Photograph: Palani Mohan/Getty Images

I’m sorry, I’m trying, but I just can’t NOT find this funny. My article earlier today: He’s Just Not That Into You.

• Anxious European Leaders Seek An Early Audience With Trump, Before Putin (AP)

European leaders, anxious over Donald Trump’s unpredictability and kind words for the Kremlin, are scrambling to get face time with the new American president before he can meet with Russian President Vladimir Putin, whose provocations have set the continent on edge. One leader has raised with Trump the prospect of a U.S.-EU summit early this year, and the head of NATO — the powerful military alliance Trump has deemed “obsolete” – is angling for an in-person meeting ahead of Putin as well. British Prime Minister Theresa May is working to arrange a meeting in Washington soon after Friday’s inauguration. For European leaders, a meeting with a new American president is always a sought-after – and usually easy-to-obtain – invitation.

But Trump has repeatedly defied precedent, making them deeply uncertain about their standing once he takes office. Throughout his campaign and in recent interviews, Trump has challenged the viability of the EU and NATO, while praising Putin and staking out positions more in line with Moscow than Brussels. “There are efforts on the side of the Europeans to arrange a meeting with Trump as quickly as possible,” Norbert Roettgen, the head of the German Parliament’s foreign committee and a member of Chancellor Angela Merkel’s party, told AP. In fact, eager to stage an early show of Trans-Atlantic solidarity, Donald Tusk – the former Polish prime minister who heads the EU’s Council of member state governments – invited Trump to meet with the EU early in his administration, according to a EU official.

But a senior Trump adviser essentially rebuffed the offer, telling the AP this week that such a gathering would not be a priority for the incoming president, who wants to focus on meetings with individual countries, not the 28-nation bloc. Trump backs Britain’s exit from the EU, casting the populist, anti-establishment movement as a precursor to his own victory. In a recent joint interview with two European newspapers, Trump said of the EU, “I don’t think it matters much for the United States.” Such rhetoric alone was enough to set off alarm bells in Europe. And Trump’s praise for Putin and promise of closer ties to Moscow have deepened the uncertainty.

“..he was sure no EU state wanted to follow Britain’s example and leave the bloc..”

• Hands off EU, Trump; We Don’t Back Ohio Secession: Juncker (R.)

Donald Trump should lay off talking about the break-up of the European Union, the bloc’s chief executive said on Wednesday, pointing out that Europeans do not push for Ohio to secede from the United States. In pointed remarks on the eve of Trump’s inauguration as U.S. president, Jean-Claude Juncker said the new administration would realize it should not damage transatlantic relations but added it remained unclear what policies Trump would now pursue. Juncker told Germany’s BR television, according to a transcript from the Munich station, that he was sure no EU state wanted to follow Britain’s example and leave the bloc, despite Trump’s forecast this week that others would quit:

“Mr. Trump should also not be indirectly encouraging them to do that,” Juncker said. “We don’t go around calling on Ohio to pull out of the United States.” Juncker, the president of the European Commission, said he had yet to speak to Trump — contrary to what the President-elect said earlier this week. Juncker said Trump had confused him with European Council President Donald Tusk. “Trump spoke to Mr. Tusk and mixed us up,” said Juncker, taking a jab at the American billionaire’s grasp of his new role. “That’s the thing about international politics,” he said. “It’s all in the detail.”

If even Jamie Dimon can understand it…

• Jamie Dimon Says Eurozone May Not Survive (BBG)

The euro region could break up if political leaders don’t get to grips with the discontent that’s spurring support for populist leaders across the continent, JPMorgan Chase CEO Jamie Dimon said. Dimon said he had hoped European Union leaders would examine what caused the U.K. to vote to leave and then make changes. That hasn’t happened, and if nationalist politicians including France’s Marine Le Pen rise to power in elections across the region “the euro zone may not survive,” Dimon, 60, said in a Bloomberg Television interview with John Micklethwait. “What went wrong is going wrong for everybody, not just going wrong for Britain, but in some ways it looks like they’re kind of doubling down,” Dimon said in the interview Wednesday at the annual meeting of the World Economic Forum in Davos.

Unless leaders address underlying concerns, “you’re going to have the same political things about immigration, the laws of the country, how much power goes to Brussels.” Dimon’s remarks on Europe were unusually pessimistic, coming in a wide-ranging interview in which he also criticized regulations that he said stunt economic growth. But he reiterated optimism for President-elect Donald Trump. Minutes later, Goldman Sachs CEO Lloyd Blankfein also expressed concern about Europe, telling CNBC that leaders are facing a backlash in the midst of a long, complicated process to create an economic bloc. “That’s complicated, that’s very hard to do,” said Blankfein. “It’s not done, and it’s not accomplished. We’re finding the pain of that.” [..] The bottom line is that Europe must become more competitive, Dimon said. “I say this out of respect for the European people, but they’re going to have to change,” he said. “They may be forced by politics, they may be forced by new leadership.”

Journalist Jean Quatremer is Mr. Europe. He’s been called an ‘ayatollah of European federalism’.

• In Europe We See Only One Loser From Brexit – And It Won’t Be Us (Quatremer)

When someone wants the impossible, in French we say that they want “the butter, the money from the butter, and the dairymaid’s smile”. In more vulgar usage we say they want something rather more from the dairymaid than a smile. This is precisely what we can take away from Theresa May’s speech on the “hard Brexit” she wants. It is “hard” only for the other 27 states but “soft” for Britain – because May wants to keep all the benefits of EU membership and concede nothing in return. That is not really a surprise since she had already announced it in October during the Conservative party conference. She even considers that any other kind of agreement would be unacceptable, because it would amount to “punishing” the British.

May is threatening to turn Britain into a tax haven by way of retaliation, if, by some misfortune, the Europeans refuse to bend to the demands of Her Glorious Majesty’s subjects. We might think we are dreaming, but no: it is either arrogance or recklessness (or, more likely, a mixture of the two). Let’s sum up: on the one hand, of course, May would like a clear, “clean break” with the union, which means no longer sitting in its institutions, contributing to the budget or respecting EU law. On the other hand, she does not want the status of some kind of “partial or associate” member, which would imply having to meet EU’s requirements in all kinds of areas.

Thus far, we get it: the UK will be treated like any other third country – Zimbabwe, for instance. That’s clear and “clean”. But after that it gets complicated, at least for a continental mind that lacks the subtleties of reflection of a product of Oxbridge. Because May considers it possible for British companies to retain the greatest possible access to the single market, in particular to negotiate sectoral customs agreements with the union. And that’s where things get interesting. Because customs duty or no, importing goods into a market presupposes compliance with local norms and standards: to be clear, if the British want to export their cars (which are in fact German or Japanese cars) to the continent, they need to respect European laws. That means submitting (I know, what an awful word) to those laws. So in reality, the clear, “clean break” could only concern one part of UK industry – the part that manufactures for the local market.

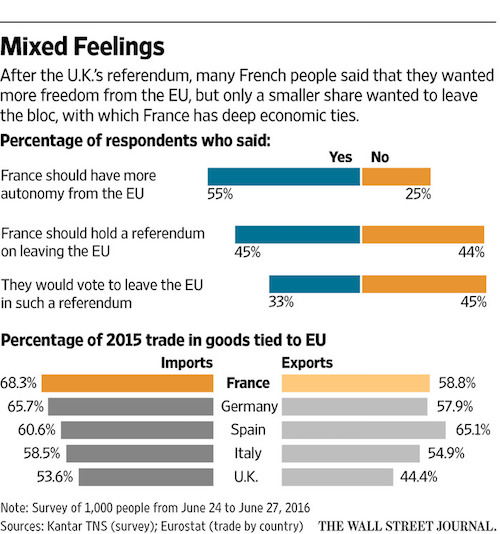

Le Pen is smartening up. She’s a true contender now.

• Marine Le Pen Centers Presidential Run on Getting France Out of Eurozone (WSJ)

National Front leader Marine Le Pen is seeking to turn May’s presidential election into a referendum on the European Union by detailing a strategy to pull France from the bloc and its single currency if she wins. She last ran in 2012 with an initial promise of a sharp and sudden break from the euro, but this time Ms. Le Pen has sought broader support from a splintered French electorate. She says she would organize an orderly exit rather than crashing out with unpredictable consequences. If elected, she and top National Front officials say, her administration will spend its first six months negotiating the creation, along with other disappointed euro nations, of a basket of shadow European currencies. A newly reinstated franc, she says, would eventually be pegged to that basket, replacing the euro.

Ms. Le Pen says other countries struggling to meet European rules would be willing to enter into talks on pulling the EU apart. The threat of having to leave the euro, she says, has been used to blackmail Greece and other Southern European countries into implementing austerity programs their people reject. “The euro has not been used as a currency, but as a weapon—a knife stuck in the ribs of a country to force it to go where the people don’t want to go,” Ms. Le Pen said this month. “Do you think we accept living under this threat, this tutelage? It’s absolutely out of the question.”

[..] An attempt by France, the eurozone’s second-largest economy, to pull out would be far more challenging than Brexit, which doesn’t touch on currency questions. A “Frexit” would likely unleash chaos across the currency union and undermine the broader EU in a way Britain’s departure wouldn’t. No country has attempted to leave the euro, and French polls show that while people want to claw back control from Brussels, a majority wouldn’t vote to leave the currency. The complications of an exit weren’t as clear to Ms. Le Pen in 2012, when she garnered only 17.9% of the presidential vote with her push for a clean break with the euro. “We set off on the idea in 2012 of an immediate exit, slamming the door,” said Jean-Richard Sulzer, a senior economic adviser to Ms. Le Pen. “Things were said too quickly, but this time Marine is much more prudent.”

Yeah, why not blame Trump for that too.

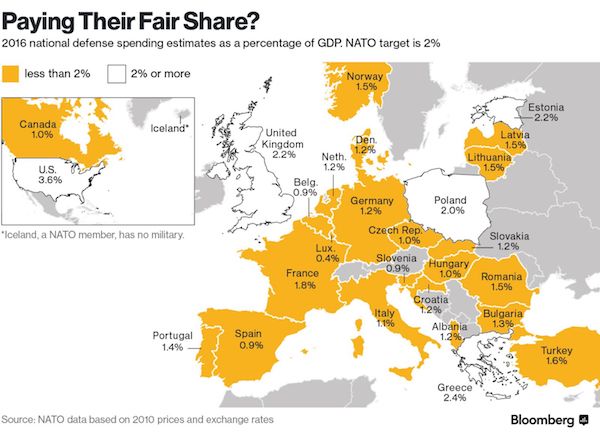

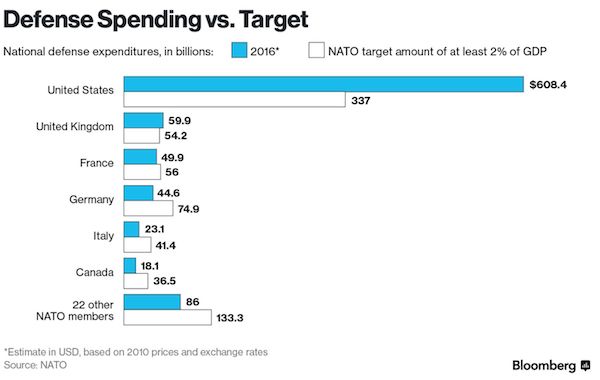

• By Ripping NATO, Trump Makes Europe Nervous and Arms Trade Happy (BBG)

Donald Trump is right to say America’s NATO allies aren’t paying their fair share. But, to the delight of the arms industry, that may be changing. Trump himself is the change-maker. He reaffirmed his skepticism about the North Atlantic Treaty Organization, and his readiness to make deals with Russia, in European media interviews published last weekend. Trump isn’t famous for his policy consistency, but those positions have held fairly steady – leaving European leaders wondering whether they can still rely on the American security umbrella. “Let’s not fool ourselves,” German Chancellor Angela Merkel said last week. “There is no infinite guarantee.”

So Merkel’s Germany, and many other European nations, are boosting military budgets. The plans predate Trump, and under NATO rules they should’ve been carried out long ago. The alliance expects its members to spend 2% of GDP on defense. But it’s no secret that most of them don’t. The shortfall added up to about $121 billion last year at 2010 prices, according to Bloomberg calculations based on NATO country estimates.

Since Trump is promising to increase America’s already enormous military budget too, the prospect of a European arms-shopping spree is a win-win for suppliers. Investors have noticed: From Raytheon to Lockheed Martin to Thales, defense contractors have hit all-time highs since Trump’s election. “This is the best market for defense in many years, across the board,” said Richard Aboulafia, an aerospace analyst with the Teal Group in Fairfax, Virginia. NATO was established after World War II to protect western democracies against the Soviet Union. A key tenet is that an attack on any alliance member is considered an attack on all. And that’s what Trump has questioned. If Russia moved against one of NATO’s Baltic members, Trump told the New York Times in July, he’d come to their aid only after reviewing whether they have “fulfilled their obligations to us.”

Brilliant! Please don’t miss this!

It’s just that I thought Steve made his own Melania doll (no kidding.) And then she started talking.

• Steve Keen Exposes Next Global Economic Shockwaves (FinFeed)

Steve, who is Trump going to be pouring drinks for, as in economic growth and benefits, in 2017?

Steve Keen: He is trying to pour it just for his own economy. And this is going to be the dramatic challenge he faces. Because he is someone who actually knows a lot about money and banks and debt, having used it extensively in his own professional career.

Lelde Smits: And succeeded and failed and hopefully learnt from the failures.

Steve Keen: He’s turned failure into success in many, many ways, and let’s not go there in terms of how beneficial that was for his various suppliers but he understands going bankrupt, he understand re-organisation, he understands finance.

Lelde Smits: So where is this liquid in 2017?

Steve Keen: He’s going to realise at some point he owns his own bank now. Because he’s running the country he is going to spend.

Lelde Smits: So we have the Federal Reserve right?

Steve Keen: The Federal Reserve is there and can top him up as much as it likes.

Lelde Smits: So when does this stop Steve? That’s the magic question.

Steve Keen: It never has to stop. He’s going to enable the American economy to spend dramatically. Taxation is going to be cut. There will be an increase in government spending. There will be a large deficit coming out of that. So the government is going to be creating a lot of money and running a lot of infrastructure projects and so on. There are 4 million Americans who aren’t employed now who were employed in 2000. They are people who are going to get jobs in construction and start spending domestically and so on. And Trump is going to see that as boosting up the American economy. It’s all about Buy America, Made in America and so on.

How different do we think this is from what happened with Goldman and Greece? How to hide losses 101.

• How Deutsche Bank Made €367 Million Disappear at Monte dei Paschi (BBG)

On Dec. 1, 2008, most of the world’s banks were still panicking through the financial crisis. Lehman Brothers had collapsed. Merrill Lynch had been sold. Citigroup and others had required multibillion-dollar bailouts to survive. But not every institution appeared to be in free fall. That afternoon, at the London outpost of Deutsche Bank, the stolid-seeming, €2 trillion German powerhouse, a group of financiers met to consider a proposal from a team led by a trim, 40-year-old banker named Michele Faissola. The scion of an Italian banking family, Faissola was the head of Deutsche’s global rates unit, a division that created and sold financial instruments tied to interest rates. He’d been studying the problems of one of Deutsche’s clients, Italy’s Banca Monte dei Paschi di Siena, which, as the crisis raged, was down €367 million ($462 million at the time) on a single investment.

Losing that much money was bad; having to include it in the bank’s yearend report to the public, as required by Italian law, was arguably much worse. Monte dei Paschi was the world’s oldest bank. It had been operating since 1472 [..] . If investors were to find out the extent of its losses in the 2008 credit crisis, the consequences would be unpredictable and grave: a run on the bank, a government takeover, or worse. At the Deutsche meeting, Faissola’s team said it had come up with a miraculous solution: a new trade that would make Paschi’s loss disappear. The bankers in the room had seen some financial sleight of hand in their day, but the maneuver that Faissola’s staffers proposed was audacious.

They described a simple trade in two parts. For one half of the deal, Paschi would make a sure-thing, moneymaking bet with Deutsche Bank and use those winnings to extinguish its 2008 trading losses. Of course, Deutsche doesn’t give away money for free, so for the second half of the deal, the Italians would make a bet that was sure to lose. But while the first transaction was immediate, the second would play out slowly, over many years. No sign of the €367 million sinkhole would need to show up when Paschi compiled its yearend financial reports.

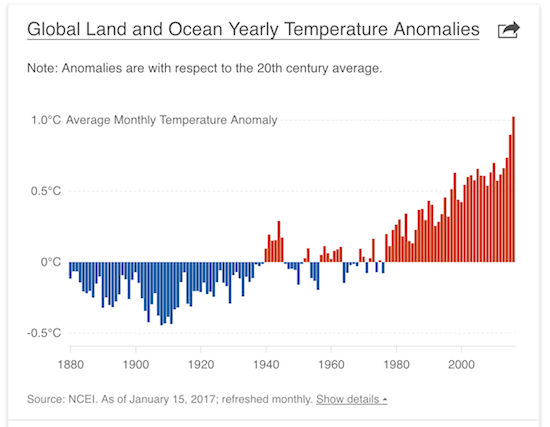

New records set in 2005, 2010, 2014, 2015 and 2016.

• Earth Breaks Heat Record In 2016 For Third Year In A Row (AFP)

Last year, the Earth sweltered under the hottest temperatures in modern times for the third year in a row, US scientists said Wednesday, raising new concerns about the quickening pace of climate change. Temperatures spiked to new national highs in parts of India, Kuwait and Iran, while sea ice melted faster than ever in the fragile Arctic, said the report by the National Oceanic and Atmospheric Administration. Taking a global average of the land and sea surface temperatures for the entire year, NOAA found the data for “2016 was the highest since record keeping began in 1880,” said the announcement. The global average temperature last year was 1.69 Fahrenheit (0.94 Celsius) above the 20th century average, and 0.07 degrees F (0.04 C) warmer than in 2015, the last record-setting year, according to NOAA.

This was “not a huge margin to set a new record but it is larger than the typical margin,” Deke Arndt, chief of NOAA global climate monitoring, said on a conference call with reporters. A separate analysis by the US space agency NASA also found that 2016 was the hottest on record. The World Meteorological Organization in Geneva confirmed the US findings, and noted that atmospheric concentrations of both carbon dioxide and methane reached new highs. The main reason for the rise is the burning of fossil fuels like oil and gas, which send carbon dioxide, methane and other pollutants known as greenhouse gasses into the atmosphere and warm the planet. The mounting toll of industrialization on the Earth’s natural balance is increasingly apparent in the record books of recent decades. “Since the start of the 21st century, the annual global temperature record has been broken five times (2005, 2010, 2014, 2015 and 2016),” said NOAA.

Denial is a river in the Arctic.

• ‘A Cat In Hell’s Chance’ (Simms)

What’s so special about 2C? The simple answer is that it is a target that could be politically agreed on the international stage. It was first suggested in 1975 by the environmental economist William Nordhaus as an upper threshold beyond which we would arrive at a climate unrecognisable to humans. In 1990, the Stockholm Environment Institute recommended 2C as the maximum that should be tolerated, but noted: “Temperature increases beyond 1C may elicit rapid, unpredictable and non-linear responses that could lead to extensive ecosystem damage.” To date, temperatures have risen by almost 1C since 1880. The effects of this warming are already being observed in melting ice, ocean levels rising, worse heat waves and other extreme weather events.

There are negative impacts on farming, the disruption of plant and animal species on land and in the sea, extinctions, the disturbance of water supplies and food production and increased vulnerability, especially among people in poverty in low-income countries. But effects are global. So 2C was never seen as necessarily safe, just a guardrail between dangerous and very dangerous change. To get a sense of what a 2C shift can do, just look in Earth’s rear-view mirror. When the planet was 2C colder than during the industrial revolution, we were in the grip of an ice age and a mile-thick North American ice sheet reached as far south as New York. The same warming again will intensify and accelerate human-driven changes already under way and has been described by James Hansen, one of the first scientists to call global attention to climate change, as a “prescription for long-term disaster”, including an ice-free Arctic.

Nevertheless, in 1996, a European Council of environment ministers, that included a young Angela Merkel, adopted 2C as a target for the EU. International negotiators agreed the same in 2010 in Cancun. It was a commitment repeated in the Paris Climate Accord of 2015 where, pushed by a new group of countries called the Climate Vulnerable Forum, ambitions went one step further, agreeing to hold temperature rises to “well below 2C above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5C”.

I don’t know how much longer I can witness this. At what point do we set up a private army?

“The industries at work in tropical forest areas are expected to be served by an extra 25 million km of roads by 2050..”

• Over Half of World’s Wild Primate Species Face Extinction (G.)

Top row l-r: brown-headed spider monkey, chimpanzee, Western gorilla; Bottom row l-r: Bornean orangutan, Siau Island tarsier, ring-tailed lemur. Composite: Alamy and Getty Images

More than half of the world’s apes, monkeys, lemurs and lorises are now threatened with extinction as agriculture and industrial activities destroy forest habitats and the animals’ populations are hit by hunting and trade. In the most bleak assessment of primates to date, conservationists found that 60% of the wild species are on course to die out, with three quarters already in steady decline. The report casts doubt on the future of about 300 primate species, including gorillas, chimps, gibbons, marmosets, tarsiers, lemurs and lorises. Anthony Rylands, a senior research scientist at Conservation International who helped to compile the report, said he was “horrified” at the grim picture revealed in the review which drew on the International Union for the Conservation of Nature (IUCN) red list, peer-reviewed science reports and UN databases.

“The scale of this is massive,” Rylands told the Guardian. “Considering the large number of species currently threatened and experiencing population declines, the world will soon be facing a major extinction event if effective action is not implemented immediately,” he writes in the journal Science Advances, with colleagues at the University of Illinois and the National Autonomous University of Mexico. The most dramatic impact on primates has come from agricultural growth. From 1990 to 2010 it has claimed 1.5 million square kilometres of primate habitats, an area three times the size of France. In Sumatra and Borneo, the destruction of forests for oil palm plantations has driven severe declines in orangutan populations. In China, the expansion of rubber plantations has led to the near extinction of the northern white-cheeked crested gibbon and the Hainan gibbon, of which only about 30 or animals survive.

More rubber plantations in India have hit the Bengal slow loris, the western hoolock gibbon and Phayre’s leaf monkey. Primates are spread throughout 90 countries, but two thirds of the species live in just four: Brazil, Madagascar, Indonesia and the Democratic Republic of the Congo (DRC). In Madagascar, 87% of primate species face extinction, along with 73% in Asia, the report states. It adds that humans have “one last opportunity” to reduce or remove the threats facing the animals, to build conservation efforts, and raise worldwide awareness of their predicament. The market for tropical timber has driven up industrial logging and damaged forest areas in Asia, Africa and the neotropics. Mining for minerals and diamonds have also taken a toll. On Dinagat island in the Philippines, gold, nickel and copper mining endanger the Philippine tarsier. In the DRC, hunters working around the tin, gold and diamond mine industry are the greatest threat to the region’s Grauer’s gorilla. The industries at work in tropical forest areas are expected to be served by an extra 25 million km of roads by 2050, further fragmenting the primates’ habitats.

If you were an elephant … You would still feel love, hurt and grief.

“Perhaps one of the reasons we’re so keen to deny non-human creatures minds, consciousness and personhood is that, if they’re people, they’re embarrassingly better people than we are. They build better communities; they live at peace with themselves and aren’t, unlike us, actively psychopathic towards other species. ”

• If you were an elephant … (Foster)

If you were an elephant living wild in a western city, you’d be confused and disgusted. You’d have one two-fingered hand swinging from your face – a hand as sensitive as tumescent genitals, but which could smash a wall or pick a cherry. With that hand you’d explore your best friends’ mouths, just for the sake of friendship. With that hand you’d smell water miles away and the flowers at your feet. You’d sift it all, triaging. Category 1: immediate danger. Category 2: potential threat. Category 3: food and water. Category 4: weather forecasts – short and long range. Category 5: pleasure. Grumbles from trucks and cabs would shudder through the toxic ground, tickle the lamellar corpuscles in your feet and ricochet up your bones. You’d hear with your feet, and your femurs would be microphones.

As you walked 10 miles for your breakfast you’d chatter with your friends in 10 octaves. A nearby human would throb like a bodhran as subsonic waves bounced around her chest. Even if it swayed with grass instead of being covered in concrete and dog shit, the city would be far, far too small for you. You’d feel the ring roads like a corset. You’d smell succulent fields outside, and be wistful. But you’d make the most of what you had. You’d follow a labyrinth of old roads, relying on the wisdom of long-dead elephants, now passed down to your matriarch. You’d have the happiest kind of political system, run by wise old women, appointed for their knowledge of the world and their judgment, uninterested in hierarchy for hierarchy’s sake, and seeking the greatest good for the greatest number.

No room here for the infantile phallocentric Nietzscheanism that is destroying modern human culture. If you were a boy you’d be on the margins, drifting between family groups (but never allowed to disrupt them) or shacked up with your bachelor pals in the elephant equivalent of an unswept bedsit (though usually your behaviour would be gentler, more convivial and more urbane than cohabiting human males). Your function would be to inseminate, and that’s all. Government would be the business of the females. You’d be a communitarian. Relationality would be everything. It’s not that you couldn’t survive alone, although there would certainly be a survival benefit from being a member of a community, just as humans live longer if they are plugged into a church, a mosque or a bowling club.

Yes, at some level your altruism might be reciprocal altruism, where you scratch my back if I scratch yours, or kin selection, where you are somehow persuaded to sacrifice yourself if your death or disadvantage will preserve a gene in a sufficiently closely related gene-bearer. But at a much more obvious and important level you’d be relational – joyously shouldering the duties that come with community – because it made you happy. Why do elephants seek out other elephants? Not primarily for sex, or for an extra arsenal of receptors to pick up the scent of poachers, or because they assume that the others will have found particularly nutritious food, but because they like other elephants.

[..] As an elephant, you’d have a mind. You would, no doubt at all, be conscious. All the evidence agrees. None – absolutely none – disagrees. You’d have a sense of yourself as distinct from other things. When you looked out contemptuously at humans, wondering why they ate obviously contaminated food, opted to be miserable and alone, or wasted energy on pointless aggression and anxiety, it would be your contempt, as opposed to generic elephantine contempt, or reflexive contempt that bypassed your cerebral cortex, or the contempt of your sister. It would be you looking out, and you’d know it was you.

Photograph: Palani Mohan/Getty Images