NPC Congressman John C. Schafer of Wisconsin 1924

As the Automatic Earth has said for many years, he USD won’t be the first to go. It’s about dollar-denominated debt.

• Is the U.S. Dollar Set to Soar? (CH Smith)

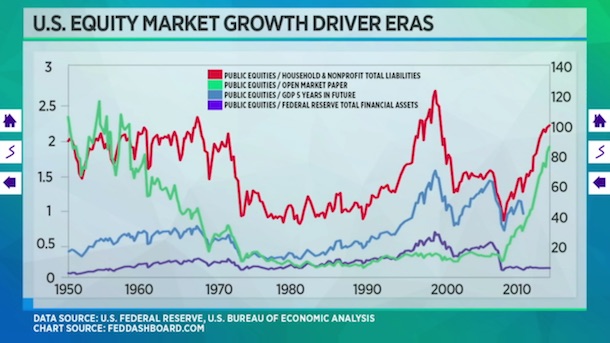

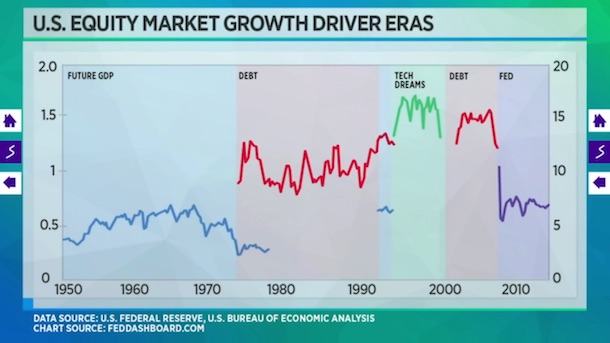

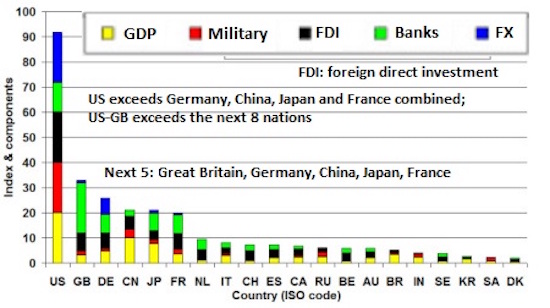

Which blocs/nations are most likely to face banking/liquidity crises in the next year? Hating the U.S. dollar offers the same rewards as hating a dominant sports team: it feels righteous to root for the underdogs, but it’s generally unwise to let that enthusiasm become the basis of one’s bets. Personally, I favor the emergence of non-state reserve currencies, for example, blockchain crypto-currencies or precious-metal-backed private currencies – currencies which can’t be devalued by self-serving central banks or the private elites that control them. But if we set aside our personal preferences and look at fundamentals and charts, odds seem to favor the U.S. dollar making a major move higher in the next few months. Let’s start with a national index of finance-power which combines GDP, military spending, banking, foreign direct investment (FDI) and foreign exchange:

The key take-away is the preponderance of the U.S. and the Anglo-American alliance, a.k.a. the special relationship of Great Britain and the U.S. The U.S. exceeds Germany, China, Japan and France combined, and the U.S.-Great Britain alliance is roughly equal to the next 10 nations: the four listed above plus The Netherlands, Switzerland, Italy, Spain, Canada and the Russian Federation. We don’t have to like it, but as investors it’s highly risky to act like it isn’t reality.

If the whining about Beautiful Brexit would finally stop in the UK, maybe they could do something constructive.

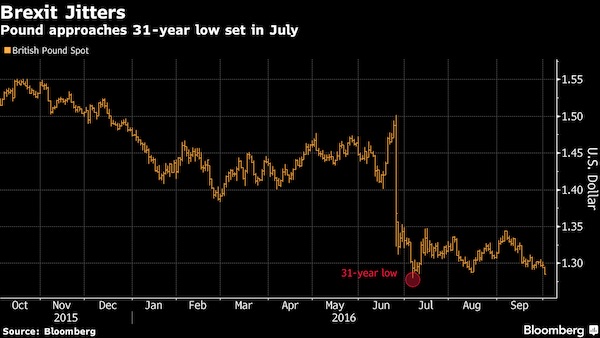

• Pound Nears Three-Decade Low as May Sets Date for Brexit Trigger (BBG)

The pound approached the three-decade low set in the days following the Brexit referendum after U.K. Prime Minister Theresa May said she’ll begin the process of withdrawal from the European Union in the first quarter of 2017. Sterling dropped to the weakest level since July 6, the day it reached its 31-year low of $1.2798, and slipped against all of its 31 major peers. Hedge-fund data showed speculators raised bets that the currency would fall. May told delegates at her Conservative Party’s annual conference that she’ll curb immigration, stoking speculation the nation is headed toward a so-called hard Brexit. Stocks of U.K. exporters rose, boosted by the weaker currency. “We’re back to the Brexit risks,” said Vishnu Varathan, a senior economist at Mizuho Bank Ltd. in Singapore. “Sterling has taken a bit of a knock.”

Let’s see large-scale global issuance of debt in yuan. Then we talk.

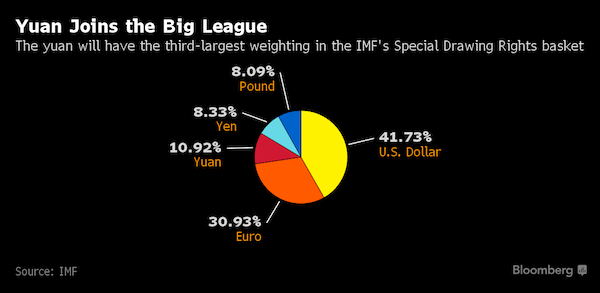

• China Seeking To Succeed Where Japan Failed In Reserve Currency Push (BBG)

Like the yuan, the yen’s march toward liberalization was gradual and marked with ambivalence. Under the Bretton Woods system after World War II, the Japanese currency was fixed at 360 a dollar, before a trading band was introduced in 1959 to make it slightly more flexible. For three decades, all capital flows except those explicitly permitted were banned, making it easier for the government to achieve policy goals. It wasn’t until 1998 that approval or notification requirements for financial transactions and outward direct investments were abolished. The push to internationalize the yen initially came from the U.S., which wanted greater global use to fuel appreciation and reduce Japan’s trade surplus with America. China’s situation now isn’t dissimilar.

Having thrived on an economic model of closed borders and accumulation of reserves for decades, its capital account is still closed, individuals’ foreign-exchange conversions are capped and inter-country money flows occur mainly through specific programs. Policy makers have tightened controls on outflows in the past year after the yuan’s August 2015 devaluation exacerbated depreciation pressures. The currency was little changed Friday at 6.68 per dollar. Lowering the hurdles to create a true freely traded currency might risk a flight of capital during times of weakness, a concept China doesn’t always seem comfortable with. “Everyone wants this thing called ‘exorbitant privilege,’ but if you try to give it to them, they get furious and they tell you to stop,” said Michael Pettis, a finance professor at Peking University.

“Countries like China that are running huge surpluses because of insufficient domestic demand – basically they are creating the role of the dollar as the dominant reserve currency.” The term “exorbitant privilege,” coined by former French finance minister Valery Giscard D’Estaing in 1965, referred to the benefits the U.S. received for the dollar’s status. Daniel McDowell, a Syracuse University political science assistant professor who studies international finance, made the point that the appeal of a nation’s sovereign debt market plays a key role in a currency’s internationalization. The yen never became a major reserve currency because its government bonds weren’t as attractive or as plentiful as the U.S., he said.

Everyone’s just trying to save face by now. Merkel, Obama, DOJ.

• Deutsche Bank Races Against Time To Reach US Settlement (R.)

Deutsche Bank is throwing its energies into reaching a settlement before next month’s presidential election with U.S. authorities demanding a fine of up to $14 billion for mis-selling mortgage-backed securities. The threat of such a large fine has pushed Deutsche shares to record lows, and a cut-price settlement is urgently needed to reverse the trend and help to restore confidence in Germany’s largest lender. Its shares won’t trade in Germany on Monday because of a public holiday, but they will resume trading on the U.S. market later on Monday. A media report late on Friday that Deutsche and the U.S. Department of Justice were close to agreeing on a settlement of $5.4 billion lifted the stock 6% higher, but that report has not been confirmed.

The Wall Street Journal reported on Sunday that the bank’s talks with the DOJ were continuing. Details are in flux, with no deal yet presented to senior decision makers for approval on either side, the paper said, citing people familiar with the matter. “Clearly, so long as a fine of this order of magnitude ($14 billion) is an even remote possibility, markets worry,” UniCredit Chief Economist Erik F. Nielsen wrote in a note on Sunday. Ratings agency Moody’s said it would be positive for bondholders if the lender could settle for around $3.1 billion, while a fine as high as $5.7 billion would dent 2016 profitability but not significantly impair the bank’s capital position.

[..] The Bild am Sonntag newspaper wrote on Sunday that Deutsche’s chairman had informed Berlin just before it disclosed the potential $14 billion fine but had not asked for help. The same newspaper quoted the president of the Bavarian Finance Centre, Wolfgang Gerke, as saying that the German government should step in and buy a 20% stake in the bank before its value fell any further. The group represents financial services companies in the southern German state. “Fundamentally, I’m against state interventions,” he told the newspaper, but added that in this case a government stake would be “a signal that could turn the whole market”.

Making Merkel’s day, no doubt. It wasn’t nearly hard enough for her yet.

• German Economy Minister Accuses Deutsche Bank Of Hypocrisy (Pol.)

Germany’s economy minister has highlighted the irony of Deutsche Bank blaming speculators for its falling share price when the bank itself has built its business on speculation. “I did not know if I should laugh or get angry that the bank that made speculation a business model is now saying it is a victim of speculators,” Sigmar Gabriel told journalists on a plane to Tehran on Sunday, Der Spiegel reported. The threat of a $14 billion fine by U.S. authorities over the sales of mortgage-backed securities before the financial crisis sent Deutsche Bank’s shares to new lows this month. Gabriel was responding to a letter sent by Deutsche Bank CEO John Cryan to staff Friday blaming “new rumors” for causing the plunge in share prices and saying “forces” wanted to weaken trust in Germany’s largest bank.

“US banks won’t be nearly as badly hit by the measure as their European counterparts, which is no doubt why their regulators are gunning so hard for it.”

• It’s Not Just Deutsche. European Banking is Utterly Broken (Tel.)

[..] as is evident from the events of the last week, the banking crisis itself is far from over. Nine years after the initial eruption, it still rumbles on, with the epicentre now moved from the US to Europe. Only it’s not the same crisis; in large measure, it is completely different. Today’s mayhem is not so much the result of reckless bankers and asleep at the wheel regulators, but rather of the public policy response to the last crisis itself – that is to say, regulatory over-reach and central bank money printing. All eyes are naturally focused on the specific problems of Deutsche Bank, but Deutsche is in truth no more than the canary in the coal mine. As Tidjane Thiam, chief executive of Credit Suisse, observed last week, as an entire sector, European banks are still “not really investable”.

Much the same disease as afflicts Continental banks also applies to British counterparts, including RBS, Barclays and even Lloyds. All are fast being enveloped by a perfect storm of negatives, and this time around, it is substantially the policymakers and law enforcers who are to blame. There are essentially four factors at work here. First, it’s virtually impossible to make money out of banking in a zero interest rate environment, frustrating attempts to rebuild capital buffers after the bad debt write-downs of recent years. In circumstances where central banks have bought right along the yield curve, flattening it down to virtually nothing, the margin from maturity transformation all but disappears. Much the same thing has happened to the once lucrative returns of investment banking.

Even Goldman Sachs has been forced to admit that it is struggling to cover its cost of capital. Second is ever tougher international capital requirements, the latest instalment of which is dubbed Basel IV. The renewed crackdown is understandable, given what occurred nine years ago, but also ill-conceived and discriminatory, unfairly penalising European banks against their American counterparts. The technical details need not concern us too much here, suffice it to say that in order to stop banks gaming the system, regulators are attempting to impose a so-called “output floor”, tightly limiting the scope for easier capital requirements on risk weighted assets. US banks won’t be nearly as badly hit by the measure as their European counterparts, which is no doubt why their regulators are gunning so hard for it.

That is so convenient for Abe…

• Kuroda Blamed For Abenomics Failure, Ruins Chance Of Second Term (BBG)

Governor Haruhiko Kuroda has ruined his chances of getting a second full term, according to Nobuyuki Nakahara, who has advised the prime minister on the economy and was an intellectual father of the Bank of Japan’s first run at quantitative easing in 2001. The central bank’s switch to yield-curve targeting compounds its earlier error of adopting negative interest rates and is a disappointing move away from monetary-base expansion, Nakahara, 81, said in an interview on Sept. 30. In a stinging attack on the BOJ’s recent actions, he said the decision to conduct a comprehensive review of monetary policy had invited defeat on reflationist efforts and would raise questions about Abenomics as a whole.

Prime Minister Shinzo Abe’s economic program consists of three so-called arrows: the first being aggressive monetary policy, the second fiscal spending and the third structural reform. The central bank’s program, which began when Abe tapped Kuroda for the BOJ role in early 2013, has been the most prominent and highly debated aspect of Abenomics. “They are trying to clean up the mess of negative rates. It’s impossible to do a stupid thing like keeping the yield curve under government control,” said Nakahara. “They changed the regime to rates from quantity, meaning those who support quantitative easing were defeated. Reflationists on the BOJ policy board lost. An exit from deflation is going to be far away.”

After being greeted with fanfare when he took the helm, Kuroda, 71, now faces a reversal of fortunes on multiple fronts. Markets have moved against him and critics are growing more vocal. The extended honeymoon he enjoyed with a rising stock market and falling yen are long gone and his 2% inflation goal is nowhere in sight. Kuroda has less than 19 months to go in his term. While no BOJ governor has been tapped for a second five-year term since the 1960s, Kuroda’s central role in Abenomics has led to speculation that he may be different.

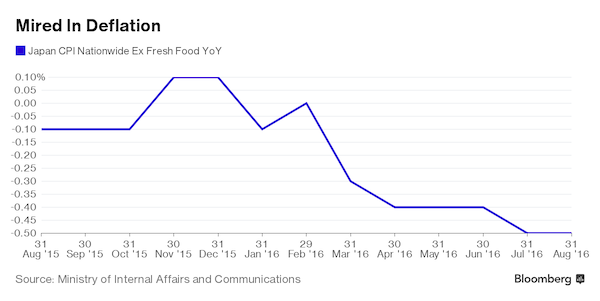

If you don’t know what deflation is, you can’t fight it.

• BOJ Deploys US World War II Tactics That Failed to Spur Prices (BBG)

In deciding to target bond yields, Japan is deploying a monetary strategy to combat deflation used by its former enemy in World War II. The trouble is that America’s experience back then suggests that the tactics probably won’t work on their own. Economists who have studied that period say that it was increased government spending, along with heightened inflation expectations, that eventually led to a stepped-up pace of U.S. price increases more than a half century ago. Once inflation was humming along, the Federal Reserve’s strategy of pegging long-term interest rates did nothing to put a lid on it, which is why the central bank pushed for a 1951 agreement with the Treasury to abandon the long-term yield fix.

If inflation expectations are contained, simply targeting yields won’t necessarily spur price pressures, according to Barry Eichengreen, a professor at the University of California at Berkeley who co-wrote a paper on U.S. monetary and financial policy from 1945 to 1951. But if people already expect faster inflation, then the tool can help promote it. That’s not a helpful conclusion for Bank of Japan Governor Haruhiko Kuroda and his colleagues, who last month switched the focus of their monetary stimulus to controlling yields across a range of maturities, after simply expanding the monetary base through debt purchases. It set the target for the yield on the 10-year Japanese government bond at around 0%.

Another piece of their new framework: trying to shock inflation expectations higher by pledging to keep stimulus in place until prices are rising even faster than their 2% target. Their struggle is to overturn subdued household and corporate expectations that have been set hard by decades of deflation. For the Fed in World War II and its aftermath, capping long-term yields at 2.5% had nothing to do with inflation per se. Its goal was to limit the government’s borrowing costs and so support the war effort. Inflation was held down by price controls during the war, then spiked higher after hostilities ended, hitting a high of 19.7% in 1947. The surge proved short-lived, as an economic recession that began late the following year produced a return of the deflation that had plagued the country during the Great Depression.

And if successful, they’re all going to do it? Oops, too late.

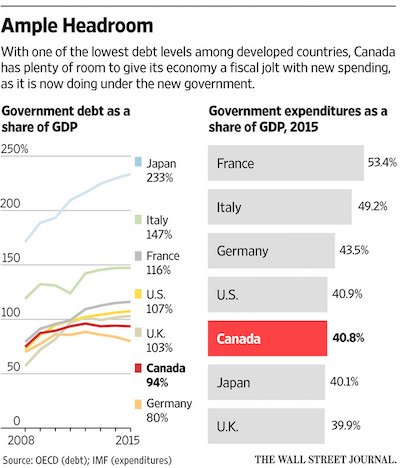

• Canada’s Big Bet on Stimulus Draws Global Attention (WSJ)

In the global struggle to boost growth, a Canadian experiment in fiscal spending is providing a test case for some of the world’s biggest economies. PM Justin Trudeau’s Liberal government unveiled a plan last spring to spend heavily on tax benefits and infrastructure, with $120 billion CAD (US$91.39 billion) going into infrastructure over the next decade, including about one-tenth of that on short-term projects. It’s a bold bet to inject life into an economy struggling with a rout in commodity prices, especially crude oil, which was once Canada’s top export. It also highlights the limits of monetary stimulus, since the country’s central bank cut rates twice in 2015, to 0.5%, and has acknowledged—as its counterparts around the world have—that monetary policy becomes a less powerful tool when interest rates are already low.

Mr. Trudeau’s big infrastructure spend will be largely financed by a bigger deficit, which is projected to reach C$29.4 billion this fiscal year, or about 1.5% of GDP. That’s a sharp turn from the balanced-budget promise of his Conservative predecessor, who hewed the austerity path Mr. Trudeau is now shunning. Canada’s efforts stand in contrast to many of the world’s economies, whose finance ministers and central bankers meet this week in Washington for semiannual meetings of the International Monetary Fund and World Bank. Some—like Australia, also hit by the commodity rout—are trying to use coordinated fiscal and monetary policy. But larger advanced economies are holding firm to tight budgets, making Canada’s embrace of debt-fueled stimulus unusual.

“The eyes of the world—the economists—will be watching to see how Canada performs,” said Martin Eichenbaum, a Northwestern University economist who is also an international fellow at the C.D. Howe Institute, a Canadian think tank. “We’re all watching to see: Will they get it right?”

Yeah. Not going to happen….

• Jail Wells Fargo CEO and Chairman John Stumpf! (Nomi Prins)

Consider this. You’re a mob boss. You run a $1.8 trillion network of businesses across state lines and continents. Many of these are legit, but a select subset of them – not so much. Every so often the illegal components flare up; some Washington commission launches an investigation, someone blows a whistle, people lose their homes, a pack of investors sheds a ton of money and lawsuits fly. You get reprimanded and have to pay lawyers and accountants overtime to deal with the paperwork. You settle on fines with the government — $10 billion worth. Then you keep going with no one the wiser, no wings clipped, no hard time. After all of that — you say you’re sorry, forfeit some money you didn’t even make yet, and (maybe) resign with boatloads more of it.

This is what we’re dealing with regarding Wells Fargo CEO and Chairman John Stumpf. He could be a really nice guy and wears some lovely tailored attire. (Hell, even Al Capone cared about proper milk expiration date labels.) But he’s also a crook, plain and simple. He’s cheated shareholders and taxpayers and customers, and used a stockpile of FDIC-backed deposits as fodder for illicit activities that have been repeatedly investigated and fined. And he made hundreds of millions of dollars doing it. This is not conjecture, nor sour grapes from the nonmillionaire swath of the population. It’s based on documented facts. But by no means is Wells the only guilty bank on the street, or Stumpf the only “apologetic” CEO. Apologies are cheap, and so is money when it’s a small piece of a much larger pie.

Somewhere, Jamie Dimon and Lloyd Blankfein are sighing in relief that this time it was Stumpf and not one of them, the other two of the three (of the Big Six bank) CEOs left standing since the crisis. These are just some highlights of those nearly $10 billion in total fines Wells agreed to, rather than take matters to court, since 2009. The sheer sum of those fines reveal a recidivist attitude toward ethics, regulations and the law. The associated transgressions were all committed under Stumpf’s leadership. There’s no way a regular citizen committing a fraction of a fraction of anything like these wouldn’t be in jail. Complexity is no excuse for criminal behavior. Nor is calling these practices “abuses” rather than felony fraud for misleading, at the very least, investors and shareholders in a publicly traded mega-company that violates securities laws.

… but if not the Wells Fargo CEO, at least some people will go to jail…

• The Government Is Turning the Entire United States into a Debtors Prison (TAM)

Since the United States was founded, citizenship has represented a safe haven from oppressive regimes around the world. By preserving the principles of small government and free markets, those who were willing to work hard found success, and America became a magnet for innovation. But as the U.S. continues to erode personal and economic freedom, more people than ever before are handing over their U.S. passports to seek better opportunities abroad. The staggering amount of debt held by the American empire ensures the public will be working it off for generations to come. The government has already begun its campaign to make it more difficult to leave the country, and it has also begun to crack down on the finances of the eight million Americans living abroad.

Regardless of whether you’re a millionaire with multiple foreign bank accounts or a recent college graduate with a boatload of debt, the status of being a United States citizen brings with it a burden that will only grow heavier over time. Since 2008, the number of individuals giving up their citizenship has increased by almost 560%, setting new records each of the past three years. Some of these expats are motivated by the extra tax load paid when working abroad, while others are trying to avoid student loan debt. Others have just had enough of the encroaching police state. Every taxpayer left in the country now owes more than $149,000 of the national debt, so it’s no surprise the tide is beginning to turn. By hook or by crook, in the coming years, citizens will be fleeced of that money through higher taxes, savings that are inflated away, and an overall drop in their standard of living.

Many can see the writing on the wall and have become determined to protect themselves from the years of economic repression coming down the pipe. Draconian steps have already been taken to slow the rate of expatriation. For one, the IRS has broadened its reach into foreign bank accounts through the Foreign Account Tax Compliance Act. Through agreements with over 100 nations, the law is able to require all financial institutions abroad to report the account details of any American customers they have. With access to this new information, the IRS can revoke the passports of potential tax evaders and hinder their ability to travel using yet another additional power the agency was granted last year.

The gift that keeps on contaminating.

• Fukushima Has Contaminated The Entire Pacific Ocean, Going To Get Worse (TA)

What was the most dangerous nuclear disaster in world history? Most people would say the Chernobyl nuclear disaster in Ukraine, but they’d be wrong. In 2011, an earthquake, believed to be an aftershock of the 2010 earthquake in Chile, created a tsunami that caused a meltdown at the TEPCO nuclear power plant in Fukushima, Japan. Three nuclear reactors melted down and what happened next was the largest release of radiation into the water in the history of the world. Over the next three months, radioactive chemicals, some in even greater quantities than Chernobyl, leaked into the Pacific Ocean. However, the numbers may actually be much higher as Japanese official estimates have been proven by several scientists to be flawed in recent years.

If that weren’t bad enough, Fukushima continues to leak an astounding 300 tons of radioactive waste into the Pacific Ocean every day. It will continue do so indefinitely as the source of the leak cannot be sealed as it is inaccessible to both humans and robots due to extremely high temperatures. It should come as no surprise, then, that Fukushima has contaminated the entire Pacific Ocean in just five years. This could easily be the worst environmental disaster in human history and it is almost never talked about by politicians, establishment scientists, or the news. It is interesting to note that TEPCO is a subsidiary partner with General Electric (also known as GE), one of the largest companies in the world, which has considerable control over numerous news corporations and politicians alike.

Could this possibly explain the lack of news coverage Fukushima has received in the last five years? There is also evidence that GE knew about the poor condition of the Fukushima reactors for decades and did nothing. This led 1,400 Japanese citizens to sue GE for their role in the Fukushima nuclear disaster. Even if we can’t see the radiation itself, some parts of North America’s western coast have been feeling the effects for years. Not long after Fukushima, fish in Canada began bleeding from their gills, mouths, and eyeballs. This “disease” has been ignored by the government and has decimated native fish populations, including the North Pacific herring. Elsewhere in Western Canada, independent scientists have measured a 300% increase in the level of radiation.

It won’t stop Orban.

• Hungary’s Refugee Referendum Not Valid After Voters Stay Away (G.)

The Hungarian prime minister, Viktor Orbán, has failed to convince a majority of his population to vote in a referendum on closing the door to refugees, rendering the result invalid and undermining his campaign for a cultural counter-revolution within the European Union. More than 98% of participants in Sunday’s referendum sided with Orbán by voting against the admission of refugees to Hungary, allowing him to claim an “outstanding” victory. But more than half of the electorate stayed at home, rendering the process constitutionally null and void.

Orbán himself put a positive spin on the low turnout. He argued that while “a valid [referendum] is always better than an invalid [referendum]” the extremely high proportion of no-voters still gave him a mandate to go to Brussels next week “to ensure that we should not be forced to accept in Hungary people we don’t want to live with”. He argued that the poll would encourage a wave of similar votes across the EU. “We are proud that we are the first,” he said.

NOTE: Less than 2 weeks ago, the EU refused Greece permission to move the refugees to the mainland, because they might try to travel north.

“Athens will be overwhelmed, [as will] the mainland, people will be forced to live in fields, there will be scenes we’ll never have imagined.”

• Vulnerable Refugees To Be Moved From ‘Squalid’ Camps On Greek Islands (G.)

Greece is poised to transfer thousands of refugees from overcrowded camps on its Aegean islands to the mainland amid escalating tensions in the facilities and protests from irate locals. The government said unaccompanied minors, the elderly and infirm would be among the first to be moved as concerns mounted over the future of a landmark EU-Turkey deal to stem migrant flows. “The situation on the islands is difficult and needs to be relieved,” said deputy minister for European affairs Nikos Xydakis. “Accommodation on the mainland will be more suitable. We will start with transfers of those who are most vulnerable, always in the sphere of implementing and protecting the EU-Turkey agreement.”

The operation, expected to be put into motion this week, came as Ankara warned the pact would not hold if Brussels failed to honour its pledge to allow Turks visa-free travel to the bloc. In a fiery speech before the newly reconvened parliament at the weekend, Turkish president Erdogan gave his clearest signal yet that the six-month-old agreement was in danger of collapse because of slow progress over visa liberalisation. [..] Refugee flows, although rising again, have dropped by 90% since the deal was signed. [..] Western diplomats in the Greek capital raised the spectre of chaos if the agreement collapsed. “If it does, there will be an influx of a million or more and this country is totally unprepared,” one European ambassador confided. “Athens will be overwhelmed, [as will] the mainland, people will be forced to live in fields, there will be scenes we’ll never have imagined.”

[..] Acknowledging that camp conditions were far from ideal, Xydakis blamed the backlog in asylum applications on the EU’s failure to dispatch promised staff and push ahead with an agreed relocation scheme to other parts of the continent. “We were promised 400 experts in asylum procedures but so far only have around 29 on the islands. We are continuing to recruit and look for more staff but it is not easy,” he said. “The deal is not only in the hands of Turkey but Europe … some EU states are not respecting but neglecting their responsibilities.”

To reiterate what I said yesterday on this topic:

“It was Germany that last year declared Dublin null and void. They will say that was only temporaray, but regulations like this are not light switches that selected parties can flick on and off when it suits them.

What happens now is quite simply that both the refugees and Greece are the victims of Angela Merkel’s falling poll numbers. And that is insane. It’s cattle trade. Athens should take Berlin to court over this.

Greece is already little more than a greatly impoverished holding pen for the unwanted, and it threatens to fall much deeper into the trap. That’s why the Automatic Earth effort to support the poorest people is not just still needed, but more now than ever. We will soon start a new campaign to that end. In the meantime, please do continue to donate through our Paypal widget in amounts ending in $.99 or $.37.”

• Germany Wants Migrants Sent Back To Greece, Turkey (AFP)

Germany called Sunday for asylum seekers who entered the European Union via Greece to be forced to return there, while also urging Athens to send more migrants back to Turkey. In an interview with a Greek daily, German interior minister Thomas de Maiziere said he wants to reinstate EU rules which oblige asylum seekers to be sent back to Greece as the first EU country they reached. “I would like the Dublin convention to be applied again… we will take up discussions on this in a meeting with (EU) interior ministers” later in October, he told the Greek daily Kathimerini. The Dublin accord gives responsibility for asylum seekers’ application to the first country they reach – which put Greece on the frontline of more than a million migrants who arrived in the EU last year.

The accord also says asylum seekers should be sent back to the first country they arrived in if they subsequently reach another EU state before their case is examined. A huge proportion of the migrants ended up in Germany. But this clause was suspended for Greece in 2011 after the country lost an EU legal complaint which condemned the mistreatment of migrants seeking international protection. “Since then, the EU has provided substantial support, not only financially,” to Greece to improve its asylum seeker procedures, the German minister said. In an interview on German television Sunday evening, De Maiziere also criticised Athens for failing to fully implement an EU agreement with Turkey to return migrants there.

The EU reached a deal with Turkey in March to stop the influx to the Greek islands in return for financial aid and eased visa conditions for its citizens. But the deal has looked shaky in the wake of a coup attempt in Turkey in July. “Greece must carry out more expulsions,” he told the ARD television station.