power. According to the politician, the leadership of the association is encroaching on the sovereignty of its participants, and failing to resolve any crises along the way. Since the very beginning of the conflict in Ukraine, the Hungarian government has consistently advocated for its peaceful resolution and has called on its allies to resume dialogue with Russia. Hungary also refuses to support Ukraine’s accelerated accession to the EU, warning that this would cause serious damage to the European economy and could lead to a direct military clash with Russia.

Raw power game.

• Brussels Pushing To Silence Dissent Among EU Members (RT)

The European Commission has announced plans to scrap consensus-based decision-making in EU foreign policy, in a step that could sideline member states resisting Brussels’ line. Brussels has long weighed replacing unanimity – a founding principle of EU foreign policy – with majority voting, arguing the change would speed up decisions and stop individual states from blocking measures such as sanctions and military aid for Ukraine. Under the current system, all 27 members must agree for decisions to pass. The proposed reform would require a qualified majority, meaning decisions would be adopted if backed by a set threshold of states. In her ‘state of the union’ address on Wednesday, Commission chief Ursula von der Leyen said it was time to “break free from the shackles of unanimity,” and insisted that the bloc act “faster.”

“I believe that we need to move to qualified majority in some areas, for example in foreign policy,” she stated. The EC chief, who has repeatedly invoked the “Russian threat” to justify military aid to Ukraine, sanctions, and the push for accelerated militarization, was met with opposition from Slovakia and Hungary. Both governments have repeatedly threatened to use their veto powers to block EU actions they view as harmful to their national interests. Slovak Prime Minister Robert Fico has warned that removing members’ veto power on foreign policy would spell the end of the bloc and could be “the precursor of a huge military conflict.”

Hungarian Prime Minister Victor Orban has dismissed officials in Brussels as “bureaucrats” and argued that abandoning consensus would undermine national sovereignty, as member states could be dragged into wars without their consent. Orban said the EU is on the verge of collapse and will not survive beyond the next decade without a “fundamental structural overhaul” and disentanglement from the Ukraine conflict. Moscow has accused the West of pursuing “uncontrolled militarization” to prepare for war with Russia, while dismissing claims it intends to attack NATO or EU states as “nonsense.” Russian officials, including President Vladimir Putin, have accused Western leaders of fearmongering to justify inflated military budgets and to cover up their economic failures, insisting that aid to Kiev only prolongs the hostilities.

Hahaha:

“Ukraine will only pay back the loan once Russia pays for the reparations,” she said.”

• EU Eyes Russian Assets For Ukraine ‘Reparations Loan’ (RT)

European Commission President Ursula von der Leyen has proposed leveraging Russian assets illegally frozen in the EU for a “reparations loan” for Ukraine. Delivering a state of the union address to the EU parliament on Wednesday, the former German defense minister did not propose outright confiscation of the Russian assets, reportedly comprising some $300 billion. Moscow has condemned the asset freeze and warned that seizure would amount to “robbery” and violate international law, while also backfiring on the West. Von der Leyen introduced what she said was an urgently needed new mechanism to finance Kiev’s warchest, using Russia’s immobilized funds. Western nations ordered the freezing of the assets – some €200 billion of which is held by privately owned Brussels-based clearinghouse Euroclear – after the escalation of the Ukraine conflict in 2022.

The funds have accrued billions in interest, and the West has explored ways to use the revenue to finance Ukraine. ”With the cash balances associated to these Russian assets, we can provide Ukraine with a reparations loan,” von der Leyen claimed, noting that “the assets themselves will not be touched” and that the risk would have to be “carried collectively.” “Ukraine will only pay back the loan once Russia pays for the reparations,” she said. The money, von der Leyen added, would fund Kiev’s military and ensure the security of the civilian population. Von der Leyen gave no figures, while the G7 last year backed a plan to provide Kiev with $50 billion in loans to be repaid using the profits. The EU pledged $21 billion.

She also announced an initiative aimed at boosting Ukraine’s military, including through a proposed “drone alliance,” explaining that the EU would “frontload” €6 billion. The proposal stops short of confiscation, which most EU states reject due to financial and legal risks. Several countries have also dismissed the idea of a “reparations loan,” warning it could breach international law. Belgium has been especially vocal. Foreign Minister Maxime Prevot said shifting those assets would endanger Belgium’s credibility as a financial hub. “Confiscating those Russian sovereign assets is really not an option,” Prevot said. “It would be a very bad signal to other countries worldwide” and could also “erode confidence and trust in the euro,” according to the minister.

Did they miss them on purpose? Or do they just have poor aim?

• Gulf Cooperation Council to Support Any Action by Qatar After Israeli Attack (Sp.)

The Gulf Cooperation Council (GCC) stands in solidarity with Qatar and will support any response following the Israeli strikes on Doha, GCC Secretary General Jasem Albudaiwi said. “The Council states express full solidarity with the State of Qatar and support any measures it takes,” GCC Secretary General Jasem Albudaiwi said. On Tuesday, the Israel Defense Forces said it had carried out strikes in Doha targeting senior officials of Palestinian movement Hamas. Eyewitnesses told Sputnik that several explosions occurred in the center of Qatar’s capital. World powers, including the United Kingdom, Germany and India, have condemned the Israeli airstrike on Hamas members in Doha and called for restraint.

“Today’s airstrike by Israel against Hamas leaders in Doha breaches international law and Qatar’s territorial integrity, and risks a further escalation of violence in the region,” the European External Action Service said in a statement. UK Prime Minister Keir Starmer condemned Israel’s strike and called for “immediate ceasefire, the release of hostages, and a huge surge in aid into Gaza.” India is concerned about the Israeli airstrike on Doha and calls for restraint to ensure peace and security in the region are not jeopardized, the Indian Foreign Ministry noted. “The Netherlands condemns the Israeli airstrike in Doha. The sovereignty of states must be respected. Additionally, this step doesn’t bring a much needed ceasefire in the Gaza Strip any closer,” Dutch Foreign Minister David van Weel said on X.

German Foreign Minister Johann Wadephul noted that the Israeli attack not only violates Qatar’s territorial sovereignty, “but also jeopardizes our efforts to free the hostages.” Wadeful urged all parties to make every effort to achieve a ceasefire and free the hostages. “Cuba expresses its strongest condemnation of the Israeli attack on the Hamas headquarters in Doha, which constitutes a new extrajudicial execution by Zionism, a flagrant violation of international law and the sovereignty of Qatar, and a serious threat to regional security and stability,” Cuban Foreign Minister Bruno Rodriguez Parrilla said on X.

Venezuelan Foreign Minister Yvan Gil also condemned “the cowardly attack by the [Israeli Prime Minister Benjamin] Netanyahu regime on the sovereignty and territorial integrity of Qatar,” calling the airstrike “an act of state terrorism, a flagrant violation of international law and a challenge to the principles of peaceful coexistence among nations.” On Tuesday, the Israel Defense Forces said it had carried out strikes in Doha targeting senior officials of Palestinian movement Hamas. Eyewitnesses told RIA Novosti that several explosions occurred in the center of Qatar’s capital.

An eye for an eye hands the world to the blind.

• We’ll Get Them Next Time – Israeli Envoy Rues Hamas-Qatar Strike Failure (RT)

Israel is determined to kill Hamas leaders wherever they reside and will continue its efforts until they are all dead, Israeli Ambassador to the United States Yechiel Leiter told Fox News on Tuesday. Earlier in the day, Israeli airstrikes hit a residential building in Doha, Qatar, targeting senior figures of Hamas’ political wing. The group said its officials survived, while the attack has been criticized by the White House and condemned by Qatar. “If we didn’t get them this time, we’ll get them the next time,” Leiter said. The ambassador described Hamas as “enemies of Western civilization” and argued that Israel’s actions were reshaping the Middle East in ways “moderate” states understood and valued. “Right now, we may be subject to a little bit of criticism. They’ll get over it,” he said of the Arab countries.

US President Donald Trump said that while dismantling Hamas was a legitimate goal, striking a US ally undermined both American and Israeli interests. Leiter noted that Israel had “never had a better friend in the White House” and that Washington and West Jerusalem remained united in seeking the militant group’s destruction. Qatar, which hosts Hamas officials as part of its role as a mediator, said a Qatari security officer was among six people killed in the Israeli strike. Qatari Emir Sheikh Tamim bin Hamad al-Thani has denounced the attack as a “heinous crime” and an “act of aggression,” while Doha’s Foreign Ministry has accused Israel of “state terrorism.”

Israel has vowed to hunt down Hamas leaders, who it blames for the deadly October 2023 attack which was launched from Gaza into southern Israel. The ambassador vowed that those responsible “are not going to survive,” no matter where they are. Israel’s military response has left at least 64,000 dead in Gaza, according to local authorities. Critics have accused West Jerusalem of committing genocide by rendering the blockaded enclave uninhabitable and worsening famine conditions through restrictions on food aid.

“Get ready for Israel’s next war–Washington’s military attack on Iran. Russia and China, by leaving Iran unprotected, have invited the attack.”

• Unaccountable Israel (Paul Craig Roberts)

The Criminal State of Israel continues to initiate acts of war against states that are not at war with Israel. The most recent was an Israeli attack on a residential building in Qatar. Qatar’s Foreign Ministry accused Israel of “state terrorism.” A residential building is a place where people reside. Israel’s criminal action managed to kill six Qatari citizens, but not the Hamas leaders Israel allegedly was targeting. Israel’s ambassador to Washington, Yechiel Leiter, described Israel’s enemies as “enemies of Western civilization,” but Hamas has made no attacks on Western civilization. Leiter dismissed Israel’s critics with “they’ll get over it,” they always do. To calm the troubled waters Leiter played Israel’s US card: “Israel has never had a better friend in the White House and Washington and Israel are united in seeking the destruction of Hamas.”

Leiter summed up: “If we didn’t get them this time, we’ll get them the next time.” Qatar has joined Iran, Syria, Lebanon, Yemen, and the United States if you believe those who explain that Israel was involved in the murder of President John F. Kennedy as countries that are victims of Israel’s self-righteous aggression. Yet Israel remains protected by the US, UK, EU, and the rest of the Western world, by most of what little remains of the Arab world, and by Putin. Yet Russia is demonized for protecting Russians in the Russian areas of Ukraine from massacre by neo-Nazis. How have Ukrainian neo-Nazis, financed and supported by Washington and Israel, avoided the demonization applied to Hamas? Hamas is fighting for its own country–Palestine, which has been destroyed by Israel armed with US money, weapons, and diplomatic cover.

Currently Israel and the Zionist neoconservatives who have wormed their way into US foreign policy are pressuring President Trump–“Israel’s greatest friend”–to use nuclear weapons against Iran, a country who has done nothing to the US but nevertheless is under US sanctions and threats imposed at Israel’s insistence. The “powerful American superpower” cannot even control its own foreign policy. The blustering, threatening Trump doesn’t dare threaten Israel. Get ready for Israel’s next war–Washington’s military attack on Iran. Russia and China, by leaving Iran unprotected, have invited the attack.

Let us further compare the West’s treatment of Russia compared to its treatment of Israel. Poland has asked NATO to invoke “Article Four” against Russia for allegedly violating Poland’s air space. No attack was made on Poland. Moreover, the alleged drone incursions came from Belarus, not Russia, and Belarus warned Poland in advance that some drones had “lost their track as a result of the impact of the parties’ electronic warfare assets.” “This allowed the Polish side to respond promptly to the actions of the drones by scrambling their forces on duty,” said General Pavel Muraveiko, the chief of the general staff of Belarus. So, Poland wants Article Four invoked against Russia for a non-event, but it is anti-semitic to complain of Israel’s genocide of Palestine, both the people and the country, and Israel’s military/assassination attacks on other countries. Clearly, the future of freedom does not reside in such a corrupt Western world.

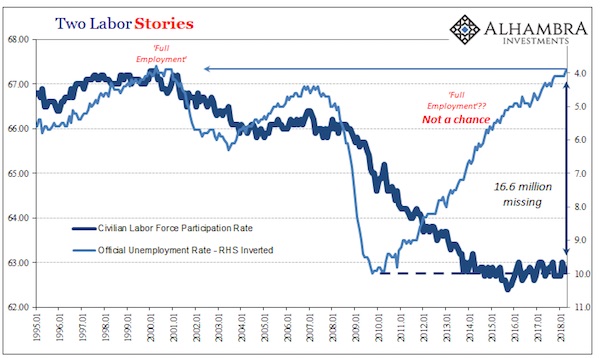

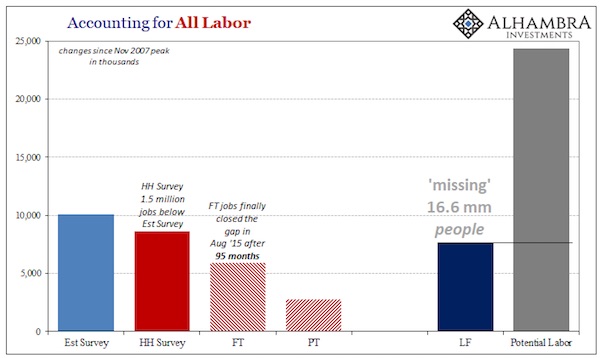

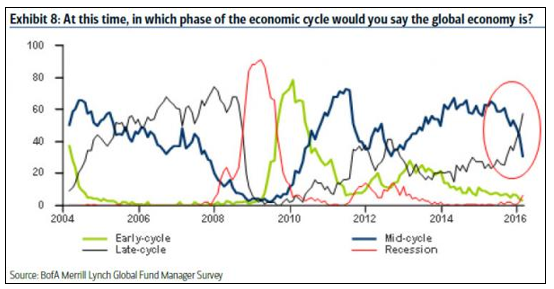

“This brings the Biden jobs overstatement to a staggering 1.5M.”

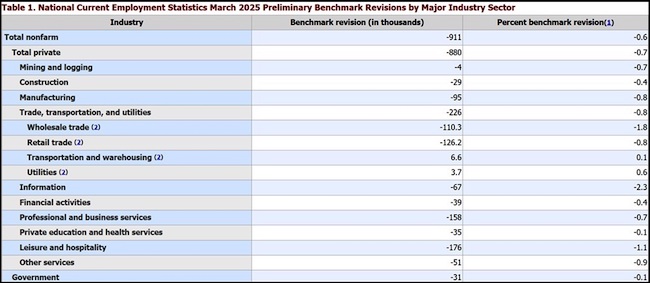

• BLS Announces 911,000 Fewer Jobs Created April ’24 through March ’25 (CTH)

Treasury Secretary Scott Bessent noted, when you add the previous Biden revision of -577,000 to the current revision of -911,000 the Bureau of Labor and Statistics (BLS) had overreported Biden’s job growth by almost 1.5 million jobs. The BLS reports today an annual revision of 911,000 fewer jobs that previously reported. These further puts President Trump’s decision to fire the head of the BLS into context.

Bessent: “Now it’s official: 2024 job gains were exaggerated by nearly 1M workers, and this is on top of an already reported 577K in downward revisions. This brings the Biden jobs overstatement to a staggering 1.5M. The truth: President Trump inherited a far worse economy than reported, and he’s right to say the Fed is choking off growth with high rates.

.@kwelkernbc pushed back last week when I warned that the BLS jobs data would show a massive downward revision.

Now it’s official: 2024 job gains were exaggerated by nearly 1M workers, and this is on top of an already reported 577K in downward revisions. This brings the Biden… pic.twitter.com/Aaz0LirOxg

— Treasury Secretary Scott Bessent (@SecScottBessent) September 9, 2025

“The numbers prove that Biden’s presidency was a failure even on its own terms.”

• Joe Biden’s Economy Was So Much Worse Than We Thought (Margolis)

For four years, Joe Biden bragged about presiding over the “strongest economy in history.” He propped up his narrative with the return of jobs after the COVID shutdowns and falsely claimed his policies created them. Even liberal outlets admitted he was padding the numbers, but Biden never stopped repeating the lie. Now the lie has officially collapsed. The Bureau of Labor Statistics just confirmed what President Trump has been saying all along: Biden’s “strong economy” was nothing but smoke and mirrors. On Monday, the BLS issued the largest downward revision in its history, wiping out nearly a million jobs — 911,000 to be exact. That’s not a minor correction; that’s proof Biden’s economic record wasn’t just exaggerated, but was a fraud from the start.

“Today, the BLS released the largest downward revision on record proving that President Trump was right: Biden’s economy was a disaster and the BLS is broken,” White House Press Secretary Karoline Leavitt said in a statement. She continued, “This is exactly why we need new leadership to restore trust and confidence in the BLS’s data on behalf of the financial markets, businesses, policymakers, and families that rely on this data to make major decisions.” She’s exactly right. This revelation comes just over a month after President Donald Trump fired Bureau of Labor Statistics Commissioner Erika McEntarfer, a Biden appointee.

“I was just informed that our Country’s ‘Jobs Numbers’ are being produced by a Biden Appointee, Dr. Erika McEntarfer, the Commissioner of Labor Statistics, who faked the Jobs Numbers before the Election to try and boost Kamala’s chances of Victory,” Trump wrote in a post on Truth Social last month. “We need accurate Jobs Numbers. I have directed my Team to fire this Biden Political Appointee, IMMEDIATELY. She will be replaced with someone much more competent and qualified.” Many on the left claimed that action was in response to a weaker than expected jobs report, but this revelation should prove beyond a reasonable doubt that the BLS under McEntarfer had clearly become politicized, with grossly inflated jobs numbers designed to boost Biden before the 2024 election.

But the scandal goes much deeper than that. Think about how many Americans made financial choices, how many businesses planned investments, and how many policymakers made decisions based on jobs data that now turns out to have been flat-out wrong. And it’s not just one bad revision. The BLS admitted they had overstated Biden’s “job creation” by about 1.5 million. That’s no small mistake. In fact, that’s not a mistake at all. That’s actively misleading the public, and that’s why firing McEntarfer was the right move, and why Trump’s nominee to replace her, E.J. Antoni, must be confirmed. The numbers prove that Biden’s presidency was a failure even on its own terms. He flooded the labor market with illegal immigrants, pumped out trillions in reckless spending, and handed out subsidies like candy.

Even then, he couldn’t match the jobs growth from Trump’s first term. That is nothing short of humiliating. For years, the media parroted Biden’s talking point that he “created more jobs than any president in history.” Now we know the truth: those jobs were fake, inflated, or outright imaginary. Biden built his presidency on a lie, and now the lie has collapsed. The so-called “historic job growth” was never real—it was a mirage propped up by partisan bureaucrats and repeated endlessly by a complicit media desperate to protect him. Meanwhile, Trump’s warnings about Biden’s phony numbers turned out to be exactly right, just as they were about inflation, gas prices, and the border. The revision is a complete repudiation of Biden’s entire economic narrative.

Shale. oil and gas. And gold.

• Maduro Suggests Reason Behind Us Military Buildup Around Venezuela (RT)

Washington is seeking to gain access to Venezuela’s natural resources, the Latin American nation’s President Nicolas Maduro has told RT in response to the arrival of US warships off the country’s coast in recent weeks. He dismissed Washington’s claims that it had mounted the effort to combat drug traffickers as a ruse. Last month, the US deployed at least eight Navy vessels and an attack submarine to the region, with an estimated 4,000 troops involved in the operation. Appearing on RT Spanish’s ‘Talking with Correa’ show on Tuesday, Maduro claimed that the US operation “is not about drug trafficking… they need oil [and] gas.”

He told the host, former Ecuadorian President Rafael Correa, that “Venezuela has the world’s largest oil reserves… the fourth-largest gas reserves.” He also noted that his country potentially boasts the “world’s largest gold reserves.” He lamented that Washington’s “aggression” against Caracas has surpassed anything seen in the region since the 1962 Cuban missile crisis. According to Maduro, these actions toward Venezuela fit into a broader “war plan,” which is supposedly aimed at subjugating the entire world to the will of the US. “But it is impossible… We already have a multipolar world with new power centers,” such as China, Russia and India, the official argued.

Maduro dismissed US allegations that Venezuela is a major drug-producing and trafficking hub. He insisted that Venezuela has eliminated all major drug-trafficking operations on its soil, and vanquished prominent gangs, including the Tren de Aragua. Relations between the two nations have been tense for years. Washington refused to recognize Maduro’s reelection in 2018, instead backing the Venezuelan opposition and imposing sweeping sanctions on the country. Last week, Russian Foreign Ministry spokeswoman Maria Zakharova warned that the “situation is… being unacceptably escalated” around Venezuela, with potentially far-reaching ramifications for regional and global security.

No, Frank and countless others. Trump never called the victims’ testimonnies a hoax, of course he didn’t, he’s neither stupid nor insensitive. He called the way in which the Dems presented the story a hoax.

• Melania, Please Talk to Donald About Epstein (Frank Miele)

Last Wednesday, an extraordinary press conference was held in the shadow of the U.S. Capitol by victims of sexual abuser Jeffrey Epstein. Anyone who watched these women pour out their hearts to demand justice for themselves and other victims could not help but be moved. Unfortunately, President Donald Trump did not watch, and then – almost simultaneously – dismissed the women’s heartfelt pleas for a public reckoning of Epstein’s abuse as “a Democrat hoax.” No doubt, Trump is a rhetorical genius who has been able to define issues to his own benefit for years, but this was a low point in his presidency. Much as it is understandable that Trump perceives the attention being given to Epstein’s life and mysterious death in a federal prison as a distraction, that must be weighed against the human toll that Epstein took.

Calling it a hoax belittles the pain and suffering of women who were victims of, at worst, rape and, at best, sexual abuse. And though Trump judged the women before he had even had a chance to hear them speak, they had already rejected his label: “This is not a hoax. It’s not going to go away,” said Marina Lacerda, who was a witness in Epstein’s 2019 indictment that led to his imprisonment and death. Abuse survivor Haley Robson, who introduced herself as a registered Republican, invited the president to meet her “in person so you can understand this is not a hoax. We are real human beings. This is real trauma.” After the president made his dismissive remarks, Republican Congresswoman Marjorie Taylor Greene called Trump to ask him to meet with the women at the Oval Office, but he did not accept – as of yet.

“It’s not a hoax,” Greene explained, “because Jeffrey Epstein is a convicted pedophile. That takes away the whole hoax thing. It’s not a hoax. It’s not a lie.” Greene challenged Trump to get past the political suspicions he has expressed. “I want him to be the hero and champion of this issue. And I want him to fight for these women, because I know him to be a fighter.” Indeed, President Trump has repeatedly shown a capacity for empathy in his capacity as a private individual and as president, most notably when he promised justice for the Angel Moms who had lost children as a result of the actions of illegal aliens. But in this case, Trump has conflated how his political enemies may seize upon the Epstein case as a weapon with the entirely unrelated issue of justice for the victims.

Speaking out about a “Democratic hoax” before he had ever seen the victims’ statements, or heard their perfectly reasonable demands, could prove to be one of the worst mistakes in Trump’s career, political or otherwise. It is not enough to know the names of Epstein and his procurer Ghislaine Maxwell; common decency demands that the names of all those who abetted them in abusing women be revealed. If there were powerful men in finance or politics who exploited these women, their names should be known too. And what about the officials who looked the other way? I don’t believe Trump has any culpability for his friendship with Epstein years ago. At the press conference, the women survivors said none of them knew of any evidence against Trump. But the president’s political opponents will surely seize upon his unwillingness to ensure justice for the Epstein victims, and plant seeds of doubt that could harm him and the nation – just exactly what Trump says he wants to avoid.

In order to avoid that fate, there is perhaps one person – and one person only – who could convince the president not to view the matter through a partisan lens. That, of course, is first lady Melania Trump. Melania’s willingness to lobby for generosity of spirit was recently apparent in the letter she wrote to Russian president Vladimir Putin when he and her husband met in Alaska to discuss the Ukraine war. Although Putin has been intransigent on the possibility of a ceasefire in the war he started, Melania urged him to think about the millions of children impacted by the bloodshed and to “nurture the next generation’s hope.” A simple yet profound concept, Mr. Putin, as I am sure you agree, is that each generation’s descendants begin their lives with a purity – an innocence which stands above geography, government, and ideology. … In protecting the innocence of these children, you will do more than serve Russia alone – you serve humanity itself. Such a bold idea transcends all human division, and you, Mr. Putin, are fit to implement this vision with a stroke of the pen today. It is time.

Just as Melania called upon Putin to protect the innocence of the children of war, so too she could – and should – call on her husband to honor the lost innocence of Epstein’s victims.

She probably doesn’t need to write a letter to Trump, but since they share a residence at 1600 Pennsylvania Avenue, it would make perfect sense for her to call him aside one night and sit him down for “the discussion.” The short version would go something like this: “Donald, you have enemies. We both know it. But sometimes your worst enemy is yourself. We both know that too. So I’m going to give you some advice. When women are young and pretty, rich and powerful men take advantage of them. That’s not a Democrat hoax. It’s a fact of life. Please watch these women, or better yet, meet with them. Find out what they want, and then help them get it. They don’t deserve shame because of what happened to them. They deserve our thanks for coming forward. They aren’t trying to hurt you; they are trying to help themselves and other women to make sure that powerful men are held accountable. It is time.”

Autism

https://twitter.com/liz_churchill10/status/1965583932549927385

RFK

https://twitter.com/VigilantFox/status/1965510416836038916

In a shocking exposé, Robert F. Kennedy Jr. details an alleged decades-long campaign by the World Health Organization (WHO) to covertly sterilize populations across the globe. Citing a specific program in Kenya, RFK Jr. claims the WHO, with influence from the Gates Foundation,… pic.twitter.com/JQ16fkm3ve

— Camus (@newstart_2024) September 9, 2025

https://twitter.com/MAGAVoice/status/1965498764992676036

Tulsi Obama

https://twitter.com/Real_RobN/status/1965469191563284869

mRNA

This is stunning. Dr Jake Scott goes dead silent.

[@SenRonJohnson]: "Do you not know?"

Senator Ron Johnson has to walk Dr Jake Scott through how mRNA vaccines work, because he doesn't have a clear understanding of the mechanism's of the technology and still thinks it… pic.twitter.com/cmLDujOLrQ

— Humanspective (@Humanspective) September 9, 2025

Ford

https://twitter.com/NicHulscher/status/1965492776998682759

A MUST WATCH!

Aaron Siri just revealed that a vaccinated vs. unvaccinated study from Henry Ford Medical Center was buried because it showed unvaccinated children were healthier.

“Del Bigtree and I met with Dr. Marcus Zervos, head of infectious disease at Henry Ford Medical… pic.twitter.com/ptXRqOSbeN

— End Tribalism in Politics (@EndTribalism) September 9, 2025

Insulation

Thermal footage from 83°N reveals polar bears’ extreme insulation: heat escapes only from the snout and eyespic.twitter.com/qJtkHnjQTW

— Massimo (@Rainmaker1973) September 9, 2025

Malone

Dr. Robert Malone explains how Covid was "the most massive… globally co-ordinated propaganda campaign in the history of the Western world".

"Western governments, non-governmental organisations, transnational organisations, pharmaceutical industry corporations, media and… pic.twitter.com/JQAAt0dERd

— Wide Awake Media (@wideawake_media) September 10, 2025

Siri

https://twitter.com/TheChiefNerd/status/1965543653319004590

Stare off

https://twitter.com/buitengebieden/status/1965496058529939748

Tucker

https://twitter.com/wideawake_media/status/1965801981735502145

https://twitter.com/naturelife_ok/status/1965766187624841307

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.