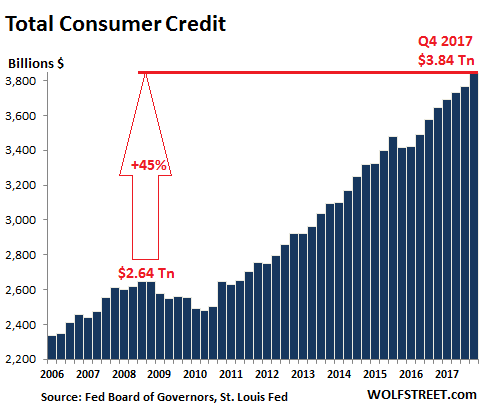

Total consumer credit rose 5.4% in the fourth quarter, year over year, to a record $3.84 trillion not seasonally adjusted, according to the Federal Reserve. This includes credit-card debt, auto loans, and student loans, but not mortgage-related debt. December had been somewhat of a disappointment for those that want consumers to drown in debt, but the prior months, starting in Q4 2016, had seen blistering surges of consumer debt. Think what you will of the election – consumers celebrated it or bemoaned it the American way: by piling on debt. The chart below shows the progression of consumer debt since 2006 (not seasonally adjusted). Note the slight dip after the Financial Crisis, as consumers deleveraged – with much of the deleveraging being accomplished by defaulting on those debts. But it didn’t last long. And consumer debt has surged since. It’s now 45% higher than it had been in Q4 2008. Food for thought: Over the period, the consumer price index increased 17.5%:

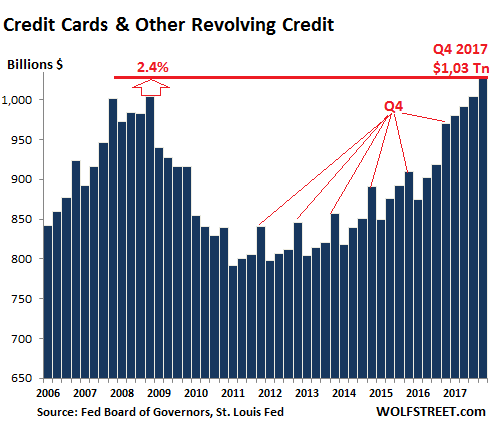

Credit card debt and other revolving credit in Q4 rose 6% year-over-year to $1.027 trillion, a blistering pace, but it was down from the 9.2% surge in Q3, the nearly 10% surge in Q2, and the dizzying 12% surge in Q1. So the growth of credit card debt in Q4 was somewhat of a disappointment for those wanting to see consumers drown in expensive debt. The chart below shows the leap of the past four quarters over prior years. This pushed credit card debt in Q3 and Q4 finally over the prior record set in Q4 2008 ($1.004 trillion), before it came tumbling down via said “deleveraging.” These are not seasonally adjusted numbers, and you can see the seasonal surges in credit card debt every Q4 during shopping season (as marked), and the drop afterwards in Q1. But then came 2017. In Q1 2017, credit card debt skyrocketed to an even higher level than Q4, when it should have normally plunged – a phenomenon I have not seen before.

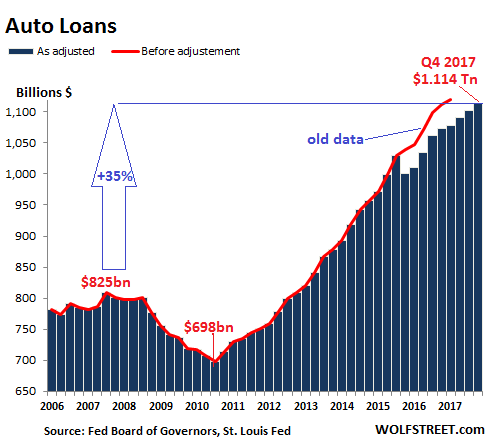

This shows what kind of credit-card party 2017 and Q4 2016 was. Over the four quarter period, Americans added $58 billion to their credit card debt. Over the five-quarter period, they added $109 billion, or 12%! Celebration or retail therapy. Auto loans rose 3.8% in Q4 year-over-year to $1.114 trillion. It was one of the puniest increases since the auto crisis had ended in 2011. Since then, the year-over-year increases were mostly in the 6% to 9% range. These are loans and leases for new and used vehicles. So the weakness in new-vehicle sales volume in 2017 was covered up by price increases in both new and used vehicles in the second half and strong used-vehicle sales:

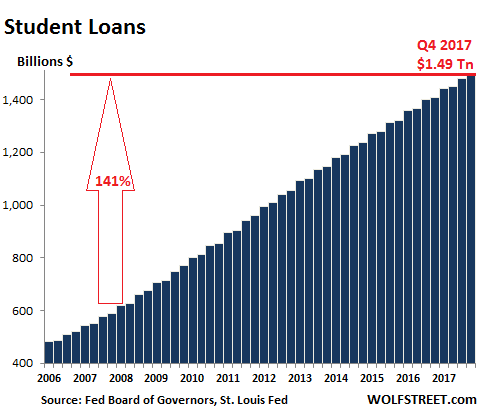

[..] Student loans surged 5.6% in Q4 year-over-year. This seems like a shocking increase, but the year-over-year increases in Q3 and Q4 were the only such increases below 6% in this data series. Between 2007 – as far back as year-over-year comparisons are possible in this data series – and Q3 2012, the year-over-year increases ranged from 11% to 15%:

In a recent article, Yale scholar Stephen Roach points out that between 2008 and 2017 the combined balance sheets of the central banks of the U.S., Japan and the eurozone expanded by $8.3 trillion, while nominal GDP in those same economies expanded $2.1 trillion. What happens when you print $8.3 trillion in money and only get $2.1 trillion of growth? What happened to the extra $6.2 trillion of printed money? The answer is that it went into assets. Stocks, bonds, emerging-market debt and real estate have all been pumped up by central bank money printing. What makes 2018 different from the prior 10 years? The answer is that this is the year the central banks stop printing and take away the punch bowl. The Fed is already destroying money (they do this by not rolling over maturing bonds).

Last week, the Fed reduced its balance sheet by $22 billion. While that doesn’t seem like much when you’re talking about a $4 trillion balance sheet, it was the Fed’s largest cut to date. Funny how the market hit the skids just after this happened. But you haven’t heard the mainstream media mention that. By the end of 2018, the annual pace of money destruction will be $600 billion — if the Fed under new chairman Jerome Powell stays on course. The ECB and Bank of Japan are not yet at the point of reducing money supply, but they have stopped expanding it and plan to reduce money supply later this year. In economics everything happens at the margin. When something is expanding and then stops expanding, the marginal impact is the same as shrinking. Apart from money supply, all of the major central banks are planning rate hikes, and some, such as those in the U.S. and U.K., are actually implementing them.

Reducing money supply and raising interest rates might be the right policy if price inflation were out of control. But despite a recent uptick in some inflation measures, prices have mostly been falling. The “inflation” hasn’t been in consumer prices; it’s in asset prices. The impact of money supply reduction and higher rates will be falling asset prices in stocks, bonds and real estate — the asset bubble in reverse. [..] This will not be a soft landing. The central banks — especially the U.S. Fed, first under Ben Bernanke and later under Janet Yellen — repeated Alan Greenspan’s blunder from 2005–06. Greenspan left rates too low for too long and got a monstrous bubble in residential real estate that led the financial world to the brink of total collapse in 2008. Bernanke and Yellen also left rates too low for too long. They should have started rate and balance sheet normalization in 2010 at the early stages of the current expansion when the economy could have borne it. They didn’t.

What happened? Did the market sneeze, cough, or was something misread and today perceived in a different light? In my opinion this is what happened: The Plunge Protection Team, as they have done on previous equity market drops, or the Federal Reserve operating for the Working Group on Financial Markets, sent a purchase order for S&P futures to the trading floor. The hedge funds, seeing the incoming bid, front-ran the bid by stepping in and buying S&P futures. This pushed the market back up, ended the correction, and prevented financial panic.

The Plunge Protection Team was created in 1987, approaching the end of the Reagan administration, in order to prevent a market correction from costing George H. W. Bush the presidential election as Reagan’s successor. The Republican Establishment was desperate to reestablish its control over the party. The Republican Establishment, convinced by Wall Street that the Reagan tax cut would result in high inflation, found themselves instead confronted with a long economic expansion. In those days that meant that the expansion could be nearing its end, and a stock market correction could deny the presidency to George H.W. Bush. To prevent any such correction, the US Treasury and Federal Reserve created a “working group” to intervene in the stock market in order to support values. Whenever the market starts to drop, the team purchases S&P futures which halts the market decline.

We have witnessed this on several occasions. And, most likely, again this week. Pundits who speak about “market forces” are speaking about something that doesn’t exist. “Market forces” are the interventions that support existing values with money infusions. How long can the fraudulent valuation of equities continue? My sometimes coauthor Dave Kranzler and I think it can continue until the dollar as reserve currency comes under attack. Neither of us believed that the fraud could be perpetrated this long. The two other world powers, Russia and China, are moving away from use of the US dollar, but the consequence for the dollar could still be in the future. In the meantime, liquidity supplied by central banks and the interventions of the Plunge Protection Team could send equity prices higher.

The European Central Bank should wind down its giant bond-buying program after September despite a stronger euro currency and volatility on global financial markets, German central bank President Jens Weidmann said Thursday. Speaking at a conference in Frankfurt, Mr. Weidmann, who sits on the ECB’s 25-member rate-setting committee, said “substantial net [asset] purchases beyond the announced amount do not seem to be required” if economic growth “progresses as currently expected.” ECB officials are weighing how quickly to phase out their stimulus policies as the region’s economy heats up. The ECB has pledged to buy €30 billion a month of eurozone bonds at least through September under its €2.5 trillion quantitative easing program, and ECB President Mario Draghi has signaled that the program won’t end abruptly.

Mr. Weidmann didn’t rule out a short extension of QE. But he argued that the eurozone’s economic recovery might be more advanced than that in the U.S. when the Fed wound down its own QE program in 2014. “The favorable economic outlook lends credence to the expectation that wage growth and therefore domestic price pressures will gradually increase,” Mr. Weidmann said. This week’s pay deal in Germany’s engineering sector “is consistent with this picture,” suggesting that inflation will pick up in Germany as unemployment falls, he said. Crucially, he urged policy makers not to be distracted by a rising euro or the situation in financial markets, which have gyrated wildly in recent days amid concerns about the reduction of monetary stimulus from central banks. “U.S. equity prices rose over a prolonged period without any notable corrections, which was unusual given that valuations have been high overall, Mr. Weidmann said.

The tech billionaire Elon Musk sent one of his Tesla electric cars into space yesterday, a day before the company that built it announced its biggest ever quarterly loss. Musk’s Tesla electric car and energy storage company lost $675.4m in the three months ending 31 December, the company announced on Thursday, compared with a loss of $121m for the same period last year. The company has been spending heavily as it rolls out the next generation of electric cars, the Model 3 sedan, a semi truck and other products. The company has struggled to keep up with is production targets for the Model 3 but said it would probably build about 2,500 Model 3s per week by the end of the first quarter and that it plans to reach its goal of 5,000 vehicles per week by the end of the second quarter. On Wednesday Musk’s private aerospace company, SpaceX, blasted a cherry red Tesla Roadster sports car into space in a successful test of its Falcon Heavy rocket.

The car and its dummy driver are now heading towards the asteroid belt. Tesla delivered 101,312 Model S sedans and Model X SUVs last year, up 33% over 2016 and ahead of its targets, according to preliminary figures released last month. But it fell woefully short on the Model 3, which went into production in July. Tesla made just 2,425 Model 3s in the fourth quarter, and has pushed back production targets multiple times. At one point, Tesla had 500,000 people on a waiting list for the Model 3, but it’s not clear if all of them are continuing to wait. On a call with analysts Musk said production was getting back on track. “If we can send a Roadster to the asteroid belt we can probably solve Model 3 production,” he said. Musk is set to collect a $55.8bn (£40bn) bonus – probably be the largest ever – if he can build Tesla into a $650bn company over the next decade. In the meantime the 46-year-old has agreed to work unpaid for the next 10 years.

Turkey is recruiting and retraining Isis fighters to lead its invasion of the Kurdish enclave of Afrin in northern Syria, according to an ex-Isis source. “Most of those who are fighting in Afrin against the YPG [People’s Protection Units] are Isis, though Turkey has trained them to change their assault tactics,” said Faraj, a former Isis fighter from north-east Syria who remains in close touch with the jihadi movement. In a phone interview with The Independent, he added: “Turkey at the beginning of its operation tried to delude people by saying that it is fighting Isis, but actually they are training Isis members and sending them to Afrin.” An estimated 6,000 Turkish troops and 10,000 Free Syrian Army (FSA) militia crossed into Syria on 20 January, pledging to drive the YPG out of Afrin.

The attack was led by the FSA, which is a largely defunct umbrella grouping of non-Jihadi Syrian rebels once backed by the West. Now, most of its fighters taking part in Turkey’s “Operation Olive Branch” were, until recently, members of Isis. Some of the FSA troops advancing into Afrin are surprisingly open about their allegiance to al-Qaeda and its offshoots. A video posted online shows three uniformed jihadis singing a song in praise of their past battles and “how we were steadfast in Grozny (Chechnya) and Dagestan (north Caucasus). And we took Tora Bora (the former headquarters of Osama bin Laden). And now Afrin is calling to us”.

Livestock raised for food in the US are dosed with five times as much antibiotic medicine as farm animals in the UK, new data has shown, raising questions about rules on meat imports under post-Brexit trade deals. The difference in rates of dosage rises to at least nine times as much in the case of cattle raised for beef, and may be as high as 16 times the rate of dosage per cow in the UK. There is currently a ban on imports of American beef throughout Europe, owing mainly to the free use of growth hormones in the US. Higher use of antibiotics, particularly those that are critical for human health – the medicines “of last resort”, which the WHO wants banned from use in animals – is associated with rising resistance to the drugs and the rapid evolution of “superbugs” that can kill or cause serious illness.

The contrast between rates of dosage in the US and the UK throws a new light on negotiations on Brexit, under which politicians are seeking to negotiate trade deals for the UK independently of the EU. Agriculture and food are key areas, particularly in trading with the US, which as part of any deal may insist on opening up the UK markets to imports that would be banned under EU rules. When negotiating outside the EU for a new trade deal, the UK will come under severe pressure to allow such imports. Over the summer, a row broke out over the potential for imports of US chlorinated chicken – bleaching chicken, according to experts in the UK, is a dangerous practice because it can serve to disguise poor hygiene practices in the food chain.

But Ted McKinney, US under-secretary for trade and foreign agricultural affairs, told an audience of British farmers last month he was “sick and tired” of hearing British concerns about chlorinated chicken and US food standards, providing further indication that the US government is likely to strike a hard deal on agricultural products as part of any trade agreement. Antibiotic use in the US is three times higher in chickens than it is in the UK, double that for pigs, and five times higher for turkeys, according to research by the Alliance to Save Our Antibiotics [..]

Suzi Shingler, at the Alliance to Save Our Antibiotics, said: “US cattle farmers are massively overusing antibiotics. This finding shows the huge advantages of British beef, which is often from grass-reared animals, whereas US cattle are usually finished in intensive feedlots. Trade negotiators who may be tempted to lift the ban on US beef should not only be considering the impact of growth hormones, but also of antibiotic resistance due to rampant antibiotic use.”

Concerns are rising about conditions at reception centers for migrants on the islands of the eastern Aegean amid delays in much-needed infrastructure upgrades and increasingly cramped conditions, with reports of a spike in cases of mental health problems. Last summer, authorities completed a feasibility study for an upgrade of the drainage and sewerage systems at Moria, the main reception center on Lesvos. But the plan appears to have become mired in bureaucracy. Originally designed to house 1,000 migrants, the camp at Moria is currently hosting nearly seven times that number. The overcrowded and dirty conditions, and the uncertainty, are taking their toll on the mental health of many camp residents, Gavriil Sakellaridis, the head of Amnesty International’s Greek chapter, said on Wednesday.

Following a visit to camps on Lesvos and Chios, Sakellaridis expressed concern at the large number of migrants suffering from depression and called for the transfer of asylum seekers to the mainland. “The living conditions of asylum seekers at Moria and Vial [on Chios] are an open wound for Greece and Europe and for human rights,” Sakellaridis said. “The lives of those people have been put on hold for a period of up to two years in some cases and as a result the cases of despair and mental distress are growing,” he said.

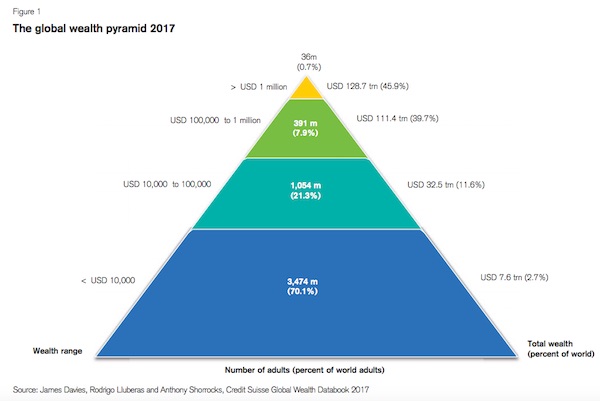

The world’s richest 1% of families and individuals hold over half of global wealth, according to a new report from Credit Suisse. The report suggests inequality is still worsening some eight years after the worst global recession in decades. The release of the Paradise Papers, a trove of leaked documents uncovered by investigative journalists detailing the offshore tax holdings of the world’s super wealthy, has reinforced just how rampant the problem of wealth inequality has become. “The bottom half of adults collectively own less than 1% of total wealth, the richest decile (top 10% of adults) owns 88% of global assets, and the top percentile alone accounts for half of total household wealth,” the Credit Suisse report said.

Put another way: “The top 1% own 50.1% of all household wealth in the world.” This handy pyramid chart, which shows the relative number of people at different wealth levels and how much of the world’s assets each bracket controls, speaks volumes about the level of income concentration, which by some measures has not been seen since the early 20th century:

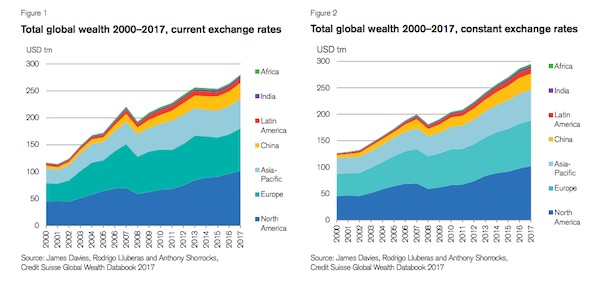

In most countries, including the United States, a large wealth gap translates into those at the top accruing political power, which in turn can lead to policies that reinforce benefits for the wealthy. President Donald Trump’s tax cut plan, for instance, has been widely criticized for favoring corporations and the wealthy over working families. Measured overall, Credit Suisse found total global wealth rose 6.4% in the year between mid-2016 and mid-2017 to $280.3 trillion. Stock market gains helped add $8.5 trillion to US household wealth during that period, a 10.1% rise. US inequality is considerably worse than in its more developed-country peers.

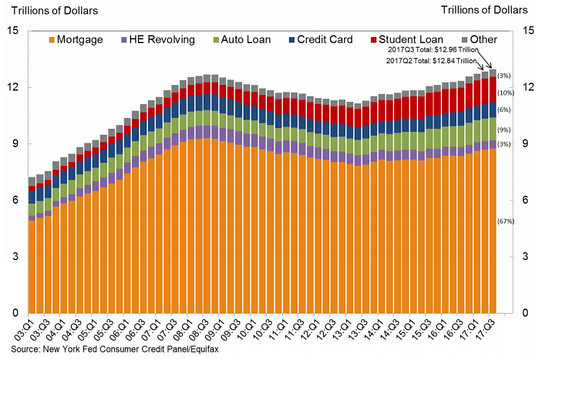

Given Americans’ ceaseless urge to borrow and spend, household debt in the third quarter surged by $610 billion, or 5%, from the third quarter last year, to a new record of $13 trillion, according to the New York Fed. If the word “surged” appears a lot, it’s because that’s the kind of debt environment we now have: Mortgage debt surged 4.2% year-over-year, to $9.19 trillion, still shy of the all-time record of $10 trillion in 2008 before it all collapsed. Student loans surged by 6.25% year-over-year to a record of $1.36 trillion. Credit card debt surged 8% to $810 billion. “Other” surged 5.4% to $390 billion. And auto loans surged 6.1% to a record $1.21 trillion. And given how the US economy depends on consumer borrowing for life support, that’s all good.

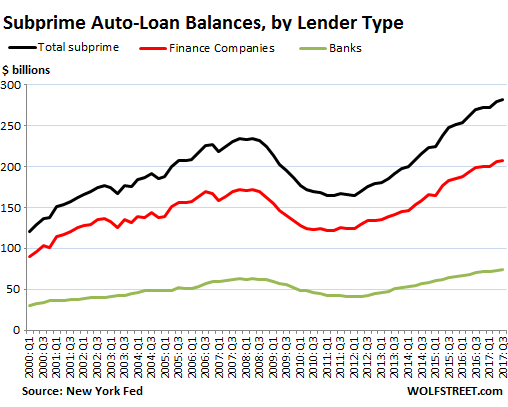

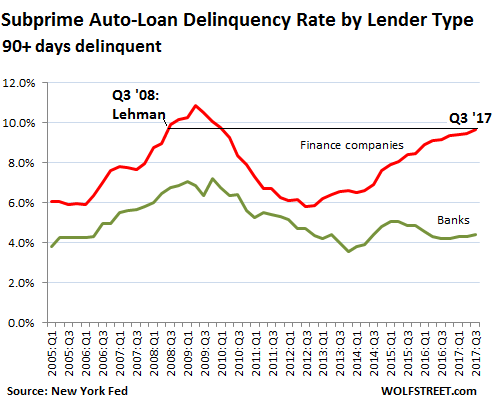

However, there are some big ugly flies in that ointment: Delinquencies – not everywhere, but in credit cards, and particularly in subprime auto loans, where serious delinquencies have reached Lehman Moment proportions. Of the $1.2 trillion in auto loans outstanding, $282 billion (24%) were granted to borrowers with a subprime credit score (below 620). Of all auto loans outstanding, 2.4% were 90+ days (“seriously”) delinquent, up from 2.3% in the prior quarter. But delinquencies are concentrated in the subprime segment – that $282 billion – and all hell is breaking lose there. Subprime auto lending has attracted specialty lenders, such as Santander Consumer USA. They feel they can handle the risks, and they off-loaded some of the risks to investors via subprime auto-loan-backed securities. They want to cash in on the fat profits often obtained in subprime lending via extraordinarily high interest rates.

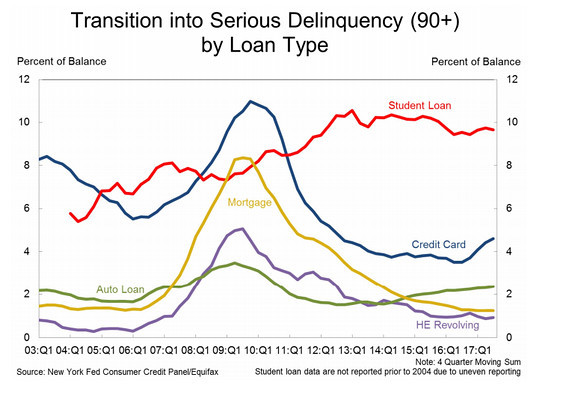

The numbers: Household debt rose by $116 billion, or 0.9%, to $12.96 trillion in the third quarter, the New York Fed said Tuesday. Credit-card debt rose by 3.1% while home equity lines of credit, or HELOC, balances fell by 0.9%. There were small gains in mortgage, student and auto debt. Flows into credit-card and auto loans delinquencies rose, with 4.6% of credit card debt 90 days or more delinquent, up from 4.4% in the second quarter, and 2.4% of auto loan debt seriously delinquent, up from 2.3%. That’s still nowhere near the 9.6% of student loan debt that is delinquent, which itself is understated because about half of those loans are currently in deferment, grace periods or in forbearance.

What happened: U.S. households aren’t aggressively leveraging up, and the ones that are did so had better credit. The higher level of auto loan originations was mainly to prime borrowers, and the median credit score to individuals originating new mortgages ticked up to 760 from 754. [..] Auto loans have grown for 26 straight quarters. But there are some worries as subprime auto loan performance continues to deteriorate — the delinquency rate for auto finance companies have grown by more than 2 percentage points since 2014, the New York Fed said.

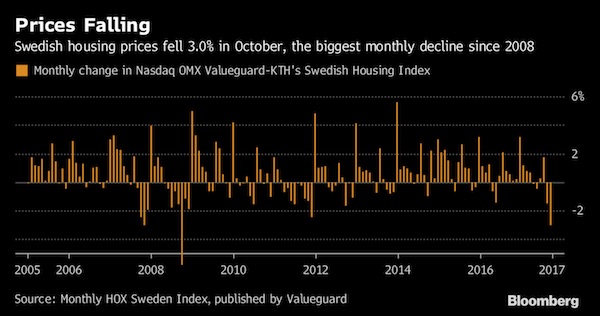

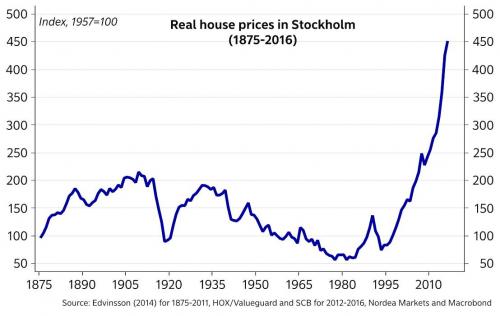

Can a central bank steer the housing market? Not so long ago, Sweden’s Riksbank decided: no. Now, there’s a risk that decision may backfire as the biggest property market in Scandinavia risks sinking into a correction. The evidence of price declines was so worrying on Tuesday that it contributed to a 1.5 percent slump in the krona against the euro. A weak currency puts the Riksbank’s inflation target at risk. So should it be looking at the housing market more closely? Developments in Sweden’s housing market “could spark some doubts at the Riksbank as it may affect the overall economic outlook and inflation,” Nordea analyst Andreas Wallstrom said in a note. Sweden’s Riksbank has thrown all its energy into fighting deflation and, earlier this year, finally regained credibility on its inflation mandate.

Policy makers now say they may be ready to start raising rates in the middle of next year. At the same time, the Riksbank may extend a bond purchase program due to end this year. But in the minutes of the Riksbank’s latest rate meeting, Deputy Governor Cecilia Skingsley suggested that monetary policy, “under certain circumstances, can be used to combat the effects of major household debt.” She also said the housing market “must be carefully monitored,” given the latest developments. Nordea’s Wallstrom says the central bank will probably need to see a “sharp drop” in house prices with a direct impact on the real economy before it will look into adding significant stimulus. But the bank might decided to signal rates will stay where they are for even longer.

The European Central Bank intensified its push for a tool that would hand authorities the power to stop deposit withdrawals when a bank is on the verge of failing. ECB executive board member Sabine Lautenschlaeger said that bank resolution cases this year showed that a so-called moratorium tool, which would temporarily freeze a bank’s liabilities to buy time for crucial decisions, is needed. Her comment comes as policy makers in Brussels debate how such measures should be designed, and just days after the ECB officially called for the moratorium to extend to deposits as well. “If we have a long list of exemptions and we have a moratorium that doesn’t work, I do not want to have a moratorium tool,” Lautenschlaeger told a conference in Frankfurt on Tuesday. “Then you will never use it.”

EU member states appear ready to heed the request, according to a Nov. 6 paper that develops their stance on a bank-failure bill proposed by the European Commission. They suggest giving authorities the power to cap deposit withdrawals as part of a stay on payments only after an institution has been declared “failing or likely to fail.” The power to install a moratorium “can in principle apply to eligible deposits,” the paper reads. “However, resolution authority should carefully assess the opportunity to extend the suspension also to covered deposits, especially covered deposits held by natural persons and micro, small and medium sized enterprises, in case application of suspension on such deposits would severely disrupt the functioning of financial markets.”

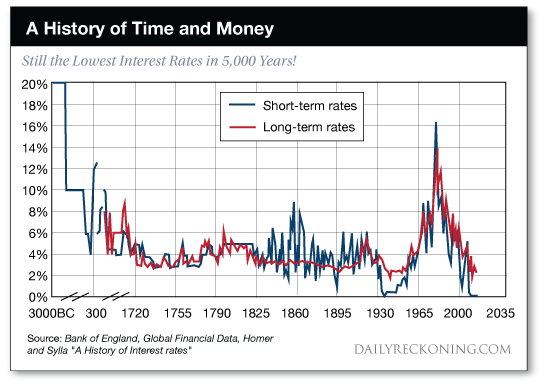

“At no point in the history of the world has the interest on money been so low as it is now.” Who can dispute the good Sen. Henry M. Teller of Colorado? For lo eight years, the Federal Reserve has waged a ceaseless warfare upon interest rates. Economic law, history, logic itself, stagger under the onslaughts. We suspect that economic reality will one day prevail. This fear haunts our days… and poisons our nights. But let us check the date on the senator’s declaration… Kind heaven, can it be? We are reliably informed that Sen. Teller’s comment entered the congressional minutes on Jan. 12… 1895. 1895 — some 19 years before the Federal Reserve drew its first ghastly breath! Were interest rates 122 years ago the lowest in world history? And are low interest rates the historical norm… rather than the exception?

Today we rise above the daily churn… canvass the broad sweep of history… and pursue the grail of truth. The chart below — giving 5,000 years of interest rate history — shows the justice in Teller’s argument. Please direct your attention to anno Domini 1895: Rates had never been lower in all of history. They would only sink lower on two subsequent occasions — the dark, depressed days of the early 1930s — and the present day, dark and depressed in its own right. A closer inspection of the chart reveals another capital fact… Absent one instance at the beginning of the 20th century and a roaring exception during the mid-to-late 20th century, long-term interest rates have trended lower for the better part of 500 years.

Paul Schmelzing professes economics at Harvard. He’s also a visiting scholar at the Bank of England, for whom he conducted a study of interest rates throughout history. Could the sharply steepening interest rates that began in the late 1940s be a historical one-off… an Everest set among the plains? Analyst Lance Roberts argues that periods of sharply rising interest rates like this are history’s exceptions — lovely exceptions. Why lovely? Roberts: Interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. In this view, rates rose steeply at the dawn of the 20th century because rapid industrialization and dizzying technological advances had entered the scenery.

Likewise, Roberts argues the massive post-World War II economic expansion resulted in the second great spike in interest rates: There have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy. The second period occurred post-World War II as America became the “last man standing”… It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed.

We know from the Snowden leaks on the NSA, the CIA files released by WikiLeaks, and the ongoing controversies regarding FBI surveillance that the US intelligence community has the most expansive, most sophisticated and most intrusive surveillance network in the history of human civilisation. Following the presidential election last year, anonymous sources from within the intelligence community were haemorrhaging leaks to the press on a regular basis that were damaging to the incoming administration. If there was any evidence to be found that Donald Trump colluded with the Russian government to steal the 2016 election using hackers and propaganda, the US intelligence community would have found it and leaked it to the New York Times or the Washington Post last year.

Mueller isn’t going to find anything in 2017 that these vast, sprawling networks wouldn’t have found in 2016. He’s not going to find anything by “following the money” that couldn’t be found infinitely more efficaciously via Orwellian espionage. The factions within the intelligence community that were working to sabotage the incoming administration last year would have leaked proof of collusion if they’d had it. They did not have it then, and they do not have it now. Mueller will continue finding evidence of corruption throughout his investigation, since corruption is to DC insiders as water is to fish, but he will not find evidence of collusion to win the 2016 election that will lead to Trump’s impeachment. It will not happen. This sits on top of all the many, many, many reasons to be extremely suspicious of the Russiagate narrative in the first place.

[..] If you attribute all your problems to Trump, you’re guaranteeing more Trumps after him, because you’re not addressing the disease which created him, you’re just addressing the symptom. The problem is not Trump. The problem is that America is ruled by an unelected power establishment which maintains its rule by sabotaging democracy, exacerbating economic injustice and expanding the US war machine. Stop listening to the lies that they pipe into your echo chambers and turn to face your real demons.

Lorry driver Abu Fawzi thought it was going to be just another job. He drives an 18-wheeler across some of the most dangerous territory in northern Syria. Bombed-out bridges, deep desert sand, even government forces and so-called Islamic State fighters don’t stand in the way of a delivery. But this time, his load was to be human cargo. The Syrian Democratic Forces (SDF), an alliance of Kurdish and Arab fighters opposed to IS, wanted him to lead a convoy that would take hundreds of families displaced by fighting from the town of Tabqa on the Euphrates river to a camp further north. The job would take six hours, maximum – or at least that’s what he was told. But when he and his fellow drivers assembled their convoy early on 12 October, they realised they had been lied to. Instead, it would take three days of hard driving, carrying a deadly cargo – hundreds of IS fighters, their families and tonnes of weapons and ammunition.

Abu Fawzi and dozens of other drivers were promised thousands of dollars for the task but it had to remain secret. The deal to let IS fighters escape from Raqqa – de facto capital of their self-declared caliphate – had been arranged by local officials. It came after four months of fighting that left the city obliterated and almost devoid of people. It would spare lives and bring fighting to an end. The lives of the Arab, Kurdish and other fighters opposing IS would be spared. But it also enabled many hundreds of IS fighters to escape from the city. At the time, neither the US and British-led coalition, nor the SDF, which it backs, wanted to admit their part. Has the pact, which stood as Raqqa’s dirty secret, unleashed a threat to the outside world – one that has enabled militants to spread far and wide across Syria and beyond?

Virtually unknown among large swaths the general public both in Britain and the U.S is the fact that Bashar-al Assad’s secular government won the first contested presidential election in Ba’athist Syria’s history on July 16, 2014, which was reported as having been open, fair and transparent. American Peace Council delegate, Joe Jamison, who was allowed unhindered travel throughout Syria, stated: “By contrast to the medieval Wahhabist ideology, Syria promotes a socially inclusive and pluralistic form of Islam. We [the USPC] met these people. They are humane and democratically minded…. The [Syrian] government is popular and recognised as being legitimate by the UN. It contests and wins elections which are monitored. There’s a parliament which contains opposition parties – we met them. There is a significant non-violent opposition which is trying to work constructively for its own social vision.”

Jamison added: “Our delegation came to Syria with political views and assumptions, but we were determined to be sceptics and to follow the facts wherever they led us”, he said. “I concluded that the motive of the US war is to destroy an independent, Arab, secular state. It’s the last of this kind of state standing.” The notion that the United States government and its allies and proxies, want to see the destruction of Syria’s pluralistic state under Assad destroyed, is hardly a secret. Indeed, one of Washington’s key allies in the region, Israel, has conceded as much. The claim by Israel’s defence minister, Avigdor Lieberman, that Assad’s removal is the empires “ultimate goal”, would appear to be consistent with the notion that the aim of the U.S government is to stymie the non-violent opposition inside Syria. Washington has been engaged in this strategy since early 2012 after having deliberately helped scupper Kofi Annan’s six point peace plan.

Members of the Syrian opposition within a newly reformed constitution who wanted to participate in democratic politics have instead been encouraged by the Western axis – as a result of bribing government forces to defect and through funding the Free Syrian Army – to overthrow the Assad government by violent means. As commentator Dan Glazebrook put it: “Within days of Annan’s peace plan gaining a positive response from both sides in late March, the imperial powers openly pledged, for the first time, millions of dollars for the Free Syrian Army; for military equipment, to provide salaries to its soldiers and to bribe government forces to defect. In other words, terrified that the civil war is starting to die down, they are setting about institutionalising it.”

The Russian Defense Ministry has said it has obtained evidence the US-led coalition provides support for the terrorist group Islamic State (outlawed in Russia). “The Abu Kamal liberation operation conducted by the Syrian government army with air cover by the Russian Aerospace Force at the end of the last week revealed facts of direct cooperation and support for ISIS terrorists by the US-led ‘international coalition,’” the Russian Defense Ministry said. The ministry showed photo shoots made by Russian unmanned aircraft on November 9 which show kilometers-long convoys of IS armed groups leaving Abu Kamal towards the Wadi es-Sabha passage on the Syrian-Iraqi border to avoid strikes by the Russian aviation and the government army.

The US refused to conduct airstrikes over the leaving IS convoy. “Americans peremptorily rejected to conduct airstrikes over the ISIS terrorists on the pretext of the fact that, according to their information, militants are yielding themselves prisoners to them and now are subject to the provisions of the Convention relative to the Treatment of Prisoners of War,” the Russian Defense Ministry said. The Defense Ministry specified that “the Russian force grouping command twice addressed the command of the US-led ‘international coalition’ with a proposal to carry out joint actions to destroy the retreating ISIS convoys on the eastern bank of the Euphrates.” The Americans failed to answer the Russian side’s question on why IS militants leaving in combat vehicles heavily equipped are regrouping in the area controlled by the international coalition to conduct new strikes over the Syrian army near Abu Kamal, the Russian Defense Ministry stressed.

Mugabe under house arrest and according to South African media ‘planning to step down’. Rumors that Emmerson Mnangagwa, the vice-president Mugabe fired recently, will be interim president. Which in turn would confirm that the army acted because it doesn’t want Grace Mugabe in power.

The armed forces seized power in Zimbabwe after a week of confrontation with President Robert Mugabe’s government and said the action was needed to stave off violent conflict in the southern African nation that he’s ruled since 1980. The Zimbabwe Defense Forces will guarantee the safety of Mugabe, 93, and his family and is only “targeting criminals around him who are committing crimes that are causing social and economic suffering in the country in order to bring them to justice,” Major-General Sibusiso Moyo said in a televised address in Harare, the capital. All military leave has been canceled, he said. Denying that the action was a military coup, Moyo said “as soon as we have accomplished our mission we expect the situation to return to normalcy.” He urged the other security services to cooperate and warned that “any provocation will be met with an appropriate response.”

The action came a day after armed forces commander Constantine Chiwenga announced that the military would stop “those bent on hijacking the revolution.” As several armored vehicles appeared in the capital on Tuesday, Mugabe’s Zimbabwe African National Union-Patriotic Front described Chiwenga’s statements as “treasonable” and intended to incite insurrection. Later in the day, several explosions were heard in the city. The military intervention followed a week-long political crisis sparked by Mugabe’s decision to fire his long-time ally Emmerson Mnangagwa as vice president in a move that paved the way for his wife Grace, 52, and her supporters to gain effective control over the ruling party. Nicknamed “Gucci Grace” in Zimbabwe for her extravagant lifestyle, she said on Nov. 5 that she would be prepared to succeed her husband.

Short-term rental website Airbnb, which has been challenging traditional hotel operators such as Accor and Marriott, said it would automatically cap the number of days its hosts can rent their property each year in central Paris. The decision, which goes into effect in January and mirrors initiatives already in place in London and Amsterdam, will force hosts to effectively comply with France’s official limit on short-term rentals of 120 days a year for a main residence. It comes as Airbnb, similar to its taxi-hailing peer Uber, is facing a growing crackdown from legislators worldwide – triggered in part by lobbying from the hotel industry, which sees the rental service as providing unfair competition. Airbnb and other rental platforms have also been criticized for driving up property prices and contributing to a housing shortage in some cities such as Paris or Berlin.

Airbnb, which has denied having a significant impact on housing shortages, has been trying to placate local authorities. “Paris is Airbnb number one city worldwide and we want to insure our community of hosts expands in a responsible and sustainable manner,” said Emmanuel Marill, Airbnb general manager for France. In Paris, the automatic rental cap will apply only to the city’s first four districts (“arrondissements”) unless the property owner has proper authorization. These districts include tourist hotspots such as the Marais, and landmarks such as the Louvre and the place de la Concorde square. Airbnb is implementing the cap as the Paris city council has made it mandatory from December for people renting their apartments on short-term rental websites to register their property with the town hall.

Ian Brossat, the housing advisor to the Paris Mayor, told Reuters that the cap should extend to the whole of Paris. “Under the law, websites must withdraw listings that do not comply with the law throughout Paris. One cannot accept that a website complies with the law only in the first four arrondissements of Paris,” said Brossat. With over 400,000 listings, France is Airbnb’s second-largest market after the United States. Paris, which is the most visited city in the world, is Airbnb’s biggest single market, with 65,000 homes.

Airbnb refused to provide the Greek Finance Ministry with information on property rentals thus delaying the launch of an online platform where owners should register the rental transactions and pay the necessary taxes. According to information obtained by economic news website economy365.gr, the Finance Ministry has tried for five months to get in touch with executives of the company in California as well as of other companies (Novasol etc). However, the companies showed no intention to cooperate with Greek authorities who have requested that the tax number of property owner is being registered to every property at the Airbnb platform. Owner’s tax number would facilitate the imposition of taxes on rentals via Airbnb. The tax legislation on short-term leases through digital platform like Airbnb was voted last year. The law foresees taxes of 15%-45% and a limited number of rentals per year.

Registration is mandatory. Authorities will provide the property owner with a certification number that has to be declared on any website and social media advert, including, of course, the Airbnb platform. Fines can reach up to 5,000 euros, if a property owner does not register on the Greek authorities registration platform and tries to evade taxes from short-term rentals. The state has estimated that revenues from Airbnb rentals could reach 48 million euros per year. According to the Finance Ministry property owners try to bypass the 3% commission to Airbnb and upcoming taxes by direct contact to customers via messenger or telephone. The payments are done cash at the arrival and not through the platform. In this way, property owners can bypass not only the commission but also registration of the rentals and future taxes. Just in case and even if one day, the Airbnb decides to hand over its Greek data to the tax authorities. For the time being it looks as the Greek goal to tax Airbnb properties has to be postponed.

We asked this question one week after Trump was elected: “What does history predict for the Trump presidency?” The answer we furnished — based on over a century of data — was this: “A 100% chance of recession within his first year.” Not a 90% chance, that is. Not even a 99% chance. But a 100% chance of recession. That answer came by way of a certain Raoul Pal. He used to captain one of the largest hedge funds in the world. And to prove his case he called the unimpeachable witness of history to the stand… Crunching 107 years worth of data, he showed the U.S. economy enters or is in a recession every time a two-term president vacates the throne: “Since 1910, the U.S. economy is either in recession or enters a recession within 12 months in every single instance at the end of a two-term presidency… effecting a 100% chance of recession for the new president.”

Obama was a two-term president – if memory serves. Only two incoming presidents were not treated to a recession within the first year of office. And both followed one-term reigns: “Not every single election sees a recession, only every two-term incumbent change… Only two presidents in history did not see a recession, and they were inaugurated after single-term presidents.” Mr. Pal couldn’t fully explain the phenomenon. Maybe it takes two terms for presidential mischief to work its way into the economic machinery. One-term presidents just can’t heave enough sand in the gears. Regardless of the reason, this fellow’s research pointed him to one conclusion: “It is not a coincidence.” Trump’s now five months into his first 12. Where does the prediction stand? By grace of God or Janet Yellen or neither or both, no recession yet.

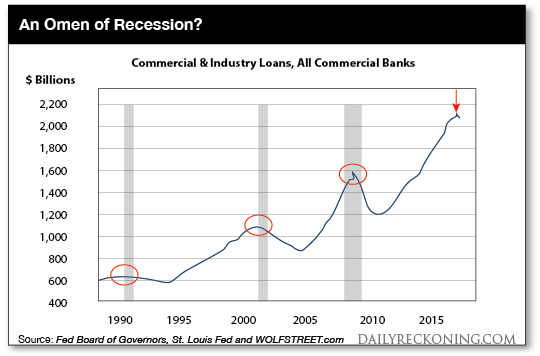

But our pessimistic side reminds us that seven months remain. And anxiety riles the deeps of our being… For we’ve spotted ill omens… disturbing portents of recession among the recent economic data… Old Daily Reckoning hand Wolf Richter: Over the past five decades, each time commercial and industrial loan balances at U.S. banks shrank or stalled… a recession was either already in progress or would start soon. There has been no exception since the 1960s. Last time this happened was during the financial crisis. “Now,” Wolf says, “it’s happening again.” Last month commercial and industrial loans (C&I) outstanding fell to $2.095 trillion, according to the St. Louis Fed. That’s down 4.5% from their November 2016 peak, says Wolf. And it marked the 30th consecutive week of no growth in C&I loans. Wolf argues C&I loans matter because they directly reflect the real economy – unlike today’s stock market, which is crooked as a Brit’s teeth.

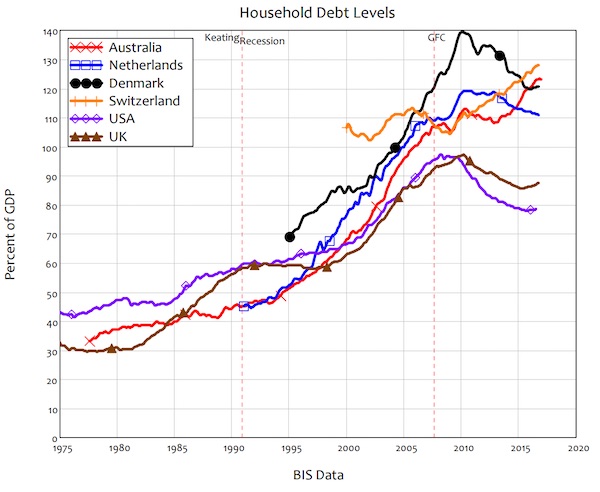

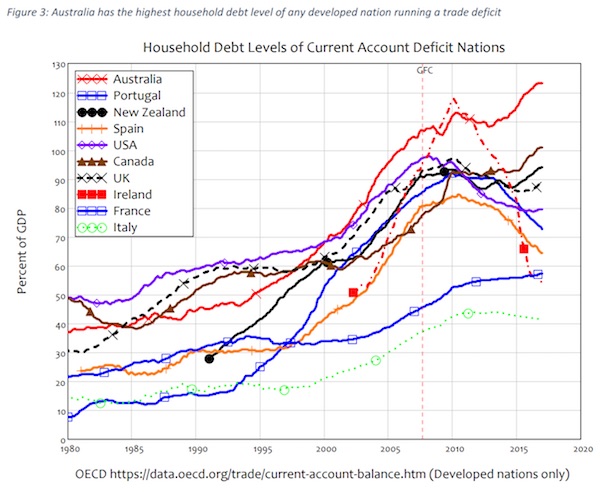

Much was made of the fact that Australia recently replaced The Netherlands as the world record holder for the longest period without a recession (using the colloquial definition of two consecutive quarters of negative growth). The Netherlands went just under 26 years (103 quarters between 1982 and 2008) without a recession, and Australia surpassed this when it recorded 0.3% growth in the March 2017 quarter (for an annual growth rate of 1.7%).

Rather less attention was given to another Australian record: household debt. Before its recession-free record was set, Australia had already overtaken The Netherlands for the record of the highest level of household debt ever recorded for a large country (one with more than 10 million people).

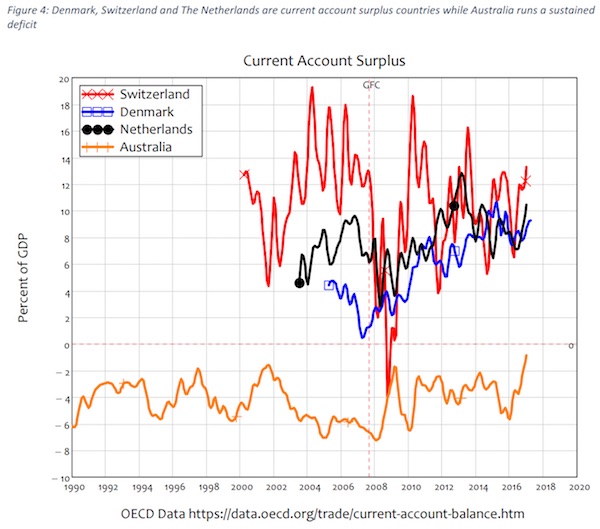

Australia’s household debt level of 123% of GDP has been exceeded only by Switzerland (population 8.3 million, household debt of 128% of GDP in 2016 Q3) and Denmark (population 5.6 million, 139% of GDP in 2009).2 Australia also stands apart from its household leverage competitors in another important respect: Denmark, Switzerland and The Netherlands also run significant current account surpluses—Switzerland’s average surplus since 2000 has been the highest on the planet at over 10% of GDP; Denmark’s has averaged 5.75% since 2005; The Netherlands’ average current account surplus is around 8% of GDP.

Australia, in contrast, has averaged a current account deficit of 3.2% of GDP since 1960, and 4.3% since 2000. Australia therefore holds the record of the highest level of household debt for a country running a trade deficit, and has done so since 2010, when it overtook the previous record-holder: Ireland. Ireland’s household debt level has also plunged since then, from a peak of 118% of GDP in 2010 to 54%. Australia’s closest competitor now is Canada, which has a household debt level 22% lower than Australia’s, and an average trade deficit of 1.4% of GDP, versus Australia’s long-run average of 3.2%.

Why does this matter? Because Australia’s two records are related: Australia avoided a recession in 2008 only by adding additional leverage to its already over-indebted household sector, and the only ways that Australia can keep its winning streak on GDP growth going (given that its government is obsessed with trying to run a surplus) is to either to achieve a huge trade surplus, or for the household sector to continue piling on debt faster than GDP itself grows. A trade surplus is one of three ways to increase both aggregate demand and the amount of money in an economy:3 goods you sell to foreigners are paid for in US dollars, which the exporter then effectively sells to its country’s Central Bank in return for domestic currency (on that front, The Netherlands is, like Germany, a huge beneficiary of the Euro).

A valiant effort, and economics should be redefined for sure, but Ann shirks far too close to assuming Brexit was about economics only and purely. Tempting when you’re an economist, but…

If the British economy crashes as a result of Brexit, it will not vindicate economists. It will simply illustrate once again, their failure. I and my colleagues at Policy Research in Macroeconomics (PRIME) believe there is urgent need for an independent, public inquiry into the economics profession, and its role in precipitating both the financial crisis of 2007-9, the subsequent very slow ‘recovery’; and in the British European referendum campaign. Financial disarray is not unlikely under Brexit, but whether this turns into anything material depends in the first instance on economic policy. How can we trust economists at the Treasury not to impose more disastrous policies? Economists have once again proved themselves not only irrelevant, but a dangerous irrelevance. For too long they have resisted call after call for reform. If they will not do it themselves then it is time for others to take control.

The profession should be brought to account through a public inquiry into the this failure. In voting to leave the EU, England overwhelmingly has rejected economics – and in particular the dominant economic narrative. Unfortunately, the economics profession as a whole cannot resign, though perhaps the President of the RES, Andrew Chesher, should consider his position. Because this hardship is indirectly a consequence of the economics profession. Economists led the way to financial liberalisation of the past 40 years, which led to soaring levels of debt, crises and financial ruin. Economists dictated the terms for austerity that has so harmed the economy and society over the past years. As the policies have failed, the vast majority of economists have refused to concede wrongdoing, nor have societies been offered alternative economics policies.

While it is risky to second guess public opinion, it may just be that the prospect of hardship to come might not have been very compelling for those already suffering the hardship of low wages, insecure low-skilled jobs, bad housing, high rents, an under-resourced and increasingly privatised NHS, and other forms of public sector ‘austerity’. With this historic vote, the British people have not just rejected the EU. They have done something that should worry the British establishment, and their friends in the City of London, and internationally, far more. Perhaps most symbolically, even the Queen suggested they did not know what they were doing. It is hardly surprising, therefore, that the British public did not find the opinion of Remain ‘experts compelling’.

As the nightmare of the Grenfell Tower disaster continues to unfold, one of the many painful questions being asked by survivors is: ‘Where are we going to live now?’ Kensington & Chelsea Council have still been unable to give firm assurances that residents will be rehoused in the area, issuing a statement on Friday afternoon (later contradicted) that “Given the number of households involved, it is possible the council will have to explore housing options that may become available in other parts of the capital”. On Friday, the Times reported that Jeremy Corbyn had an alternative solution. “Corbyn: seize properties of the rich for Grenfell homeless” ran its above-the-fold headline (£). This was not, of course, what Corbyn had actually proposed, as the article itself revealed.

In a parliamentary debate, the Labour leader had suggested that “Properties must be found, requisitioned if necessary, to make sure those residents do get rehoused locally… It cannot be acceptable that in London you have luxury buildings and flats kept as land banking for the future while the homeless and the poor look for somewhere to live.” Not quite the State appropriation of private property conveyed by the sub-editor’s fevered headline, then – but a proposal for making better use of empty housing which happens to be supported by 59% of the British public, according to YouGov. So how many empty homes are there in Kensington? A lot, it turns out. The Department for Communities and Local Government regularly publishes statistics on vacant dwellings, broken down by local authority area.

The latest figures for Kensington & Chelsea reveal there are 1,399 vacant dwellings in the borough, as of April 2017 – and the number hasn’t dropped below a thousand for over a decade. 600 people lived in Grenfell Tower – so there are more than enough empty homes in the borough to house them all, if the properties could be accessed. But where are these empty homes? And who owns them? It turns out that Kensington Council themselves know precisely where they are. In a report published in July 2015, the council’s Housing and Property Scrutiny Committee examined in detail the problem of ‘buy to leave’ in the borough. ‘Buy to leave’ is the phenomenon of purchasing a property where the buyer has no intention to live in it; where the home is regarded purely as an investment – one that, in London’s super-heated property market, will rapidly accrue in value.

The council’s report used a variety of methods to locate empty housing, from council tax registers and payment data, to energy use and Land Registry records. Their findings broadly corroborate central government stats – that there are around a thousand long-term empty homes in Kensington & Chelsea. And on page 13 of the report, they display an extraordinary map of the 941 homes classified as unoccupied dwellings for the purposes of council tax:

Saying that you don’t care about privacy because you have nothing to hide is no different than saying you don’t care about freedom of speech because you have nothing to say.” That comment was made by famed whistleblower Edward Snowden during a recent interview on the Ron Paul Liberty Report. In his conversation with Dr. Paul and Daniel McAdams, published Tuesday, an articulate Snowden discusses the true meaning of freedom, the nature of the deep state, and even his upbringing as a child of a government family. “I’d like to know a little bit, what do you do all day long?” a genuinely curious Dr. Paul asks as his opening question. After talking about the insanity that erupted — both in the political spectrum and his personal life — following the revelations he made back in 2013, Snowden says he’s now become a hot commodity for groups championing causes.

“They want me to sort of front for these issues of privacy and civil liberties and protection of people’s rights,” Snowden replies. “And I want to do what I can, but I’m not a politician. I’m an engineer.” The whistleblower goes on to talk about how he’s now, at long last, finally able to devote time to more practical applications. For him, this means focusing on the area that holds the key to finding a balance between rights and laws in the digital age — technology. “How technically is this even happening?” Snowden poses, digging straight to the heart of the issue of mass surveillance. “How is it that so many governments are spying on so many people? Because even if we pass the best legal reforms in the world in the United States, that doesn’t do anything against China, or Russia, or Germany, or France or Brazil or any other country in the world.”

Continuing, Snowden says that future generations’ rights and protections will be dependent on the current generation’s ability to adapt to a constantly shifting environment: “We need to find new means, new mechanisms, for enforcing these rights in the new times. And I think that’s going to be primarily through science and technology.”

Brazil’s federal police has said that investigators have found evidence the president, Michel Temer, received bribes to help businesses, raising a new threat that the embattled leader could be suspended from office pending a corruption trial. Temer has been under investigation due to plea bargain testimony by the wealthy businessman Joesley Batista of the giant meatpacking company JBS that linked the president and an aide to bribes and the president to an alleged endorsement of hush money for jailed ex-House Speaker Eduardo Cunha. Temer has denied any wrongdoing and insists he will not resign. If Brazil’s top prosecutor agrees with the federal police recommendation, Congress will decide whether Temer should be investigated by the supreme court, which is the only body that can formally investigate the president.

If two-thirds of Congress voted to allow the investigation, Temer would be suspended from office pending trial. In a report published on Tuesday by Brazil’s top court, federal police investigators said they had enough evidence of bribes being paid to warrant a formal investigation of Temer for “passive corruption” – Brazil’s charge for the act of taking bribes. It said former Temer aide Rodrigo Rocha Loures directly received bribes from JBS on the president’s behalf. A previously released video made by investigators shows Loures carrying a suitcase filled with about $150,000 in cash allegedly being sent from JBS to the president. Loures later gave the bag and most of the money to Brazil’s federal police, authorities have said.

After recruiting Trump, the KGB and Moscow have clearly also managed to make all House Republicans their puppets, because the Senate bill that passed last week and slapped new sanctions on Russia (but really was meant to block the production on the Nord Stream 2 gas pipeline from Russia and which Germany, Austria and France all said is a provocation by the US and would prompt retaliation) just hit a major stumbling block in the House. At least that’s our interpretation of tomorrow’s CNN “hot take.” Shortly after House Ways and Means Chairman Kevin Brady of Texas said that House leaders concluded that the legislation, S. 722, violated the origination clause of the Constitution, which requires legislation that raises revenue to originate in the House, and would require amendments, Democrats immediately accused the GOP of delaying tactics and “covering” for the Russian agent in the White House.

“House Republicans are considering using a procedural excuse to hide what they’re really doing: covering for a president who has been far too soft on Russia,” Senate Minority Leader Chuck Schumer of New York said in a statement. “The Senate passed this bill on a strong bipartisan vote of 98-2, sending a powerful message to President Trump that he should not lift sanctions on Russia.” And, if the House does pass it, a huge diplomatic scandal would erupt only not between the US and Russia, but Washington and its European allies who have slammed this latest intervention by the US in European affairs… a scandal which the Democrats would also promptly blame on Trump. That said, the bill may still pass: Brady pushed back against Democrat suggestions that House GOP leadership is trying to delay the bill, stressing that he thought the Senate legislation was sound policy.

“I strongly support sanctions against Iran and Russia to hold them accountable. We were willing to work with the Senate throughout the process, but the final bill and final language violated the origination clause in the Constitution,” Brady told reporters on Tuesday. “I am confident working with the Senate and Chairman [Ed] Royce that we can move this legislation forward. So at the end of the day, this isn’t a policy issue, it’s not a partisan issue, it is a Constitutional issue that we will address.”

This is your fault, Clinton Democrats. You created this, and if our species is plunged into a new world war or extinction via nuclear holocaust, it will be your fault. You knuckle-dragging, vagina hat-wearing McCarthyite morons made this happen. American military provocations against the pro-Assad coalition in Syria are fast becoming a daily occurrence. In response to the US air force’s gunning down of a Syrian military plane on Sunday, Russia has cut off its hotline with which it was coordinating operations with America to avoid aerial collisions, and has warned that all US aircraft west of the Euphrates river will now be tracked and treated as potential targets. Today, 25 miles northwest of the Russian enclave of Kaliningrad, a US reconnaissance plane was intercepted by an armed Russian aircraft which came within five feet of the plane’s wingtip.

This on the same day that the US shot down yet another Iranian military drone in Syria. Clintonists have been working tirelessly since the election to manufacture these new Cold War tensions. Stephen Cohen, easily America’s foremost authority on US-Russia relations, has warned again and again that the political pressures being placed on the Trump administration to maintain escalations with Russia without conceding an inch has placed our species in a situation that is in some ways even more dangerous than those we faced at the height of the Cuban Missile Crisis. If Kennedy had had to negotiate that crisis while being pressured by his entire country to keep escalating tensions with the USSR without yielding an inch, there is no way any terrestrial life would have existed beyond 1962. The Clintonists (along with their neocon buddies on the other side of the aisle) are responsible for creating those pressures.

“You know it’s easy to joke about this, except that we’re at maybe the most dangerous moment in US-Russian relations in my lifetime, and maybe ever. And the reason is that we’re in a new cold war, by whatever name.

We have three cold war fronts that are fraught with the possibility of hot war, in the Baltic region where NATO is carrying out an unprecedented military buildup on Russia’s border, in Ukraine where there is a civil and proxy war between Russia and the west, and of course in Syria, where Russian aircraft and American warplanes are flying in the same territory. Anything could happen.”

~ Stephen Cohen

It wasn’t enough for these Democratic neocons to try and elect a woman who had been pushing for dangerous escalations with Russia since long before any hacking allegations and who campaigned on a promise to invade Syria and seize control of an airspace wherein Russian military planes were conducting operations. No, once their initial bid to start World War 3 failed, these deranged death cultists began attacking Trump for any movement away from escalations with Russia or regime change in Syria and showering him with praise when he launched a missile strike against a Syrian airbase. The current administration is culpable for its own actions and should be unequivocally condemned for bowing to these pressures instead of honoring Trump’s campaign promises of pursuing detente with Russia and avoiding regime change in Syria, but if Clintonists had been pushing for peace instead of war this entire time the situation would doubtless look very, very different.

Iran has accused the United States of interfering in its domestic affairs after calls by the US Secretary of State to support “elements” that would ensure a “peaceful transition” in the Islamic Republic. Tehran also officially delivered a note of protest to the UN. Speaking last Wednesday before the House Foreign Affairs Committee, Rex Tillerson said Washington will support efforts of a regime change in Iran. “Our policy towards Iran is to push back on this hegemony, contain their ability to develop obviously nuclear weapons, and to work toward support of those elements inside of Iran that would lead to a peaceful transition of that government. Those elements are there, certainly as we know,” Tillerson said on June 14. In addition to voicing Washington’s apparent support of a regime change, Tillerson also said the US could pursue sanctions on Iran’s entire Islamic Revolutionary Guard Corps.

Tillerson’s remarks sparked an avalanche of criticism and condemnation from Iran. In the latest development, the Iranian Foreign Ministry summoned the Swiss charge d’affaires to Tehran to protest Washington’s policy. The Embassy of Switzerland represents American interests in the Islamic Republic after the US cut diplomatic relations with Iran in April 1980 in the wake of the 400-day US Embassy hostage crisis of 1979-1981. “Following the interfering and meddling statements made by the US Secretary of State Rex Tillerson… the charge d’affaires of the European country was summoned to express Iran’s complaint about Tillerson’s anti-Iran remarks in the country’s House of Representatives,” Iran’s Foreign Ministry spokesperson said in a statement, Mehr News reported.

[..] Tillerson’s remarks “is a brazen interventionist plan that runs counter to every norm and principle of international law, as well as the letter and spirit of UN Charter, and constitutes an unacceptable behavior in international relations,” Iran’s UN Ambassador Gholamali Khoshroo said in the letter. Tehran further accused the US of violating the 1981 Algiers Accords, a set of agreements signed by Washington and Tehran to end the Iran hostage crisis. “The United States pledges that it is and from now on will be the policy of the United States not to intervene, directly or indirectly, politically or militarily, in Iran’s internal affairs,” Point I of the Accord reads.

On the ground, the Syrian army is now undertaking one of its most ambitious operations since the start of the war, advancing around Sueda in the south, in the countryside of Damascus and east of Palmyra. They are heading parallel with the Euphrates in what is clearly an attempt by the government to “liberate” the surrounded government city of Deir ez-Zour, whose 10,000 Syrian soldiers have been besieged there for more than four years. If they can lift the siege, the Syrians will have another 10,000 soldiers free to join in the recapture of more territory. More importantly, however, the Syrian military suspects that Isis – on the verge of losing Raqqa to US-supported Kurds and Mosul to US-backed Iraqis – may try to break into the garrison of Deir ez-Zour and declare an alternative “capital” for itself in Syria.

In this context, the American strike on Monday was more a warning to the Syrians to stay away from the so-called Syrian Democratic Forces – the facade-name for large numbers of Kurds and a few Arab fighters – since they are now very close to each other in the desert. The Kurds will take Raqqa – there may well have been an agreement between Moscow and Washington on this – since the Syrian military is far more interested in relieving Deir ez-Zour. The map is quite literally changing by the day. But the Syrian military are still winning against Isis and its fellow militias – with Russian and Hezbollah help, of course – although comparatively few Iranians are involved. The US has been grossly exaggerating the size of the Iranian forces in Syria, perhaps because this fits in with Saudi and American nightmares of Iranian expansion. But the success of the Assad regime is certainly troubling the Americans – and the Kurds.

So who is fighting Isis? And who is not fighting Isis? Russia claims it has killed the terrible and self-appointed “caliph of the Islamic State”, al-Baghdadi. Russia says it is firing Cruise missiles at Isis. The Syrian army, supported by the Russians, is fighting Isis. I have witnessed this with my own eyes. But what is America doing attacking first Assad’s air base near Homs, then the regime’s allies near Al-Tanf and now one of Assad’s fighter jets? It seems that Washington is now keener to strike at Assad – and his Iranian supporters inside Syria – than it is to destroy Isis. That would be following Saudi Arabia’s policy, and maybe that’s what the Trump regime wants to do. Certainly, the Israelis have bombed both the Syrian regime forces and Hezbollah and the Iranians – but never Isis.

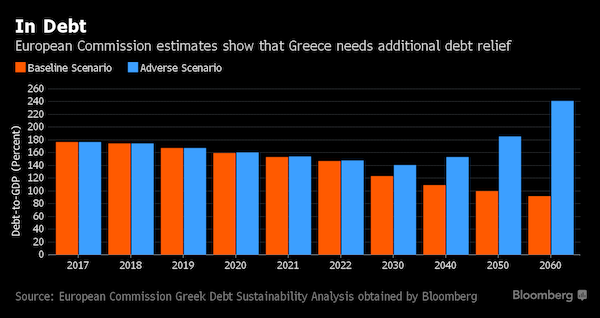

Greece will need additional debt relief to regain the trust of investors, even though it’s likely to exit its bailout with a €9 billion ($10 billion) cash buffer, the European Commission said in a draft report obtained by Bloomberg. The country’s €86 billion third bailout program from the European Stability Mechanism, agreed by Prime Minister Alexis Tsipras and European creditors in 2015, will expire in August 2018 with €27.4 billion left unused, the commission estimates in the so-called “compliance report” dated June 16. Disbursements up to then should also “cater for the build-up of seizable cash buffer” of around €9 billion, according to the document. The report contains an analysis of the country’s public debt that points to potential wrangling with the IMF following an agreement last week to disburse bailout funds, in which the fund only agreed to a new program “in principle.”

Even as the commission’s analysis points “to serious concerns regarding the sustainability of Greek public debt,” its assumptions about the country’s future growth prospects are still more optimistic than those of the IMF. The IMF hasn’t disbursed funds to Greece in almost three years on fears that the country’s debt is unsustainable. Last week’s compromise deal averts a Greek financing crisis this summer by allowing release of €8.5 billion of ESM funds, while the IMF holds out for more Greek debt relief from European creditors at a later stage before it gives out new loans. The June 15 deal by euro-area finance ministers commits to capping gross financing needs at 15% of GDP for the medium term, and 20% thereafter. The country’s gross financing needs will drop to 9.3% of GDP in 2020 from 17.5% this year, before rising again and surpassing 20% after 2045, according to the baseline scenario of the commission’s debt sustainability report.

[..] The baseline scenario is based on nominal GDP growth rates between 3 and 4% until 2060, considerably higher than past IMF baseline estimates. The fund’s own assessment will be released before its executive board meets to approve the in-principle stand-by arrangement next month. The debt dynamics “become explosive” from the mid-2030s in the the most adverse scenario. In this scenario, which is still more optimistic than IMF assumptions, Greece’s gross financing needs exceed 20% in 2033, reaching 56% by 2060, while debt skyrockets to 241.4% of Greek GDP by 2060.

The deal struck last week between Greece and its euro-zone creditors is business as usual – and that’s not a good thing. This protracted game of “extend and pretend” serves nobody’s long-term interests: not those of the Greek government, the IMF or, most of all, the people of Greece. Euro-zone finance ministers have unlocked a payment of €8.5 billion ($9.5 billion), the newest installment of a rescue plan worth €86 billion. This will let Athens make debt repayments of €7 billion that fall due next month. But there’s still no agreement on how to get Greece’s debt burden under control. The IMF had previously insisted that this question should be settled now. It was right, and it should have stuck to that position. The new agreement fails to recognize what everybody knows: that Greece’s debt is unsustainable on the current terms.

In an effort to pretend otherwise, Athens has promised primary budget surpluses (meaning net of interest payments) of 3.5% of GDP until 2022, and then of “above but close to 2%” until 2060. True, the Greek economy achieved a better-than-expected primary surplus last year. As the European recovery gathers pace, there could be more good fiscal news. But the idea that Greece can maintain this degree of fiscal control for the next 40 years is ridiculous. For instance, at some point during the next four decades, there might be another recession. Stranger things have happened. The blow to the credibility of the IMF could prove to be lasting damage. The fund points to its refusal to disburse money at this point as proof it’s serious about debt relief. Yet it remains a partner in a project that, by its own analysis, is bound to fail.

It should have said, enough. Europe doesn’t need the fund’s money or expertise. Governments only sought the fund’s seal of approval – and should have been denied it. Granted, the euro zone has done a lot to support Greece since its fiscal crisis began. Athens has been granted no fewer three rescue packages, worth €326 billion€ in total. The euro zone has allowed generous grace periods for official loans, extended their maturities and lowered the interest rate. As a result, Greece’s debt repayments are actually quite manageable for now.

The value of the local property market has plummeted some €2 trillion since the outbreak of the financial crisis eight years ago, according to the calculations of a Greek real estate consultancy. CBRE-Atria calculated that the Greek market has lost 65% of its value in the years from 2009 to 2017, dropping from about €3 trillion to €1 trillion today. The head of the consultancy, Yiannis Perrotis, says the problem is that the majority of properties are not quality assets, which means that the economic crisis has affected them more by increasing their value loss. “Properties such as old apartments in less popular areas, fields in non-touristic areas, stores or offices of low standards in secondary spots,” Perrotis explains, have been hardest hit.

The drop in values has been aggravated by the imposition of high taxation. It’s easy to find examples of properties whose value has dropped 60-65% in the last few years: Data from estate agents show that a new fifth-floor apartment of 60 square meters in Kypseli, central Athens, which sold for €150,000 in 2008, was resold at end-2016 for just €60,000, a decline of 60%; a newly built apartment in Ambelokipi, also in Athens, was sold for €270,000 before the crisis, and today is for sale for just €120,000, down 55%.

More than 120 refugees are feared to have drowned in the Mediterranean after a boat sank off the Libyan cost on Friday, the International Organization for Migration (IOM) has said. Four survivors who were rescued by Libyan fishermen said the boat sank after its motor was stolen by human traffickers, according to IOM spokesman Flavio Di Giacomo. After drifting for a while, the boat, believed to have been carrying 130 refugees — most of them of Sudanese and Nigerian nationality — capsized. News of the deaths comes on World Refugee Day, during which NGOs encourage the world to commemorate and show support for those forced to flee persecution. But there is little sign of the plight of refugees in the Mediterranean abating.

The death toll passed 1,000 in April — marking a record high with that figure not reached until the end of May last year — and the latest count by the IOM shows at least 1,850 have lost their lives on the dangerous crossing. Up to 146 people drowned when a refugee boat sunk in March, and up to 250 refugees, including a baby, were reported to have drowned in May after two refugee boats sunk in the Mediterranean Sea. It comes after a report earlier this month accused the EU of disregarding human rights and international law in its desperation to slow refugee boat crossings across the Mediterranean Sea. The bloc has pledged tens of millions of euros in funding for authorities in Libya, despite the country’s ongoing civil war and allegations of torture, rape and killings earning it the moniker “hell on Earth” among migrants, according to the report, published by the US-based Refugees International (RI) group.

U.S. President Donald Trump has told “confidants,” including the head of the Environmental Protection Agency Scott Pruitt, that he plans to leave a landmark international agreement on climate change, Axios news outlet reported on Saturday, citing three sources with direct knowledge. On Saturday, Trump said in a Twitter post he would make a decision on whether to support the Paris climate deal next week. A source who has been in contact with people involved in the decision told Reuters a couple of meetings were planned with chief executives of energy companies and big corporations and others about the climate agreement ahead of Trump’s expected announcement later in the week. It was unclear whether those meetings would still take place.

“I will make my final decision on the Paris Accord next week!” he tweeted on the final day of a G7 summit in Italy at which he refused to bow to pressure from allies to back the landmark 2015 agreement. The summit of G7 wealthy nations pitted Trump against the leaders of Germany, France, Britain, Italy, Canada and Japan on several issues, with European diplomats frustrated at having to revisit questions they had hoped were long settled. [..] Although he tweeted that he would make a decision next week, his apparent reluctance to embrace the first legally binding global climate deal that was signed by 195 countries clearly annoyed German Chancellor Angela Merkel. “The entire discussion about climate was very difficult, if not to say very dissatisfying,” she told reporters. “There are no indications whether the United States will stay in the Paris Agreement or not.”

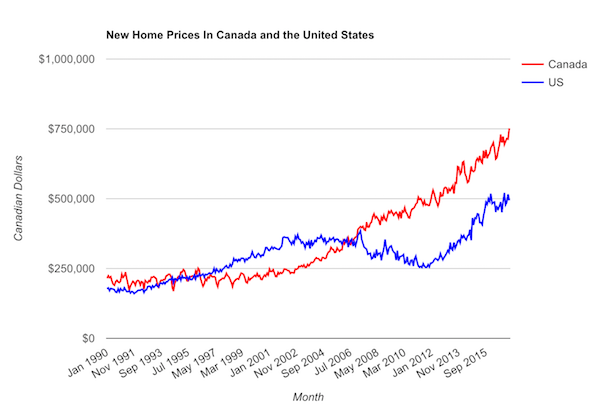

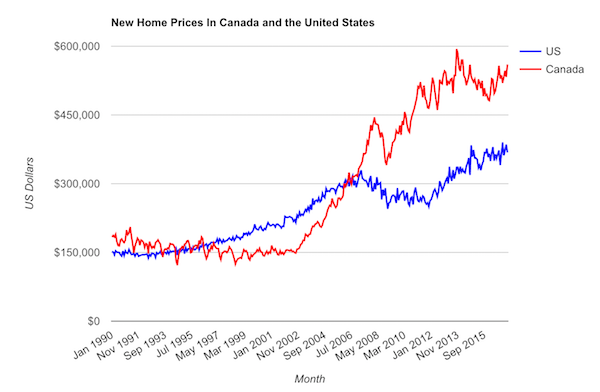

The price of new homes is quickly diverging in Canada and the US. Data from the Canadian Housing and Mortgage Corporation (CMHC) show that new homes are selling for substantially more than the same time last year. Meanwhile south of the border, data from the US Bureau of Census show that new home prices are on the decline. This has lead to an even wider gap between the average price of a new home in Canada and the US. The price of a new home across Canada is up for the second month in a row. The average sale price in April was CA$751,881 (US$559,123). This represents an 11% increase from the same time last year, when measured in Canadian dollars. When compared in US dollars, that increase drops to a much more conservative 2.64%. Even after factoring in the loonie’s decreased buying power in Canada, new home prices still climbed.

American new home builders aren’t seeing such steep climbs in sale prices. Actually, they aren’t seeing climbs at all. The average price of a new home in the US was CA$495,271 (US$368,300). This represents a 3% decline from the same time last year, when measured in US dollars. In Canadian dollars, this was a 0.49% decline from the same time last year. Both forms of measurement show declining home prices in the US, curious since their economy is in a much better state than Canada right now. New homes are trading at substantially higher values in Canada than the US in April. The average new home in April 2017 was 51% higher in Canada than the US. The same time last year, prices in Canada were only 36% higher. It appears in a post-crash United States, new home buyers are taking much more conservative strides. In a hasn’t-crashed-in-decades Canada, new home buyers are optimistic about future values.

Of all the dangers in the world of finance, the enduring low level of market volatility is the most significant. How quiet is quiet? Recently, the six-month realized volatility for the S&P 500 dipped to 6.7 percent, lower than even the period leading up to the financial crisis of 2008-09. During the mid-’90s, volatility was as low as it is now, but the size, complexity and interlinkages of financial market exposures were far less significant. Now, fluctuations are severely muted, and thus send a false signal of safety to both investors and policy makers who misread the calm as an “all clear” sign, dismissing the events above as insufficiently relevant. The result is an inability to appreciate how quickly market conditions can change, especially as trading strategies that capitalize on quiet markets become vulnerable to unwind, serving to amplify a risk-off event.