How black would you like your Thanksgiving Friday slash weekend? Many Americans don’t even appreciate the term, or the events, at all anymore (or so they say), but the idea of getting what you don’t need, or want, on the cheap, will still prove irresistible. But then, when all of your desires have been fulfilled, food wise and gadget wise, and you’re still feeling empty, maybe we can help and offer a sweeping redefinition of the term Black Friday.

Since we live in times that see many other things on the verge of being sweepingly redefined, too, and imminently so, perhaps that’s only fitting. How about this, for starters? Black enough for you?

Turkish state media say six children have drowned when boats carrying migrants to Greece sank in two incidents off the Turkish coast. A wooden boat smuggling some 20 people to the island of Kos capsized in bad weather off the Aegean resort of Bodrum early on Friday. The state-run Anadolu Agency says most of the migrants made it to shore with the help of rescuers, but two sisters aged 4 and 1 drowned. Their nationalities were not immediately known. The agency says a second boat carrying as many as 55 migrants from Syria and Afghanistan sank hours later off the town of Ayvacik, further north. Four Afghan children drowned in that incident, Anadolu reported. Ayvacik is a main crossing point for migrants trying to reach the island of Lesvos.

Or have we already all gotten too blasé about those dead babies by now? They’ve been washing up on those beaches for half a year or so, after all. How about those who survive the seas, and then get stuck behind a razor wire fence halfway to their preferred destinations?

Remember the men who had sewn their lips shut? Not even that is enough for more than a few hours of media attention anymore. Not nearly as much as being suspected of terrorism; that sells much better than desperation. So, presumably, will being in the way of goods of ‘important’ companies like Sony and HP’s goods reaching their destination, even if you can’t reach yours. Life is all about priorities.

A protest by migrants on Greece’s border with the Former Yugoslav Republic of Macedonia (FYROM) is putting railway operator Trainose at risk of losing major international clients. Migrants have over the last few days been protesting FYROM’s decision not to let them cross from Greece. Many migrants have camped on the railway lines connecting the two countries, which means that no trains have come in or out of Greece for the last week. This means that the freight Trainose is responsible for carrying has not been able to reach its destinations. The railway company serves major international clients such as Hewlett Packard and Sony.

Is there a better way to sum it up than this sign at the Greece/FYROM (Macedonia) border? We doubt it.

Or perhaps there is a better way after all. The absolute cluelessness of Europe’s ‘leaders’. Here’s a brilliant example of the gap between them and the real world:

The EU risks suffering the same fate as the Roman empire if it does not regain control of its borders and stop the “massive influx” of refugees from the Middle East and central Asia, the Dutch prime minister has warned. Mark Rutte, whose government assumes the EU’s rotating presidency in January, said southern EU countries had yet to implement policies agreed to stem the flow [..] Mr Rutte said Greece, where more than 700,000 have landed this year, might have to increase its “reception capacity” to at least 100,000. Athens has so far committed to about half that, insisting that it does not want to become a giant refugee camp.

“As we all know from the Roman empire, big empires go down if the borders are not well-protected”, said Mr Rutte in an interview with a group of international newspapers. “So we really have an imperative that it is handled.” [..] Mr Rutte said the EU needed to act quickly to stem the migrant flow, adding that he was optimistic that Sunday’s summit in Brussels between President Recep Tayyip Erdogan of Turkey and EU leaders would help ease conditions by providing €3 billion to improve refugee camps in Turkey and disrupting the “business model” of human smugglers channelling migrants in boats to Greece.

It’s all still about ‘stemming the flow’. Actually, it’s more about that by the day, and that’s precisely because ‘stemming the flow’ doesn’t work. The idea is that the Greeks do more .. yeah, what exactly? Tell dinghies loaded with desperate refugee families, half of whom suffer from hypothermia, that they should turn around? What, to get back to Turkey? So Turkey can send them back to Syria?

That’s just nonsense, of course, the product of malfunctioning neurons. Then again, there’s too much of those going around Europe to mention. The above quote is more remarkable for a few other things. First, to claim that the Roman empire went down because it didn’t protect its borders is so contentious no serious historian would want to claim it as his/her own.

And that’s without asking how the Romans should have implemented that protection. Second, say we take Mr. Rutte’s assertion at face value, then the only peoples those borders should have been protected from, the ones who actually sacked Rome, were the Barbarians. Rutte, ergo, compares the Syrian refugees to Barbarians. And that doesn’t look all that smart.

And now that the article mentions Erdogan, and the €3 billion he’s been promised by Europe, as well as the fast track route into EU membership, let’s see what he has to contribute to Black Weekend.

First off, he had two prominent journalists arrested on espionage and related charges for publishing an article way back in May about his own secret service people smuggling arms across Turkey’s border with Syria. And Brussels is going to reward this interpretation of ‘freedom of the press’ with €3 billion?

Then of course he had a Russian jet shot down this week, maybe just as a patsy to the US -or others-, maybe to avenge Russian bombs falling on transports such as that conducted by those same secret services, or oil deliveries from ISIS managed by his son. That’s Erdogan’s Thanksgiving Turkey: Arms out, oil in.

What should be clear is that shooting down a Russian plane, and under questionable pretext to boot, is not done. Whether you do it to please someone else or just yourself. Turkey will lose a lot more than those €3 billion in tourism and trade with Russia once Putin gets on Erdogan’s case for real (and Russia will not forgive this no matter what other policies need attention), so Brussels can figure out where the money will go. Russian tourism in Turkey alone brings in $2.7 billion a year. And it’s been halted.

Turkey claims it gave 10 warnings to a plane that might have been in its airspace for 17 seconds (a highly contested claim), only to shoot it in Syrian airspace?! It claims it hadn’t recognized the plane as being Russian? Since they apparently fire at anything that moves, what do we think would have happened if this had been an American plane? Or a French one? There doesn’t seem to be anything Turkey has said about the incident that rings true.

But then, that’s the case for so many things so many people say. In the meantime, our morality -let alone the high ground- is washing up on Greek beaches with those babies whose lives our societies don’t deem worth saving, the lives we judge to be not worthy of living.

Our honesty, our sense of fairness, our decency, basically all things that various prophets have proclaimed are the most important qualities in life, are washing up lifeless on cold deserted patches of sand. And ‘we’ are seeking to further vilify Russia and tempt it into acts we ‘must’ respond to. We are aligning ourselves to that end with Erdogan and Saudi Arabia, the main supporters of those we claim in public to be at war with.

Here’s how this works: If the end justifies the means, and we make sure there never is an end to this, then arms will continue to be traded, profits will continue to be made, and lies will be told till no-one can tell up from down, since all means are justified until the end of time.

That this leaves us morally utterly rudderless then becomes just another one of those justified means. Anything goes.

The US E&P sector could be on the cusp of massive defaults and bankruptcies so staggering they pose a serious threat to the US economy. Without higher oil and gas prices – which few experts foresee in the near future – an over-leveraged, under-hedged US E&P industry faces a truly grim 2016. How bad could things get and when? It increasingly looks like a number of the weakest companies will run out of financial stamina in the first half of next year, and with every dollar of income going to service debt at many heavily leveraged independents, there are waves of others that also face serious trouble if the lower-for-longer oil price scenario extends further.

“I could see a wave of defaults and bankruptcies on the scale of the telecoms, which triggered the 2001 recession,” Timothy Smith, president of consultancy Petro Lucrum, told a Platts energy conference in Houston last week. Much has been made about the resiliency of US oil production in the face of low prices, but the truth is that many producers are maximizing their output — even unprofitable volumes — because they need the cash flow to service their debt (related). “As an industry, we’re at the point where every dollar of free cash flow now goes to paying back debt,” Angle Capital’s Steve Ilkay told the same conference. Ilkay, who advises North American producers on asset management, said during the boom years of 2012-14 about 55% of the sector’s free cash flow, which is calculated by subtracting capital expenditures from operating cash flow, was allocated toward debt repayment.

With West Texas Intermediate (WTI) stuck below $50 per barrel since August – and closer to $40 recently – the industry has responded with deeper cuts to capex and a greater focus on efficiency. However, experts say this won’t be enough to avoid a bloody reckoning with persistent low oil and gas prices, as the sector grapples with some $200 billion-plus in high-yield debt, which it absorbed to finance the shale oil boom. Credit quality has been steadily deteriorating since June 2014, when WTI peaked at $108/bbl. Standard and Poor’s says there have been 19 defaults so far in 2015 across the US oil and gas industry, while another 15 companies have filed for bankruptcy. Besides those that have missed interest or principal payments, the default category also includes companies that have entered into “distressed exchanges” with their creditors, including Halcon, SandRidge, Midstates, Goodrich, Warren, Exco, Venoco and Energy XXI.

Of the 153 oil and gas companies that S&P applies credit ratings to, roughly two-thirds are E&P firms. Among these E&Ps, 77% now have high-yield or “junk” ratings of BB+ or lower. 63% are rated B+ or worse, and 31% – or 51 companies – are rated below B-. What does this all mean in layman’s terms? “Quite frankly it’s a lot of gloom and doom,” says Thomas Watters, managing director of S&P’s oil and gas ratings. “I lose sleep over what could unfold.” He says companies with ratings of B- or below are “on life support,” while those further down the ratings scale at C+ or lower are “maybe looking at a year, year-and-a-half before they default or file for bankruptcy.”

America’s annual Black Friday shopping extravaganza was short on fireworks this year as U.S. retailers’ discounts on electronics, clothing and other holiday gifts failed to draw big crowds to stores and shopping malls. Major retail stocks including Best Buy and Wal-Mart closed lower while Target, picked out by one analyst for its promotion strategy, saw its shares tick up. Bargain hunters found relatively little competition compared with previous years. Some had already shopped Thursday evening, reflecting a new normal of U.S. holiday shopping, where stores open up with deals on Thanksgiving itself, rather than waiting until Black Friday. Retailers “have taken the sense of urgency out for consumers by spreading their promotions throughout the year and what we are seeing is a result of that,” said Jeff Simpson, director of the retail practice at Deloitte.

Traffic in stores was light on Friday, while Thursday missed his expectations, he said. As much as 20% of holiday shopping is expected to be done over the Thanksgiving weekend this year, analysts said. But the four days are not considered a strong indicator for the entire season. A slow start last year led to deeper promotions and a shopping rush in the final ten days of December. Steve Bratspies, chief merchandising officer at Wal-Mart, told Reuters he was not surprised that a store would see thinner crowds on Friday after it kicked off Black Friday deals on Thursday night. Suntrust Robinson Humphrey analysts were more blunt, calling Thursday a “bust”. “Members of our team who went to the malls first had no problem finding parking or navigating stores,” he wrote in a note.

One popular delusion that won’t seem to go away is the notion that policy makers can stimulate robust economic growth by setting interest rates artificially low. The general theory is that cheap credit compels individuals and businesses to borrow more and consume more. efore you know it, the good times are here again. Profits increase. Jobs are created. Wages rise. A new cycle of expansion takes root. These are the supposed benefits to an economy that central bankers can impart with just a little extra liquidity. Unfortunately, this policy antidote doesn’t always work out in practice. Certainly cheap credit can have a stimulative influence on an economy with moderate debt levels. But once an economy has reached total debt saturation, where new debt fails to produce new growth, the cheap credit trick no longer works to stimulate the economy.

In fact, the additional credit, and its counterpart debt, actually strangles future growth. Present monetary policy has landed the economy at the unfavorable place where more and more digital monetary credits are needed each month just to stand still. After seven years of ZIRP, financial markets have been distorted to the point where a zero bound federal funds rate has become restrictive. At the same time, applications of additional debt only serve to further the economy’s ultimate demise. The fundamental fact is that the current financial and economic paradigm, characterized by heavy handed Federal Reserve intervention into credit markets, is dying. Debt based stimulus is both sustaining and killing the economy at the same time. No doubt, this is a strange situation that has developed.

The American student loan crisis is often seen as a problem of profligacy and predation. Wasteful colleges raise tuition every year, we are told, even as middle-class wages stagnate and unscrupulous for-profit colleges bilk the unwary. The result is mounting unmanageable debt. There is much truth in this diagnosis. But it does not explain the plight of Liz Kelley, a Missouri high school teacher and mother of four who made a series of unremarkable decisions about college and borrowing. She now owes the federal government $410,000, and counting. This is a staggering and unusual sum. The average undergraduate who borrows leaves school with about $30,000 in debt. But Ms. Kelley’s circumstances are not unique.

Of the 43.3 million borrowers with outstanding federal student loans, 1.8%, or 779,000 people, owe $150,000 or more. And 346,000 owe more than $200,000. Ms. Kelley’s debt woes are also mostly a matter of interest, not principal, a growing problem for the nation’s student debtors. According to the Federal Reserve Bank of New York, the number of active borrowers enrolled in college has declined to roughly nine million today from about 12 million in 2010. Yet the total amount of outstanding debt continues to increase, because many borrowers are not paying back their older loans. This is partly a function of continuing economic hardship. But it also reflects how the federal government has become the biggest, nicest and meanest student lender in the world.

China’s stocks tumbled the most since the depths of a $5 trillion plunge in August as some of the nation’s largest brokerages disclosed regulatory probes, industrial profits fell and two more companies said they’re struggling to repay bonds. The Shanghai Composite Index sank 5.5%, with a gauge of volatility surging from the lowest level since March. Citic Securities and Guosen Securities plunged by the daily limit in Shanghai after saying they were under investigation for alleged rule violations. The probe into the finance industry comes as the government widens an anti-corruption campaign and seeks to assign blame for the selloff earlier this year. Authorities are testing the strength of a nascent bull market by lifting a freeze on initial public offerings and scrapping a rule requiring brokerages to hold net-long positions, just as the earliest indicators for November signal a deterioration in economic growth.

A Chinese fertilizer maker and a pig iron producer became the latest companies to flag debt troubles after at least six defaults this year. “The sharp decline will raise questions whether the authorities’ confidence that we are seeing stability in the Chinese markets may be a tad premature,” said Bernard Aw, a strategist at IG Asia in Singapore. “The rally since the August collapse was not fundamentally supported. The removal of restrictions for large brokers to sell and the IPO resumptions may not have been announced at an opportune time.” Friday’s losses pared the Shanghai Composite’s gain since its Aug. 26 low to 17%. The Hang Seng China Enterprises Index slid 2.5% in Hong Kong. The Hang Seng Index retreated 1.9%. A gauge of financial shares on the CSI 300 slumped 5%. Citic Securities and Guosen Securities both dropped 10%. Haitong International Securities slid 7.5% for the biggest decline since Aug. 24 in Hong Kong.

Half of the gold coming from mines may not be viable at current prices, underscoring the industry’s need for consolidation and output cuts, according to the best-performing producer of the metal in the past decade. “The more we continue to produce unprofitable gold, the more pressure we put on the gold price,” Randgold Resources CEO Mark Bristow said in Toronto on Friday. “In the medium term, it’s a very bullish outlook for the gold industry. The question is, how long are we going to supply it with unprofitable gold?” Gold fell to a five-year low on Friday as a rising dollar and speculation that U.S. policy makers will boost interest rates next month curbed the appeal of bullion as a store of value. While industrial metal producers have promised output cuts, “we don’t have that psyche in the gold industry, we just send it off our mine and somebody buys it,” Bristow said.

Gold miners buffeted by the drop in prices are shortening the life of mines by focusing only on the best quality ore, a practice known as high grading, which will restrict future output and support higher prices, according to Bristow. He said in a presentation to bankers in Toronto that the industry life span is down to about five years because companies have been aggressively high grading at the expense of future production. “The industry has moved away from looking at optimal life of mines because everyone is trying to demonstrate short-term delivery,” he said in the interview after the presentation. “Where is all this value that people promised in the gold industry? It’s not there.”

The whistleblower who exposed wrongdoing at HSBC’s Swiss private bank has been sentenced to five years in prison by a Swiss court. Hervé Falciani, a former IT worker, was convicted in his absence for the biggest leak in banking history. He is currently living in France, where he sought refuge from Swiss justice, and did not attend the trial. The leak of secret bank account details formed the basis of revelations – by the Guardian, the BBC, Le Monde and other media outlets – which showed that HSBC’s Swiss banking arm turned a blind eye to illegal activities of arms dealers and helped wealthy people evade taxes. While working on the database of HSBC’s Swiss private bank, Falciani downloaded the details of about 130,000 holders of secret Swiss accounts. The information was handed to French investigators in December 2008 and then circulated to other European governments.

It was used to prosecute tax evaders including Arlette Ricci, the heir to France’s Nina Ricci perfume empire, and to pursue Emilio Botín, the late chairman of Spain’s Santander bank. Switzerland’s federal prosecutor had requested a record six-year term for Falciani for aggravated industrial espionage, data theft and violation of commercial and banking secrecy. It was the longest sentence ever demanded by the confederation’s public ministry in a case of banking data theft. The trial was also the first conducted by the country’s federal criminal court in which the accused had not been present. The defendant’s lawyers had demanded a reduced sentence, of between two and three years, “compatible with the granting of a reprieve”.

Falciani himself refused to appear in the dock, on the grounds that he would not be allowed a fair trial. He described the process as a “parody of justice”. [..] Falciani’s lawyer, Marc Henzelin, pointed out that his client was on trial at a time when Switzerland was in the process of dismantling its banking secrecy practices with proposals for new laws that would pave the way for automatic information exchange about offshore accounts held in Switzerland. In fact, Switzerland announced on 4 November that the country’s finance ministry temporarily shelved the plans for reform. “It is not Falciani who is being judged. It is the court. It is Switzerland,” said Henzelin.

The New York Stock Exchange is delisting American depositary receipts of National Bank of Greece SA after they lost 91% of their value this year. The ADRs were suspended on Friday, when their value slumped to 16 cents from as much as $1.96 in February. NYSE cited an “abnormally low” price in a statement. Losses spiraled to a record this month, after the Greek lender sold new shares at a more than 90% discount to market prices. The nation’s four largest banks have been raising capital to help fill a €14.4 hole in their accounts identified by the European Central Bank. National Bank of Greece has the right to appeal the decision to a committee of the board of directors of NYSE. The stock in Athens closed at a record low of 8 euro cents, taking its weekly slump to 64%.

“What is unsettling is that the organisers are from the three areas of the world where there seems to be, among scientists at least, the most enthusiasm for going forward.”

The question could hardly be more profound. Having stumbled upon a simple means to make precise changes to the code of life, should humans take control of their genetic fate, and rewrite the DNA of future generations? Once an idea explored only in fiction, the prospect is now a real one. The inexorable rise of gene editing has put the technology in labs across the globe. The first experiments on human embryos have been done, in a bid to correct faulty genes that cause disease. To thrash out an answer, or at least find common ground, an international group of experts will descend on Washington DC next week for a three day summit. Convened with some urgency by the US, UK and Chinese national academies, the meeting is billed as a “global discussion”. It is a chance to take stock of a revolutionary technology that has the power to do good, and the potential to wreak havoc.

“This new technology for gene editing, that is, selectively inserting and removing genes from an organism’s DNA, is spreading around the world,” says Ralph Cicerone, president of the US National Academy of Sciences, where the summit will take place. With the number of experiments ballooning, the uses and risks the technology brings must be worked through now, he adds. The last time scientists met like this was in 1975, when it became clear that the DNA from one species could be spliced into another. One experiment underway at the time aimed to put DNA from a cancer-causing monkey virus into bacteria that infect humans. The potential for disaster led to a meeting in Asilomar, California, to agree and make public fresh safeguards for the experiments.

Jennifer Doudna, an inventor of a gene editing tool called Crispr-Cas9, said Asilomar was much in mind when the summit was organised. “I think it’s this generation’s version of Asilomar,” she says. “It’s a very exciting time, but as with any powerful technology, there is always the risk that something will be done either intentionally or unintentionally that somehow has ill effects.” [..] Marcy Darnovsky, director of the Center for Genetics and Society, and a speaker at the summit, said that the meeting could make a real contribution to the debate, but needed to be far more inclusive. “What is unsettling is that the organisers are from the three areas of the world where there seems to be, among scientists at least, the most enthusiasm for going forward.”

Darnovsky wants a total ban on editing human embryos that are destined to become people. “It’s way too risky and it’s likely to remain that way,” she says. If editing was allowed to prevent diseases being passed on, it would quickly lead to designer babies, she argues. “People say it is a slippery slope. I don’t call that a slippery slope, I call that jumping off a cliff,” she says. “We would be well on the way to a world in which people who could afford to do so would attempt to give their children the best start in life, and competitive and commercial pressures would kick in. We’d end up in a world of genetic haves and have-nots, and risk introducing new kinds of inequality when we already have shamefully way too much.”

In Chinese mythology, the Monkey King is a beast with magical fur. All he has to do is pull out a hair, blow on it and it is instantly transformed into a clone of himself. Xu Xiaochun, chief executive of BoyaLife, says the fable is not far from reality, as far as his Chinese biotechnology company is concerned. This week he announced an investment of $31m in a joint venture with South Korea’s Sooam Biotech that aims to clone 1m cows a year from their hair cells. The Monkey King “sounds like a fairy tale but we are really doing the same thing”, he says. “We pull out 200 hairs, blow on them — and boom!” Sometime next year, researchers in BoyaLife’s laboratory on the outskirts of the coastal city of Tianjin will take skin cells from a few carefully chosen cattle (Kobe beef is Mr Xu’s favourite).

The scientists will extract the nucleus from each cell and place it into an unfertilised egg from another cow. The cloned embryos will then be implanted in surrogate dairy cows housed on cattle ranches throughout China. His ambition is staggering. Starting with 100,000 cloned cattle embryos a year in “phase one”, Mr Xu envisages 1 million annually at some point in the future. That would make BoyaLife by far the largest clone factory in the world. Mr Xu says the latest techniques enable cloning to be carried out in an “assembly line format” at a rate of less than 1 minute per cell. Based on a four- hour shift and 250 working days a year, a proficient cloner would “manufacture” 60,000 cloned cow embryos a year, he says, adding that a team of 50 will be sufficient for the planned scale of the project. Mr Xu plans to have a staff of 300 and eventual total investment is estimated at $500m.

If the venture comes anywhere near achieving its goal, it will be another example of the recent surge of path-breaking, taboo-busting biotechnology research, with China introducing mass production and commercialisation of projects that are still in the experimental and clinical stages elsewhere. China’s flag-bearer in biotech is BGI, formerly known as Beijing Genomics Institute and now based in Shenzhen. BGI has grown into the world’s biggest genomics organisation, with a huge capacity to read, analyse and alter DNA from plants, microbes, people and animals. It employs more than 2,000 PhD-level scientists and 200 top-of-the-range gene-sequencing machines. In September BGI captured the public imagination with an announcement that “micropigs”, originally developed for biomedical research through gene editing and cloning, would be sold as pets.

Count Russian reserves as another casualty of income inequality that Thomas Piketty believes is reshaping the world’s biggest economies. Russia, which is struggling to rebuild holdings depleted during last year’s currency crisis, has missed out on building a bigger stockpile in the past 15 years by failing to create a more transparent financial system to ease inequality and distribute the spoils of a boom in commodities prices, said Piketty, the author of the bestselling “Capital in the 21st Century.” Jailing “a couple of billionaires from time to time” is no way to address the challenge, the French economist said in an interview in Moscow on Thursday. “In the long term, Russia should have much more reserves, given the level of its trade surplus,” he said.

“It’s important to realize that Russia is being stolen money from, by capital flight and by the fact that billionaires and millionaires outside Russia and sometimes inside Russia are able to benefit from natural resources of Russia much more than they should.” Piketty, 44, who gave a lecture at the Higher School of Economics in Moscow, may already be preaching to the converted. The government is looking to wring greater revenue from the energy industry with a tax increase, while the Bank of Russia has set a target of about $500 billion for reserves after burning through a fifth of its holdings to prop up the ruble last year. Vladimir Putin, in power for 16 years as premier or president, has backed efforts to repatriate as much as $1 trillion in capital held by companies and high-ranking officials abroad as part of what he’s called the “de-offshorization” of the economy.

Putin, who introduced a 13% flat income tax rate in 2001, has also seen top ministers broach the subject of re-instituting a progressive tax system. The current income levy is “relatively small” in a country with “a lot of inequality” and “far too little transparency,” Piketty said. “Russia would be in a much better situation today if this reform for more transparency, progressive taxation would have been conducted before,” Piketty said. “It’s time, especially in the current crisis, to change course and to deal with inequality and transparency in a much more front-faced way.”

The debate is gaining urgency after the government allowed household finances to bear the brunt of the country’s first recession in six years, putting Russia on track for the biggest drop in consumption during Putin’s rule. This year, 21.7 million people, or about 15% of the population, are living beneath the subsistence level, according to the Federal Statistics Service. The crisis marks the “first significant” increase in Russia’s poverty since the crisis in 1998-1999, according to the World Bank.

Over the course of the last four or so weeks, the media has paid quite a bit of attention to Islamic State’s lucrative trade in “stolen” crude. On November 16, in a highly publicized effort, US warplanes destroyed 116 ISIS oil trucks in Syria. 45 minutes prior, leaflets were dropped advising drivers (who Washington is absolutely sure are not ISIS members themselves) to “get out of [their] trucks and run away.” The peculiar thing about the US strikes is that it took The Pentagon nearly 14 months to figure out that the most effective way to cripple Islamic State’s oil trade is to bomb… the oil. Prior to November, the US “strategy” revolved around bombing the group’s oil infrastructure.

As it turns out, that strategy was minimally effective at best and it’s not entirely clear that an effort was made to inform The White House, Congress, and/or the public about just how little damage the airstrikes were actually inflicting. There are two possible explanations as to why Centcom may have sought to make it sound as though the campaign was going better than it actually was, i) national intelligence director James Clapper pulled a Dick Cheney and pressured Maj. Gen. Steven Grove into delivering upbeat assessments, or ii) The Pentagon and the CIA were content with ineffectual bombing runs because intelligence officials were keen on keeping Islamic State’s oil revenue flowing so the group could continue to operate as a major destabilizing element vis-a-vis the Assad regime.

Ultimately, Russia cried foul at the perceived ease with which ISIS transported its illegal oil and once it became clear that Moscow was set to hit the group’s oil convoys, the US was left with virtually no choice but to go along for the ride. Washington’s warplanes destroyed another 280 trucks earlier this week. Russia claims to have vaporized more than 1,000 transport vehicles in November. Of course the most intriguing questions when it comes to Islamic State’s $400 million+ per year oil business, are: where does this oil end up and who is facilitating delivery?

Turkish President Tayyip Erdogan warned Russia on Friday not to “play with fire”, citing reports Turkish businessmen had been detained in Russia, while Moscow said it would suspend visa-free travel with Turkey. Relations between the former Cold War antagonists are at their lowest in recent memory after Turkey shot down a Russian jet near the Syrian border on Tuesday. Russia has threatened economic retaliation, a response Erdogan has dismissed as emotional and indecorous. The incident has proved a distraction for the West, which is looking to build support for the U.S.-led fight against Islamic State in Syria. The nearly five-year-old Syrian civil war has been complicated by Russian air strikes in defense of President Bashar al-Assad.

Turkey, which has long sought Assad’s ouster, has extensive trade ties with Moscow, which could come under strain. Erdogan condemned reports that some Turkish businessmen had been detained for visa irregularities while attending a trade fair in Russia. “It is playing with fire to go as far as mistreating our citizens who have gone to Russia,” Erdogan told supporters during a speech in Bayburt, in northeast Turkey. “We really attach a lot of importance to our relations with Russia … We don’t want these relations to suffer harm in any way.” He said he may speak with Russian President Vladimir Putin at a climate summit in Paris next week. Putin has so far refused to contact Erdogan because Ankara does not want to apologize for the downing of the jet, a Putin aide said.

Erdogan has said Turkey deserves the apology because its air space was violated. Russian Foreign Minister Sergei Lavrov said on Friday Moscow would suspend its visa-free regime with Turkey as of Jan. 1, which could affect Turkey’s tourism industry. Turkey’s seaside resorts are among the most popular holiday destinations for Russians, who make up Turkey’s largest number of tourist arrivals after Germany. An association of Russian defense factories, which includes the producers of Kalashnikov rifles, Armata tanks and Book missile systems, has recommended its members suspend buying materials from Turkey, according to a letter seen by Reuters. That could damage contracts worth hundreds of millions of dollars. Russia’s agriculture ministry has already increased checks on food and agriculture imports from Turkey, in one of the first public moves to curb trade.

Russia may resume visa-free travel with Turkey if Ankara stops helping the Islamic State terrorists, the head of the State Duma’s international affairs committee said on Friday. Russia has decided to suspend the visa-free regime with Turkey from the January 1, 2016, Foreign Minister Sergei Lavrov said on Friday after a meeting with his Syrian counterpart Walid Muallem in Moscow. “Relations between Russia and Turkey are the main factor here… If Ankara continues its de-facto support for ISIL militants, provides them with everything they need and endorses their actions in Syria, then we will not be able to restore the visa-free regime,” Alexei Pushkov said at a news briefing in Moscow.

Driving the Islamic State militants out of the territories they now control in Iraq and Syria would help lessen the threat they pose to the rest of the world. Destroying the ISIL headquarters would facilitate our joint fight against the terrorist threat, Pushkov added. “The terrorists use Turkish territory as a transit zone to bring reinforcements and arms to the conflict zone in Syria. Some of these militants may be sent to carry out terrorist attacks here in Russia, so our decision to suspend the visa-free regime with Turkey will help keep them out. This is exactly what the French did after the Paris attacks and the EU is now considering a closure of its external borders in the face of the terrorist threat,” Pushkov noted.

European and Turkish officials are working to smooth out their remaining differences on an agreement to help stem flows of migrants to Europe, which they hope will be signed on Sunday by European Union leaders and Turkey’s prime minister. Turkish President Tayyip Erdogan broadly accepted a proposed action plan last month, under which the EU would provide €3 billion in aid for the 2.3 million Syrian refugees in Turkey. It will also “re-energize” talks on Ankara’s joining the bloc and ease visas for Turks visiting Europe. But diplomats and officials said on Friday that differences remained on just what Turkey would commit to do in return – and when – to prevent migrants from making the short but risky crossing to Greek islands and to accept the return of people who reach the EU but fail to qualify for asylum.

German Chancellor Angela Merkel, a driving force behind seeking Turkish help in easing the refugee crisis, has faced criticism from EU allies for encouraging Erdogan to increase his demands. A senior German official stressed on Friday that Ankara also had much to gain from greater cooperation. Bolstered by the victory of his AK party in a parliamentary election early this month, Erdogan re-appointed Prime Minister Ahmet Davutoglu and, EU officials and diplomats say, Turkey is now driving a hard bargain – notably seeking 3 billion euros per year instead of the EU offer of the same amount over two.

“There are things that can still go wrong. It’s not a simple negotiation. Among the 28 member states, there are different sensibilities about Turkey, then with Turkey itself a dialogue needs to be found,” a senior EU official said on Friday. “It’s always possible there won’t be an agreement.” A diplomat in Ankara said: “Turkey is pushing its luck. They’re asking for a lot and the atmospherics aren’t good. “At the same time, there are a lot of important actors within Europe that have a soft spot for Turkey and really want to find ways of taking the relationship forward.”

A protest by migrants on Greece’s border with the Former Yugoslav Republic of Macedonia (FYROM) is putting railway operator Trainose at risk of losing major international clients. Migrants have over the last few days been protesting FYROM’s decision not to let them cross from Greece. Many migrants have camped on the railway lines connecting the two countries, which means that no trains have come in or out of Greece for the last week. This means that the freight Trainose is responsible for carrying has not been able to reach its destinations. The railway company serves major international clients such as Hewlett Packard and Sony.

There is concern that if the protest does not end soon, these companies will be forced to transport their goods by road. “The issue is not paying compensation to the companies, which we can pay even if the situation is not our fault,” said Trainose CEO Thanasis Ziliaskopoulos. “What is more important is that the country’s credibility is at stake.” Trainose’s contract with Chinese giant Cosco to transport goods that arrive at Piraeus port is seen as a key part of the goal to make Greece a logistics hub in Southeastern Europe.

Turkish state media say six children have drowned when boats carrying migrants to Greece sank in two incidents off the Turkish coast. A wooden boat smuggling some 20 people to the island of Kos capsized in bad weather off the Aegean resort of Bodrum early on Friday. The state-run Anadolu Agency says most of the migrants made it to shore with the help of rescuers, but two sisters aged 4 and 1 drowned. Their nationalities were not immediately known. The agency says a second boat carrying as many as 55 migrants from Syria and Afghanistan sank hours later off the town of Ayvacik, further north. Four Afghan children drowned in that incident, Anadolu reported. Ayvacik is a main crossing point for migrants trying to reach the island of Lesvos.

European banks are sitting on bad debts of €1tn – the equivalent to the GDP of Spain – which is holding back their profitability and ability to lend to high street customers and businesses. According to a detailed analysis of 105 banks across 21 countries in the European Union conducted by the European Banking Authority (EBA), the experience of Europe’s banks to troubled customers is worse than that of their counterparts in the US. The €1tn (£706bn) of so-called non-performing loans amount to almost 6% of the total loans and advances of Europe’s banks, and 10% when lending to other financial institutions are excluded. The equivalent figure for the US banking industry is around 3%.

Piers Haben, director of oversight at the EBA, said that while the resilience of the financial sector was improving because more capital was being accumulated in banks, he remained concerned about bad debts. “EU banks will need to continue addressing the level of non-performing loans which remain a drag on profitability,” Haben said. Banks in Cyprus have half their lending classified as non-performing while in the UK the figure is 2.8%. Capital ratios – a closely watched measure of financial strength – had reached 12.8% by June 2015, well above the regulatory minimum, as banks held on to profits and also took steps to raise capital – for instance, by tapping shareholders for cash. In 2011 the figure was 9.7%.

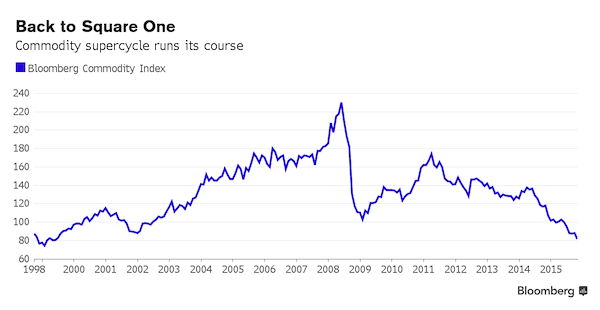

For commodities, it’s like the 21st century never happened. The last time the Bloomberg Commodity Index of investor returns was this low, Apple’s best-selling product was a desktop computer, and you could pay for it with francs and deutsche marks. The gauge tracking the performance of 22 natural resources has plunged two-thirds from its peak, to the lowest level since 1999. That shows it’s back to square one for the so-called commodity super cycle, a hunger for coal, oil and metals from Chinese manufacturers that powered a bull market for about a decade until 2011. “In China, you had 1.3 billion people industrializing – something on that scale has never been seen before,” said Andrew Lapping, deputy chief investment officer at Allan Gray Ltd., a manager of $33 billion of assets in Cape Town.

“But there’s just no way that can continue indefinitely. You can only consume so much.” If slowing Chinese growth, now headed for its weakest pace in 25 years, put the first nail in the coffin of the super cycle, the Federal Reserve is about to hammer in the last. The first U.S. interest rate increase since 2006 is expected next month by a majority of investors, helping push the dollar up by about 9% against a basket of 10 major currencies this year. That only adds to the woes of commodities, mostly priced in dollars, by cutting the spending power of global raw-materials buyers and making other assets that generate yields such as bonds and equities more attractive for investors.

The Bloomberg Commodity Index takes into account roll costs and gains in investing in futures markets to reflect the actual returns. By comparison, a spot index that tracks raw materials prices fell to a more than six-year low Monday, and a gauge of industry shares to the weakest since 2008 on Sept. 29. The biggest decliners in the mining index, which is down 31% this year, are copper producers First Quantum Minerals, Glencore and Freeport-McMoran. With record demand through the 2000s, commodity producers such as Total SA, Rio Tinto Group and Anglo American Plc invested billions in long-term capital projects that have left the world awash with oil, natural gas, iron ore and copper just as Chinese growth wanes. “Without fail, every single industrial commodity company allocated capital horrendously over the last 10 years,” Lapping said.

Oil is among the most oversupplied. Even as prices sank 60% from June 2014, stockpiles have swollen to an all-time high of almost 3 billion barrels. That’s due to record output in the U.S. and a decision by OPEC to keep pumping above its target of 30 million barrels a day to maintain market share and squeeze out higher-cost producers. A Fed move on rates and accompanying gains in the dollar will make it harder to mop up excesses in raw-materials supply. Mining and drilling costs often paid in other currencies will shrink relative to the dollars earned from selling oil and metals in global markets as the U.S. exchange rate appreciates. Russia’s ruble is down more than 30% against the dollar in the past year, helping to maintain the profitability of the country’s steel and nickel producers and allowing them to maintain output levels.

“..not only affecting our business in China but also in the other international operation markets outside of China because these economies are so dependent on China..”

You wouldn’t know it from looking at stocks, but the US manufacturing sector came darn close to contracting in October. Readings above 50 indicate expansion in the ISM gauge of manufacturing activity, and the October reading of 50.1 was the lowest in 29 months. Overall manufacturing activity has expanded for 34 straight months, but the pace of growth in the main ISM gauge has deteriorated for four consecutive months. There is reason for optimism. Factories saw new orders come in at a faster pace and production was strong. But, other than that, the ISM details were far from impressive. Not surprisingly, the prices paid index came in below 40 for the third consecutive month, reflecting the deflationary headwinds flowing through the economy.

More importantly, the employment details showed a sharp contraction, down to 47.6 versus 50.5 in September. The market is more concerned about non-farm payroll figures, but this sure seems to be a leading indicator, especially when you consider the weakness from September’s NFP report. It’s the same story in Germany, where mechanical engineering orders slumped 13% Y/Y in September, hit by an 18% drop in foreign demand. In a sign that the weakness in September wasn’t just a blip, foreign orders from outside the eurozone were down 7% in the nine months through September from the same period a year earlier, hit by a slowdown in developing economies that account for around 42% of Germany’s plant and machinery exports. It’s clear that most of this industrial weakness is being driven by China.

Domestic orders for Germany’s mechanical engineering industry were up 2% in the nine months through September from the same period a year ago, while eurozone demand rose 13% over this period. European demand looks ok, it’s just not strong enough to offset the weakness driven by China. German car maker Audi said Monday that falling Chinese demand is forcing it to slash production of Audi models at a plant in Changchun nearly 11%. General Motors Chief Executive Mary Barra last month said the slowdown in China, the world’s second-largest economy, “is not only affecting our business in China but also in the other international operation markets outside of China because these economies are so dependent on China.”

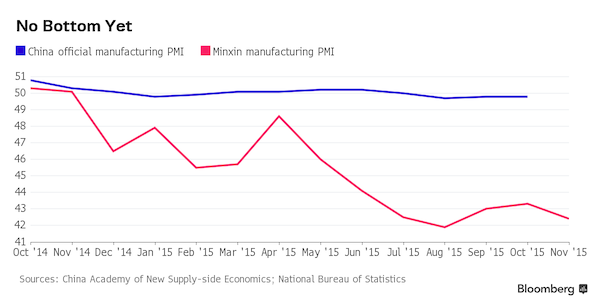

China’s economy is still showing a muted response to waves of monetary and fiscal easing as of the half-way mark for the last quarter of the year, some of the earliest indicators suggest. A privately compiled purchasing managers’ index and a gauge based on search engine interest in small and medium-sized businesses deteriorated this month, while a sentiment indicator dropped sharply from October. Combined, the reports make gloomy reading ahead of official releases, the earliest of which will be manufacturing and services PMI reports due Dec. 1. Six interest-rate cuts in a year and expedited fiscal spending have yet to revive growth as overcapacity and weakness in old drivers like manufacturing and residential construction weigh on the world’s second-biggest economy. If official data confirm the sluggishness, Premier Li Keqiang’s growth goal may be missed for a second-straight year.

Here’s a look at what the economy’s earliest tea leaves show: The unofficial purchasing managers indexes for manufacturing and services sectors both declined, snapping increases in the two previous months. The manufacturing PMI declined to 42.4 in November from 43.3 in October, while the non-manufacturing reading fell to 42.9 from 44.2, according to reports jointly compiled by China Minsheng Banking and the China Academy of New Supply-side Economics. Numbers below 50 signal deteriorating conditions. “China’s economy hasn’t bottomed yet and downward pressures are mounting,” Jia Kang, director of the Beijing-based academy and former head of the finance ministry’s research institute, wrote. “We expect authorities to step up growth stabilization measures.” The Minxin PMIs are based on a monthly survey covering more than 4,000 companies, about 70% of which are smaller enterprises. The private gauges have shown a more volatile picture than the official PMIs in the past year.

Iron ore has taken a fresh beating, with prices sinking to the lowest level in six years as output cuts at Chinese mills hurt demand while low-cost supplies from the biggest miners expand. It may get worse. “The key problem for iron ore is oversupply: the iron ore heavyweights have overestimated China’s appetite,” Gavin Wendt, founding director at MineLife in Sydney, said after prices dropped on Tuesday to the lowest level since daily data began in 2009. “Further price weakness is inevitable.” The commodity has been hurt this year by increasing output from the biggest miners including BHP Billiton, Rio Tinto and Vale and faltering demand for steel in China, where mills account for half of global output. Goldman Sachs said last week that the global market is oversupplied, with steel consumption in China remaining weak. Mills are battling sinking prices that have eroded profit margins.

“We’re going through a very difficult time,” said Philip Kirchlechner, director of Iron Ore Research. “It was always expected that it would come down to the $40s again, but not over a sustained period,” said Kirchlechner, former head of marketing at Fortescue Metals Group Ltd. Ore with 62% content delivered to Qingdao fell 1.9% to $43.89 a dry metric ton on Tuesday, according to Metal Bulletin Ltd. The commodity is headed for a third annual retreat, and the latest fall eclipsed the previous low of $44.59 set in July. The steel industry in China is reaching a critical point, according to Andy Xie, an independent economist who’s been bearish for years and sees a drop below $40 before year-end. Mills will have to cut production, said Xie, a former Asia-Pacific chief economist at Morgan Stanley. Crude-steel output in China will drop 23 million tons to 783 million tons next year, according to the China Iron & Steel Association.

Last month, the nation’s leading industry group reported wider losses and noted that while official interest rates in China have been cut, mills faced higher funding costs. The biggest miners are betting that higher production will enable them to cut costs and raise market share while less efficient suppliers get squeezed. Rio’s Andrew Harding, chief executive officer for iron ore and Australia, said this month the company will keep defending market share and if it cut output, volumes would simply be taken by less efficient rivals. Kirchlechner said that the onset of winter in China may bring something of a reprieve for prices as local ore producers are forced to curtail supplies, spurring increased demand for cargoes from overseas.

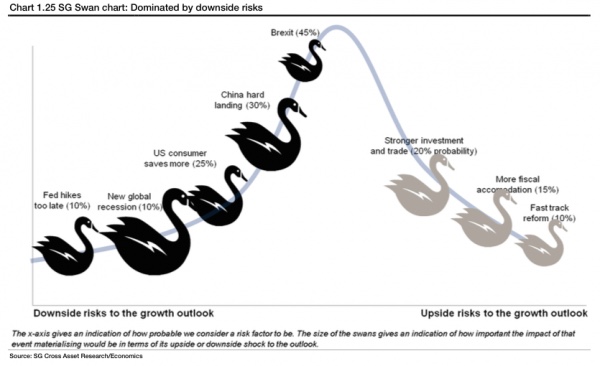

In its latest quarterly Global Economic Outlook, SocGen takes a look at five political and economic black swans that could touch down in 2016 and also warns that “high levels of public sector debt, already overburdened monetary policy, still high debt stocks and on-going balance sheet clean ups in a number of economies leave the global economy will a low level of ammunition to deal with new shocks.” Here’s the latest SG “swan chart” which is “dominated by downside risks”:

As we and a bevy of others have pointed out, QE is bumping up against the law of diminishing returns and it’s no longer clear that doubling and tripling down on monetization will do anything at all to boost aggregate demand, juice global trade, or raise inflation expectations (but what it surely will do is continue to inflate asset bubbles). In this environment, fiscal stimulus may be the only “solution.” As SocGen puts it, “in the event of a major new significant shock, our baseline scenario remains that both the US and Europe would opt first for further monetary policy stimulus. Later on, however, as this proves inefficient, we would expect fiscal stimulus to be considered.” China, of course, has already gone this route, boosting fiscal spending by 36% in Ocotber as the country’s credit impulse disappeared despite six rate cuts in less than a year. From SocGen:

• Brexit at a probability of 45%, remains our highest probability risk. At this time, a date has yet to be set for the referendum but 3Q16 seems a likely timing, based on the idea that Prime Minister Cameron will want to hold the referendum within a reasonable timeframe on concluding an agreement with his EU partners (which could come as early as the December 2015 Summit, but more likely in March 2016).

• China hard landing remains a significant risk at 30%. Medium-term, we set an even higher probability of 40% on a lost decade scenario. As opposed to a hard landing, however, such a risk scenario would manifest itself only gradually. The most likely trigger for a China hard- landing is policy error with miscalculation of how much financial risk management or structural reform the system can absorb. We identify three main triggers. In practice, a combination thereof seems the most likely cause of such a risk scenario.

• Credit crunch: An intensification of capital outflows, a growing number of non-performing loans and an insufficient response from the PBoC could result in a credit crunch. Such risks could be further exacerbated by pressure coming from Chinese corporations’ foreign exchange denominated debt and overall high level of leverage.

• Dry-up in housing demand: Should a new housing shock emerge, triggering a buyers strike, then real estate developers (also burdened with foreign currency loans) could suffer renewed stress, triggering a significant scaling back of investment.

• Capacity overhang: The still-large excess capacity in the manufacturing sector would be further exacerbated in such a scenario, weighing on corporate margins and profits. The risk is to see bankruptcies and unemployment increase in such a bleak scenario.

One by one, the giant investment funds are quietly switching out of government bonds, the most overpriced assets on the planet. Nobody wants to be caught flat-footed if the latest surge in the global money supply finally catches fire and ignites reflation, closing the chapter on our strange Lost Decade of secular stagnation. The Norwegian Pension Fund, the world’s top sovereign wealth fund, is rotating a chunk of its $860bn of assets into property in London, Paris, Berlin, Milan, New York, San Francisco and now Tokyo and East Asia. “Every real estate investment deal we do is funded by sales of government bonds,” says Yngve Slyngstad, the chief executive. It already owns part of the Quadrant 3 building on Regent Street, and bought the Pollen Estate – along with Saville Row – from the Church Commissioners last year. But this is just a nibble.

The fund is eyeing a 15pc weighting in property, an inflation-hedge if ever there was one. The Swiss bank UBS – an even bigger player with $2 trillion under management – has issued its own gentle warning on bonds as the US Federal Reserve prepares to kick off the first global tightening cycle since 2004. UBS expects five rate rises by the end of next year, 60 points more than futures contracts, and enough to rattle debt markets still priced for an Ice Age. Mark Haefele, the bank’s investment guru, said his clients are growing wary of bonds but do not know where to park their money instead. The UBS bubble index of global property is already flashing multiple alerts, with Hong Kong off the charts and London now so expensive that it takes a skilled worker 14 years to buy a broom cupboard of 60 square metres.

Mr Haefele says equities are the lesser risk, especially in Japan, where the central bank has bought 54pc of the entire market for exchange-traded funds (ETFs) and is itching to go further. As of late November, roughly $6 trillion of government debt was trading at negative interest rates, led by the Swiss two-year bond at -1.046pc. The German two-year Bund is at -0.4pc. The Germans and Czechs are negative all the way out to six years, the Dutch to five, the French to four and the Irish to three. Bank of America says $17 trillion of bonds are trading at yields below 1pc, including most of the Japanese sovereign debt market. This is a remarkable phenomenon given that global core inflation – as measured by Henderson Global Investor’s G7 and E7 composite – has been rising since late 2014 and is now at a seven-year high of 2.7pc.

In the eurozone, the M1 money supply is rising at a blistering pace of 11.9pc. A case can be made that the ECB should go for broke, deliberately stoking a short-term monetary boom to achieve “escape velocity” once and for all. The risk of a Japanese trap is not to be taken lightly. Yet even those who feared looming deflation in Europe two years ago are beginning to wonder whether the bank is losing the plot. If the ECB doubles down next week with more quantitative easing and a cut in the deposit rate to -0.3pc, as expected, it will validate the iron law that central banks are pro-cyclical recidivists, always and everywhere behind the curve. Caution is in order. The investment graveyard is littered with the fund managers who bet against Japanese bonds, only to see the 10-year yield keep falling for two decades, plumbing new depths of 0.24pc this January.

Some Turkish officials have ‘direct financial interest’ in the oil trade with the terrorist group Islamic State, Russian PM Dmitry Medvedev said as he detailed possible Russian retaliation to Turkey’s downing of a Russian warplane in Syria on Tuesday. “Turkey’s actions are de facto protection of Islamic State,” Medvedev said, calling the group formerly known as ISIS by its new name. “This is no surprise, considering the information we have about direct financial interest of some Turkish officials relating to the supply of oil products refined by plants controlled by ISIS.” “The reckless and criminal actions of the Turkish authorities… have caused a dangerous escalation of relations between Russia and NATO, which cannot be justified by any interest, including protection of state borders,” Medvedev said.

According to Medvedev, Russia is considering canceling several important projects with Turkey and barring Turkish companies from the Russian market. Russia has already recommended its citizens not to go Turkey citing terrorist threats, which have resulted in several tourist operators withdrawing tours to Turkey from the market. Russia may further scrap a gas pipeline project, aimed at turning Turkey into a major transit country for Russian natural gas going to Europe, and the construction of the country’s first nuclear power plant. Turkey shot down a Russian bomber over Syria on Tuesday, claiming it had violated Turkish airspace. Russia says no violation took place and considers the hostile act as ‘a stab in the back’ and direct assistance to terrorist forces in Syria.

Russia is prepared to coordinate strikes against Islamic State militants in a joint command with the United States, France and others who want to participate, including Turkey, Moscow’s envoy to Paris said on Wednesday. French President Francois Hollande is trying to rally more international support to destroy Islamic State following the Nov. 13 attacks in Paris. He visited Washington on Tuesday and is due to meet Russian President Vladimir Putin on Thursday. “This coalition is a possibility,” Russia’s ambassador to France, Alexandre Orlov, told Europe 1 radio. “For our part, we are prepared to go further, to plan strikes against Daesh (Islamic State) positions together and to set up a joint command with France, America and any country that wants to join this coalition,” he said, noting that this included Turkey.

Volkswagen is facing a new criminal investigation after publishing incorrect emissions data that gave some drivers tax breaks that may have been unjustified. Prosecutors in Braunschweig, already looking into Volkswagen diesels, are now formally examining tax issues linked to faulty carbon-dioxide readings as well, spokesman Klaus Ziehe said by phone Tuesday. A separate probe was necessary because the accusations involve other cars and other people, he said. Five suspects are being investigated, Ziehe said, without identifying them. “German prosecutors like these kinds of investigations,” said Michael Kubiciel, a criminal law professor at the University of Cologne. “It’s easier to pursue charges under German tax law than under environmental protection rules.”

Volkswagen has said the people who bought the cars won’t have to pay the difference in taxes. The bill adds to the mounting tab of recall costs and regulatory fines the carmaker faces over irregular and falsified vehicle emissions, a scandal that began more than two months ago with Volkswagen’s admission to rigging diesel engines in 11 million vehicles worldwide. The CO2 issue arose Nov. 3, after the automaker said about 800,000 cars, mostly in Europe, had emissions of the greenhouse gas that didn’t match up with the levels promised. That matters because CO2 is a key measure for setting tax rates for motor vehicles in many European countries. Improperly labeled cars with higher-than-marketed emissions may lead authorities to reclaim the tax breaks.

Volkswagen estimated the financial risk of manipulating the ratings at about €2 billion. That sum includes paying governments for missing tax revenue. The carmaker already set aside €6.7 billion in the third quarter to fix diesel cars with engine software that allowed them to pass emission tests by illegally restricting pollution during testing. European regulators have approved Volkswagen’s proposals for how to repair about 70% of the diesel engines affected worldwide, Chief Executive Officer Matthias Mueller told a gathering of executives in Wolfsburg, Germany, on Monday. Meanwhile, Volkswagen’s Audi division will resubmit a revised version of software that the EPA and California Air Resources Board has targeted in its latest probe. If approved, the fix for 85,000 Audi, Volkswagen and Porsche cars with 3.0-liter diesel engines should cost roughly €50 million. EPA and CARB will review and test the revised software.

I think that today we will say farewell to all that made the UK a compassionate, decent, fair and civilised society. After George Osborne has had his way I have a deeply uncomfortable feeling that this country will be more brutal, unequal, divided and profoundly individualistic. Once Margaret Thatcher said there was no such thing as society. Today I feel like George Osborne is trying to prove it. Tax is not going to be the focus of today, I suspect. It should be: if George Osborne wants to pursue the goal of a balanced budget (which has no economic merit, at all) then tackling the tax gap and cutting tax expenditures would be the obvious thing to do and that would deliver increased economic fairness and social justice. But those will not be at the heart of today.

Today is about shrinking the state. Apart from the economic illiteracy of this (at the macro level cutting government spending is the same as cutting GDP if there is spare capacity in the economy, and so the policy Osborne is pursuing makes it harder for him to achieve his goal) there is the massive social injustice that this entails to worry about. Social inequality will increase as a result of today. The disabled will be worse off again. The young will suffer disproportionately. The education of many will be harmed. Our long term prospects will be reduced. Those in need of care will have less available. Society will be more vulnerable. And yes, some will die as a result of today. That has to be said.

Those are all choices. And none of them is necessary. The policy of austerity is a political affectation designed to increase the wealth of a few, to favour large companies and to appease bankers. It cannot work, although I think George Osborne does not realise that although the evidence is obvious. And so the question as to why it has been adopted has to be asked. And that comes down to greed, a sense of entitlement, a lack of empathy, and a blunt indifference to others.

Bank of England policymakers may need to take action to prevent a risky consumer borrowing binge as the economy recovers, the bank’s chief economist has warned. Appearing before the cross-party Treasury select committee alongside the Bank’s governor, Mark Carney, Andy Haldane warned that consumer credit, in particular personal loans, had been “picking up at a rate of knots. That ultimately might be an issue that the financial policy committee [FPC] might want to look at fairly carefully.” The Financial Policy Committee (FPC), created after the financial crisis, is meant to prevent a future crash by allowing the Bank to take action in particular markets without using the blunter tool of interest rates. Chaired by the governor, it has 10 members – but does not include Haldane.

The FPC has already stepped in to constrain mortgage lending but its powers to confront a credit bubble are untested. The latest data from the Bank showed the rate of growth of consumer credit picking up sharply. Andrew Tyrie, the Conservative MP who chairs the Treasury select committee, said: “The FPC has huge new powers which only small numbers of the public have so far been aware of, and it is particularly important that we hold them accountable. Many of these decisions were formerly the preserve of politicians.” Carney told MPs he was limited as to how much he could say about the FPC, as he was in “purdah”, as its next meeting approached; but he confirmed the rapid pace of credit growth was something it might need to look at.

He added that the separate monetary policy committee (MPC), which sets interest rates, has to take into account the historically high debt levels of Britain’s households as it made interest rate decisions. “Without question, more indebted households are more vulnerable,” he said. “The pressure on households because of the debt burden is significant. There is less margin for error.”

We can have it all: that is the promise of our age. We can own every gadget we are capable of imagining – and quite a few that we are not. We can live like monarchs without compromising the Earth’s capacity to sustain us. The promise that makes all this possible is that as economies develop, they become more efficient in their use of resources. In other words, they decouple. There are two kinds of decoupling: relative and absolute. Relative decoupling means using less stuff with every unit of economic growth; absolute decoupling means a total reduction in the use of resources, even though the economy continues to grow. Almost all economists believe that decoupling – relative or absolute – is an inexorable feature of economic growth. On this notion rests the concept of sustainable development.

It sits at the heart of the climate talks in Paris next month and of every other summit on environmental issues. But it appears to be unfounded. A paper published earlier this year in Proceedings of the National Academy of Sciences proposes that even the relative decoupling we claim to have achieved is an artefact of false accounting. It points out that governments and economists have measured our impacts in a way that seems irrational. Here’s how the false accounting works. It takes the raw materials we extract in our own countries, adds them to our imports of stuff from other countries, then subtracts our exports, to end up with something called “domestic material consumption”. But by measuring only the products shifted from one nation to another, rather than the raw materials needed to create those products, it greatly underestimates the total use of resources by the rich nations.

For instance, if ores are mined and processed at home, these raw materials, as well as the machinery and infrastructure used to make finished metal, are included in the domestic material consumption accounts. But if we buy a metal product from abroad, only the weight of the metal is counted. So as mining and manufacturing shift from countries such as the UK and the US to countries like China and India, the rich nations appear to be using fewer resources. A more rational measure, called the material footprint, includes all the raw materials an economy uses, wherever they happen to be extracted. When these are taken into account, the apparent improvements in efficiency disappear. In the UK, for instance, the absolute decoupling that the domestic material consumption accounts appear to show is replaced with an entirely different chart.

Not only is there no absolute decoupling; there is no relative decoupling either. In fact, until the financial crisis in 2007, the graph was heading in the opposite direction: even relative to the rise in our gross domestic product, our economy was becoming less efficient in its use of materials. Against all predictions, a recoupling was taking place. While the OECD has claimed that the richest countries have halved the intensity with which they use resources, the new analysis suggests that in the EU, the US, Japan and the other rich nations, there have been “no improvements in resource productivity at all”. This is astonishing news. It appears to makes a nonsense of everything we have been told about the trajectory of our environmental impacts.

A report published on Tuesday by Concord, the European NGO confederation for relief and development, documents an emerging trend among member states to divert aid budgets from sustainable development to domestic costs associated with hosting refugees and asylum seekers. Some of the expenditure items EU countries report as aid do not translate into a real transfer of resources to developing countries or, ultimately, to people who are poor and marginalised, the report has found. This is not the first time that NGOs have reported that EU monies are increasingly being spent on tackling the refugee crisis and border security, rather than fighting poverty and inequality.

But this time the Concord AidWatch report contains data from the OECD CRS dataset complemented by updated national figures. In some cases, data from the European commission and Eurostat is also used. Concord says that some EU countries are misreporting some of their official development assistance (ODA) expenses by including costs which, under existing guidelines, should not have been counted. The reporting of non-eligible migration-related expenses in Spain and Malta, or the misreporting of refugee costs in Hungary, are among the examples cited. Inflated aid is calculated on the bilateral component of EU aid. Many of the components – imputed student costs, refugee costs, interest and tied aid – do not apply to multilateral aid.

The report found that in 2014, the EU28 and the European institutions inflated their aid by €7.1bn, which represents 12% of all aid flows. Some countries inflate aid more than others. While the percentage of inflated aid for Luxembourg is estimated at 0.3% of the country s total aid, and at 0.5% for the UK, it is, in contrast, 50.6% for Malta, 30.9% for Austria and 27.2% for Portugal. The EU institutions are no different from the member states, having ‘inflated’ their aid by 9.9%.

The number of refugees arriving in the European Union from violence-scarred regions of the Middle East and Africa is set to fall in November as traveling conditions worsen and member states looked to strengthen the bloc’s external borders. The number of migrants crossing the Mediterranean Sea to reach the EU this month fell to 116,579 through Nov. 23 compared with a record 220,535 in October, according to the United Nations refugee agency. The deepening chaos in nations from Libya to Syria has spawned an unprecedented wave of more than 860,000 people seeking shelter within the EU this year. The influx opened divisions within the bloc as German Chancellor Angela Merkel insisted Europe must honor its asylum commitments while other leaders such as Hungary’s Viktor Orban complained of the strain on their communities.

The pressure on Merkel increased this month when jihadists who attacked restaurants and a music venue in Paris. At least two of the assailants are thought to have entered the EU as refugees. On Friday EU nations agreed to bolster controls on frontiers around the bloc. They agreed to start carrying out systematic registration, including fingerprinting of all migrants entering into the Schengen area. All travelers will have their passports checked when they arrive in Europe, extending the full-blown screening that is currently limited to non-EU passport holders. The number of people entering Hungary slowed to a trickle this month after Orban closed the country’s border with Croatia on Oct. 18. Austria overtook Croatia as the nation with most arrivals during the first two weeks of November as the number of people embarking on the journey to Europe declined.

After a brief dip in the number of refugees and migrants arriving on Greece’s eastern Aegean islands, an increase was noted on Tuesday in the quantity of boats reaching Greek shores from Turkey. The uptick came a day ahead of Frontex’s management board meeting in Warsaw on Wednesday, when it is expected that the European Union border agency will decide to move its operational office from Piraeus. The office has been located in the port city since 2010 and its removal would be seen as a diplomatic blow for Greece, especially given the current flow of refugees to the country. More than 60 dinghies carrying migrants arrived on Lesvos on Tuesday as Alternate Foreign Minister Nikos Xydakis and Immigration Policy Minister Yiannis Mouzalas guided the ambassadors of European Union countries around the island so they could get a closeup view of the impact of the refugee crisis.

Greece has been under pressure to improve the registration process for arrivals and Lesvos is expected to host a so-called hotspot at the Moria camp, where authorities are hoping to register between 1,000 and 1,500 people a day. Police officials said they expect the hotspot to be ready in less than two weeks. The recent letup in the number of people reaching Lesvos allowed authorities in Athens, where migrants are transferred, to empty the sports hall in Galatsi, which is being used for temporary shelter, and move everyone to the Tae Kwon Do Stadium in Faliro. Tuesday’s arrivals on Lesvos included a yacht carrying 140 migrants who had each paid around 3,000 euros to travel from Turkey in its relative safety. Two bodies also washed up in the island pn Tuesday.

Greece has so far this year spent more than €800,000 in healthcare for about 2,000 migrants and refugees, according to data from the Health Ministry. According to the data, which were presented by General Secretary for Public Health Yiannis Baskozos during a conference of the World Health Organization (WHO) in Rome on Tuesday, demand for the EKAV emergency medical assistance service has increased by 42% compared to 2014. Ambulance calls doubled between June – November – when the refugee crisis peaked – over the same period last year. “[Greece] has managed to fulfill the current healthcare needs for refugees and migrants notwithstanding the absence of EU funding,” Baskozos told the conference.

The collapse in oil prices following the shale revolution has stolen the limelight for investors mulling the end of the commodities supercycle. But the real “poster child for problems in commodities markets is perhaps the global steel industry,” according to Macquarie analysts led by Colin Hamilton, the firm’s global head of commodities research. The front-month contract for U.S. hot-rolled coil steel futures traded on the New York Mercantile Exchange is down nearly 40% year-over-year/ Forecasts for a boom in Chinese consumption helped spur a rise in production that left the segment with a massive glut. The successful realization of economic rebalancing in China, meanwhile, necessarily entails a material slowdown in that nation’s demand for steel. Macquarie observes that global steel consumption has contracted on an annual basis throughout 2015.

“With 1.6 billion tonnes of consumption globally, steel remains the lynchpin of industrial growth,” wrote Hamilton. “However, the growth part of this equation is an increasing problem, and not only in China.” India, which has the potential to buoy demand for steel, is also contributing significantly to supply growth. Bloomberg Intelligence’s Yi Zhu notes that 37 million metric tons of production capacity in India are currently under construction or in planning to be added. “The only people who still seem to think there is significant upside in global steel consumption akin to the past decade are the major iron ore producers—for example BHP’s belief global steel consumption will hit 2.5 billion tonnes by 2030—just a further 50% upside required there!” Hamilton wrote in a separate note.