Hieronymus Bosch The Conjurer 1502

What happens when markets don’t function. Manipulation is the name of the game.

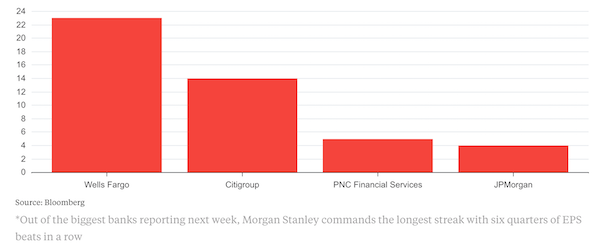

• Big Banks Continue Winning Streak, With Street at Least (BBG)

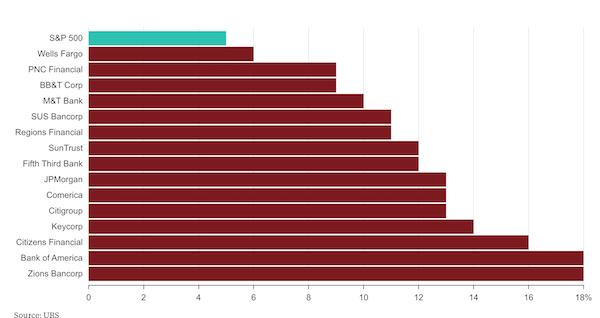

U.S. bank earnings have kicked off without any tumult. Investors should be grateful for that increasing sense of dependability, though they appear to be looking for more. JPMorgan Chase, Wells Fargo, Citigroup and PNC Financial Services each delivered second-quarter results on Friday that topped Wall Street’s expectations. On a measure of earnings per share, each bank has improved its respective streaks of beating or meeting analysts’ estimates:Reliability Factor The U.S. banks that reported earnings on Friday lengthened their streak of surpassing or matching expectations which, to be fair, are managed by bank executives:

The business of fixed-income trading, which has been a bright spot over the past year, has received outsize attention as it has fallen from grace after a long stretch of low volatility and tepid volumes, as expected. Instead, its quarterly gyrations should be accepted by shareholders just as they withstand changes in the weather, according to JPMorgan’s chairman and CEO Jamie Dimon. He has a point – the diversity of JPMorgan combined with the size of its overall corporate and investment bank, which houses the fixed-income trading business, gives the bank a level of flexibility. That defense might not stick if JPMorgan’s other businesses weren’t performing, but they are. The bank posted quarterly net income of $7 billion in the three months ended June 30.

That was its biggest haul ever, driven in part by a significant jump in net interest income, a direct result of the Federal Reserve’s rate increases. Its efforts to bulk up asset and wealth management, where revenues have roughly doubled since 2006, have borne fruit. Net income for the business climbed 20% compared with results in the same period last year to a record $624 million. And for now, despite broad concerns about auto and credit card loans, there’s no need to worry about widespread cracks. The bank’s so-called net charge-off rate, which measures delinquencies, remains minimal. [..] Bank stocks have rallied in part because the expected growth in their respective earnings per share, or EPS, in 2018 far exceeds that of the benchmark index:

Because you get to make record profits while others only get deeper into debt? Is that what Dimon is talking about?

• ‘It’s Almost An Embarrassment Being An American’ – Jamie Dimon (G.)

JP Morgan just had the most profitable 12 months ever for a US bank – but it wasn’t enough for Jamie Dimon, the bank’s boss. “It’s almost an embarrassment being an American traveling around the world and listening to the stupid shit Americans have to deal with in this country,” Dimon told journalists after the bank released its latest quarterly results on Friday. The world’s largest bank reported a profit of $7.03bn for the second quarter, 13% higher than last year. It has made $26.5bn over the past 12 months, a record profit for a US bank. But Dimon, who last year turned down Donald Trump’s offer to become treasury secretary, seemed more concerned about low rates of growth in the US and the health of the American body politic.

He blamed bad policy for “holding back and hurting the average American” and financial journalists for concentrating on the bank’s trading results when they should be focusing on policy. “Who cares about fixed-income trading in the last two weeks of June? I mean, seriously,” Dimon said after a reporter asked about the health of the bonds markets. “That is the weather,” he said of changes in the markets. “It goes up and down, this and that, and that’s 80% of what you guys focus on.” Dimon said financial journalists would be better off concentrating on the “bad policies” that are hurting average Americans. “It’s almost an embarrassment being an American traveling around the world and listening to the stupid shit Americans have to deal with,” he said. “At one point, we would have to get our act together, do what we’re supposed to do to the average American.”

[..] “We need infrastructure reform,” he said. “We need corporate tax reform. We need better skills and education. If we don’t focus on these things, we are hurting average Americans every day. “The USA has to start to focus on policy which is good for all Americans, and that is regulation, tax, education, we have to get those things done. You guys [journalists] should be writing a lot more about that stuff. That is holding it back and hurting the average American citizen if we don’t do it.

Or is Dimon embarrassed over this?

• US House Backs Massive Increase In Defense Spending (R.)

The U.S. House of Representatives passed its version of a massive annual defense bill on Friday, leaving out controversial amendments on transgender troops and climate policy but backing President Donald Trump’s desire for a bigger, stronger military. The vote was 344-81 to pass the National Defense Authorization Act (NDAA), which sets military policy and authorizes up to $696 billion in spending for the Department of Defense. Underscoring bipartisan support for higher defense spending in Congress, 117 Democrats joined 227 Republicans in backing the measure. Only eight Republicans and 73 Democrats voted no. But the measure faces more hurdles before it can become law, notably because it would increase military spending beyond last year’s $619 billion bill, defying “sequestration” caps on government spending set in the 2011 Budget Control Act.

Trump wants to pay for a military spending increase by slashing nondefense spending. His fellow Republicans control majorities in both the House and Senate, but they will need support from Senate Democrats, who want to increase military spending, for Trump’s plans to go into effect. The House NDAA also increases spending on missile defense by 25%, adds thousands more active-duty troops to the Army, provides five new ships for the Navy and provides a 2.4% salary increase for U.S. troops, their largest pay raise in eight years. And it creates a new Space Corps military service, pushed by lawmakers worried about China and Russia’s activities in space, but opposed by Defense Secretary Jim Mattis.

Oh well, money’s cheap after all.

• US Deficits To Jump $248 Billion Over Next Two Years Due To Tax Shortfall (R.)

The budget deficit for President Donald Trump’s first two years in office will be nearly $250 billion higher than initially estimated due to a shortfall in tax collections and a mistake in projecting military healthcare costs, budget chief Mick Mulvaney reported on Friday. In a mid-year update to Congress, Mulvaney, director of the Office of Management and Budget, revised the estimates supplied in late May when the Trump administration submitted its first spending plan. Since then, Mulvaney said, the deficit projected for the current fiscal year has increased by $99 billion, or 16.4%, to $702 billion. For 2018, the deficit will be $149 billion more than first expected, increasing by 33% to $589 billion.

The figures come as the administration is facing widespread doubts among economists and analysts that it can erase government deficits largely by boosting economic growth and changing laws like the Affordable Care Act. ACA reform is facing a difficult path in Congress, and the Congressional Budget Office on Thursday said the administration’s growth and deficit reduction plans were optimistic. The letter from Mulvaney said the bulk of the problem this year and next stems from lower-than-expected tax collections. Individual and corporate income taxes and other collections for this year are expected to be $116 billion less than the administration anticipated in May. Tax receipts in 2018 are expected to be $140 billion less than initially estimated.

A reference to JFK. Our next discovery will be that debt is a harsh mistress.

• We Do These Things Because They’re Easy (CHS)

We are now totally, completely dependent on expanding debt for the maintenance of our society and economy. Every sector of the economy–households, businesses and government–all borrow vast sums just to maintain the status quo for another year. Compare buying a new car with easy, low-interest credit and saving up to buy the car with cash. How easy is it to borrow $23,000 for a new $24,000 car? You go to the dealership, announce all you have to put down is a trade-in vehicle worth $1,000. The salesperson puts a mirror under your nose to make sure you’re alive, makes sure you haven’t just declared bankruptcy to stiff previous lenders, and if you pass those two tests, you qualify for a 1% rate auto loan. You sign some papers and drive off in your new car. Easy-peasy!

Scrimping and saving to pay for the new car with cash is hard. You have to save $1,000 each and every month for two years to save up the $24,000, and the only way to do that is make some extra income by working longer hours, and sacrificing numerous pleasures–being a shopaholic, going out to eat frequently, $5 coffee drinks, jetting somewhere for a long weekend, etc. The sacrifice and discipline required are hard. What’s the pay-off in avoiding debt? Not much–after all, the new auto loan payment is modest. If we take a 5-year or 7-year loan, it’s even less. By borrowing $23,000, we get to keep all our fun treats and spending pleasures, and we get the new car, too. At the corporate level, it’s the same story: borrow a billion dollars and use it to buy back shares.

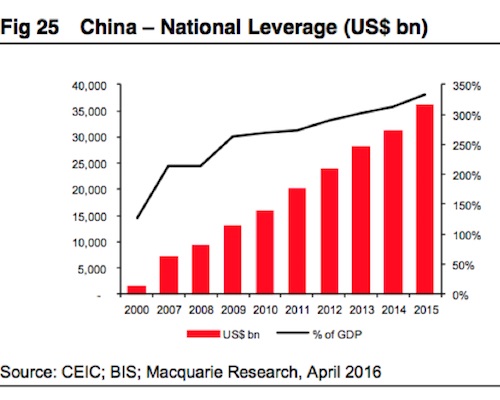

Increasing the value of the corporation’s shares by increasing profit margins and actual value is hard; boosting the share price with borrowed money is easy. It’s also the same story with politicians and the government: cutting anything is politically painful, so let’s just float a bond, i.e. borrow money to pay for what was once paid out of tax revenues: maintaining parks, repaving streets, funding pensions, etc. This dependence on expanding debt for maintaining the status quo is a global trend. Debt is exploding in China in every sector, and the same is true in other nations, developed and developing alike. Borrowing more money from the future is easy, painless and requires no trade-offs, sacrifices or accountability–until the debt-addicted economy collapses under its own weight of debt service and insolvency.

“..all those elaborate plans depend on no more war. And there’s the rub.”

• The New Silk Road Will Go Through Syria (Escobar)

Amid the proverbial doom and gloom pervading all things Syria, the slings and arrows of outrageous fortune sometimes yield, well, good fortune. Take what happened this past Sunday in Beijing. The China-Arab Exchange Association and the Syrian Embassy organized a Syria Day Expo crammed with hundreds of Chinese specialists in infrastructure investment. It was a sort of mini-gathering of the Asia Infrastructure Investment Bank (AIIB), billed as “The First Project Matchmaking Fair for Syria Reconstruction”. And there will be serious follow-ups: a Syria Reconstruction Expo; the 59th Damascus International Fair next month, where around 30 Arab and foreign nations will be represented; and the China-Arab States Expo in Yinchuan, Ningxia Hui province, in September.

Qin Yong, deputy chairman of the China-Arab Exchange Association, announced that Beijing plans to invest $2 billion in an industrial park in Syria for 150 Chinese companies. Nothing would make more sense. Before the tragic Syrian proxy war, Syrian merchants were already incredibly active in the small-goods Silk Road between Yiwu and the Levant. The Chinese don’t forget that Syria controlled overland access to both Europe and Africa in ancient Silk Road times when, after the desert crossing via Palmyra, goods reached the Mediterranean on their way to Rome. After the demise of Palmyra, a secondary road followed the Euphrates upstream and then through Aleppo and Antioch. Beijing always plans years ahead. And the government in Damascus is implicated at the highest levels.

So, it’s not an accident that Syrian Ambassador to China Imad Moustapha had to come up with the clincher: China, Russia and Iran will have priority over anyone else for all infrastructure investment and reconstruction projects when the war is over. The New Silk Roads, or One Belt, One Road Initiative (Obor), will inevitably feature a Syrian hub – complete with the requisite legal support for Chinese companies involved in investment, construction and banking via a special commission created by the Syrian embassy, the China-Arab Exchange Association and the Beijing-based Shijing law firm. Few remember that before the war China had already invested tens of billions of US dollars in Syria’s oil and gas industry. Naturally the priority for Damascus, once the war is over, will be massive reconstruction of widely destroyed infrastructure.

China could be part of that via the AIIB. Then comes investment in agriculture, industry and connectivity – transportation corridors in the Levant and connecting Syria to Iraq and Iran (other two Obor hubs). What matters most of all is that Beijing has already taken the crucial step of being directly involved in the final settlement of the Syrian war – geopolitically and geo-economically. Beijing has had a special representative for Syria since last year – and has already been providing humanitarian aid. Needless to add, all those elaborate plans depend on no more war. And there’s the rub.

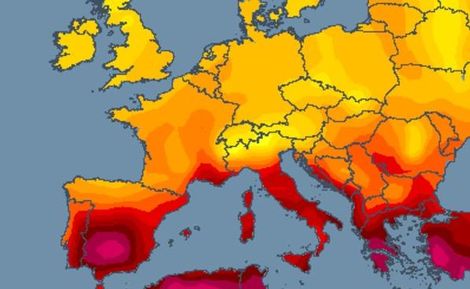

Southern Europe: getting poorer and hotter.

• One Of Worst Droughts In Decades Devastates South Europe Crops (R.)

Italian durum wheat and dairy farmer Attilio Tocchi saw warning signs during the winter of the dramatic drought to come at his holding a mile away from the Tuscan coast. “When it still hadn’t rained at the beginning of spring we realized it was already irreparable,” he said, adding that he had installed fans to try and cool his cows that were suffering in the heat. Drought in southern Europe threatens to reduce cereal production in Italy and parts of Spain to its lowest level in at least 20 years, and hit other regional crops including olives and almonds. Castile and Leon, the largest cereal growing region in Spain, has been particularly badly affected, with crop losses estimated at around 60 to 70%.

“This year was not bad, it was catastrophic. I can’t remember a year like this since 1992 when I was a little child,” said Joaquin Antonio Pino, a cereal farmer in Sinlabajos, Avila. Pino said many of his fields had not even been harvested, because crop revenues would not cover the wages of laborers who gathered them. While the EU is collectively a major wheat exporter, Spain and Italy both rely on imports from countries including France, Britain and Ukraine. Spanish soft wheat imports are expected to rise by more than 40% to 5.6 million tonnes in the 2017-2018 marketing year, according to Agroinfomarket. The drought has helped support EU wheat futures, which have risen around 6% since the beginning of June, although the prospect of a larger harvest in France this year should ensure adequate overall supplies in the trading bloc.

Germans love cash.

• People Not Amused by EU Efforts to “De-Cash” their Lives (DQ)

In January 2017 the European Commission announced it was exploring the option of imposing upper limits on cash payments, with a view to implementing cross-regional measures as soon as 2018. To give the proposal a veneer of respectability and accountability the Commission launched a public consultation on the issue. Now, the answers are in, but they are not what the Commission was expecting. A staggering 95% of the respondents said they were opposed to a cash ceiling at EU level. Even more emphatic was the answer to the following question: “How would the introduction of restrictions on payments in cash at EU level benefit you, or your business or your organisation (multiple replies are possible)?” In the curious absence of an explicit “not at all” option, 99.18% chose to respond with “no answer.”

In other words, less than 1% of the more than 30,000 people consulted could think of a single benefit of the EU unleashing cross-regional cash limits. Granted, 37% of respondents were from Germany and 19% from Austria (56% in total), two countries that have a die-hard love for physical lucre. Even among millennials in Germany, two-thirds say they prefer paying in cash to electronic means, a much higher level than in almost any other advanced economy with the exception of Japan. Another 35% of the survey respondents were from France, a country that is not quite so enamored with cash and whose government has already imposed a maximum cash limit of €1,000. By its very nature the survey almost certainly attracted a disproportionate number of arch-defenders of physical cash.

As such, the responses it elicited are unlikely to be a perfect representation of how all Europeans would feel about the EU’s plans to introduce maximum cash limits. Nonetheless, the sheer strength of opposition should (but probably won’t) give the apparatchiks in Brussels pause for thought. The biggest cited concern for respondents was the threat the cash restrictions would pose to privacy and personal anonymity. A total of 87% of respondents viewed paying with cash as an essential personal freedom. The European Commission would beg to differ. In the small print accompanying the draft legislation it launched in January, it pointed out that privacy and anonymity do not constitute “fundamental” human rights.

Be that as it may, many Europeans still clearly have a soft spot for physical money. If the EU authorities push too hard, too fast in their war on cash, they could provoke a popular backlash. In Germany, trust in Europe’s financial institutions is already at a historic low, with only one in three Germans saying they have confidence in the ECB. The longer QE lasts, the more the number shrinks.

When they were elected in January 2015, Syriza’s approval rating was some 75%. But when you turn your back on your promises, and then unleash more austerity….

• Just 13% of Greeks Trust Their Government (K.)

Just 13% of Greeks trusted the government in 2016, according to the Organization for Economic Cooperation and Development’s (OECD) biennial Government at a Glance report, placing Greece among the four member states with the sharpest decline in confidence in their administrations. According to the report, which was published by the Paris-based organization on Thursday and shows 2016 data, Greece joins Chile, Finland and Slovenia in recording a significant loss of trust between citizens and the government, slipping to 13% in 2016 from 19% in 2014. Confidence has also declined over the past decade across the OECD’s member states, though at a rate of 3%, coming to 42% in 2016 from 45% in 2007.

In terms of specific sectors, Greeks have lost faith across the board, with the Greek health system having the trust of just 31% of citizens from 35% in the 2015 study for 2014, public education of 44% from 45% and the judicial system of 42% from 44%. A new area added in this year’s survey is the police, where confidence was high last year at 69%. Across the OECD, average confidence in the health system came to 70%, education to 67% and justice to 55%.

You’d almost wish they would fight back.

• World’s Large Carnivores Being Pushed Off The Map (BBC)

Six of the world’s large carnivores have lost more than 90% of their historic range, according to a study. The Ethiopian wolf, red wolf, tiger, lion, African wild dog and cheetah have all been squeezed out as land is lost to human settlements and farming. Reintroduction of carnivores into areas where they once roamed is vital in conservation, say scientists. This relies on human willingness to share the landscape with the likes of the wolf. The research, published in Royal Society Open Science, was carried out by Christopher Wolf and William Ripple of Oregon State University. They mapped the current range of 25 large carnivores using International Union for Conservation of Nature (IUCN) Red List data. This was compared with historic maps from 500 years ago.

The work shows that large carnivore range contractions are a global issue, said Christopher Wolf. “Of the 25 large carnivores that we studied, 60% (15 species) have lost more than half of their historic ranges,” he explained. “This means that scientifically sound reintroductions of large carnivores into areas where they have been lost is vital both to conserve the large carnivores and to promote their important ecological effects. “This is very dependent on increasing human tolerance of large carnivores – a key predictor of reintroduction success.” The researchers say re-wilding programmes will be most successful in regions with low human population density, little livestock, and limited agriculture. Additionally, regions with large networks of protected areas and favourable human attitudes toward carnivores are better suited for such schemes.

“Increasing human tolerance of large carnivores may be the best way to save these species from extinction,” said co-researcher William Ripple. “Also, more large protected areas are urgently needed for large carnivore conservation.” When policy is favourable, carnivores may naturally return to parts of their historic ranges. This has begun to happen in parts of Europe with brown bears, lynx, and grey wolves. The Eurasian lynx and grey wolf are among the carnivores that have the smallest range contractions. The dingo and several types of hyena are also doing relatively well, compared with the lion and tiger.