Ben Shahn Quick lunch stand in Plain City, Ohio 1938

Is COVID19 topping out in China? It’s possible, but they want it too much, and they’ve played loose with the numbers a lot. Strangest thing is perhaps that despite a cavernous drop in manufacturing PMI, a rise in freight train cargo is reported for February.

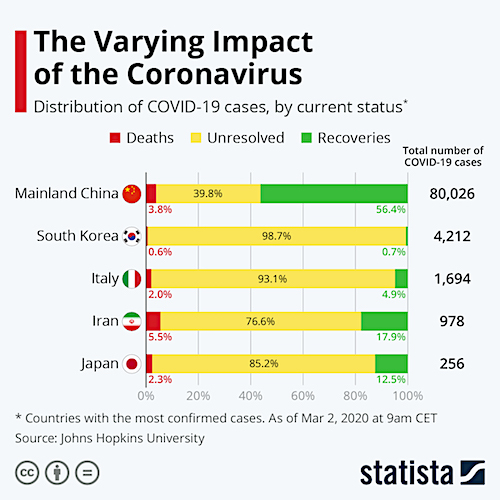

Most interesting these days, I find, are Italy, South Korea, Iran, which are in their exponential rise phases, and other countries (US?) that may soon follow suit. As I said yesterday: “Italy: only 10 days ago, on Feb 22, when S. Korea cases jumped to 156(!) [now 5,186], Italy first became a thing with 30 cases and 2 deaths. 2,000 cases now, 52 deaths and a 2.5% death rate.”

That Italy has exported the virus to as many as 24 countries also gives me pause for thought. So for now I’ll keep the usual numbers and graphs coming.

But in the run-up to Stupid Tuesday I can also finally pay some attention to the Dems, now that the DNC power grab has become so blatantly obvious.

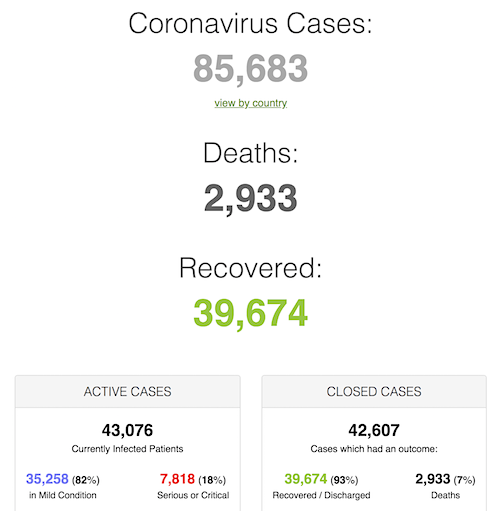

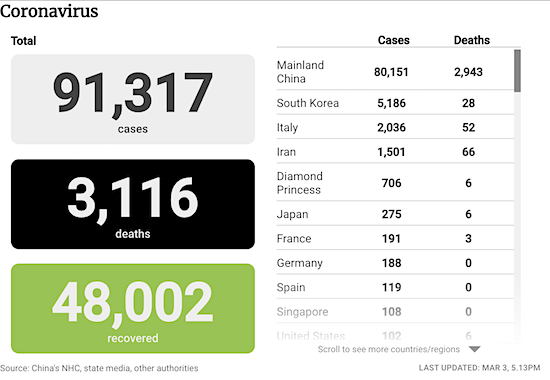

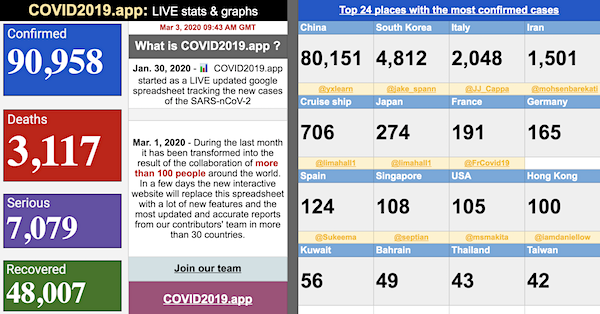

• Cases 91,317 (+ 2,069 from yesterday’s 89,248, when gain was 1,616)

• Deaths 3,120 (+ 62 from yesterday’s 3,058)

• Hubei 114 new cases, 31 new deaths – Total 67,217 cases, 2,834 deaths.

• South Korea 851 new cases, total 5,186, 34 deaths

• Italy 346 new cases, total 2,048, 52 deaths

• Iran 523 new cases, total 1,501, 66 deaths

• France 191 (from 130 yesterday), 3 deaths

• US 103 cases, 6 deaths

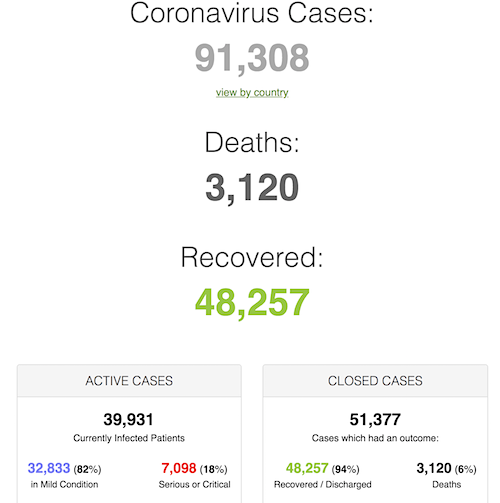

From SCMP:

From Worldometer (Note: mortality rate at 6%):

From COVID2019.app:

This article is a few days old, but I like the idea. Original title was “Italy Has Exported 24 Cases Of Coronavirus To 14 Countries”, but time won’t stand still.

A list I picked up on Twitter of countries linking infections to Italy: China, Holland, Denmark, Nigeria, US (GA, NH, MA), Iceland, UK, Croatia, Israel, Romania, Spain, Austria, Algeria, Brazil, Finland, Switzerland, Macedonia, Greece, Estonia, Sweden, France, Germany, Lithuania, San Marino.

• Italy Has Exported Cases Of Coronavirus To 24 Countries – WHO (TMZNaija)

The World Health Organization (WHO) has revealed that Italy has exported 24 cases of coronavirus to 14 countries. The global health body also revealed that 97 cases have been exported from Iran to 11 countries. In his opening remarks at the media briefing on COVID-19 – on Friday, 28 February 2020, WHO’s Director-General, Tedros Adhanom Ghebreyesus, stated that in the past 24 hours, China reported 329 cases – the lowest in more than a month. Ghebreyesus who reeled out figures regarding the spread of the virus said that as of 6am Geneva time this morning, China reported a total of 78,959 cases of COVID-19 to WHO, including 2791 deaths. “Outside China, there are now 4351 cases in 49 countries and 67 deaths.

“Since yesterday, Denmark, Estonia, Lithuania, Netherlands, and Nigeria have all reported their first cases. All these cases have links to Italy,” Ghebreyesus told newsmen. The Director-General also said that the continued increase in the number of cases, and the number of affected countries over the last few days, are clearly of concern. He, however, noted that WHO’s epidemiologists have been monitoring these developments continuously, and have now increased its assessment of the risk of spread and the risk of the impact of COVID-19 to very high at a global level.

“What we see at the moment are linked epidemics of COVID-19 in several countries, but most cases can still be traced to known contacts or clusters of cases. We do not see evidence as yet that the virus is spreading freely in communities. “As long as that’s the case, we still have a chance of containing this virus, if robust action is taken to detect cases early, isolate and care for patients and trace contacts. “As I said yesterday, there are different scenarios in different countries and different scenarios within the same country,” Ghebreyesus said.. According to him, the key to containing this virus is to break the chains of transmission. Meanwhile, according to BBC, not less than 210 people has died from coronavirus disease in Iran.

This is what’s going on in Iran amid #coronavirus outbreak. Reminiscent of early days of COVID19 epidemic in China. My friend, a journalist from Iran just translated this video and confirmed the authenticity, I’ll post it shortly. (Video by @HeshmatAlavi)

pic.twitter.com/dV9pi3b526— Max Howroute▫️ (@howroute) March 3, 2020

An index of smaller companies than the Beijing one covers.

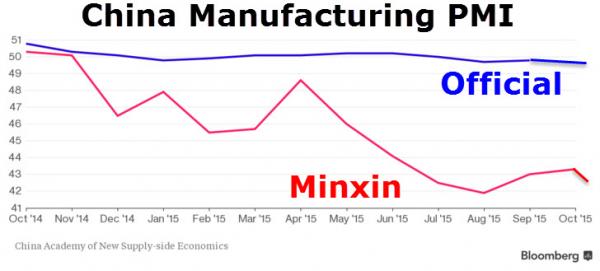

• China Manufacturing Collapse Confirmed By Private Sector Factory Survey (SCMP)

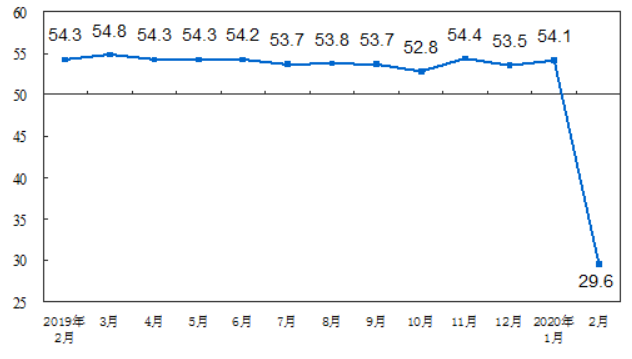

A collapse in China’s manufacturing sector in February was confirmed on Monday, with a new survey of privately-owned producers emphasising the economic damage caused by the coronavirus epidemic. The Caixin/Markit manufacturing purchasing managers’ Index (PMI), a gauge of sentiment among the country’s smaller factory operators, plunged to 40.3 in February from 51.1 in January. The weak data will reinforce expectations that China could report negative growth in the first quarter of 2020 for the first time since the Cultural Revolution in the late-1960s and early-1970s. It will also renew calls for Beijing to take more aggressive steps to support the economy.

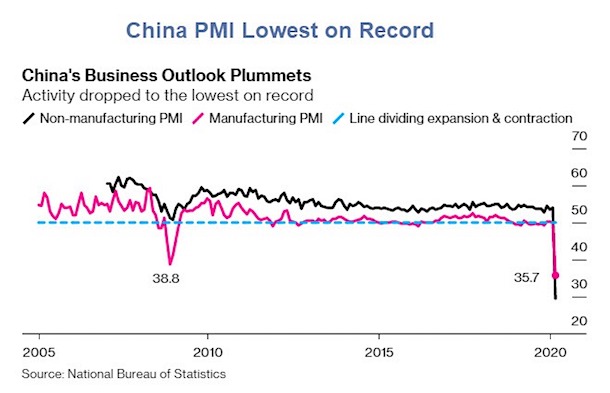

The survey was well below market expectations for a drop to 46.0 and marks the lowest reading since the survey began in April 2004. It was weaker than 40.9 in November 2008 amid the global financial crisis. The Caixin index follows Saturday’s release of the official manufacturing PMI, which crashed to a record low of 35.7 in February, below the previous trough of 38.8 reached in November 2008 at the start of the global financial crisis, the National Bureau of Statistics said. The survey for the official gauge covers more larger and state-owned firms, while the Caixin survey covers smaller firms. A reading below 50 means activity in the manufacturing sector is contracting. The further below 50 the index falls, the larger the contraction.

#Apple to be hard hit by #COVID19:

-At Shanghai's Changshuo plant, which delivers 40% of #iphone handsets, only 10,000 workers or 1/4 of the workforce have come back at the production line.

–#Foxconn's Zhengzhou plant is short of 50,000 workers, or 22% of the plant's capacity pic.twitter.com/HOzmmAWP1t— Global Times (@globaltimesnews) March 3, 2020

Was this coordinated with Xi?

• China Reports Surprising Rail Freight Growth In February (SCMP)

China’s official railway operator has said that rail freight rose in February, despite the coronavirus outbreak forcing large parts of the country into lockdown, and the official purchasing managers’ indices for manufacturing and services tumbling to all-time lows. China Railway, the state-owned railway operator, said in a statement on Sunday that total railway freight amounted to 310 million tonnes in February, a rise of 4.5 per cent from a year earlier, just a day after the National Bureau of Statistics (NBS) announced that China’s factory and service sector activity sunk into deep contraction.

The supplier delivery time sub-index in China’s manufacturing purchasing managers’ index (PMI), which measures logistics efficiency by railway, road and air for factories, dropped to 32.1 in February, a sign that raw material supplies to the manufacturing sector were at record lows last month, the NBS said. China Railway, meanwhile, said that China loaded 171,000 railway cars per day on average last month, a daily increase of 4,945 from a year earlier. Container freight on railways surged 39.5 per cent to 26.61 million tonnes, it added, in an surprisingly stable account of China’s rail freight network. In the January-February period, China’s freight cargo rose by 0.6 per cent to 670 million tonnes, an all-time high, according to China Railway.

Steve’s elaborate write-up of things to do.

• A Modern Jubilee As A Cure To Financial Ills Of Coronavirus (Steve Keen)

Extraordinary measures are needed now to stop the health effects of the Coronavirus triggering a financial crisis that could in turn make the Coronavirus worse. All of these actions can be undertaken by Central Banks and financial regulators, once they have been given permission by governments. Two of these measures are already being undertaken by some Central Banks:

• A per capita payment to all citizens so that renters can pay the rent, mortgagors can service their mortgages, and workers, whether unemployed or not, can buy food and other critical goods. This can be financed as Quantitative Easing was financed, without recourse to the Treasury, or taxation (Hong Kong has already done this);

• Normal bankruptcy rules for companies and especially banks should be suspended, to allow them to continue operating despite falling into negative equity if revenues fall sharply and share prices plunge; and

• Central Banks should buy shares directly to support share prices, rather than simply buying bonds under Quantitative Easing, to prevent a stock market collapse undermining both business and banks (Japan’s Central Bank is already doing this, though for other reasons).

Argument – There is no doubting now that the Coronavirus is a pandemic. This is the first one we have experienced since the “Spanish Flu”, which lasted from January 1918 till December 1920. Other recent serious diseases have had much lower levels of transmissibility. This is the first disease to compare to the Spanish Flu in terms of both transmissibility and virulence. Europe was embroiled in World War I at the outbreak of the Spanish Flu. Its health and population impacts were huge: estimates of the death toll vary between 40 and 100 million in a global population of 1.8 to 1.9 billion.

Here I want to focus on its financial effects. They were mild, because the great financial crisis of the 20th century, the Great Depression, lay ten years in the future. Disruptions to life were extreme, but disruptions to the economy were relatively small, and it was a war economy anyway for much of the world. This meant there was guaranteed employment and wages for military personnel, rationing for the general public, and other wartime measures. All these things limited the financial contagion from the medical contagion. Crucially, private debt was a mere 55% of US GDP when the flu outbreak began. The private sector was relatively robust.

“Is there anything you can think of over at the Wal Mart or the Walgreens that isn’t made in China?”

• This Ain’t No Fooling’ Around (Kunstler)

Is there anything you can think of over at the Wal Mart or the Walgreens that isn’t made in China? I mean, everything from a dustpan to a lint brush? I can’t say for sure, because I’m not over in China, but the place is apparently not open for business these days. One must surmise that a lot of activities in the USA may not be open for business much longer, either. The action in my local supermarket yesterday had an undercurrent of stealth desperation; no overt panic buying, no fighting in the aisles, but an edge of suspense. Personally, I cleaned out an entire product-line of cat food, loaded up on cooking oil, rice, dry beans, and evaporated milk — and I wasn’t the only one checking out with the sixteen-roll bindle of toilet paper.

Obviously, many products were still there on the shelves to get (minus that cat food). Is the time perhaps at hand when a lot of stuff won’t be? Just sayin’. The message is getting out — though not from US authorities yet — that everybody may soon be spending a lot of time home alone. That’s exactly what has happened in China and a region of northern Italy. France banned events with more than 5,000 people (why that number, exactly?). Japan has canceled school for the time being — duration unknown for now. So a USA lockdown is not merely hypothetical. These, then, are two fundamental conditions the world faces for a while: nobody moves and nothing gets produced.

Are we taking this thing too seriously (some might ask)? I don’t pretend to know the answer, except, again, to point to China and think that they can’t possibly just be fooling around with all those zombified cities and shuttered factories. The next question might be: will the global economy return at some point to “normal” operating conditions, that is, the fabulously complex network of supply lines, markets, and payment arrangements as they worked up until January 2020? I am for sure not sure about that. Once a gigantic and fantastically precise mechanism breaks, I doubt it comes back together neatly and quickly. In the physical universe, the power of emergence is like the cue ball on a billiard table, and it appears that all the rest of the colored balls will be bouncing off the bumpers and sinking into pockets for while… and eventually the global table will look a lot different.

Stupid Tuesday.

• Tucker Carlson On Democrats: ‘They’re Pushing A Defective Product’ (Fox)

Tucker Carlson mocked those pushing and supporting former Vice President Joe Biden Monday, in particular those who think he’s the candidate to stop the nomination of Vermont Senator Bernie Sanders. “And tonight, they have found their war horse, a hero they imagine will carry them forth to victory against the wild-haired infidel from Vermont. It is this candidate whom you should know is literally now the youngest man in the Democratic race,” Carlson said on “Tucker Carlson Tonight.” “This is the man they believe has the competence, the intensity, the intellect to repel the seething horde of Sanders-ites. Ladies and gentlemen, Mr. Joe Biden.” Carlson played a montage of clips showing Biden fumble on the campaign. The host then chastised those pushing Biden to continue running, calling it “cruel.”

“Running Joe Biden for president is like making your dog wear a dress,” Carlson deadpanned. “It may make for an amusing Instagram post, but it’s wrong. You can see the confusion in the dog’s eyes.” The host ripped former Democratic presidential candidates Pete Buttigieg and Amy Klobuchar, among others, for endorsing Biden who he referred to as a “defective product.” “Today, both Pete Buttigieg and Amy Klobuchar endorsed Biden. So did former Senate Majority Leader Harry Reid and Beto O’Rourke,” Carlson said. “These are party people doing the bidding of their corporate masters. There’s nothing warm or sentimental about it. They’re pushing a defective product on consumers and they know it. They’re selling lawn darts.”

Carlson believes the threat from Sanders is about “institutional control.” “The Biden campaign isn’t about ideas, much less ideals. The Democratic establishment’s only concern is institutional control,” Carlson said. “That’s where all of their power comes from. From holding together and running things. If the Democratic coalition breaks down, they are by definition powerless.” “They have nothing. And the real threat of Bernie Sanders is the threat he poses to the party. He could split it in half and break it forever,” Carlson added. “That cannot happen. Joe Biden is their last chance. That’s why they’re backing him.”

If they fail to stop his candidacy, what other tricks are up their sleeves?

• What Could Divide The Democrats More Than Conspiring To Stop Bernie? (Tracey)

Perhaps the intense wave of establishment Democratic party consolidation around Joe Biden over the past 48 hours isn’t a concerted conspiracy — no smoke-filled rooms, no corrupt deals, no villainous blackmail schemes. But the Democratic party establishment (which we’re often told does not exist) is clearly making every effort to give the appearance of something conspiratorial going on. Take yesterday, for instance. Pete Buttigieg meets for breakfast with 95-year-old Jimmy Carter (?), ensures the visit is well-publicized, then heads home to South Bend and pulls the rug out from under his campaign. Wait, what? Is this the same Pete Buttigieg whose aides just a few days earlier released an elaborate memo detailing his surefire path to a formidable delegate acquisition?

Yet suddenly his Super Tuesday plans are scrapped, and the thousands of early votes already cast for him in California and elsewhere are effectively nullified. We’re all supposed to pretend this is normal behavior? Because it seems a bit sociopathic. I personally would never have voted for Pete. Nor would I have voted for Amy Klobuchar, who pulled the same 11th-hour dropout stunt today. But part of me still finds it disgraceful that these candidates would gut-punch their staff, volunteers, supporters, and voters in such a manner — hours before a major national election they’d been working toward for a full year — after both candidates gave every indication that they were going to actively contest. Instead of patting themselves on the back, shouldn’t Amy and Pete be begging for forgiveness, especially from those who already voted for them in Super Tuesday states — as it turns out, on false pretenses?

Beto 9 months ago:

“We cannot return to the past. We cannot simply be about defeating Donald Trump,” Beto O’Rourke tells @Morning_Joe.@WillieGeist: “So, is Joe Biden a return to the past?”

O’Rourke: “He is.” pic.twitter.com/NHIrznMwUs

— MSNBC (@MSNBC) June 13, 2019

John Solomon is back again.

• Ukraine Court Throws Wrench Into Joe Biden’s 2020 Election Plans (Solomon)

A Ukrainian court has ordered an investigation into whether Joe Biden violated any laws when he forced the March 2016 firing of the country’s chief prosecutor. The ruling could revive scrutiny of Hunter Biden’s lucrative relationship with an energy firm in that corruption-plagued country just as the former vice president’s campaign for the Democratic presidential nomination is surging after a lackluster start. Former Prosecutor General Viktor Shokin, who has long alleged he was fired because he would not stop investigating the Burisma Holdings firm that employed Hunter Biden, secured the ruling last month. Ukrainian officials confirmed the State Bureau of Investigation has since complied and initiated the probe.

The Pecherskyi District Court of Kyiv ruled last month that Shokin’s lawyers had provided sufficient evidence to warrant a probe and “obliged the authorized officials of the State Bureau of Investigation” to accept the ex-prosecutor’s complaint and “start pre-trial investigation of the reported data,” according to an official English translation of the ruling provided by Shokin’s attorney. The ruling does not mention Biden by name, but court filings by Shokin’s lawyers that led to the decision show that the former prosecutor had alleged “the commission of a criminal offense against him by Joseph Biden, a citizen of the United States of America, in Ukraine and abroad: interference in the activities of a law enforcement officer.”

[..] Joe Biden and his defenders have denied any wrongdoing, saying the vice president sought Shokin’s firing because the prosecutor was ineffective in fighting corruption. His supporters have also claimed that the Burisma investigation was dormant at the time Shokin was fired and therefore not a high priority. But evidence has emerged in recent weeks that the probe into Burisma, in fact, was heating up when Shokin was fired in spring 2016. The prosecutor’s office had secured a ruling re-seizing assets of Burisma’s owner in early February 2016, and the Latvian government acknowledges it sent a warning to Ukraine officials that same month flagging several Burisma transactions, including payments to Hunter Biden, as “suspicious.”

A tale in 2 headlines:

"Sanders Doubles Lead Over Biden Among Texas Hispanic Voters, Poll Shows" @Newsweek, Mar 1st

"Texas closes hundreds of polling sites, making it harder for minorities to vote" @guardiannews, Mar 2nd

— Lee Camp [Redacted] (@LeeCamp) March 2, 2020

“..the Justice Department inexplicably still takes the position that the court should close discovery and rule on dispositive motions. The Court is especially troubled by this.”

• Hillary Clinton Ordered To Give Sworn Deposition On Email Server, Benghazi (ZH)

Hillary Clinton has been ordered to give a sworn deposition to Judicial Watch regarding her emails and documents related to the attack on the US consulate in Benghazi, Libya while she was Secretary of State. The ruling is in response to the conservative legal group’s lawsuit, “Judicial Watch v. U.S. Department of State” – specifically regarding “talking points or updates on the Benghazi attack.” “Judicial Watch famously uncovered in 2014 that the “talking points” that provided the basis for Susan Rice’s false statements were created by the Obama White House. This Freedom of Information Act (FOIA) lawsuit led directly to the disclosure of the Clinton email system in 2015.” -Judicial Watch

Discovery in the case began in December, 2018, when Judge Royce C. Lamberth allowed Judicial Watch to explore whether Clinton’s use of a private email server was intended to circumvent the Freedom of Information Act (FOIA). JW also sought to determine: “whether the State Department’s intent to settle this case in late 2014 and early 2015 amounted to bad faith; and whether the State Department has adequately searched for records responsive to Judicial Watch’s request.” “The court also authorized discovery into whether the Benghazi controversy motivated the cover-up of Clinton’s email. The court ruled that the Clinton email system was “one of the gravest modern offenses to government transparency.” The State and Justice Departments continued to defend Clinton’s and the agency’s email conduct.” -Judicial Watch

On Monday, Judge Lamberth overruled Clinton and the State Department’s objections to limited additional discovery, writing “Discovery up until this point has brought to light a noteworthy amount of relevant information, but Judicial Watch requests an additional round of discovery, and understandably so. With each passing round of discovery, the Court is left with more questions than answers.” Lamberth also said that he is troubled by the fact that both Clinton and the State Department want discovery to end.

“[T]here is still more to learn. Even though many important questions remain unanswered, the Justice Department inexplicably still takes the position that the court should close discovery and rule on dispositive motions. The Court is especially troubled by this. To argue that the Court now has enough information to determine whether State conducted an adequate search is preposterous, especially when considering State’s deficient representations regarding the existence of additional Clinton emails. Instead, the Court will authorize a new round of discovery “-Judge Lamberth

Erdogan told Bulgarian PM he doesn’t want to talk to Greek PM, and won’t send any refugees to Bulgaria (a few km away from Greek-Turkish border)

• Erdogan’s Use Of Refugees To Pressure EU Is ‘Unacceptable’ – Merkel (RT)

German Chancellor Angela Merkel has called Turkey’s decision to release thousands of migrants toward the EU “unacceptable,” and accused Turkish President Recep Tayyip Erdogan of pressuring the EU “on the back of the refugees.”Turkey allowed thousands of migrants to leave its territory over the weekend, accusing EU leaders of failing to back its plans for a Turkish-controlled ‘safe zone’ inside Syrian territory. With Turkish forces engaged in open warfare with the Syrian government in Idlib, Erdogan opened the floodgates to Europe, in a move seemingly designed to put pressure on his NATO allies to back his Syrian offensive.

“I understand that Turkey is facing a very big challenge regarding Idlib,” Merkel told reporters on Tuesday. “Still, for me it’s unacceptable that he – President Erdogan and his government – are not expressing this dissatisfaction in a dialogue with us as the European Union, but rather on the back of the refugees. For me, that’s not the way to go forward.”

Already, Greek authorities have struggled to hold back the human wave that has crashed upon its border with Turkey. “This is an invasion,” Development Minister Adonis Georgiadis told Skai TV on Monday, as police fired tear gas at migrants attempting to storm the border fence, and as the Greek coast guard tried to stop dinghies full of refugees from landing on the country’s southern islands. Though criticized for her “open door” migration policy during the 2015 migrant crisis, Merkel has since attempted to reduce the influx. However, despite promising Erdogan additional aid in January in exchange for holding more than 3 million migrants on Turkish soil, Merkel refused to support her Turkish counterpart’s military operation in northern Syria, prompting Erdogan to follow through last weekend on his long-standing threat to release the migrants into Europe.

Stories about Greek guards killing refugee(s) are fake news, says Athens, spread by Erdogan.

• Greece Seeks To Fortify Borders Amid Erdogan Threats (K.)

As Turkish President Recep Tayyip Erdogan warned on Monday that soon the number of refugees crossing into Europe “will reach millions” unless the European Union takes responsibility for the crisis, Greece continued efforts to fortify its borders and diplomatic initiatives to tackle what it calls an “asymmetrical threat.” On the diplomatic front, the government’s initiatives have led to a planned visit on Tuesday to the Greek-Turkish border in Evros by the presidents of the European Commission, Council and Parliament – Ursula von der Leyen, Charles Michel and David Sassoli – accompanied by Prime Minister Kyriakos Mitsotakis. Even though Athens believes the visits send a powerful message, it is expecting practical support from its partners, stressing that Greece’s borders with Turkey are also European.

On Sunday, Greece announced emergency measures to tackle the crisis, including a further tightening of border controls to the maximum level, a temporary one-month suspension of asylum applications and the immediate return of undocumented migrants to their country of origin. According to the International Organization for Migration (IOM), the number of refugees and migrants at the Greek border is estimated at around 13,000 people and tensions are rising as they try to push through. Tensions were also running high on the islands following the arrival over the weekend of around 1,000 refugees and migrants, with locals trying to prevent one smuggling boat from docking. A child died when one vessel capsized.

Yeah, you’re really helping.

• UN Says Greece Has No Right To Stop Accepting Asylum Requests (K.)

The United Nation’s refugee agency said on Monday that Greece had no right to stop accepting asylum applications as Athens struggled with a sudden increase of arrivals at its border of Middle East refugees and migrants from Turkey. Greek Prime Minister Kyriakos Mitsotakis said on Sunday his country would not be accepting any new asylum requests for a month after two days of clashes between border police and thousands of people seeking to enter the EU from Turkey. “It is important that the authorities refrain from any measures that might increase the suffering of vulnerable people,” UNHCR said in a statement.

“All states have a right to control their borders and manage irregular movements, but at the same time should refrain from the use of excessive or disproportionate force and maintain systems for handling asylum requests in an orderly manner.” The UN agency said neither international nor EU law provided “any legal basis for the suspension of the reception of asylum applications.” Its statement came as the EU scrambled to help Greece police the frontier and sought to put pressure on Turkey to go back to preventing refugees and migrants stranded on its territory from seeking to reach Europe.

“I am as confident as a psychiatrist can ever be that, if extradition to the United States were to become imminent, Mr Assange would find a way of suiciding.”

• The Armoured Glass Box is an Instrument of Torture (Craig Murray)

The defence was impeded by their inability to communicate confidentially with their client during proceedings. In the next stage of trial, where witnesses were being examined, timely communication was essential. Furthermore they could only talk with him through the slit in the glass within the hearing of the private company security officers who were guarding him (it was clarified they were Serco, not Group 4 as Baraitser had said the previous day), and in the presence of microphones. Baraitser became ill-tempered at this point and spoke with a real edge to her voice. “Who are those people behind you in the back row?” she asked Summers sarcastically – a question to which she very well knew the answer. Summers replied that they were part of the defence legal team.

Baraitser said that Assange could contact them if he had a point to pass on. Summers replied that there was an aisle and a low wall between the glass box and their position, and all Assange could see over the wall was the top of the back of their heads. Baraitser said she had seen Assange call out. Summers said yelling across the courtroom was neither confidential nor satisfactory. This is the photo taken illegally (not by me) of Assange in the court. If you look carefully, you can see there is a passageway and a low wooden wall between him and the back row of lawyers. You can see one of the two Serco prison officers guarding him inside the box. Baraitser said Assange could pass notes, and she had witnessed notes being passed by him. Summers replied that the court officers had now banned the passing of notes.

Baraitser said they could take this up with Serco, it was a matter for the prison authorities. Summers asserted that, contrary to Baraitser’s statement the previous day, she did indeed have jurisdiction on the matter of releasing Assange from the dock. Baraitser intervened to say that she now accepted that. Summers then said that he had produced a number of authorities to show that Baraitser had also been wrong to say that to be in custody could only mean to be in the dock. You could be in custody anywhere within the precincts of the court, or indeed outside. Baraitser became very annoyed by this and stated she had only said that delivery to the custody of the court must equal delivery to the dock. To which Summers replied memorably, now very cross “Well, that’s wrong too, and has been wrong these last eight years.”

I have been wondering why it is so essential to the British government to keep Assange in that box, unable to hear proceedings or instruct his lawyers in reaction to evidence, even when counsel for the US Government stated they had no objection to Assange sitting in the well of the court. The answer lies in the psychiatric assessment of Assange given to the court by the extremely distinguished Professor Michael Kopelman [..] : “Mr Assange shows virtually all the risk factors which researchers from Oxford have described in prisoners who either suicide or make lethal attempts. … I am as confident as a psychiatrist can ever be that, if extradition to the United States were to become imminent, Mr Assange would find a way of suiciding.”

Automatic Earth commenter/contributor Dr. John Day telling Tulsi Gabbard yesterday at a townhall in Austin, Texas that the US needs to purchase 6 billion doses of chloroquine phosphate to treat everybody (assuming a high infection rate, eventually).

If you read us, please support us. It’s the only way the Automatic Earth can survive. Donate on Paypal and Patreon.