G. G. Bain Temporary footpath, Manhattan Bridge 1908

New cases in:

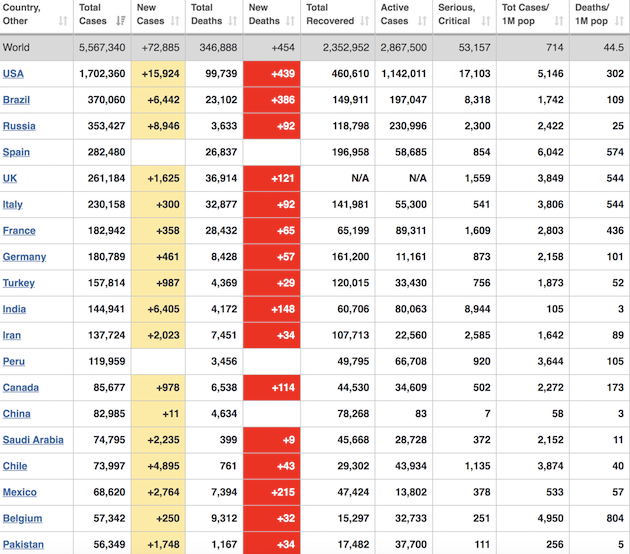

• US + 19,790

• Brazil + 11,456

• Russia + 8,946

• India + 6,589

• Chile + 4,895

BREAKING: Coronavirus Outbreak

US still going down slowly due to decline in top states, NY, NJ, IL, MA, increase in others. CA just passed MA. Testing has reached new high, 441k

Yesterday 20,634, states with most new cases IL, CA, NY. Today now 19,754

Good news on Italy next pic.twitter.com/PXzZpVPxrZ

— Yaneer Bar-Yam (@yaneerbaryam) May 26, 2020

Note: only 1,300 deaths worldwide in 24 hours?!

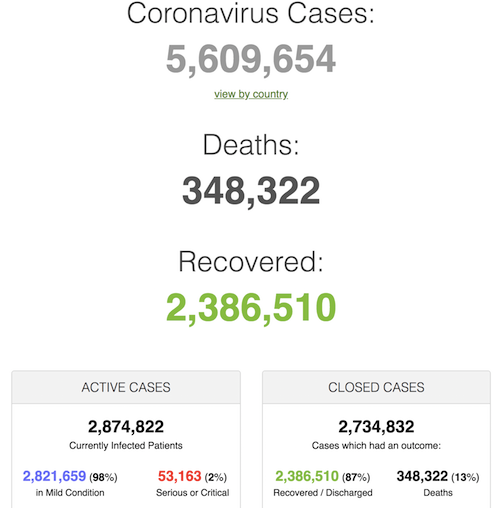

• Cases 5,609,654 (+ 88,909 from yesterday’s 5,520,745)

• Deaths 348,322 (+ 1,300 from yesterday’s 347,022)

From Worldometer yesterday evening -before their day’s close-

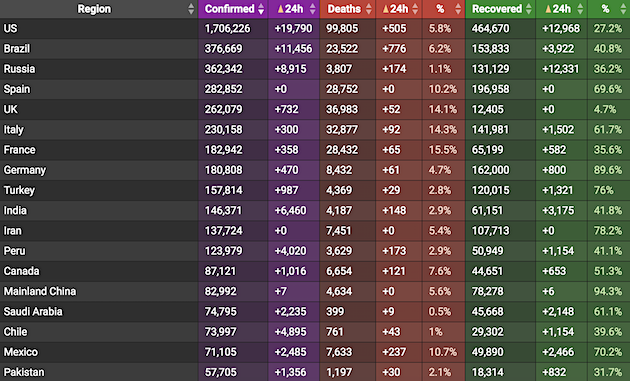

From Worldometer

From SCMP:

From COVID19Info.live:

Few certainties, but important research, that every country and city should do.

• 8,000 Additional Deaths In Mexican Capital As Coronavirus Rages – Study (R.)

Mexico’s capital registered 8,072 more deaths in the first five months this year than the average from the same period over the past four years, an analysis by independent researchers showed on Monday, suggesting a possible surge due to the coronavirus. Health officials have reported 1,655 deaths from the virus in Mexico City, out of 7,394 deaths nationwide. They have also acknowledged that the true death toll is higher, but difficult to estimate due to a low testing rate. Software developer Mario Romero Zavala and economic consultant Laurianne Despeghel, whose analysis was published in Mexican magazine Nexos, tallied 39,173 fatalities this year through May 20 by extracting data from Mexico City’s online database of death certificates.

Over the prior four years, they calculated just 31,101 deaths on average during the same period, using the same database. Mexico City’s official count of deaths from the coronavirus represents just over 20% of the study’s “excess mortality” – a term used by epidemiologists to estimate the increase in deaths, versus normal conditions, attributable to a public health crisis. Excess mortality is difficult to calculate in Mexico because the most recent data on fatalities from the national statistics institute is from 2018. Despeghel said the analysis was only a first step to measuring the virus’ impact. “While studying excess deaths allows us to identify a higher mortality rate during the COVID-19 crisis, it is not sufficient to attribute it directly or solely to the virus,” she said.

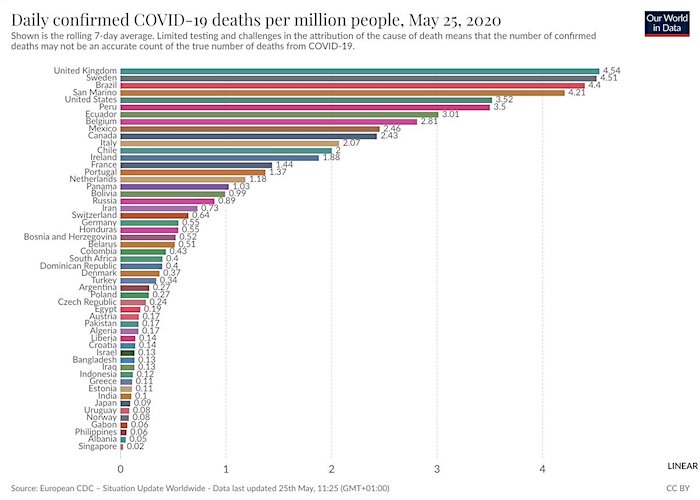

But the US will come roaring back. Note that Sweden is in second place after the UK over the past week.

• Brazil Surpasses US In Daily Coronavirus Death Toll (R.)

Brazil daily coronavirus deaths were higher than fatalities in the United States for the first time over the last 24 hours, according to the country’s Health Ministry. Brazil registered 807 deaths over the last 24 hours, whereas 620 died in the United States. Brazil has the second worst outbreak in the world, with 374,898 cases, behind the U.S. with 1.637 million cases. Total deaths in the U.S. has reached 97,971, according to Reuters tally compared with Brazil at 23,473.

I kid you not, they call it a “solidarity trial”. Do keep providing it for malaria and lupus, but, because of ONE article in the Lancet, not for COVID19.

• WHO Halts Hydroxychloroquine Trial For Coronavirus Amid Safety Fears (G.)

The World Health Organization has said it will temporarily drop hydroxychloroquine — the malaria drug Donald Trump said he is taking as a precaution — from its global study into experimental coronavirus treatments after safety concerns. The WHO’s director-general Tedros Adhanom Ghebreyesus said in light of a paper published last week in the Lancet that showed people taking hydroxychloroquine were at higher risk of death and heart problems than those who were not, it would pause the hydroxychloroquine arm of its solidarity global clinical trial. “The executive group has implemented a temporary pause of the hydroxychloroquine arm within the solidarity trial while the safety data is reviewed by the data safety monitoring board,” Tedros said on Monday. “The other arms of the trial are continuing,”

He said the concern related only to the use of hydroxychloroquine and chloroquine for Covid-19, adding that the drugs were accepted treatments for people with malaria and auto-immune diseases. Other treatments in the WHO’s solidarity trial, including the experimental drug remdesivir and an HIV combination therapy, are still being pursued. Hydroxychloroquine has been licensed for use in the US since the mid-1950s and is listed by the WHO as an essential medicine. There are numerous trials under way of the two drugs against coronavirus but neither is a proven treatment. The US National Institutes of Health is also running a clinical trial to establish whether the drug, administered with the antibiotic azithromycin, can prevent hospital admissions and death from Covid-19.

A controversial French doctor who has promoted the use of hydroxychloroquine and chloroquine for coronavirus said on Monday he stood by his belief the drugs could help patients recover. He also rejected the Lancet study of the records of 96,000 patients across hundreds of hospitals. “How can a messy study done with ‘big data’ change what we see?”, Prof Didier Raoult asked in a video posted on the website of his infectious diseases hospital in Marseille. “Here we have had 4,000 people go through our hospital, you don’t think I’m going to change because there are people who do ‘big data’, which is a kind of completely delusional fantasy,” he said.

Following a conference call with Chinese experts on March 18, Costa Rica was the first and only Central American country to immediately adopt hydroxychloroquine against COVID.

The resulting divergence of the course of the pandemic grows more spectacular day after day. pic.twitter.com/T1tmerB9pE— Covid19Crusher (@Covid19Crusher) May 25, 2020

Every decision maker should take an in-depth crash course in risk.

• Tail Risk Of Contagious Diseases – Cirillo/Taleb (Nature)

The central point we wish to convey is the following: the more fat-tailed a statistical distribution, the more the ‘tail wags the dog’. That is to say, more statistical information resides in the extremes and less in the ‘bulk’—the events of high frequency—where it becomes almost noise. Under fat tails, the law of large numbers works slowly, and moments—even when they exist—may become uninformative and unreliable5. All this makes EVT the most effective and robust approach for risk management purposes, even with relatively small datasets like ours. The presence of a fat right tail in the distribution of pandemic fatalities has the following policy implications, useful in the wake of the COVID-19 pandemic.

First, it should be evident that it is not appropriate to compare fatalities from multiplicative infectious diseases (fat-tailed, like a Pareto distribution) to those from car accidents, heart attacks or falls from ladders (thin-tailed, like a Gaussian). This remains a common (and costly) error in policy making, and in both the decision sciences and the journalistic literature. Some research papers even criticise the wider public’s ‘paranoia’ with respect to pandemics, not appreciating that such a paranoia is merely responsible (and realistic) risk management in front of potentially destructive events. The main problem is that those articles—often relied upon for policy making—consistently use the wrong thin-tailed distributions, underestimating tail risk, so that every conservative or preventative reaction is bound to be considered an overreaction.

— Nassim Nicholas Taleb (@nntaleb) May 25, 2020

Have you seen Bill Gates lately? That’s the guy that all these tough -formerly- Americans are so afraid of.

Are these people still using Microsoft software, further enriching Gates?

• 44% of Republicans Think Bill Gates Will Use Vaccine To Implant Microchip (BI)

A new survey by Yahoo News and YouGov has found that 44% of Republicans believe that Bill Gates will use the COVID-19 vaccination to implant a location-tracking microchip into the vaccine recipient, a conspiracy theory that has gained traction among fringe groups and conservative pundits. The survey also found that 26% of Republicans do not believe the false microchip vaccine narrative, while 31% remained undecided on the topic. Half of the people surveyed who use Fox News as their main source of TV news also believe the debunked theory. However, the poll also noted that 19% of Democrats, 24% of Independents, and 15% of people who use MSNBC as their source of TV news also believe the microchipping myth.

For the survey, YouGov conducted an online interview of a “nationally representative” group of 1,640 US adults who were a part of YouGov’s opt-in panel between May 20 and 21. There is about a 3% margin of error. An earlier Yahoo News and YouGov poll also found that only 55% of Americans surveyed would want the coronavirus vaccine when it becomes available. The rest were either unsure (26%) or did not plan on receiving the vaccine (19%). President Donald Trump has said that he is “very confident” that a coronavirus vaccine will be ready by the end of the year, while experts have predicted that the vaccine development could take up to 12 to 18 months to prepare.

You’re right, maybe this is all Bill Gates too. Maybe he bought the Forbidden City.

• China’s Coronavirus Campaign Offers Glimpse Into Surveillance System (R.)

The coronavirus outbreak in China has given unprecedented glimpses into how an extensive system of surveillance cameras works, as monitoring stations are rebranded epidemic “war rooms” helping to check people’s movements and stifle the disease. China is trying to build one of the world’s most sophisticated surveillance technology networks, with hundreds of millions of cameras in public places and increasing use of techniques such as smartphone monitoring and facial recognition. This year, cities and villages across the country have used the system for what the government has labelled “an all-out people’s war on coronavirus”.

While authorities have primarily used mobile location data and ID-linked tracing apps to flag people coming back from abroad for quarantine, the camera surveillance system has played a crucial role, according to officials, state media and residents. The network has been used to trace the contacts of people confirmed as infected with the virus, and to punish businesses and individuals flouting restrictions. “This is a war situation,” said a civil servant surnamed Wang in Tianjin city, who was involved in tracing thousands of people linked to a coronavirus cluster at a department store. “We must adopt war-time thinking.” Despite the hi-tech ambitions of the system, it is heavily dependent on a lot of people watching footage on screens. Known as “grid members”, they sit in monitoring rooms or squint over smart-phone feeds from the networks of cameras.

“This type of surveillance is far more human driven than it is tech driven, said James Leibold, associate Professor at Australia’s La Trobe University, who researched similar systems in China’s far-west Xinjiang. State media, officials and local governments have given accounts of the system in action in the campaign against the coronavirus. In Donghan village in Hubei, the province where the coronavirus emerged late last year, grid member Liu Ganhe saw six villagers gathering without masks, so he called the authorities. “Village cadres rushed to the scene to disperse the crowd and educate the people,” media said, praising the “wartime restrictions” the system was able to enforce.

There are really people who could see this happening in the west?!

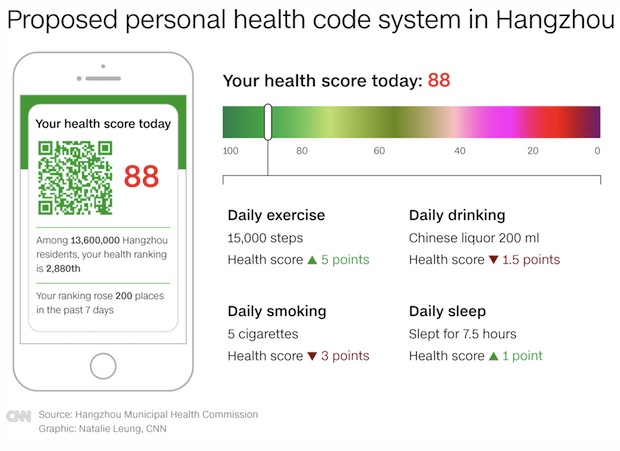

• Chinese City To Score And Rank Its Residents Based On Health, Lifestyle (CNN)

Imagine a smartphone app that has access to your medical records and assigns you a daily score based on your preconditions, recent checkups and lifestyle habits — how much you’ve drunk, smoked, exercised and slept on any given day can all affect your points total, boosting or lowering your ranking. That “health score” will be embedded in a digital QR code accessible on your phone, ready to be scanned whenever needed. This is what the city government of Hangzhou in eastern China has envisioned for its more than 10 million residents, inspired by a “health code” system it adopted during the Covid-19 pandemic to profile people based on their risk of infection.

Across the globe, governments have stepped up the collection of personal data in their fight against the novel coronavirus, which has killed more than 345,000 people and infected close to 5.5 million, according to data collected by Johns Hopkins University. But there are also fears that some of these extraordinary measures could be here to stay even after the public health crisis is over, posing a long-term threat to privacy. That concern was amplified among Hangzhou residents when their municipal government announced Friday that it was planning to make permanent a version of the “health code” app used during the pandemic.

Since February, the Chinese government has used a color-based “health code” system to control people’s movements and curb the spread of the coronavirus. The automatically generated quick response codes, commonly abbreviated to QR codes, are assigned to citizens on their smartphones as an indicator of their health status. The color of these codes — in red, amber or green — decides whether users can leave home, use public transport and enter public places. The health codes can also serve as a tracker for people’s movements, as residents have their QR codes scanned as they enter public places. Once a confirmed case is diagnosed, authorities are able to quickly trace where the patient has been and identify people who have been in contact with that individual.

Hangzhou, a coastal city about a hundred miles southwest of Shanghai, was among the first cities to use the health code system to decide which citizens should go into quarantine. But now, the city government says it wants the “health code” to be “normalized” — meaning it could be here to stay well beyond the pandemic.

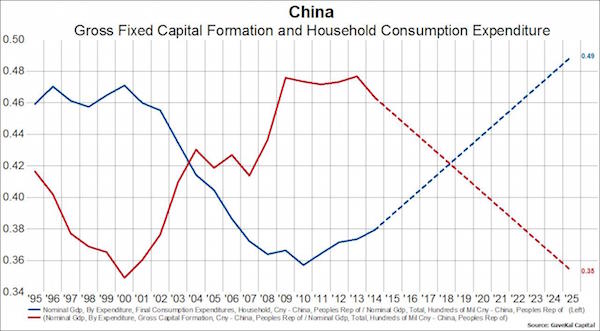

Two years ago, the reserve requirement ratio was 14.2%, now it’s 9.4%. But Chinese banks haven’t shed risk. So this is dangerous. The RRR, simplified, is a gauge of the bad debt they hold, and I bet you it’s way more than 9.4%.

• PBOC Lowers RRR For China Financial Institutions To 9.4% (Xinhua)

The average reserve requirement ratio (RRR) for financial institutions stood at 9.4 percent on May 15, down 5.2 percentage points from the beginning of 2018, the People’s Bank of China (PBOC) said. The PBOC has lowered the RRR 12 times since 2018, releasing about 8 trillion yuan (about 1.12 trillion U.S. dollars) in long-term funds to bolster the real economy. Of the total, four RRR cuts in 2018 released 3.65 trillion yuan, five RRR cuts in 2019 released 2.7 trillion yuan and three RRR cuts in the first five months this year released 1.75 trillion yuan. The RRR cuts have led to the contraction of the balance sheet of the PBOC, but this will not cause the tightening of money supply and is contrary to the balance sheet reduction of the central banks of the developed economies such as the U.S. Federal Reserve to reduce the bond holdings, the PBOC said.

The contraction has a strong expansion effect and the main reason is that lowering the RRR means commercial banks will have less money locked up by the central bank and more money for free use, the PBOC said. The RRR cuts have helped meet the liquidity demand of the banking system, boost support for small businesses, cut the social financing cost, promote the market-oriented and law-based debt-to-equity swaps, the central bank said. The cuts have encouraged the rural financial institutions to serve local entities, supported the epidemic prevention and control as well as enterprise work resumption, and played a positive role in bolstering the real economy, the PBOC said.

The protests will pick up again.

• Hong Kong Homebuyers Walk Away, Forfeit $1.5 Million In Deposits (SCMP)

Nineteen Hong Kong homebuyers who put down deposits for flats at the height of a market rally around June 2018 have walked away from their purchases, forfeiting as much as HK$11.83 million (US$1.53 million) and HK$12.4 million in two instances over the past month. Nine buyers walked away from Hong Kong developer K Wah International’s Solaria project in Tai Po district, forfeiting the HK$11.83 million on Friday, according to the project’s Register of Transactions. The second instance, of 10 forfeitures, was reported from Solaria on April 29. Altogether, more than 100 homebuyers have walked away from their purchases so far this year, according to reports.

Hong Kong’s economy has taken a battering since the heydays of June 2018. The year-long US-China trade war, the city’s anti-government protests and the novel coronavirus outbreak have all taken their toll, pushing the city’s economy into recession over two quarters of economic contraction. The proposed introduction of a new national security law by Beijing, announced at “Two Sessions” last week, has added to the turmoil by sparking fears about market stability.

Centa-City Leading Index, Centaline’s timelier price index for used homes, has declined about 5 per cent between June 2018 and now. It has dropped about 6.8 per cent since June 2019.

What exactly is the game? Is CNN supporting Trump?

• Why Joe Biden Can Do No Wrong (Turley)

Below is my column in The Hill newspaper on special dispensation given Joe Biden by members of Congress, commentators, and the media. We previously discussed the muted media response to false legal comments from President Barack Obama and other Obama officials on the Flynn case. The pattern of media avoidance is more glaring with recent Biden controversies. Notably, the column ran when Biden gave his interview on the radio show “The Breakfast Club” that “if you have a problem figuring out whether you’re for me or Trump, then you ain’t black.” This weekend, I was critical of segments on CNN and NBC’s Meet the Press which quoted Biden but cut off the line where he falsely claimed to have received multiple endorsements from the NAACP.

CNN’s John King derisively referred to controversy as something people are “trying to make hay” out of and then played the interview. However, CNN clipped the tape to leave out the next line where Biden declared “The NAACP has endorsed me every time I’ve run. Come on, take a look at my record.” Despite that invitation to look at his record, CNN and other media routinely cut out the false statement and also omitted any discussion of the false claim linked to the NAACP. On a story about Biden’s claim that all black voters must vote for him (or not be truly black), it would seem material that he also falsely claimed endorsements from the leading organization in the African American community. However, it was routinely omitted from the tape and Biden has not been asked to respond to the rebuttal from the NAACP. It is precisely the type of crafting of the coverage to confine damage for Biden that is discussed in the column.

Once Emmet Sullivan gives in, Michael Flynn will be free to speak.

What “the Resistance” really fears more than anything is General Michael Flynn’s mouth. He’s been under a judicial gag order since his case went before Judge Emmet Sullivan’s federal district court. Understandably, Gen. Flynn wasn’t eager to complicate his unjust plight with a contempt citation. Judge Sullivan’s recent shenanigans have one object: to keep that gag order in force as long as possible. The moment Judge Sullivan confirms the DOJ’s move to dismiss the charges, as he is duty-bound to do, General Flynn will be free to offer his views to the public. That might be inconvenient in an election season.

I’m sure he has a lot to say. Gen. Flynn was head of the Defense Intelligence Agency for two years (2012 – 2014) under Barack Obama, and he knows a ton about every crooked operation Mr. Obama presided over, including the Benghazi fiasco, the Ukraine regime change op, and especially Mr. Obama’s hijacking of the NSA supercomputer surveillance database known as “the Hammer,” which was set up originally to track terrorists and then used by DNI James Clapper and CIA chief John Brennan to spy on Americans, most particularly Mr. Obama’s political adversaries. It’s rumored that Mr. Obama took the database with him when he left the White House, and it is said to contain great gouts of usefully damning information about just about everyone in government, including senators, congressmen, and Supreme Court justices.

Gen. Flynn became an antagonist to Obama & Co. when he objected to the nuclear deal they were cooking up with Iran and when he spoke out against the CIA’s 2013 Timber Sycamore op to arm and give money to Isis terrorists opposing Syrian President Bashar al-Assad. Mr. Obama canned Gen. Flynn in 2014. What really sealed Gen. Flynn’s fate was when he started publicly complaining about the politicization of John Brennan’s CIA. The New York Times quoted him saying, “They’ve lost sight of who they actually work for. They work for the American people. They don’t work for the president of the United States. Frankly, it’s become a very political organization.”

After McMaster replaced Flynn he asked Susan Rice who he should appoint as his personal aide

She suggested someone she considered loyal in the Obama Admin who was still on NSC

His name?

Eric Ciaramella

— Jack Posobiec (@JackPosobiec) May 26, 2020

There’s a major battle coming, but I don’t see Bill Barr playing a major role in it.

• Bill Barr Calls Action of Mueller and Rosenstein “Abhorrent” (CTH)

For well over a year we’ve been saying AG Bill Barr’s biggest challenge is not investigating the soft-coup but rather managing through what We The People are already aware of. With that in mind; and with congress moving to put former DAG Rod Rosenstein and former Special Counsel Robert Mueller under a microscope; it is interesting to note AG Bill Barr recently conceding his two friends were corrupt.

[Transcript] …”Now what happened to the president – and I’ve said this many times – what happened to the president in the 2016 election; and throughout the first two years of his administration was abhorrent. It was a grave injustice and it was unprecedented in American history.” “The law enforcement and intelligence apparatus of this country were involved in advancing a false and utterly baseless Russian-collusion narrative against the president.” The proper investigative and prosecutive standards of the Dept of Justice were abused, in my view, in order to reach a particular result.” ~ (AG Barr, May 18, 2020)

How can AG Barr say the DOJ/FBI conduct during the first two years of the administration “was abhorrent” without specifically implying his two friends, Robert Mueller and Rod Rosenstein were complicit in the “grave injustice” he outlines? It is interesting that no media (of any disposition) has ever questioned AG Barr about Rosenstein and Mueller considering his words that outline their behavior as abhorrent.

For two years, @CNN was THE platform for Adam Schiff and James Clapper to claim there was "significant evidence" of Russian collusion.

Now we know multiple former Obama admin. officials said under oath they saw no such evidence… including Clapper. pic.twitter.com/5mwAJSFeJO

— MRCTV (@mrctv) May 18, 2020

Watch what happens RIGHT after James Clapper is FINALLY asked a tough question by CNN.

Seriously, wait for it…pic.twitter.com/8pDwh0fZdF

— Former Democrats for Trump (@YoungDems4Trump) May 24, 2020

4 seconds.

Note: it’s not a Michael Moore film, his name was used only for publicity. And now the detractors use it too. Is that wise?

• Michael Moore Film Planet of the Humans Removed From YouTube (G.)

YouTube has taken down the controversial Michael Moore-produced documentary Planet of the Humans in response to a copyright infringement claim by a British environmental photographer. The movie, which has been condemned as inaccurate and misleading by climate scientists and activists, allegedly includes a clip used without the permission of the owner Toby Smith, who does not approve of the context in which his material is being used. In response, the filmmakers denied violating fair usage rules and accused their critics of politically motivated censorship. Smith filed the complaint to YouTube on 23 May after discovering Planet of the Humans used several seconds of footage from his Rare Earthenware project detailing the journey of rare earth minerals from Inner Mongolia.

Smith, who has previously worked on energy and environmental issues, said he did not want his work associated with something he disagreed with. “I went directly to YouTube rather than approaching the filmmakers because I wasn’t interested in negotiation. I don’t support the documentary, I don’t agree with its message and I don’t like the misleading use of facts in its narrative.” Planet of the Humans director Jeff Gibbs said he was working with YouTube to resolve the issue and have the film back up as soon as possible. He said in a statement: “This attempt to take down our film and prevent the public from seeing it is a blatant act of censorship by political critics of Planet of the Humans. It is a misuse of copyright law to shut down a film that has opened a serious conversation about how parts of the environmental movement have gotten into bed with Wall Street and so-called “green capitalists.” There is absolutely no copyright violation in my film. This is just another attempt by the film’s opponents to subvert the right to free speech.”

Planet of the Humans, which has been seen by more than 8 million people since it was launched online last month, describes itself as a “full-frontal assault” on the sacred cows of the environmental movement. Veteran climate campaigners and thinkers, such as Bill McKibben and George Monbiot, have pointed out factual errors, outdated footage and promotion of myths about renewable energy propagated by the fossil fuel industry. Many are dismayed that Moore – who built his reputation as a left-wing filmmaker and supporter of civil rights – should produce a work endorsed by climate sceptics and right-wing thinktanks. Several have signed a letter urging the removal of what they called a “shockingly misleading and absurd” documentary. Climate scientist Michael Mann said the filmmakers “have done a grave disservice to us and the planet” with distortions, half-truths and lies.

Buiter is your typical career insider. His opinions are pretty useless.

• Time for a Selective Debt Jubilee (Willem Buiter)

Across most advanced economies, much of the additional private debt accumulated during the crisis will likely end up being owned by public entities, including central banks, and most of it will never be repaid. To protect their independence and political legitimacy, central banks should not act as fiscal principals. And yet, in the case of small and medium-size enterprises, it is simply obvious that COVID-19-related debt will have to be forgiven. The national Treasury will need to compensate the central bank for any losses it incurs.For publicly traded companies the debt held by public creditors should be turned into equity, in the form of non-voting preference shares, which would minimize the impression that the pandemic had inaugurated a new era of central planning.

Again, the national Treasury will have to indemnify the central bank for any losses it incurs. An equitization option should be attached to all newly issued public debt. The resulting equity instruments could represent claims on part of the government’s primary budget surplus, or their interest rates could be linked to GDP growth. But poorer countries will not have this option. According to the Brookings Institution, emerging markets and developing countries already owe about $11 trillion in external debt and face $3.9 trillion in debt-service costs this year. In April, the World Bank and the IMF offered a modicum of debt relief to many of these countries, and the G20 agreed to a temporary payment standstill for official debt, which paved the way for hundreds of private creditors to do the same.

Yet these forms of assistance offer too little, too late. The fact is that most of these debts never should have been issued in the first place. Grants are the proper way to transfer resources to low-income countries. After World War II, the Marshall Plan involved only grants; today, the case for “corona grants” to low-income countries could hardly be stronger. Under the IMF and the World Bank’s 1996 Heavily Indebted Poor Countries (HIPC) initiative, some 36 countries received full or partial debt relief. It is time to return to that idea, starting with a comprehensive round of debt forgiveness for the world’s poorest countries. This selective jubilee should include debts owed to the IMF, the World Bank, other multilateral lenders, national sovereigns, official bodies like state-owned enterprises, and private creditors.

Debt is a dangerous instrument. For far too long, the world has used it to avoid awkward but unavoidable decisions. In the midst of an unprecedented global crisis, something will have to give.

I don’t think many people understand how bad the situation will be during and after the virus. Recovery and return to normal are pretty much empty terms now.

• Debt, Liberty and “Acts of God” (Michael Hudson)

Western civilization distinguishes itself from its predecessors in the way it has responded to “acts of God” disrupting the means of support and leaving debts in their wake. The great question always has been who will lose under such conditions. Will it be debtors and renters at the bottom of the economic scale, or creditors and landlords at the top? This age-old confrontation between creditors and debtors, landlords and tenants over how to deal with the unpaid debts and back rents is at the economic heart of today’s 2020 coronavirus pandemic that has left large and small businesses, farms, restaurants and neighborhood stores – along with their employees who have been laid off – unable to pay the rents, mortgages, other debt service and taxes that have accrued.

For thousands of years ancient economies operated on credit during the crop year, with payment falling due when the harvest was in – typically on the threshing floor. Normally this cycle provided a flow of crops and corvée labor to the palace and covered the cultivator’s spending during the crop year, with interest owed only when payment was late. But bad harvests, military conflict or simply the normal hardships of life occasionally prevented this buildup of debt from being paid, threatening citizens with bondage to their creditors or loss of their land rights. Mesopotamian palaces had to decide who would bear the loss when drought, flooding, infestation, disease or military attack disrupted economic activity and prevented the settlement of debts, rents and taxes.

Recognizing that this was an unavoidable fact of life, rulers proclaimed amnesties for taxes and the various debts that were incurred during the crop year. These acts saved smallholders from having to work off their debts by personal bondage and ultimately to lose their land. Classical antiquity, and indeed subsequent Western civilization, rejected such Clean Slates to restore social balance. Since Roman times it has become normal for creditors to use social misfortune as an opportunity to gain property and income at the expense of families falling into debt. In the absence of kings or democratic civic regimes protecting debtor rights and liberty, pro-creditor laws obliged debtors to lose their land or other means of livelihood to foreclosing creditors, sell it under distress conditions and fall into bondage to work off their debts, becoming clients or quasi-serfs to their creditors without hope of recovering their former free status.

We try to run the Automatic Earth on people’s kind donations. Since their revenue has collapsed, ads no longer pay for all you read, and your support is now an integral part of the interaction.

Thank you.

Even if every single person in New York City had already been infected, 0.3% of New York City would be about 24000, and New York City had already passed that in excess deaths by the end of April. In other words, this is complete nonsense. https://t.co/d8tuGcAFAA

— Christopher D. Long (@octonion) May 25, 2020

He fought and survived Ebola, and now he's on the frontline of #COVID19 in NYC.

This is a day working in the ER, as told by Dr.@Craig_A_Spencer. pic.twitter.com/gXmnD4qbW7

— AJ+ (@ajplus) May 24, 2020

Support the Automatic Earth in virustime.