Labour Campaign Poster 1922

I know the echo chamber won’t agree, but after watching quite a bit of it, four things stood out for me in the Comey testimony, other than the somewhat too loud remarks about how the entire White House lied about him and the FBI:

1) He admitted to leaking information of his private talk with Trump in the Oval Office. Comey said he didn’t understand why Trump asked everyone to leave the room, but, well, perhaps it’s this: that if anything leaked, it would be clear whodunnit. And leaking info about a private talk with your president is not an obvious thing to do. Illegal? Borderline? Comey stated that he did it because he thought it would lead to a special counsel being appointed. But who is he to ‘promote’ such a thing?

2) He finally said in public that Trump himself had not been under investigation, something the president had asked him to do on three occasions. There was some excuse about not doing it because he might have to walk that back later, but the fact remains: no Trump investigation, and despite all other leaks, no public acknowledgement of that.

3) Comey insisted in no uncertain terms that the entire US intelligence community is convinced that Russia interfered in the 2016 elections, and Russia here means the Kremlin, re: Putin. Well, let’s finally see the proof.

4) He recounted how then-AG Loretta Lynch pushed him to relabel the criminal investigation into the Clinton server as a “matter”, a term the Clinton campaign used. But why would an AG do it too, and push the FBI to do the same? Very odd. And then Comey added that this was a reason to call the press conference in which he advised the Department of Justice not to indict Clinton.

• Trump Accuses Comey Of Lying About Leaked Memo (ZH)

As we detailed earlier, during his testimony today, former FBI Director Comey testified that he only leaked the memo about his contact with the President AFTER he saw President Trump’s tweet…

COMEY: I asked — the president tweeted on Friday after I got fired that I better hope there’s not tapes. I woke up in the middle of the night on Monday night because it didn’t dawn on me originally, that there might be corroboration for our conversation. There might a tape. My judgement was, I need to get that out into the public square. I asked a friend of mine to share the content of the memo with a reporter. Didn’t do it myself for a variety of reasons. I asked him to because I thought that might prompt the appointment of a special counsel. I asked a close friend to do it. [..] A close friend who is a professor at Columbia law school.Pretty clear – it was a response to a tweet. But, as President Trump’s personal lawyer Marc Kasowitz states: “Today, Mr. Comey admitted that he unilaterally and surreptitiously made unauthorized disclosures to the press of privileged communications with the President. The leaks of this privileged information began no later than March 2017 when friends of Mr. Comey have stated he disclosed to them the conversations he had with the President during their January 27, 2017 dinner and February 14, 2017 White House meeting. Today, Mr. Comey admitted that he leaked to friends his purported memos of these privileged conversations, one of which he testified was classified.

He also testified that immediately after he was terminated he authorized his friends to leak the contents of these memos to the press in order to “prompt the appointment of a special counsel.” Although Mr. Comey testified he only leaked the memos in response to a tweet, the public record reveals that the New York Times was quoting from these memos the day before the referenced tweet, which belies Mr. Comey’s excuse for this unauthorized disclosure of privileged information and appears to entirely retaliatory. We will leave it the appropriate authorities to determine whether this leak should be investigated along with all those others being investigated”

So the question is – having called President Trump a liar, did Comey just get caught in an even bigger lie… ?

At least on his personal involvement.

• Chris Matthews: “There’s No ‘There’ There” On Trump-Russia ‘Collusion’ (ZH)

If you count yourself among the die-hard, disaffected Hillary supporters still holding out hope that President Trump will be impeached for conspiring with Russian spies to stage a coup in the United States, then you may want to sit down because earlier today one of your biggest cheerleaders just threw in the towel on that whole narrative. Yes, MSNBC’s very own Chris Matthews, the same man who confessed he “got a thrill up his leg” from simply watching Obama speak, admitted today that Comey’s testimony pretty much confirmed that “there’s no ‘there’ there” when it comes to Trump colluding with the Russians.

“The assumption of the critics of the President, of his pursuers, you might say, is that somewhere along the line in the last year is the President had something to do with colluding with the Russians … to affect the election in some way. Some conversation he had with Michael Flynn or Pual Manafort or somewhere.” “And yet what came apart this morning was that theory in two regards…the President said, according to the written testimony of Mr. Comey, go ahead and get any satellites of my operation and nail them. I’m with you on that…” “And then also, Comey said that basically Flynn wasn’t central to the Russian investigation.” “And I’ve always assumed that what Trump was afraid of was that he had said something to Flynn and Flynn could be flipped on that and Flynn would testify against the President that he’d had some conversation with Flynn in terms of dealing with the Russians affirmatively.” “And if that’s not the case, where’s the there-there?”

And when Chris Matthews throws in the towel on a liberal narrative, you know the gig is up. Oh, and by the way, this probably doesn’t help your case either… Burr: “Director Comey, did the President at any time ask you to stop the FBI investigation into Russian involvement in the 2016 U.S. elections?” Comey: “Not to my understanding, no.” Burr: “Did any individual working for this administration, including the Justice Department, ask you to stop the Russian investigation?” Comey: “No.”

Theresa May can stay until the Tories throw her out; she’s proven to be an awful liability, not a leader. Far too risky. How much would she lose next time around? Their problem is there’s no-one else who’s obvious, there must be dirty fights in dark and rainy alleys first.

So: Tories will throw out May, while Corbyn will have to throw the Blairites out of Labour who made his position a living hell.

Most likely seems Corbyn as PM of a minority government. But that’s a big risk going into Brexit talks.

• Theresa May Has ‘No Intention Of Resigning’ After Losses (BBC)

The UK faces the prospect of a hung parliament with the Conservatives as the largest party after the general election produced no overall winner. With nearly all results in, Theresa May faces having fewer seats than when she called the election. The Tories are projected to get 318 seats, Labour 261 and the SNP 35. Jeremy Corbyn has urged the PM to resign but the BBC understands she has no intention of doing so at this stage and will try to form a government. The prime minister has said the country needs stability after the inconclusive election result and the BBC’s political editor Laura Kuenssberg said Mrs May intended to try and govern on the basis that her party had won the largest number of votes and seats.

Labour is set to make 29 gains with the Tories losing 13 seats – and the SNP down by 22 seats in a bad night for Nicola Sturgeon, with her party losing seats to the Tories, Labour and Lib Dems. The Conservatives are forecast to win 42% of the vote, Labour 40%, the Lib Dems 7%, UKIP 2% and the Greens 2%. Turnout so far is 68.7% – up 2% up on 2015 – but it has been a return two party politics in many parts of the country, with Labour and the Conservatives both piling up votes in numbers not seen since the 1990s. UKIP’s vote slumped dramatically but rather than moving en masse to the Tories, as they had expected, their voters also switched to Labour.

New elections? One positive for the former Empire: the threat of Scottish independence was wiped out.

• This Is Where Theresa May’s Arrogance Will Lead Us Next (Ind.)

Despite a lot of the good news streaming out of counts everywhere right now, make no mistake: this is going to be chaos. A deep and growing sense of frustration is about to ripple through the country, because what May has essentially done in her arrogance is take a gamble that could cost us decades of stability and prosperity. It is likely that what awaits us over the next few weeks is, to put it bluntly, a mess. Hung parliament. No clear majority. No willingness to form a coalition. A possible resignation from the Prime Minister (whether she’s pushed or jumps is yet to be seen) and then yet another leadership contest. Boris Johnson is said on the Westminster grapevine to already be positioning himself as a candidate, yet his reputation has turned increasingly sour over the last few years.

Many now regard him as a cynical power-grabber without much regard for the people he claims to represent. The Tories have spent the last two years playing Russian roulette with the electorate in the hope of cementing their credibility, and causing utter shambles along the way. Having barely recovered from a referendum result which caused deep divisions and painful rifts within our society, and as Europe watches us scramble for any sort of political legitimacy, who will now head into the talks that will determine our economic and political future? Theresa May has now shoved us off a cliff into political unknowns just when what we actually needed was, ironically enough, some strong and stable leadership.

Any reassurance from Westminster that the lives of ordinary people in this country mattered more than political point-scoring would be welcome. What we’ll get instead, despite the Labour surge, is yet another election, whether that be in two months’ or two years’ time. It feels inspiring and hopeful that we have so many progressive and wonderful MPs back in the Commons. But until we have a government and a plan of how to get ourselves through this, that hope is limited to a symbolic step in the right direction. In the words of one particularly concise campaign poster: strong and stable, my arse.

It’s going to get terrible no matter what. But for now the EU has no-one to talk to. They’re not going to sit down with May if she may last only a few more weeks.

• UK’s Shock Election Result May Hamper Brexit Talks, EU Leaders Warn (G.)

The EU will force a humiliated Theresa May to explain her intentions at a face-to-face meeting in Brussels as senior diplomats and politicians warned that the hung parliament resulting from the UK election was a “disaster” that hugely increases the chance of a breakdown in the Brexit negotiations. The result is likely to delay the point at which Michel Barnier, the EU’s chief negotiator, has someone with whom to negotiate. Sources said a meeting of the European council on 22 June was the deadline by which time the EU27 would want to know the prime minister’s plans. Guenther Oettinger, the German member of the European commission, said: “We need a government that can act. With a weak negotiating partner, there’s the danger than the negotiations will turn out badly for both sides … I expect more more uncertainty now.”

It had been hoped that officials from both sides would have informal talks next week over the logistics of the negotiations, before formal talks began on the week starting 19 June. With the prime minister needing to both seek to form a minority or coalition government, as well as potentially revise her goals for the talks in the light of the election result, the original timetable seems unrealistic to officials in Brussels. The EU had, until now, believed it understood that May wanted to take the UK out of both the single market and the customs union, but in the early hours of Friday morning the Brexit secretary, David Davis, had suggested the election result could prompt a rethink.

All on red.

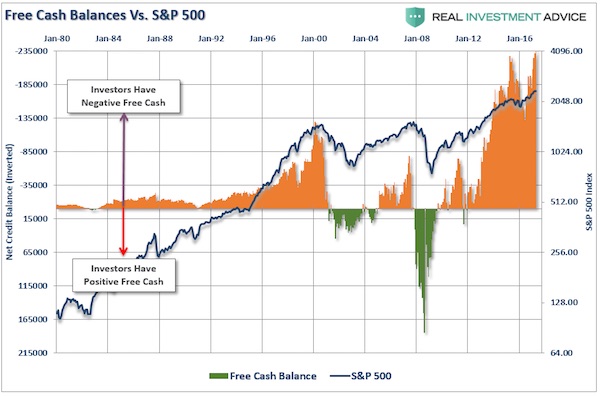

• The Myth of “Cash on The Sidelines” (Roberts)

[..] despite 8-years of a bull market advance, one of the prevailing myths that seeming will not die is that of “cash on the sidelines.” To wit: “Underpinning gains in both stocks and bonds is $5 trillion of capital that is sitting on the sidelines and serving as a reservoir for buying on weakness. This excess cash acts as a backstop for financial assets, both bonds and equities, because any correction is quickly reversed by investors deploying their excess cash to buy the dip,” Nikolaos Panigirtzoglou, the managing director of global market strategy at JPMorgan, wrote in a client note. This is the age old excuse why the current “bull market” rally is set to continue into the indefinite future. The ongoing belief is that at any moment investors are suddenly going to empty bank accounts and pour it into the markets.

However, the reality is if they haven’t done it by now after 3-consecutive rounds of Q.E. in the U.S., a 200% advance in the markets, and ongoing global Q.E., exactly what will that catalyst be? However, Clifford Asness previously wrote: “There are no sidelines. Those saying this seem to envision a seller of stocks moving her money to cash and awaiting a chance to return. But they always ignore that this seller sold to somebody, who presumably moved a precisely equal amount of cash off the sidelines.” Every transaction in the market requires both a buyer and a seller with the only differentiating factor being at what PRICE the transaction occurs. Since this must be the case for there to be equilibrium to the markets there can be no “sidelines.”

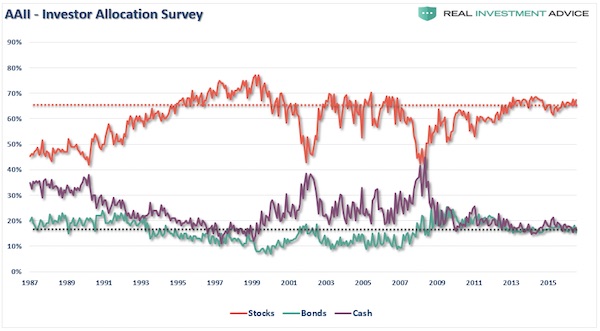

Each month, the Investment Company Institute releases information related to the mutual fund industry. Included in this data is the total amount of assets invested in mutual funds, ETFs and money market funds. As a rough measure of investor sentiment, this indicator looks at the total assets invested in equity mutual funds and ETFs, and compares it to the total assets invested in the safety of money market funds. The higher the ratio, the more comfortable investors have become holding stocks; the lower the ratio, the more uncertainty there is in the market. Currently, with the ratio at the highest level on record there is little fear of holding stocks. Negative free cash balances also suggest the same as investors have piled on the highest levels of leverage in market history.

Furthermore, with investors once again “fully invested” in equities, it is not surprising to see cash and bond allocations near historic lows. Cash on the sidelines? Not really. Everyone “all in the boat?” Absolutely. Historical outcomes from such situations? Not Great.

The No Price Discovery Bubble.

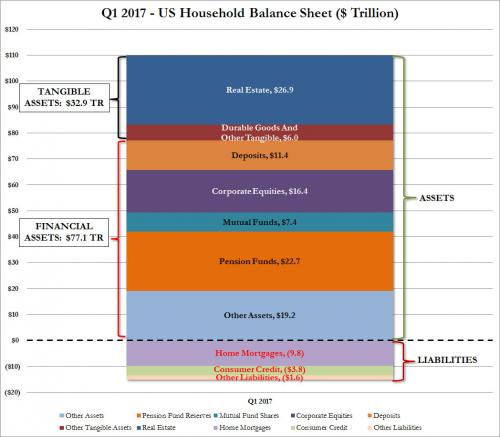

• US Household Net Worth Hits Record $95 Trillion… There Is a Catch (ZH)

In the Fed’s latest Flow of Funds report, today the Fed released the latest snapshot of the US “household” sector as of March 31, 2017. What it revealed is that with $110.0 trillion in assets and a modest $15.2 trillion in liabilities, the net worth of the average US household rose to a new all time high of $94.835 trillion, up $2.4 trillion as a result of an estimated $500 billion increase in real estate values, but mostly $1.78 trillion increase in various stock-market linked financial assets like corporate equities, mutual and pension funds, as the stock market continued to soar to all time highs . At the same time, household borrowing rose by only $36 billion from $15.1 trillion to $15.2 trillion, the bulk of which was $9.8 trillion in home mortgages.

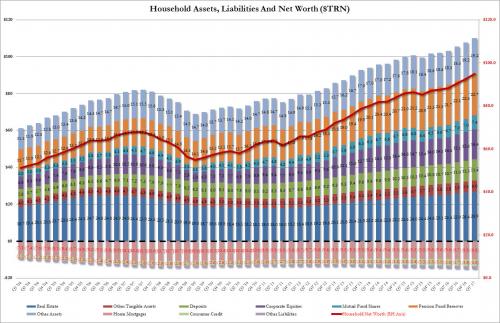

And the historical change of the US household balance sheet.

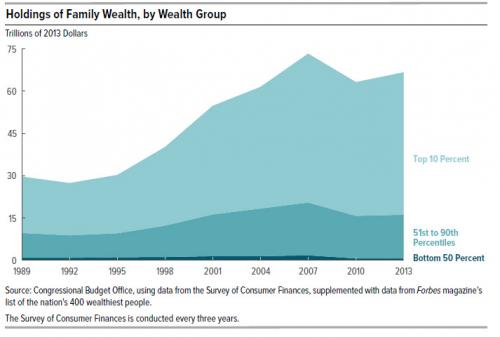

And while it would be great news if wealth across America had indeed risen as much as the chart above shows, the reality is that there is a big catch: as shown previously, virtually all of the net worth, and associated increase thereof, has only benefited a handful of the wealthiest Americans. As a reminder, from the CBO’s latest Trends in Family Wealth analysis, here is a breakdown of the above chart by wealth group, which sadly shows how the “average” American wealth is anything but.

While the breakdown has not caught up with the latest data, it provides an indicative snapshot of who benefits. Here is how the CBO recently explained the wealth is distributed: In 2013, families in the top 10% of the wealth distribution held 76% of all family wealth, families in the 51st to the 90thpercentiles held 23%, and those in the bottom half of the distribution held 1%. Average wealth was about $4 million for families in the top 10% of the wealth distribution, $316,000 for families in the 51st to 90th percentiles, and $36,000 for families in the 26th to 50th percentiles. On average, families at or below the 25th percentile were $13,000 in debt In other words, roughly three-quarter of the $2.4 trillion increase in assets went to benefit just 10% of the population, who also account for roughly 76% of America’s financial net worth,

Trump and Congress had better go out and do something.

• Opioid Overdoses The Leading Killer Of American Adults Under 50 (ZH)

The opioid crisis that is ravaging urban and suburban communities across the US claimed an unprecedented 59,000 lives last year, according to preliminary data gathered by the New York Times. If accurate, that’s equivalent to a roughly 19% increase over the approximately 52,000 overdose deaths recorded in 2015, the NYT reported last year. Overdoses, made increasingly common by the introduction of fentanyl and other powerful synthetic opioids into the heroin supply, are now the leading cause of death for Americans under 50. And all evidence suggests the problem has continued to worsen in 2017. One coroner in Western Pennsylvania told a local newspaper that his office is literally running out of room to store the bodies, and that it was recently forced to buy a larger freezer. The initial data points to large increases in these types of deaths in states along the East Coast, particularly Maryland, Florida, Pennsylvania and Maine.

In Ohio, which filed a lawsuit last week accusing five drug companies of abetting the opioid epidemic, the Times estimated that overdose deaths increased by more than 25% in 2016. In some Ohio counties, deaths from heroin have virtually disappeared. Instead, the primary culprit is fentanyl or one of its many analogues. In Montgomery County, home to Dayton, of the 100 drug overdose deaths recorded in January and February, only three people tested positive for heroin; 97 tested positive for fentanyl or another analogue. In some states in the western half of the US, data suggest deaths may have leveled off for the time being – or even begun to decline. Experts believe that the heroin supply west of the Mississippi River, traditionally dominated by a variant of the drug known as black tar which is smuggled over the border from Mexico, isn’t as easily adulterated with lethal analogues as the powder that’s common on the East Coast.

Fake News.

• Trump’s $110 Billion Arms Deal With Saudis Mostly Speculative (RT)

That $110 billion arms deal President Donald Trump signed with Saudi Arabia isn’t much of a deal at all, according to reports which found the majority of the agreement was based on memos, rather than contracts. On May 20, Trump negotiated an arms deal with Riyadh. The State Department said it was worth nearly $110 billion to support “the long-term security of Saudi Arabia and the Gulf region in the face of malign Iranian influence and Iranian related threat.” White House Press Secretary Sean Spicer hailed it the “largest single arms deal in US history.” The State Department then released a general list of the weapons that were included in the deal. However, many experts have said that most of the arms sales had not been cleared by the State Department, Congress or even the industries themselves.

On Thursday, Defense News released a more detailed list of the weapons included in the deal, according to documents they obtained from the White House. The ‘deal’ lists $84.8 billion under memos of intent (MOI) “to be offered at visit,” and $12.5 billion under letters of agreement (LOA), rather than contracts. NPR also obtained a list of commercial deals from a White House spokeswoman and found that it added up to $267 billion, but said most of the deals were listed as “memoranda of understanding” (MOU). “There is no $110 billion deal,” Brookings Institution Senior Fellow Bruce Riedel wrote in blog post Monday. “Instead, there are a bunch of letters of interest or intent, but not contracts,” Riedel said. “Even then the numbers don’t add up. It’s fake news.”

So what did they do to prove that?

• Defense Minister Kammenos Says US Is Greece’s Best International Ally (K.)

Washington is Greece’s only true international ally, Defense Minister Panos Kammenos insisted on Thursday, and accused the country’s European partners of showing a lack of respect. “The Greek people are well aware that the United States has been the country’s only genuine ally,” Kammenos said. “The others are allies, but they are [allies] only in the form of creditors, without [any sense of] respect and this is because some of them will never forget that they lost World War II to this country,” Kammenos, who is also leader of junior coalition partner Independent Greeks, added during a speech marking the 70th anniversary of the US Office of Defense Cooperation in Athens yesterday. “For this reason, we welcome US support at this very difficult moment for our country,” said Kammenos, who also called for the strengthening of the Hellenic Navy with US help so “that it can operate from Crete to the Suez.”

Bolstering the navy and the country’s military aviation capabilities are necessary, he said, to intercept the flow of drugs, weapons and fuel through which terrorism is funded. He also said that Greece is positively inclined to extend the time frame of the defense agreement between the two countries, adding that Prime Minister Alexis Tsipras and his government are working in that direction. He also referred to the latest developments in the Gulf states and stressed that he supports describing the Muslim Brotherhood as a terrorist organization. Aiming his fire at Turkey, he said that each country must choose “whose side they want to be on.” It is certain, he said, that “Greece will be on the side of the US.” For his part, US Ambassador to Greece Geoffrey Pyatt praised relations between Athens and Washington, adding that as Greece’s economy stabilizes, it will become even more active in its role as a bridge between countries of the region.

Nobody cares unless you hold their feet to the fire.

• European Court Of Justice: Refugee Crisis Trumps Dublin Regulation (K.)

Any countries in the European Union receiving asylum requests from refugees have an obligation to process them irrespective of where the applicants first entered into the bloc, an advocate general at the European Court of Justice said on Thursday. Eleanor Sharpston said in a non-binding opinion that under the “exceptional circumstances” of the refugee crisis, member states should not be bound by the Dublin Regulation’s requirement that first-entry states handle all asylum applications, even after a refugee or migrant has moved on to a different country. “The words ‘irregular crossing’ in the Dublin III Regulation do not cover a situation where, as a result of the mass inflow of people into border member states, those countries allowed third-country nationals to enter and transit through their territory in order to reach other member states,” she wrote.

Sharpston referred to the case of a Syrian national who traveled to Slovenia via Croatia and that of an Afghan family that entered Europe in Greece and then made its way to Austria. Slovenia and Austria should be responsible for examining their asylum applications, she said. “If border member states… are deemed to be responsible for accepting and processing exceptionally high numbers of asylum seekers, there is a real risk that they will simply be unable to cope with the situation,” Sharpston wrote. “This in turn could place member states in a position where they are unable to comply with their obligations under EU and international law,” she added.

The last thing Greece has left is rumored to be on the way out.

• The Shield of Law and Humanism (K.)

It is difficult to believe that after Greece’s judiciary offered protection to eight members of the Turkish military, rejecting Ankara’s request for their extradition, the government would agree to the illegal, secret and inhuman expulsion of people who requested asylum here. Yet unease grows. On Wednesday the government spokesman stated, “The Greek government does not engage in pushbacks.” Let us hope that is so. The Hellenic League for Human Rights cites two instances where groups of Turkish citizens who requested asylum in Greece appear to have been handed over illegally to Turkish authorities. The Council of Europe’s commissioner for human rights, Nils Muiznieks, the UN High Commissioner for Refugees and the head of the Alliance of Liberals and Democrats in the European Parliament, Guy Verhofstadt, have expressed concern at the possibility.

There is also the strange story of three Turkish military men who where arrested in Edirne last month, accused of being part of a group that intended to kidnap President Recep Tayyip Erdogan during the failed coup last July. Turkish media said the men were arrested while on their way to Greece; some Greek lawyers, however, claim that the three had crossed into Greece when they disappeared, only to turn up in Turkish custody. The Citizens’ Protection Ministry in Greece scoffed that the claims were “fairy tales.” The case of the eight servicemen who arrived in Alexandroupoli in a helicopter the day after the coup attempt shows how difficult it is for any country to withstand Ankara’s pressure. It is understandable that no government would like to open a new front with a neighbor who can cause problems at will. But it is of paramount importance that Greece withstand such pressures.

In the past few years, among our country’s very few victories were the welcome provided to refugees and the institutional way in which it dealt with the “Eight.” Our great wound, though, is the lack of strategy, of method, of goals – of follow-up. On the refugee issue, government incompetence undermined the initial, heroic efforts of citizens. In the case of Turkish asylum seekers, the difficulties of handling the case of the Eight should not lead to cynicism, to injustice, to the violation of international conventions. Greece has a responsibility toward its own people and toward the Turkish people, to serve the principles of humanism, to abide by the law. Strenuous defense of these principles is part of the identity we aspire to but also our shield. And it is the best thing that we can offer our neighbors – the hope that there is something better than that which they are now enduring.