Esther Bubley Waiting for Greyhound bus trip from Memphis to Louisville, KY 1943

Been scribbling several some post-election notes over the past few days, it seemed a good idea to not publish things too soon after the upset, even if I at least had the advantage that it wasn’t that much of a surprise or upset. But I’ve read far too many people too eager to write about how they haven’t moved an inch, and too many others who have -mostly reluctantly- moved but don’t know how or where to. It’s okay to think about such matters first, guys and dolls. Make that: it’s better. There’s too much nonsense out there as is. Why bother adding to the pile? Here’s a few thoughts in no particular order:

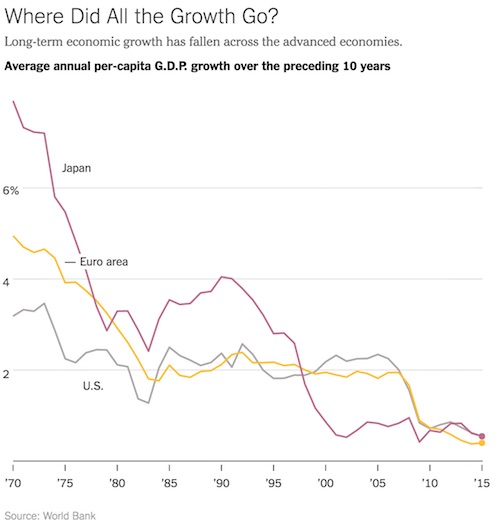

The transition we find ourselves in, into an era as profoundly different as it will be from the one that preceded it, can only possibly be chaotic. Smooth is not an option. Because it takes much time for people to recognize let alone accept that there is such a transition to begin with, and not everyone acknowledges or accepts it at the same time. Many never will at all, they will be left behind in their own realities tied down by the chains of what once was.

This transition is the one away from economic growth and globalization -centralization in general- and towards smaller, less centered and grandiose, politics and markets. It is not an idealistic transition towards self-sufficiency, it’s simply and inevitably what’s left once unfettered growth hits the skids. It doesn’t have to be anywhere near as bad as people would have you believe, or at least not necessarily so. What could make it real bad, though, is the widespread resistance and denial which seem certain to meet it.

Our entire worldviews and ‘philosophies’ are based on ever more and ever bigger and then some, and our entire economies are built upon it. That has already made us ignore the decline of our real markets for many years now. We focus on data about stock markets and the like, and ignore the demise of our respective heartlands and flyover countries, even as we experience Brexit and Trump and similar movements set to come to many more countries.

Donald Trump looks very much like the ideal fit for this transition – but nor because he understands the issue itself, or its implications. What matters is he promises to bring back jobs to America, and that’s what the country needs. Not so they can then export their products, but to consume them at home, and sell them in the domestic market.

That is the future of the world post-growth, and post-globalization. Every country and every society needs to focus on self-reliance, not as some idealistic luxury choice, but as a necessity. And that is not as bad or terrible as people would have you believe, and it’s not the end of the world. What would be terrible is if all we do is try and restart growth and globalization, because that would be a hideous waste of time and resources.

You’ll be flooded in the years to come, even more than today if you can imagine, with terms like protectionism and isolationism and even populism, but ignore all that. There’s nothing economically -let alone morally- wrong with people producing what they and their families and close neighbors themselves want and need without hauling it halfway around the world for a meagre profit, handing over control of their societies to strangers in the process.

There’s nothing wrong or negative with an American buying products made in America instead of in China. At least not for the man in the street. It’s not a threat to our ‘open societies’, as many claim. That openness does not depend on having things shipped to your stores over 1000s of miles, that you could have made yourselves at a potentially huge benefit to your local economy. An ‘open society’ is a state of mind, be it collective or personal. It’s not something that’s for sale.

Earlier this week I read what looks to be an apt observation: ‘Every white person in New York who didn’t vote for Trump is now out in the streets protesting against him’. But the people who protest now are miles off target and months too late: they should have stood up for Bernie when it became clear that the Hillary camp and the DNC conspired to oust him. Indeed, Bernie himself should have stood up back then, not for himself but for his supporters; they would have stood up with him.

Whether they all like it or not, being asleep and/or silent when big things happen that count, does carry a price. If you drop the ball, you can’t just pick it back up again and pretend it didn’t fall. Shouting ‘not my president’ in the wake of an election is a sign of weakness, no matter how well-intentioned. The protests should have taken place before the election, not after.

Moreover, to a large extent people are up in protest against the image the Hillary campaign and the media have painted of Trump, not the man himself. A difference they cannot see. Would these same people have been protesting if Hillary had won? No, they wouldn’t. But why?

Many voices expressed the wish that Americans would vote for Hillary, a story about a woman and a glass ceiling, instead of for the male and allegedly sexist and misogynist Donald Trump. Simply because she’s a woman, and it’s time for a female president.

These voices have been consistently and for a long time been blind to the fact that Hillary’s campaign and Foundation, in legal, shady and downright illegal ways, have long been financed to a substantial degree by uber-rich men in charge of Middle East oil extracting nations who have far more misogynist views and attitudes towards women than Trump will ever have.

These men carry things like misogyny, racism, xenophobia and homophobia high and proudly in their banners. Also, they’re well on their way towards obliterating not just an entire country in Yemen, but indeed an entire people, all with the enthusiastic support of Obama, Hillary and their friends and donors in the arms industry. And lest we forget, they sponsor ISIS too. Is that the future Americans want?

The bright side is the chances of a war with Russia have gone down substantially. While the odds have gone up dramatically of much fewer US servicemen and -women being sent abroad to engage in endless and countless battles and wars that never seemed to have much to do with the US, going back all the way to Korea and Vietnam.

How can either of these things can be perceived as negative? The continuation and expansion of -often proxy- hostilities versus Moscow would have been cast in stone had Hillary been elected, it was a milestone of her entire campaign. And a major part of this would have been fought at some desert location in the Middle East.

Where America has needlessly squandered the lives of many of its young and finest, to and in a mad scramble over control of oil resources which has resulted in nothing but a shapeless chaos that has equally needlessly killed millions of people, sent millions of others fleeing their homes and razed entire ancient civilizations, accomplishments that will follow America around the world for many years to come. Is that the future Americans want? Double down?

There’s -undeniably- still a risk that Donald Trump will succumb to the mighty hand of the military industrial complex. But at the same time, he may well be the country’s -and the world’s- best if not only chance at making that hand that much less mighty. There may be many things wrong with Trump -there are- but being in the pockets of arms manufacturers and other doctors of death is so far not among them, to our best knowledge.

Hillary and her crowd ran the entire election process from inside a cocoon, built largely on hubris and a lack of contact with the world outside. They had the media so much on their side that TV and newspapers became part of the Hillary cocoon, and reporters got locked into a groupthink mode that then in its turn infected the campaign itself.

What I mean is you can’t stop at saying Trump is a disaster, so let’s pick the other side, it was always very much a choice between two disasters. And at the same time, as I wrote at the Automatic Earth the day of the election, the US presidency is a poisoned chalice. There’s nothing simple about this.

Trump means a big clean-up for the GOP, and the Hillary loss means the chance for the Democrats to do the same. You bet those folks realize achingly well they could have won with Bernie. Hopefully that wing can take over substantially from the lying conniving machinery the DNC has turned out to be.

Someone summed it up as: Trump swept aside the Republicans, the Democrats, the Bush dynasty and the Clinton dynasty, all in one fell swoop, and we should perhaps be thankful to him for that.

Trump has run his campaign catering to the anger that exists among Americans. And people experience and label that as ‘terrible’ and ‘awful’. His Republican friends and opponents find it terrible, because it scares the bejeezus out of them, and they’re too scared to go anywhere near that anger. Trump embraced the anger. Because he knew from the start, instinctively, that it was the only way he could win.

And you can think like the majority of your peers do, that all that commingling with the anger, with racists and bigots and what have you, is inexcusable. But what you miss out on if you take that approach and hold on to it, is that in that case the anger does not get addressed at all. It’s instead left free to just wander over the land and fester and grow on society, out of reach of politics, media, everything.

A certain by now very vilified cartoonist explained that what Trump does is to ‘feel’ what the angry crowd wants, and then play into it by making over the top statements targeted at the anger. That way this crowd will follow him, gather around him. This has worked like a charm. But no, that doesn’t make him look like a certain German dictator.

Because it does not mean that Trump is going to literally do everything he said in the over the top statements he made. It’s all just a basic sales trick. Trump makes the angry people feel like he knows, and cares about, their grievances. Just like a car salesman makes you think he knows just what you want and need in a car, and praises the assets of that car in such a way that it touches that part of you which makes you want the car.

But that doesn’t mean at the end of the day he’ll drive the same car home that you just bought off of him. He makes you think he is like you, and knows what you want, so he can sell you that car. That’s all. He’s judged you to be the right ‘target’ for that vehicle.

That is how Trump has reeled in America’s hidden anger, how he has gathered its lost hidden mob. And before you say anything else, it’s perhaps a good idea to wonder where that anger would go without Trump. Because it’s not going to go away by itself. It’s been growing and festering for a long time, and it’s well-armed, lest you forget.

The question then becomes: would America be a better, or a safer, place if the entire angry part of its population had again, and still, been ignored by everyone? Or is it better to have them gathered under the umbrella of Donald Trump? Take your pick. Don’t be shy.

Another way to phrase the issue is this: without the exact same sales tactics that Trump used to ‘gather the anger’ around him, the TV ads (most ads in general) you see on a daily basis would look completely different. Whatever products these ads sell, from detergents to cars, they do it by referring to your unconscious, not your rational abilities.

The ads, like Trump, sell feelings, not facts (if you don’t get that, you’re lost).

Yet nobody would think of taking the companies whose products are advertized this way to court -nobody even gets really angry with them- because the happy smily people and unending open roads bathed in sunshine from the ads do not magically appear once you purchase the product. We would even find that crazy, that anyone might take the images shown in the ads, literally.

We should interpret Trump’s campaign words along those same lines, the same way we ‘undergo’ the ads that play to our subconscious. The problem is, how do you do that? How do you interpret what you are largely unaware of on a rational level?

The president-elect will now need the same skills in order to ‘come down that mountain’ without antagonizing each and every side of the discussion, of the nation. He’ll have to convince the liberal camp that he didn’t mean everything he said in a literal sense, while at the same time keeping his ‘angry mob’ satisfied that he will do enough of what he promised them.

That will take a lot of persuading. But at the same time that happens to be the one thing he’s really good at. He’ll have to convince his voters that he’s not breaking his promises, just adjusting them in ways that will, if at all possible, be even more beneficial to them than the original ones.

Difficult, but if he can convince them that there are signs, delivered relatively fast, that their living conditions are improving, he may succeed. They just vent their anger at people that are visibly not themselves, but that’s not where the anger stems from.

There are all sorts of nasty things going on, racists and supremacist etc. But you can’t say that Trump caused that to happen. The most you could say is that he gives the people involved in that stuff the idea that because someone finally hears them, they can, are allowed to, make themselves heard.

But just because a few loose cannons let loose, doesn’t mean America has 60 million loose cannons who all voted for Trump and should all be condemned including Trump himself for good measure because there’s a few incidents. Not only is that a misinterpretation of what goes on, it prevents you from understanding what lies behind.

Those incidents at least have a lot to do with the fact that so many ignored Americans live in what Washington has long considered flyover country. It would be a lot more positive and productive at this point in time if everyone looks at what they themselves have gotten wrong over the past years -not just this election campaign- before pointing fingers at everyone but themselves.

But seeing the dug-in heels in Britain almost five months after the Brexit vote, it’s hard to get your hopes up about people coming together, or even doing some genuine introspection. It’s easier to just remain stuck in your comfy little rut.

Thing is, the world is rapidly changing -it already has-, America is changing, Britain is, and many more countries will, it just takes an election to show how much. We’re transitioning to a next phase, and trying to deny we are with all our might, good luck and good night.

Or in a more poetic fashion – we can do that too-:

the blizzard of the world

has crossed the threshold

and it has overturned

the order of the soul

![U.S. Secretary of State John Kerry sits with British Prime Minister Theresa May in the White Room No. 10 Downing Street in London, U.K., on July 19, 2016. [State Department Photo]](https://consortiumnews.com/wp-content/uploads/2016/07/28376382456_56ae215c9f_k.jpg)