Dorothea Lange Depression refugee family from Tulsa, Oklahoma 1936

Why it has to stop. Or rather, why it will be stopped.

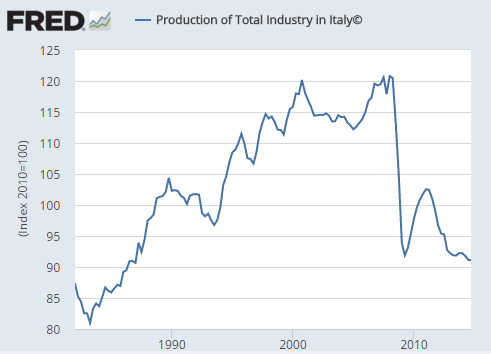

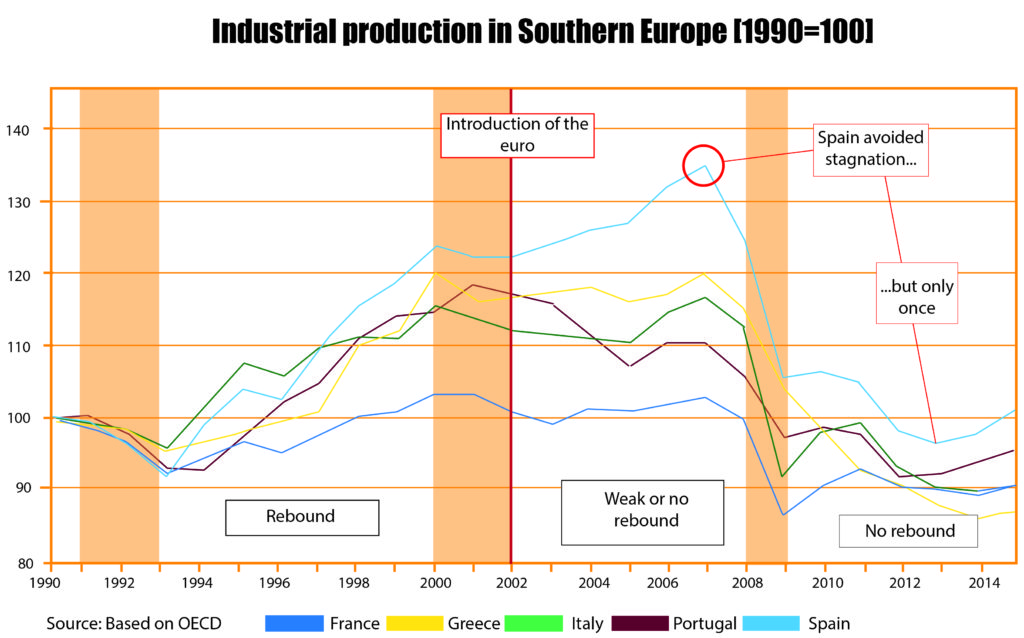

• The Euro Has Been A Disaster For Southern European Production (Gefira)

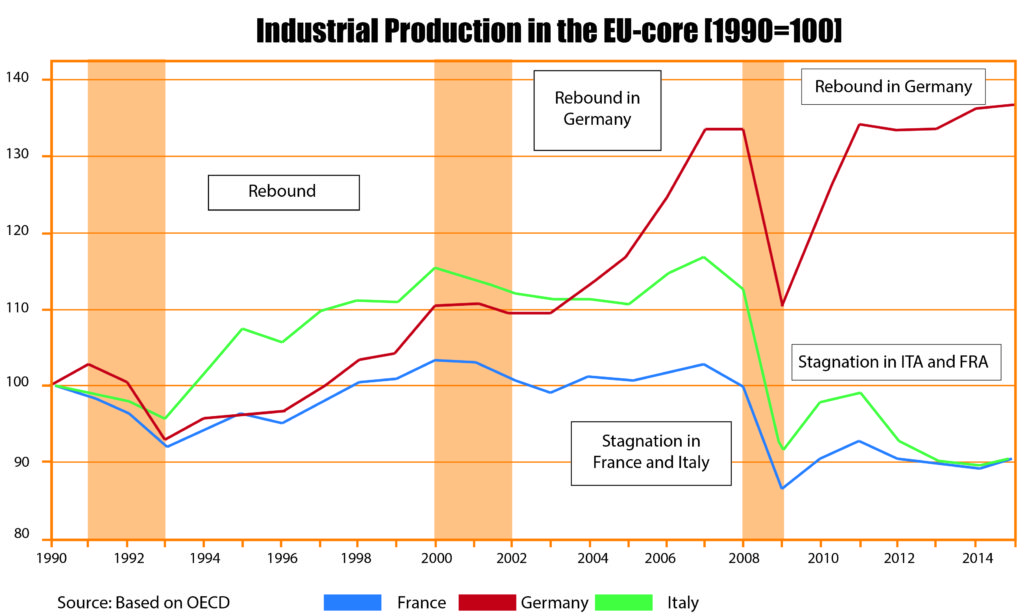

Some say that the common currency prevents less productive economies from cheating by weakening their national currencies and forces them to become more efficient and competitive. Industrial production data shows that it is not the case. Italy, France, Greece and Portugal have not only stopped producing more; they are producing now less than in 1990! The decay started immediately after the introduction of the euro in 2002! The OECD industrial production data analysis leads to the following conclusions: 1. since 1990 industrial production (manufacturing and construction included) has been growing in volume at large, even in the most developed countries; 2. the disproportion between industrial output in Germany and two other biggest euroarea economies, Italy and France, occurred already just after the 2001-2002 crisis; 3. Southern Europe’s economies have lost their ability to rebound in industrial production alongside the adoption of the euro.

1. Industrial output can increase In most of the most developed countries in the world industrial production has grown in volume since 1990, although a great deal of manufacturing capacities have been moved from the West to the emerging markets. Moreover, in countries like the USA, Israel, Switzerland, Austria and Germany the output has surpassed the 2008 pre-crisis levels. However, if we take a look at the euroarea or the Group of Seven (G7), then numbers are still lower than in 2008 but definitely higher than in 1990.

2. The euroarea has a problem A closer look at the European industrial production numbers gives a clear signal: something bad has happened after 2000. Before the introduction of euro, production trends ran more or less in the same direction. Meanwhile after the 2001-2002 crisis, French and Italian output did not rebound, while production in Germany expanded enormously and was able to reach the 2008 level quickly after the last crisis. Industry in France and Italy not only has not rebounded but also has started to curb.

3. Southern Europe will not rebound with the euro

Countries with a sovereign currency can easily build up their economies because of one simple mechanism: depreciation. A relatively strong currency (strong in comparison to the economic condition) would not have to be a problem for Italy or Greece if there still were some capacities for more debt. Then internal consumption could prop up industrial production. But Spain, Greece, Italy and Portugal have had neither a weak sovereign currency nor the possibility of incurring more debt.

Industry is very important for the economy, as it creates jobs and innovations. The euroarea in the current form is preventing Southern Europe’s industry from developing because of a different type of economy there. “Roman” economies are not worse than than Germany’s. They just need other tools, so restricting all these various economies in the German fashion will destroy the euro as well as the European unity.

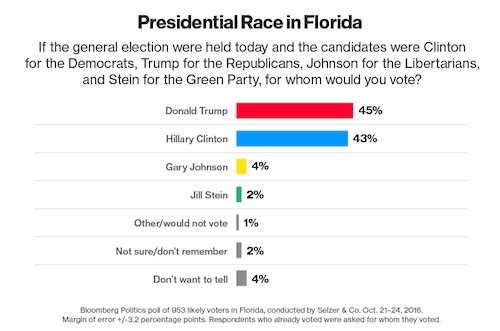

Steve Keen on which employment numbers are actually relevant. Curious to see how many people think Hillary’s got it in the bag. As an example, here’s a Bloomberg poll that just came out:

• Washington: Don’t Think It’s Over When Trump Loses (Steve Keen)

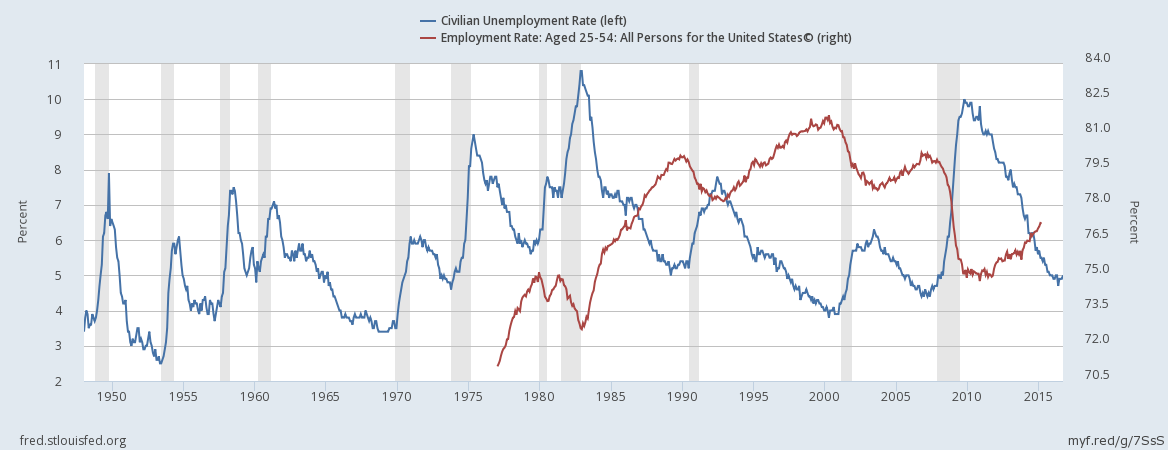

Trump’s fans certainly have their “dark fantasies”, but Washington and Krugman have a “bright fantasy” if they believe that unemployment is genuinely low. My favourite and unimpeachable proof that this is false is an easily-obtained data series: the percentage of Americans aged 25-54 who have a job. While the “Unemployment Rate” is back within half a per cent of its pre-crisis low, the percentage of Americans aged 25-54 who have a job today is 2% lower than it was before the crisis. Perhaps an even more important fact that explains the anger behind Trump (and Sanders too, before he was eliminated by the Democratic Party’s peculiar primary process) is that the employment rate actually peaked in 2000, and even after this recovery, it is still 4% lower than in 2000 (78% today versus 82% in 2000).

What that means in terms of people with jobs is even more telling. The number of people aged 25-54 with a job in the USA peaked at 104.7 million in December 2007. It bottomed at 100.3 million in October 2013, and as of February 2015 (the most recent data) it was 101.2 million. So when Washington is talking about achieving “full employment” again, there are still more than 3 million less people employed today than in 2007. Demographic change has caused this segment of the population to decline since December 2007—from 126 million then to 125 million in February 2015—but that still means 2 million more people are unemployed today than in 2007. So if you look at the unemployment rate, everything is wonderful. That seems to be what Washington insiders—all with well-paying jobs—are doing. But if you look at the employment rate, the economy is still in the doldrums. Which series is telling the truth about the US economy?

The employment to population ratio is telling the truth, because it’s derived by asking employers how many people they have on their payroll. The unemployment rate, on the other hand, lies about the real level of unemployment, because it is derived by asking individuals whether they fulfil a number of criteria, including whether they have looked for a job in the last 4 weeks. The employment ratio accurately tells you the number of people receiving a salary; the unemployment ratio does not accurately tell you who is not receiving one. It’s no comfort to someone not receiving a salary to be told that they are not also unemployed, according to the official definition. Their justified reaction is to tell the “official definition” what to do with itself.

A few billion here and a few billion there in debt.

• 213 North American Oil Industry Companies Have Now Declared Bankruptcy (FF)

Fewer and fewer oil exploration and production companies are declaring bankruptcy. But more oilfield service companies are. So far this month, only one North American E&P firm filed for Chapter 11 protection, according to data released on Tuesday by the Dallas law firm Haynes & Boone. That’s down from two in September, three in August and four in July. But it’s been an especially tough few months for service companies. As crude prices began crashing in 2014, drillers started idling rigs. That led to fewer jobs for the companies that make their money helping producers pump oil and gas. Moreover, when producers did hire service companies, they often forced them to heavily discount their rates.

Eight service companies filed this month. Seven filed last month, and eight again the month before. Almost 50 have filed in the last six months, half of the 108 over two years. In total, 213 North American oil and gas companies have now filed for bankruptcy since the start of 2015, listing more than $85 billion in debt. The most recent exploration firm: the private oil and gas company Mountain Divide, based in Montana, filed on Oct. 14, and listed $83 million in debt. On the oilfield services side, Houston-based Key Energy Services filed on Monday, with more than $1 billion in debt. And Basic Energy Services, headquartered in Fort Worth, said Monday it had reached an agreement with debt holders to file by Tuesday.

While at the same time letting Chinese foreign purchases escalate.

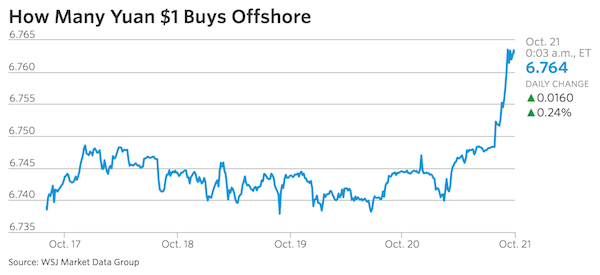

• China Tightens Capital Controls Amid Yuan’s Continuing Slide (Nikkei)

China has toughened restrictions on capital flows to prevent a negative feedback loop between a weakening yuan and capital flight. The State Administration of Foreign Exchange has introduced new capital measures in areas such as Shanghai and Guangzhou since the beginning of autumn, asking foreign and regional banks to cap the amount of foreign currency they will sell to customers during 2016. These limits, though ostensibly up to banks’ discretion, are set by negotiation with authorities and so are essentially directed by the government, a financial sector source said. A gag order has been imposed surrounding the measures, the source said. Some banks apparently have set steep exchange rates to pre-emptively curb foreign currency sales, a practice that could pose issues for foreign companies in China trying to repatriate earnings, for example.

China’s trade has flagged in recent months, with exports dropping 10% in September from the year-earlier level in dollar terms. The prospect of an interest rate hike in the U.S., meanwhile, has market players expecting further declines in the yuan’s value. Stashing assets abroad, rather than keeping them in China, is increasingly seen as the safer option. This view has led to further selling of the yuan, giving rise to a downward spiral that capital controls aim to break. Both the foreign exchange regulator and the People’s Bank of China have given banks several directives this year to curb outflows and the currency’s slide. Institutions are asked to report on corporate clients’ plans for buying foreign currency. Large fund transfers that involve foreign currency purchases must be explained by the institutions ahead of time. Individuals traveling overseas are asked to make reservations when exchanging money.

The yuan continues to depreciate despite these efforts. The central bank Tuesday set its daily guidance rate for the Chinese currency at 6.77 yuan to the dollar – just a little shy of the 6.82- to 6.83-to-the-dollar range at which the yuan was fixed for nearly two years following the September 2008 financial crisis. At the time, the goal was to prevent the currency from strengthening to stave off an economic slump. The concern now is that the yuan will become weaker and capital will flow out.

The best thing to could happen in Britain.

• London House Prices Forecast to Plunge as Brexit Chokes Market (BBG)

London property prices are set to fall next year as uncertainty about Britain’s exit from the EU damps the U.K. housing market, according to the Centre for Economics and Business Research. London, and especially the priciest areas of the capital’s housing market, will be most affected, with prices dropping 5.6% in 2017, according to the consultancy’s predictions. Across the U.K., while property value growth will accelerate to 6.9% in 2016, it’s set to slow to 2.6% next year. “Nervousness and uncertainty are starting to show,” said Kay Daniel Neufeld, an economist at Cebr. “We expect to see house-price growth across the U.K. slowing considerably in the fourth quarter of 2016, a trend that is set to continue in 2017.”

While the housing market was already facing headwinds from tax changes before June’s EU referendum, investors are becoming increasingly nervous about the possibility of a so-called hard Brexit. That could see the U.K. giving up membership of Europe’s single market for goods and services to secure greater control of immigration. Accelerating inflation, increasing unemployment and slowing business investment are all set to weigh on house prices, while curbs on migration and a retreat from the single market could slow demand from international buyers, the Cebr said.

Wait till we find out what Google does.

• AT&T Is Spying On Americans For Profit (DB)

In 2013, Hemisphere was revealed by The New York Times and described only within a Powerpoint presentation made by the Drug Enforcement Administration. The Times described it as a “partnership” between AT&T and the U.S. government; the Justice Department said it was an essential, and prudently deployed, counter-narcotics tool. However, AT&T’s own documentation—reported here by The Daily Beast for the first time—shows Hemisphere was used far beyond the war on drugs to include everything from investigations of homicide to Medicaid fraud. Hemisphere isn’t a “partnership” but rather a product AT&T developed, marketed, and sold at a cost of millions of dollars per year to taxpayers.

No warrant is required to make use of the company’s massive trove of data, according to AT&T documents, only a promise from law enforcement to not disclose Hemisphere if an investigation using it becomes public. These new revelations come as the company seeks to acquire Time Warner in the face of vocal opposition saying the deal would be bad for consumers. Donald Trump told supporters over the weekend he would kill the acquisition if he’s elected president; Hillary Clinton has urged regulators to scrutinize the deal. While telecommunications companies are legally obligated to hand over records, AT&T appears to have gone much further to make the enterprise profitable, according to ACLU technology policy analyst Christopher Soghoian.

“Companies have to give this data to law enforcement upon request, if they have it. AT&T doesn’t have to data-mine its database to help police come up with new numbers to investigate,” Soghoian said. AT&T has a unique power to extract information from its metadata because it retains so much of it. The company owns more than three-quarters of U.S. landline switches, and the second largest share of the nation’s wireless infrastructure and cellphone towers, behind Verizon. AT&T retains its cell tower data going back to July 2008, longer than other providers. Verizon holds records for a year and Sprint for 18 months, according to a 2011 retention schedule obtained by The Daily Beast.

Just so you know.

• The US Is Currently Bombing Seven Countries (PF)

For this fact check, we wondered if the U.S. is bombing seven countries. That at least has been so: In September 2014, PunditFact rated True a bombed-countries claim by Ryan Lizza of The New Yorker. Lizza referred to President George W. Bush and his successor, Barack Obama, in a tweet that said: “Countries bombed: Obama 7, Bush 4.” At the time, the U.S. on Obama’s watch had bombed Afghanistan, Iraq, Pakistan, Somalia, Yemen, Libya and Syria. When we asked Stein for her backup information, spokeswoman Meleiza Figueroa pointed out various web posts including a September 2014 CNN news story stating that Obama had ordered air strikes in seven countries through the bulk of his eight years in the office.

[..] The Bureau of Investigative Journalism, a nonprofit news service based at City University London, maintains a running list of U.S. military actions in a number of countries. The bureau annotates each incident with links to press reports. When we looked, the bureau’s accounts by country indicated the latest U.S drone strike in Pakistan occurred in May 2016; the latest strike in Somalia was in September 2016; and the latest U.S. strikes in Yemen and Afghanistan were in October 2016. Separately, we noticed, the Department of Defense said in an Oct. 11, 2016, web post that countries including the U.S. battling the Islamic State of Iraq and the Levant, or ISIL, have conducted 15,634 air strikes to date – 10,129 in Iraq, 5,505 in Syria – with the U.S. conducting 6,868 in Iraq and 5,227 in Syria. In a Sept. 30, 2016, post, the U.S. Air Force said attacks from the air have affected ISIL’s “ability to fight and conduct operations in Iraq, Syria and Afghanistan.”

Too, in August 2016, the New York Times reported the U.S. had “stepped up a new bombing campaign against the Islamic State in Libya, conducting its first armed drone flights from Jordan to strike militant targets” in Libya’s coastal city of Sirte. That news story quoted Obama saying during a news conference that the airstrikes were critical to helping Libya’s fragile United Nations-backed government to drive Islamic State militants out of Sirte, which the group has controlled since June 2015. Obama promised the air campaign would continue as long as necessary to make sure that the extremist group “does not get a stronghold in Libya,” the newspaper said.

Trump -rightly- mirrors something I said a few days ago in Ungovernability “..her harsh criticism of Putin raised questions about “how she is going to go back and negotiate with this man who she has made to be so evil,” if she wins the presidency.”

• Trump Says Clinton Policy On Syria Would Lead To World War Three (R.)

U.S. Republican presidential nominee Donald Trump said on Tuesday that Democrat Hillary Clinton’s plan for Syria would “lead to World War Three,” because of the potential for conflict with military forces from nuclear-armed Russia. In an interview focused largely on foreign policy, Trump said defeating Islamic State is a higher priority than persuading Syrian President Bashar al-Assad to step down, playing down a long-held goal of U.S. policy. Trump questioned how Clinton would negotiate with Russian President Vladimir Putin after demonizing him; blamed President Barack Obama for a downturn in U.S. relations with the Philippines under its new president, Rodrigo Duterte; bemoaned a lack of Republican unity behind his candidacy, and said he would easily win the election if the party leaders would support him.

“If we had party unity, we couldn’t lose this election to Hillary Clinton,” he said. On Syria’s civil war, Trump said Clinton could drag the United States into a world war with a more aggressive posture toward resolving the conflict. Clinton has called for the establishment of a no-fly zone and “safe zones” on the ground to protect non-combatants. Some analysts fear that protecting those zones could bring the United States into direct conflict with Russian fighter jets. “What we should do is focus on ISIS. We should not be focusing on Syria,” said Trump as he dined on fried eggs and sausage at his Trump National Doral golf resort. “You’re going to end up in World War Three over Syria if we listen to Hillary Clinton.”

[..] On Russia, Trump again knocked Clinton’s handling of U.S.-Russian relations while secretary of state and said her harsh criticism of Putin raised questions about “how she is going to go back and negotiate with this man who she has made to be so evil,” if she wins the presidency.

“Less than half the public (43%) say they have a great deal of confidence that their vote will be counted accurately..”

• Most Americans Do Not Feel Represented By Democrats Or Republicans (G.)

As they go to the polls in a historic presidential election, more than six in 10 Americans say neither major political party represents their views any longer, a survey has found. Dissatisfaction with both Democrats and Republicans has risen sharply since 1990, when less than half held that neither reflected their opinions, according to research by the Public Religion Research Institute (PRRI). The seventh annual 2016 American Values Survey was carried out throughout September among a random sample of 2,010 adults in all 50 states. Both party establishments have been rattled by the outsider challenges of Donald Trump, who was successful in winning his party’s nomination, and Bernie Sanders, who was not. In a year that seems ripe for third-party candidates, Libertarian Gary Johnson and Jill Stein of the Green party are seeking to capitalise but have fallen back in the polls in recent weeks.

61% of survey respondents say neither political party reflects their opinions today, while 38% disagree. 77% of independents and a majority (54%) of Republicans took this position, while less than half (46%) of Democrats agree. There was virtually no variation across class or race. Both Democratic presidential nominee Hillary Clinton and Republican standard bearer Trump continue to suffer historically low favourability ratings, with less than half of the public viewing each candidate positively (41% v 33%). Clinton is viewed less favourably than the Democratic party (49%), but Trump’s low rating is more consistent with the Republican party’s own favourability (36%).

The discontent with parties and candidates extends to the electoral process itself, which Trump claims is rigged against him. Less than half the public (43%) say they have a great deal of confidence that their vote will be counted accurately, while 38% have some confidence and 17% have hardly any confidence. [..] The PRRI found that pessimism about the direction of the US is significantly higher today (74%) than it was at this time during the 2012 presidential race, when 57% of the public said the country was on the wrong track.

Slightly confused: I thought he was pro-Hillary?!

• The Biggest F*ck Ever Recorded In Human History (Michael Moore)

I know a lot of people in Michigan that are planning to vote for Trump and they don’t necessarily agree with him. They’re not racist or redneck, they’re actually pretty decent people and so after talking to a number of them I wanted to write this. Donald Trump came to the Detroit Economic Club and stood there in front of Ford Motor executives and said “if you close these factories as you’re planning to do in Detroit and build them in Mexico, I’m going to put a 35% tariff on those cars when you send them back and nobody’s going to buy them.” It was an amazing thing to see. No politician, Republican or Democrat, had ever said anything like that to these executives, and it was music to the ears of people in Michigan and Ohio and Pennsylvania and Wisconsin – the “Brexit” states.

You live here in Ohio, you know what I’m talking about. Whether Trump means it or not, is kind of irrelevant because he’s saying the things to people who are hurting, and that’s why every beaten-down, nameless, forgotten working stiff who used to be part of what was called the middle class loves Trump. He is the human Molotov Cocktail that they’ve been waiting for; the human hand grande that they can legally throw into the system that stole their lives from them. And on November 8, although they lost their jobs, although they’ve been foreclose on by the bank, next came the divorce and now the wife and kids are gone, the car’s been repoed, they haven’t had a real vacation in years, they’re stuck with the shitty Obamacare bronze plan where you can’t even get a fucking percocet, they’ve essentially lost everything they had except one thing – the one thing that doesn’t cost them a cent and is guaranteed to them by the American constitution: the right to vote.

They might be penniless, they might be homeless, they might be fucked over and fucked up it doesn’t matter, because it’s equalized on that day – a millionaire has the same number of votes as the person without a job: one. And there’s more of the former middle class than there are in the millionaire class. So on November 8 the dispossessed will walk into the voting booth, be handed a ballot, close the curtain, and take that lever or felt pen or touchscreen and put a big fucking X in the box by the name of the man who has threatened to upend and overturn the very system that has ruined their lives: Donald J Trump.

They see that the elite who ruined their lives hate Trump. Corporate America hates Trump. Wall Street hates Trump. The career politicians hate Trump. The media hates Trump, after they loved him and created him, and now hate. Thank you media: the enemy of my enemy is who I’m voting for on November 8. Yes, on November 8, you Joe Blow, Steve Blow, Bob Blow, Billy Blow, all the Blows get to go and blow up the whole goddamn system because it’s your right. Trump’s election is going to be the biggest fuck ever recorded in human history and it will feel good.

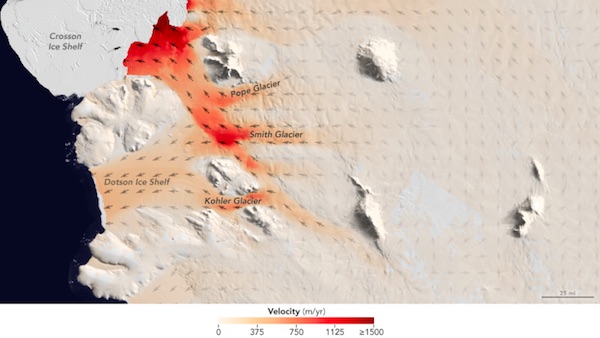

“.. like ice cubes rising as a soft drink is poured into a glass.”

• Antarctic Glaciers Are Melting at a ‘Staggering’ Rate (Gizm.)

Scientists have long viewed the Amundsen sea embayment as the Achilles heel of West Antarctica, with papers in the 1970s and ‘80s describing it as “uniquely vulnerable,” “unstable,” and the “weak underbelly” of the continent. The fear, then and now, was that warm ocean waters lapping against the foot of the glaciers could cause the ice to pop up off of its rocky floor, like ice cubes rising as a soft drink is poured into a glass. When ice detaches from its so-called “grounding line,” it kickstarts a chain reaction that can trigger a lot of melting. “When water gets between ice and land, it moves quickly, bringing lots of heat in, and melting the ice above it more rapidly,” said Thomas Wagner, the director of NASA’s polar science program. “The Amundsen sea embayment is a place where we know this is happening.”

Indeed, satellite and radar data show that two of West Antarctica’s largest glaciers, Pine Island and Thwaites, have seen their grounding line retreat many miles since 2000, causing fresh water to pour off the ice and into the ocean. This process is so effective that glaciologists recently declared the total collapse of the Amundsen sea embayment—whose glaciers contain enough water to raise global sea levels by four feet—to be “unstoppable.” Here’s the rub: We still have no idea how quickly all of that ice will go, meaning we have no idea whether to prepare for a lot more sea level rise in ten years, in a generation, or at the end of the century. A new study, led by glaciologist Ala Khazendar of NASA’s Jet Propulsion Laboratory, points to ice disappearing sooner rather than later.

For years, NASA has been conducting an airborne campaign called Operation Ice Bridge, flying across sections of our planet’s north and south polar ice sheets and using ground-penetrating radar to measure changes beneath the surface. When Khazendar examined Ice Bridge’s datasets for the Amundsen sea embayment, he realized that NASA flew almost exactly the same path in 2009 that it did in 2002. “This presented an excellent opportunity to look at how ice thickness changed,” he said.

NOTE: we know our Comments section doesn’t function properly. We’re looking into it.