G.G. Bain St. Paul’s Church and St. Paul Building from Woolworth Building, NYC Apr 1919

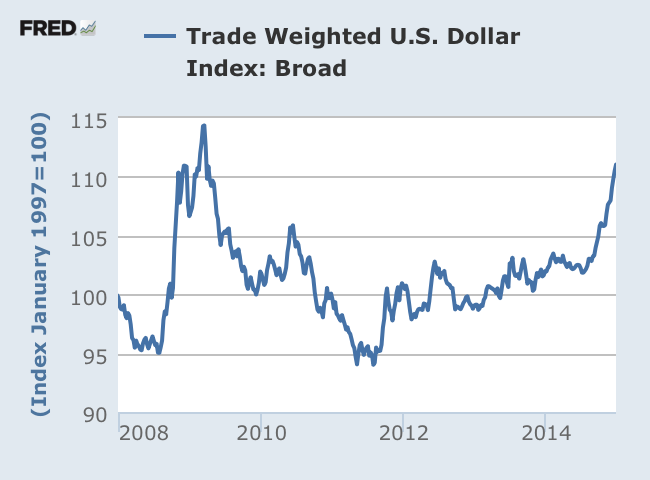

Ambrose is all over the place here. But the core is dead on: the dollar will decide a lot in 2015, it’ll be a global wrecking ball.

• The Year Of Dollar Danger For The World (AEP)

America’s closed economy can handle a surging dollar and a fresh cycle of rising interest rates. Large parts of the world cannot. That in a nutshell is the story of 2015. Tightening by the US Federal Reserve will have turbo-charged effects on a global financial system addicted to zero rates and dollar liquidity. Yields on 2-year US Treasuries have surged from 0.31% to 0.74% since October, and this is the driver of currency markets. Since the New Year ritual of predictions is a time to throw darts, here we go: the dollar will hit $1.08 against the euro before 2015 is out, and 100 on the dollar index. Sterling will buckle to $1.30 as a hung Parliament prompts global funds to ask why they are lending so freely to a country with a current account deficit reaching 6% of GDP.

There will be a mouth-watering chance to invest in the assets of the BRICS and mini-BRICS at bargain prices, but first they must do penance for $5.7 trillion in dollar debt, and then do surgery on obsolete growth models. The MSCI index of emerging market stocks will slide another third to 28 before touching bottom. The Yellen Fed will be forced to back down in the end, just as the Bernanke Fed had to retreat after planning a return to normal policy at the end of QE1 and QE2. For now the Fed is on the warpath, digesting figures showing US capacity use soaring to 80.1%, and growth running at an 11-year high of 5% in the third quarter. The Fed pivot comes as China’s Xi Jinping is trying to deflate his own country’s $25 trillion credit boom, early in his 10-year term and before it is too late. He does not need or want uber-growth.

The Politburo will more or less keep its nerve as long as China continues to meet its target of 10m new jobs a year – easily achieved in 2014 – and job vacancies outstrip applicants. Uncle Xi will ultimately blink, but traders betting on a quick return to credit stimulus may lose their shirts first. Worse yet, when he blinks, a tool of choice may be to drive down the yuan to fight Japan’s devaluation, and to counter beggar-thy-neighbour dynamics across East Asia. This would export yet more Chinese deflation to the rest of the world. At best we are entering a new financial order where there is no longer an automatic “Fed Put” or a “Politburo Put” to act as a safety net for asset markets.

That may be healthy in many ways, but it may also be a painful discovery for some. A sated China is as much to “blame” for the crash in oil prices as America’s shale industry. Together they have knouted Russia’s Vladimir Putin. The bear market will short-circuit at Brent prices of $40, but not just because shale capitulates. Marginal producers in Canada, the North Sea, West Africa and the Arctic will share the punishment. The biggest loser will be Saudi Arabia, reaping the geostrategic whirlwind of its high stakes game, facing Iranian retaliation through the Shia of the Eastern Province where the oil lies, and Russian retaliation through the Houthis in Yemen.

This is about much more than oil: “The Iranian deputy minister also criticised Saudi military involvement in Bahrain, which has been gripped by tension since 2011 protests led by majority Shi’ite Muslims demanding reforms and a bigger role in running the Sunni-ruled country.”

• Iran Says Saudi Arabia Should Move To Curb Oil Price Fall (Reuters)

Falling world oil prices will hurt countries across the Middle East unless Saudi Arabia, the world’s biggest crude exporter, takes action to reverse the slump, Iran’s deputy foreign minister told Reuters. Hossein Amir Abdollahian described Saudi Arabia’s inaction in the face of a six-month slide in oil prices as a strategic mistake and said he still hoped the kingdom, Tehran’s main rival in the Gulf, would respond. Oil prices closed on Wednesday at a 5-1/2 year low, registering their second-biggest ever annual decline after OPEC oil exporters, led by Saudi Arabia, chose to maintain oil output despite a global glut and calls from some of the cartel’s members – including Iran and Venezuela – to cut production.

“There are several reasons for the drop of the price of oil but Saudi Arabia can take a step to have a productive role in this situation,” Abdollahian said. “If Saudi does not help prevent the decrease in oil price … this is a serious mistake that will have a negative result on all countries in the region,” Abdollahian said in an exclusive interview on Wednesday evening. His comments highlight continued tensions between the Shi’ite Muslim republic and Sunni Muslim kingdom, locked in a battle for regional power and influence despite hopes of rapprochement since the inauguration of Iran’s President Hassan Rouhani in August 2013.

Abdollahian said Iran would have more discussions with Saudi Arabia about the oil price, both through oil officials at OPEC and through the foreign ministry. He did not give specific details on when any meeting might take place. Saudi Arabia said last month that it would not cut output to prop up oil markets even if non-OPEC nations did so. The Iranian deputy minister also criticised Saudi military involvement in Bahrain, which has been gripped by tension since 2011 protests led by majority Shi’ite Muslims demanding reforms and a bigger role in running the Sunni-ruled country. Abdollahian said Bahraini authorities’ continued detention of Shi’ite opposition leader Sheikh Ali Salman would have “serious consequences” for the government there.

Tehran and Riyadh accuse each other of interfering in the pro-Western Gulf island kingdom, one of several countries where their power struggle has played out. They also support opposing sides in wars and disputes in Iraq, Syria, Lebanon and Yemen. Abdollahian dismissed United States efforts to fight Islamic State, also known by its Arabic acronym Daesh, as a ploy to advance U.S. policies in the region. “The reality is that the United States is not acting to eliminate Daesh. They are not even interested in weakening Daesh, they are only interested in managing it,” he said.

“.. the impact on that on production would only be start to felt in 2016 onwards and not as much as we would like to see in 2015.”

• Could 2015 Herald A ‘New Oil Order’? (CNBC)

Last year was a tumultuous year for oil, with Brent crude prices declining around 50% since June on the back of an over-supplied market and lack of global demand. From “old school” oil producers Russia and Saudi Arabia in the east to shale oil in California and oil sands in Alberta in the west, the glut of oil and its impact on currencies and economies has been felt across the world. When OPEC decided not to cut production when it met in November, the 12 major oil producers effectively threw down the gauntlet to the young guns of U.S. oil to see who could withstand the fall in prices and who would blink first and trim production. As of January 2, benchmark Brent crude was trading at $57.58, having fallen from a high of around $115 a barrel hit in mid-June.

With prices falling fast and hitting five-year lows in mid-December, commodities research teams at the world’s investment houses and banks scrambled to revise their 2015 predictions for oil and the potential impact on global economies. And as wildly fluctuating as the price of oil has been, so have the predictions. While HSBC told investors to prepare for $95 a barrel by the end of 2015, other analysts were far more bearish. Morgan Stanley cut its 2015 forecast for Brent saying that in a worst case scenario crude prices could fall to $43 per barrel in 2015, although its base case scenario was for $70. The U.S. shale revolution and its accompanying rise in oil production has been a decisive factor in the fall in the price this year. The newcomer has affronted the old guard of producers like Saudi Arabia, the biggest oil exporter in the OPEC group and analysts believed its decision not to cut production was a move to put price pressure on U.S. producers.

The U.S. might not give up so easily though, according to Citi’s commodities research team who said in their 2015 outlook for the commodities markets that there is a “distinctive underlying ‘Made in America’ quality that looks likely to dominate the commodity complex through 2015.” Whether U.S. shale oil producers can withstand the fall in prices into 2015 and dent OPEC’s market share is a key matter for debate, however. “Prices are already approaching the danger point for the bulk of U.S. shale output, so industry costs would have to fall for prices to be sustainable at these lower levels,” Melanie Debono, economist at Capital Economics, said in the consultancy’s accompanying note.

There was a risk, Debono added, that an extended period of lower oil prices would lead to large cuts in output in both the U.S. and Canada. Companies like ConocoPhillips who are active in the U.S. shale industry have already announced that it would “defer significant investment” in Canada and the U.S. as returns looked far less attractive. “It’s very clear if oil prices remain below in the region of $64 per barrel for a sustained period of time – that’s about a three to six month period at least – we would start seeing increased scale backs in the U.S.,” Abhishek Deshpande, oil and gas analyst at Natixis. “But the impact on that on production would only be start to felt in 2016 onwards and not as much as we would like to see in 2015.”

Oil and the dollar.

• Falling Oil Raises Headache For Developing Nations (MarketWatch)

The drops last year in the prices of oil and other commodities are threatening to stunt growth in poor African and Latin American nations that sought to use vast natural-resource wealth to climb the development ladder. During a decadelong boom, governments on those continents vowed to use a windfall from surging raw-material prices to lift the vast underclass. Governments that sought big development leaps by funding social-welfare programs and ambitious infrastructure initiatives, such as building roads, ports and power plants, may now have less money to do so. “The good-governance records in many [Latin American] countries were linked to commodity prices, and this will be tested by the end of the commodity boom,” said Jorge Castaneda, Mexico’s former foreign minister.

The commodity-rich nations of Africa and Latin America are also facing a slowdown in China, a key buyer of exports from South Africa, Nigeria, Brazil, Chile and others. The two regions have been hit by a global selloff of emerging-market stocks, bonds and currencies. The stakes are high for these often-volatile economies, which have some of the world’s widest rich-poor gaps. Economic slowdowns and declining investment flows threaten to stretch budgets. In Latin America, credit-ratings firm Fitch expects to downgrade more countries than it upgrades in 2015. In some cases, the declines could expose levels of corruption and mismanagement that weren’t detected during the good times. In resource-rich Brazil, millions of families escaped extreme poverty and joined a growing working class.

Now, the country’s growth has stagnated, investment is declining and currency declines are raising inflation fears. Allegations of widespread corruption at the state oil firm Petroleo Brasileiro SA are adding to the pain. Brazilian officials had placed the oil firm at the center of a far-reaching plan to overhaul the economy and lift millions of poor into better paying jobs. Shares of Petrobras have fallen to multiyear lows. The situation is worse in Venezuela, where President Nicolás Maduro is seeking to use oil wealth to fuel a Socialist revolution. With oil prices plunging, investors are gauging the risk that Venezuela may fail to pay its debt. Default would add to the woes of an economy saddled with double-digit inflation and shortages of basic items.

Even countries with more moderate policy mixes, such as Chile, among the biggest copper exporters, are getting hit. Chile cut its 2015 growth outlook by half a percentage point to 2.5% in December. In Africa, the impact is magnified by the dependence of some fast-growing economies, such as Zambia, on the export of a single commodity. If the price of that commodity falls–in Zambia’s case, copper–the fallout can be far-reaching. Countries that didn’t balance budgets or curtail corruption while times were good will face painful choices, said Jack Allen of Capital Economics in London. Capital Economics forecasts average growth in sub-Saharan Africa to fall by one percentage point in 2015, to 4%, the slowest pace in more than a decade.

Race to the bottom.

• Russia Oil Output Hits Post-Soviet High (Reuters)

Russia’s 2014 oil output hit a post-Soviet record high average of 10.58 million barrels per day (bpd), rising by 0.7% helped by small non-state producers, Energy Ministry data showed on Friday. Oil and gas condensate production in December hit 10.67 million bpd, also a record high since the collapse of the Soviet Union. The data showed Russia’s so-called small producers, mostly privately held, increased their output by 11% to just over 1 million barrels per day. Crude oil exports via state monopoly Transneft fell 5% to 195.5 million tonnes due to rising domestic demand and refinery runs.

Exports to China reached a new high of 22.6 million tonnes (452,000 bpd), up 43% on the year as Russia seeks to diversify its energy customers. Russian producers capitalized on rising oil prices in the first half of 2014, when they reached over $113 per barrel. However, they have halved since then. Hurt by falling oil prices and Western sanctions prompted by Moscow’s role in Ukraine, growth in oil output in 2014 slowed from a gain of 1.4% in 2013. Top listed oil company Rosneft, which produces more oil than OPEC members Iraq or Iran, saw its output slip 0.7% as it struggled to arrest declining production at its West Siberian fields. Oil and gas fund about half of Russia’s budget.

The country’s economy is slipping into recession following a fall in oil prices and could see oil output decline to 525 million tonnes in 2015, according to an Energy Ministry forecast. The International Energy Agency (IEA) expects Russian oil output to fall by 1%. The country’s natural gas production in 2014 fell by 4% to 640.237 billion cubic meters (bcm). Top producer Gazprom posted an output fall of 9% to an all-time low of 432 bcm due to its pricing dispute with Ukraine, once its second-largest customer after Germany.

Sounds crazy?

• Oil At $14 A Barrel? Here’s How It Could Happen (CNBC)

No one really saw 2014’s dramatic plunge in oil price coming, so it’s probably fair to say that any predictions about where it’s going from here fall somewhere between educated guesses and picking a number out of a hat. In that light, it’s less than shocking to see one analyst making a case—albeit in a pure outlier sense—for a drop all the way below $14 a barrel. Abigail Doolittle, who does business under the name Peak Theories Research, posits that current chart trends point to the possibility that crude has three downside target areas where it could find support—$44, $35 and the nightmare scenario of, yes, $13.65. Make no mistake, she thinks that’s an extreme case.

Her target for the more likely move is the $35 range, which in itself is quite a call considering light crude had been just above $100 a barrel this summer and the move would represent a 33% or so plunge just from current levels. But Doolittle makes room for an even more extreme scenario, in which technical support gives way as part of what she describes as a triangular pattern forming in an “ascending trend channel” that brings about the extreme case. “There is a wild case scenario for a massive fall in oil and it is made by both the triangle and the possibility that oil’s true trading path will turn out to be sideways on a potential false initial reaction of epic proportions,” Doolittle explained in a report she distributed Wednesday morning.

“This possibility cannot be ignored or discounted because it is simply too strong from a technical standpoint.” She acknowledges that the scenario “may sound outrageous” but cautions “odds appear fairly strongly” that the move could be triggered by “a false initial reaction or basically a massive head fake caused by a variety of factors.” Before consumers get too giddy about the cost of even lower fuel prices at the pump, Doolittle offers a word of caution. “Clearly this would seem to be a tail wind for consumers, but the various shocks and possible financial market crashes that could be triggered by such a collapse in oil would not be, and thus this seems a very dangerous scenario indeed,” she said.

“Italian and Spanish bond yields dropped to record lows after the interview was published and the euro fell to the weakest since June 2010.”

• Draghi Says ECB Prepares Action as Deflation Risk Non-Negligible (Bloomberg)

European Central Bank President Mario Draghi said he can’t exclude the risk of deflation in the euro area, hinting that the likelihood of large-scale quantitative easing is increasing. “The risk that we don’t fulfill our mandate of price stability is higher than it was six months ago,” Draghi said in an interview with German newspaper Handelsblatt. “We are in technical preparations to alter the size, speed and composition of our measures at the beginning of 2015, should this become necessary, to react to a too-long period of low inflation. There’s unanimity in the ECB council on that.”

While policy makers agree in principle, the debate over whether fresh stimulus is needed at this point has reopened a rift on the ECB’s Governing Council that now comprises 25 officials after Lithuania joined the currency region on Jan. 1. With inflation seen turning negative this year, some have warned of a deflationary spiral, as others have urged waiting to allow previously agreed measures to show their effect. Draghi said on deflation that “the risk cannot be entirely excluded, but it is limited” and “we have to act against such risk.” Asked how much the ECB will have to spend on government bonds, he said “it’s difficult to say.” Italian and Spanish bond yields dropped to record lows after the interview was published and the euro fell to the weakest since June 2010.

“A break-up of the euro zone? That will not happen. That’s why there is no plan B ..,”

• Draghi: Risk of ECB Failing Its Mandate Higher Than 6 Months Ago (Reuters)

European Central Bank President Mario Draghi said the risk of the central bank not fulfilling its mandate of preserving price stability was higher now than half a year ago, and reiterated its readiness to act early this year should it become necessary. In an interview with German financial daily Handelsblatt, Draghi urged politicians to implement necessary reforms, reduce tax burdens and cut red tape to support the euro zone recovery, which Draghi said was “fragile and uneven”. There was a limited risk of deflation in the euro zone, Draghi said, but if inflation remained too low for too long and led to receding inflation expectations and a delay in spending, the ECB would need to act to fulfill its mandate.

“The risk that we do not fulfill our mandate of price stability is higher than six months ago,” Draghi was quoted as saying in an interview that will be published on Friday. “We are in technical preparations to adjust the size, speed and compositions of our measures early 2015, should it become necessary to react to a too long period of low inflation. There is unanimity within the Governing Council on this.” He added that government bond purchases were among the tools the ECB could use to fulfill its mandate, but that state financing – which is prohibited by the EU treaty — had to be avoided.

Printing money to buy government bonds, a step known as quantitative easing (QE), is seen as one of the last tools the ECB has to revive inflation, with the key interest rate at 0.05% and growing doubts about the impact of earlier measures. Euro zone inflation stands at 0.3%, far below the ECB’s target of just under 2%, and calls for more ECB action have grown louder as policymakers warn that plunging oil prices could push inflation below zero in coming months. Concerns are that weaker price expectations could affect wages and investments and dampen growth prospects. Regardless, Draghi ruled out a break-up of the euro zone. “A break-up of the euro zone? That will not happen. That’s why there is no plan B,” he said.

Beggar thy world.

• Euro Forecasters See Pain After Worst Year Since 2005 (Bloomberg)

Midway through European Central Bank President Mario Draghi’s May press conference in Brussels, the euro rose to its strongest level during his tenure. Then he said the ECB was ready to introduce more stimulus measures, sending it into a slide that strategists say will extend into 2015. Europe’s common currency, which appreciated to $1.3993 that May day, ended last year down 12% against the dollar at $1.2098, its biggest loss since 2005. Strategists, who were too timid with their call for a decline in 2014 to $1.28, now see a slump to $1.18 by the end of this year. A weaker euro is key for Draghi as he tries to spur the region’s struggling economy and ward off deflation. This week, ECB Chief Economist Peter Praet told German newspaper Boersen-Zeitung the threat of a drop in consumer prices is increasing, bolstering speculation policy makers will soon start actions such as buying bonds that tend to weigh on a currency.

“The euro-bearish consensus was struggling hard for the first half of the year, but it has come good as the ECB has driven rates down,” Kit Juckes, a global strategist at SocGen in London, said in a Dec. 30 phone interview. “The best thing the ECB can try to engineer is still a weaker euro.” Juckes forecasts the euro will weaken to $1.14 by year-end, a level last seen in 2003. With inflation languishing below the ECB’s goal of just under 2% and the market’s outlook for consumer prices crumbling as crude oil declines, more than 90% of respondents in a monthly Bloomberg survey in December predicted that the ECB would expand the supply of euros by beginning to purchase sovereign bonds in 2015. That’s up from 57% the previous month.

The euro-area may see “negative inflation during a substantial part of 2015” amid a slide in crude, and the Governing Council “cannot simply look through” that, Praet said in comments published Dec. 31 on the ECB’s website. “Inflation expectations are extremely fragile” and “the risk of second-round effects seems to be greater today than it was in the past,” he said. Since the May meeting, the ECB cut its deposit rate below zero for the first time on record, began a program of targeted loans, and started purchasing asset-backed securities and covered bonds. At the same time, the dollar is strengthening as the Federal Reserve moves closer to raising interest rates.

The Germans are not about to give in.

• Merkel Ally Urges ECB Not To Buy Struggling States’ Bonds (Reuters)

A senior member of Angela Merkel’s party warned the European Central Bank not to pour money into Greece and other struggling euro zone states through bond purchases, saying this would reduce pressure on them to enact much-needed reforms. Michael Fuchs, deputy parliamentary floor leader of the German chancellor’s Christian Democrats (CDU), told Deutschlandfunk radio on Friday: “We shouldn’t pump extra money into these states, but rather make sure they continue along the reform path. “I’d be grateful if (ECB President Mario) Mr Draghi would make statements along these lines.” In an interview with German financial daily Handelsblatt published on Friday, Draghi urged politicians to implement necessary reforms, reduce tax burdens and cut red tape to support a fragile euro zone recovery.

He also said the risk of the central bank not fulfilling its price stability mandate was higher now than half a year ago, and reiterated its readiness to act soon if needed, with government bond purchases among the tools it could use. With the euro zone flirting with deflation, financial markets interpreted Draghi’s comments on Friday as strongly suggesting the ECB would soon embark on outright money-printing, and the euro sank to a 4-1/2 year low against the dollar. Printing money to buy government bonds, a measure known as quantitative easing (QE), is seen as one of the last tools the ECB has to revive inflation. The bank has already pushed its key interest rate down to a record low of 0.05% and doubts are growing about the impact of earlier measures.

“I expect there to be fierce discussion over this at the next ECB meeting,” said Fuchs, referring to opposition to the bond-buying plan by the head of the Bundesbank Jens Weidmann. The ECB’s next policy meeting is on Jan. 22. Fuchs has frequently expressed frustration felt by many German politicians and the public about the pace of reform in twice-bailed-out Greece. He was quoted as saying in a newspaper interview published on Wednesday that euro zone politicians were not obliged to rescue Greece as the country was no longer of systemic importance to the single currency bloc. Greece holds a general election just three days after the ECB meeting and polls suggest the left-wing Syriza party, which rejects the terms of Greece’s euro zone bailouts, will emerge as the strongest party.

A decade filled with wrong decisions and futile policies.

• New Year Brings Eurozone Closer To A Lost Decade (MarketWatch)

It looks like it will be a “lost decade” after all. As the eurozone enters the eighth year of a slump that began with the 2008 financial crisis, only true optimists believe that the bloc will find a path to faster growth over the next couple of years. Slow growth and rock-bottom inflation have set in. This combination inevitably delays a reduction of the bloc’s heavy private- and public-sector debt burdens. While their debt loads remain high and their incomes in nominal terms are stagnant, people perpetuate slow growth by saving rather than spending. As 2015 begins, economic activity in the eurozone is below the level it was at the start of 2008. The hardest-hit economies are a long way below. With growth so anemic, it doesn’t take much of a shock to turn it negative. Last year, the imposition of European Union sanctions on Russia and its modest retaliation were almost enough to tip the bloc into recession.

This year starts once again with political uncertainties in Greece–and a Jan. 25 general election–that may further set back faltering confidence. And as long as the bloc’s economic prospects remain sickly, the more likely become political crises among members of the currency union. In Greece and in other debt-burdened countries such as Italy and Spain, antiausterity, antiestablishment parties of the left are gaining ground. In Europe’s core, including France, anti-EU, anti-immigration parties of the right are finding traction. At the least, these political shifts are likely to weaken appetite for more supply-side reforms to improve the functioning of labor and goods markets. They may also further fan an incipient backlash against U.S. companies in the vanguard of technological change that would be a motor for long-term growth.

But it could be worse. History offers a cautionary tale about what happens when societies struggle to pay back debt burdens, argues Moritz Kraemer, an analyst with Standard & Poor’s in Frankfurt, in Germany’s struggles after World War I to repay its heavy debts. “While the political and economic environment is hardly comparable one hundred years on and the stakes are not likely to be nearly as high, elevated and sustained debt burdens could still pose risks to social cohesion and political stability,” he wrote in a report last month. To be sure, thanks in part to their expectation that the European Central Bank would step in to save the currency, investors rate the risk of a euro breakup far lower than they did a few years ago. “The existential question for the euro is nowhere near as potent as it was back in 2010 and 2011,” said Peter Goves, a bond strategist at Citi Research in London.

Good read. The Vineyard Saker also has Russian versions of Automatic Earth articles .

• 2014 “End Of Year” Report And A Look Into What 2015 Might Bring (Saker)

Introduction: By any measure 2014 has been a truly historic year which saw huge, I would say, even tectonic developments. This year ends in very high instability, and the future looks hard to guess. I don’t think that anybody can confidently predict what might happen next year. So what I propose to do today is something far more modest. I want to look into some of the key events of 2014 and think of them as vectors with a specific direction and magnitude. I want to look in which direction a number of key actors (countries) “moved” this year and with what degree of intensity. Then I want to see whether it is likely that they will change course or determination. Then adding up all the “vectors” of these key actors (countries) I want to make a calculation and see what resulting vector we will obtain for the next year. Considering the large number of “unknown unknowns” (to quote Rumsfeld) this exercise will not result in any kind of real prediction, but my hope is that it will prove a useful analytical reference.

The main event and the main actors A comprehensive analysis of 2014 should include most major countries on the planet, but this would be too complicated and, ultimately, useless. I think that it is indisputable that the main event of 2014 has been the war in the Ukraine. This crisis not only overshadowed the still ongoing Anglo-Zionist attack on Syria, but it pitted the world’s only two nuclear superpowers (Russia and the USA) directly against each other. And while some faraway countries did have a minor impact on the Ukrainian crisis, especially the BRICS, I don’t think that a detailed discussion of South African or Brazilian politics would contribute much. There is a short list of key actors whose role warrants a full analysis. They are: The USA, The Ukrainian Junta, The Novorussians (DNR+LNR), Russia, The EU. NATO. China. I submit that these seven actors account for 99.99% of the events in the Ukraine and that an analysis of the stance of each one of them is crucial. So let’s take them one by one:

1 – The USA Of all the actors in this crisis, the USA is by far the most consistent and coherent one. Zbigniew Brzezinski, Hillary Clinton and Victoria Nuland were very clear about US objectives in the Ukraine:

Zbigniew Brzezinski: Without Ukraine Russia ceases to be empire, while with Ukraine – bought off first and subdued afterwards, it automatically turns into empire…(…) the new world order under the hegemony of the United States is created against Russia and on the fragments of Russia. Ukraine is the Western outpost to prevent the recreation of the Soviet Union.

Hillary Clinton: There is a move to re-Sovietise the region (…) It’s not going to be called that. It’s going to be called a customs union, it will be called Eurasian Union and all of that, (…) But let’s make no mistake about it. We know what the goal is and we are trying to figure out effective ways to slow down or prevent it.

Victoria Nuland: F**k the EU!

Much of it coming from emerging nations. That’s a triple hit: oil, dollar and other commodities.

• Commodity Prices Are Cliff-Diving: The Case Of Iron Ore (David Stockman)

Crude oil is not the only commodity that is crashing. Iron ore is on a similar trajectory and for a common reason. Namely, the two-decade-long economic boom fueled by the money printing rampage of the world’s central banks is beginning to cool rapidly. What the old-time Austrians called “malinvestment” and what Warren Buffet once referred to as the “naked swimmers” exposed by a receding tide is now becoming all too apparent. This cooling phase is graphically evident in the cliff-diving movement of most industrial commodities. But it is important to recognize that these are not indicative of some timeless and repetitive cycle – or an example merely of the old adage that high prices are their own best cure.

Instead, today’s plunging commodity prices represent something new under the sun. That is, they are the product of a fracturing monetary supernova that was a unique and never before experienced aberration caused by the 1990s rise, and then the subsequent lunatic expansion after the 2008 crisis, of a cancerous regime of Keynesian central banking. Stated differently, the worldwide economic and industrial boom since the early 1990s was not indicative of sublime human progress or the break-out of a newly energetic market capitalism on a global basis. Instead, the approximate $50 trillion gain in the reported global GDP over the past two decades was an unhealthy and unsustainable economic deformation financed by a vast outpouring of fiat credit and false prices in the capital markets.

For that reason, the radical swings in commodity prices during the last two decades mark the path of a central bank generated macro-economic bubble, not merely the unique local supply and demand factors which pertain to crude oil, copper, iron ore, or the rest. [..] What really happened is that the central bank instigated global macro-economic bubble ripped commodity pricing cycles out of their historical moorings, resulting in a one time eruption of price levels that had no relationship to sustainable supply and demand factors in the mines and petroleum patch. What materialized, instead, was an unprecedented one-time mismatch of commodity production and use that caused pricing abnormalities of gargantuan proportions.

Let’s see how many will be allowed to fail.

• China Property Developer Fails To Repay $51 Million Loan (Reuters)

Chinese property developer Kaisa Group Holdings said it had failed to repay a HK$400 million ($51.3 million) loan and warned it may default on more debt, the latest problem to hit the firm amid a downturn in the real estate sector. In a stock market filing late on Thursday, the company said the payment of the loan and its interest became compulsory on Dec. 31, following the resignation of its chairman Kwok Ying Shing. The failure to repay the HSBC term loan may trigger default on other loan facilities, debt and equity securities, co-chairman Sun Yuenan said in the filing to the Hong Kong exchange. Last month, Kaisa said the Chinese authorities had imposed a sales blockage on some its projects in the southern city of Shenzhen. Independent research firm CreditSights said the Shenzhen projects were expected to account for around a fifth of Kaisa’s saleable resources by book value.

It also said two other senior executives – Vice Chairman Tam Lai Ling and Chief Financial Officer Cheung Hung Kwong – had left in December. Analysts have questioned the company’s fund raising ability since these two executives left, as they were instrumental in arranging Kaisa’s offshore debt issues. Trading in Kaisa’s shares, which has a market capitalisation of HK$8.2 billion, was halted on Monday. Its bond yields have also more than trebled, with the yield on its bonds due 2018 rising to more than 29% from around 9% at the start of the month. On Friday, its bonds due 2019 and 2020 were both indicated at 40-50 cents on the dollar, after trading as high as 101 and 104 cents on the dollar in December. Moody’s downgraded its credit rating to B3 from B1, warning of further cuts, and Standard & Poor’s said its sales and operations could be “significantly affected” over the next year.

“In 2013, 3,000 pig carcasses were seen floating in Shanghai’s Huangpu river, one of the city’s key sources of drinking water.”

• China Goes Organic Amid Food Scandals (CNBC)

An organic food craze is emerging among China’s urbanites as food safety scandals spur the younger generation toward alternative ways to buy fresh produce and meat. So far, organic foods’ penetration into China appears small, accounting for 1.01% of total food consumption, but that’s nearly triple 2007’s 0.36%, according to data from organic trade fair Biofach. A series of high-profile food scandals over the past seven years has been a primary catalyst for growth in the organic food market. Biofach expects the segment’s share of China’s overall food market to hit 2% this year. China was ranked as one of the world’s worst safety-violation offenders by American food consulting firm Food Sentry this year. In 2013, 3,000 pig carcasses were seen floating in Shanghai’s Huangpu river, one of the city’s key sources of drinking water.

A few months later, reports that a Beijing crime ring was selling rat and fox meat as lamb sparked international outrage, resulting in the arrest of more than 900 people. The trouble continued in 2014, with the Chinese affiliate of U.S. meat supplier OSI Group accused of using expired meat. OSI caters to major fast-food chains such as McDonald’s and Yum Group’s KFC operating on the mainland. Wal-Mart was also dragged into the limelight this year following revelations that its donkey meat product contained fox meat. Most recently, Subway also came under scrutiny after Chinese media reported in late December that workers at a Beijing franchise changed expiry dates on meat and vegetables to extend their use.

“Mr Piketty added that the government instead “would do better to concentrate on reviving growth in France and Europe.“ Oh well, now I don’t have to read those 600 pages.

• Piketty Rejects Légion d’Honneur Award (FT)

France’s sputtering economy was a source of endless frustration for President François Hollande in 2014. It found a new way to torment the French president on the first day of the new year when Thomas Piketty, one of the country’s most celebrated economists, rejected a Légion d’Honneur award, saying the government had no standing to grant such recognition. Mr Piketty, whose 2014 book Capital in the Twenty-First Century has already sold more than 1m copies, told the AFP on Thursday: “I refuse this nomination because I do not think it is the government’s role to decide who is honourable.”

In a clear indictment of Mr Hollande’s economic record, Mr Piketty added that the government instead “would do better to concentrate on reviving growth in France and Europe”. Mr Piketty’s comments come on top of a series of disappointing performances and false dawns on the economic front ever since Mr Hollande and his socialist government took office. Unemployment has remained persistently high in spite of promises to change the upward trend by the end of last year. Meanwhile, sluggish growth — the economy was stagnant for the first six months of 2014 — has helped drag down Mr Hollande’s popularity to the lowest levels of any French president in modern history.

But the rejection of the award by the French economist – who argues for the redistribution of concentrated wealth in his best-selling book, which was the Financial Times and McKinsey Business Book of the Year – is particularly galling coming on the same day that the French president dumped his supertax scheme for the rich. The measure to increase tax rates to 75% on earnings over €1m, which earned Mr Hollande support from the left when he announced the plan to great fanfare in 2012, was on Thursday abandoned after bringing in just a small portion of the expected revenue. In rejecting the Legion of Honour, Mr Piketty joins a list of personalities that includes Claude Monet, Jean-Paul Sartre, Albert Camus, Hector Berlioz and Brigitte Bardot – all of whom declined the award for varying reasons.

Curious article.

• The 10 Most Generous Nations (MarketWatch)

Have you helped a stranger in the past month? If you live in the U.S., Iraq or Trinidad and Tobago, chances are you have. Americans more likely than any other nationality to help strangers, with 79% of people doing so last year, according to an annual index of the most giving nations. The World Giving Index is based on a Gallup survey of more than 130,000 people in 2013 and evaluates charitable behavior in 135 countries around the world. It is sponsored by the Charitable Aid Foundation. The index scores countries based on an average of three measures of giving behavior — the percentage of people who in a typical month donate money to charity, volunteer their time, and help a stranger.

Giving is about more than just existing wealth, the report notes — only five of the top 20 most generous countries are members of the G-20, a group representing the largest economies in the world. Women were more likely to give money than men, but only in high income countries. The country that scored worst in the index was Yemen, where only 3% of people volunteered their time in 2013. Based on the World Giving Index, these are the 10 most generous nations:

He should simply write his own.

• The Pope Blesses the Climate Treaty (Bloomberg)

When a church that once felt threatened by heliocentrism sees hydrocarbons as a threat to God’s creation, there is reason to hope that today’s science skeptics will find religion, too. Fresh off his success in helping to end one of the last remaining battles of the Cold War, Pope Francis is turning his attention – and bringing his considerable star power – to the fight against global warming. His decision to push for an international treaty on climate change in Paris in December may alienate some conservative Catholics who are skeptical of climate science. But Francis’s leadership on the issue is a hopeful sign that 2015 could be the year that the nations of the world finally commit themselves to collective action. Francis could be forgiven for concentrating on other weighty matters: He is challenging the church’s approach to divorced couples and gays and lesbians, reforming its change-resistant curia, and cleaning up its scandal-plagued bank.

All are mammoth undertakings that will earn him enemies. But this pope has shown no interest in shying away from major controversies. His new focus on climate change is a natural outgrowth of his concern for the poor, who will suffer most if droughts and storms worsen, allowing disease and instability to spread more easily. He is not the first pope to sound the alarm on climate change: Both John Paul II and Benedict XVI did so, and in 2011 the Vatican’s Academy of Sciences issued a report that called on “all people and nations to recognize the serious and potentially irreversible impacts of global warming” caused by human activity. Francis is not changing church teaching, only seizing the moment, as a public consensus emerges around the need for coordinated action. In March, he is expected to visit Tacloban, the Philippine city hardest hit by last year’s typhoon Haiyan, which killed thousands and left millions homeless.

As the planet warms and the seas rise, severe storms are expected to become even more destructive. This trip may be followed by a papal encyclical on climate change, a letter to the bishops that will formalize the church’s position on the issue and guide its ministry at the parish level. In September, Francis will have a chance to raise the issue when he addresses the UN General Assembly. He may also convene a summit of religious leaders to focus attention on climate change, which has generated widespread ecumenical agreement. All these steps will occur in the run-up to the UN summit on climate change in Paris at the end of this year. Francis, who has no lack of ambition, is throwing the weight of the church – and his papacy – behind an international agreement.

Well, Tolstoy was an interesting character.

• The Secret To A Happy Life – Courtesy Of Tolstoy (BBC)

We can learn a lot about the art of living from Tolstoy’s War and Peace. It acutely observes vanity and folly, sexual jealousy and family relationships. But we can also learn from the life of the master novelist himself, writes Roman Krznaric. Tolstoy, who was born in 1828 and died in 1910, was a member of the Russian nobility, from a family that owned an estate and hundreds of serfs. The early life of the young count was raucous, debauched and violent. “I killed men in wars and challenged men to duels in order to kill them,” he wrote. “I lost at cards, consumed the labour of the peasants, sentenced them to punishments, lived loosely, and deceived people…so I lived for ten years.” But he gradually weaned himself off his decadent, racy lifestyle and rejected the received beliefs of his aristocratic background, adopting a radical, unconventional worldview that shocked his peers.

So how exactly might his personal journey help us rethink our own philosophies of life?

1. Keep an open mind

2. Practice empathy

3. Make a difference

4. Master the art of simple living

5. Beware your contradictions

6. Become a craftsman

7. Expand your social circle