DPC Near Lewiston, Minnesota – The Pulpit. 1899

Nice attempt by Haque, but no, some kind of ‘leadership’ would not solve our problems.

• The Beginning of the End of the World (Umair Haque)

The beginning of the end of the world means that yesterday’s model of prosperity – let’s call it capitalist liberal democracy – has reached its limits. It is like an aging machine that shudders and backfires more violently and regularly, because it is broken. And yet, we are unsure, as a world, where to go next.

Let’s take it in four levels. At the macro level, liberal capitalism’s a set of agreements and institutions. These agreements are being torn up, rejected, abandoned. Witness Brexit. The world is left in a state of void, just as the UK is now. Let me try to translate that: there is not a single leader in the world today who appears to have a vision for a stagnant global economy. The kind of great and radical vision that Keynes, Marshall, JFK had. Maybe we don’t agree with the vision – but what is important is that are visions to discuss, debate, inspire, cohere, lead. That level of vision is missing when it is most badly needed. Without such a vision, what happens?

A void of vision, leadership, direction to fix any of the existential threats of inequality, fragility, insecurity, at the global level inevitably means social discontent, decay, decline. Why be a part of societies and unions that step on your future? The beginning of the end of the world at the social level means: entire societies are beginning to fracture. As they fracture, so there is a return to tribalism, dynasty, feudal and authoritarian ways of ordering society. You don’t have to look much further than the US election to see it. In the void of democracy, feudalism is the darkness, and fascism is midnight. What happens when societies begin to splinter and fracture, regress and decline?

At the institutional level, the level of corporations and organisations, the end of the world means that there is now an even more severe power imbalance. Institutions hold far more power than relatively powerless, ossified, fractured states. And they exercise it. They set the terms and define the rules of trade, freedom, work, reward. What does that mean for people? At the personal level, the end of the world is already here. This is the first generation in modern history that’s going to suffer worse living standards than their parents. The question is: how much worse? Very badly worse. With stagnant incomes, no savings, this generation will never retire, vacation, advance, enjoy, or own. Their relationships, health, and productivity will suffer as a result. The quality of their lives is going to be long, bleak, and pointless. Worked to the grave to make a dwindling number of dynasties wealthy, largely by serving them hand and foot, not really enhancing human life.

Tyler presents inequality as the catch, but the -admittedly related- asset bubble is a much bigger one.

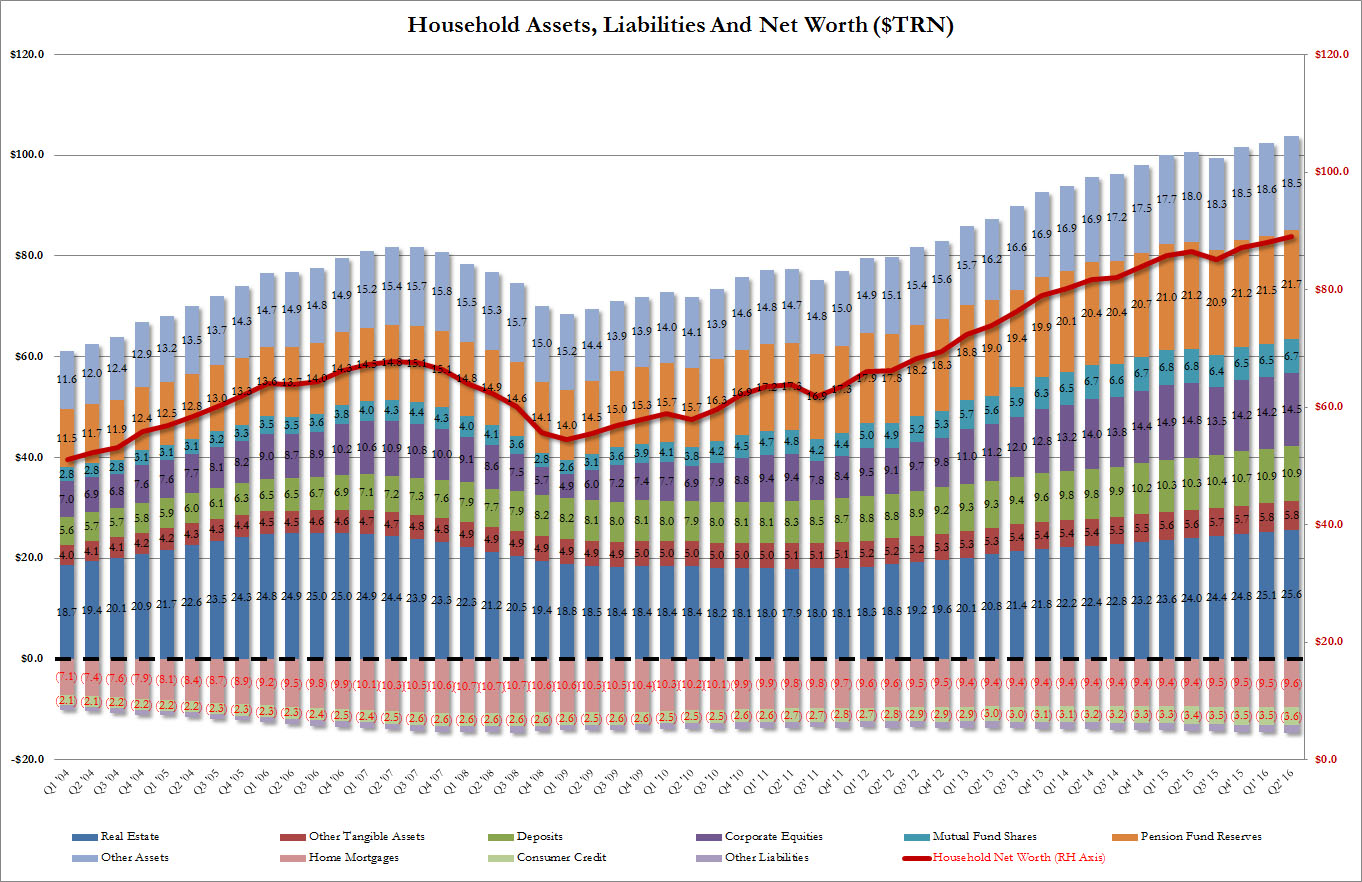

• US Household Net Worth Hits Record $89 Trillion, But There’s A Catch (ZH)

As part of its quarterly Flow of Funds update, earlier today the Fed released snapshot of the US “household” sector as of June 30. What it revealed is that with $103.8 trillion in assets and a modest $14.7 trillion in liabilities, the net worth of the average US household rose to a new all time high of $89.1 trillion, up $1.1 trillion as a result of an estimated $474 billion increase in real estate values, and mostly $750 billion increase in various stock-market linked financial assets like corporate equities, mutual and pension funds. Household borrowing rose at a 4.4% annual rate, with total household liabilities grew growing by $200 billion from $14.5 trillion to $14.7 trillion, the bulk of which was $9.6 trillion in home mortgages. The breakdown of the total household balance sheet as of Q2 is shown below.

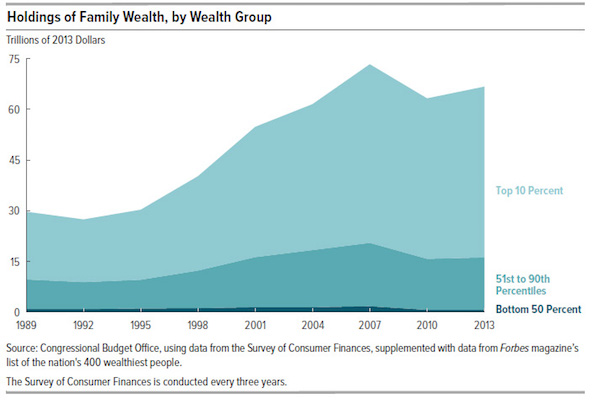

And while it would be great news if wealth across America had indeed risen as much as the chart above shows, the reality is that there is a big catch: as shown previously, virtually all of the net worth, and associated increase thereof, has only benefited a handful of the wealthiest Americans. As a reminder, from the CBO’s latest Trends in Family Wealth analysis, here is a breakdown of the above chart by wealth group, which sadly shows how the “average” American wealth is anything but. While the breakdown has not caught up with the latest data, it provides an indicative snapshot of who benefits.

Here is how the CBO recently explained the wealth is distributed: In 2013, families in the top 10% of the wealth distribution held 76% of all family wealth, families in the 51st to the 90th %iles held 23%, and those in the bottom half of the distribution held 1%. Average wealth was about $4 million for families in the top 10% of the wealth distribution, $316,000 for families in the 51st to 90th%iles, and $36,000 for families in the 26th to 50th %iles. On average, families at or below the 25th %ile were $13,000 in debt.

Maybe Draghi and Kuroda can buy them all.

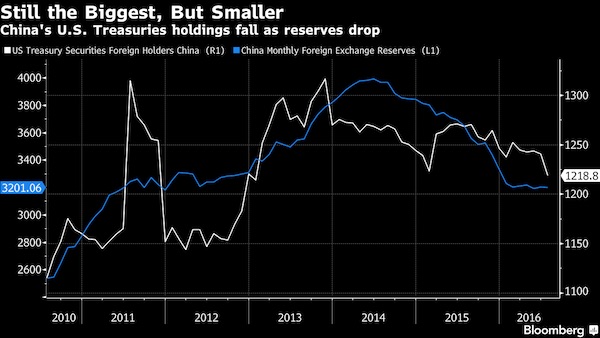

• China’s Holdings of US Treasuries Fall to Lowest Since 2013 (BBG)

China’s holdings of U.S. Treasuries fell in July to the lowest level in more than three years, as the world’s second-largest economy pares its foreign-exchange reserves to support the yuan. The biggest foreign holder of U.S. government debt had $1.22 trillion in bonds, notes and bills in July, down $22 billion from the prior month, in the biggest drop since 2013, according to U.S. Treasury Department data released Friday in Washington and previous figures compiled by Bloomberg. The portfolio of Japan, the largest holder after China, rose $6.9 billion to $1.15 trillion. Saudi Arabia’s holdings of Treasuries declined for a sixth straight month, to $96.5 billion.

The figures compare with official Chinese data showing that the nation’s foreign-exchange reserves were little changed in July at $3.2 trillion, though they’re down from a peak of close to $4 trillion in 2014. The reserves dropped $16 billion in August to the lowest level since 2011. The report, which also contains data on international capital flows, showed net foreign buying of long-term securities totaling $103.9 billion in July. It showed a total cross-border inflow, including short-term securities such as Treasury bills and stock swaps, of $140.6 billion. Net foreign selling of U.S. Treasuries was $13.1 billion in July, while foreigners scooped up a net $26.1 billion in equities, $20.7 billion of corporate debt and $38.9 billion in agency debt, according to the report.

Stockman knows what he’s talking about on this issue, far more than most. Not perfect, but useful.

• Trump’s Economic Plan: Some Decent Ideas, Lots Of Really Bad Fiscal Math (DS)

[..] the Reagan White House—me included – fell for the theory of “dynamic scoring” and that the big cuts in the income tax rates would partially pay for themselves via revenue “flowback”. Back in those days the latter was expressed in an economic forecast known as Rosy Scenario, which assumed that in response to the supply side tax cuts, the US economy would get up on its hind legs and leap forward at a real GDP growth rate of more than 4% per year, and as far as the eye could see. What happened instead, of course, is that the US economy plunged into the drink of the deep 1982 recession and the Federal deficit soared to 5% of GDP—a truly shocking outcome back in those innocent days when the old-time fiscal religion still had roots inside the beltway.

And it would have also caused enormous economic havoc had not the Gipper’s advisors—me included—talked him to signing three tax bills over 1982-1984 that recaptured roughly 40% of the revenue loss from his cherished tax cuts. Even then, the public debt grew by 250% during Reagan’s eight years – or by more than under any peacetime President in American history. Yet even to this day the GOP politicians and their economic advisers profess a case of heavy duty amnesia about what happened, claiming that real GDP grew by upwards of 4.5% and that these results were proof positive that “dynamic scoring” of tax cuts is valid.

Worse still, they appear to have convinced Donald Trump of this same fallacious revisionist history because it was embedded at the core of the Thursday speech’s fiscal math. To wit, Trump claimed that $2.6 trillion or 60% of the revenue loss from his $4.4 trillion tax cut would be recouped by, yes, 4% economic growth as far as the eye can see.

As Merkel pushes back.

• US Is Investigating Bosch in Widening VW Diesel-Cheat Scandal (BBG)

U.S. prosecutors are investigating whether Germany’s Robert Bosch, which provided software to Volkswagen, conspired with the automaker to engineer diesel cars that would cheat U.S. emissions testing, according to two people familiar with the matter. Among the questions the Justice Department is asking in the criminal probe, one of them said, is whether automakers in addition to VW used Bosch software to skirt environmental standards. Bosch, which is also under U.S. civil probe and German inquiry, is cooperating in investigations and can’t comment on them, said spokesman Rene Ziegler.

The line of inquiry broadens what is already the costliest scandal in U.S. automaking history. VW faces an industry-record $16.5 billion, and counting, in criminal and civil litigation fines after admitting last year that its diesel cars were outfitted with a “defeat device” that lowered emissions to legal levels only when it detected the vehicle was being tested. More than a half dozen big manufacturers sell diesel-powered vehicles in the U.S. The people familiar with the matter declined to say whether specific makers are under scrutiny. A second supplier may also be part of the widening probe: When prosecutors in Detroit outlined their case last week against a VW engineer who pleaded guilty to conspiracy in the matter, they said he had help from a Berlin-based company that is 50% owned by Volkswagen, described as “Company A” in a court filing. That company, according to a another person familiar with the matter, is IAV, which supplies VW and other automakers.

“..the data told them to…”

• Why the Fed Destroyed the Market Economy (Gordon)

Kashkari’s a man with crazy eyes. But he’s also a man with even crazier ideas. After stating that politics is not part of presidential election year Fed policy, Kashkari explained how Fed policy is set. “We look at the data,” he said. In hindsight, this clarification was more revealing than the initial denial. Clearly, Kashkari’s never thought about what exactly it is he’s looking at when looking at the data. If he had, he’d likely conclude that the approach of using data to identify apparent aggregate demand insufficiencies and perceived supply gluts is crazy. Unemployment. GDP. Price inflation. These data points are all fabricated and fudged to the government number crunchers’ liking. What’s more, for each headline number there are a list of footnotes and qualifiers. Hedonic price adjustments. Price deflators. Seasonal adjustments. Discouraged worker disappearances. These subjective adjustments greatly affect the results.

Yet what’s even crazier is that Kashkari believes that by finagling around with the price of money the Fed can improve the outputs of their bogus data. According to central planners, better data – i.e. higher GDP, greater consumer demand, 2% inflation – means a better economy. But after 100-years of mismanagement, the last eight being in the radically extreme, the Fed has scored a big fat rotten tomato. The data still stinks – GDP’s still anemic. But the downside of their actions is downright putrid. Policy makers have pushed public and private debt well past their serviceable limits. They’ve debased the dollar to less than 5% of its former value and propagated bubbles and busts in real estate, stock markets, emerging markets, mining, oil and gas, and just about every other market there is. Aside from enriching private bankers, we now know the answer to why the Fed destroyed the market economy. According to Kashkari, the data told them to.

“..a former French finance minister who has more than a passing knowledge of the debt crisis in the country formerly known as Greece..”

• IMF’s Lagarde: Big Salary, Big Ideas (TO Sun)

You probably didn’t get invited to the International Forum of the Americas conference held in Toronto this week. Neither did I. Just as well. From $700 for a “regular” one-day pass to $3,500 for an “executive club” three-day pass, the croissants and coffee must have been vastly superior to the fare at Tim Hortons. We both missed the opportunity to hear Christine Lagarde, the managing director of the IMF, pontificate on the rise of protectionist political rhetoric in the developed world. Lagarde drew criticism for praising Prime Minister Justin Trudeau’s fiscal plan from my friends Tony Clement, who’s in the running for the leadership of the federal Conservatives and Lisa Raitt, who hasn’t yet said whether she will run. Lagarde commented that she hoped Trudeau’s fiscal approach of spend now, pay later would go viral.

It’s an interesting take on how to build a strong, national economy, particularly from a former French finance minister who has more than a passing knowledge of the debt crisis in the country formerly known as Greece. The IMF has been intricately involved in the economic and political meltdown of Greece and, early in her tenure as managing director, Lagarde raised hackles by agreeing Greeks had “had a nice time” but it was now “payback time”. It’s hard to square the gap between praising Trudeau for “stimulus” spending and borrowing, while criticizing Greeks for not paying their way.

[..] I found Lagarde’s comments on the protectionist political wave sweeping over much of the developed world more interesting, and unintentionally, insightful. I had the pleasure of hearing her speak at a forum in New York. She is intelligent, informed and opinionated, all things I like. She’s also an elite, globe-traveling bureaucrat with a $500,000 tax-free salary and an expense account commensurate with a lifestyle unrecognizable to average folk. From her lofty, enlightened position Lagarde offered that blue-collar workers in developed countries should be offered educational opportunities. Apparently that will help them adjust to factory closings.

The author was a cabinet minister in the Conservative government of Ontario premier Mike Harris from 1995 to 2002.

Barton Gellman takes down an idiot report.

• House Intelligence Committee’s Terrible, Horrible, Very Bad Snowden Report (TCF)

Since I’m on record claiming the report is dishonest, let’s skip straight to the fourth section. That’s the one that describes Snowden as “a serial exaggerator and fabricator,” with “a pattern of intentional lying.” Here is the evidence adduced for that finding, in its entirety.

“He claimed to have left Army basic training because of broken legs when in fact he washed out because of shin splints.” This is verifiably false for anyone who, as the committee asserts it did, performs a “close review of Snowden’s official employment records.” Snowden’s Army paperwork, some of which I have examined, says he met the demanding standards of an 18X Special Forces recruit and mustered into the Army on June 3, 2004. The diagnosis that led to his discharge, on crutches, was bilateral tibial stress fractures.

“He claimed to have obtained a high school degree equivalent when in fact he never did.” I do not know how the committee could get this one wrong in good faith. According to the official Maryland State Department of Education test report, which I have reviewed, Snowden sat for the high school equivalency test on May 4, 2004. He needed a score of 2250 to pass. He scored 3550. His Diploma No. 269403 was dated June 2, 2004, the same month he would have graduated had he returned to Arundel High School after losing his sophomore year to mononucleosis. In the interim, he took courses at Anne Arundel Community College.

“He claimed to have worked for the CIA as a ‘senior advisor,’ which was a gross exaggeration of his entry-level duties as a computer technician.” Judge for yourself. Here are the three main roles Snowden played at the Central Intelligence Agency (CIA). (1) His entry level position, as a contractor, was system administrator (one among several) of the agency’s Washington metropolitan area network. (2) After that he was selected for and spent six months in training as a telecommunications information security officer, responsible for all classified technology in U.S. embassies overseas. The CIA deployed him to Geneva under diplomatic cover, complete with an alias identity and a badge describing him as a State Department attache. (3) In his third CIA job, the title on his Dell business card was “solutions consultant / cyber referent” for the intelligence community writ large—the company’s principal point of contact for cyber contracts and proposals. In that role, Snowden met regularly with the chiefs and deputy chiefs of the CIA’s technical branches to talk through their cutting edge computer needs.

“He also doctored his performance evaluations…” Truly deceptive, this. I will tell the story in my book. Suffice to say that Snowden discovered and reported a security hole in the CIA’s human resources intranet page. With his supervisor’s permission, he made a benign demonstration of how a hostile actor could take control. He did not change the content of his performance evaluation. He changed the way it displayed on screen.

But they control.

• Western Media Credibility In Free Fall Collapse (Paul Craig Roberts)

The latest from the Gallup Poll is that only 32% of Amerians trust the print and TV media to tell the truth. Republicans, 18 to 49 year old Americans, and independents trust the media even less, with trust rates of 14%, 26%, and 30%. The only group that can produce a majority that still trusts the media are Democrats with a 51% trust rate in print and TV reporting. The next highest trust rate is Americans over 50 years of age with a trust rate of 38%. The conclusion is that old people who are Democrats are the only remaining group that barely trusts the media. This mistaken trust is due to their enculturation. For older Democrats belief in government takes the place of Republican belief in evangelical Christianity.

Older Democrats are firm believers that it was government under the leadership of President Franklin D. Roosevelt that saved America from the Great Depression. As the print and TV media in the 21st century are firmly aligned with the government, the trust in government spills over into trust of the media that is serving the government. As the generation of Democrats enculturated with this mythology die off, Democratic trust rates will plummet toward Republican levels. It is not difficult to see why trust in the media has collapsed. The corrupt Clinton regime, which we might be on the verge of repeating, allowed a somewhat diverse and independent media to be 90% acquired by six mega-corporations. The result was the disappearance of independence in reporting and opinion.

The constraints that corporate ownership and drive for profits put on journalistic freedom and resources reduced reporting to regurgitations of government and corporate press releases, always the cheapest and uncontroversial way to report. With journalistic families driven out of journalism by estate taxes, the few remaining newspapers become acquisitions like a trophy wife or a collector Ferrari. Jeff Bezos, CEO and founder of amazon.com, handed over $250 million in cash for the Washington Post. Jeff might be a whiz in e-commerce, but when it comes to journalism he could just as well be named Jeff Bozo.

Taleb’s been tweeting on this for a long time. Wonder if he’s read Ivan Illich’s work on institutionalism.

• The Intellectual Yet Idiot (Taleb)

The Intellectual Yet Idiot is a production of modernity hence has been accelerating since the mid twentieth century, to reach its local supremum today, along with the broad category of people without skin-in-the-game who have been invading many walks of life. Why? Simply, in most countries, the government’s role is between five and ten times what it was a century ago (expressed in%age of GDP). The IYI seems ubiquitous in our lives but is still a small minority and is rarely seen outside specialized outlets, think tanks, the media, and universities – most people have proper jobs and there are not many openings for the IYI. Beware the semi-erudite who thinks he is an erudite. He fails to naturally detect sophistry.

The IYI pathologizes others for doing things he doesn’t understand without ever realizing it is his understanding that may be limited. He thinks people should act according to their best interests and he knows their interests, particularly if they are “red necks” or English non-crisp-vowel class who voted for Brexit. When Plebeians do something that makes sense to them, but not to him, the IYI uses the term “uneducated”. What we generally call participation in the political process, he calls by two distinct designations: “democracy” when it fits the IYI, and “populism” when the plebeians dare voting in a way that contradicts his preferences. While rich people believe in one tax dollar one vote, more humanistic ones in one man one vote, Monsanto in one lobbyist one vote, the IYI believes in one Ivy League degree one-vote, with some equivalence for foreign elite schools, and PhDs as these are needed in the club.

More socially, the IYI subscribes to The New Yorker. He never curses on twitter. He speaks of “equality of races” and “economic equality” but never went out drinking with a minority cab driver. Those in the U.K. have been taken for a ride by Tony Blair. The modern IYI has attended more than one TEDx talks in person or watched more than two TED talks on Youtube. Not only will he vote for Hillary Monsanto-Malmaison because she seems electable and some other such circular reasoning, but holds that anyone who doesn’t do so is mentally ill. The IYI has a copy of the first hardback edition of The Black Swan on his shelves, but mistakes absence of evidence for evidence of absence. He believes that GMOs are “science”, that the “technology” is not different from conventional breeding as a result of his readiness to confuse science with scientism.

Everyone should read this. And then realize that Russia in not a threat to us.

• The Existential Madness of Putin-Bashing (Robert Parry)

the United States dispatched financial “experts” – many from Harvard Business School – who arrived in Moscow with neoliberal plans for “shock therapy” to “privatize” Russia’s resources, which turned a handful of corrupt insiders into powerful billionaires, known as “oligarchs,” and the “Harvard Boys” into well-rewarded consultants. But the result for the average Russian was horrific as the population experienced a drop in life expectancy unprecedented in a country not at war. While a Russian could expect to live to be almost 70 in the mid-1980s, that expectation had dropped to less than 65 by the mid-1990s.

The “Harvard Boys” were living the high-life with beautiful women, caviar and champagne in the lavish enclaves of Moscow – as Yeltsin drank himself into stupors – but there were reports of starvation in villages in the Russian heartland and organized crime murdered people on the street with near impunity. Meanwhile, Presidents Bill Clinton and George W. Bush cast aside any restraint regarding Russia’s national pride and historic fears by expanding NATO across Eastern Europe, including the incorporation of former Soviet republics. In the 1990s, the “triumphalist” neocons formulated a doctrine for permanent U.S. global dominance with their thinking reaching its most belligerent form during George W. Bush’s presidency, which asserted the virtually unlimited right for the United States to intervene militarily anywhere in the world regardless of international law and treaties.

Without recognizing the desperation and despair of the Russian people during the Yeltsin era – and the soaring American arrogance in the 1990s – it is hard to comprehend the political rise and enduring popularity of Vladimir Putin, who became president after Yeltsin abruptly resigned on New Year’s Eve 1999. (In declining health, Yeltsin died on April 23, 2007). Putin, a former KGB officer with a strong devotion to his native land, began to put Russia’s house back in order. Though he collaborated with some oligarchs, he reined in others by putting them in jail for corruption or forcing them into exile.

Putin cracked down on crime and terrorism, often employing harsh means to restore order, including smashing Islamist rebels seeking to take Chechnya out of the Russian Federation. Gradually, Russia regained its economic footing and the condition of the average Russian improved. By 2012, Russian life expectancy had rebounded to more than 70 years. Putin also won praise from many Russians for reestablishing the country’s national pride and reasserting its position on the world stage.

Why?

• Russia Says US Refuses To Share Syria Truce Deal With UN Council (R.)

Russia said on Friday that a U.N. Security Council endorsement of a Syria ceasefire deal between Moscow and Washington appeared unlikely because the United States does not want to share the documents detailing the agreement with the 15-member body. Russian U.N. Ambassador Vitaly Churkin and U.S. Ambassador Samantha Power had been due to brief the council behind closed-doors on Friday but that was canceled at the last minute. “The main problem … which in my mind makes it impossible to produce any resolution, is that they are refusing to give those documents to members of the Security Council or even to read those documents to the members of the Security Council,” Churkin told reporters.

“We believe that we cannot ask them (council members) to support documents which they haven’t seen,” said Churkin, suggesting there was lack of unity in U.S. President Barack Obama’s administration toward the agreement. The U.S. mission to the United Nations said it could not agree with Russia on a way to brief the council that would “not compromise the operational security of the arrangement.” [..] Churkin said Russia has given two drafts of a possible Security Council resolution to the United States. He said on Thursday that Moscow hoped a resolution could be adopted next week during the annual U.N. gathering of world leaders. “They, in their typical way, came up with a completely different thing, which is trying to interpret and reinterpret the agreement,” Churkin said, referring to U.S. officials.