Arthur Rothstein Migratory fruit pickers’ camp in Yakima, Washington Jul 1936

Right back to the poisoned chalice I wrote about on the morning of election day.

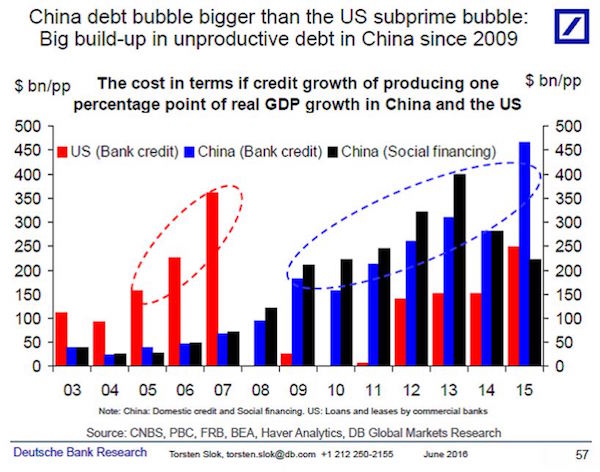

• Trumponomics Will Collapse Under a Mountain of Debt (Stockman)

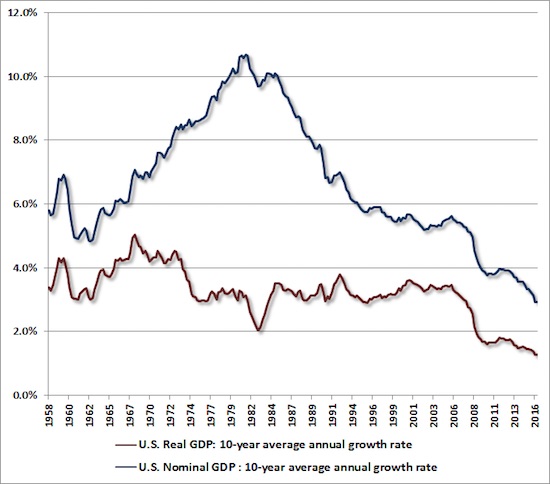

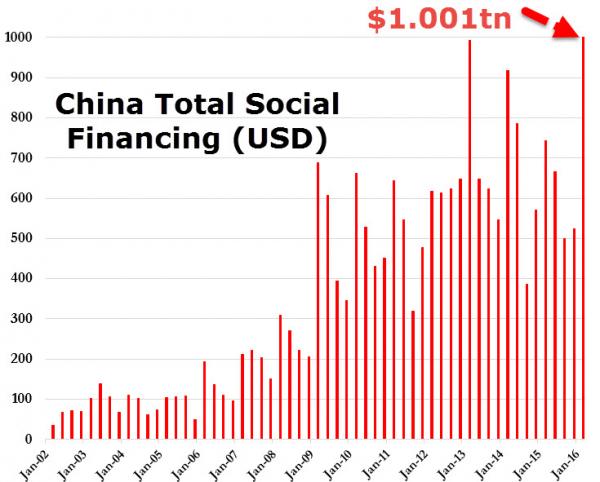

Financial markets are heading straight into a perfect storm of central bank failure, bond market carnage, a worldwide recession and a spectacular fiscal bloodbath in Washington. Investors should be heading for the hills with all deliberate speed. What is going to stop Trumponomics cold is debt — roughly $64 trillion of it. That’s what is crushing the American economy, and until the mechanics of its relentless growth are stopped and reversed, the odds of achieving and sustaining the 3–4% real economic growth that Trump’s economics team is yapping about is somewhere between slim and none. Here’s the newsflash. The nation’s monumental debt problem wasn’t newly created by the Obama Administration or the fact that Nancy Pelosi never met a spending program she couldn’t embrace.

The last eight years have surely made the problem far worse and the Democrats are culpable without question. But quite frankly the debt problem is a thoroughly bipartisan creation that is completely immune to the fact that the White House and both sides of Capitol Hill are now under GOP control. In fact, the nation’s debt affliction actually goes back to August 1971 when Nixon closed the gold window and launched the world on the current destructive experiment with massive central bank driven credit expansion. However, it was after 1980 that the wraps really started coming off the debt monster that was spawned by the world’s unshackled central banks. In that context, Paul Volcker was the last honest central banker, and with Ronald Reagan’s acquiescence he did break the back of the virulent commodity and consumer goods inflation that had been unleashed by his immediate predecessors during the 1970s.

Yet Volcker’s great handiwork was for naught because of two other developments – the breakdown of fiscal rectitude and the final destruction of sound money by Alan Greenspan – that also occurred on the Gipper’s watch. In fact, the gigantic Reagan deficits — which nearly tripled the national debt from $930 billion to $2.7 trillion during his eight years in office — is exactly what led Greenspan to crank up the printing press at the Fed after the stock market crash in October 1987.

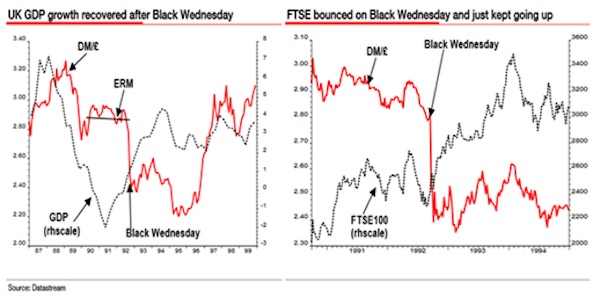

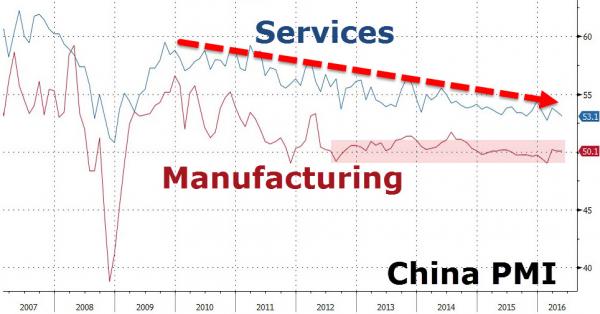

What Stockman said, but now in a graph.

• Shiller CAPE Ratio Signals ‘Overvaluation On A Very Grand Scale’ (CNBC)

While the S&P 500 is reaching all-time highs on optimism over Donald Trump’s economic agenda, some Wall Street strategists are increasingly worried about a widely followed valuation measure that’s reached levels that preceded most of the major market crashes of the last 100 years. “The cyclically adjusted P/E (CAPE), a valuation measure created by economist Robert Shiller now stands over 27 and has been exceeded only in the 1929 mania, the 2000 tech mania and the 2007 housing and stock bubble,” Alan Newman wrote in his Stock Market Crosscurrents letter at the end of November. Newman said even if the market’s earnings increase by 10% under Trump’s policies “we’re still dealing with the same picture,.”

The Shiller “cyclically adjusted price-to-earnings ratio” (CAPE) is calculated using price divided by the index’s average historical 10-year earnings, adjusted for inflation. Yale economics professor Robert Shiller’s research found future 10-year stock market returns were negatively correlated to high CAPE ratio readings on a relative basis. He won the Nobel Prize in economics in 2013 for his work on stock market inefficiency and valuations.

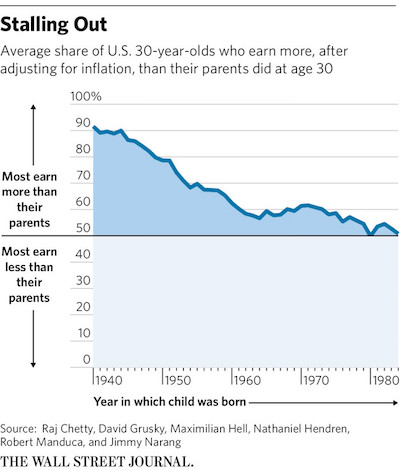

Barely half of US 30-year-olds earn more than their parents did at that age..

• The American Dream Is Fading And May Be Very Hard To Revive (WSJ)

Barely half of 30-year-olds earn more than their parents did at a similar age, a research team found, an enormous decline from the early 1970s when the incomes of nearly all offspring outpaced their parents. Even rapid economic growth won’t do much to reverse the trend. Economists and sociologists from Stanford, Harvard and the University of California set out to measure the strength of what they define as the American Dream, and found the dream was fading. They identified the income of 30-year-olds starting in 1970, using tax and census data, and compared it with the earnings of their parents when they were about the same age. In 1970, 92% of American 30-year-olds earned more than their parents did at a similar age, they found. In 2014, that number fell to 51%.

“My parents thought that one thing about America is that their kids could do better than they were able to do,” said Raj Chetty, a prominent Stanford University economist who emigrated from India at age 9 and is part of the research team. “That was important in my parents’ decision to come here.” Although there are many definitions of the American Dream—the freedom to speak your mind, for instance, or the ability to rise from poverty to wealth—the economists chose a measure that they said was possible to define precisely. The percentage of young adults earning more than their parents dropped precipitously from 1970 to about 1992, to 58%, found Mr. Chetty et al.

Draghi says two or more completely contradictory things all in one breath. It’s what they pay him the big bucks for.

• Europe’s Comfort Blanket Is Being Pulled Away (AEP)

The long-feared moment of bond tapering in the eurozone has arrived. The comfort blanket is being pulled away – gently – for the first time since the region first crashed into a debt crisis. The ECB has tried to cushion the blow with dovish rhetoric and a glacially slow exit but there is no denying that monetary policy has reached a critical turning point. “The ECB has delivered an unwelcome surprise,” said Luigi Speranza from BNP Paribas. Europe’s incipient tightening has begun just as the US Federal Reserve prepares to raise interest rate next week, probably the first of several rises over the next twelve months as the incoming Trump administration launches a fiscal boom. It comes as China takes action to choke off a property bubble and rein in shadow banking. The world’s three big monetary blocs will all be draining liquidity at the same time.

The ECB will wind down quantitative easing from €80bn to €60bn a month when the current programme expires in March. Societe Generale says that this is just the start, predicting more tapering of €10bn in June, and then further cuts of €10bn at each meeting – a truly drastic outlook. Doves at the ECB warned that it would be dangerous to start any tapering at this delicate juncture, given that there has been no flicker of life in core inflation – still stuck at 0.8pc – and given that imported monetary tightening from the US has already led to a doubling of Italian 10-year yields over the last three months. The doves were over-ruled. It is clear that a German-led bloc on the ECB’s governing council blocked efforts to roll over the existing QE structure for another six months.

Bond purchases will carry on for longer instead. The new €60bn regime will run for nine months until the end of 2017. The ultimate stock of ECB bonds will be higher. You could call it a compromise. But despite appearances – and logical inference – these are not an equivalent forms of stimulus. The stormy saga of bond tapering by the Fed shows that investors react more to the monthly “flow” of QE than they do to the “stock” of bonds held – the balance sheet syndrome that looms large in the theoretical models of central banks. [..] Mario Draghi, the ECB’s president, was at pains to insist that there is no tightening whatsoever coming next year. “The presence of the ECB on the markets will be there for a long time. The key message is that there is no tapering in sight,” he said. Nothing is on auto-pilot and the volume of QE could rise again if need be. “It can go back to €80bn,” he said.

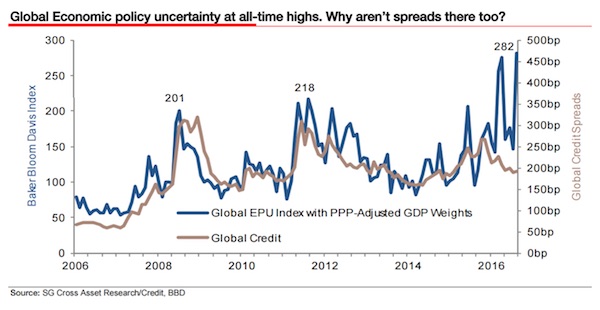

“..a ghoulish quest to harvest bad news with a forceful sweep of my scythe..”

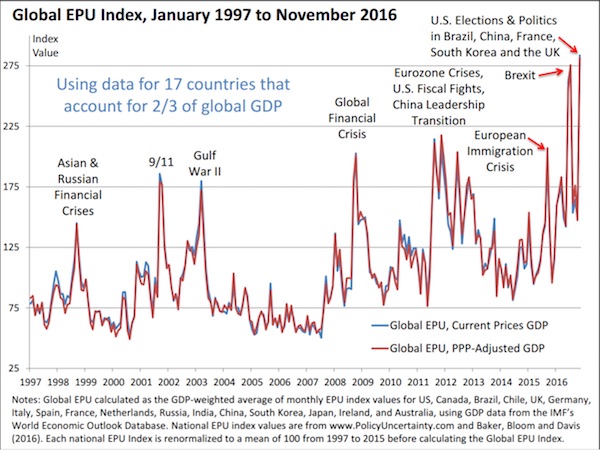

• Albert Edwards’ ‘Most Frightening Chart’ (MW)

Albert Edwards, a global strategist at Société Générale, has been steadily beating the doomsday drum for decades. But despite the perma-bear’s repeated warnings about an impending economic disaster, investors are still likely to take notice when he gleefully shares the “most frightening chart” he’s seen in a while — especially when the stupendous postelection rally in U.S. stocks has stoked fears that a correction might be just around the corner. “I sometimes feel like ‘The Grim Reaper,’ scouring the research savannah in a ghoulish quest to harvest bad news with a forceful sweep of my scythe. Imagine then my perverse delight when our credit team produced what is one of the scariest charts I have seen for a very long time,” writes Edwards in his report. The chart by Guy Stear, head of emerging markets and credit research at Société Générale, shows credit spreads holding steady even as political uncertainty spikes to an unprecedented level.

According to Edwards, that cognitive dissonance is all wrong. “Markets shrugged off the Brexit vote in a couple of days. They shrugged off Donald Trump’s election in a single day. They shrugged off the Italian referendum result in a couple of hours. Heck, in this mood they would shrug off an alien invasion of planet Earth,” he said. “But global political risk is now at such elevated levels that investors must surely be on another planet.” The graph is based on the economic policy uncertainty index developed by three U.S. professors — Scott Baker, Nick Bloom and Steven Davis. This is the original chart that shows the EPU index at 282, significantly above 201 in 2008 and 218 in 2011, two previous periods of panic:

Really?: “If the economy tracks along okay, it might turn out that this thing sorts itself out.”

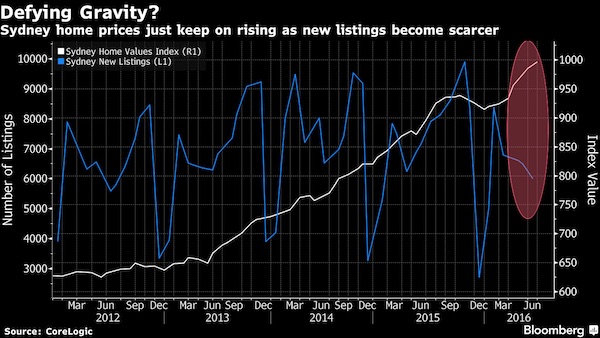

• Australia Property Market Mirrors Tulip Bubble, Says Former Bank CEO (ND)

Australia’s property market now mirrors one of the worst speculative manias in human history, according to a former Commonwealth Bank CEO. In a televised interview that drew little media attention, David Murray warned that the entire economy is “vulnerable” because of overvalued house prices in Sydney and Melbourne. “All the signs of a bubble are there. Many of the signs are the same as the Dutch tulips,” Mr Murray told Sky News on December 1. Starting in 1634, the Dutch bid up the price of tulip bulbs to extraordinarily high levels. Then, in 1637, the price collapsed, turning the craze into a byword for speculative insanity. Since 2009, Sydney dwelling prices have risen by 95% and Melbourne by 85%, according to CoreLogic, a prominent property analysis firm.

Mr Murray, who chaired a recent inquiry into the health of Australia’s financial sector, said we may yet avoid a Dutch-style price plunge. It is a risk, not a certainty. “If the economy tracks along okay, it might turn out that this thing sorts itself out. But when those risks are there, something needs to be done about it in a regulatory sense, and the Reserve Bank and APRA need to stay on it.” In recent years, APRA has imposed tougher lending policies on the big banks, including forcing them to hold more capital as a buffer against mortgage defaults. This was a recommendation made by Mr Murray during his financial sector review. The former bank boss has been warning of a property bubble since at least last year.

The fact that prices in Melbourne and Sydney have not corrected already is a further cause for concern, he said in his latest interview. “When we get a momentum in a market like this, when you get these self-amplifying price spirals, the fact they keep going on and on longer than expected is another sign that it’s not very healthy.” The crash, if it eventuates, would be triggered by a large number of landlords being forced to sell their investment properties all at once, thereby driving down prices, Mr Murray said. “We have more investors in the market than we’ve had historically and those investors typically, even people on lower incomes, own multiple properties and those properties are often collateralised in the system. So they’re the people who become forced sellers, and that’s the risk to the system.”

Now President Mattarella is rumored to have asked Renzi to form a new government?!

• Top Official In Italy’s M5S Increases Call For Referendum On Euro (G.)

A top official in the Italian anti-establishment Five Star Movement (M5S) is ratcheting up his party’s call for a referendum on the euro, signalling that Italy’s possible exit from the single currency could become a central issue in the next election. Alessandro Di Battista, 38, who is a prime contender to represent M5S in the next poll, said in an interview with German newspaper Die Welt that he did not support an exit from the EU but did support a referendum on the euro. “The euro and Europe are not the same thing. We only want for Italians to decide on the currency,” he said. Asked whether the party had considered the repercussions of leaving the euro, which most economists believe would carry big risks for Italy and the global markets, Di Battista said he “understood well the consequences of the introduction of the euro”.

The single currency, he said, had shrunk Italians’ buying power and earnings and caused higher unemployment and “social deprivation”. “If Europe does not want to implode you must accept that you can not go on like this,” he said. M5S’s opposition to the euro is not new, but the remarks are important in the wake of the departure of the centre-left prime minister Matteo Renzi, who submitted his resignation to Sergio Mattarella, the Italian president, on Wednesday evening. Mattarella is meeting the leaders of all the major political parties over the next few days in the hope they can agree on an interim prime minister. Renzi resigned after he was trounced in a referendum on Sunday, with nearly 60% of Italians opposing constitutional reforms he backed. Even if the parties agree on the next prime minister an early election is expected to be called in 2017.

[..] The chances of M5S winning the next election are fairly strong, according to most analysts. But its ability to hold a referendum would depend on whether the party could win strong majorities in both chambers of parliament. That rests on the fate of a controversial electoral law that is under legal review and will dictate how parliamentary seats will be allocated in the next election. Italy’s constitutional court is due to rule on the electoral law on 24 January. Even if M5S wins the next election, Italy’s exit from the euro would be complicated. Italy’s constitution sets a high threshold for the country to abandon an international treaty via a popular vote. M5S would have to pass an amendment before calling a referendum, which would then require winning two-thirds majorities in both chambers of parliament. Even if a referendum passed, the issue could come up for review by the constitutional court.

Oh, no, not almost.

• It Is Almost Certain There Will Be Another Euro Crisis In 2017 (McWilliams)

It is almost certain that there will be another euro crisis in 2017. The last time we had a euro crisis, the focus of attention was Greece; today the vortex is Italy. Italy is not Greece. Italy is the third-largest economy in the Eurozone. Italy is the second-largest manufacturing nation in the EU after Germany. Italy is the largest debtor in Europe. The third-largest Italian bank is irredeemably bankrupt. Italy has no government and the people who are likely to win the next election want to take Italy out of the euro and replace the euro with their own currency, the lira. These are the facts. Our Finance Minister has said there is no problem in the Eurozone. I really don’t know what planet he is living on. Unfortunately for the EU, if Greece was a tricky issue to deal with, Italy is — in economic terms — a massive Greece.

Unlike Greece when it was going bust, Italy can’t be patronised, isolated and vilified by the likes of Slovakia, Finland and – shamefully – our own Government. Italy is a country of close to 60 million people and unlike the British, who were always semi-detached Europeans, the Italians are founding members of the EU and original signatories of the Treaty of Rome, which is 60 years old in March. By March, it is likely that Marine Le Pen will be the frontrunner in the French presidential election. Could she win? Of course she could. And if she wins, the euro is toast. There is already a massive capital flight from Italy. This flight of money will extend to France in the months ahead. The euro is the problem and if the EU wants to save itself, it may have to abandon the euro.

Quite what that looks like is anyone’s guess, but here are the political facts: the two main Italian opposition parties, the people who won on Sunday, want Italy to hold a referendum on leaving the euro. Furthermore, Le Pen has explicitly stated that the day she wins, if she does, she will pull France out of the euro and reinstate the French franc. Le Pen currently has 40pc of the electorate. All she needs is the same type of momentum that propelled Brexit, Donald Trump, and the vote in Italy, where the government lost — not by a few%, but by a whopping 60pc to 40pc.

Not even close.

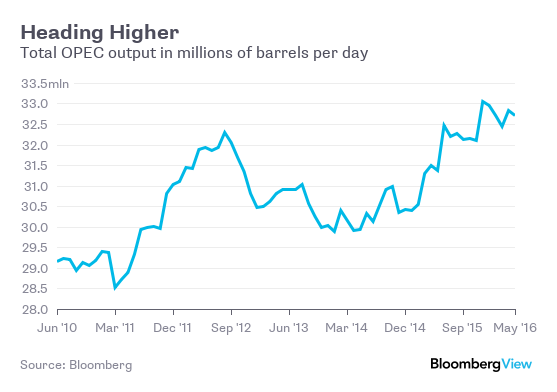

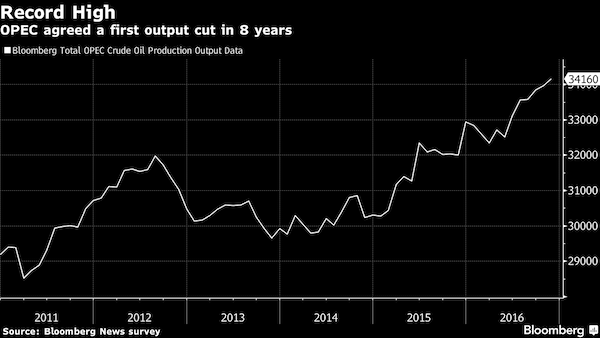

• OPEC Deal Won’t Be Enough to Drain Oil Stockpiles (BBG)

OPEC is likely to bring the oil market into balance by the middle of next year, but its production cut looks set to fall short of its stated goal of draining the stockpiles that are depressing prices. The oil market will rebalance “toward the middle of next year,” according to Nigeria’s Minister of State for Petroleum Emmanuel Kachikwu, bringing an end to more than three years when supply exceeded demand. However, Bloomberg News calculations based on OPEC data show that across the whole of 2017 there will be little overall reduction in record oil inventories – even if the group convinces non-members to join supply curbs at a meeting on Saturday. “Even with 100% compliance from both OPEC and non-OPEC producers global stocks are unlikely to fall in the first half of 2017,” said Tamas Varga at PVM Oil Associates in London. “That should keep oil prices in check.”

Crude prices could rise to $60 to $70 a barrel if the OPEC succeeds in bring inventories back to a normal level, Venezuelan Oil Minister Eulogio del Pino said last week, echoing a widely held view within the group, from Saudi Arabia to Iran. The portents for achieving this are mixed. OPEC’s track record shows the group only delivers 80% of promised cuts. While Russia has pledged to come to the party and lower output by 300,000 barrels a day in the first half of 2017, other non-OPEC producers, such as Mexico, Azerbaijan and Colombia, are likely to dress up involuntary production declines, already factored in by traders, as cuts. That scenario would leave largely unchanged the 300 million-barrel global stockpile surplus Del Pino and his colleagues are targeting.

OPEC has said its agreement will accelerate the decline of global stockpiles and an optimistic Bloomberg scenario shows the call on the group’s supply exceeding its output by 1.2 million barrels a day in third quarter. That depends on full compliance by OPEC members and for Russia to make good on its pledge, even as other non-OPEC producers make little contribution. The analysis of the market re-balancing by Bloomberg News is based on OPEC’s own estimates and projections of crude supply and demand adjusted for potential scenarios of cooperation from Russia and other non-OPEC countries. Other consultancies and agencies have different views. The International Energy Agency expects the re-balancing will happen early next year, while consultants at Rystad Energy expect a 1.26 million barrels-a-day deficit in the first quarter of next year if Russia is the only non-OPEC country to join the effort.

You should take your government to court for this, guys. Let them prove this is beneficial to the country.

• UK Sells Majority Stock In Gas Infrastructure To China, Qatar (Ind.)

National Grid has agreed to sell a majority stake in the UK’s gas pipe network to a team of investors, including the Chinese and Qatari states. The UK’s power network operator confirmed it is offloading the 61% shareholding to a consortium led by Australian investment bank Macquarie in a deal that values the unit at around £13.8bn. The division controls an important part of the country’s infrastructure, which delivers gas to 11 million homes through 82,000 miles of pipeline, and its sale will reignite concerns about the ownership of critical national assets by foreign investors. In August Theresa May said such deals would face tighter regulation as she gave the green light to the French and Chinese-funded Hinkley Point nuclear reactor.

National Grid said it would distribute a £150m voluntary payment to benefit British energy customers, while some £4bn of the proceeds will be returned to the company’s shareholders. It will keep 31% of the business but said it could potentially sell another 14% stake to the consortium under the terms of the deal. The sale, which is set to complete before the end of March next year, comes as part of a move to rebalance National Grid’s business towards higher growth areas and create extra value for shareholders. Dave Prentis, Unison union general secretary, said: “The experience of Thames Water customers when Macquarie was running the show should have been a red flag to ministers and regulators as how unsuitable this company is to be in charge of the UK’s gas supply. ”Macquarie has poor form already – in building up huge company debt, repatriating massive dividends to the southern hemisphere and charging customers more for a much poorer service.

Lovely. And funny.

• UK Village Unleashes Anger With Syrian Refugees: £600 Worth Of Jumpers (Ind.)

Last week I was in Torrington, North Devon, the village that’s been in the news because local people organised a massive collection of clothes and toys, for Syrian refugees placed in the area. Hundreds took part in the collection, and the local theatre was filled with provisions. It’s a story that would make any reasonable person look at those children’s faces and say, “What a bunch of do-gooding whining liberals, this is typical of the metropolitan elites in their cosy London boroughs such as North Devon.” North Devon obviously isn’t in Devon, because a law of modern life is that in the real neglected England that no one ever talks about, real proper people think all immigrants are thieving dogs, and they understand these matters because they’ve never seen a mango.

So it’s lucky the Daily Mail was able to report, “Fury as refugees are settled in Devon”, and another paper told us the refugees “faced anger” from the community. Because when the mayor, local theatre and hundreds of residents organised the collections, and arranged meetings to welcome the refugees, you could at first sight see this as motivated slightly by kindness. But these newspapers weren’t fooled, and understand it’s tradition in North Devon to express your anger by buying a room full of clothes and arranging them in a hall. Whatever you do when you’re in South Molton, don’t shout at a tractor driver to move out of your way, or they’ll lose their temper and collect six hundred pounds worth of jumpers and line them up in their kitchen, insisting you take the lot. Because a lifetime of working on the land makes them vicious.

Five national newspapers told the story of this rage against the refugees, all quoting one man who said: “We’re receiving 50 to 70 refugees, and 50 to 70 is a huge number in an area with restricted public transport.” There’s no doubt 50 to 70 would create a problem for local public transport, if all 50 to 70 of them were housed on one bus. The 7.15am from St Mary’s Church to Barnstaple would be a dreadful crush, so it’s no wonder this man was annoyed, and you can see why the newspapers regard him as the spokesman for the entire region, rather than the hundreds of people who provided all the clothes, who represent no one but themselves.

But it gets worse, because every newspaper covering the story told how refugee children “annoyed locals” by “relaxing playing basketball on a basketball court”. That’s just taking the piss, isn’t it? How dare children play sports in an area specially designated for that specific sport? They should reward our hospitality by playing sports in the wrong areas, such as basketball on a chess board, or skiing on a snooker table.

Here’s an issue the EU does need to speak up about. But doesn’t.

• Relations With Ankara Sour As Turkey Disputes Greek Sovereignty (Kath.)

Greek Foreign Minister Nikos Kotzias and his Turkish counterpart Mevlut Cavusoglu met Thursday on the sidelines of the annual OECD Summit in Hamburg amid escalating tensions brought on by the nationalistic rhetoric coming out of Ankara and Defense Minister Panos Kammenos’s reference to President Recep Tayyip Erdogan as a “ruthless dictator” who “at this moment is threatening our country.” “If they [Turkey] threaten our country, they will meet with our response and they will know that we shall not make concessions in the name of diplomacy on issues of national sovereignty,” Kammenos said in a radio interview Thursday, referring to recent remarks by Erdogan questioning the 1923 Treaty of Lausanne that set the borders between Greece and Turkey, as well as by other Turkish politicians who have disputed Greek sovereignty over a string of islets in the eastern Aegean.

The remarks by Kammenos, the leader of junior coalition partner Independent Greeks, followed strong statements by Turkey’s Deputy Parliament Speaker Tugrul Turkes, who described his country as the guarantor power of the whole of Cyprus, rather than just the breakaway state in the north, while a lawmaker of the opposition CHP, Tanju Ozcan, upped the ante even further, saying he would raise the Turkish flag on 18 Greek islands. “I will go to the islands and if need be I myself will raise the Turkish flag. Then I will fold the Greek one and send it to the Greek government with a courier,” he told the Turkish Parliament. The latest acrimonious rhetoric comes as tensions also simmer over the outcome of Turkey’s extradition request for eight officers who landed in Greece in July in the aftermath of a botched coup attempt in the neighboring country.

But ‘green’ sells, and delivers votes. Still: “Charging an electric car for 100 miles of travel could use about 30kwh – roughly the same amount of energy an average US home uses in three or four days.”

• Electric Cars Are Only As Clean As Their Power Supply (G.)

Electric cars have never been closer to the mainstream, the market pushed ahead by California subsidies for electric car buyers, and a wide array of new models from established car firms such as Toyota and Chevy. Tesla’s focus on luxury, high-performance vehicles has also broadened their appeal; electric cars are no longer purely an environmental statement, but a tech status symbol too. Yet the “zero emissions” claim grates on some experts, who have continued to argue over whether electric cars are really more environmentally friendly than gas guzzlers, once the manufacturing process for the vehicles and their batteries are taken into account.

Electric cars rely on regular charging from the local electricity network. The power plants providing that energy aren’t emission-free; even in California, 60% of electricity came from burning fossil fuels in 2015, while solar and wind together made up less than 14%. “I couldn’t bear to hear them say the words ‘zero emissions vehicle’ one more time,” says Joshua Graff Zivin, who advised one of California’s three main utilities, San Diego Gas & Electric, on electric cars. Graff Zivin is a professor of economics and public policy at the University of California, San Diego. [..] “All of the action is in the hourly,” says Graff Zivin. It’s not only the region that an electric vehicle plugs into that matters. The hour of the day is equally critical. “The cheapest power is not the greenest power.”

In California, the cheapest power is produced at night, mostly from natural gas, hydroelectric dams and nuclear. Night is when many people will charge their electric cars. However, the greenest power gets generated during the day, when solar power can feed the grid; solar doesn’t work in the dark, windmills stop spinning if there’s no wind and, in today’s grid, there is almost the capacity to store solar and wind-generated electricity to use later. Grid storage is slowly expanding, but most electricity has to be used as it is produced. Units of electricity also can’t be tagged according to where and how they were generated, so nobody can verify whether the electricity they use is from a sustainable source – unless they plug directly into their own solar panel or windmill.

[..] Graff Zivin, along with economics researchers Matthew Kotchen and Erin Mansur, waded into this contentious territory in a 2014 paper. Zivin concluded that a plug-in electric vehicle, such as the Nissan Leaf, always produces less carbon dioxide emissions than a hybrid electric- and gas-powered car – but only in selected regions that rely on less coal, like the western United States and Texas. Charging from the coal-dependent grid in the upper midwest of the US at night could generate more emissions than an average gasoline car. And, in some US regions, plugging in at different times of day could even double an electric car’s emissions impact. Charging an electric car for 100 miles of travel could use about 30kwh – roughly the same amount of energy an average US home uses in three or four days.