DPC Sternwheeler Falls City, the levee, Vicksburg, Mississippi 1900

The hills are alive with the sound of too little money.

• Austria Is Fast Becoming Europe’s Latest Debt Nightmare (Telegraph)

Ah Austria, land of schnitzel, lederhosen, Mozart, alpine meadows and beer drinking. Less widely appreciated is its special place in the history of catastrophic banking crises. It was the failure of Creditanstalt, a Viennese bank founded in 1855 by Anselm von Rothschild, that arguably sparked the Great Depression, setting off an unstoppable chain reaction of bankruptcies throughout Europe and America. No-one would think that what happened last week at Austria’s failed Hypo Alpe-Adria Bank International falls into quite the same category; we are meant to be in the recovery phase of the latest global banking crisis, so this is more about re-setting the system than again bringing it to its knees, right? Well, make up your own mind. I suspect neither financial markets nor policymakers have yet caught onto the full significance of the latest turn of events.

In a nutshell, the Austrian government has had enough of funding the bank’s losses, and announced plans to “bail-in” external creditors to the tune of €7.6bn instead. As such, this marks a test case of new European rules to make creditors pay for failing banks. About time too, you might say. What took them so long? Only in this case, the bonds are notionally guaranteed by the Austrian state of Carinthia, which now theoretically becomes liable for the bail-in. It’s an echo of the mess Ireland got itself into at the height of the banking crisis, when it foolishly attempted to stem the panic by underwriting all Irish banking liabilities; the move very nearly ended up bankrupting the entire country. Hypo will bankrupt Carinthia. Essentially, what the Austrian government is doing is cutting loose an entire region, rather in the way the federal authorities in the US allowed Detroit to go bust a number of years ago.

It’s a mini-Greece going off in the heartlands of Europe. In Hypo’s case, the bail-in also threatens knock-on consequences for public bodies elsewhere, including Bayern Landesbank, a big holder of Hypo bonds which is owned by the German state of Bavaria, and the Munich based FMSW, which is again publicly underwritten. All this is just the tip of the iceberg; Europe is awash with interlinked banking and public liabilities, many of which will never be repaid and basically need to be written off. Massive creditor losses are in prospect. The European authorities had us all half convinced that Europe’s debt crisis was over. In truth, it may have barely begun.

Read more …

Good interview. Read.

• Tsipras: ‘We Don’t Want to Go on Borrowing Forever’ (Spiegel)

SPIEGEL: Mr. Prime Minister, most of your European partners are indignant. They accuse you of saying one thing in Brussels and then saying something completely different back home in Athens. Do you understand where such accusations come from?

Tsipras: We say the same things in Germany as we do in Greece. But sometimes, problems can be viewed differently, depending on the perspective. (He points to his water glass.) This glass here can be described as being half full or half empty. The reality is that it is a glass filled half-way with water.

SPIEGEL: In Brussels, you have given up your demands for a debt haircut. But back home in Athens, you continue talking about a haircut. What does that have to do with perspective?

Tsipras: At the summit meeting, I used the language of reality. I said: Prior to the bailout program, Greece had a sovereign debt that was 129% of its economic output. Now, it is 176%. No matter how you look at that, it’s not possible to service that debt. But there are different ways to solve this problem: via a debt cut, debt restructuring or bonds whose payback is tied to growth. The most important thing, though, is solving the true problem: the austerity which has driven debt way up.

SPIEGEL: Are you a linguist or a politician? You told the Greeks that you got rid of the troika and sold it as a victory. But the European Commission, the International Monetary Fund (IMF) and the European Central Bank (ECB) are still monitoring your reforms. Now, they are simply called “the institutions.”

Tsipras: No, it isn’t a question of terminology. It has to do with the core of the issue. Every country in Europe has to work together with these institutions. But that is something very different than a troika that is beholden to nobody. Its officials came to Greece to strictly monitor us. Now, we are again speaking directly with the institutions. Europe has become more democratic because of this change.

SPIEGEL: What change? You still have to submit your reform plans to three “institutions” for approval.

Tsipras: The reforms won’t be approved by the institutions. They have a say in the process and establish a framework that applies to all in Europe. Previously, the situation was such that the troika would send an email telling the Greek government what it had to do. Our planned reforms are necessary, but we are deciding on them ourselves. They aren’t being forced onto us by anyone. We want to stop large-scale tax evasion and tax fraud more than anybody. Thus far, it has only been the low earners and not the wealthy that paid. We also want to make the state more efficient.

Read more …

Lots of emptiness.

• Eurogroup To Consider Greek Reform Proposals Amid Scramble For Funding (Kath.)

Greece faces another tough Eurogroup summit Monday when a slew of reform proposals from Athens are to come under the microscope in Brussels, with the two sides apparently far from a compromise even as state coffers in Athens are close to emptying. Finance Minister Yanis Varoufakis is expected to face a barrage of questions from his eurozone counterparts on a series of proposals set out in an 11-page letter he sent to Eurogroup President Jeroen Dijsselbloem, which include the creation of a so-called fiscal council to generate budget savings, the revision of licensing for gaming and lotteries and the hiring of non-professionals, including students and tourists, as tax agents to help a foundering crackdown on tax evasion.

Sources suggested over the weekend that the proposals had met with skepticism from eurozone officials. In comments on Saturday on the sidelines of a conference in Venice, Varoufakis said he had received a response from Dijsselbloem. He added that Greece was keen to move forward with reforms but that the two sides must agree on “the process by which the reforms will be made more specific, implemented and evaluated so that they can be reviewed by the Eurogroup.” Varoufakis added that Greece’s reform program would be “discussed by technical teams that will convene shortly in Brussels.” Some eurozone officials appeared to be running out of patience. ECB governing council member Luc Coene said in an interview on Saturday that Greece must realize “there is no other way than to reform,” noting that Greeks had been sold “false promises.”

Read more …

“Perhaps the cupboards of the monetary bureaucrats are short a few plates and in need of a little pharmacological fine-tuning. Just saying.”

• The ECB’s Lunatic Full Monty Treatment (Tenebrarum)

The belief that the market economy requires “steering” by altruistic central bankers, who make decisions influencing the entire economy based on their personal epiphanies, has rarely been more pronounced than today. Most probably it has actually never been stronger. It is both highly amusing and disconcerting that so many economists who would probably almost to a man agree that it would be a very bad idea if the government were to e.g. take over the computer industry and begin designing PCs and smart phones by committee, think that government bureaucrats should determine the height of interest rates and the size of the money supply.

We know of course that central banks are the major income source for many of today’s macro-economists, so it is in their own interest not to make any impolitic noises about these central planning institutions and their activities. Besides, most Western economists have not exactly covered themselves with glory back when the old Soviet Union still existed. Even in the late 1980s, Über-Keynesian Alan Blinder for instance still remarked that the question was not whether we should follow its example and adopt socialism, but rather how much of it we should adopt. The recent ECB announcement detailing its new “QE” program once again confirms though that there is nothing even remotely “scientific” about what these planners are doing. Common sense doesn’t seem to play any discernible role either. [..]

Leaving for the moment aside how sensible it is for the bond yields of virtually insolvent governments mired in “debt trap” dynamics to trade at less than 1.3%, one must wonder: what can possibly be gained by pushing them even lower? Does this make any sense whatsoever? Meanwhile, the ECB let it be known that it wouldn’t buy any bonds with a negative yield-to-maturity exceeding 20 basis points – the level its negative deposit rate currently inhabits as well. What a relief! What makes just as little sense is that the economic outlook presented by Mr. Draghi on occasion of his press conference was actually quite upbeat. To summarize: yields are at record lows, with about €2 trillion in European government bonds sporting negative yields to maturity. The economic outlook is said to be good.

The current slightly negative HICP rate is held to be a transitory phenomenon (it very likely will be). Needless to say, the arbitrary 2% target for “price inflation” makes absolutely no sense anyway. Not a single iota of wealth can be created by pushing prices up. Last but certainly not least, year-on-year money supply growth in the euro area has soared into double digits recently. And the conclusion from all this is that the central bank needs to boost its balance sheet by €1 trillion with a massive debt monetization program? Are these people on drugs? If not, then they should perhaps see a shrink. Perhaps the cupboards of the monetary bureaucrats are short a few plates and in need of a little pharmacological fine-tuning. Just saying.

Read more …

It’s no longer useful to view this from an investor point of view.

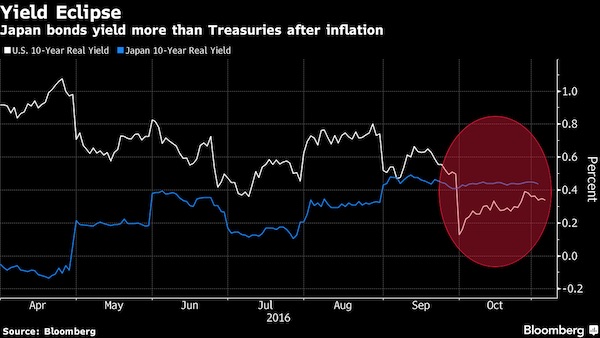

• 7 Things To Know About The ECB’s QE Game Plan (MarketWatch)

After years of discussion, months of urgent calls and weeks of preparation, the European Central Bank is about to write history—on Monday it will kick of its €1.1 trillion-euro, quantitative-easing program. Unlike its U.S., U.K. and Japanese central-bank peers, the ECB never resorted to sovereign QE at the height of the global financial crisis. Instead, it’s attempted an array of other extraordinary policy measures, including a negative deposit rate, programs to provide cheap funding to eurozone banks, and a less-powerful bond-buying program, often called “private QE,” focused on purchasing asset-backed securities and covered bonds. Now, as investors prepare for the launch of full-blown QE on March 9, here’s what we know about the program so far.

What’s the aim of the QE? Under quantitative easing, a central bank creates money electronically, which it then uses to buy securities, such as government bonds, from banks and other institutions. It’s hoped that these institutions will then use the new bank reserves to buy other assets, lowering interest rates and encouraging spending. The ECB hopes QE will revive growth and inflation in the eurozone. Despite repeated attempts to spur an economic recovery, the currency bloc is still grappling with painfully high unemployment, slow growth and negative inflation among its members.

Will the ECB buy government bonds with negative yields?Yes, but nothing that carries a yield below the ECB’s own deposit rate, which currently stands at negative 0.2%. The limit means that bonds currently yielding more than the deposit rate have room to fall further. Even before the big QE bazooka has been fired, yields for most eurozone countries have tanked. For Germany, France, Austria, Belgium, Holland and Finland borrowing costs for shorter-dated debt are now negative, meaning that bondholders essentially agree to pay issuers to hold their debt.

What will QE do to bond yields? Initially, sovereign QE and lower bond yields should march together hand in hand. As the ECB buys large quantities of government debt, bond prices should go up, which will send yields lower. On Friday, borrowing costs for Italy, Spain and Portugal dropped to record lows in anticipation of QE takeoff. However, big moves in the bond markets show much of the impact may have already been priced in. Longer-term, as the QE liquidity injection begins to work on the eurozone economy, and likely boost inflation and growth, bond yields should start to rise to reflect the stronger economy. The latest eurozone data indicate that the region may be turning a corner, leaving room for higher borrowing costs.

Read more …

London is a wasteland. It may be rich, but it’s still a wasteland. No there there.

• 30 Years Of A Polarised Economy Have Squeezed Out The Middle Class (Observer)

London has always been a city of extremes but the extent to which it has become polarised between rich and poor is laid bare in research that reveals a 43% decrease in middle-income households between 1980 and 2010. England is increasingly divided between the rich and the poor, with a 60% increase in poor households and a 33% increase in wealthy households. This has come at a time – 1980 to 2010 – when the number of middle-income households went down by 27%. But the trend is most marked in London, according to an analysis of census data by Benjamin Hennig and Danny Dorling of the School of Geography and the Environment at the University of Oxford.

Over the three decades, the capital has seen an 80% increase in poor households, an 80% increase in wealthy households – and a 43% decrease in middle households. Around 36% of London households are now classified as poor (up from 20% in 1980), while 37% are middle income (down from 65%). The largest%age point fall in households in the middle has been in Westminster, which saw its middle reduce from nearly three-quarters of all households to just one-third. The largest%age-point increase in wealthy households has been in Richmond-upon-Thames, where more than half of households are now wealthy, compared with a fifth in 1980. In contrast, in Newham, almost one in two households is now poor.

The researchers have drawn up maps of England according to wealth, described by Dorling as “fancy pie charts”. The polarising of wealth has been exacerbated in recent years, with economic growth having been slower than had been hoped, and wages in the middle failing to rise in parallel with the recovery. The economic divide between the beneficiaries of the property bubble and non-homeowners also continues to widen in the country as a whole, with upward pressure on land values. Dorling said: “This analysis shows that England is becoming more polarised, with an increase in households that are poor and those that are wealthy. The number of households in poverty has jumped by 60% since 1980, meaning that now almost three in 10 are poor.

Read more …

So more PBOC QE too?

• Foreign Banks Tighten Lending Rules For China State-Backed Firms (Reuters)

Some banks are adopting stricter lending criteria for China’s state-owned enterprises (SOEs), demanding collateral from some companies they used to deem as safe as government debt, as Beijing tries to reform its bloated firms and the economy slows. Singapore’s DBS Group, which recently suffered a loss on a bad loan to an SOE-related firm it had assessed as risk-free, plans to launch a “decision grid” to assess the creditworthiness of SOEs, according to draft internal risk guidelines reviewed by Reuters. A banker at Taiwan’s Chang Hwa Commercial Bank said that from the beginning of this year his bank would only lend to state-owned Chinese companies that provide collateral, in recognition that SOEs were no longer risk free.

Such changes in policy suggest some foreign banks are preparing for a rise in defaults in the world’s second-largest economy, which is growing at its slowest pace in a quarter of a century and where the government is trying to make the state sector more efficient.

DBS will now lend more conservatively to SOEs seen as receiving less government support, as China plans to prioritize SOEs in strategic sectors. The January-dated DBS document said: “Not all SOEs receive the same degree of government support. It is our further belief that the differentiation of such support will widen in the future as the government continues to pursue market economy.” DBS will now divide SOEs into tiers according to their likely level of government support, with subsidiaries considered more risky than top-level holding companies.

Group companies that are not consolidated into the parent SOE’s financial statements will be evaluated as an ordinary borrower, the decision grid shows. DBS effectively acknowledges that lenders can no longer take for granted implicit support from above. “Compared to ordinary corporates, implicit support obtained from the parents of SOEs are subject to higher risks because of the risk of policy and people changes,” the document said. A DBS spokeswoman said: “It is still business as usual for us in China. With slower regional economic growth, we continue to be disciplined and watchful of risks in all the markets we operate in..”

Read more …

C’mon, admit it, you were due for a good laugh.

• China’s February Exports Surge 48.3% (CNBC)

China’s exports surged 48.3% on year in February, sharply above analysts’ forecasts, potentially signaling stronger economic growth for its trade partners. Imports fell 20.5% for the period, according to data from China’s customs department. A Reuters poll had forecast exports would rise 14.2% and imports would fall 10%. For January and February combined – a common metric to help smoothe distortions from the Lunar New Year holiday period – exports rose 15% from a year earlier, while imports declined 20.2%. “The demand from the advanced economies bodes well,” ANZ said in a note Sunday, citing data showing shipments to the U.S. and European Union rose 40.3% and 36.6% on-year respectively.

But the bank noted that the jump in exports could be due to a base effect. “The February 2014 figures were extremely low as Chinese authorities cracked down the round-tripping trade flows,” it said. “We still see strong headwinds facing China’s exports this year,” ANZ said, citing weak export order PMI data. ANZ attributed the decline in imports to weak commodity demand compounded by sharp drops in commodity prices, citing as an example the 45.4% on year drop in the value of iron-ore imports, although the iron-ore import volume only fell 0.9%. As well, “Chinese commercial banks have significantly tightened the trade financing facilities for commodity traders,” ANZ said.

Read more …

“..it is not likely that she came to Baku with positive intentions, or even with a positive image of the country in her mind.”

• Azerbaijan Should Be Very Afraid of Victoria Nuland (GR)

The US’ Assistant Secretary of State for European and Eurasian Affairs, Victoria Nuland, visited Baku on 16 February as part of her trip to the Caucasus, which also saw her paying stops in Georgia and Armenia. While Azerbaijan has had positive relations with the US since independence, they’ve lately been complicated by Washington’s ‘pro-democracy’ rhetoric and subversive actions in the country. Nuland’s visit, despite her warm words of friendship, must be look at with maximum suspicion, since it’s not known what larger ulterior motives she represents on behalf of the US government. [..]

Given the ideological context in which Nuland likely sees eye-to-eye on with her husband, plus her experience in instigating the Color Revolution in Ukraine, it is not likely that she came to Baku with positive intentions, or even with a positive image of the country in her mind. This is all the more so due to the recent scandal over Radio Free Europe/Radio Liberty. The US-government-sponsored information agency was closed down at the end of December under accusations that it was operating as a foreign agent. While the US has harshly chided the Azeri government for this, at the end of the day, it remains the country’s sovereign decision and right to handle suspected foreign agents as it sees fit. Azerbaijan’s law is similar to Russia’s, in that entities receiving foreign funds must register as foreign agents, and interestingly enough, both of these laws parallel the US’ own 1938 Foreign Agents Registration Act (FARA).

So why does the US feel that it reserves the sole right to register foreign agents and entities, and if need be, identify and punish those that are acting in the country illegally, but Azerbaijan is deprived of this exercise of sovereignty? The reason is rather simple, actually – it’s the US that is the most likely to use these foreign agents to destabilize and potentially overthrow governments (as in Ukraine most recently), whereas Azeri agents in America, should they even exist, are nothing more than an administrative nuisance incapable of inflicting any real harm on the authorities. This double standard is at the core of the US’ relations with all countries in the world, not just Azerbaijan, but it’s a telling example of the power and leverage Washington attempts to hold over Baku, which is seen most visibly by the blistering criticism leveled on the government after Radio Free Europe/Radio Liberty’s closing in compliance with the law.

Read more …

Too little too late. Fait accompli.

• EU Won’t Be Pushed Into Confrontation Over Ukraine – Foreign Policy Chief (RT)

The EU is resisting calls from hotheads to supply arms to Ukraine, saying it won’t be pulled into a confrontation with Russia. Europeans cite the progress in implementing a ceasefire in eastern Ukraine between Kiev and local rebels. The idea of providing lethal aid to Kiev is popular among many NATO officials and American politicians. US House Speaker John Boehner and a bipartisan group of top lawmakers called on President Barack Obama to deliver the weapons. But Europeans are opposing the move, which would likely escalate tensions with Russia. “The European Union today is extremely realistic about developments in Russia. But we will never be trapped or forced or pushed or pulled into a confrontative [sic] attitude,” the EU’s Foreign Policy Chief Federica Mogherini told the media on Friday, following an informal meeting of EU foreign ministers in Riga, Latvia.

“We still believe that around our continent – not only in but around – cooperation is far better than confrontation. We still argue for that,” she added. Austrian Foreign Minister Sebastian Kurz said the EU’s goal in Ukraine is “a ceasefire, not an escalation.” Germany has been among the most vocal critics of sending arms to Ukraine and now German officials question the assessment of the situation in the country voiced by Kiev armament pundits. “The statements [on Ukraine] from our source do not fully coincide with the statements made by NATO and the US,” German FM Frank-Walter Steinmeier said after the conference. “We are interested in not allowing it to grow into a misunderstanding.” The German Spiegel magazine reported on Saturday that Chancellor Angela Merkel’s government suspects the US and NATO of trying to derail the EU’s mediation effort in Ukraine.

The Minsk ceasefire agreement between Kiev and rebels in eastern Ukraine was brokered last month by Germany, France and Russia. So far, it’s mostly holding, with both parties pulling some of their heavy weapons back from the front line, and OSCE monitors reporting a significant reduction in violence. The EU says it wants to increase the number of OSCE observers on the ground, doubling its current ceiling of 500. “The main point is obviously working to increase the number of selected and skilled people that can do the job,” Mogherini said. The more observers the tougher it would be to violate the conditions of the Minsk agreement with impunity. Kiev and its foreign backers, particularly in Washington, accuse Russia of propping up the rebel forces with weapons and troops. Moscow insists that it has no involvement in the armed conflict and has only delivered humanitarian aid to the ravaged areas.

Read more …

“86% of the respondents approve of Vladimir Putin as Russia’s president. When asked to name five or six politicians or government officials they trust, 59% responded: ”Putin”.”

• Why Do Russians Still Support Vladimir Putin? (New Statesman)

The news of the assassination of Boris Nemtsov, a Russian opposition politician, dominated the news this weekend. It was possible to imagine – just for a day or two – that the charismatic Boris Nemtsov, who first entered the national political arena in Russia back in the Yeltsin days, had been a prominent figure without whom the opposition would struggle to have a say against Kremlin. Unfortunately, the truth is that Nemtsov was hardly a force to be reckoned with. However open his position on Putin was and however brave his last interview to the Moscow radio station Echo Moskvy was, just hours before his death, Boris Nemtsov was not important. Like any other opposition leader in Russia, he was a scribble on the margin of current affairs. The overwhelming majority of the Russian population supports the country’s president, Vladimir Putin.

A recent poll, conducted between 20-23 February 2015 among 1,600 Russians aged 18 or more in 46 different regions of Russia by an independent Russian not-for-profit market research agency Levada Centre for Echo Moskvy radio station, found that 54% of the population agreed that “[Russia] is moving in the right direction”. 86% of the respondents approve of Vladimir Putin as Russia’s president. When asked to name five or six politicians or government officials they trust, 59% responded: ”Putin”.

Let’s put aside the possibility of rigged polls because there is little to suggest Putin’s popularity is fake. Putin is respected, if not revered. He is referred to as batyushka, the holy father. Many Russians are particularly upset and angry about Nemtsov’s murder because western fingers are pointing at Putin. In their opinion, Nemtsov was most likely killed as a provocation to destabilise Russia and fuel hostility between Kremlin and the west. “With all due respect to the memory of Boris Nemtsov, in political terms he did not pose any threat to the current Russian leadership or Vladimir Putin, said presidential press secretary Dmitriy Peskov. “If we compare popularity levels, Putin’s and the government’s ratings and so on, in general Boris Nemtsov was just a little bit more than an average citizen.”

Read more …

Who’s “our son of a bitch“?

• The Dark Undercurrents Of The War In The Ukraine (Saker)

The situation in the Ukraine is more or less calm right now, and this might be the time to step back from the flow of daily reports and look at the deeper, underlying currents. The question I want to raise today is one I will readily admit not having an answer to. What I want to ask is this: could it be that one of the key factors motivating the West’s apparently illogical and self-defeating desire to constantly confront Russia is simply revanchism for WWII? We are, of course, talking about perceptions here so it is hard to establish anything for sure, but I wonder if the Stalin’s victory against Hitler was really perceived as such by the western elites, or if it was perceived as a victory against somebody FDR could also have called “our son of a bitch“. After all, there is plenty of evidence that both the US and the UK were key backers of Hitler’s rise to power (read Starikov about that) and that most (continental) Europeans were rather sympathetic to Herr Hitler.

Then, of course and as it often happens, Hitler turned against his masters or, at least, his supporters, and they had to fight against him. But there is strictly nothing new about that. This is also what happened with Saddam, Noriega, Gaddafi, al-Qaeda and so many other “bad guy” who began their careers as the AngloZionists’ “good guys”. Is it that unreasonable to ask whether the western elites were truly happy when the USSR beat Nazi Germany, or if they were rather horrified by what Stalin had done to what was at that time the single most powerful western military – Germany’s? [..] for the western elites, [..] they must have known that their entire war effort was, at most, 20% of what it took to defeat Nazi Germany and that those who had shouldered 80%+ were of an ideology diametrically opposed to capitalism. Is there any evidence of that fear? I think there is and I already mentioned them in the past:

Plan Totality (1945): earmarked 20 Soviet cities for obliteration in a first strike: Moscow, Gorki, Kuybyshev, Sverdlovsk, Novosibirsk, Omsk, Saratov, Kazan, Leningrad, Baku, Tashkent, Chelyabinsk, Nizhny Tagil, Magnitogorsk, Molotov, Tbilisi, Stalinsk, Grozny, Irkutsk, and Yaroslavl.

Operation Unthinkable (1945) assumed a surprise attack by up to 47 British and American divisions in the area of Dresden, in the middle of Soviet lines.This represented almost a half of roughly 100 divisions (ca. 2.5 million men) available to the British, American and Canadian headquarters at that time. (…) The majority of any offensive operation would have been undertaken by American and British forces, as well as Polish forces and up to 100,000 German Wehrmacht soldiers.

Operation Dropshot (1949): included mission profiles that would have used 300 nuclear bombs and 29,000 high-explosive bombs on 200 targets in 100 cities and towns to wipe out 85% of the Soviet Union’s industrial potential at a single stroke. Between 75 and 100 of the 300 nuclear weapons were targeted to destroy Soviet combat aircraft on the ground.

But the biggest proof is, I think, the fact that none of these plans was executed, even though at the time the Anglosphere was safely hidden behind its monopoly on nuclear weapons (and have Hiroshima and Nagasaki not been destroyed in part to “scare the Russians”?). And is it not true that the Anglos did engage in secret negotiations with Hitler’s envoys on several occasions? (The notion of uniting forces against the “Soviet threat” was in fact contemplated by both Nazi and Anglo officials, but they did not find a way to make that happen.) So could it be that Hitler was, really, their “son of a bitch”?

Read more …

“We support sanctions that bring the other side to the negotiation table.. But we are against sanctions that are imposed simply because someone is angry.”

• ‘Give Peace A Chance, Decide Sanctions Later’: EU Rethinks Russia (RT)

The latest EU meeting has shown that many of its members are in no rush to extend the sanctions which were imposed on Russia last year following a US example, or to exert any more pressure on Moscow, as long as the Minsk ceasefire agreement is holding. Most foreign ministers at the EU two-day meeting in the Latvian capital expressed hopes that the latest Minsk agreement would be a success, and there would be no need to impose further sanctions on Russia. The meeting had a format of an informal discussion, where the ministers touched the topics of the Minsk agreements and the OSCE mission in Ukraine, as well as the possible stepping up of pressure on Russia to “promote peace.”

Scheduled ten days before an official summit in Brussels, the meeting has shown that the EU can’t yet agree even on the automatic extension of existing sanctions – a move that some of the hawkish states have been actively promoting. “In my opinion, we must not make any other steps, we have to give peace a chance. The extension could take place, but only if there is no improvement of the situation,” Spanish FM Jose Manuel Garcia-Margallo said, expressing his views after the meeting , according to Russian news agency RIA Novosti. The Spanish FM is heading to Moscow, during which he will not only discuss the Ukrainian crisis, but will also meet with the Russian Energy minister.

Meanwhile, Italian FM Paolo Gentiloni told reporters the he sees “encouraging signals” on the ground in eastern Ukraine, and so “at the moment we don’t need either new sanctions or automatic renewals.” Austrian Foreign Minister Sebastian Kurz shared the views of his Italian counterpart, saying that there is a “glimpse of hope” following the Minsk agreements: “We should do everything now to improve the situation and decide later whether that improvement really happened and we can reduce the sanctions, or, if we have to, extend them,” Kurz said. Greece has also spoke out against any new sanctions as long as Russia supports the Minsk agreements, with Greek Foreign Minister Nikos Kotzias saying the Greek experience suggests that “not every sanction is constructive” and can succeed. “We support sanctions that bring the other side to the negotiation table,” Kotzias told German ARD. “But we are against sanctions that are imposed simply because someone is angry.”

Read more …

Wait! Where have we heard this before? “Owner will throw in a brand new car..” “Just pick your favorite colour.”

• Layoffs And Empty Streets As Australia’s Boom Towns Go Bust (Reuters)

When Probo Junio got a visa to work in Australia, he thought he had won a ticket to the good life. In 2013, the 45-year-old boilermaker left his hometown of Cebu in the Philippines, where he was getting paid about $10 a day, to work in Karratha in Western Australia for $30 an hour. Enough to support his relatives and build a new life Down Under. What Junio didn’t expect was that Australia’s booming resources industry would go bust less than two years later, taking his job, and leaving him just 60 days to find work or go home. “It’s very difficult because most of the companies don’t want 457 visa holders,” he said, referring to temporary permits for skilled workers.Across the country, people like Junio are falling victim to downsizing. Jobs, once plentiful and well paid, are scarce.

Real estate prices in boom towns are sinking and even the notoriously high coffee prices in mining capital Perth have levelled off at under $4. Prices of iron ore and coal, the country’s two biggest export earners, have plunged during the last two years amid falling demand from China, in the wake of its economic slowdown. Just a few years ago, foreign workers were flooding into Australia, lured by huge pay as the resources industry scrambled to fill positions. Truck driving and cooking jobs offering $100,000 a year made headlines abroad. But those workers, like Junio, are now hard-pressed to find work, especially if they are on temporary visas. Even permanent residents have to take lower pay. “There is reality coming into the marketplace about salaries,” said John Downing, who runs global resources recruiting firm Downing Teal, adding that salary expectations have fallen 10% to 25%.

“For Lease” signs are everywhere in West Perth, the headquarters of many mining, oil and gas companies. “You could shoot a cannon down those streets,” said resources analyst Peter Strachan. “There’s nobody there.”Commercial vacancy rates in the city are near a 20-year high of 15% as resources companies downsize or shut down, said Joe Lenzo, of the Property Council of Australia. The real estate market has also been hit in the coal country of Queensland, across the continent. “Owner will throw in a brand new car,” read advertisements for houses in the coal-mining town of Moranbah. “Just pick your favorite colour.”

Read more …

There’s something very positive about South America.

• Venezuela To Get South American Help For Food Crisis (BBC)

Foreign ministers from 12 South American nations gathering in Caracas have promised to help Venezuela overcome an ongoing shortage of food, medicine and other products. The regional Unasur bloc agreed with President Nicolas Maduro to provide items that have gone missing from many Venezuelan supermarkets. The shortage of staples has contributed to popular discontent. Unasur highlighted the importance of safeguarding democratic stability. “The idea is to get all the countries to support the distribution of staples,” said Ernesto Samper, Secretary-General of Unasur (Union of South American Nations). “We will work together with the Venezuelan authorities to strengthen the distribution networks in our countries so they help Venezuela,” said Mr Samper.

He criticised recent anti-government protests in Venezuela that descended into violence. The opposition must “express its opinions in a democratic, peaceful and lawful manner,” said Mr Samper. The Unasur ministers will meet opposition leaders and government officials in the next few days to seek guarantees that Venezuela will be able to hold free and fair elections later this year. Opposition leader Henrique Capriles told the AFP news agency on Tuesday that Mr Maduro could cancel the vote, which is scheduled for the second half of this year. “The government had never had such a large deficit [in the polls] heading into an election. Now it does. How does it change that? It rigs the game,” said Mr Capriles. Mr Maduro said the elections would go ahead as planned.

Read more …

“For us, water is [now] more important than oil.”

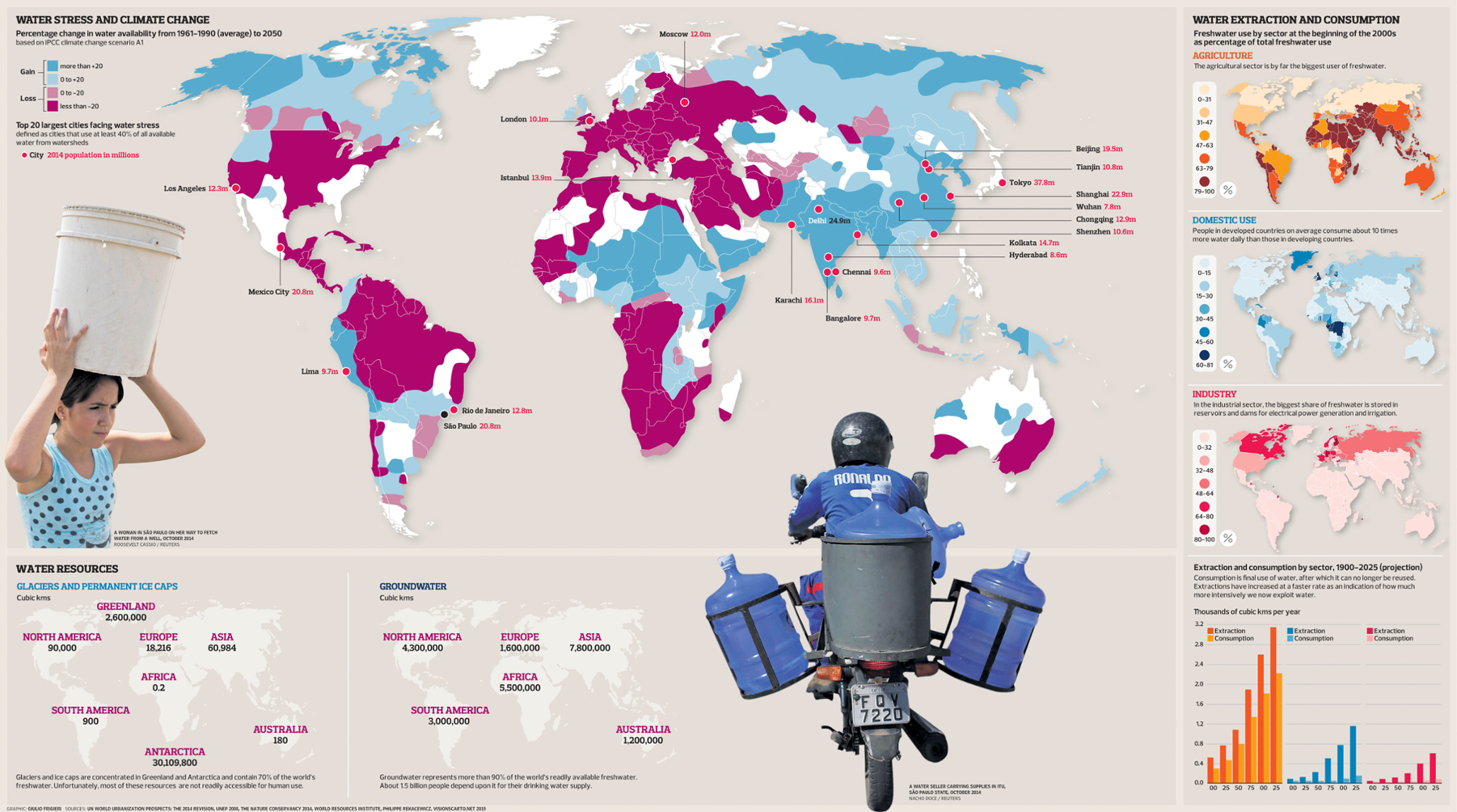

• Why Fresh Water Shortages Will Cause The Next Great Global Crisis (Guardian)

Water is the driving force of all nature, Leonardo da Vinci claimed. Unfortunately for our planet, supplies are now running dry – at an alarming rate. The world’s population continues to soar but that rise in numbers has not been matched by an accompanying increase in supplies of fresh water. The consequences are proving to be profound. Across the globe, reports reveal huge areas in crisis today as reservoirs and aquifers dry up. More than a billion individuals – one in seven people on the planet – now lack access to safe drinking water. Last week in the Brazilian city of São Paulo, home to 20 million people, and once known as the City of Drizzle, drought got so bad that residents began drilling through basement floors and car parks to try to reach groundwater.

City officials warned last week that rationing of supplies was likely soon. Citizens might have access to water for only two days a week, they added. In California, officials have revealed that the state has entered its fourth year of drought with January this year becoming the driest since meteorological records began. At the same time, per capita water use has continued to rise. In the Middle East, swaths of countryside have been reduced to desert because of overuse of water. Iran is one of the most severely affected. Heavy overconsumption, coupled with poor rainfall, have ravaged its water resources and devastated its agricultural output. Similarly, the United Arab Emirates is now investing in desalination plants and waste water treatment units because it lacks fresh water.

As crown prince General Sheikh Mohammed bin Zayed al-Nahyan admitted: “For us, water is [now] more important than oil.” The global nature of the crisis is underlined in similar reports from other regions. In south Asia, for example, there have been massive losses of groundwater, which has been pumped up with reckless lack of control over the past decade. About 600 million people live on the 2,000km area that extends from eastern Pakistan, across the hot dry plains of northern India and into Bangladesh, and the land is the most intensely irrigated in the world. Up to 75% of farmers rely on pumped groundwater to water their crops and water use is intensifying – at the same time that satellite images shows supplies are shrinking alarmingly.

Read more …

“I look at . . . so many forests, all cut, that have become land . . . that can [no] longer give life..”

• The Francis Miracle: Inside The Transformation Of The Pope And The Church (TIME)

It was probably inevitable that the first pope named Francis—inspired by a saint who preached to birds and gave pet names to the sun and the moon—has turned out to be a strong environmentalist. In fact, Francis has said that concern for the environment is a defining Christian virtue. (The young Jorge Bergoglio trained as a chemist, so he has a foundation to appreciate the scientific issues involved.) This element of the social gospel bubbled to the surface as early as his inaugural mass, when Francis issued a plea to “let us be ‘protectors’ of creation, protectors of God’s plan inscribed in nature, protectors of one another and of the environment.” St. Francis’s imprint on this pope is clearly strong. In unscripted comments during a meeting with the president of Ecuador in April 2013, he said, “Take good care of creation. St. Francis wanted that.

People occasionally forgive, but nature never does. If we don’t take care of the environment, there’s no way of getting around it.” The two previous popes were also environmentalists. The mountain-climbing, kayaking John Paul II was a strong apostle for ecology, once issuing an almost apocalyptic warning that humans “must finally stop before the abyss” and take better care of nature. Benedict XVI’s ecological streak was so strong that he earned a reputation as “the Green Pope” because of his repeated calls for stronger environmental protection, as well as gestures such as installing solar panels atop a Vatican audience hall and signing an agreement to make the Vatican Europe’s first carbon-neutral state. Francis is carrying that tradition forward.

Among other things, he told French President François Hollande during a January 2014 meeting that he is working on an encyclical on the environment. (An encyclical is considered the most developed and authoritative form of papal teaching.) The Vatican has since confirmed that Francis indeed intends to deliver the first encyclical ever devoted entirely to environmental issues. In a July 2014 talk at the Italian university of Molise, Francis described harm to the environment as “one of the greatest challenges of our times.” It’s a challenge, he said, that’s theological as well as political in nature. “I look at . . . so many forests, all cut, that have become land . . . that can [no] longer give life,” the pope continued, citing South American woodlands in particular. “This is our sin, exploiting the Earth. . . . This is one of the greatest challenges of our time: to convert ourselves to a type of development that knows how to respect creation.”

Read more …