Pablo Picasso Mother and child at the seaside 1922

It’s certainly true that Nancy Pelosi gets more popular because she opposes Trump. In the same way that the NYT and CNN got milliions more viewers and readers by echo-chambering their Trump ‘resistance’.

But still, if she refuses to hold the State of the Union, Trump simply takes her plane away. Being more popular in the echo chamber isn’t the same as being popular. So many Americans, in media, politics, and in the street, have lived in their echo chambers for so long, they think it’s the entire country. That is not true.

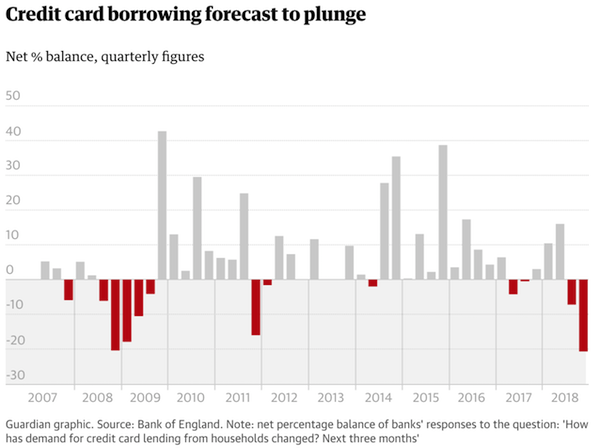

Yes, Britain should wean off personal debt as much as any nation. But do it too fast and your engines fail and bring you to a full standstill.

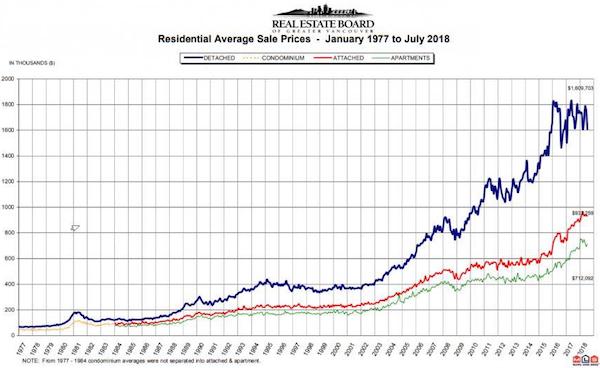

• Demand For Credit Cards And Mortgages In UK Falling Fast (G.)

Borrowing on credit cards is expected to plunge to the lowest levels since 2007 in the three months before Brexit, according to the Bank of England, in another indication of stresses facing the UK economy. According to the latest quarterly health check on credit conditions from Threadneedle Street, high street banks forecast borrowing on plastic will decline in the first quarter by the most since records began 12 years ago. It comes amid growing concern over consumer spending on the high street after the worst Christmas for retailers since the financial crisis, setting the economy up for a weak first quarter. The Bank said its measure of demand for credit card lending over the three months to the end of March dropped to -20.7 from -7.2.

Its gauge for mortgage lending also dropped to -17.5 in the final quarter of 2018, from -0.2 in the third quarter, its lowest level since the end of 2010. The looming threat of a no-deal Brexit in less than 80 days dragged down the UK property market further in December, according to a report from Britain’s top surveyors, with prices falling at the fastest rate in six years and the outlook for sales the weakest in two decades. Economists said that the drop in mortgage lending likely reflected banks reining in their lending in response to the risk of a no-deal Brexit, with Threadneedle Street warning that prices could drop by almost a third. Despite the warnings, prices have continued to rise sharply in some parts of the UK, including Manchester and Birmingham, even as the value of homes in London stalls or declines.

May’s legacy: failed Brexit, hostile environment and murder of a reasonably well functioning health system.

• May’s 10-Year Plan ‘Still Not Enough’ To Save NHS – (Ind.)

The NHS is financially “unsustainable” and the government’s much-trumpeted 10-year plan is inadequate to rescue cancer, mental health and social care services, the National Audit Office (NAO) has warned. Years of underinvestment have resulted in longer waiting times, critical staff shortages and “substantial deficits” that have been covered up by raiding funds for long-term reform, an NAO review found. These factors “do not add up to a picture that we can describe as sustainable”, it said. NHS England’s recently published 10-year plan sets out how it aims to spend the pledged £20.5bn increase in its budget by 2023 to break this cycle.

But the NAO warns its success is dependent on the government producing – and funding – a long-delayed plan to reform social care and an estimated £6bn repair bill to fix run-down buildings. While NHS England expects to bring in thousands of staff from overseas to fill gaps, the report says ambitions to transform services will require significant additional growth. “The NAO has laid bare just how difficult it will be to achieve the ambitions of the NHS long-term plan given where the NHS is starting from,” Richard Murray, chief executive of the King’s Fund think tank, said. With health services finances “bedevilled by short-term fixes, fragile workarounds, and unrealistic expectations”, he said the NAO was right to make clear the government’s flagship investment is not an NHS panacea.

[..] key decisions about the future of waiting-time standards such as the four-hour treatment target in A&E departments have been deferred to a separate report. Auditors warned more than £700m will be required just to bring the NHS surgical waiting list down from a 10-year high of more than 4.3 million, to March 2018 levels. A workforce plan has also been delayed and the report says: “There is a risk that the NHS will be unable to use the extra funding optimally because of staff shortages.” This is because scarce funds are currently being squandered on costly agency staff to plug more than 100,000 vacant posts, and there could be too few people in key roles – like cancer or community services – to deliver its goals.

May rules out a customs union and a second referendum, but not a “no deal”. Is that impossible, or merely her ‘principles’?

“..the prime minister was determined to stick to her “principles” on Brexit, including rejecting a customs union and a second referendum.”

• May Tells Corbyn It Is ‘Impossible’ To Rule Out No Deal (G.)

Theresa May has told Jeremy Corbyn his demand that she rule out a no-deal scenario as a prerequisite for Brexit talks is “an impossible condition” and called on him to join cross-party discussions immediately. In a letter to Corbyn on Thursday afternoon, written after the Labour leader dismissed her request for talks as a “stunt”, May said that she would be “happy to discuss” the Labour leader’s ideas. She urged him to “talk and see if we can begin to find a way forward for our country on Brexit”. Referring to Corbyn’s instruction to Labour MPs not to meet with her, May asked: “Is it right to ask your MPs not to seek a solution with the government?”

The proposed talks have been stymied by Corbyn’s insistence that a no-deal must be ruled out as a precondition and May’s insistence that doing so would not be workable. In her letter she wrote: “It is not within the government’s power to rule out no deal.” May has been meeting other party leaders in the aftermath of the resounding defeat for her Brexit plan in the House of Commons earlier this week. A number of Labour MPs have defied their leader’s instruction not to engage in discussions designed to find a plan that might command a majority. Earlier, Downing Street insisted the prime minister was determined to stick to her “principles” on Brexit, including rejecting a customs union and a second referendum.

With the clock running down to Brexit day on 29 March, May kicked off Thursday’s talks with the Green party MP, Caroline Lucas. May’s official spokesman insisted these conversations would be approached “in a constructive spirit, and wanting to hear what the various groups have to say”. But when asked whether May was willing to flex any of her negotiating red lines, he said they remained in place.

Absolutely savage pic.twitter.com/jaFZdLMalL

— ARTIST TAXI DRIVER (@chunkymark) January 17, 2019

Yanis inserts a bit of -much needed- game theory into the debate. A deadline defeats the process, because there will be nothing happening before the deadline.

• Run Down the Brexit Clock (Varoufakis)

Members of Parliament deserve congratulations for keeping their cool in the face of a made-up deadline. That deadline is the reason why Brexit is proving so hard and potentially so damaging. To resolve Brexit, that artificial deadline must be removed altogether, not merely re-set. [..] Once we are at, or close to March 29, heightened urgency will dissolve tactical procrastination. May’s deal will have bitten the dust, and Remainers will be closer to accepting that time is not on the side of a Brexit-annulling second referendum, perhaps turning their attention to the legitimate aim of a future referendum to re-join the EU.

At that point, government and opposition will recognize that only two coherent options remain for the immediate future. The first is Norway Plus, which would mean Britain would remain for an indeterminate period in the EU single market (like Norway), and also in a customs union with the EU. The second is an immediate full exit, with Britain trading under World Trade Organization rules while Northern Ireland remains within a customs union with the EU to avoid a hard border with the Republic of Ireland. Narrowing it down to two options will enable Parliament to choose. Once MPs acknowledge that freedom of movement between the UK and the EU is a red herring, the most likely outcome is Norway Plus for an indeterminate, deadline-free period.

Then and only then will Parliament and the people have the opportunity to debate the large-scale issues confronting Britain, not least the future of the UK-EU relationship. Norway Plus would, of course, leave everyone somewhat dissatisfied. But, unlike May’s deal or a hasty second referendum, at least it would minimize the discontent that any large segment of Britain’s society might experience in the medium term. And, because minimizing the discontent, along with a deadline-free horizon, are prerequisites for the people’s debate that Britain deserves, the overwhelming defeat of May’s deal may well be remembered as a vindication of democracy.

It wouldn’t get more toxic that that.

• Nigel Farage Urges Brexiteers To Prepare For Second Referendum (PA)

Nigel Farage has urged Leave campaigners to prepare for a second referendum as Britain’s Brexit deadlock continues. The former Ukip leader spoke at a packed Leave Means Leave rally in London, alongside former Conservative leader Iain Duncan-Smith, MP Esther McVey and Hotelier Rocco Forte. Mr Farage said he believed “it is now quite possible that we will see an extension of Article 50”. He added: “When I’ve talked in the past about being worried that they may force us into a second referendum. I don’t want it anymore than you do but I am saying to you we have to face reality in the face. Don’t think the other side aren’t organised, don’t think the other side aren’t prepared, don’t think they haven’t raised the money, don’t think they haven’t got the teams in place, they have.”

The audience at the Leave Means Leave rally were fired up and heckling throughout the nights speeches. Mr Duncan-Smith said Britain’s “greatness” lies in the post-Brexit future. He added: “I love this country dearly, I love it with all my heart. I love people whether they’re Remainers or Leavers, I don’t care. But I know one thing, this country’s greatness lies ahead of it and we have an opportunity and a duty to deliver it. I pledge to you tonight, I will not sleep, I will not rest, I will not wake to find a Britain that is otherwise than independent and free once again.” He branded the European Union a “political project that we have never fully been told the truth about” and described anti-Brexit arguments as “a load of rubbish”.

As I’ve been saying for a while. “The phenomenon has been dubbed debt-trap diplomacy.”

• More Countries To Cut Down Their Belt And Road Investments (CNBC)

Some countries are scaling down or scrapping entire projects that are part of China’s Belt and Road Initiative amid mounting financial concerns over the continent-spanning venture. In recent months, developing nations such as Pakistan, Malaysia, Myanmar, Bangladesh and Sierra Leone have either canceled or backed away from previously negotiated BRI commitments, citing worries over high project costs and their impact on national debt and the economy. That revised stance not only confirms global fears over the terms of BRI financing, it could also indicate that developing countries are now more willing to prioritize sovereign interests over their need for foreign investment.

The BRI — Beijing’s signature foreign policy program — is the superpower’s attempt to stretch its economic power across the globe through the construction of maritime and overland transportation links across Asia, the Middle East, Africa and Europe. But critics see it as a means to benefit China’s military, increase opportunities for Chinese companies and help Beijing gain political leverage. Under the trillion-dollar endeavor, Chinese state-owned entities flush with cash offer participating countries cheap loans and credit to build large-scale projects such as ports and railways.

[..] Many of these countries want to avoid the same fate as Sri Lanka. Shock waves rippled throughout the developing world when Colombo handed over a strategic port to Beijing in 2017, after it couldn’t pay off its debt to Chinese companies. It was seen as an example of how countries that owe money to Beijing could be forced to sign over national territory or make steep economic concessions if they can’t meet liabilities. The phenomenon has been dubbed debt-trap diplomacy

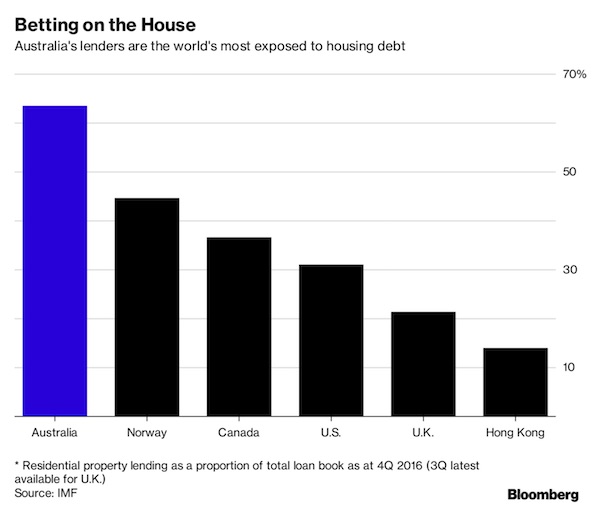

The biggest housing bubble of them all.

• China’s Slowing Economy Takes Hong Kong’s Housing Market Down With It (BI)

One of the world’s most expensive housing markets is facing a major slowdown. Analysts at HSBC dimmed their outlook for Hong Kong’s real-estate market on Wednesday, according to a research note. Previously forecasting activity would plateau, they now estimate prices will fall from 10% to 15% over the next six months. “We expect the first half of 2019 to be a challenging period for the Hong Kong housing market,” the analysts said. “Prices have already corrected 8% from the recent peak in August 2018 due to macro uncertainties and several events occurring in the property market that concerned investors.”

Hong Kong was ranked the most-expensive housing market in the world for eight consecutive years, benefitting from capital controls in mainland China that incentivize real-estate investments closer to home. But activity has slowed sharply in recent months, with property values falling by the most since the global financial crisis in 2008 in November. With China’s economy expected to continue to lose steam in coming months, the housing market looks poised to fall further. [..] Also helping to bring prices down from August highs, a vacancy tax aimed at discouraging investors from holding empty Hong Kong homes was introduced last year. Still, some are confident residential real estate activity will start to recover despite a slowing economy, with HSBC predicting annual price drops to shrink to between 5% and 10% by the end of the year.

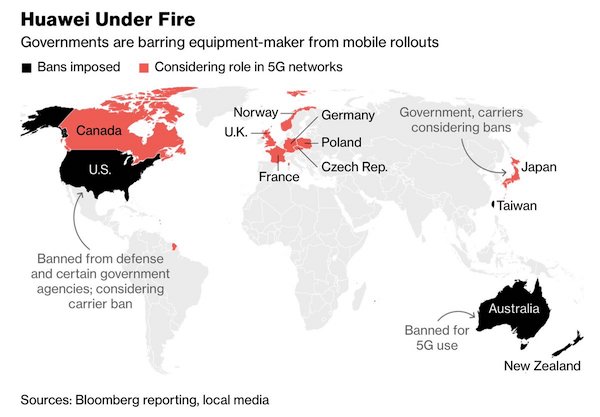

It’s about our intelligence controlling us. We don’t want Chinese intelligence to do that, and the only alternative we have is the CIA, MI6 etc.

• Germany ‘Looks To Ban Huawei’ From 5G Build (BBC)

Germany is considering ways to block Huawei from its next generation mobile phone network, according to reports. Berlin is exploring stricter security requirements which may prevent Huawei products being used in its 5G network. Many countries have pushed against the involvement of the Chinese technology firm in their 5G networks over security concerns. The networks represent the next big wave of mobile infrastructure. The Chinese company, one of the world’s biggest producers of telecoms equipment, has faced resistance from foreign governments over the risk that its technology could be used for espionage. Huawei has denied claims it poses a spying risk.

Germany’s interior ministry had previously said it opposes banning any suppliers from its 5G network. But it may consider stricter security requirements and other ways to exclude Huawei, according to reports. Such a move would bring it in line with other Western countries. The Australian government has banned Huawei from providing 5G technology to its wireless networks, while New Zealand blocked a proposal to use its telecoms equipment over national security concerns. The US and UK have raised concerns with Huawei, and the firm has also been scrutinised in Japan and Korea.

Some people have all the funding they need.

• Huawei Funding Suspended By Oxford University (PA)

Oxford University is suspending research grants and funding donations from Huawei, amid growing security concerns about the Chinese firm’s telecommunication technology. Existing research contracts already received or committed with Huawei will go ahead, but the university will not pursue new funding opportunities with the company. There are two ongoing projects in which Huawei has committed £692,000, the university said.

“Oxford University decided on January 8 this year that it will not pursue new funding opportunities with Huawei Technologies Co Ltd or its related group companies at present,” an Oxford University spokesman said in a statement. “Huawei has been notified of the decision which the university will keep under review. The decision applies both to the funding of research contracts and of philanthropic donations. “The decision has been taken in the light of public concerns raised in recent months surrounding UK partnerships with Huawei. We hope these matters can be resolved shortly and note Huawei’s own willingness to reassure governments about its role and activities.

The Democrats have their own Trump. But they don’t understand how that works, and personal desire for power is far too great amongst the octogenarians (or soon to be) anyway.

• Alexandria Ocasio-Cortez Teaches Fellow Democrats How To Use Twitter (Ind.)

There are some things, such as courage and a sense of humour, that you cannot teach. But becoming a titan of social media? That may just be possible to learn. Such is the hope, at least, of Democrats on Capitol Hill, who have undergone a class in how to tweet more effectively, from Alexandria Ocasio-Cortez, the veritable Twitter superpower. “With @AOC, @RepDebDingell, @jahimes, @davidcicilline, @RepCartwright & @Twitter representatives at training session on Twitter for Democratic Members of Congress,” tweeted California congressman Ted Lieu, after the lesson. “The below pic is called a selfie.”

Nobody in the Democratic party – Michelle and Barack Obama included – has as much Twitter power as the 29-year-old congresswoman of New York’s 14th district. Axios reported recently that from December 11 2018, to January 11 2019, Ms Ocasio-Cortez, had 11.8m Twitter interactions, second only to Donald Trump, – who had 39.8m – among politicians or the news media. Senator Kamala Harris was third with 4.6m, Barack Obama was fourth with 4.4m, and CNN came fifth with 3.1m.

Robert Hockett is professor of Law and Public Policy at Cornell University. “How will we pay for it?” is not that interesting. “What’s in it?” is a much better question.

I don’t think I’m going to like the answer. Because I don’t think the people proposing the various Green New Deals can see sufficiently across the wide range of fields involved: finance, pollution, energy, politics, psychology etc.

• How We’ll Pay For Green New Deal Isn’t ‘A Thing’ – Nor Is Inflation (F.)

Representative Alexandria Ocasio-Cortez’s announcement of an ambitious new Green New Deal Initiative in Congress has brought predictable – and predictably silly – callouts from conservative pundits and scared politicians. ‘How will we pay for it?,’ they ask with pretend-incredulity, and ‘what about debt?’ ‘Won’t we have to raise taxes, and will that not crowd-out the job creators?’ Representative Ocasio-Cortez already has given the best answer possible to such queries, most of which seem to be raised in bad faith. Why is it, she retorts, that these questions arise only in connection with useful ideas, not wasteful ideas? Where were the ‘pay-fors’ for Bush’s $5 trillion wars and tax cuts, or for last year’s $2 trillion tax giveaway to billionaires?

Why wasn’t financing those massive throwaways as scary as financing the rescue of our planet and middle class now seems to be to these naysayers? The short answer to ‘how we will pay for’ the Green New Deal is easy. We’ll pay for it just as we pay for all else: Congress will authorize necessary spending, and Treasury will spend. This is how we do it – always has been, always will be. The money that’s spent, for its part, is never ‘raised’ first. To the contrary, federal spending is what brings that money into existence. If years of bad or no economic education make that ring counterintuitive to you, you’re not alone: politicians and pundits who ought to know better are with you. But the problem is readily remedied: just take a look at a dollar (or five dollar, or ten dollar, or … dollar) bill.

The face you see is George Washington’s – a public official’s – not yours or some other private sector person’s. The signatures you’ll find, for their part, are those of the Treasurer and the Treasury Secretary, not yours or some other private sector person’s. And the inscription you’ll read across the top is ‘Federal Reserve Note,’ not ‘Private Sector Sally’s Note.’ ‘Note’ here, note carefully, means ‘promissory note.’ Money betokens a promise. Hence money’s relation to credit. We’ll come back to this later. The money that Treasury spends is, in any event, jointly Fed- and Treasury-issued, not privately issued. That is to say it’s the citizenry’s issuance, not some single citizen’s issuance. It’s like a promise we make to each other. Hence the term ‘full faith and credit’ you’ll hear about when asking what ‘backs’ our currency and our Treasury securities.

A narrative repeated so often most people will think it must be at least partly true. But then there’s this very curious line: “Whether the political distemper in the West was sown by a Russian intelligence operation masterminded by Putin may not matter because he is making a belated effort at winning the peace after the end of the Cold War.”

• Another Good Day For Putin As Turmoil Grips US and UK (CNN)

The news just keeps on getting better for Vladimir Putin. On either side of the Atlantic, the United States and Britain, the two great English-speaking democracies that orchestrated Moscow’s defeat in the Cold War, are undergoing simultaneous political breakdowns. And the Russian leader may have had a hand in triggering the turmoil.

The allies are experiencing the reverberations of populist revolts that erupted in 2016 – in the Brexit vote and the election of Trump – and are now slamming into legislatures and breeding division and stasis. The result is that Britain and the United States are all but ungovernable on the most important questions that confront both nations. That’s music to Putin’s ears. The Russian leader has made disrupting liberal democracies a core principle of his near two-decade rule, as he seeks to avenge the fall of the Soviet empire, which he experienced as a heartbroken KGB agent in East Germany. Russia has been accused of meddling in both the Brexit vote and the US election in 2016 – the critical events that fomented the current crisis of the West.

Over the last five years, Putin has defied Western scorn about Russia’s frayed economic power and made the best of a bad hand, working to re-establish influence in the former Soviet orbit. He has seized Crimea from Ukraine and restored Moscow’s former political beachhead in the Middle East. In the last two years, Putin has had a witting, or unwitting, ally in Trump, whose attacks on NATO and US allies and decision to pull US troops out of Syria played into Russia’s goals. Whether the political distemper in the West was sown by a Russian intelligence operation masterminded by Putin may not matter because he is making a belated effort at winning the peace after the end of the Cold War.

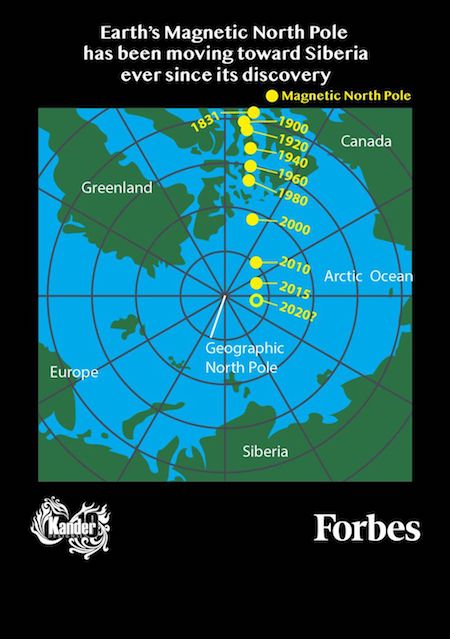

Original headline was “The Magnetic North Pole Has Moved. Here’s What You Need To Know”, but obviously this alternative one, phrased by someone on Twitter, is so much better.

Other than that, I’m curious to know how this affects animals that use magnetic poles, like migrating birds and insects. Unfortunately, the article doesn’t address the issue.

• Putin Stole Santa’s Home (F.)

Earth’s magnetic pole is moving in the direction of Siberia and away from Canada. This is something that scientists have been tracking for a long time. It’s fairly easy to look up the location of the magnetic pole dating back to the early 1900s. The recent changes of the drifting pole are raising some concerns but the direction is not the problem. In fact, the direction of the drifting pole has been roughly the same for as long as scientists have been tracking it. The speed is the issue. Every five years scientists recalculate the location of the magnetic pole. This is important information for global navigation, which includes GPS satellites and other technology. These changes can make a big difference in our everyday lives.

The movement of the pole is caused by flows of molten liquid iron in the Earth’s core. This liquid and how it moves creates the Earth’s magnetic field. Variations in the liquid flow cause the magnetic field to change over time and cause the location of magnetic north to move. The global model was off because of a geomagnetic pulse the occurred beneath South America in 2016. This pulse just came at a bad time. The 2015 World Magnetic Model was brand new and not scheduled to be renewed until 2020. It seems that in the future we may not be able to wait as long between updates. The poles movement has sped up in recent memory from 9 miles a year in the 1990s to about 34 miles a year at present day.