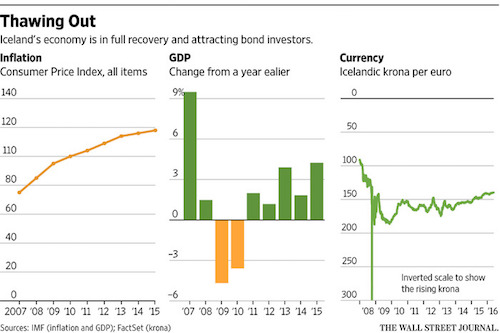

Iceland has spent eight years locking down its financial markets to keep foreign investors in. Now some are complaining the island nation is trying to shove them out. A law passed May 22 by Iceland’s parliament offers the foreign holders of about $2.3 billion worth of krona-denominated government bonds a Hobson’s choice: Sell out in June at a below-market exchange rate, or have the money they receive when their bonds mature impounded indefinitely in low-interest bank accounts. Investors, including Boston-based mutual-fund companies Eaton Vance and Loomis Sayles, a unit of Natixis, don’t want to go. They say they will reject the government’s offer. “We would like to stay invested,” said Patrick Campbell, a global bond analyst at Eaton Vance.

The dispute is the result of a wholesale turnaround in Iceland’s relationship with foreign investors. The country became synonymous with financial alchemy after its banks ballooned by borrowing in bond markets and attracting foreign depositors with high interest rates. That system imploded in 2008 when depositors made a run on the banks just as their bonds fell due, causing the krona to sharply devalue against the euro. Yet a growing number of fund managers are now buying Icelandic government bonds, including those that were marooned on the island when it applied capital controls. The country is now one of the few offering a combination of high interest rates and strong economic growth prospects.

Eaton Vance and another holder of the legacy debt, also called “offshore” debt, hedge fund Autonomy Capital LP, have been courting the government for months to allow them to keep their cash on the island, even offering to swap their holdings into long-term bonds that they would pledge to hold on to.But the country isn’t interested. Instead, officials behind the law say they aim to keep the $16.7 billion economy of the island with a population of 327,386 from being swamped anew by the ebb and flow of offshore funds. “We don’t need the money,” said Mar Gudmundsson, governor of Iceland’s central bank. “These are remnants from the last boom and bust, and we are not going to repeat that mistake.”

Japanese Prime Minister Shinzo Abe plans to delay an increase in sales tax by two and a half years, a government official said on Sunday, as the economy sputters and Abe prepares for a national election. Abe told Finance Minister Taro Aso and the secretary general of his ruling Liberal Democratic Party, Sadakazu Tanigaki, on Saturday of his plan to propose delaying the tax hike for a second time, until October 2019, said the official, who was briefed on the meeting. The prime minister, who has promised to announce steps on Tuesday to spur economic growth and promote structural reform, is also expected to order an extra budget to fund stimulus measures, just two months into the fiscal year and on the heels of a supplementary budget to pay for recovery from recent earthquakes in southern Japan.

After chairing a summit of Group of Seven leaders on Friday, Abe said Japan would mobilize “all policy tools” – including the possibility of delaying the tax hike – to avoid what he called an economic crisis on the scale of the global financial crisis that followed the 2008 Lehman Brothers bankruptcy. “There is a risk of the global economy falling into crisis if appropriate policy responses are not made,” Abe told a news conference after the summit. To play its part, Japan “must reignite powerfully the engine of Abenomics,” he said, referring to his easy-money policies aimed at getting Japan out of two decades of deflation and fitful growth. Abe has long said he would proceed with a plan to raise the tax rate to 10% from 8% next April unless Japan faced a crisis on the magnitude of the Lehman shock.

He said the G7 “shares a strong sense of crisis” about the global outlook, with the most worrisome risk being a global contraction led by a slowdown in emerging economies like China. Other G7 leaders, however, appeared to differ with Abe on the risk of a global crisis, fuelling comment that Abe was using the G7 to justify delaying the painful tax hike.

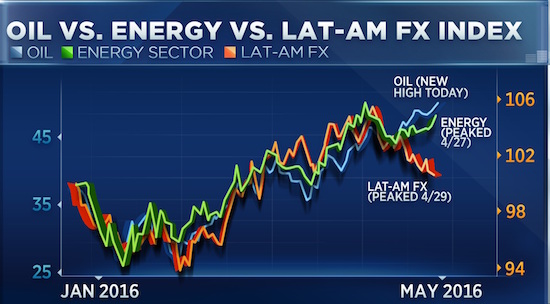

This week, oil broke above the key $50 level for the first time since October 2015. Yet rather than interpret the move as a sign to buy, one top technician is warning investors not to chase the rally. “I think it’s all about risk-reward and there’s probably no more important chart right now than the oil chart,” Chris Verrone, a technician at Strategas Research Partners, told CNBC’s “Fast Money” this week. According to Verrone, it’s the steepness of the move that bothers him most. In the past 72 days, oil has moved 20% above its 200-day moving average. “It looks excessive to us, we think there’s a higher likelihood you come back and retest the 200 near 39, 40 bucks,” said Verrone.

Also troubling to Verrone is the fact that while crude has surged to new highs, energy stocks and the Mexican peso — both of which are closely tied to oil — have not made new highs in a month. Energy names have fallen since peaking on April 27, whereas crude has surged 12%. Since peaking back April 29, the peso’s gains are still lagging those in oil. They are up 8% and 33%, respectively, this year. Indeed, analysts at Bank of America Merrill Lynch warned this week that continued strength in the dollar could trigger a series of knock-on effects that may push crude off its new highs. The bank said a “black swan event” such as Saudi Arabia removing its currency peg could lead to a collapse of Brent crude to as deep as $25 per barrel, and it expects oil prices to average $46 per barrel this year. On Friday, crude ended the session above $49 per barrel.

As the politics of this election year heat up, the chances of Congress debating — let alone passing — either of the White House’s marque trade deals continue to melt away. Oh, there’s plenty of talk about the westward-looking Trans-Pacific Partnership and the Euro-centered Transatlantic Trade and Investment Partnership, or TPP and TTIP, respectively. Most of the yakking, however, flows from Obama Administration officials; nary a word trickles out of Congress. Worse than Capitol Hill silence is the vocal pounding free trade takes when any of Obama’s would-be successors talk trade.

Bernie Sanders, a Democrat by name but socialist by heart, makes it crystal clear that he would rather eat glass than back “free” trade. Hillary Clinton, who three years ago called the TPP “exciting,” “innovative” and “ambitious,” now sees it as an agreement that has “failed to provide the basic safety net support needed” for American workers. Take that as an “innovative” no. And the Donald? He’s against TPP because, as he noted in one Republican debate this spring, “It’s a deal that was designed for China to come in, as they always do, through the back door … ” China, however, is not part of the Trans-Pacific Partnership, so whatever Trump meant must have been more of a “suggestion” than a fact. Whatever.

[..] Big Ag’s big push for the pending trade deals is understandable, given the two changed realities of today’s election year politics. First, even as we lean on the EU to alter its biotech food rules, the U.S. Senate still can’t agree on how to write a biotech food labeling law here. Members know the tide has turned on labeling; 89 out of 100 Americans want it. Majority Republicans, however, don’t and they continue to search for a way to be anti-labeling without becoming anti-incumbents. Second, not one presidential contender sees free trade as a vote-winning issue. Taken together, it’s hard to see how any trade deal goes anywhere this year. After that, you have to take the word of Hillary or Bernie or Donald. Well, maybe not Donald. Or Hillary. Bernie’s solid, though.

Schrödinger’s cat is something many of us have heard of, but perhaps fewer actually understand. The idea was first dreamed up by an Austrian physicist, Erwin Schrödinger, who wanted to illustrate the mind-bending nature of quantum mechanics. He created a thought experiment in this world to illustrate the point, which would allow a cat to be both dead and alive in a box at the same time. Now, scientists have added another box. And another cat. And the first cat being dead and alive simultaneously in the first box, so this causes the second cat in the second box to also be dead and alive at the same time. Makes perfect quantum sense, right? “It’s understandable that people don’t understand it,” lead author Chen Wang of Yale University told The Washington Post.

“You can’t understand it using common sense. We can’t either.” But here’s the premise: A cat sits in a box. Alongside the cat, there’s poison. That poison will only be released upon the decay of a radioactive subatomic particle. According to quantum mechanics, and specifically the theory of “superposition,” these particles actually exist in all possible states at the same time – until, that is, someone takes a measurement. At that point, the particle falls into a single, known state. So, the particles could be decaying, and not decaying, simultaneously. As a consequence, the poison is being released – and not released. And so the cat is both dead and alive. Until someone opens the box, of course, and is observed. Then, the cat can’t be doing both things at once.

What Dr. Wang and his team have done is to add another dimension: the concept of “entanglement.” This proposes that two objects can be intimately linked, even if billions of light-years separate them, and any change that happens to one will happen to the other instantaneously, a relationship Einstein once described as “spooky action at a distance.” For our cat, this means, quite simply, that there’s a twin, in another box. And everything that happens to one, happens to the other. In Wang’s experiment, there were no cats, just light. He used two aluminum cavities, each with a wave of light bouncing around inside. The researchers induced such a state so that the light existed in two different wavelengths at the same time, in both boxes.

USA. Allensworth, California. 2014. Fence post. Allensworth has a population of 471 and 54% live below the poverty level. Matt Black/Magnum Photos

Last summer Matt Black left the Central Valley of California, where he lives, to travel 18,000 miles across the US on a road trip that took him through 30 states and 70 of the poorest towns in America. The startling image of a hand resting on a fence post against a barren backdrop was taken in the small town of Allensworth, California, where 54% of the population of 471 people live below the poverty level. “California always seemed special and unique in terms of how it symbolised promise and progress,” says Black, 45, during a break in shooting landscapes in Idaho, where he’s working on another stage of the same series, Geography of Poverty. “So it seemed somehow symbolic to begin there and travel east, but what has surprised me is the similarities I have encountered as I travelled from one community to another.

All these diverse communities are connected, not least in their powerlessness. In the mainstream media, poverty is often looked at in isolation, but it is an American problem. It seems to me that it goes unreported because it does not fit the way America sees itself.” As if to bear this out, Black tells me that the route he took was mapped out in advance using geotagged photographs found online alongside census information to identify the poorest areas. In each instance, the communities he visited were never more than a two-hour drive apart. “I was able to drive from California to the east coast and back without ever leaving these poor areas.” Black’s striking images are on show in a group exhibition, New Blood, at the Magnum Print Room in London…

USA. El Paso, Texas. 2015. El Paso has a population of 649,121 and 21.5% live below the poverty level. Matt Black/Magnum Photos

It’s been a busy winter in downtown Athens, where scaffolding, tarpaulins and dust have been symbols of hope: a mini construction boom heralding a tourist renaissance. Nine hotels are being built or restored around the city centre. Their arrival correlates with the huge upturn in holidaymakers visiting the Greek capital since a low point in late 2008, when Athens erupted into riots after the police killing of a teenage boy. “It’s a miracle, what’s been happening in Athens,” Greece’s tourism chief, Andreas Andreadis, told the Observer. “The tourist industry in Greece grew two to three times faster than in Spain, Portugal, Italy or France last year. This year we expect around 4.5 million visitors in Athens alone.”

For an economy stuck in depression-era recession, dependent on emergency bails and seemingly locked in a perpetual fiscal vice, tourism is vital. A record 23.5 million holidaymakers visited Greece in 2015 – generating €14.2bn in direct receipts, or 24% of GDP. In 2010, at the start of the country’s debt crisis – which has seen it struggle to avert default and remain in the euro – revenues from tourism were €10bn, or 15% of GDP. The Greek Tourism Confederation, Sete, is predicting another bumper season for an industry that has long been the single biggest contributor to the economy and job market. Arrivals could reach 25 million (27.5 million including cruise ship passengers), which is more than twice the country’s population. Economic recovery will depend on the sector to a great degree.

Andreadis said: “If we get 1.5 million more visitors it will produce an additional €800m in direct receipts. Such a positive kick that would come in the third and fourth quarters.” Much of the upsurge is linked to Greece’s safety record. Tourists are staying away from resort in Egypt, Tunisia, Turkey and elsewhere in the wake of high-profile attacks. Countries whose economies are also dependent on holidaymakers have suffered incalculable damage following a severe drop in arrivals. Travel advice from governments and fears of fresh violence are simply keeping tourists away. But other countries’ loss could be Greece’s gain. And it could not come at a better time: tourism provides one in five jobs in Greece, at a time when unemployment in the effectively bankrupt nation has hovered stubbornly around 25%. Youth unemployment stands at an astonishing 67%.

In the port-side café before the sun comes up, a group of men are talking. “In the beginning, when there were maybe 40 of them in the boats, all wet, we helped them. Now they’re too many. They steal chickens. They shit in the fields. They threw stones at a woman.” “Do you think it’s chance that they’re all coming here? The NGOs, the whatever they’re called, are making money off it. It’s a plan. A racket.” “Eventually they’ll set off a bomb and sink the island.” “Sink or float, what difference does it make? Are we happy, now we’re floating?” Chios, my grandfather’s island in the northeast Aegean Sea, has become an open-air prison for more than 2,000 refugees. Almost all of them arrived after the March 20 “statement” signed by the EU and Turkey, designed to stop the flow of people from Turkey to the Greek islands and then to mainland Europe.

The statement, which followed the unilateral closure by Central European countries of the western Balkans route, cut time and space like a guillotine, arbitrarily separating those who’d arrived before it from those who landed after, trapping more than 50,000 refugees and migrants in Greece. These late arrivals can’t leave the islands until their cases have been decided by the Greek asylum system, which is overloaded to the point of paralysis. The refugees are supposed to prove not only that they’re at risk in their home country but that they’d be at risk in Turkey, which the EU (but not Greece) considers a “safe third country,” if they want to have their asylum claim heard in Greece. Otherwise, they will be returned to Turkey.

Of the 8,500 women, children, and men who have landed on the islands since the agreement was signed, 400 have been returned so far, some to be detained for weeks without legal representation. About 200 have been granted asylum in Greece. The rest are rotting in overcrowded camps, “hot spots,” and locked detention centers, without information, adequate food, medical care, or security. And the boats from Turkey, though many fewer than before, continue to come in.

A flotilla of ships saved 668 people from boats in the Mediterranean Sea on Saturday, authorities in Italy said, bringing the week’s total of refugees plucked from the sea to 13,000 people. The rescues by the Italian coast guard and navy ships, aided by Irish and German vessels and humanitarian groups, are the latest by a multinational patrol south of the Italian island of Sicily. Warner spring weather has led to a surge of people attempting the perilous crossing from Africa to Europe. The Irish military said the vessel Le Roisin saved 123 people from a 12m-long (40-ft) rubber dinghy and recovered a male body. A German ship was involved in four separate rescue operations, the Italian coast guard said on Saturday evening.

Meanwhile, with shelters filling up in Sicily, the Italian navy vessel Vega headed toward Reggio Calabria, a southern Italian mainland port, bringing 135 survivors and 45 bodies from a rescue a day earlier. The Vega was due to dock on Sunday. Other survivors who arrived on Saturday in the Sicilian port of Pozzallo told authorities they had witnessed a fishing boat filled with“ hundreds” of people sink on Thursday, a Save The Children spokeswoman, Giovanna Di Benedetto, told The Associated Press by telephone from Sicily. According to survivors, two smugglers’ fishing boats and a dinghy set sail on Wednesday night from Libya’s coast. Di Benedetto said the survivors were among 500 or so aboard the one fishing boat that didn’t sink and the dinghy. “All of this must be verified, of course,” said Di Benedetto, but if the survivors’ accounts bear out, as many as 400 people could have drowned, with only a very few of those on the vessel that sank able to reach the other boats.

Migrants rescued from two boats in the Mediterranean this week told humanitarian workers in Italy that they saw another vessel carrying some 400 migrants sink, Save the Children said on Saturday. Three vessels carrying migrants already are confirmed to have sunk or capsized this week. More than 60 bodies are said to have been recovered, including those of three infants, and hundreds are believed to be missing. But the possible sinking of a fourth vessel on Thursday had not been reported, said Giovanna Di Benedetto, spokeswoman for Save the Children in Italy. That ship along with another fishing boat and a rubber boat left Sabratha in Libya late Wednesday night, according to interviews on Saturday with some of the more than 600 survivors from the two other vessels in the Sicilian port of Pozzallo.

They said the rubber boat had its own motor, but the smaller fishing boat, carrying some 400 migrants, did not. It was towed by the larger fishing vessel, which held about 500 others. Eventually the smaller boat began to take on water and, when the captain of the larger boat ordered the tow line cut, sank with most of its passengers, the survivors told Save the Children. Those aboard the other two vessels were not rescued until much later. “There were many women and children on board,” the survivors said, according to Di Benedetto. “We collected testimony from several of those rescued from both (the rubber and fishing) boats. They all say they saw the same thing.”

A dark storm is brewing in the world of private pensions, and all hell could break loose when it finally hits. As the Washington Post reports, the Central States Pension Fund, which handles retirement benefits for current and former Teamster union truck drivers across various states including Texas, Michigan, Wisconsin, Missouri, New York, and Minnesota, and is one of the largest pension funds in the nation, has filed an application to cut participant benefits, which would be effective July 1 2016, as it “projects” it will become officially insolvent by 2025. In 2015, the fund returned -0.81%, underperforming the 0.37% return of its benchmark. Over a quarter of a million people depend on their pension being handled by the CSPF; for most it is their only source of fixed income.

Pension funds applying to lower promised benefits is a new development, albeit not unexpected (we warned of this mounting issue numerous times in the past). For many years there existed federal protections which shielded pensions from being cut, but that all changed in December 2014, when folded neatly into a $1.1 trillion government spending bill, was a proposal to allow multi employer pension plans to cut pension benefits so long as they are projected to run out of money in the next 10 to 20 years. Between rising benefit payouts as participants become eligible, the global financial crisis, and the current interest rate environment, it was certainly just a matter of time before these steps were taken to allow pension plans to cut benefits to stave off insolvency.

The Central States Pension Fund is currently paying out $3.46 in pension benefits for every $1 it receives from employers, which has resulted in the fund paying out $2 billion more in benefits than it receives in employer contributions each year. As a result, Thomas Nyhan, executive director of the Central States Pension Fund said that the fund could become insolvent by 2025 if nothing is done. The fund currently pays out $2.8 billion a year in benefits according to Nyhan, and if the plan becomes insolvent it would overwhelm the Pension Benefit Guaranty Corporation (designed by the government to absorb insolvent plans and continue paying benefits), who at the end of fiscal 2015 only had $1.9 billion in total assets itself. Incidentally as we also pointed out last month, the PBGC projects that they will also be insolvent by 2025 – it appears there is something very foreboding about that particular year.

Since 2013, the federal reserve board has conducted a survey to “monitor the financial and economic status of American consumers.” Most of the data in the latest survey, frankly, are less than earth-shattering: 49% of part-time workers would prefer to work more hours at their current wage; 29% of Americans expect to earn a higher income in the coming year; 43% of homeowners who have owned their home for at least a year believe its value has increased. But the answer to one question was astonishing. The Fed asked respondents how they would pay for a $400 emergency. The answer: 47% of respondents said that either they would cover the expense by borrowing or selling something, or they would not be able to come up with the $400 at all. Four hundred dollars! Who knew? Well, I knew. I knew because I am in that 47%.

I know what it is like to have to juggle creditors to make it through a week. I know what it is like to have to swallow my pride and constantly dun people to pay me so that I can pay others. I know what it is like to have liens slapped on me and to have my bank account levied by creditors. I know what it is like to be down to my last $5—literally—while I wait for a paycheck to arrive, and I know what it is like to subsist for days on a diet of eggs. I know what it is like to dread going to the mailbox, because there will always be new bills to pay but seldom a check with which to pay them. I know what it is like to have to tell my daughter that I didn’t know if I would be able to pay for her wedding; it all depended on whether something good happened. And I know what it is like to have to borrow money from my adult daughters because my wife and I ran out of heating oil.

You wouldn’t know any of that to look at me. I like to think I appear reasonably prosperous. Nor would you know it to look at my résumé. I have had a passably good career as a writer—five books, hundreds of articles published, a number of awards and fellowships, and a small (very small) but respectable reputation. You wouldn’t even know it to look at my tax return. I am nowhere near rich, but I have typically made a solid middle- or even, at times, upper-middle-class income, which is about all a writer can expect, even a writer who also teaches and lectures and writes television scripts, as I do.

And you certainly wouldn’t know it to talk to me, because the last thing I would ever do—until now—is admit to financial insecurity or, as I think of it, “financial impotence,” because it has many of the characteristics of sexual impotence, not least of which is the desperate need to mask it and pretend everything is going swimmingly. In truth, it may be more embarrassing than sexual impotence. “You are more likely to hear from your buddy that he is on Viagra than that he has credit-card problems,” says Brad Klontz, a financial psychologist who teaches at Creighton University in Omaha, Nebraska, and ministers to individuals with financial issues. “Much more likely.”

“From a credit perspective, we’d be more comfortable with China slowing more than it is. We are getting less confident in the government’s commitment to structural reforms.”

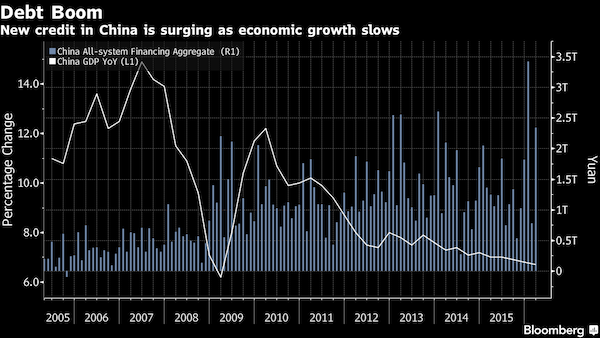

Billionaire investor George Soros said China’s debt-fueled economy resembles the U.S. in 2007-08, before credit markets seized up and spurred a global recession. China’s March credit-growth figures should be viewed as a warning sign, Soros said at an Asia Society event in New York on Wednesday. The broadest measure of new credit in the world’s second-biggest economy was 2.34 trillion yuan ($362 billion) last month, far exceeding the median forecast of 1.4 trillion yuan in a Bloomberg survey and signaling the government is prioritizing growth over reining in debt. What’s happening in China “eerily resembles what happened during the financial crisis in the U.S. in 2007-08, which was similarly fueled by credit growth,” Soros said. “Most of money that banks are supplying is needed to keep bad debts and loss-making enterprises alive.”

Soros, who built a $24 billion fortune through savvy wagers on markets, has recently been involved in a war of words with the Chinese government. He said at the World Economic Forum in Davos that he’s been betting against Asian currencies because a hard landing in China is “practically unavoidable.” China’s state-run Xinhua news agency rebutted his assertion in an editorial, saying that he has made the same prediction several times in the past. China’s economy gathered pace in March as the surge in new credit helped the property sector rebound. Housing values in first-tier cities have soared, with new-home prices in Shenzhen rising 62 percent in a year. While China’s real estate is in a bubble, it may be able to feed itself for some time, similar to the U.S. in 2005 and 2006, Soros said.

China’s economy gathered pace in March as the surge in new credit helped the property sector rebound. Housing values in first-tier cities have soared, with new-home prices in Shenzhen rising 62 percent in a year. While China’s real estate is in a bubble, it may be able to feed itself for some time, similar to the U.S. in 2005 and 2006, Soros said. “Most of the damage occurred in later years,” Soros said. “It’s a parabolic cycle.” Andrew Colquhoun at Fitch Ratings, is also concerned about China’s resurgence in borrowing. Eventually, the very thing that has been driving the economic recovery could end up derailing it, because China is adding to a debt burden that’s already unsustainable, he said.

Fitch rates the nation’s sovereign debt at A+, the fifth-highest grade and a step lower than Standard & Poor’s and Moody’s Investors Service, which both cut their outlooks on China since March. “Whether we call it stabilization or not, I am not sure,” Colquhoun said in an interview in New York. “From a credit perspective, we’d be more comfortable with China slowing more than it is. We are getting less confident in the government’s commitment to structural reforms.”

The rest of the world’s steel producers may be pressuring Beijing to slash output and help reduce a global glut that is causing losses and costing jobs, but the opposite is happening in the steel towns of China. While the Chinese government points to reductions in steel making capacity it has engineered, a rapid rise in local prices this year has seen mills ramp up output. Even “zombie” mills, which stopped production but were not closed down, have been resurrected. Despite global overproduction, Chinese steel prices have risen by 77% this year from last year’s trough on some very specific local factors, including tighter supplies following plant shutdowns last year, restocking by consumers and a pick-up in seasonal demand following the Chinese New Year break.

Some mills also boosted output ahead of mandated cuts around a major horticultural show later this month in the Tangshan area. Local mills must at least halve their emissions on certain days during the exposition, due to run from April 29 to October. China, which accounts for half the world’s steel output and whose excess capacity is four times U.S. production levels, has said it has done more than enough to tackle overcapacity, and blames the glut on weak demand. But a survey by Chinese consultancy Custeel showed 68 blast furnaces with an estimated 50 million tonnes of capacity have resumed production. The capacity utilization rate among small Chinese mills has increased to 58% from 51% in January.

At large mills, it has risen to 87% from 84%, according to a separate survey by consultancy Mysteel. The rise in prices has thrown a lifeline to ‘zombie’ mills, like Shanxi Wenshui Haiwei Steel, which produces 3 million tonnes a year but which halted nearly all production in August. It now plans to resume production soon, a company official said. Another similar-sized company, Jiangsu Shente Steel, stopped production in December but then resumed in March as prices surged, a company official said. More than 40 million tonnes of capacity out of the 50-60 million tonnes that were shut last year are now back on, said Macquarie analyst Ian Roper. “Capacity cuts are off the cards given the price and margin rebound,” he said.

China will encourage ships flying its flag to take the Northwest Passage via the Arctic Ocean, a route opened up by global warming, to cut travel times between the Atlantic and Pacific oceans, a state-run newspaper said on Wednesday. China is increasingly active in the polar region, becoming one of the biggest mining investors in Greenland and agreeing to a free trade deal with Iceland. Shorter shipping routes across the Arctic Ocean would save Chinese companies time and money. For example, the journey from Shanghai to Hamburg via the Arctic route is 2,800 nautical miles shorter than going by the Suez Canal. China’s Maritime Safety Administration this month released a guide offering detailed route guidance from the northern coast of North America to the northern Pacific, the China Daily said.

“Once this route is commonly used, it will directly change global maritime transport and have a profound influence on international trade, the world economy, capital flow and resource exploitation,” ministry spokesman Liu Pengfei was quoted as saying. Chinese ships will sail through the Northwest Passage “in the future”, Liu added, without giving a time frame. Most of the Northwest Passage lies in waters that Canada claims as its own. Asked if China considered the passage an international waterway or Canadian waters, Chinese Foreign Ministry spokeswoman Hua Chunying said China noted Canada considered that the route crosses its waters, although some countries believed it was open to international navigation.

In Ottawa, a spokesman for Foreign Minister Stephane Dion said no automatic right of transit passage existed in the waterways of the Northwest Passage. “We welcome navigation that complies with our rules and regulations. Canada has an unfettered right to regulate internal waters,” Joseph Pickerill said by email.

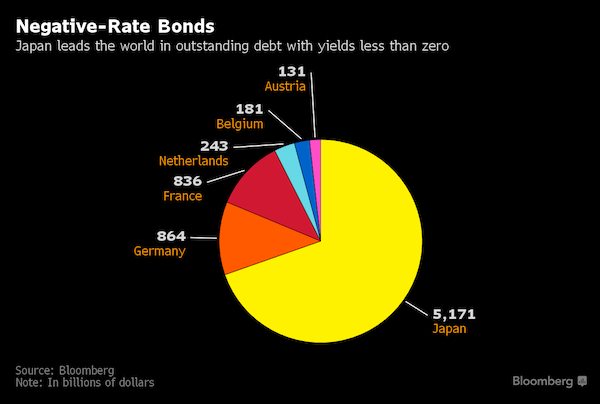

Europe’s central bank took the unorthodox step of cutting interest rates below zero in 2014. Japan followed suit earlier this year, and has become home to more negative-yielding debt than anywhere else, leading Germany, France, the Netherlands and Belgium.

Crazy free money, no strings: “Banks are encouraged to extend credit to the real economy but are not penalized for not meeting their benchmark lending targets..”

Economists and analysts have been swooning over a new series of ultra-cheap, ultra-long bank loans announced by the ECB last month, which they believe might just kickstart the region’s fragile economy. “It’s massively positive,” Erik Nielsen, global chief economist at UniCredit, told CNBC via email regarding the new breed of “credit-easing” tactics announced by ECB President Mario Draghi. These targeted long-term refinancing operations, or TLTRO IIs, advance on a previous model announced by the central bank in 2011 and effectively give free money to the banks to lend to the real economy. They’re a series of four loans – conducted between June 2016 and March 2017 – and will have a fixed maturity of four years.

The interest rate will start at nothing, but could become as low as the current deposit rate, which is currently -0.40%, if banks meet their loan targets. This means the banks will be receiving cash for borrowing from the central bank. Banks will need to post collateral at the ECB but there’s no penalty if they fail to meet their loan targets. All that will happen is that the loans will be priced at zero for four years. Frederik Ducrozet, a euro zone economist with private Swiss-bank Pictet, called it “unconditional liquidity to banks at 0% cost, against collateral.” He said in a note last month that he expects it to lower bank funding costs, mitigate the adverse consequences of negative rates, strengthen the ECB’s forward guidance and improve the transmission of monetary policy.

Abhishek Singhania, a strategist at Deutsche Bank, added that the new LTROs “reduce the stigma” attached to their use compared to the previous model. “Banks are encouraged to extend credit to the real economy but are not penalized for not meeting their benchmark lending targets,” he said in a note last month.

Ambrose muses on Europe: “The EU is a strategic relic of a post-War order that no longer exists, and a clutter of vested interests that caused Europe to miss the IT revolution.”

[..] The Justice Secretary is right to dismiss Project Fear as craven and defeatist. A vote to leave the dysfunctional EU half-way house might well be a “galvanising, liberating, empowering moment of patriotic renewal”. The EU is a strategic relic of a post-War order that no longer exists, and a clutter of vested interests that caused Europe to miss the IT revolution. “We will have rejected the depressing and pessimistic vision that Britain is too small and weak, and the British people too hapless and pathetic, to manage their own affairs,” he said. The special pleading of the City should be viewed with a jaundiced eye. This is the same City that sought to stop the country upholding its treaty obligations to Belgium in 1914, and that funded the Nazi war machine even after Anschluss in 1938, lobbying for appeasement to protect its loans. It is morally disqualified from any opinion on statecraft or higher matters of sovereign self-government.

Mr Gove is right that the European Court has become a law unto itself, asserting a supremacy that does not exist in treaty law, and operating under a Roman jurisprudence at odds with the philosophy and practices of English Common Law. It has seized on the Charter of Fundamental Rights to extend its jurisdiction into anything it pleases. Do I laugh or cry as I think back to the drizzling Biarritz summit of October 2000 when the Europe minister of the day told this newspaper that the charter would have no more legal standing than “the Beano or the Sun”? What Mr Gove cannot claim with authority is that Britain will skip painlessly into a “free trade zone stretching from Iceland to Turkey that all European nations have access to, regardless of whether they are in or out of the euro or the EU”.

Nobody knows exactly how the EU will respond to Brexit, or how long it would take to slot in the Norwegian or Swiss arrangements, or under what terms. Nor do we know how quickly the US, China, India would reply to our pleas for bi-lateral deals. Over 100 trade agreements would have to be negotiated, and the world has other priorities. Brexit might set off an EU earthquake as Mr Gove says – akin to the collapse of the Berlin Wall in the words of France’s Marine Le Pen – but it would not resemble his children’s fairy tale. The more plausible outcome is a 1930s landscape of simmering nationalist movements with hard-nosed reflexes, and a further lurch toward authoritarian polities from Poland to Hungary and arguably Slovakia, and down to Romania where the Securitate never entirely lost its grip and Nicolae Ceausescu is back in fashion.

Pocket Putins will have a field day knowing that they can push the EU around. The real Vladimir Putin will be waiting for his moment of maximum mayhem to try his luck with “little green men” in Estonia or Latvia, calculating that nothing can stop him restoring the western borders of the Tsarist empire if he can test and subvert NATO’s Article 5 – the solidarity clause, one-for-all and all-for-one. A case can be made that the EU has gone so irretrievably wrong that Britain must withdraw to save its legal fabric and parliamentary tradition. If so, let us at least be honest about what we face. One might equally quote another British prime minster, with poetic licence: ‘I have nothing to offer but blood, toil, tears, and sweat’.

Greece could crash out of the eurozone as early as this summer if Britons vote to leave the European Union in the upcoming referendum, economists have predicted. The uncertainty following a ‘yes’ vote to Britain leaving the EU would put unsustainable pressure on Greece’s cash-strapped economy at a time when it is also struggling to cope with an influx of migrants escaping turmoil in the Middle East and Africa, according to a report from the Economist Intelligence Unit. The authors of the report say it is highly likely that Greece will be forced to leave the eurozone at some point within the next five years, but that if the UK votes to leave the EU in June, it could happen much sooner. Greece is already under a huge amount of pressure and a so-called Brexit could tip it over the edge.

The country has large debt payments due in mid-2016, while structural reforms recommended in Greece’s bail-out programme are “slow burners” and unlikely to deliver any significant growth in the short term. Greece’s true GDP contracted by 0.3pc last year, while unemployment stands at 24pc. The country’s overall debt-to-GDP ratio has hit 171pc. “While the region could probably handle a Brexit, Grexit or an escalation of the migrant crisis individually, it would be unlikely to navigate successfully a situation in which several of those crises came to a head simultaneously,” the report, entitled ‘Europe stretched to the limit’, said. “It is not impossible that this could happen as early as mid-2016, when the UK votes on whether or not to remain in the EU.”

Volkswagen and U.S. officials have reached a framework deal under which the automaker would offer to buy back almost 500,000 diesel cars that used sophisticated software to evade U.S. emission rules, two people briefed on the matter said on Wednesday. The German automaker is expected to tell a federal judge in San Francisco Thursday that it has agreed to offer to buy back up to 500,000 2.0-liter diesel vehicles sold in the United States that exceeded legally allowable emission levels, the people said. That would include versions of the Jetta sedan, the Golf compact and the Audi A3 sold since 2009. The buyback offer does not apply to the bigger, 80,000 3.0-liter diesel vehicles also found to have exceeded U.S. pollution limits, including Audi and Porsche SUV models, the people said.

U.S.-listed shares of Volkswagen rose nearly 6% to $30.95 following the news. VW in September admitted cheating on emissions tests for 11 million vehicles worldwide since 2009, damaging the automaker’s global image. As part of the settlement with U.S. authorities including the Environmental Protection Agency, Volkswagen has also agreed to a compensation fund for owners, a third person briefed on the terms said. The compensation fund is expected to represent more than $1 billion on top of the cost of buying back the vehicles, but it is not clear how much each owner might receive, the person said. Volkswagen may also offer to repair polluting diesel vehicles if U.S. regulators approve the proposed fix, the sources said.

Support for the transatlantic trade deal known as TTIP has fallen sharply in Germany and the United States, a survey showed on Thursday, days before Chancellor Angela Merkel and President Barack Obama meet to try to breathe new life into the pact. The survey, conducted by YouGov for the Bertelsmann Foundation, showed that only 17% of Germans believe the Transatlantic Trade and Investment Partnership is a good thing, down from 55% two years ago. In the United States, only 18% support the deal compared to 53% in 2014. Nearly half of U.S. respondents said they did not know enough about the agreement to voice an opinion. TTIP is expected to be at the top of the agenda when Merkel hosts Obama at a trade show in Hanover on Sunday and Monday.

Ahead of that meeting, German officials said they remained optimistic that a broad “political agreement” between Brussels and Washington could be clinched before Obama leaves office in January. The hope is that TTIP could then be finalised with Obama’s successor. But there have been abundant signs in recent weeks that European countries are growing impatient with the slow pace of the talks, which are due to resume in New York next week. On Wednesday, German Economy Minister Sigmar Gabriel described the negotiations as “frozen up” and questioned whether Washington really wanted a deal.

The day before, France’s trade minister threatened to halt the talks, citing a lack of progress. Deep public scepticism in Germany, Europe’s largest economy, has clouded the negotiations from the start. The Bertelsmann survey showed that many Germans fear the deal will lower standards for products, consumer protection and the labor market. It also pointed to a dramatic shift in how Germans view free trade in general. Only 56% see it positively, compared to 88% two years ago. “Support for trade agreements is fading in a country that views itself as the global export champion,” said Aart de Geus, chairman and chief executive of the Bertelsmann Foundation.

Bottom line: “..non-performing debt [..] stands at €360bn, according to the Bank of Italy. So is Atlante — with about €5bn of equity — really enough to keep the heavens in place?”

Atlante, a new private initiative backed by the Italian government, is designed to stop the sky falling in. The fund, which takes its name from the mythological titan who held up the heavens, will buy shares in Italian lenders in a bid to edge the sector away from a fully-fledged crisis. Last week’s announcement of the fund, which can also buy non-performing loans, led to a welcome boost for Italian banks. An index for the sector gained 10% over the week — its best performance since the summer of 2012, though it remains heavily down on the year. But Italian banks have made €200bn of loans to borrowers now deemed insolvent, of which €85bn has not been written down on their balance sheets. A broader measure of non-performing debt, which includes loans unlikely to be repaid in full, stands at €360bn, according to the Bank of Italy.

So is Atlante — with about €5bn of equity — really enough to keep the heavens in place? The Italian government has been placed in a highly unusual position. It has become much harder to directly bail out its financial institutions, as other European countries did during the crisis. Meanwhile, a new European-wide approach to bank failure, which involves imposing losses on bondholders, is politically fraught in Italy, where large numbers of bonds have been sold to retail customers. The new fund also comes in the context of an extremely weak start to the year for global markets. “In this market it is impossible for anyone to raise any capital,” says Sebastiano Pirro, an analyst at Algebris, adding that, since November last year, “the markets have been shut for Italian banks”.

The government has been forced into an array of subtle interventions to provide support. Earlier this year, details emerged of a scheme for non-performing loans to be securitised — a process where assets are packaged together and sold as bond-like products of different levels, or tranches, of risk. The government planned to offer a guarantee on the most senior tranches — those with a triple B, or “investment grade” rating.

Six years ago, Saudi and American officials agreed on a record $60 billion arms deal. The United States would sell scores of F-15 fighters, Apache attack helicopters and other advanced weaponry to the oil-rich kingdom. The arms, both sides hoped, would fortify the Saudis against their aggressive arch-rival in the region, Iran. But as President Barack Obama makes his final visit to Riyadh this week, Saudi Arabia’s military capabilities remain a work in progress – and the gap in perceptions between Washington and Riyadh has widened dramatically. The biggest stumble has come in Yemen. Frustrated by Obama’s nuclear deal with Iran and the U.S. pullback from the region, Riyadh launched an Arab military intervention last year to confront perceived Iranian expansionism in its southern neighbour.

The conflict pits a coalition of Arab and Muslim nations led by the Saudis against Houthi rebels allied to Iran and forces loyal to a former Yemeni president. A tentative ceasefire is holding as the United Nations prepares for peace talks in Kuwait, proof, the Saudis say, of the intervention’s success. But while Saudi Arabia has the third-largest defence budget in the world behind the United States and China, its military performance in Yemen has been mixed, current and former U.S. officials said. The kingdom’s armed forces have often appeared unprepared and prone to mistakes. U.N. investigators say that air strikes by the Saudi-led coalition are responsible for two thirds of the 3,200 civilians who have died in Yemen, or approximately 2,000 deaths. They said that Saudi forces have killed twice as many civilians as other forces in Yemen.

On the ground, Saudi-led forces have often struggled to achieve their goals, making slow headway in areas where support for Iran-allied Houthi rebels runs strong. And along the Saudi border, the Houthis and allied forces loyal to former Yemeni president Ali Abdullah Saleh have attacked almost daily since July, killing hundreds of Saudi troops. Instead of being the centrepiece of a more assertive Saudi regional strategy, the Yemen intervention has called into question Riyadh’s military influence, said one former senior Obama administration official. “There’s a long way to go. Efforts to create an effective pan-Arab military force have been disappointing.”

Behind the scenes, the West has been enmeshed in the conflict. Between 50 and 60 U.S. military personnel have provided coordination and support to the Saudi-led coalition, a U.S. official told Reuters. And six to 10 Americans have worked directly inside the Saudi air operations centre in Riyadh. Britain and France, Riyadh’s other main defence suppliers, have also provided military assistance. Last year, the Obama administration had the U.S. military send precision-guided munitions from its own stocks to replenish dwindling Saudi-led coalition supplies, a source close to the Saudi government said. Administration officials argued that even more Yemeni civilians would die if the Saudis had to use bombs with less precise guidance systems.

More than half of the US population lives amid potentially dangerous air pollution, with national efforts to improve air quality at risk of being reversed, a new report has warned. A total of 166 million Americans live in areas that have unhealthy levels of of either ozone or particle pollution, according to the American Lung Association, raising their risk of lung cancer, asthma attacks, heart disease, reproductive problems and other ailments. The association’s 17th annual “state of the air” report found that there has been a gradual improvement in air quality in recent years but warned progress has been too slow and could even be reversed by efforts in Congress to water down the Clean Air Act. Climate change is also a looming air pollution challenge, with the report charting an increase in short-term spikes in particle pollution.

Many of these day-long jumps in soot and smoke have come from a worsening wildfire situation across the US, especially in areas experiencing prolonged dry conditions. Six of the 10 worst US cities for short-term pollution are in California, which has been in the grip of an historic drought. Bakersfield, California, was named the most polluted city for both short-term and year-round particle pollution, while Los Angeles-Long Beach was the worst for ozone pollution. Small particles that escape from the burning of coal and from vehicle tail pipes can bury themselves deep in people’s lungs, causing various health problems. Ozone and other harmful gases can also be expelled from these sources, triggering asthma attacks and even premature death.

Can Brussels survive such failure? More urgently, can Greece survive the fallout? Because it’s Greece that will suffer first, and most, if the EU pact with the devil falls through.

European diplomats are agonising over their politically perilous promise to grant visa-free travel to 80m Turks, amid strong warnings from Ankara that the EU migration deal will fold without a positive visa decision by June. The EU’s month-old deal to return migrants from Greece to Turkey has dramatically cut flows across the Aegean, easing what had been an acute migration crisis. But the pact rests on sweeteners for Ankara that the EU is struggling to deliver – above all, giving Turkish citizens short-term travel rights to Europe’s Schengen area. Germany, France and other countries nervous of a political backlash over Muslim migration have started exploring options to make the concession more politically palatable, including through safeguard clauses, extra conditions or watered-down terms.

The political calculations are further complicated by looming EU visa decisions for Ukraine, Georgia and Kosovo. Several senior European diplomats say ideas considered include a broad emergency brake, allowing the EU to suspend the visa deal under certain circumstances; limiting the visa privileges to Turkish executives and students; or opting for an unconventional visa-waiver treaty with Turkey, which would allow more rigorous, US-style checks on visitors. Selim Yenel, Turkey’s ambassador to the EU, called the efforts to water down the terms “totally unacceptable”, saying: “They cannot and should not change the rules of the game.” One senior EU official said the search for alternatives reflected “growing panic” in Berlin and Paris over the looming need to deliver the pledge.

The various options, the official added, were “a political smokescreen” to muster support in the Bundestag and European Parliament, which must also vote on the measures. The Turkish visa issue has even flared in Britain’s EU referendum campaign, forcing David Cameron, the prime minister, to clarify on Wednesday that Turks could not automatically come to the UK if they were granted visa rights to the 26-member Schengen area. The matter could come to a head within weeks. Brussels says Turkey is making good progress in fulfilling 72 required “benchmarks” to win the visa concessions and will issue a report on May 4. This is expected to say that Turkey is on course to meet the criteria by early June, passing the political dilemma to the EU member states and European Parliament.

One ambassador in Brussels said it looked ever more likely that several states would try to block visas for Turkey – a possibility that Mr Yenel also appears to anticipate. “They are probably getting cold feet since we are fulfilling the benchmarks,” he told the Financial Times. “We expect them to stick to what was agreed, otherwise how can we continue to trust the EU? We delivered on our side of the bargain. Now it is their turn.” Signs of Brussels backtracking have already prompted angry Turkish responses. “The EU needs Turkey more than Turkey needs the EU,” President Recep Tayyip Erdogan said recently. Meanwhile, Ahmet Davutoglu, Turkey’s prime minister, has warned that “no one can expect Turkey to adhere to its commitments” if the June deadline was not respected.

The much-derided Schengen Area is on the brink of collapse after furious Hungary launched a rebellion against open borders. The country’s prime minister Viktor Orban is also angry at mandatory migrant quotas enforced by the European Union. He is now touring Europe’s capital cities, where he is rallying support for a new plan with greater protection for individual states, dubbed “Schengen 2.0.” Currently, EU countries are forced to comply with orders from Brussels to accept and settle a specified number of migrants. Orban has described these quotas as “wrong-headed” and is now leading a group of other countries determined to re-take control of their borders. “The EU cannot create a system in which it lets in migrants and then prescribes mandatory resettlement quotas for every member state.”

Orban also promised a referendum in Hungary on whether the country should accept these orders, warning that some of the settled migrants were unlikely to integrate, leading to social friction. He said: “If we do not stop Brussels with a referendum, they will indeed impose on us masses of people, with whom we do not wish to live together.” Other countries may follow suit in opposing these plans and hold their own referendums, taking the power from Brussels and putting it back in the hands of their residents. Slovakia and the Czech Republic have both threatened to take legal action against the EU’s orders to take in migrants. Czech Prime Minister Bohuslav Sobotka said on Sunday: “I expect the line of opposition will be wider. Let us talk about legal action against the proposal when it is necessary.”

The action plan, which will be shared with the Czech Republic, Slovakia and Poland as well as the prime ministers of several other unspecified countries, is just the latest nail in the Schengen coffin. Last week, 2,000 soldiers in Switzerland’s tank battalion were told to postpone their summer holidays in order to be ready to rush to the border with Italy to block migrants making their way from Sicily. Austria has also begun sealing off its southern border, introducing checks on the vital Brenner Cross motorway and pledging the implementation of €1m worth of border patrols and security improvements. Brussel’s most senior bureaucrat admitted yesterday that confidence in the EU was dropping rapidly across the continent. In an astonishing confession of failure, European Commission President Jean-Claude Juncker said: “We are no longer respected in our countries when we emphasise the need to give priority to the EU.”

A team of our Automatic Earth-sponsored friends at the Social Kitchen prepares 1000s of meals for refugees daily at Elliniko. Your contributions are still as welcome as they are necessary.

Five mayors of Athens’s coastal suburbs warned Wednesday of the “enormous” health risks posed by a nearby camp housing over 4,000 migrants and refugees. “The conditions are out of control and present enormous risks to the public health,” the mayors complained in a letter to Prime Minister Alexis Tsipras, in reference to the camp at Elliniko, the site of Athens’s old airport. A total of 4,153 people, including many families, have been held there for the last month in miserable conditions. “The number of people is much higher than the capacity of the place and there are serious hygiene problems,” local mayor Dionyssis Hatzidakis told AFP.

He and his four fellow mayors from the area cited a document from Greece’s disease prevention center KEELPNO warning of the “the danger of disease contagion due to unacceptable housing conditions” at the site which they say has no more than 40 chemical toilets. Since the migrants’ favored route through the Balkans to the rest of Europe was shut down in February, numbers have been building up in Greece, with 46,000 Syrians and other nationalities now stuck in the country. Thousands of these have been transferred from the islands they arrived at to temporary centers such as the one at Elliniko, until more suitable reception centers can be set up.

The five mayors also voiced their disquiet at the “tensions and daily violent incidents between the refugees or migrants,” calling on the interior minister to boost police numbers in the area. “We are launching an appeal for help to protect the public health and security of both the refugees and the local population,” they said in their letter. Their intervention came the day after 17-year-old Afghan woman living in Elliniko with her parents died after six days in an Athens hospital. Her death was linked to a pre-existing heart condition exacerbated by the difficult journey to Greece, the doctor who treated her was quoted as saying in the Ethnos daily. Greek island officials on Tuesday began letting migrants leave detention centers where they have been held, as Human Rights Watch heaped criticism on a wave of EU-sanctioned expulsions to ease the crisis.

Recent reports have documented the growing rates of impoverishment in the U.S., and new information surfacing in the past 12 months shows that the trend is continuing, and probably worsening. Congress should be filled with guilt — and shame — for failing to deal with the enormous wealth disparities that are turning our country into the equivalent of a 3rd-world nation.

Half of Americans Make Less than a Living Wage According to the Social Security Administration, over half of Americans make less than $30,000 per year. That’s less than an appropriate average living wage of $16.87 per hour, as calculated by Alliance for a Just Society (AJS), and it’s not enough — even with two full-time workers — to attain an “adequate but modest living standard” for a family of four, which at the median is over $60,000, according to the Economic Policy Institute. AJS also found that there are 7 job seekers for every job opening that pays enough ($15/hr) for a single adult to make ends meet.

Half of Americans Have No Savings A study by Go Banking Rates reveals that nearly 50% of Americans have no savings. Over 70% of us have less than $1,000. Pew Research supports this finding with survey results that show nearly half of American households spending more than they earn. The lack of savings is particularly evident with young adults, who went from a five-percent savings rate before the recession to a negative savings rate today. Emmanuel Saez and Gabriel Zucman summarize: “Since the bottom half of the distribution always owns close to zero wealth on net, the bottom 90% wealth share is the same as the share of wealth owned by top 50-90% families.”

Nearly Two-Thirds of Americans Can’t Afford to Fix Their Cars The Wall Street Journal reported on a Bankrate study, which found 62% of Americans without the available funds for a $500 brake job. A Federal Reserve survey found that nearly half of respondents could not cover a $400 emergency expense. It’s continually getting worse, even at upper-middle-class levels. The Wall Street Journal recently reported on a JP Morgan study’s conclusion that “the bottom 80% of households by income lack sufficient savings to cover the type of volatility observed in income and spending.” Pew Research shows the dramatic shrinking of the middle class, defined as “adults whose annual household income is two-thirds to double the national median, about $42,000 to $126,000 annually in 2014 dollars.” Market watchers rave about ‘strong’ and even ‘blockbuster’ job reports.

But any upbeat news about the unemployment rate should be balanced against the fact that nine of the ten fastest growing occupations don’t require a college degree. Jobs gained since the recession are paying 23% less than jobs lost. Low-wage jobs (under $14 per hour) made up just 1/5 of the jobs lost to the recession, but accounted for nearly 3/5 of the jobs regained in the first three years of the recovery. Furthermore, the official 5% unemployment rate is nearly 10% when short-term discouraged workers are included, and 23% when long-term discouraged workers are included. People are falling fast from the ranks of middle-class living. Between 2007 and 2013 median wealth dropped a shocking 40%, leaving the poorest half with debt-driven negative wealth. Members of Congress, comfortably nestled in bed with millionaire friends and corporate lobbyists, are in denial about the true state of the American middle class. The once-vibrant middle of America has dropped to lower-middle, and it is still falling.

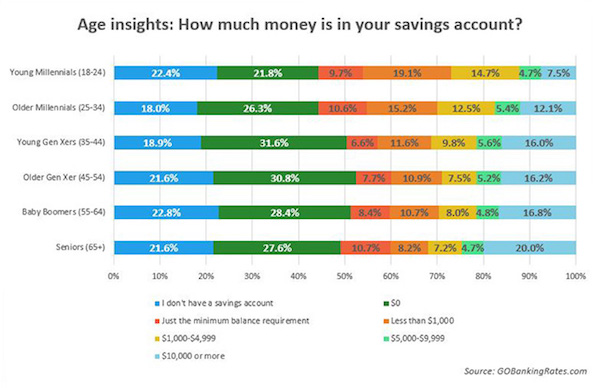

Americans are living right on the edge — at least when it comes to financial planning. Approximately 62% of Americans have less than $1,000 in their savings accounts and 21% don’t even have a savings account, according to a new survey of more than 5,000 adults conducted this month by Google Consumer Survey for personal finance website GOBankingRates.com. “It’s worrisome that such a large%age of Americans have so little set aside in a savings account,” says Cameron Huddleston, a personal finance analyst for the site. “They likely don’t have cash reserves to cover an emergency and will have to rely on credit, friends and family, or even their retirement accounts to cover unexpected expenses.”

This is supported by a similar survey of 1,000 adults carried out earlier this year by personal finance site Bankrate.com, which also found that 62% of Americans have no emergency savings for things such as a $1,000 emergency room visit or a $500 car repair. Faced with an emergency, they say they would raise the money by reducing spending elsewhere (26%), borrowing from family and/or friends (16%) or using credit cards (12%). And among those who had savings prior to 2008, 57% said they’d used some or all of their savings in the Great Recession, according to a U.S. Federal Reserve survey of over 4,000 adults released last year. Of course, paltry savings-account rates don’t encourage people to save either.

In the latest survey, 29% said they have savings above $1,000 and, of those who do have money in their savings account, the most common balance is $10,000 or more (14%), followed by 5% of adults surveyed who have saved between $5,000 and just shy of $10,000; 10% say they have saved $1,000 to just shy of $5,000. Just 9% of people say they keep only enough money in their savings accounts to meet the minimum balance requirements and avoid fees. But minimum balance requirements can vary widely and be hard to meet for some consumers. They can vary anywhere between $300 a month and $1,500 a month at some major banks.

Some age groups are less likely to have savings than others. Some 31% of Generation X — who are roughly aged 35 to 54 for the purpose of this survey — while being older and presumably more experienced with money than their younger cohorts, actually report a savings account balance of zero, which is the highest%age of all age groups. Around 29% of millennials — aged 18 to 34 — and 28% of baby boomers — aged 55 to 64 — said they have no money in their savings account. Baby boomers (17%) and seniors aged 65 and up (20%) have the most money saved of any age group while less than 10% of millennials and approximately 16% of Generation X have $10,000 or more saved.

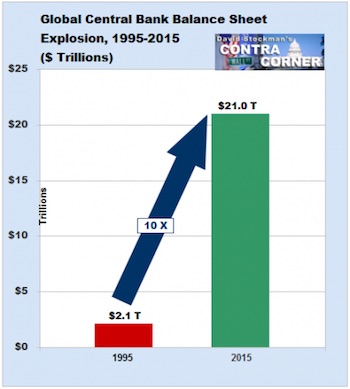

Our point yesterday was that the Fed and its Wall Street fellow travelers are about to get mugged by the oncoming battering rams of global deflation and domestic recession. When the bust comes, these foolish Keynesian proponents of everything is awesome will be caught like deer in the headlights. That’s because they view the world through a forecasting model that is an obsolete relic – one which essentially assumes a closed US economy and that balance sheets don’t matter. By contrast, we think balance sheets and the unfolding collapse of the global credit bubble matter above all else. Accordingly, what lies ahead is not history repeating itself in some timeless Keynesian economic cycle, but the last twenty years of madcap central bank money printing repudiating itself.

Ironically, the gravamen of the indictment against the “all is awesome” case is that this time is different – radically, irreversibly and dangerously so. High powered central bank credit has exploded from $2 trillion to $21 trillion since the mid-1990’s, and that has turned the global economy inside out. Under any kind of sane and sound monetary regime, and based on any semblance of prior history and doctrine, the combined balance sheets of the world’s central banks would total perhaps $5 trillion at present (5% annual growth since 1994). The massive expansion beyond that is what has fueled the mother of all financial and economic bubbles. Owing to this giant monetary aberration, the roughly $50 trillion rise of global GDP during that period was not driven by the mobilization of honest capital, profitable investment and production-based gains in income and wealth.

It was fueled, instead, by the greatest credit explosion ever imagined – $185 trillion over the course of two decades. As a consequence, household consumption around the world became bloated by one-time takedowns of higher leverage and inflated incomes from booming production and investment. Likewise, the GDP accounts were drastically ballooned by a spree of malinvestment that was enabled by cheap credit, not the rational probability of sustainable profits. In short, trillions of reported global GDP – especially in the Red Ponzi of China and its EM supply chain – represents false prosperity; the income being spent and recorded in the official accounts is merely the feedback loop of the central bank driven credit machine.

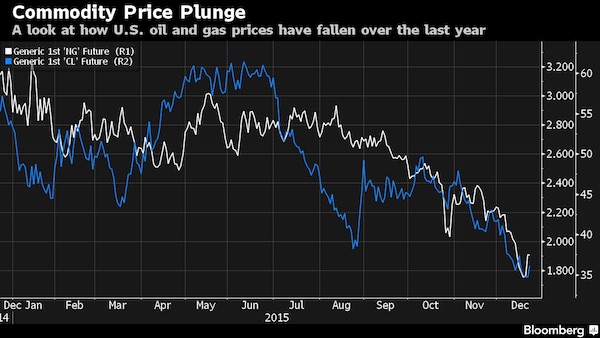

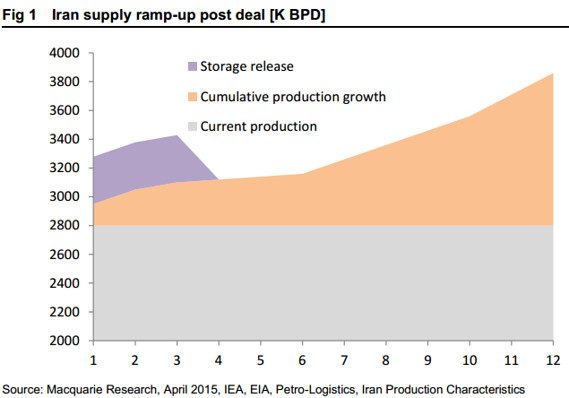

Oil speculators are buying options contracts that will only pay out if crude drops to as low as $15 a barrel next year, the latest sign some investors expect an even deeper slump in energy prices. The bearish wagers come as OPEC’s effective scrapping of output limits, Iran’s anticipated return to the market and the resilience of production from countries such as Russia raise the prospect of a prolonged global oil glut. “We view the oversupply as continuing well into next year,” Jeffrey Currie, head of commodities research at Goldman Sachs Group Inc., wrote in a note on Tuesday, adding there’s a risk oil prices would fall to $20 a barrel to force production shutdowns if mild weather continues to damp demand.

The bearish outlook has prompted investors to buy put options – which give them the right to sell at a predetermined price and time – at strike prices of $30, $25, $20 and even $15 a barrel, according to data from the New York Mercantile Exchange and the U.S. Depository Trust & Clearing. West Texas Intermediate, the U.S. benchmark, is currently trading at about $36 a barrel. The data, which only cover options deals that have been put through the U.S. exchange or cleared, is viewed as a proxy for the overall market and volumes have increased this week as oil plunged. Investors can buy options contracts in the bilateral, over-the-counter market too. Investors have bought increasing volumes of put options that will pay out if the price of WTI drops to $20 to $30 a barrel next year, the data show. The largest open interest across options contracts – both bullish and bearish – for December 2016 is for puts at $30 a barrel.

US banks face the prospect of tougher stress tests next year because of their exposure to oil in a sign of how the falling price of crude is transforming the outlook not just for energy companies but the financial sector. OPEC on Wednesday lowered its long-term estimates for oil demand and said the price of crude would not return to the level it reached last year, at $100 a barrel, until 2040 at the earliest. In its World Oil Outlook it said energy efficiency, carbon taxes and slower economic growth would affect demand. Crude oil’s price on Tuesday hit an 11-year low below $36, piling further pressure on banks that have large loans to energy companies or significant exposure to oil on their trading books.

The US Federal Reserve subjects banks with at least $50bn in assets, including the US arms of foreign banks, to an annual stress test, that is designed to ensure they could keep trading through a deep recession and a big shock to the financial system. Today’s oil prices are about 55% below their level when the Fed set last year’s stress test scenarios in October 2014. That test included looking at how banks’ trading books would fare if there was a one-off 68% fall in oil prices sometime before the end of 2017. Banks’ loan books were not tested against falls in oil prices. Banks including Wells Fargo have recently spoken about the dangers of low oil prices that could make exploration companies and oil producers unable to pay their loans.

There are now five times as many oil and gas loans in danger of default to the oil and gas sector as there were a year ago, a trio of US regulators warned in November. Michael Alix, who leads PwC’s financial services risk consulting team in New York, warned the price of oil would weigh much more heavily on the assessors when drawing up next year’s bank stress tests. “It would test those institutions [banks] for both the direct effects [of oil price falls] on their oil or commodity trading business but importantly the indirect effects [of] lending to energy companies, lending in areas of the country that are more dependent on energy companies and energy-related revenues.”

The Grinch nearly stole Christmas in the oil patch this year. Thanks to the lowest crude and natural gas prices in more than a decade, Norwegian oil and natural gas producer Statoil cut its holiday party budget by about 40% from 2014. KBR Inc. and Marathon Oil opted for smaller affairs with less swank. One Houston hotel said its seasonal party business is down 25% from 2014. Pricey wine and champagne are off the menu. The industry has shed more than 250,000 jobs and idled more than 1,000 rigs as crude prices fell by more than half since last year. Oil services, drilling and supply companies are bearing the brunt of the downturn and account for more than three quarters of the layoffs, according to industry consultant Graves & Co. “You can’t have a $2 million Christmas party while at the same time laying off half your workforce,” said Jordan Lewis at Sullivan Group, a Houston event planning company.

Independent power generators have also been stung by cheap electricity amid declining gas prices. The heating and power plant fuel slid recently to the lowest level since 1999, and is heading for the biggest annual drop since 2006 as the lack of demand leaves stockpiles at a seasonal record. The commodity rout and the layoffs that followed have dampened holiday festivities. Several hundred Statoil employees were invited earlier this month to Minute Maid Park, where Major League Baseball’s Houston Astros play, for a party that featured scaled back entertainment and décor, spokesman Peter Symons said. At the Houston-based oil and gas construction firm KBR, management canceled this year’s companywide party. Instead, individual departments were encouraged to hold their own gatherings from potlucks to group socials, spokeswoman Brenna Hapes said.

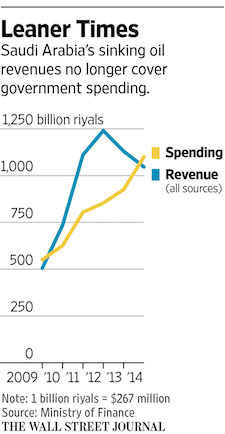

The drastic slide in global crude prices is expected to force Saudi Arabia, the world’s leading oil exporter, to slash spending and cut back on the billions of dollars it spends on generous benefits for its citizens in next year’s budget. The oil-rich kingdom spent hundreds of billions of dollars at home in the past decade to bolster its economy and dole out subsidies that provide cheap energy and food for its 30 million people, as it enjoyed years of high crude prices. But the price of oil has fallen by more than half since the middle of last year, forcing the government to dip into reserves, reassess its spending plans and look for ways to diversify sources of revenue. “I’m worried that prices would go up,” said a man waiting for his SUV to be filled in a gas station in northern Riyadh this week.

“There is a lot of talk but I think the government has put this into account,” he said, adding that he expects the increase in prices to be small. Saudi Arabia exports about seven million barrels of oil a day and those revenues make up around 90% of the government’s fiscal revenues, and around 40% of the country’s overall gross domestic product. Saudi Arabia sees the need to cut output to boost prices but so far has been reluctant to do it alone. Officials say that preserving the country’s share of the global market is more important. The 2016 budget, expected to be unveiled in the coming days, will be the first major opportunity for the government to publicly outline a strategy to cope with a prolonged period of cheap oil and soothe the nerves of both the public and investors in the Middle East’s largest economy.

It isn’t clear whether ambitious and sensitive policy changes—such as privatizations and the cutting of energy subsidies—will be included. But even if energy subsidies are cut, the government is unlikely to immediately target consumers, who have become accustomed to some of the lowest gas prices in the world. Any reduction would risk a backlash from the public. “My expectation is that it will start gradually, and that it will target non-consumers first,” said Fahad Alturki, chief economist at Riyadh-based firm Jadwa Investment, of potential subsidy cutbacks. “We won’t see a radical change….The change will be gradual, with a clear road map—and it may not be part of the budget.”

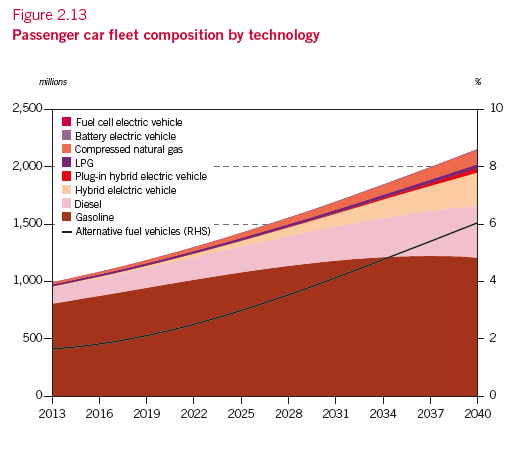

Ambrose is the posterchild for techno-happy. The thinking is that all it takes is for a lot of money to be thrown at the topic. Mind you, the projection is for the number of cars to double in 25 years. That is a disaster no matter what powers the cars. The magic word is ‘grid-connected vehicles’, but that grid would then have to expand, what, 4-fold?

OPEC remains defiant. Global reliance on oil and gas will continue unchanged for another quarter century. Fossil fuels will make up 78pc of the world’s energy in 2040, barely less than today. There will be no meaningful advances in technology. Rivals will sputter and mostly waste money. The old energy order is preserved in aspic. Emissions of CO2 will carry on rising as if nothing significant had been agreed in a solemn and binding accord by 190 countries at the Paris climate summit. OPEC’s World Oil Outlook released today is a remarkable document, the apologia of a pre-modern vested interest that refuses to see the writing on the wall. The underlying message is that the COP21 deal is of no relevance to the oil industry. Pledges by world leaders to drastically alter the trajectory of greenhouse gas emissions before 2040 – let alone to reach total “decarbonisation” by 2070 – are simply ignored.

Global demand for crude oil will rise by 18m barrels a day (b/d) to 110m by 2040. The cartel has shaved its long-term forecast slightly by 1m b/d, but this is in part due to weaker economic growth. One is tempted to compare this myopia to the reflexive certainties of the 16th Century papacy, even as Erasmus published in Praise of Folly, and Luther nailed his 95 Theses to the door of Wittenberg’s Castle Church. The 407-page report swats aside electric vehicles with impatience. The fleet of cars in the world will rise from 1bn to 2.1bn over the next 25 years – topping 400m in China – and 94pc will still run on petrol and diesel. “Without a technology breakthrough, battery electric vehicles are not expected to gain significant market share in the foreseeable future,” it said. Electric cars cost too much. Their range is too short. The batteries are defective in hot or cold conditions.

OPEC says battery costs may fall by 30-50pc over the next quarter century but doubts that this will be enough to make much difference, due to “consumer resistance”. This is a brave call given that Apple and Google have thrown their vast resources into the race for plug-in vehicles, and Tesla’s Model 3s will be on the market by 2017 for around $35,000. Ford has just announced that it will invest $4.5bn in electric and hybrid cars, with 13 models for sale by 2020. Volkswagen is to unveil its “completely new concept car” next month, promising a new era of “affordable long-distance electromobility.” The OPEC report is equally dismissive of Toyota’s decision to bet its future on hydrogen fuel cars, starting with the Mirai as a loss-leader. One should have thought that a decision by the world’s biggest car company to end all production of petrol and diesel cars by 2050 might be a wake-up call.

Goldman Sachs expects ‘grid-connected vehicles’ to capture 22pc of the global market within a decade, with sales of 25m a year, and by then – it says – the auto giants will think twice before investing any more money in the internal combustion engine. Once critical mass is reached, it is not hard to imagine a wholesale shift to electrification in the 2030s. Goldman is betting that battery costs will fall by 60pc over the next five years, driven by economies of scale as much as by technology. The driving range will increase by 70pc. This is another world from OPEC’s forecast.

Kazakhstan’s $55 billion sovereign-wealth fund helped pull the country through the global financial crisis and offered funding for the country’s bid to host the 2022 Winter Olympics. But the collapse in oil prices has hit Kazakhstan and its fund, Samruk-Kazyna JSC, hard. In October, the fund borrowed $1.5 billion in its first syndicated loan to help a cash-strapped subsidiary saddled with a troubled oil-field investment. “Our oil company lost lots of its revenues,” says the fund’s chief executive, Umirzak Shukeyev. “Currently, we are trying to adjust to the situation.” Funds like Samruk are at a critical juncture. For years, sovereign-wealth funds—financial vehicles owned by governments—swelled in size and number, fueled by rising oil prices and leaders’ aspirations to increase economic growth, invest abroad and boost political influence.