Hugo Simberg The Wounded Angel 1903

It was always going to the Supreme Court. More interesting right now is how strongly this is dividing the White House team. Kelly refused to enact some of Bannon’s demands. Tillerson and Mattis are not sitting comfortable either. And the legal team has gained in standing, a lot. Trump cannot afford too many of these snags, even if they love the attention and controversy coming from it. All in all, a good thing that the legal system gets tested, never a thing to fall asleep on.

• US Appeals Court Denies Request To Restore Trump’s Immigration Ban (R.)

A U.S. appeal court late on Saturday denied an emergency appeal from the U.S. Department of Justice to restore an immigration order from President Donald Trump barring citizens from seven mainly Muslim countries and temporarily banning refugees. “Appellants’ request for an immediate administrative stay pending full consideration of the emergency motion for a stay pending appeal is denied,” the ruling by the U.S. Court of Appeals for the Ninth Circuit said. It said a reply from the Department in support of the emergency appeal was due on Monday. The Department filed the appeal a day after a federal judge in Seattle ordered Trump’s travel ban to be lifted. The president’s Jan. 27 order had barred admission of citizens from the seven nations for 90 days.

Law.

• DHS Suspends Actions On Travel Ban; ‘Standard Policy’ Now In Effect (R.)

A Seattle federal judge on Friday put a nationwide block on U.S. President Donald Trump’s week-old executive order that had temporarily barred refugees and nationals from seven countries from entering the United States. The judge’s temporary restraining order represents a major setback for Trump’s action, though the White House said late Friday that it believed the ban to be “lawful and appropriate” and that the U.S. Department of Justice would file an emergency appeal. As a result of the ruling, the Department of Homeland Security suspended its enforcement of the ban, announcing on Saturday that “standard policy and procedures” were now in effect. “In accordance with the judge’s ruling, DHS has suspended any and all actions implementing the affected sections of the Executive Order entitled, “Protecting the Nation from Foreign Terrorist Entry into the United States,” DHS said in a statement.

“DHS personnel will resume inspection of travelers in accordance with standard policy and procedure,” it stated, adding that the Justice Department would file an emergency stay to “defend the president’s executive order, which is lawful and appropriate.” The move came on the heels of the State Department announcing it was reversing the revocation of visas that left countless travelers stranded at airports last weekend. The move all but ensures a protracted public and legal battle over one of Trump’s most controversial policies, barely two weeks after he was inaugurated. Early Saturday morning, Trump criticised the ruling as “ridiculous” and warned of big trouble if a country could not control its borders.

Quite right. Putin bashing is a losing strategy.

• Trump Tells O’Reilly He ‘Respects’ Putin in Super Bowl Interview (Fox)

On Sunday, Bill O’Reilly will hold a special Super Bowl pre-game interview with President Trump at 4 p.m. ET on your local FOX broadcast station. In a special preview, Trump revealed his plans for dealing with Russian President Vladimir Putin. O’Reilly asked Trump whether he “respects” the former KGB agent: “I do respect him, but I respect a lot of people,” Trump said, “That doesn’t mean I’m going to get along with him.” Trump said he would appreciate any assistance from Russia in the fight against ISIS terrorists, adding that he would rather get along with the former Cold War-era foe than otherwise. “But, [Putin] is a killer,” O’Reilly said. “There are a lot of killers,” Trump responded, “We’ve got a lot of killers. What do you think? Our country’s so innocent?”

For the EU, like NATO, Putin bashing is the only thing left that provides a reason to be. That’s just dangerous.

• As Trump Weighs Thaw With Putin, EU Set to Renew Its Blacklist (BBG)

The European Union plans to renew asset freezes and travel bans against key allies of Russian President Vladimir Putin who are accused of destabilizing Ukraine, at a time when Donald Trump is weighing warmer ties with Moscow. Four EU officials said member governments intend by mid-March to prolong the sanctions for another six months on more than 100 Ukrainians and Russians. Among them: Arkady Rotenberg, co-owner of SMP Bank and InvestCapitalBank, and Yury Kovalchuk, the biggest shareholder in Bank Rossiya, the Brussels-based officials said. The officials spoke on condition of anonymity because the deliberations are confidential. Trump, who had a phone call with Putin on Jan. 28, has left open the possibility of easing the U.S.’s sanctions against Russia.

Former President Barack Obama drew up the American penalties in coordination with the 28-nation EU after Putin annexed the Ukrainian region of Crimea in 2014 and lent support to separatist rebels. “The Europeans are waiting to see what hand grenade Trump throws into the Russia-Ukraine pond,” Michael Emerson, a foreign-policy expert at the CEPS think tank in Brussels, said by phone. With the asset freezes and travel bans due to expire on March 15, “European politicians and diplomats will be cautious and stick to the status quo,” he said. The planned renewal of the blacklist highlights the EU’s political commitment to a policy that Angela Merkel and Francois Hollande guided in step with Obama. The European sanctions against Russia resemble the U.S. penalties and include a separate set of curbs – prolonged for another six months just before Trump took office on Jan. 20 – on Russia’s financial, energy and defense industries.

Volatility.

• Goldman Throws Cold Water On Trump Agenda (CNBC)

The policy halo effect that provided ballast to the stock market and fueled investor optimism is already being dimmed by political realities, according to Goldman Sachs, which may have negative implications for economic growth. In a note to clients on Friday, the investment bank noted President Donald Trump’s agenda was already running into bipartisan political resistance, with doubts growing about potential tax reform and a repeal of the Affordable Care Act, among other marquee Trump administration initiatives. Just two weeks into his tenure, “risks are less positively tilted than they appeared shortly after the election ,” Goldman wrote. Growing resistance to Trump’s executive orders on immigration and financial reform has galvanized opposition while dividing members of the president’s own Republican Party.

It has also curbed the enthusiasm of investors, who sent stocks on a roller-coaster ride this week as they struggled to reconcile the new restrictions on immigration with Trump’s professed pro-business bent. “While bipartisan cooperation looked possible on some issues following the election, the political environment appears to be as polarized as ever, suggesting that issues that require bipartisan support may be difficult to address,” the bank added. The balance of risks “are less positively tilted than they appeared shortly after the election,” Goldman said, which may blunt the force of future growth. Amid reports that top GOP members are reportedly becoming nervous about the impact of a full-fleged repeal of health care, that political pushback “does not bode well for reaching a quick agreement on tax reform or infrastructure funding, and reinforces our view that a fiscal boost, if it happens, is mostly a 2018 story.”

Steve on Twitter: “Coulnd’t resist it: sanctimonious carbon price pap, & belief market can solve an ecological problem just baug me. So my satirical gene fired.”

• Economists Say Action On Carbon Is Vital, Or Say Nothing At All (Age)

There is no consensus. Economists either believe it is vital that Australia becomes a low-carbon intensity economy, or that the issue is so unimportant – or perhaps that it is so politically divisive – that they choose not to volunteer an opinion. Asked about the importance of reducing the country’s carbon footprint and how best to do it, more than half of 27 economists from industry, consultancy, academia and finance questioned for the annual BusinessDay Scope survey agreed it was a must. Another 10 left the question blank. Whether this indicates a lack of interest or the contentious nature of climate change policy is unclear. But none of those who did answer made the case that cleaning up the economy did not matter. They overwhelmingly said action should be swift and include a market-based carbon pricing scheme.

[..] Steve Keen, of London’s Kingston University, made what – we think – was a similar point about the importance of climate action, albeit less conventionally. “Nah mate! Wassa matta, dontcha own a pair of budgie smugglers?” he wrote. “It’s all a conspiracy by Marxists anyway to undermine the Ostralyan way of life – you know, burning stuff and damn well enjoying it rather than whingeing. “A bit a coal never hurt anyone, matter of fact it tastes even better than a raw onion!”

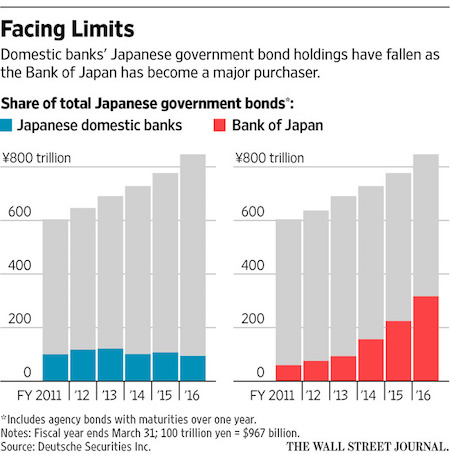

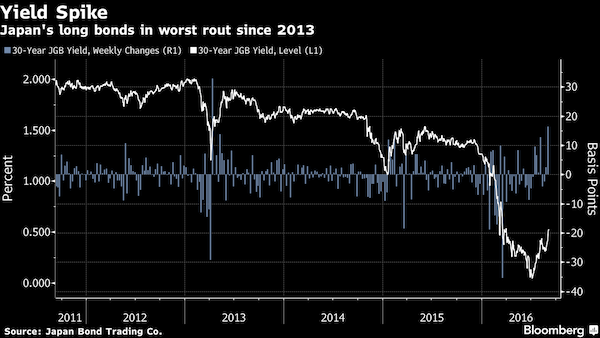

“I am shorting JGBs with both fists.”

• Japan – It’s Finally Happening (Muir)

I still shake my head at the stupidity. One of the most overindebted countries in the history of modern finance trading with a 0% thirty year bond. Professor Malkiel – stick that in your pipe and smoke it. But into that panic a crazy thing happened. Worried its bonds would trade at negative yields and pressure the financial system, the Bank of Japan pegged its 10 year yield at 0%. In doing so, the Bank of Japan moved from a set rate of balance sheet expansion to one that varies based on whether that peg is either too high, or too low. If the equilibrium level of 10 year rates was in fact below 0%, the Bank of Japan would be forced to sell bonds to keep rates stuck at 0%. If there was demand for credit and 10 year rates moved higher, then the BoJ would be forced to buy bonds to keep them from declining.

The BoJ program was a little more nuanced, and there were some caveats, but at its heart, the BoJ was giving up control of its balance sheet so it could peg a specific part of the yield curve. Of course Central Banks do this all the time. The difference is they usually operate at the front part of the curve, and when there is too much demand or supply, they change the rate. When the Bank of Japan took this unprecedented step, I walked away from my short JGB position. I figured there were better fixed income markets to short. Yet I highlighted that by pegging the 10 year rate, the Bank of Japan had not eliminated volatility, but merely postponed it. Eventually the Bank of Japan’s massive balance sheet expansion would kick in. At that point, inflation would pick up, credit would be demanded and the Bank of Japan would be forced to defend the 0% peg.

Yet this defending would be expansionary as they would be forced to buy bonds and expand the amount of base money, which if not offset with a decline in the velocity of money, would create more inflation, etc… All of this would be occurring with an already highly supercharged Japanese Central Bank balance sheet. I have been sitting and waiting for this expansionary feedback loop to kickstart. Until recently, the Bank of Japan had not been forced to buy any bonds to keep the rate pegged at 0%. When 10 year rates drifted far enough above 0%, the Bank of Japan made a bid to buy an unlimited number of bonds at a level below the market, which scared the market back to the pegged level. But this week the market decided to test the BoJ’s resolve.

The JGB 10 Year bond spiked through the previous high yield on news the Bank of Japan would not be expanding their balance sheet quite as aggressively as expected in their regular QE program. As yields popped through the previous 0.10% yield ceiling, the Bank of Japan came charging into the market. The BoJ bid 3-4 basis points through the market with unlimited size to push yields back down to the 0.10% level. What does this mean? The market is finally saying the demand for credit is enough to force the Bank of Japan to buy bonds to keep rates down. And that was the signal I was waiting for. I am shorting JGBs with both fists. It probably won’t happen tomorrow, nor the next day. Heck it probably won’t even happen next month, but we have reached the point where I need to be short JGBs.

The pressure will continue to build and when it finally bursts, the torrent will be overwhelming and quick. Although many traders think they will be able to climb on board, it will most likely be extremely difficult – like jumping on a raft bouncing down a raging river, it always seems way easier than it is. I hate German bunds, but I now have a fixed income instrument I hate even more. I expect bund yields to double or even triple in the coming quarters, but JGBs will eventually trade significantly though bunds. It would be just like the Market Gods to finally usher in the JGBs collapse once all the hedge fund guys had given up on it…

Count her out at your own peril.

• Le Pen Kicks Off Campaign With Promise Of French ‘Freedom’ (R.)

French far-right leader Marine Le Pen kicked off her presidential campaign on Saturday with a promise to shield voters from globalization and make their country “free”, hoping to profit from political turmoil to score a Donald Trump-style upset. Opinion polls see the 48-year old daughter of National Front (FN) founder Jean-Marie Le Pen topping the first round on April 23 but then losing the May 7 run-off to a mainstream candidate. But in the most unpredictable election race France has known in decades, the FN hopes the scandal hitting conservative candidate Francois Fillon and the rise of populism across the West will help convince voters to back Le Pen. “We were told Donald Trump would never win in the United States against the media, against the establishment, but he won… We were told Marine Le Pen would not win the presidential election, but on May 7 she will win!” Jean-Lin Lacapelle, a top FN official, told several hundred party officials and members.

In 144 “commitments” published at the start of a two-day rally in Lyon, Le Pen proposes leaving the euro zone, holding a referendum on EU membership, slapping taxes on imports and on the job contracts of foreigners, lowering the retirement age and increasing several welfare benefits while lowering income tax. The manifesto also foresees reserving certain rights now available to all residents, including free education, to French citizens only, hiring 15,000 police, curbing migration and leaving NATO’s integrated command. “The aim of this program is first of all to give France its freedom back and give the people a voice,” Le Pen said in the introduction to the manifesto.

[..] “This presidential election puts two opposite proposals,” Le Pen said in her manifesto. “The ‘globalist’ choice backed by all my opponents … and the ‘patriotic’ choice which I personify.” If elected, Le Pen says she would immediately seek an overhaul of the European Union that would reduce it to a very loose cooperative of nations with no single currency and no border-free area. If, as is likely, France’s EU partners refuse to agree to this, she would call a referendum to leave the bloc.

Horse barn.

• Theresa May Abandons ‘Home Owning Democracy’ of Thatcher and Tories (G.)

A major shift in Tory housing policy in favour of people who rent will be announced by ministers this week as Theresa May’s government admits that home ownership is now out of reach for millions of families. In a departure from her predecessor David Cameron, who focused on advancing Margaret Thatcher’s ambition for a “home-owning democracy”, a white paper will aim to deliver more affordable and secure rental deals, and threaten tougher action against rogue landlords, for the millions of families unable to buy because of sky-high property prices. Ministers will say they want to change planning and other rules to ensure developers provide a proportion of new homes for “affordable rent” instead of just insisting that they provide a quota of “affordable homes for sale”.

They will also announce incentives to encourage landlords to offer “family-friendly” guaranteed three-year tenancies, new action to ban unscrupulous landlords who offer sub-standard properties, and a further consultation on banning many of the fees that are charged by letting agents. A senior Whitehall source said: “We want to help renters get more choice, a better deal and more secure tenancies.” They added that the government did not want to scare people off from renting out homes, but offer incentives to encourage best practice and isolate the worst landlords. By emphasising the rights of renters, as well as trying to boost house building, the white paper will mark a turning point for a party that since the 1980s, and the first council house sales, has promoted home ownership as a badge of success, while neglecting the interests of renters.

The Tory manifesto for the 2015 general election spelt out plans for 200,000 new “starter homes” that could be bought by first-time buyers at 20% discounts, but said little about promoting the interests and improving the lot of so-called “generation rent”. Cameron also pushed the idea of getting people on the housing ladder through shared ownership schemes, an idea that is no longer such a priority. The white paper will be seen as part of May’s deliberate break with Cameron, and her drive to create a country “that works for everyone, not just the privileged few”.

Makes no difference anymore to Greece and Italy.

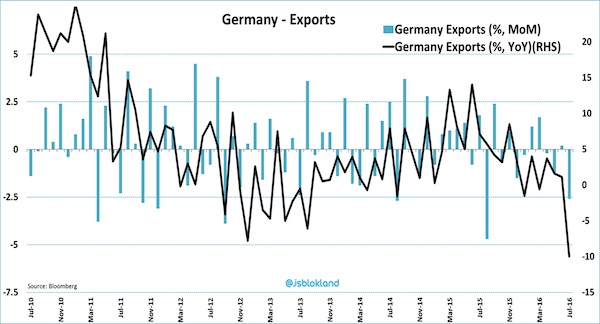

• Attention Trade Warriors: Germany’s Surplus is on the Wane (BBG)

The Trump administration appears intent on escalating the long-standing U.S. practice of attacking Germany’s current-account surplus. Good news for those on the receiving end: It has probably peaked. As officials like National Trade Council director Peter Navarro rail against the trade imbalance that dominates the balance of payments between the two countries, pensioners, home-buyers and immigrants are quietly working to bring that $297 billion current-account surplus down. According to research by Deutsche Bank, demographics and a housing boom are two factors that will drive the current account balance – the difference between what a country earns from abroad and what it spends – to its lowest level in seven years by 2020.

That may offer little consolation to the German delegation when it hosts a Group of 20 meeting of finance ministers in March, as they’ll likely face intensified criticism for allowing such an imbalance to continue. Germany has long faced flak, both within the euro area and outside it, for failing to encourage greater domestic spending and imports to balance out its external excess. Still, while the weaker euro will continue to make German exports attractive in the U.S. – think expensive sedans, high-tech machinery – there are countervailing factors at play on the other side of the equation. “In the medium term we expect the demographic development and the solid domestic economy, driven by a sustained positive development on the property market, to push the surplus down to 7 percent of GDP,” Deutsche Bank economist Heiko Peters said by phone.

A rising share of pensioners in the German population, who normally have less money to save than people in jobs, will crimp household savings rates, while an increasing number of immigrants such as refugees will contribute to boosting German imports, Peters wrote in a study first published last year. And with housing valuations outpacing income and rent growth since 2009, home owners feel richer, save less toward retirement and borrow against their property. That leads to rising imports of building materials to fuel the property boom and increased demand for foreign consumer goods on the back of the wealth effect. 7% of GDP is still a mighty big number for an economy as large as Germany’s. “That’s still a relatively high level until 2020,” Peters says. “But an even greater demographic effect is then expected for 2020-2025, and the surplus should then decline clearly further.”

Another ‘curious’ WaPo feat.

• Dennis Kucinich Rages Against The Military-Industrial-Complex (FB)

I have dedicated my life to peace. As a member of Congress I led efforts to avert conflict and end wars in countries such as Afghanistan, Iraq, Lebanon, Libya, Syria and Iran. And yet those of us who work for peace are put under false scrutiny to protect Washington’s war machine. Those who undermine our national security by promoting military attacks and destroying other nations are held up as national leaders to admire. Recently Rep. Tulsi Gabbard and I took a Congressional Ethics-approved fact finding trip to Lebanon and Syria, where we visited Aleppo and refugee camps, and met with religious leaders, governmental leaders and people from all sides of the conflict, including political opposition to the Syrian government.

Since that time we have been under constant attack on false grounds. The media and the war establishment are desperate to keep hold of their false narrative for world-wide war, interventionism and regime change, which is a profitable business for Washington insiders and which impoverishes our own country. Today, Rep. Gabbard came under attack yet again by the Washington Post’s Josh Rogin who has been on a tear trying to ruin the reputations of the people and the organization who sponsored our humanitarian, fact-finding mission of peace to the Middle East. Rogin just claimed in a tweet that as community organization I have been associated with for twenty years does not exist. The organization is in my neighborhood. Here’s photos I took yesterday of AACCESS-Ohio’s marquee.

It clearly exists, despite the base, condescending assertions of Mr. Rogin. Enough of this dangerous pettiness. Let’s dig in to what is really going on, inside Syria, in the State Department, the CIA and the Pentagon. In the words of President Eisenhower, let’s beware (and scrutinize) the military-industrial-complex. It is time to be vigilant for our democracy.

These leaders of the Christian faith in Aleppo begged for the US to stop funding terrorists in #Syria. They expressed that before international interventions (covert and overt) Syrians lived in peace without concern as to whether they were Christian, Muslim or Jew.

Line of the day: “Why are we spending £160bn on renewing Trident when we now know its missiles are more likely to hit Australia if they were aimed at Russia?..”

• NATO, Not Russia, Has Deployed Tanks To Poland & Baltic States – Galloway (RT)

British Defense Secretary speech on “Russian threat” is a desperate attempt to “save jobs and budgets” for the Cold War crowd, which is worried the new US leader will not consider Russia an enemy, broadcaster and former British MP George Galloway told RT. Addressing a group of university students, the UK’s defense secretary Michael Fallon warned of a resurgent Russia and said that it is becoming aggressive. RT: What did you make of Michael Fallon’s speech? George Galloway: Well, Michael Fallon puts the ‘squeak’ in the word ‘pipsqueak.’ He is of course the defense minister of a small and semi-detached European power with not much military prowess and which wants to feel big about itself.

And these people, and he’s not alone – the military industrial complex in the United States is up to the same game – they are desperately thrashing around to save their jobs, to save their budgets, to save their roles as muscle-men in the world. And Fallon got used to, as did other European powers, going around the world, threatening people with America’s army. Now America’s army is not quite so reliable, because America has a President who might not want to use the army in the way that these people want him to, at least one hopes not. And so they desperately seek to continually exacerbate the existing tensions with Russia to defend their own relevance. The people are asking, “What’s NATO for?”

The people are asking, “Why are we spending £160bn on renewing Trident when we now know its missiles are more likely to hit Australia if they were aimed at Russia? And in any case Russia has thousands of nuclear weapons, and we only a handful.” So it’s all pretty pitiful, actually. Right down to the audience of university students, hoping that none of them would challenge him. I’d like him to debate these matters with me, he knows me well, he comes from the same town in Scotland as me. I’d really love to get my metaphorical hands on him to have some of these matters out. The truth is that the European Union is having to come to terms with the fact that the US now has a President that doesn’t want war with Russia and they – who have built their entire 50-60 years of history on the possibility of war with Russia – are all at sea, except we don’t have that many battleships left either.

Greece turning into an impoverished prison camp is a feature not a bug.

• Varoufakis Calls on PM Tspiras to Ditch Bailout Restructuring (GR)

Yanis Varoufakis wrote in an op-ed in Efimerida ton Syntakton on Saturday. The former finance minister called on Prime Minister Alexis Tspiras to adopt a plan originally proposed by Varoufakis while he was still in office. The plan would unilaterally restructure the loans the ECB holds. In addition according to BitCoin Magazine and reiterated in the former FM’s op-ed a payment system that could operate in euros but which could be changed into drachmas “overnight” if necessary would be implemented along with a parallel payment system. “This two-pronged preparation is the only way to prevent another excruciating retreat by the prime minister in the short-term and [German Finance Minister Wolfgang] Schaeuble’s plan in the long-term,” Varoufakis wrote. Varoufakis has been a vocal protester to Greek bailout plans and restructuring as it stands now, hence his resignation. He firmly believes that the current plan could lead to Greece leaving the Eurozone of their own accord.

More on that. “In reality there was never a basis for hope that the toxic 3rd bailout would be gradually rationalized, in terms that the European Commission would support Athens so that the austerity and anti-social IMF measures would relax..”

• Varoufakis Urges Tsipras To Ditch Negotiations, Adopt “Parallel System” (KTG)

Former finance minister Yanis Varoufakis strikes back and urges Prime Minister Alexis Tsipras to turn his back on Greece’s lenders, adopt a parallel payment system and to unilaterally restructure the loans held by the ECB. In an op-ed in Efimerida ton Syntakton, Varoufakis, Varoufakis calls on Tispras to prepare for rupture with creditors in order to avoid rupture. “This two-pronged preparation is the only way to prevent another excruciating retreat by the prime minister in the short term and [German Finance Minister Wolfgang] Schaeuble’s plan in the long term,” Varoufakis wrote. In his article, Varoufakis suggested that Schaeuble’s strategy is to lead Greeks to the point of exhaustion so they ask to leave the euro themselves.

Noting that the “parallel payment system was already designed in 2014”, Varoufakis stresses that Tsipras had “two delusions” that led the government to the current impasse: A) that on the night of the referendum, the dilemma was between Schaeuble’s Grexit Plan and the 3rd bailout, and B) that the obedience to the 3rd bailout could be politically manageable through a parallel, society-friendly program. Both of these “working assumptions” were based only on autosuggestion, the ex finance minister stresses adding that he tried to explained this to the Prime Minister on the night of the referendum

“In reality there was never a basis for hope that the toxic 3rd bailout would be gradually rationalized, in terms that the European Commission would support Athens so that the austerity and anti-social IMF measures would relax, the IMF would force Berlin to accept debt restructuring and lower primary surpluses, the ECB would include Greece in the bond purchase program (QE),” Varoufakis wrote. He accused leading European negotiators of lying. “That Moscovici [EU Monetary Affairs Commissioner], Coerer [ECB] and Sapen [French finance minister] might have given such promises was not an excuse. Since May 2015 we were fully aware that these gentlemen know how to lie and fail to deliver on their promises when they do not lie.”

Completely devoid of any comprehension or compassion. Moral Bankruptcy. Throw money at it, that should work… And then keep bombing, British involvement in that makes a lot of profit.

• UK: Refugees Heading To Europe To Be Sent To Asia And Latin America (Ind.)

Refugees heading to Europe will be urged to settle in Asia and Latin America instead, under a new £30m British aid package. Theresa May announced the scheme at an EU summit in Malta, arguing it showed the Government is “stepping up its support for the most vulnerable refugees”. The package will see Britain provide lifesaving supplies for people facing freezing conditions across Eastern Europe and Greece, including warm clothing, shelter and medical care. However, it will also pay for better infrastructure in far-flung countries willing to take refugees who had hoped to settle in Europe. The move builds on an existing scheme run by The UN Refugee Agency (UNHCR), but it is the first time Britain’s aid budget has been used to bolster it. It risks adding to criticism that the Prime Minister is unwilling for the UK to accept a reasonable share of the refugees and migrants fleeing Syria and other war zones.

Only a few thousand Syrian refugees have been resettled in Britain – and the Government has refused to take part in an EU-wide programme to co-ordinate the continent’s response to the crisis. Government sources stressed that people would only be diverted to countries in Asia and Latin America if they were willing to be resettled there. The Department for International Development is expected to release a list of interested countries later. In Malta the Prime Minister insisted the focus of the £30m programme was “helping migrants return home rather than risk their lives continuing perilous journeys to Europe”. It would provide assistance to refugees and migrants across Greece, the Balkans, Libya, Egypt, Tunisia, Morocco, Algeria and Sudan. Priti Patel, the International Development Secretary, said: “Conflict, drought and political upheaval have fuelled protracted crises and driven mass migration. We cannot ignore these challenges.

The package will be delivered by UNHCR, the International Organisation for Migration (IOM) and NGO collective Start Network. Its aim is to:

* provide 22,400 life-saving relief items including tents, blankets, winter clothes such as hats and gloves and hygiene kits including mother and baby products

* help more than 60,000 people with emergency medical care, legal support and frontline workers to identify those at risk of violence and trafficking

* allow up to 22,000 people to reunite with family members they have become separated from

* help countries in Asia and Latin America that “might be able to resettle refugees put the infrastructure and systems in place to do so”

* provide more than 1,500 refugees in Egypt, including those fleeing Syria and other conflicts, with urgent health assistance and educational grants for students to go back to school

* provide a migrant centre in Sudan to enable “voluntary returns home when safe”, replicating a successful scheme in Niger.