Floris van Schooten Still-Life with Glass, Cheese, Butter and Cake 1st half 17th century

Dark money

Just a reminder that Mark Zuckerberg spent $400 million on the 2020 election. They had no problem with big tech influence on the election until Elon backed Trump. pic.twitter.com/Ndw2TGj4Ss

— Clint Russell (@LibertyLockPod) October 20, 2024

MSNBC

NEW: MSNBC has a struggle session after Donald Trump picked up a shift at McDonald’s, says Trump is “not well.”

Mission successful.

“There's no logic to it. It's a stunt.”

“He, as you know, appears to be not well. And he's engaged in some really bizarre types of activities… pic.twitter.com/GScpyy4niD

— Collin Rugg (@CollinRugg) October 20, 2024

Speaker

Just this week a Democrat-leaning publication called Trump “Hitler, Mussolini, and Stalin” all rolled into one. Leading Dems in DC have said even worse.

Is it a surprise that such rhetoric leads unstable people to violence?

The constant lies about Trump are dangerous. pic.twitter.com/dTgTbJx69y

— Speaker Mike Johnson (@SpeakerJohnson) October 20, 2024

PA

JUST IN: Donald Trump thanks @ElonMusk for campaigning for him in Pennsylvania.

"And so I just want to thank Elon Musk."

"But when you look at his endorsement, when he endorsed me, I mean, he's now going around all over Pennsylvania, day and night, day and night, it's like he's… pic.twitter.com/ETfLiZwgXV

— Kyle Becker (@kylenabecker) October 20, 2024

https://twitter.com/i/status/1848133402559721646

JD

BOOM: JD Vance just called out the Democrats that say the McDonalds visit was staged:

“The fact that some are accusing President Trump of a "staged" event… OF COURSE he has to have security after two attempts on his life in two months.”

“He was talking to the employees, he was… pic.twitter.com/DIQ3uvWMe7

— Gunther Eagleman™ (@GuntherEagleman) October 21, 2024

Trump Biden

https://twitter.com/i/status/1848020588679348583

No tax

Q: Will you commit to protecting Social Security and Medicare?

TRUMP: "The answer is yes… People on fixed income have been decimated by the Biden and Harris regime."

— Benny Johnson (@bennyjohnson) October 20, 2024

Racist

If Donald Trump is a racist, he is really bad at it. Listen until the end. pic.twitter.com/rzcfXwZePB

— Insurrection Barbie (@DefiyantlyFree) October 21, 2024

Bronx

NEW: Trump visits a barber shop in the Bronx.

A retired NYC Detective asked: ‘how do we control sanctuary cities, because New York is a sanctuary city.”

Trump: ‘We get rid of them… you know what they’re for? Criminals’

America is fed up with funding these people’s existence… pic.twitter.com/zOSOWt7qMF

— Gunther Eagleman™ (@GuntherEagleman) October 21, 2024

DOJ

“That’s what they are doing to me.” pic.twitter.com/ntMfj2B7vb

— James Hirsen (@thejimjams) October 21, 2024

“Donald Trump is probably the current biggest threat to the free world. His buddy Musk [is] at least public enemy number two..”

• Musk Fires Back At Der Spiegel Over ‘Enemy No. 2’ Claim (RT)

Elon Musk has hit back at German magazine Der Spiegel, after it branded the billionaire “public enemy No.2” and claimed he is working with Republican presidential candidate Donald Trump to “decompose liberal democracy.” In response, Musk insisted that he is a staunch defender of democracy. The German outlet published an article on Sunday with a cover depicting a close-up of the tech mogul with Trump’s features emerging through part of his face. The piece noted that the X owner and Tesla CEO has amassed huge economic clout and a prominent media profile. “Within a few years, he [Musk] has not only become the political right-wing hardliner, but also a declared opponent of the liberal democracy in the US. The Troll-in chief has mutated into a political agitator.

“One could say: Donald Trump is probably the current biggest threat to the free world. His buddy Musk [is] at least public enemy number two,” the article said, drawing parallels with Nazi leader Adolf Hitler, who rose to power thanks in no small part to the support of German industrial moguls. Musk addressed the accusation during a townhall meeting with American voters in Pennsylvania. “I’m like, enemy No. 2 of what? Democracy? I mean I’m pro-democracy. I’m literally trying to uphold the Constitution and ensure we have a free and fair election,” he fired back, drawing cheers from the crowd.

The billionaire added that he would “definitely upgrade… my security” after the article, noting that he is sometimes “shocked” by what he sees from the left. “You know, the level of vitriolic hatred on the left, which is supposed to be tolerant. They claim they are tolerant and yet they are incredibly intolerant and spewing hate.” Musk, a self-described “free speech absolutist,” endorsed Trump after the failed assassination attempt on the former president in July, and has since donated tens of millions of dollars to his campaign. He has repeatedly expressed concern about what he describes as increasing censorship in the US, as well as an overbearing bureaucracy that prevents any meaningful action. Meanwhile, Trump has vowed to create a Musk-led government efficiency commission to audit the entire federal government if he returns to the White House.

“The left’s ideas have failed and failed spectacularly, and all they have left is cheating.” Elizabeth Nickson.

• Surprise, Surprise! (James Howard Kunstler)

Of course, there’s no “pandemic” this time to cover for the trip that the Party of Chaos wants to lay on the country, no excuse for gross and glaring ballot fuckery, for the days of anxious uncertainty following an election. Everybody and his uncle expect a gigantic tantrum to follow November 6 if Mr. Trump somehow overcomes the tide of bogus harvested votes, illegal alien votes, phantom overseas votes, voting machine swapped votes, lost-and-found votes, last-minute rafts of votes, and other products of the Marc Elias election sabotage machine. I am not so sure that the tantrum will materialize. Despite the orgy of Orwellian language inversions you have been subjected to in recent years, and the bending of reality it induced, you will know a real insurrection if you see it. You already know the real reason the Democratic Party went insane: its crime spree against the citizens of this land was so obvious and outrageous that a thousand Beltway bureaucrats are now going crazy in fear of prosecution.

The tantrum everyone expects them to provoke would be a real insurrection and they are liable to find themselves in even deeper trouble for resorting to it. Crime is the whole reason for the Democrats’ desperation. There was no “policy” the past four years, only crime. The Covid operation was a mass murder. The open border was not something that just happened, like a spell of bad weather. It was a colossal racketeering operation. They worked it hard. “Joe Biden” paid dozens of NGO cut-outs to systematically jam more than ten million sketchy interlopers into the country, and then support them lavishly with cash payments when they got here. The political prosecutions of AG Merrick Garland are gauche and lawless. The pervasive censorship by DHS and other agencies is an affront to our constitution. The transgender campaign is a malicious prank against American children (and their parents).

Our CIA may be a party to the fentanyl crisis. The war in Ukraine is a failed resource-grab, unbelievably stupid in inception. “Joe Biden’s” empty treasury is writing trillions in IOUs to stealthily bail out the banks and jack-up the stock market. Everything about our government has become criminal and those responsible for it know they are bound for a reckoning now. Will the Democrats’ Antifa street-army be allowed to terrorize the cities? I expect the remaining cops not de-funded in DC, New York, Chicago, and LA won’t hold back this time, no matter what mayors Muriel Bowser, Eric Adams, Brandon Johnson, and Karen Bass tell them to do. You will instead see the return of something that has been missing for years: a sense of duty to public safety and the common good. Won’t that be a surprise? And there will be nothing that the FBI can do about. It’s one thing to incite a riot among a mob of ordinary middle-aged folks moiling around the US Capitol. It’s another thing to try to subvert the police in carrying out their duties. New heroes will emerge and there will be no ambiguity about what happens.

Black Lives Matter had already been outed as a lowlife money-grubbing hustle. But the Democratic Party may no longer depend on its old “plantation” field-hands to stage mostly peaceful anarchy and arson if the election goes the wrong way for the masters. Forty years of pretending to be an oppositional culture hasn’t worked. It was just minstrelsy updated, when all was said and done. Too many black men are rising up to speak out in support of Donald Trump, and of one America, and of acting like men. They appear to be tired of self-stigmatizing as designated victims in the Woke-Jacobin DEI psychodrama. A new generation of black male leaders is emerging to replace embarrassing con artists like Al Sharpton, Michael Eric Dyson, and Ibram X. Kendi. It’s been a long time coming.

“..while the Democrats accuse Trump of planning to use the military on the American people, the government is already making moves to do just that..”

• Alex Jones Issues Terrifying Post-Election Prediction (VF)

He forecasts that once Trump becomes president, “Black Lives Matter, Antifa, and all these Islamic hordes that are allied with the left” will “engage in massive civil unrest.” The possibility is certainly real. And this scenario becomes even more terrifying when you realize that Senator Richard Blumenthal (D-Connecticut) is working on a bill to cripple Trump’s ability to respond to civil unrest. Specifically, Blumenthal is introducing legislation to limit unchecked presidential authority under the Insurrection Act ahead of Trump’s forecasted victory. What the bill means, if passed, is that Trump will be severely handicapped in the face of widespread violence and unrest. Blumenthal’s legislation is designed to handcuff the president by requiring approval from Congress before the military can be deployed to deal with domestic threats.

Adding to the possibility of civil unrest, Bill Gates, the man who seems to always financially profit when disaster happens, said in 2022 that America’s “political polarization may bring it all to an end.” He predicted that at some point, “We’re going to have a hung election and a civil war.” The trigger to civil unrest could be the election, of course. However, Alex Jones warned that an incident like the one we saw with George Floyd in 2020 could be exploited again to spark widespread riots. Jones pointed out that while the Democrats accuse Trump of planning to use the military on the American people, the government is already making moves to do just that. Adding to all the things that can go wrong is U.S. Department of Defense Directive 5240.01, which is an absolute nightmare.

What that directive does is that it gives the DoD the power to step in and use lethal force within U.S. borders, even against its own citizens, when it deems lives are at risk. Don’t want to wear a mask? You’re putting lives at risk. Lethal force could technically be used against you. Don’t want to take a vaccine? The same story exists. The potential for abuse is limitless here. The scope of this authority is chilling because the directive specifically states that the decision to use lethal force only needs the Secretary of Defense’s approval. Once lethal force is approved, anything can happen. For years, Alex Jones warned about martial law and domestic military control, and now we’re seeing that terrifying scenario unfold right before our eyes.

https://twitter.com/i/status/1848122086826606881

“Only 31 percent express a “great deal” or “fair amount” of confidence in the media. Adults with no trust at all in the media is greater at 36 percent. In the 1970s, trust in the media ranged from 68 percent to 72 percent.”

• A Citizen Journalist Wins Key Reversal for New Media (Turley)

This week, there was a little-noticed order out of the Supreme Court that decided a narrow legal question with much great implications for journalism. The justices tossed a decision of the United States Court of Appeals for the Fifth Circuit that barred a lawsuit by Priscilla Villarreal. Known online as La Gordiloca (loosely translated as “the fat, crazy lady”), Villareal is part of a growing number of new media journalists. At a time when the public is rejecting legacy or mainstream media, the case is the latest reminder of a rising force of citizen journalists. Technically, the court instructed the lower courts to review the case in light of the recent decision in Gonzalez v. Trevino. That decision relaxed the standards for citizens suing over retaliatory arrests. Villareal was not just a citizen but a citizen journalist who claimed to be performing the same newsgathering functions as conventional journalists.

Villarreal had alleged that she was arrested for seeking and obtaining nonpublic information from police as a journalist — the identity of a person who had killed himself — and publishing it on Facebook. The Fifth Circuit ruled that the police could claim immunity from the lawsuit she brought, and the justices just set that decision aside. As I discuss in my book, “The Indispensable Right, journalism is in free fall in the U.S. as citizens reject the establishment media as biased and unreliable. For years, journalism schools have taught students that they have to abandon objectivity and neutrality for advocacy. Advocacy journalism is now the norm. Former New York Times writer (and now Howard University journalism professor) Nikole Hannah-Jones has declared that “all journalism is activism.” Emilio Garcia-Ruiz, editor-in-chief at the San Francisco Chronicle, similarly announced that “Objectivity has got to go.”

After a series of interviews with more than 75 media leaders, Leonard Downie Jr., former Washington Post executive editor, explained that objectivity is viewed as a trap and reporters “feel it negates many of their own identities, life experiences and cultural contexts, keeping them from pursuing truth in their work.” The response of the public has been to look elsewhere for news. Indeed, the mantra “Let’s Go Brandon!” was embraced by millions as a criticism of the media as much as it was a criticism of President Biden. Recently, the new Washington Post publisher and CEO William Lewis was brought into the paper to stop a collapsing readership and revenue. He told the staff, “Let’s not sugarcoat it…We are losing large amounts of money. Your audience has halved in recent years. People are not reading your stuff. Right? I can’t sugarcoat it anymore.”

They are, however, reading “the stuff” of figures like La Gordiloca, who is described as “a tattooed one-woman mobile newsroom who, until the coronavirus lockdown, often broadcast live while driving her car.” Her following on Facebook is now larger than her local newspaper. The New York Times described how La Gordiloca “reflects how many people on the border now prefer to get their news.” The paper admitted that she is is a “swearing muckraker who is upending border journalism.” New media journalists are more H.L. Mencken or sometimes even Hunter S. Thompson but they are viewed as more authentic and independent. Millions of Americans now get their news from social media and blogs. Various traditional media outlets have either closed or are fighting for their existence. What they are not doing is seriously questioning their course in adopting advocacy journalism.

Journalism has become a ship of fools who increasingly write for each other rather than the dwindling numbers of actual readers. And they have written off half of the country with their plunge into advocacy journalism. As a consequence, many have come to view mainstream media as a de facto state media. Today, over half of U.S. adults (54 percent) say they get news from social media. Only 27 percent now rely on TV as their first choice with only 6 percent preferring radio and only 5 percent preferring print. The recent polling figures from Gallup show how much harm this generation of editors and reporters has done to the field. Trust in the media is at an all-time low, continuing a consistent decline. Only 31 percent express a “great deal” or “fair amount” of confidence in the media. Adults with no trust at all in the media is greater at 36 percent. In the 1970s, trust in the media ranged from 68 percent to 72 percent.

Turley

Jonathan Turley: CEOs like Zuckerberg caved like a house of cards, but Musk couldn't be coerced or scared. They'll never forgive him for that.

“It's like another scene out of The Lord of the Flies. You have all these pundits and politicians chasing him around the island, and… pic.twitter.com/kuwXQIq8kO

— ELON DOCS (@elon_docs) October 21, 2024

He wants a bonus, but: “..the plaintiff had argued against Twitter paying the bonus while he was under employment with the firm..”

• Court Denies Class Action Status for Lawsuit Against Twitter (ET)

A California court dismissed class action certification for a lawsuit filed by a former employee that accused Twitter of not paying laid off workers bonuses that were allegedly promised. Mark Schobinger, the plaintiff, was Twitter’s senior director of compensation during 2022–23, a time when the company was in the process of being acquired by Elon Musk, according to an Oct. 16 order issued by the U.S. District Court, Northern District of California. At the time, Schobinger was a member of a group of employees eligible to receive annual bonuses in early 2023. However, the company was under no obligation to pay, a fact that is “undisputed” under the terms of the bonus, the order noted. Paying the bonus was “a matter of discretion” for the firm. Schobinger alleged that the company promised employees in April, May, and August of 2022 that it would pay the bonus provided the workers stayed with the firm throughout the acquisition.

The plaintiff claimed he did stay during this phase because of the promise. He filed the lawsuit after not getting paid, and sought class certification. On Wednesday, U.S. District Judge Vince Chhabria denied Schobinger’s motion, noting he is unfit to act as a class representative. The judge pointed out that the plaintiff had argued against Twitter paying the bonus while he was under employment with the firm. In November 2022, months after Twitter’s bonus promise, Schobinger sent a message to the company’s “Head of People Experience,” stating that whether to pay the bonus was purely dependent on the “discretion” of Musk. Schobinger also wrote that he recommended not to pay the bonus. In February 2023, the plaintiff sent a “white paper” to several executives on the issue, stating that “not paying a bonus would be prudent.” Evidence also points to Schobinger telling Musk in a meeting a month earlier that the firm need not pay the bonus, the order stated.

These statements make Schobinger “not an adequate class representative,” Chhabria wrote. “At his deposition, Schobinger offered a convoluted explanation for how he could possibly have believed he was entitled to the bonus while simultaneously advocating that the company not pay it. It seems likely that Schobinger’s explanation is untrue,” the judge said. “But even if he is telling the truth, that’s beside the point for purposes of this motion. Because even if he is telling the truth, his conduct makes him the worst possible candidate to serve as a litigation representative for the other Twitter employees who didn’t get a bonus.” The court also highlighted a major issue with the motion—a “large number” of proposed class members signed arbitration agreements with Twitter, some of which also waived off class action lawsuits against the company.

“In Russian diplo-speak, “restraint” means “Russia will not intervene if you do your worst”.

• Russian “Restraint” Towards Assassination of Arab Leaders (Helmer)

The Libyan leader Muammar Qaddafi was murdered on October 20, 2011, and to mark the thirteenth anniversary of his death, the Russian Foreign Ministry received Qaddafi’s daughter, Aisha Qaddafi, in Moscow on Friday. This is the first open meeting in Russia between high-ranking Russian officials and the Qaddafi family. The political significance was buried in the communiqué. “On October 18, the Special Representative of the President of the Russian Federation for the Middle East and Africa, Deputy Minister of Foreign Affairs of Russia Mikhail Bogdanov received Libyan public figure and artist Aisha Gaddafi, who is in Moscow in connection with the opening of an exhibition of her paintings at the State Museum of the East. During the conversation, issues of further strengthening historically friendly Russian-Libyan ties in the scientific, cultural and educational spheres were discussed.

At the same time, the Russian side confirmed its unchanged position in support of achieving Libyan national accord in the interests of ensuring the unity, territorial integrity and state sovereignty of Libya.” The official reason for Aisha Qaddafi’s visit to Moscow to open the exhibition of her paintings omitted that the paintings are in memory of her father, brother and other members of her family assassinated by the US and its proxies in Libya. “I show these works for the first time to honour my father and my brother on the anniversary of their deaths,” Qaddafi said in Moscow. “I can tell you that these pictures are painted not with my hand but with my heart.” Assassination of Qaddafi had been a secret US Government policy during the Carter Administration and then an open policy of the Reagan Administration.

Assassination of the Arabs of Palestine, including the leaders of Hamas and Hezbollah, is the open policy of the current US and Israeli governments. In this context, the unofficial reason for Aisha Qaddafi’s visit to Moscow is that the Russian Foreign Ministry is signaling its opposition to this decades-old US and Israeli policy. The signal also hints through several years of rumour and disinformation at fresh Russian support – that means armed protection – for Saif Qaddafi’s campaign to become the end-of-civil war president of Libya. “If the Libyans choose a strong president,” Saif told the New York Times in 2021, “the only thing is a strong president. That’s it. The Libyans will choose a strong one. Everything will be solved automatically.”

“Allegations of Pyongyang supplying soldiers and equipment to Russia were originally raised by Ukrainian leader Vladimir Zelensky last week..”

• EU Troops Could Be Deployed To Ukraine – Politico (RT)

The EU should return to the idea of putting boots on the ground in Ukraine, Lithuanian Foreign Minister Gabrielius Landsbergis has argued in a statement to Politico. The diplomat insisted that Brussels should revive talks about deploying EU forces in Ukraine in response to reports of North Korean ammunition and soldiers supposedly taking part in the hostilities on the side of Russia. “If information about Russia’s killing squads being equipped with North Korean ammunition and military personnel is confirmed, we have to get back to ‘boots on the ground’ and other ideas proposed by Emmanuel Macron,” Landsbergis told the outlet. Allegations of Pyongyang supplying soldiers and equipment to Russia were originally raised by Ukrainian leader Vladimir Zelensky last week and have been seconded by South Korea.

However, neither the US nor NATO has yet been able to confirm any of these reports, while Moscow has dismissed the speculations as a “bogus story.” Meanwhile, Macron’s continued refusal to rule out the potential deployment of French troops to Ukraine has repeatedly been criticized by other EU leaders who have argued that such a move would lead to a serious escalation of the conflict. At the same time, Brussels is reportedly considering the possibility of deploying peacekeepers to Ukraine after the conflict has ended, Politico has said. Washington’s former ambassador to Japan, Kenneth Weinstein, has told the outlet that such a move would show that the EU still has “skin in the game.”

“If there is going to be a DMZ [demilitarized zone] between Ukraine and Russia, my suggestion would be to have it manned by EU troops — not NATO troops, and not U.S. troops,” the former diplomat, who is now chairman to the Hudson Institute, a conservative DC-based think tank, told the outlet. One EU lawmaker, who chose to remain anonymous, has also confirmed to Politico that the question of European peacekeepers in Ukraine “will come up” after the conflict is over. Moscow has repeatedly warned against the deployment of Western forces to Ukraine. Russian President Vladimir Putin has stressed that such a move could lead to a “serious conflict in Europe and a global conflict.”

“..over the weekend the Pentagon refused to back the reports, with Secretary of Defense Lloyd Austin explaining that he can’t confirm this narrative..”

• Pentagon Pours Cold Water On Claim Of North Korean Troops In Ukraine (ZH)

Ukrainian President Volodymyr Zelensky has of late begun pushing hard new accusations that at least 10,000 North Korean troops are being sent to Ukraine where they will fight on behalf of the Russians. South Korea’s spy agency had also backed Zelensky’s claim, chiming in on Friday to say that at least 1,500 North Korean special forces have already been sent. The spy agency says it has satellite images tracking these movements. But over the weekend the Pentagon refused to back the reports, with Secretary of Defense Lloyd Austin explaining that he can’t confirm this narrative. “I’ve seen those reports in the media. I can’t confirm those reports at this point in time. This is something that we will certainly continue to investigate,” Austin said Sunday.

Zelensky has been pushing the idea that the ‘enemies’ of the West have formed an axis to fight in Ukraine and ultimately push back NATO. He’s identified them as Russia, Iran, and North Korea. He’s touted this curiously alongside desperate pleas for more urgent funding and weaponry from his Western backers. Kiev has especially sought long-range weapons for use inside Russian territory. As an example of this, Zelensky said in a weekend video address, “Now we have clear evidence that people are being supplied to Russia from North Korea, and these are not just workers for industries, but also military personnel. And we expect a normal, honest, strong reaction from our partners to this.” He followed by emphasizing, “In fact, this is another state joining the war against Ukraine.”

But not even NATO leadership is backing these assertions. NATO Secretary-General Mark Rutte recently said there’s no evidence of an influx of North Korean troops into the conflict. “At this moment, our official position is that we cannot confirm reports that North Koreans are actively now as soldiers engaged in the war effort,” he stated. Some video clips of unknown context, origin or location have circulated online in the past days, purporting to show North Korean troops being outfitted by Russia’s military before battle. Pundits have described one circulating video as showing a base in Russia’s eastern Primorye region, which shares a small border with North Korea, incredibly far away from front lines in Ukraine.

“..there should be a “full-fledged counterweight” to the US, such as during the time of the USSR..”

• Medvedev Warns Of ‘Total War’ (RT)

The US must abandon its ambitions of “world domination” or risk a war which could lead to the “complete extermination” of humanity, former Russian President Dmitry Medvedev warned on Monday. According to Medvedev, who currently serves as the deputy head of Russia’s Security Council, Washington’s goal is “domination over the Old World, as well as over the rest of the world.” However, this policy is merely leading to the “weakening and humiliation of the West, including Europe” within the framework of the modern multipolar global order, Medvedev wrote on his Telegram channel. The official issued the post in the context of the upcoming BRICS summit in the Russian city of Kazan, which is set to kick off on Tuesday. Medvedev argued that the world needs a balance of powers rather than a dominant one, meaning there should be a “full-fledged counterweight” to the US, such as during the time of the USSR.

The development of BRICS as a global power, as well as the growth of similar regional unions and the comprehensive development of relations with the countries of the Global South, are signs that such a balance is already in the making, Medvedev argued. “After all, the alternative to such a balance of power is a total war leading to the complete extermination of humanity,” the senior official warned. A world without balance in today’s conditions will not last even a decade. If the West does not realize this simple truth, it is the end for everyone. And this is not a situation where the death of some will mean the victory of others. Medvedev was Russian president from 2008 to 2012, before serving as prime minister until 2020. He is well known for his hardline stance on the Ukraine conflict and the West’s sanctions policy against Russia. He has also accused the US of pursuing a “global neocolonialism” agenda.

BRICS, which is widely seen as a rival to the G7 group of countries, is holding its 16th annual summit later this week. Initially founded in 2006 by Brazil, Russia, India, and China, it now consists of nine countries, including South Africa, Egypt, Iran, Ethiopia and the UAE, representing about 46% of the world’s population and over 36% of global GDP, according to estimates by global financial institutions. Many analysts have suggested that the rapid development of the group signals that the Western monopoly over the international system is over, and that the world is firmly headed toward multipolarity.

“This summit could mark the beginning of the end of Western supremacy and the emergence of a new era..”

• A New World Order In The Making: This BRICS Summit Will Be Special (Behanzin)

The upcoming BRICS summit in Kazan, Russia could mark a turning point in global geopolitical history. Faced with the slow erosion of the Western world order, a new balance is emerging, driven by a coalition that seems increasingly determined to chart its own course. This unique event brings together 24 heads of state from various nations, including iconic figures such as China’s Xi Jinping. The inclusion of Antonio Guterres, the Secretary-General of the United Nations, in this assembly raises major questions about the current dynamics of global governance. Traditionally, the UN has been seen as a bastion of multilateralism, but its alignment with the Western powers is being called into question. This summit in Kazan could be the catalyst for a strategic repositioning, where the UN might seek to navigate between old alliances and emerging trends.

The BRICS are no longer just an economic coalition; they are asserting themselves as a viable alternative to the historical dominance of Western countries. The unipolar world, as we have known it, seems to be giving way to a multipolar era, where several emerging powers are claiming their rightful place in the global decision-making process. The Kazan summit represents an unprecedented opportunity for the BRICS to draw a new map of international cooperation. The heads of state present will discuss a multitude of issues, ranging from the economy to security, including environmental challenges. By forming strategic alliances, this group, which represents over 45% of the world’s population, seeks not only to strengthen its influence but also to offer an alternative platform for developing countries that often feel marginalized within traditional Bretton Woods institutions like the IMF or the World Bank.

These discussions could lead to agreements that, depending on their scope, might redefine the rules of the international economic game. The West, rather than standing on the sidelines, is forced to respond to the growing and increasingly popular BRICS dynamic. Western governments, which often disagree and are divided over their approaches, may be compelled to reassess their relationship with emerging market countries. The current situation is marked by growing tensions, as illustrated by the declining confidence in Western-centered institutions. The stance of NATO and European actors towards the BRICS could become the focus of heated debates, highlighting an inevitable need for adaptation.

By attending this event, Guterres is likely illustrating the UN’s desire to revitalize its role in a changing world. His intervention could underscore the growing importance of South-South dialogue, and exchanges aimed at establishing cooperative partnerships that transcend the usual divides. [..] Multilateralism, as it was conceived after World War II, is facing a period of uncertainty. Established institutions struggle to effectively address contemporary challenges such as climate change, growing inequality, and governance crises. The BRICS summit could offer a new vision of multilateralism, more inclusive and adapted to current realities. This model could create synergies among the countries of the Global South, proposing an alternative to the rigidities of the current Western framework.

The future looks fascinating with the BRICS summit in Kazan. This is not just a series of diplomatic discussions but a laboratory for forging a new global architecture. As the West may witness a redistribution of power in international affairs, the developing countries, represented by the BRICS, are taking the reins of this transformation. This summit could mark the beginning of the end of Western supremacy and the emergence of a new era where the voice of the Global South is finally heard. The events in Kazan thus promise to have lasting repercussions on how we conceive the world order in the decades to come.

‘Not an Anti-Western Group, Just a Non-Western Group’

• Date With Destiny – BRICS Offers Hope in a Time of War (Pepe Escobar)

This is it. A date with destiny. All set for the most crucial geopolitical/geoeconomic gathering of the year and arguably the decade: the BRICS Summit under the Russian presidency in Kazan, capital of Tatarstan, where Sunni Tatars coexist in perfect harmony with Orthodox Christians. All the excruciating work by sherpas and analysts throughout 2024 – supervised by the lead Russian diplomat in charge of BRICS, Deputy Foreign Minister Sergey Ryabkov – converged to three final, separate key meetings in Moscow before the summit, grouping BRICS finance ministers and central bank governors, working groups, and the Business Council. All that in a context that is now familiar for the Global Majority. The combined GDP of the current BRICS nations is over $60 trillion, way ahead of the G7; their average growth rate by the end of this year is projected to be 4%, higher than the 3.2% global average; and the bulk of economic growth for the near future will come from BRICS member-nations.

Even before the meeting of finance ministers and central bank governors, Russian Finance Minister Anton Siluanov was stressing that BRICS is keen to bypass “politicized” Western platforms – a subtle reference to the sanctions tsunami and the weaponization of the US dollar – as BRICS work to create their own, Global Majority-friendly international payments system. The context for what will be decided in Kazan this week is no less than incandescent, as the uncontrolled chaos of the Hegemon’s Forever Wars – from Ukraine to West Asia – has even materially affected the heavy work of BRICS and the necessity to build a new international system of geoeconomic relations practically from scratch. A credible war escalation scenario may have been thwarted by the leak of secret high-level intel to the Five Eyes on the preparations by Israel-US to strike Iran. The strike will eventually happen – with dire consequences – but probably not this week, when it could have been timed to explicitly, and completely, disrupt the summit in Kazan and expel it from global headlines.

The joint statement by the BRICS finance ministers and central bank governors may not sound too adventurous, but the constraints reflect not only caution when facing a dangerous, cornered Hegemon, but internal contradictions among BRICS members. The statement recognizes “the need for a comprehensive reform of the global financial architecture to enhance the voice of developing countries and their representation.” Yet it remains clear the US has less than zero interest in a profound reform of the IMF, the World Bank and the Bretton Woods system. Russia and China, especially, are fully aware that what is needed is a post-Bretton Woods. The statement is more forceful on the BRICS Cross-Border Payments Initiative, dubbed BCBPI, welcoming “the use of local currencies in international trade” and “the strengthening of banking networks” to enable them. Yet everything for the moment is only “voluntary and non-binding.” Kazan is expected to give the process some edge.

“And was there outreach to you to be part of the search committee prior to January 1, 2021?” “Absolutely..”

• Fani Willis Laid Groundwork For Prosecuting Trump Before Taking Office (JTN)

House Judiciary Committee Jim Jordan on Monday released the transcript of closed-door testimony from Nathan Wade, the special prosecutor hired by Fulton County District Attorney Fani Willis to help manage her office’s Donald Trump election interference case before coming under scrutiny for his romantic-financial relationship with Willis. Wade testified that Willis was planning to prosecute Trump and began discussing a search committee to find a special prosecutor to investigate the former president prior to assuming office in January 2021. The former special prosecutor was also confronted with his own records showing that he met with White House officials, for eight hours on one occasion, though he told investigators he could not recall the details of the meetings.

Wade served on that search committee, which was instated on day one of Willis’ term in January 2021. After an unsuccessful search, Wade was ultimately invited to assume the role himself, which he claimed he reluctantly accepted. “And so the search committee, you said that began when DA Willis took office on January 1, 2021. Is that correct?” investigators asked. “Yes,” Wade replied. “And was there outreach to you to be part of the search committee prior to January 1, 2021?” “Absolutely,” he confirmed, saying the outreach began “Sometime after the election, but prior to her taking office.” The transcript of Wade’s deposition Tuesday was released by Jordan’s committee a week after the interview. The GOP-led committee subpoenaed Wade as part of an investigation into his relationship with Willis. Last year, Willis indicted Trump and 18 codefendants in Georgia over their alleged efforts to challenge the 2020 election results in the state.

Wade resigned from the case in March after a Georgia judge made his stepping aside a condition of allowing Willis to remain on the case after evidence of an improper financial and romantic relationship emerged between them. Wade also failed to recall key details about meetings with White House officials, despite recording them in his invoices to Willis’ office. According to the transcript, Wade billed Willis’ office for an eight hour meeting with White House lawyers. These meetings were reported by Just the News after court documents filed by a Trump codefendant showed Wade recorded an entry for a meeting with the White House Counsel’s office in Athens, Georgia in May 2022.

Though Wade testified that he did not remember the meeting, he told congressional investigators that “the invoice says travel to Athens. So that means to me that I traveled to Athens.” The invoices provided in the suit show at least one more meeting with Biden White House staff, on November 2022, that appears to have taken place in Washington, D.C., though there is no record of a visit by Wade in the White House visitor logs. Willis last week attempted unsuccessfully to block Wade from testifying to the committee on the grounds that it could “improperly divulge confidential information” about her investigation of the former president.

Failures?!

• Trump Assassination Probe Finds ‘Stunning’ Failures (RT)

The US Congress task force investigating the July 13 attempt on the life of Republican presidential candidate Donald Trump has confirmed that the Secret Service and local law enforcement did not coordinate properly. Trump was speaking at a rally in Butler, Pennsylvania when a bullet nicked his ear. One rally-goer was killed and two more seriously injured before the Secret Service neutralized the attacker on the roof of a nearby factory. “Put simply, the evidence obtained by the Task Force to date shows the tragic and shocking events of July 13 were preventable and should not have happened,” said the preliminary report published by the bipartisan body on Monday. The 53-page document contained eight main findings, starting with the lack of planning and coordination between the Secret Service and local law enforcement.

The factory roof from which Thomas Crooks opened fire was not included in the security perimeter, despite having “clear sight lines to the stage, and elevated position,” the report said. Local officers posted inside the building did not secure the complex or the roof, believing their job was just “overwatch” of the rally site. The Secret Service and local police had separate command posts and did not have a shared radio channel, the report said. This created gaps in communication which Crooks was able to slip through. A member of Congress with a law enforcement background who investigated the site in early August suggested that the FBI investigators may have destroyed evidence in the case by scrubbing the roof and allowing Crooks’ body to be cremated before the autopsy results were made available.

The Butler County Coroner’s office released the remains to Crooks’ family after the FBI said no additional evidence was necessary, the new report said. According to the autopsy, Crooks died of a single gunshot wound to the head, presumably inflicted by a Secret Service counter-sniper. He managed to fire eight shots prior to that, however, and may have stopped only after a local police officer shot at him. The coroner did not find evidence of alcohol or drugs in Crooks’ blood, but did find traces of antimony, selenium, and lead.

The new report also clarifies that Crooks did not use a ladder to get to the top of the building, but climbed using the outside air conditioning unit. The ladder seen in the photos after the incident was placed there by local police afterward to let investigators access the roof. Secret Service Director Kimberly Cheatle resigned ten days after the Butler shooting. The House of Representatives task force consists of both Republicans and Democrats and has been charged with investigating both the Butler incident and the thwarted ambush at Trump’s Florida golf course in September. Their final report is due December 13, well after the presidential election.

“..before Marvel Studios’ costume department comes knocking on the door of the EU clown tent to ask for their capes back..”

• The EU Doesn’t Need Moscow To Interfere In Its Democracy (Marsden)

The EU superheroes did it, guys. They stopped Russian President Vladimir Putin from being elected to Brussels. And now they’re telling us all about how they did it, before Marvel Studios’ costume department comes knocking on the door of the EU clown tent to ask for their capes back. The Russians and their “disinformation” didn’t have any impact on the European Elections earlier this year. That’s now the official word from the EU itself. Vera Jourova, the Vice President of the European Commission for Values and Transparency, has emerged from an Orwellian novel to announce that “based on currently available information, no major information interference operation capable of disrupting the elections was recorded.” So much for the public freak out that European parliamentarians were having back in April 2024, demanding even more censorship of “Kremlin-backed media outlets” and “disinformation campaigns” in what they qualified as “Kremlin-backed attempts to interfere with and undermine European democratic processes.”

We’re supposed to believe that it’s all because Jourova had embarked on a crackdown, er, “Democracy Tour” to commiserate not just with election officials and authorities, but also with “civil society” NGOs, industry, and media. Surely it has nothing to do with the fact that there wasn’t really much disinformation to begin with and that they’ve been blowing the issue way out of proportion. Jourova herself acknowledged that even the EU’s Digital Media Observatory was only able to find between 4% to 8% of what they qualify as “disinformation” among all articles analyzed between May 2023 and March 2024, and that the figure climbed to just 15% in May 2024, right before the EU’s June election. This means that around EU election time, a whopping 85% of information and analysis floating around in the public domain was EU-approved.

Jourova said that “disinformation narratives followed the topics we expected: there were allegations that the elections are rigged, but mostly topics that trigger a strong emotional impact – the war on Ukraine, the Middle East, false narratives on climate change, and migrants.” We used to call those things topics of debate. But that was before they decided that the agendas Brussels was trying to ram down everyone’s throats across the entire bloc wouldn’t be served by messy democratic dissent. Best to just dismiss, marginalize, or censor opposing information and narratives and be forced to deal with being violently mugged by reality later on issues like Ukraine’s not actually “winning,” regardless of how expensive life has become for EU citizens as a result of the bloc’s suicidal pro-Ukraine policies, and migration being an actual five-alarm problem for the EU as it faces the palpable rise of populism backlash for not doing enough earlier.

And the EU elections are certainly not rigged! The people elect representatives to EU parliament, then a ‘president’ is handpicked behind closed doors and plopped in front of them for a simple yes/no confirmation vote. That person, currently ‘Queen’ Ursula von der Leyen, who has never actually been elected to the EU parliament, then runs a ‘royal’ European Commission of bureaucratic desk jockeys that crafts and dictates policy for the entire bloc. Anyone calling this anything other than a model democratic institution must be a Russian agent.

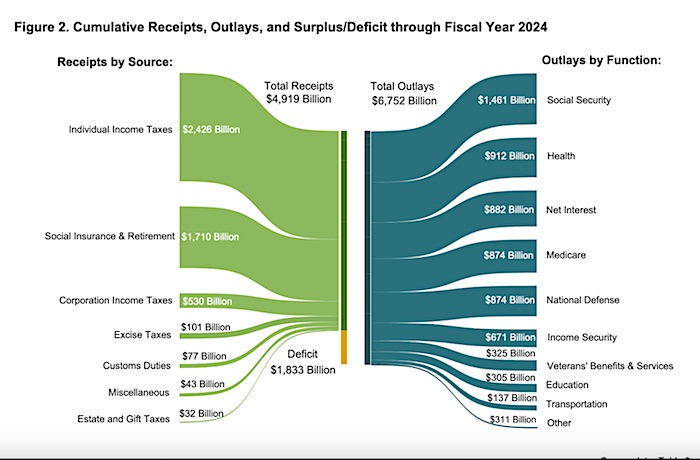

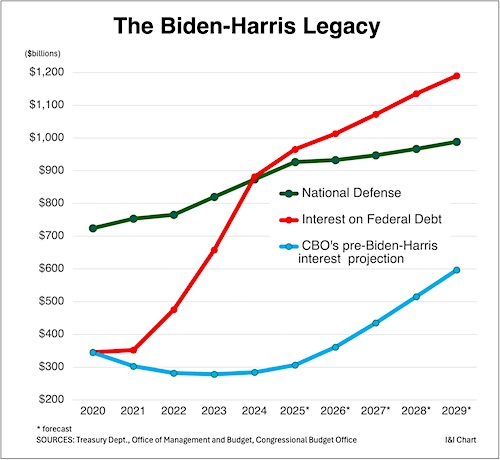

“..interest payments on the national debt. These payments hit $882 billion in FY 2024, the Treasury report says. That’s a 35% jump from last year..”

• US Interest Payments Top Defense Spending For First Time In History (I&I)

“SUNNY HOSTIN: Would you have done something differently than President Biden during the past four years? KAMALA HARRIS: There is not a thing that comes to mind in terms of — and I’ve been a part of most of the decisions that have had impact.”

On Friday, the Treasury Department released a report showing the kind of impact Harris is talking about. If nothing else does, it should cost her the election. The latest monthly Treasury report shows spending and revenues for the full fiscal year 2024, which ended in September. Among the terrible results: The federal deficit topped $1.8 trillion in 2024 — the third highest in history and eclipsed only by the two COVID-19 panic spending years. That’s not for lack of revenues, which were up by nearly half a trillion dollars this year. Spending under Biden-Harris this fiscal year climbed more than $617 billion – a 10% increase.

But the real shocker is the explosive growth in interest payments on the national debt. These payments hit $882 billion in FY 2024, the Treasury report says. That’s a 35% jump from last year. And it’s $8 billion more than we spent on National Defense. This marks the first time in our nation’s history that interest on the debt has exceeded defense spending. And the gap is on track to rapidly widen – with the government spending $200 billion more in interest than in protecting America from her enemies by 2029. Why the massive run-up in interest costs? Blame Harris’ tie-breaking votes (something for which she routinely brags). Because of them, Biden-Harris added trillions in new spending at a time when the economy had already fully recovered from the COVID-19 panic. That sparked a huge increase in inflation, which in turn drove up interest rates. More debt and higher interest rates meant a sharp increase in the cost of financing that debt.

How do we know Biden and Harris are to blame? Before they took office, the Congressional Budget Office (CBO) projected net interest payments for the next decade, based on the policies that Donald Trump had in place. The CBO said that, had Biden not spent us to the poorhouse, interest payments on the national debt this year would have been only $284 billion. In other words, Harris and her tie-breaking votes are responsible for a 210% increase in interest costs this year alone. What would Kamala Harris do about this terrible state of affairs if she were elected president? No one has bothered to ask her. But we do know that she wants to do exactly what she and Biden have already done: add trillions of dollars of inflationary spending, impose economically ruinous tax hikes, and pile on still more growth-killing regulations. Harris is right about one thing. It is time to turn the page — before it’s too late.

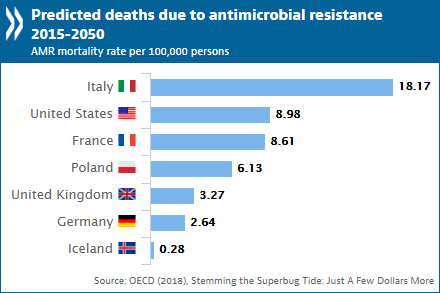

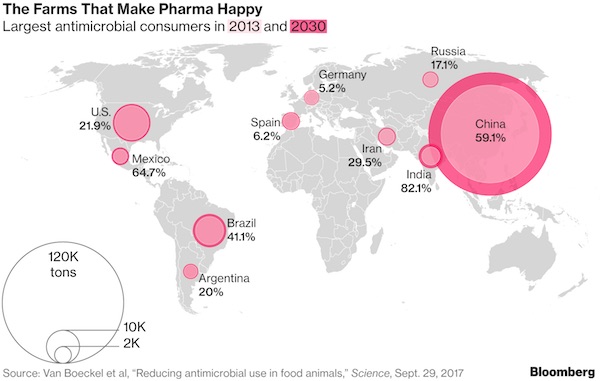

“..up to 39 million deaths around the world by 2050 due to antibiotic-resistant pathogens..”

• German Doctors Alarmed At Growing Failures Of Antibiotics – Bild (RT)

The world risks going back to the era before the discovery of penicillin, German doctors have cautioned, pointing to the rise in antibiotic-resistant pathogens. Penicillin, discovered in the late 1920s, extended the human lifespan by up to 30 years by countering most bacterial infections, according to the outlet Bild. All of that progress is now reportedly in peril. “We are currently losing the achievements of modern medicine and falling back into the time before the discovery of penicillin,” Mathias Pletz, head of the Paul Ehrlich Society for Infection Therapy, told Bild. “Antibiotics were the greatest achievement of medicine ever,” said Professor Yvonne Mast, a microbiologist and researcher at the Leibniz Institute in Braunschweig. “The fact that more and more resistance is now emerging and new antibiotics are lacking is a major threat.”

The German outlet quoted a study that estimated up to 39 million deaths around the world by 2050 due to antibiotic-resistant pathogens. Such infections already account for 35,000 deaths in the EU every year. According to Professor Frank Brunkhorst of the Jena University Hospital, one of the reasons is that doctors overprescribe antibiotics for outpatient procedures. For example, antibiotics are useless against almost all respiratory infections, which are caused by viruses. “Second, many resistant germs are coming to us due to international travel, which is booming again after [Covid],” Brunkhorst said, pointing to resistant strains “especially in countries like Greece, Portugal, Turkiye, but also in India and other Asian countries.” He warned Germans returning from vacations that the germs they bring back could be “life-threatening” to their grandparents.

The medical industry has been slow to develop new antibiotics because the research is too long and too expensive, while the profits are too low, according to Professor Mast. Only 12 new medications have been approved since 2017, she said. Only one in 5,000 substances reaches market maturity, the development period is anywhere from 8-15 years, and R&D costs can range up to $2 billion, according to Mast. She urged more funding for research and faster approvals, noting that China has already overtaken Germany in this field. “It is a huge task for politicians to bring antibiotic production back to Germany and Europe. Today, not a single drug is manufactured here anymore; everything comes from India or China. And we are dependent on it,” said Professor Brunkhorst.

KY/NC

https://twitter.com/i/status/1848109522230837705

NC

This Video is Not From Weeks Ago, This is NEW

“We're up in Chimney Rock, North Carolina — These people up here have not even been checked on — Guys on horseback found people today that it's the first people that they've seen on day 22, it's just baffling to me”

“it's… pic.twitter.com/dxxUu0T1wO

— Wall Street Apes (@WallStreetApes) October 20, 2024

Starship

Size of Space X Starship, humans for scale

pic.twitter.com/cWexHUMWSx— Science girl (@gunsnrosesgirl3) October 21, 2024

Summer’s day

https://twitter.com/i/status/1848233408469881293

Owls

— Photographer (@photo5065) October 20, 2024

Waterfall

Stunning jump into a waterfall basinpic.twitter.com/XSl8GpI3ZJ

— Massimo (@Rainmaker1973) October 21, 2024

Deep

https://twitter.com/i/status/1848386780409823724

Rube Goldberg

https://twitter.com/i/status/1848237891765354548

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.