Inge Morath Street Corner at World’s End London 1954

Over the summer I introduced a two-fold assertion: 1) global economic growth is over (and has been for years and won’t come back for many more years) and 2) the end of growth marks the end of all centralization, including globalization. You can read all about these themes in “Globalization Is Dead, But The Idea Is Not” and “Why There is Trump” There are also extensive quotes of the second essay in wicked former UK MI6 spymaster Alastair Crooke’s “‘End of Growth’ Sparks Wide Discontent”.

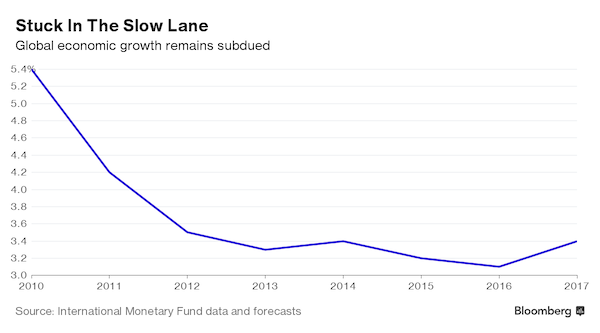

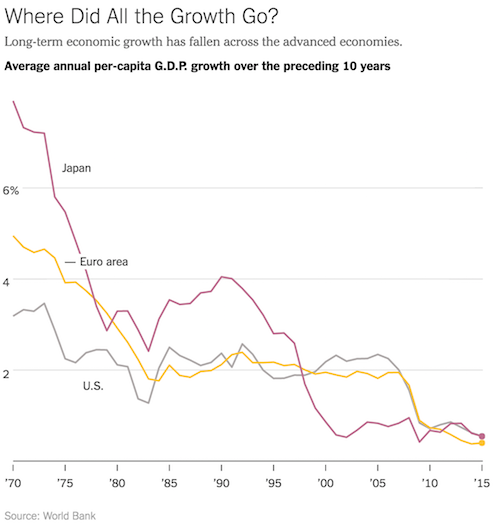

When I say ‘the end of growth’, I don’t mean that in a Limits to Growth kind of way, or peak oil or things like that. Not because I seek to invalidate such things, but because I mean economics, finance only. Our economies simply ceased growing, and quite a few years ago. The only reason that is not, and very widely, recognized is the $21 trillion and change that central banks have conjured up ostensibly to kickstart a recovery that always remains just around the corner.

That those $21 trillion will have massive negative effects on all of us is not my point either right now. Just that growth is gone. And that’s hard enough to swallow for a system that’s based uniquely on that growth. That is what this ‘essay’ is about: what consequences that will have.

All that said, I don’t have the idea that too many people are willing to accept the notion of the end of eternal economic growth (let alone right this minute), nor of globalization’s demise. Which may be partially understandable, but not more than that. Instead, quite a few people may honestly feel that the end of growth will make ‘leaders’ try for more, not less, centralization/globalization, but that, if it happens, is temporary. Unless, as I wrote earlier, we see dictators in the west.

Because, as I said in those articles, the overbearing principle is, and must be, that when centralized power ceases to deliver benefits to people, they will no longer accept that decisions about their – ever poorer- lives are taken by people hundreds or thousands of miles away from where they live. People allow that only when they reap sufficient benefits from it. With growth gone, there are no such benefits left. Look at Greece and Italy and Brexit, and look at why Trump is where he is.

Since it will apparently take a while for the above to sink in – which is not because I’m wrong-, I’m a little hesitant to introduce the next assertion, which is very closely related to the other two and takes it a step further. That assertion is that there are multiple countries in the western world -and perhaps beyond- today that run a serious risk of becoming de facto ungovernable. I’ll refrain from using the term anarchy.

I’ve been playing around in my head for a while with the thought that it is striking that the last two major global powers, which together have dominated world politics and economics for over 200 years, look well on their way towards becoming ungovernable. It is perhaps even more striking that nobody appears to understand or even contemplate this.

Both Britain and America are caught in an apparent trap in which various groups of their citizens blame each other for everything that’s going wrong with their lives -which admittedly is plenty-. But that’s where the end of growth and globalization comes in: societies are in urgent need of new ways of organizing themselves, of formulating new goals, priorities and policies.

And since nary a soul recognizes that the old ways have expired, this is bound to be a very difficult process. Before formulating anything new, we will first see (well, we already do) forces, movements and individuals rise to the fore whose claim to fame is kicking against the existing grain without providing much in the way of -coherent- ideas of what should come next.

In fact, most of these ‘transitory forces’ don’t even realize or acknowledge the need for any novel paradigms; they -often hugely- gain in popularity basing themselves on talk of tweaking existing paradigms, on the notion of pretty much leaving things as they are but with a few different focus points here and there. Re-arranging deckchairs.

And if anyone would try on ‘real change’, they’d likely be voted down in record numbers, because the end of growth will mean loss of wealth and prosperity everywhere. And neither the people nor the times are ready for that message. Let alone the media machine or the establishment it serves. Which would rather go to war than admit they lost and give up their profits.

Before moving on to the most prominent and perhaps urgent examples, the US and UK, let’s take a look at a handful or so European countries. By the way, the European Union is a prime example of an entity that is caught blinded on the way towards being ungovernable like a deer in 27/28 pairs of headlights. No growth, no EU.

In the same way that, as I explained in the earlier articles, all supranational entities face the fate of the dodo. Or at least the existing ones do, with their structures geared towards ever increasing centralization of power and money. Countries, societies, people will always find ways to trade and cooperate, and they will again, but the next time they do it will be only if and when they keep control over decisions that concern what’s important to them.

But on to those European countries on their way towards challenging existing power structures and governability. Italy has a -constitutional- referendum on December 4, and it looks right now like PM Renzi will lose that, opening the way for our friend Beppe Grillo and his M5S Five Star movement to take over. Beppe wasn’t against the euro when we met in 2010, but he is now. And M5S has since grown hugely, into a solid national force.

In the rich core of the EU, there are general elections in Holland in March 2017, France in April and Germany in September 2017. Holland’s traditional parties have been losing clout for a long time, and Geert Wilders’ anti-Islam anti-EU pro-Freedom party scores big in the polls. And that in a country that says it’s doing great, talks about raising wages across the board and is stuck in a massive housing bubble.

France has a president, Hollande, who’s polling lower numbers (a while ago it was 6%) than any US president probably ever did in history, and that’s saying something. France has new crown princes on Hollande’s Socialist side in PM Manuel Valls and Economy Minister Emmanuel Macron, but they are badly tainted by Hollande’s ‘achievements’.

They have old crown princes for the Republican conservative party in ex-PM Sarkozy and the for some reason very popular Alain Juppé, but both can really only try and steal votes from Marine Le Pen’s Front National by leaning ever further right. Which leaves Le Pen, who has sworn to take France out of the EU, as the no. 1 contender.

Given what might happen in Italy, Holland and France, one must wonder what the September 2017 German elections will even matter anymore when they happen. Unless an M5S type movement stands up there, Merkel will have no choice but to pull sharply to the right to try and hold off the right wing AfD from getting into a kingmaker position. Germany’s once proud and strong left wing movement looks bound for near extinction.

Belgium and Spain don’t have elections scheduled for 2017, but both have recently endured long periods without functioning governments, and both look no closer to solving the issues than they were before. Just look at Wallonia blocking the CETA trade deal between the EU and Canada. One might say they already are, for all intents and purposes, on the verge of being ungovernable.

Grillo, Wilders, Le Pen and Spain’s Podemos are very different people and movements, but what they have in common is they can produce such a backlash in their respective countries, win or lose, that they can render the existing political structures obsolete and thereby their countries ungovernable. Maybe, then, those structures are already obsolete, and maybe that’s why they’ve gained such popularity?!

Plenty of candidates in Europe for governmental chaos; and I haven’t even touched on many countries, including in Eastern Europe, where the end of growth will shatter many dreams and promises of better lives that have been put on hold indefinitely. Even as many Czechs and Polish workers risk being sent back home from countries like Britain. Europe truly is a continent full of powder kegs. Even before you add refugees.

However, I still think the US and UK are first in line when it comes to the risk of being rendered ungovernable. Partly simply because of timing, and partly because the differences between various ‘groups’ and movements are as pronounced as they are already today. Both countries are running out of carpet to sweep their dirt under.

A conspicuous part in all this is played by the nations’ respective media, who seem to have given up all attempts at pretending to be neutral, a.k.a. ‘journalistic’. Traditional media, newspapers and radio and TV channels, used to have reporters and then, separately, they would have opinion columns, and the difference would be clear. But that’s all gone, every single article is now an opinion piece, which goes a long way towards explaining why people turn their backs on them.

The MSM media are digging their own graves. Or, rather, their graves were being digitally dug anyway, and they’re greatly speeding up the process of their own demise. What America and Britain would need right now is a ‘traditional media outlet’ -just one- that is actually objective; the first one that tries that approach could make a killing, but all are scared of being killed in the process.

Moreover, most ‘reporters’ have fooled themselves into thinking that they ARE objective; that ‘objective’ means Trump and Brexit MUST be condemned, as well as everyone and everything that has anything to do with the two, and some that don’t, like Putin. Which happens to play a major role into how both countries inexorably slide down into a state of chaos.

Their traditional political parties are self-immolating as we speak, and yet in neither country is there space for new parties to stand up. That seems to be a major difference (perhaps it’s an Anglo thing?) from countries in continental Europe, and even there things are screaming out of hand. The post-growth model appears to be: new parties or not, the incumbents are toast. Plenty room for big gaping holes.

Post Brexit, the UK has the Tories, who lost the Brexit vote but for some reason are still in power, just with a different figurehead. But they are hopelessly divided in pro-Brexit and pro-EU factions, and they appear so far to be messing up anything at all having to do with Brexit. All the egos collide too, of course; egos are all that politics has left to provide us.

Then there’s the Labor Party, which is equally hopelessly divided into the pro-Corbyn camp and the anti-Corbyn ‘Blairites’, which have conducted a kind of guerrilla warfare that might put the Viet Cong to shame. The Blairites have made such a fuss over Corbyn not being electable that they made their wishes come true like a boomerang. But that’s the MPs, not the voters or even the party members, who are behind Corbyn in massive droves.

The UK doesn’t have a general election scheduled until 2020, but with all the infighting and even more importantly the ‘real’ start of Brexit that’s supposed to come in early 2017, and/or a potential parliamentary vote seeking to make the referendum null and void, it’s hard to see how the country could NOT descend into total chaos way before 2020.

The people who were comfortable before June 23 blame it all on ‘Brexiteers’, but they conveniently forget that before that date they completely ignored the people who did vote to Leave the EU, and are therefore now grasping at straws when it comes to explanations. The term ‘deplorables’ has been patented by the Hillary camp, but it seems to express quite well how Remain feels about Brexit voters today. And that’s toxic for any society.

This is just not good enough. Brexit voters from what I can see are a mix between those who have been hit hardest by former PM Cameron and his goon squad (and ignored by Remainers), and those who really find the EU a failed experiment, an aspect I rarely see discussed in Britain. They should be elated to be rid of Brussels, but it’s all only about how much money they will have short term, not about identity or pride or anything.

A country full of people pointing fingers at others, while remaining blind to their own failures. The mote and the beam, a recipe for mayhem. So you have this entire godawful political mess, and now imagine throwing in the end of growth, and deteriorating economic circumstances from here on in.

Britain had better start some kind of National Conversation first on where it wants to go, hire something in the vein of a bunch of National Therapists to tell people it’s not okay to blame everything on somebody else, whether they’re Brits or foreigners, or, with Scotland planning another independence vote, we could be back all the way to Braveheart.

That leaves the US. The country that has elections before any of the other ‘basket cases’. And, this being America, the land that’s better than anyone at painting pictures of itself as tempting as they can be false, the antagonism is dripping off the walls and through the streets. The land that discusses which lives matter.

It’s glaringly obvious that the majority of the US media would like you to believe that when it comes to ungovernability, a Trump victory would be a sure bet to lead the US into political mayhem. That may be true, though it’s by no means guaranteed, they make it up as they go along, but a Hillary win may well end up being even worse.

As I wrote mid-September in “Hillary Became Unelectable Long Ago”, Mrs. Clinton faces a ton of unanswered questions that will not just go away just because she might win a vote. If anything, scrutiny may well increase, and a lot, if she wins on November 8. And that’s not just because the Donald is a sore loser (which also may or may not be true).

There are a lot of intelligence (FBI) voices protesting the decision to not charge Hillary for her email shenanigans. There are plenty of serious issues related to the capture of the DNC by Hillary’s campaign, and the subsequent ousting of Bernie Sanders and all his supporters. The campaign went so far as to pay people to -violently- disrupt Trump events. Now spell democracy for me.

What may play an even bigger role going forward is the unrelenting blame game played by the campaign on Russia and Vladimir Putin, a litany of allegations for which precious little proof, if any, has been presented. Trying to link Putin to Trump to Julian Assange may have seemed a winning election strategy, and it may prove to be one, crazy as it is, but on November 9 the world will still keep turning and-a churning. And where are they all then?

Trump will not forget this. The Republicans won’t. The FBI won’t. All the people who support Wikileaks won’t. Vladimir Putin won’t. And neither will the leaders of a lot of other countries. They have now seen that sovereign nations and their leaders can be used as cannon fodder in a US election, or any other US political purposes, and that’s going to make them feel queasy, and then some, for a long time.

It’s very hard to see how Hillary and her people, as well as the American media, can climb down from the stance they’ve taken. It’s not exactly something you can easily apologize for after the fact. So the only thing to do would be to dig in and persevere.

For the media, as I said, it’ll be merely another step towards irrelevance. Just a bit steeper. For Hillary and her supporters, it won’t be that smooth of a way down. When they dig in deeper into their trenches, all that’s left them is to try and escalate the Russia tension.

But while an attack on Russia may go down reasonable well in American minds, Hillary would need to involve NATO, and there are plenty of member countries, and their citizens, who will not accept anything of the kind, no matter what their leaders say. The fact that NATO relies on unity would become a liability instead of an asset, in the same way that the EU will experience.

NATO would fall apart if the US under a Hillary presidency attacks Russia. So would the EU, which will fall apart anyway. And that’s just on the international front.

Domestically, the Obama reign has been ‘saved’ by those trillions from the Fed, by the crazy growth in debt, both public and private, and by a list as long as your arm of questionable ‘official’ data, unemployment numbers, personal ‘wealth’, that sort of thing. While we all know that there would not be a Trump if those numbers reflected Americans’ real lives.

Trump may go away, though it won’t be in silence, but what he represents will not. And what he represents is 180º squarely removed from Hillary. And it’s not going to be subdued, silent or obedient. Blaming that on Trump, or on things he says, misses the point by a mile.

Given what the Hillary campaign has perpetrated, given the links to the Clinton Foundation, and given a ton of other things, it’s not all that crazy that Trump says he may not accept an election result off the bat. And given what many voices in the Democratic party, including Obama, have said in the past about elections and systems being rigged, it’s nonsense to try and demonize him for suggesting that.

Of course American elections can be rigged. Hanging chads or not. As long as people have to wait in line for hours in certain districts to cast their vote, and as long as Diebold machines are used, they can be rigged. But you can’t say it out loud?

Look, if Trump wins, how docile will the Democrat crowd be, given the propaganda machine targeted at Putin and Assange and anyone else (Bernie!) who dared stand in Hillary’s way? If the result is close, will Hillary accept it without a single protest or question? She won’t. But if Trump says he’ll keep you in suspense about the exact same thing, he’s a threat to democracy itself?

Points of view and belief are so far apart that indeed, democracy is under threat. But not because of Trump. That threat goes back to times long before him.

Hillary owes her position, and her wealth, to the Saudis and Qataris and Wall Street banks and US industrial/military neocons. And they will all demand that she return the favor. But they want something completely different than the people who vote for her. And since the economy is shrinking, she will have to take whatever it is they demand in return for putting her on her pedestal, away from the people who voted for her.

And no matter how much propaganda is unleashed upon Americans, as they see their lives deteriorate, they will be on to this, more and more. And they will lean towards Trump or Bernie Sanders -or someone else in the future-, anyone they feel expresses their frustration.

Hillary won’t be able to ‘cure’ the economy any more than Obama has, she won’t have the Fed’s virtual trillions to help her veil the real state of the economy, and she’s already close to the lowest ‘likeability’ rate in history to begin with.

I’m thinking Trump would probably be an awful president, but he perhaps wouldn’t be the worst option. And I’m saying that from the point of view of keeping America governable going forward, something he may well screw up yuugely, but at least he’s not certain to.

It’ll be hard to keep America quiet in the years to come whoever wins, and I’m going to have to think about this more, I just wanted to say for now that what many people think and claim is a given, is not. And that is a big thing given that the elections are only 16 days away.

![U.S. Secretary of State John Kerry sits with British Prime Minister Theresa May in the White Room No. 10 Downing Street in London, U.K., on July 19, 2016. [State Department Photo]](https://consortiumnews.com/wp-content/uploads/2016/07/28376382456_56ae215c9f_k.jpg)