LOOK Detroit’s 1960 look. Sneak preview of the new models. Dodge Polara 1959

Remember the referendum in April in which voters in the Netherlands rejected the EU-Ukraine trade deal? Seems forever ago, doesn’t it? But to date nothing has been done with the outcome of the vote, even though Dutch law requires a government to implement referendum outcomes as swiftly as possible.

PM Mark Rutte told parliament this week that ‘changing’ the deal would be very difficult, and that talks on the topic in the European Council ‘don’t make him happy’. Since one of the things Rutte has demanded from the EU is a pledge that Ukraine will not become an EU member, none of this should be surprising.

But more importantly, the Dutch didn’t vote for Rutte to renegotiate the deal, they outright rejected it. Ergo, Rutte is playing fast and loose with the integrity and credibility of the Dutch legal and political systems as much as the FBI does with America’s in the Clinton email sleight of hand, and as later today Britain will do with its credibility following the Chilcot report on Tony Blair et al.

As if the Brexit fall-out hasn’t done enough damage to that credibility. One might get the distinct impression that the powers-that-be could get awfully annoyed with the riff-raff out there wanting a say in their own lives. But the riff-raff don’t just want a say anymore, they are getting mighty annoyed with the powers-that-be too.

And that is guaranteed to increase if more ‘incidents’ happen like FBI director Jim Comey’s announcement yesterday that Hillary won’t be charged. At some point credibility must come with accountability, or else. The Hillary files bring the US awfully close to that point, as well as to ‘or else’.

There can be no excuse for Obama’s depriving the public, via a grand jury decision, of the right to determine whether a full court case should be pursued in order to determine in a jury trial whether Hillary Clinton’s email system constituted a crime (or several crimes) under U.S. laws. The Obama Administration’s ‘finding’ that “clearly intentional and willful mishandling of classified information” would need to have been proven, in order for her to have been prosecuted under any U.S. criminal law, is a flagrant lie..

[..] anyone who in the future would be charged with violating any one of those six laws could reasonably cite the precedent that Ms. Clinton was not even charged, much less prosecuted, for actions which clearly fit the description provided in each one of those U.S. criminal laws. Anyone in the future who would be charged under any one of these six laws could prove discriminatory enforcement against himself or herself.

It is highly irresponsible for any government to play such games, and it’s skating on the edge of the law, something a government should always attempt to avoid. That is essential.

Someone who’s not known to be overly bothered by accountability or integrity is everybody’s favorite wino, European Commission President Jean-Claude Juncker. But Juncker, whatever else may be wrong with him, is not a stupid man. And unless I’m gravely mistaken, he has just saddled the European Union with a problem that could well trigger its undoing.

What happened was that at some point last week, reports started coming out that several parties, especially in Germany, were planning to oust Juncker from his plush job. He read them too, of course. And he may have gotten other signals as well in Brussels backrooms.

Then, Germany and France began to clamor for their parliaments to have a say in the ratification of CETA, the Comprehensive Economic and Trade Agreement between the EU and Canada. And Juncker must have seen his chance for revenge. Because yesterday he announced that all 27 parliaments of EU member nations get to have a crack at CETA.

That is Pandora’s box, and I don’t believe for a second that Juncker is not aware of it. Here’s what Deutsche Welle had to say:

European Commission chief Jean-Claude Juncker is expected to scrap plans to fast-track a trade agreement with Canada through the EU. After pressure from Germany and France, Juncker appears to be backtracking. Juncker will reportedly propose a mixed agreement – one that requires both the approval of the European parliament and national legislatures – at an European Commission meeting on Tuesday. Last week he was reported saying he “personally couldn’t care less” whether lawmakers get to vote on the deal. A report in the Financial Times noted that Germany and France wanted their national parliaments to be involved, which would inevitably lengthen the process.

That Juncker quote indicates something had been brewing for a while. Given the position he’s in, it’s quite funny, though

The deal was scheduled to be signed at the end of October during a summit in Brussels with Canadian Prime Minister Justin Trudeau, and it was due to be implemented in 2017. Trade ministers in Germany, France, Italy, the Netherlands and UK have reportedly said they will support the Comprehensive Economic and Trade Agreement, or CETA. CETA is similar to the agreement under negotiation between the EU and US and has drawn strong criticism in EU countries. Canadian and EU leaders concluded CETA in 2014, but implementation was delayed due to last-minute objections in Europe. This was related to an investment protection system to shield companies from government intervention.

Yes, CETA is TTiP on a smaller scale. A sort of test. The nonsensical audacity of ‘an investment protection system to shield companies from government intervention’ says it all.

With opposition to the EU’s impending free trade deal with Canada apparently growing, German Chancellor Angela Merkel said recently that the German parliament should be consulted on the EU’s free trade deal with Canada. “It is a highly political agreement that has been widely discussed,” said Merkel, adding that the “Bundestag is allowed to be involved of course… in national decisions”. German Economy Minister Sigmar Gabriel told the Tagesspiegel daily that Juncker’s comment was “incredibly stupid” and “would stoke opposition to other free trade deals,” including with the US. German media has also described Juncker’s position as badly timed given the growing skepticism among European voters about the EU.

What Gabriel actually said was that Juncker was “unglaublich töricht”, I looked it up. And it wasn’t his reaction to a ‘comment’, but to Juncker’s initial decision to NOT let national parliaments get their say on CETA. It’s brilliant and hilarious, isn’t it? I think I think quite a bit higher of Juncker now.

Because it was Germany itself that insisted they wanted the Bundestag to get involved (under domestic pressure). But they thought that would be it, that and the French parliament. And Jean-Claude threw it right back in their faces. Since they were going to get rid of him anyway, he decided to leave them the perfect parting gift, the ultimate poisoned chalice.

Getting back to the Dutch referendum on EU and Ukraine, one of the things to know about how this works is that the Dutch can ask for a referendum not on any topic, but only on bills the government sends to parliament to discuss. CETA will now be such a case, and a referendum looks at least quite possible.

I don’t know what comparable legislation is in other EU countries, but no doubt in many countries it’s enough to have their parliaments discuss the issue, to cause havoc. That will mean huge delays and/or worse (just what Juncker initially sought to prevent).

The ‘worse’ in this regard -in the eyes of the politicians- is the possibility of referendums, on CETA, and then on TTiP. And before you know it somewhere in Europe such a referendum will be combined with the question whether the country where it’s held should Remain in the EU or Leave it. It seems for all intents and purposes, inevitable.

How the EU can be kept together is a behemoth conundrum already, even without all these new issues. But now we can be absolutely sure that Brexit is only the beginning.

Beppe Grillo’s Five Star Movement (M5S) came out as no. 1 in a poll in Italy yesterday. When I visited Beppe almost 5 years ago in Genoa he was still torn over the EU and the euro, but he has since made up his mind: he’s determined to take Italy out of the unholy Union. Europe’s powers-that-be are in for troubled times.

And Jean-Claude Junker will be sitting somewhere in the world in a beach chair by one of his luxurious summer homes, with a big smile on his face and a stiff drink in his hand.

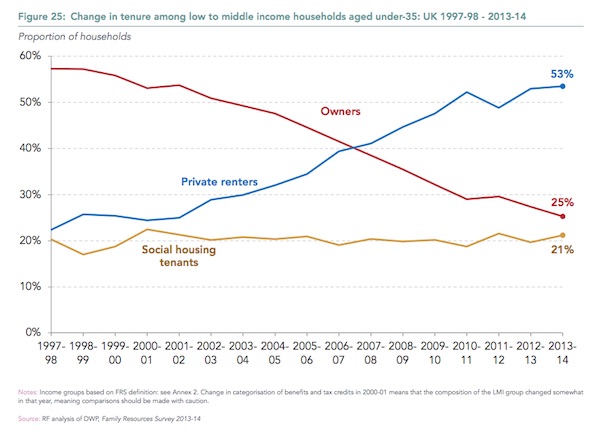

Property prices in Britain may be surging due to a horrendous imbalance of supply and demand — but the market is poised to implode. Why? Because Britons are not earning enough money to either get on the housing ladder or are spending such a large portion of their wages on mortgages that may not be sustainable. Well, not unless everyone suddenly gets a huge pay rise over the next year or so. That’s the assumption in the latest figures from think tank Resolution Foundation, which show that lower- and middle-income households are spending 26% of their salaries on housing, compared to 18% back in 1995. In London, households spend 28% of their income on housing. The think tank said this is the equivalent to adding 10 percentage points onto income tax.

Only the rich are not feeling the pressure of rising house prices. Higher-income households spend 18% of their income on housing, compared to 14% in 1995. The average price to buy a house in Britain now stands at £291,504, according to the Office for National Statistics. Meanwhile, the average London property price is at a huge £551,000. To put this into perspective, Resolution Foundation estimated that median income, at £24,300, is only around 3% higher than it was when the credit crunch hit in 2007/2008. [..] the house price-to-earnings ratio is near the pre-crisis peak. Considering the average deposit to secure a home is around 10% of the total property price, this means Britons are taking on huge amounts of debt and eating into the little savings they have to buy a home.

[..] the market is poised on a knife edge between interest rates and wages. If interest rates were to rise — and they will eventually — it could prove a major problem for the Britons who already spend 25-28% of their salaries on housing. Similarly, if another downturn depresses wages, mortgage payments will become an increasing portion of their income even without an interest rate increase. That situation is pricing out low- and middle-income people from the market, as the chart shows. Ownership rates in this group have sunk from nearly 60% in 1997 to just 25% today. That’s how fragile the housing market is: With those buyers unable to afford to buy, the market is dependent on a thinner slice of owners, whose incomes are increasingly stretched by housing costs, who can’t afford a decrease in wages, and who may not be able to afford any increase in interest.

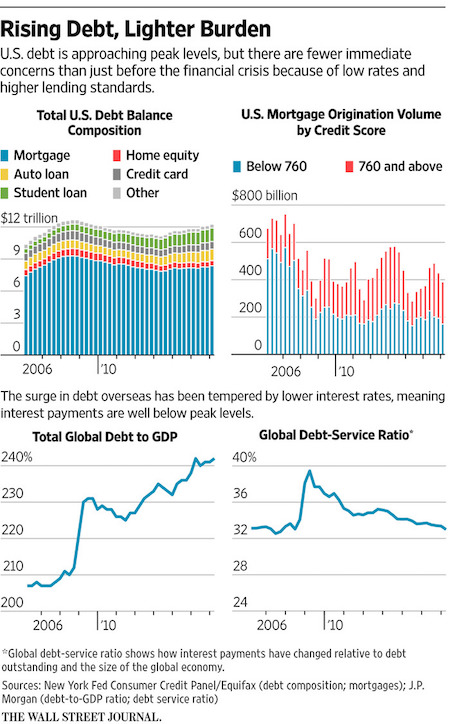

If current trends persist through the end of the year, U.S. households will owe as much as they did at the peak of borrowing in 2008. Global debt has already topped 2008 levels and keeps rising. That’s pretty astonishing so soon after debt-driven crises in the U.S. and Europe and endless worries about too much borrowing in Japan, China and emerging markets. But for all the hand-wringing, a near-term debt crisis is unlikely. Lower interest rates mean debt payments are far lower than they were before the crisis. In the U.S., household debt compared with the overall economy is way down. And overseas, loans can easily be rolled over. Yet even with low rates, the cycle of borrowing and rolling over loans has a cost. People, governments and businesses spend now instead of later, likely reducing future growth.

The cycle also allows borrowing to go on for years, which can be good—allowing reform to take hold—or not, allowing bad policies to go on almost indefinitely. U.S. households owed $12.25 trillion at the end of the first quarter, up 1.1% from the end of 2015, according to the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit, released Tuesday. If the first quarter repeats itself through the end of the year, U.S. household debt will approach its peak of $12.68 trillion, which it hit in the third quarter of 2008. Many people remember that quarter because it’s when the global financial system went off a cliff. This time is different because short-term interest rates have been stuck near zero since then. For U.S. consumers, that means household debt-service payments as a percent of disposable personal income are at their lowest level since at least 1980, despite a much higher debt load. In addition, more loans are going to higher-quality borrowers.

[..] Low rates have had an even more dramatic impact overseas, where economies are weaker or less stable. Global debt—including households, businesses and governments—has risen from 221% of GDP at the end of 2008 to 242% at the end of the first quarter. But the cost of interest payments, as a share of GDP, has fallen to 7% from a peak of 11%, according to J.P. Morgan. Japan is the prime example of how low interest rates can change the rules of the game. At 400% of GDP, Japan’s debt level is by far the highest in the world. One of the great mysteries of finance is why investors lend the government money for negligible or negative yields when it seems impossible for Japan to pay off its debt.

A senior IMF official Wednesday said it can’t help Europe with fresh emergency financing for Greece because Athens’s creditors haven’t yet committed to detailed debt relief. The comments show that the agreement touted by European finance ministers last night to release fresh bailout cash for Greece hasn’t nailed down the key elements the IMF says are critical to finally return the debt-laden country to health. Rather, the IMF’s reserved support for the deal has paved the way for Germany to approve new funds and sets the stage for more tough negotiations later this year. “Fundamentally, we need to be assured that the universe of measures that Europe will to commit to…is consistent with what we think is needed to reduce debt,” the senior official told reporters on a conference call. “We do not yet have that.”

But the official said Europe’s acknowledgment that debt relief is needed and would be detailed later this year was enough to win the fund’s conditional backing. “All the stakeholders now recognize that Greek debt is…highly unsustainable,” the official said. “They accept that debt relief is needed, they accept the methodology that is needed to calibrate the necessary debt relief. They accept the objectives of gross financing needs in the near term and in the long run. They even accept the time tables.” Many outside economists see the deal as papering over the differences and once again prolonging the crisis. “Summary of Eurogroup: Germany always wins, IMF caves under pressure from Germany and U.S., no one does what’s in Greece’s best interests,” said Megan Greene at Manulife and John Hancock Asset Management. Marc Chandler at investment bank Brown Brothers Harriman called the deal a “paper charade” that saves Europe more than it does Greece.

It was hardly a headline to set the pulse racing. “Analysing economic trends according to the situation in the first quarter: authoritative insider talks about the state of China’s economy,” read the front page of the Communist party’s official mouthpiece on the morning of Monday 9 May. Yet this headline – and the accompanying 6,000-word article attacking debt-fuelled growth – has sparked weeks of speculation over an alleged political feud at the pinnacle of Chinese politics between the president, Xi Jinping, and the prime minister, Li Keqiang, the supposed steward of the Chinese economy.

“The recent People’s Daily interview not only exposes a deep rift between [Xi and Li], it also shows the power struggle has got so bitter that the president had to resort to the media to push his agenda,” one commentator said in the South China Morning Post. “Clear divisions have emerged within the Chinese leadership,” wrote Nikkei’s Harada Issaku, claiming the two camps were “locking horns” over whether to prioritise economic stability or structural reforms. The 9 May article – penned by an unnamed yet supposedly “authoritative” scribe – warned excessive credit growth could plunge China into financial turmoil, even wiping out the savings of the ordinary citizens.

As if to hammer that point home, a second, even longer article followed 24 hours later – this time a speech by Xi Jinping – in which the president laid out his vision for the Chinese economy and what he called supply-side structural reform. “Taken together, the articles signal that Xi has decided to take the driver’s seat to steer China’s economy at a time when there are intense internal debates among officials over its overall direction,” Wang Xiangwei argued in the South China Morning Post. Like many observers, he described the front page interview as a “repudiation” of Li Keqiang-backed efforts to prop up economic growth by turning on the credit taps.

Chinese officials plan to ask their American counterparts in annual talks next month about the chance of a Fed interest-rate increase in June, according to people familiar with the matter. The Chinese delegation will try to deduce whether a June or a July rate rise is more likely, as their nation’s policy makers prepare for the potential impact on financial markets and the yuan, the people said, asking not to be named as the discussions were private. In China’s view, if the Fed does lift borrowing costs, a July move would be preferable, the people said. China’s exchange rate has already been weakening as expectations rise for the U.S. central bank to boost its benchmark rate for the first time since it ended its near-zero policy in December with a quarter%age point increase.

It’s not unusual for senior officials to press each other on their policies, and any inquiries by the Chinese about the Fed would follow repeated expressions of concern from the U.S. about China’s intentions with its exchange rate. The Treasury Department put China on a new currency watch list last month to monitor for unfair trade advantages. “The Chinese side will argue that the U.S. should tread cautiously as it tightens monetary policy and avoid any surprises,” said Mark Williams, chief Asia economist at Capital Economics in London, who participated in U.K.-China meetings when working at Britain’s Treasury. “The Federal Reserve will make its decision solely on what it deems best for the U.S. economy, but it is clear that concerns about China have influenced its thinking about the balance of risks facing the U.S.”

[..] “Chinese officials are pretty anxious about the Fed as a June rate hike – which is not fully discounted in the market – may boost the dollar,” said Shen Jianguang, chief Asia economist at Mizuho in Hong Kong. “This could pose a threat or make it difficult for the PBOC to keep a stable RMB exchange rate,” he said, referring to the People’s Bank of China’s management of the renminbi, another term for the yuan. “A less aggressive Fed stance is in China’s interest.”

Tata has refused to rule out holding on to its crisis-hit British steel division, raising fears that the business could suffer “a death by a thousand cuts”. Delivering annual results for the Tata’s global steel business, Koushik Chatterjee, executive director, declined to give details on the board’s thoughts on the seven bids the company has received for the loss-making UK plants. But pressed on whether Tata could do a U-turn and hold on to the business – which the Government has said it is willing to take a 25pc stake in and offer financial support to if this will keep it alive – he refused to deny this was an option “I don’t think we have a case as yet,” said Mr Chatterjee. “There is lots of focus only on a sale.” The results announcement – which showed Tata Steel’s revenues down 6pc to £11.9bn and an annual loss of £309m – echoed Mr Chatterjee, saying: “The board… is actively reviewing all options for the Tata Steel UK business, including a potential sale.”

Sajid Javid, the Business Secretary, met with Tata’s directors on Monday night for several hours ahead of their monthly meeting, which considered the bids. It is thought Mr Javid sees Tata keeping the UK business as a way of retaining a viable steel industry in the Britain, after bidders signalled their reluctance to take on the Tata pension scheme, which has a £500m deficit. Ministers are this week expected to start consultations on controversial proposals to restructure the pension scheme [..] The changes would alter the way pension payments are calculated by swapping from RPI inflation to the lower CPI, potentially shaving billions from the scheme’s liabilities. However, such a move would require a change off law and could set what some pensions experts have described as a dangerous precedent.

Varoufakis’s answers are quick, sharp and eloquent – and ready. He barely needs a pause when asked what he’d do if suddenly installed as Australia’s treasurer, before he’s firing off a prescription for the economy. “The first thing that has to happen in this country is to recognise two truths that are escaping this electorate, and especially the elites. “Firstly, Australia does not have a debt problem. The idea that Australia is on the verge of becoming a new Greece would be touchingly funny if it were not so catastrophic in its ineptitude. Australia does not have a public debt problem, it has a private debt problem. “Truth number two: the Australian social economy is not sustainable as it is. At the moment, if you look at the current account deficit, Australia lives beyond its means – and when I say Australia, I mean upper-middle-class people. The luxurious lifestyle is not supported by the Australian economy.

It’s supported by a bubble, and it is never a good idea to rely on the proposition that a bubble will always be there to support you. “So private debt is the problem. And secondly, because of this private debt, you have a bubble, which is constantly inflated through money coming into this country for speculative purposes.” Varoufakis is unequivocal in his conviction that current growth – which he likens to a Ponzi scheme – needs to be replaced with growth that comes from producing goods. “Australia is switching away from producing stuff. Even good companies like Cochlear, who have been very innovative in the past, have been financialised. They’re moving away from doing stuff to shuffling paper around. That would be my first priority [if I were Australian treasurer]: how to go back to actually doing things.”

Varoufakis wouldn’t be the first to compare the Australian economy to a Ponzi scheme. Economist Lindsay David has made a similar criticism of the housing market, and has also heavily criticised Australia’s reliance on Chinese investment. David and fellow economist Philip Soos have predicted the economy is heading for a crash, and Varoufakis thinks they might be right. He is quick to point out that crashes can never be predicted, but he is in little doubt that it will happen if Australia doesn’t change direction soon. “There is no doubt, if you look at the pace of house prices over the past 20 years in Australia and the pace of value creation; they’re so out of kilter that something has to give.”

Venezuela’s gold reserves have plunged to their lowest level on record after it sold $1.7 billion of the precious metal in the first quarter of the year to repay debts. The country is grappling with an economic crisis that has left it struggling to feed its population. The OPEC member’s gold reserves have dropped almost a third over the past year and it sold over 40 tonnes in February and March, according to IMF data. Gold now makes up almost 70% of the country’s total reserves, which fell to a low of $12.1 billion last week. Venezuela has larger crude reserves than Saudi Arabia but has been hard hit by years of mismanagement and, more recently, depressed prices for oil. Oil accounts for 95% of its export earnings. Despite the recent price rebound, declining oil output is likely to take a further toll on the economy. The IMF forecasts the economy will shrink 8% this year, and 4.5% in 2017, after a 5.7% contraction in 2015.

Inflation is forecast to exceed 1,642% next year, fueled by printing money to fund a fiscal deficit estimated at about 20% of GDP. Venezuela began selling its gold reserves in March 2015, according to IMF data. At roughly 367 tonnes, Venezuela has the world’s 16th-biggest gold reserves, according to the World Gold Council. In contrast, China and Russia both added to their gold holdings this year, the data show. Gold prices have risen 15% this year. Last year Venezuela’s central bank swapped part of its gold reserves for $1 billion in cash through a complex agreement with Citi. The late president Hugo Chávez had said he would free Venezuela from the “dictatorship of the dollar” and directed the central bank to ditch the US dollar and start amassing gold instead. In 2011, as a safeguard against market instability, Chávez brought most of the gold stored overseas back to Caracas.

The Wall Street Journal examined 156 criminal and civil cases brought by the Justice Department, Securities and Exchange Commission and Commodity Futures Trading Commission against 10 of the largest Wall Street banks since 2009. In 81% of those cases, individual employees were neither identified nor charged. A total of 47 bank employees were charged in relation to the cases. One was a boardroom-level executive, the Journal’s analysis found. The analysis shows not only the rarity of proceedings brought against individual bank employees, but also the difficulty authorities have had winning cases they do bring. Most of the bankers who were charged pleaded guilty to criminal counts or agreed to settle a civil case, with those facing civil charges paying a median penalty of $61,000.

Of the 11 people who went to trial or a hearing and had a ruling on their case, six were found not liable or had the case dismissed. That left a total of five bank employees at any level against whom the government won a contested case. They include Mr. Heinz, the former UBS employee. One of the few successful government cases was overturned Monday. A federal appeals court tossed civil mortgage-fraud charges and a $1 million penalty against Rebecca Mairone, a former executive at Countrywide Financial Corp., now part of Bank of America Corp. The court also threw out a related $1.27 billion penalty against Bank of America. Representatives of Ms. Mairone and the bank this week welcomed the verdict, while the Justice Department, which brought the cases, declined to comment.

There are plenty of possible explanations for the small number of successful cases. For starters, much of the institutional conduct during and after the financial crisis didn’t break the law, said law-enforcement officials. Even when the government has been able to prove illegal activity, it has rarely been traced to the upper echelons of big banks. “The typical scenario is not that the bank has this plan for world domination being cooked up by the chairman and CEO,” said Adam Pritchard, a law professor at the University of Michigan. “It’s some midlevel employee trying to keep his job or his bonus, and as result the bank gets into trouble.”

“The Fed might want to imitate the ECB but may be restricted from doing so by its charter..” “We wouldn’t discount the possibility it will try to amend, or get around, any prohibitions, however.”

[..] corporate leverage is hovering near a 12-year high and domestic capital expenditures have plunged. In the interim, reams of commentary have been devoted to share buybacks and with good reason. Companies reducing their share count have, at least in recent years, been where the hottest action is, courtyard-seat level action. But now, it looks as if the trend is finally cresting. A fresh report by TrimTabs found that companies have announced 35% less in buybacks through May 19th compared with the same period last year. And while $261.5 billion is still respectable (for the purpose of placating shareholders), it is nevertheless a steep decline from 2015’s $399.4 billion. Even this tempered number is deceiving – only half the number of firms have announced buybacks vs last year.

Have U.S. executives and their Boards of Directors finally found religion? We can only hope. The devastation wrought by the multi-trillion-dollar buyback frenzy is what many of us learned in Econ 101 as the ‘opportunity cost,’ or the value of what’s been foregone. As yet, the value of lost investment opportunities remains a huge unknown. In the event doing right by future generations does not suffice, executives might be motivated to renounce their errant ways because shareholders appear to have stopped rewarding buybacks. According to Marketwatch, an exchange traded fund that affords investors access to the most aggressive companies in the buyback arena is off 0.8% for the year and down 9.8% over the last 12 months.

The hope is that Corporate America is at the precipice of an investment binge that sparks economic activity that richly rewards those with patience over those with the burning need for instant gratification. The risk? That central bankers whisper sweet nothings the likes of which no Board or CFO can resist. Mario Draghi may already have done so. In announcing its latest iteration of QE, the ECB added investment grade corporate bonds to the list of eligible securities that can satisfy its purchase commitment. Critically, U.S. multinationals with European operations are included among qualifying issuers. As Evergreen Gavekal’s David Hay recently pointed out, McDonald’s has jumped right into the pool, issuing five-year Euro-denominated paper at an interest rate of a barely discernible 0.45%.

During the run-up to the Iraq invasion, intelligence officers would hand ministers an estimate, an allegation, a straw in the wind, in certain cases (the 45-minute claim being the most notorious example) an outright fabrication. Tony Blair’s office would then bless it with the imprimatur of a government assessment, usually employing vague wording — in the hope that the media would repeat and then amplify the message. Cameron and Osborne have become masters of this kind of politics. ‘We’re paying down Britain’s debts,’ said David Cameron in 2013. This was a straight lie: the national debt was soaring as he spoke. ‘When I became Chancellor,’ observed Osborne last year, ‘debt was piling up.’ True – and he has been piling it up ever since, even now rising by £135 million a day.

This kind of deception works: polls show that only a minority of voters realise that the national debt is still rising. George Osborne has now converted the Treasury into a partisan tool to sell the referendum, exactly as Tony Blair used the Joint Intelligence Committee to make the case for war against Iraq. Before becoming Chancellor, Osborne was critical of Gordon Brown’s Treasury, and rightly so, because it had been so heavily politicised. He rightly stripped the Treasury of its forecasting function and created an independent Office for Budget Responsibility — an encouraging sign that he was determined to avoid the culture of deceit which was such a notable feature of the Brown/Blair era. It is therefore very troubling that the Office for Budget Responsibility has not come anywhere near the two Treasury dossiers that make the case for the EU.

It’s easy to see why – they would point out straight away that the Chancellor has been engaged in fabrication. For example, let’s take a hard look at how he induced Treasury officials to endorse his central claim that families would be £4,300 ‘worse off’ if Britain left the EU. The main technique that Osborne used was his conflating GDP with household income – and referring to ‘GDP per household’, a phrase that has never been used in any Budget. As the Chancellor used to argue, GDP is a misleading indicator which can be artificially inflated by immigration. Immigration of 5% may well raise GDP by the same amount, but nobody would be any better off. ‘GDP per capita is a much better indicator,’ said Osborne when newly in office. He made no mention at all of GDP per capita when launching the Brexit documents published by the Treasury.

Having successfully used the EU to conquer the Greek people by turning the Greek “leftwing” government into a pawn of Germany’s banks, Germany now finds the IMF in the way of its plan to loot Greece into oblivion . The IMF’s rules prevent the organization from lending to countries that cannot repay the loan. The IMF has concluded on the basis of facts and analysis that Greece cannot repay. Therefore, the IMF is unwilling to lend Greece the money with which to repay the private banks. The IMF says that Greece’s creditors, many of whom are not creditors but simply bought up Greek debt at a cheap price in hopes of profiting, must write off some of the Greek debt in order to lower the debt to an amount that the Greek economy can service.

The banks don’t want Greece to be able to service its debt, because the banks intend to use Greece’s inability to service the debt in order to loot Greece of its assets and resources and in order to roll back the social safety net put in place during the 20th century. Neoliberalism intends to reestablish feudalism—a few robber barons and many serfs: the 1% and the 99%. The way Germany sees it, the IMF is supposed to lend Greece the money with which to repay the private German banks. Then the IMF is to be repaid by forcing Greece to reduce or abolish old age pensions, reduce public services and employment, and use the revenues saved to repay the IMF. As these amounts will be insufficient, additional austerity measures are imposed that require Greece to sell its national assets, such as public water companies and ports and protected Greek islands to foreign investors, principallly the banks themselves or their major clients.

So far the so-called “creditors” have only pledged to some form of debt relief, not yet decided, beginning in 2 years. By then the younger part of the Greek population will have emigrated and will have been replaced by immigrants fleeing Washington’s Middle Eastern and African wars who will have loaded up Greece’s unfunded welfare system. In other words, Greece is being destroyed by the EU that it so foolishly joined and trusted. The same thing is happening to Portugal and is also underway in Spain and Italy. The looting has already devoured Ireland and Latvia (and a number of Latin American countries) and is underway in Ukraine. The current newspaper headlines reporting an agreement being reached between the IMF and Germany about writing down the Greek debt to a level that could be serviced are false. No “creditor” has yet agreed to write off one cent of the debt.

The French government said it was prepared to endure weeks of strikes at refineries and began releasing strategic oil reserves to help ease nationwide fuel shortages. While panic-buying by motorists drove demand to three times the normal level Tuesday, France has enough stocks even if the strikes persist for weeks, Transport Minister Alain Vidalies said. The problem isn’t about supply but about delivery, he said. Oil companies have mobilized hundreds of trucks to ship diesel and gasoline around the country since the start of the week as filling stations ran dry after all the nation’s refineries experienced disruptions or outright shutdowns. By Wednesday Exxon Mobil reported that its Gravenchon plant was operating normally and able to transport fuel while elsewhere strikers have blocked refineries to try to bring shipments to a halt.

Workers are protesting against President Francois Hollande’s plans to change labor laws to reduce overtime pay and make it easier to fire staff in some cases. While the government has watered down its proposals since first floating them in February, unions are calling for them to be scrapped altogether. The new law will not be withdrawn and police will continue to ensure access to fuel depots, Prime Minister Manuel Valls told Parliament Wednesday. Total’s Feyzin refinery near Lyon and its Normandy plant have stopped production. La Mede was working at a lower rate Wednesday, while the facilities at Grandpuits near Paris and Donges close to Nantes will come to a complete halt later this week, according to a company statement.

Total may reconsider a plan to spend €500 million to upgrade the Donges facility as workers take the plant “hostage,” CEO Patrick Pouyanne said Tuesday. He urged motorists not to rush to gas stations and create an “artificial” shortage. Some 348 of Total’s 2,200 gas stations ran out of fuel and 452 faced partial shortages as of Wednesday morning, the company said. The figures are little changed from Tuesday. About one in five of the country’s 12,200 stations were facing shortages Tuesday afternoon, the government said.

As smoke rises from burning tyres on French oil refinery picket-lines, motorists queue for miles to panic-buy rationed petrol, and train drivers and nuclear staff prepare to go on strike. With the 2017 French presidential election nearing, the Socialist president François Hollande is facing his toughest and most explosive crisis yet. It is not just Hollande’s political survival at stake, though, but the image of France itself. The country is preparing to host two million visitors at the showpiece Euro 2016 football tournament in two weeks, and the back-drop is not ideal: strikes and feared fuel shortages, potential transport paralysis, a terrorist threat, a state of emergency and a mood of heightened tension and violence between street protesters and police.

Hollande, the least popular leader in modern French history whose approval ratings are festering, according to various polls, at between 13% and 20%, might not seem as though he has further to fall. But in fact he is clinging, white-knuckled, to the edge of a cliff. The Socialist was supposed to be spending May and June testing the waters for a possible re-election bid by repeating his new mantra “things are getting better” – even if more than 70% of French people don’t believe that that is true. Instead, France has been hit by an explosive trade union revolt over Hollande’s contested labour reforms. The beleaguered president has framed these reforms as a crucial loosening of France’s famously rigid labour protections, cutting red-tape and slightly tweaking some of the more cumbersome rules that deter employers from hiring.

This would, he has argued, make France more competitive and tackle stubborn mass employment that tops 10% of the workforce. But after more than two months of street demonstrations against the labour changes, the hardline leftist CGT union radically upped its strategy and is now trying to choke-off the nation’s fuel supply to force Hollande to abandon the reforms.

Bayer could receive financing from the European Central Bank that would help to fund a takeover of Monsanto, according to the terms of the ECB’s bond-buying program. U.S.-based Monsanto, the world’s largest seed company, turned down Bayer’s $62 billion bid on Tuesday, but said it was open to further negotiations. The ECB can buy bonds issued by companies that are based in the euro area, have an investment-grade rating and are not banks, provided that they are denominated in euros and meet certain technical requirements. The purpose for which the bonds are issued is not among the criteria set by the ECB, which will start buying corporate bonds on the market and directly from issuers next month.

This means that, in theory, the ECB could buy debt issued by Bayer, which said on Monday it would finance its cash bid for Monsanto with a combination of debt and equity. “It will be interesting to observe how much of such a deal would be absorbed by the central bank,” credit analysts at UniCredit wrote in a note. The ECB is buying €80 billion worth of assets every month in an effort to revive economic growth in the euro zone by lowering borrowing costs. Central bank sources told Reuters that it would not be the ECB’s first choice if the money it spent ended up financing acquisitions. But even this would have a silver lining if consolidation made an industry or sector more efficient and if it gave fresh impetus to the stock market, the source added. And if issuers ended up exchanging the euros raised through bond sales for dollars, that would also help the euro zone by weakening the euro against the greenback, the sources said.

“Russia is able to become the largest world supplier of healthy, ecologically clean and high-quality food which the Western producers have long lost..”

Russia’s Vladimir Putin is taking a bold step against biotech giant Monsanto and genetically modified seeds at large. In a new address to the Russian Parliament Thursday, Putin proudly outlined his plan to make Russia the world’s ‘leading exporter’ of non-GMO foods that are based on ‘ecologically clean’ production. Perhaps even more importantly, Putin also went on to harshly criticize food production in the United States, declaring that Western food producers are no longer offering high quality, healthy, and ecologically clean food. “We are not only able to feed ourselves taking into account our lands, water resources – Russia is able to become the largest world supplier of healthy, ecologically clean and high-quality food which the Western producers have long lost, especially given the fact that demand for such products in the world market is steadily growing,” Putin said in his address to the Russian Parliament.

And this announcement comes just months after the Kremlin decided to put a stop to the production of GMO-containing foods, which was seen as a huge step forward in the international fight to fight back against companies like Monsanto. Using the decision as a launch platform, it’s clear that Russia is now positioning itself as a dominant force in the realm of organic farming. It even seems that Putin may use the country’s affinity for organic and sustainable farming as a centerpiece in his economic strategy. “Ten years ago, we imported almost half of the food from abroad, and were dependent on imports. Now Russia is among the exporters. Last year, Russian exports of agricultural products amounted to almost $20 billion – a quarter more than the revenue from the sale of arms, or one-third the revenue coming from gas exports,” he added.

The other, grander gamble that Xi has taken is to keep the Chinese economy growing. Of course, the Communist Party since Deng Xiaoping has staked its legitimacy on economic growth, so far to good effect. But Jiang Zemin and Hu Jintao governed through a broad-based consensus of senior party leaders, which meant that the risks of legitimacy and delegitimacy were spread across the group and the institution they represented. Xi, in contrast, has taken more power – and therefore the risks of economic growth – onto his shoulders. There are many tools central government can use to keep an economy growing, and China under Xi will use them all. State-owned enterprises may be less efficient in the long run than truly private companies, but they have the enormous political benefit of responding to centralized state directives.

With good economists advising him, Xi stands a reasonable chance of transitioning China into a more consumer-driven economy, thereby assuring a source of modest continued growth even as the export-driven economy slows down. But that task, too, depends on the individual purchasing decisions of ordinary Chinese – that is, success of China’s economy, and therefore of Xi’s presidency, ultimately depends on the domestic consumer market. This brings us back to the stock market. Sure, Xi has to worry that the correction will spook emerging consumers, encouraging them to sit on their cash rather than spending it. But the much bigger political problem is that ordinary Chinese, watching the market fall, will experience the certain knowledge that Xi can’t really do anything about it.

Short-term stopgaps like closing markets during sell-offs or ordering state-owned enterprises not to sell their shares won’t address market fundamentals – because they can’t. In confirmed capitalist societies, we long ago learned that the government can’t stop the market from going where it believes it must. The reason, of course, is that the market isn’t a single entity that can be forced to take collective action. It’s an aggregation of individual decision-makers, all of whom share a competitive interest in achieving gain and limiting loss. For that reason, governments in experienced capitalist countries know that the only meaningful, long-term way to respond to market declines is by trying to create economic conditions that will restore faith in the markets.

The government of Greek Prime Minister Alexis Tsipras sought a three-year bailout loan of at least €53.5 billion ($59.2 billion), in a last-ditch effort to keep the country in the euro. In exchange, it offered a package of reforms and spending cuts, including pension savings and tax increases, similar to the one presented by creditors last month. The proposal was submitted to European institutions late Thursday and will be presented to the Greek Parliament Friday. It is set to be discussed at a summit of European Union leaders Sunday to determine whether Greece gets a new bailout, or be forced to leave the single currency. Greece offered measures that almost mirrored a proposal from creditors on June 26, which was rejected by voters in a July 5 referendum.

In return, it asked for its long-term debt to be made more manageable to allow it to rebound from a crisis that has erased a quarter of its economy. It is unclear if the proposal is enough to clinch a deal with creditors amid signs of economic deterioration since banks were closed and capital controls imposed 12 days ago. “The Greeks appear to have made significant concessions, apparently accepting much of the most recent creditor proposal,” Chris Scicluna, head of economic research at Daiwa Capital Markets in London, wrote in a note. “It remains to be seen whether creditors will want even more austerity.” The Greek government said it would use the three-year loan from the European Stability Mechanism to cover debt repayments between 2015 and 2018, mostly to the International Monetary Fund and the European Central Bank.

It will then be left with debt owed only to European Union institutions. Greece’s proposal includes creditors’ longstanding demands for sales tax increases and cuts in public spending on pensions. Greece also proposes the restructuring of its debt and a package of growth measures of €35 billion. Pressure has been mounting on Greece’s creditors to make the country’s debt more manageable. “A realistic proposal from Greece will have to be matched by an equally realistic proposal on debt sustainability from the creditors,” European Union President Donald Tusk told reporters in Luxembourg Thursday. “Only then will we have a win-win situation.”

“French leaders have waxed poetic in recent days about the special place Greece holds. Greek independence was celebrated by French writers and artists from Victor Hugo and to Eugene Delacroix..”

The race to come up with a last-minute proposal to keep Greece in the eurozone began with a Sunday night phone call from Greek Prime Minister Alexis Tsipras to French President Francois Hollande, moments after Greece’s referendum dealt a near-fatal blow to the talks. If Greece wanted to remain in the eurozone, Athens must make ambitious proposals to its creditors quickly, Mr. Hollande told him, adding: “Help me help you.” That advice was part of an urgent French campaign to salvage months of negotiations from the wreckage of the Greek referendum. After long staying out of the fray, Mr. Hollande was scrambling to keep the discussions alive. His strategy: to press Mr. Tsipras for stronger economic overhauls while persuading Angela Merkel to give Greece more time and, ultimately, hope for debt relief.

The stance reflects a particularly French vision of the eurozone as a grand political project, with strategic benefits for Europe worth defending even at high cost. A Greek exit from the eurozone would set a dangerous precedent, French officials say, turning the currency bloc into little more than an arrangement of fixed currency exchange rates that governments could discard. French leaders have waxed poetic in recent days about the special place Greece holds. Greek independence was celebrated by French writers and artists from Victor Hugo and to Eugene Delacroix, Prime Minister Manuel Valls told lawmakers Wednesday in explaining why France refuses to accept a Greek exit from the euro. “Greece is a passion for France and Europe,” Mr. Valls said.

“The goddess that gave its name to our continent is at the heart of our mythology.” Domestic politics is also at work. Mr. Hollande, a Socialist, faces a rebellion from members of his parliamentary majority who accuse him of abandoning his 2012 election pledge to push for pro-growth policies in Europe. Standing up to Berlin on behalf of Greece is a chance to brandish his leftist credentials for party hard-liners, analysts say. It is unclear whether France’s triage will lead to a deal by Sunday, when European Union leaders are due to decide Greece’s fate. But France’s intervention has helped keep the talks on life support.

I do not have the foggiest whether these latest Greek proposals will be enough to secure a deal. There are still very big obstacles to overcome. But Alexis Tsipras has achieved something that has eluded him in the past five months: he has managed to split the creditors. The IMF insists on debt relief. The French helped the Greek prime minister draft the proposal and were the first to support it openly. President François Hollande is siding with Mr Tsipras. And that changes the stakes for Angela Merkel. If the German chancellor says no now, she will stand accused of taking reckless risks with the eurozone and the Franco-German alliance. If she says yes, her own party might divide similarly to the way the British Conservatives divided over Europe. I have always predicted that the moment of truth for the eurozone will come eventually. It will come this weekend.

The financial markets seemed to have made up their mind that a deal will happen. But beware the many landmines on the path to a deal. Of those, only the first has been sidestepped with Mr Tsipras’ offer. What he is now proposing is, economically, not fundamentally different from what he, and the Greek electorate, rejected in Sunday’s referendum — but it works politically for him. The phase-in period of some of the harder measures is longer. And if there is a deal, there will have to be an explicit reference to debt relief this time. The IMF insists on it. And even Donald Tusk, the president of the European Council, says so. This is an important development, but it is not clear that all creditors will, or can, agree.

By tomorrow, the technical people and the finance ministers will need to discuss whether the Greek numbers add up. The answer is almost certainly no, not least because of the rapid deterioration of the country’s economy. The imposition of capital controls and bank withdrawal limits brought most economic activity to a standstill. Any macroeconomic adjustment programme will have to start with a realisation that the situation is worse today than two weeks ago. The Greek list takes account of this in terms of slower adjustment periods. This is economically sensible. But Ms Merkel has already said she wanted this problem taken care of through additional austerity. For a programme to be agreed, one side will have to back down here.

On top of this, there is now the acute problem of an insolvent banking system — one that is totally reliant on a special lifeline by ECB called emergency liquidity assistance. The ECB will find it hard to increase ELA. So apart from agreeing on a macroeconomic stabilisation programme, European leaders will this weekend need to answer the more immediate question of what to do with the Greek banks. This is possibly the single most complicated question because there are no easy and fast answers. What may have to happen is that the number of banks will have to shrink to three or two, and that depositors may have to be “bailed in”. I cannot see that the creditors would agree to a further bank restructuring programme, in addition to the €53.5bn in new loans currently under discussion.

Lynn Parramore: What’s your view of the attitudes of the creditor powers?

Jamie Galbraith: What happened on the 26th of June was that Alexis (Tsipras) came to realize, at long last, that no matter how many concessions he made he wasn’t going to get the first one from the creditors. That’s something Wolfgang Schäuble had made clear to Yanis (Varoufakis) months before. But it was hard to persuade the Greek government of this because its members naturally expected, as you would when you’re in a negotiation, that if you make a concession the other side will make a concession. That isn’t the way this one worked. The Greeks kept making concessions. They’d present a program and the other side would say —as you can read in the press — oh, no, that’s not good enough. Do another one. Then they’d complain that the Greeks were not being serious. What the creditors meant by that was this: when you come around and agree to what we tell you, then you’re serious. Otherwise not. This is the way bad professors treat extremely recalcitrant students. You come in with a paper draft and they say, no, that’s not good enough. Do another one.

LP: Have the individual creditors differed on how to treat Greece?

JG: There are some divisions amongst the creditors that are well known. But they’re all variations on the theme of insular, sheltered, cloistered people who do not understand what is happening in Greece and do not know the economics. So, for example, the European Commission tends to be a little bit nicer, the IMF tends to be better on debt restructuring but worse on the structural issues, and the ECB was infuriated by the fact that its technocrats couldn’t walk into any ministry in Athens and make demands and be paid attention to. So there were different aspects of this that seemed to trouble different creditors, but it all amounted to the fact that between them there was no basis for arriving at anything other than the original Memorandum of Understanding (bailout program).

LP: What exactly triggered the breakdown that led to the referendum?

JG: What happened was that the IMF took the staff level agreement draft that the Greeks had presented, and marked it up in red ink and presented it back to the Greeks as an ultimatum— this is what we will accept. Or rather (EC president) Juncker presented it back to the Greeks as an ultimatum. And Yanis was told, take it or leave it. So they basically had no choice but to walk away from it, to leave it.

LP: How do you think the referendum has changed the situation? Has it given the Greeks leverage or not?

JG: That’s a difficult question. The recent Ambrose Evans Pritchard piece is very much on the mark. The Greek government, and particularly the circle around Alexis, were worn down by this process. They saw that the other side does, in fact, have the power to destroy the Greek economy and the Greek society — which it is doing — in a very brutal, very sadistic way, because the burden falls particularly heavily on pensions. They were in some respects expecting that the yes would prevail, and even to some degree thinking that that was the best way to get out of this. The voters would speak and they would acquiesce. They would leave office and there would be a general election. But civil society took this over in the most dramatic and heroic fashion. It was an incredible thing to see. The Greeks, amazingly, voted 61% no. That, momentarily, gave a jolt of adrenaline to everybody in the government. But the next morning, they were back where they were before. And that’s why, of course, Yanis left at that point.

As the Greek saga continues, many have marveled at Germany’s chutzpah. It received, in real terms, one of the largest bailout and debt reduction in history and unconditional aid from the U.S. in the Marshall Plan. And yet it refuses even to discuss debt relief. Many, too, have marveled at how Germany has done so well in the propaganda game, selling an image of a long-failed state that refuses to go along with the minimal conditions demanded in return for generous aid. The facts prove otherwise: From the mid-90’s to the beginning of the crisis, the Greek economy was growing at a faster rate than the EU average (3.9% vs 2.4%). The Greeks took austerity to heart, slashing expenditures and increasing taxes.

They even achieved a primary surplus (that is, tax revenues exceeded expenditures excluding interest payments), and their fiscal position would have been truly impressive had they not gone into depression. Their depression—25% decline in GDP and 25% unemployment, with youth unemployment twice that—is because they did what was demanded of them, not because of their failure to do so. It was the predictable and predicted response to the austerity. The question now is: What’s next, assuming (as seems ever more likely) they are effectively thrown out of the euro? It’s likely that the European Central Bank will refuse to do its job—as the Central Bank for Greece, it should do what every central bank is supposed to do, act as a lender of last resort.

And if it refuses to do that, Greece will have no option but to create a parallel currency. The ECB has already begun tightening the screws, making access to funds more and more difficult. This is not the end of the world: Currencies come and go. The euro is just a 16-year-old experiment, poorly designed and engineered not to work—in a crisis money flows from the weak country’s banks to the strong, leading to divergence. GDP today is more than 17% below where it would have been had the relatively modest growth trajectory of Europe before the euro just continued. I believe the euro has much to do with this disappointing performance. [..]

The U.S. was generous with Germany as we defeated it. Now, it is time for the U.S. to be generous with our friends in Greece in their time of need, as they have been crushed for the second time in a century by Germany, this time with the support of the troika. At a technical level, the Federal Reserve needs to create a swap line with Greece’s central bank, which—as a result of the default of the ECB in fulfilling its responsibilities—will have to take on once again the role of lender of last resort. Greece needs unconditional humanitarian aid; it needs Americans to buy its products, take vacations there, and show a solidarity with Greece and a humanity that its European partners were not able to display.

“Greece is no-one’s hostage,” he said. “The Greek people’s No vote, and I am referring to all of the people, is not going to become a humiliating Yes.”

Greece has mapped out details of a landmark €2bn gas project with Russia, a scheme that could stir tensions with Brussels just as Athens seeks a third bail-out. Panayiotis Lafazanis, the firebrand leftist energy minister, presented the project to Greek energy executives on Thursday in a defiant speech, vowing that Athens would not be pushed around by EU institutions, writes Christian Oliver. EU policymakers are concerned that Russia could take advantage of the crisis to pull Greece deeper into its orbit and pipeline politics is critical to relations between the two nations. Athens and Moscow say their new project, the so-called South European Pipeline, will bring 47 billion cubic metres of Gazprom’s gas into Europe by 2018.

Mr Lafazanis promised that it would create 20,000 much needed jobs in Greece. This promised deal with Russia is a sharp rebuke to Brussels, which wants to reduce dependence on Gazprom and argues that southeastern Europe should diversify its supply by prioritising gas from Azerbaijan. Opening his remarks with pugnacious references to the eurozone crisis, Mr Lafazanis said that Greece was aiming to secure a deal with Brussels as quickly as possible. However, he then warned EU institutions that Athens was not about to roll over. “Greece is no-one’s hostage,” he said. “The Greek people’s No vote, and I am referring to all of the people, is not going to become a humiliating Yes.”

Germany conceded on Thursday that Greece would need some debt restructuring as part of any new loan programme to make its economy viable as the Greek cabinet raced to finalize reform proposals to avert an imminent economic meltdown. The admission by German Finance Minister Wolfgang Schaeuble came hours before a midnight deadline for Athens to submit a reform plan meant to convince European partners to give it another loan to save it from a possible exit from the euro. Greece has already had two bailouts worth €240 billion euros from the eurozone and the IMF, but its economy has shrunk by a quarter, unemployment is more than 25% and one in two young people is out of work.

Schaeuble, who has made no secret of his scepticism about Greece’s fitness to remain in the currency area, told a conference in Frankfurt: “Debt sustainability is not feasible without a haircut and I think the IMF is correct in saying that. But he added: “There cannot be a haircut because it would infringe the system of the European Union.” He offered no solution to the conundrum, which implied that Greece’s debt problem might not be soluble within the eurozone. But he did say there was limited scope for “reprofiling” Greek debt by extending loan maturities, shaving interest rates and lengthening a moratorium on debt service payments.

One of the great paradoxes of our time is how Germany has done so exemplary a job in recent decades of understanding and accepting responsibility for the horrors of the Nazi era while continuing to entertain a willful ignorance of the economic policy errors that paved the Nazis’ path to power. The solution to this riddle is that Germans’ deep-seated debt obsession (in German, the words for “debt” and “guilt” are the same) has blinded them to the consequences of that obsession. You’d think, for instance, that Germans would have learned from John Maynard Keynes’s 1920 book “The Economic Consequences of the Peace,” which correctly predicted that the onerous reparations inflicted on Germany by the Treaty of Versailles were economically unsustainable and politically perilous to the prospects for German democracy.

You’d think they’d have learned from their own descent into Nazism that balancing budgets when unemployment is at record heights can undermine a democracy’s viability. You’d think they’d have learned from the London debt agreement of 1953 that debt forgiveness and reasonable repayment terms can foster prosperity and strengthen democracy in the debtor nation — which, in this case, happened to be Germany. That Germans have learned none of these lessons is now — tragically, for Greece — apparent. Germany’s insistence that Greece continue to slash services and social investment if it is ever to qualify for debt forgiveness remains unaltered, even though Greek unemployment stands at 25%, even though 40% of Greek children live in poverty, even though a neo-Nazi party (Golden Dawn) has come out of nowhere to win seats in Greece’s parliament.

Jens Weidmann, the president of Germany’s Bundesbank, has said doubts about Greek banks solvency are legitimate and rising by the day. Mr Weidmann also said the majority of Greeks who had voted ‘no’ in Sunday’s referendum had spoken out .. against contributing any further to the solvency of their country through additional consolidation measures and reforms. The Bundesbank president, a member of the governing council of the European Central Bank who has called for Greek banks ¨ 89bn liquidity lifeline to be scrapped, said in needed to be crystal clear that responsibility for Greece lay with Athens and international creditors, and not the ECB.

The Eurosystem [of eurozone central banks] should not increase the liquidity provision, and capital controls need to stay in force until an appropriate support package has been agreed by all parties and the solvency of both the Greek government and the Greek banking system has been ensured. The Bundesbank president hit out at Athens for causing economic ruin. [Eurozone member states] can decide for themselves not to service their debts, to collect taxes inadequately, and this is something I particularly fear in the case of Greece to lead their country s economy into deep trouble, he said in Frankfurt on Wednesday. The Syriza-led government had not only walked out on the previous agreements, but has been widely criticised as an unreliable negotiating partner. Mr Weidmann’s comments came as France s finance minister Michel Sapin, who is pushing for a deal that would allow Greece to stay in the eurozone, emphasised the greater cost of a Grexit.

“What s costlier? That Greece exits the eurozone and defaults on all its debt? Asking the question is answering it”, Mr Sapin told Radio Classique on Thursday. “A deal is the best solution for Greece and Europe.” “Greek banks have been closed for more than a week. Greece is already in a pre-chaos stat”e, he said. “How history will judge us?” However, Mr Sapin reiterated the need for the Greek government to present credible reforms as well as difficult decisions to balance the budget. “There are taxes to raise, it’s difficult,” he said. Mr Sapin saluted the good attitude of Greek Finance Minister Euclid Tsakalotos at the latest eurogroup meeting of finance ministers. “He came with a lot of modesty”, he said.

A senior member of Greece’s negotiating team with its European creditors agreed to a meeting last week in Athens with Mediapart special correspondent Christian Salmon. Speaking on condition that his name is withheld, he detailed the history of the protracted and bitter negotiations between the radical-left Syriza government, elected in January, and international lenders for the provision of a new bailout for the debt-ridden country. The almost two-hour interview in English took place just days before last Sunday’s referendum on the latest drastic austerity-driven bailout terms offered by the creditors, and opposed by Prime Minister Alexis Tsipras, and which were finally rejected by 61.3% of Greek voters.

While the ministerial advisor slams the stance of the international creditors, who he accuses of leading a strategy of deliberate suffocation of Greece’s finances and economy, he is also critical of some of the decisions taken by Athens. His account also throws light on the personal tensions surrounding the talks led by former Greek finance minister Yanis Varoufakis, who resigned from his post on Monday deploring “a certain preference by some Eurogroup participants, and assorted ‘partners’, for my ‘absence’ from its meetings”. The advisor cites threats proffered to Varoufakis by Eurogroup president Jeroen Dijsselbloem, warning he would sink Greece’s banks unless the Tsipras government bowed to the harsh deal on offer, and by German finance minister Wolfgang Schäuble, who he says demanded: “How much money do you want to leave the euro?”

Struggling to pay off more than €300 billion in debts, Greece is banking on Switzerland to help it recover a treasure trove of undeclared assets that tax cheats have stashed in alpine vaults. But anti-tax haven campaigners are sceptical about “undemocratic” tax amnesties that are prone to loopholes, allowing many tax dodgers to wriggle out of their obligations. “The devil is always in the detail with these deals. If Switzerland can claim it is helping to clear untaxed assets out of its banks, this could provide it with a public relations service,” Nicholas Shaxson of Tax Justice Network told swissinfo.ch. “But amnesties generally favour wealthy people who can pay accountants to exploit loopholes, such as insurance wrappers and discretionary trusts.”

Such “slippery structures” render assets “technically declared”, allowing them to remain offshore under the radar of amnesties, Shaxson added. “Tax amnesties only make a difference if the public believe that, once they have ended, the government will assertively go after people who did not disclose,” Heather Low of Global Financial Integrity (GFI) told swissinfo.ch. “Tax cheats in the United States would be afraid of the authorities if they did not disclose during an amnesty. I’m not so sure this would be the case in Greece.” In April, former Greek Finance Minister Yanis Varoufakis announced plans for a global tax amnesty to repatriate overseas funds to Greece. It is believed the government has settled for a one-off 21% levy on those who come clean, pending parliamentary approval of the proposal.

Negotiations between Greece and Switzerland on how best to recover black money hidden in Swiss banks have been ongoing since 2012. But the two sides are reported to be edging closer to a solution that would allow banks to cooperate. While Switzerland would not be an official partner to a Greek tax amnesty, the approval and cooperation of the Swiss authorities would be integral to the scheme working. To this end, two meetings were arranged between the countries in March and April to discuss the practical details of persuading Greek tax cheats to sign up to the amnesty. While not yet concluded, Varoufakis felt encouraged enough to announce Greece’s intended global tax amnesty following a meeting with Swiss officials in April.

The mainstream news is painting the Greeks as the bad guys, and the Troika as the savior of Europe. Quite frankly, it is really disgusting. Pictures of an elderly Greek pensioner have gone viral, depicting what the Troika is deliberately doing to the Greek people by punishing them for their own failed design of the euro in a system that is just economically unsustainable. The heartbreaking photographs circulating are of 77-year-old retiree, Giorgos Chatzifotiadis, after he collapsed on the ground openly in tears, driven to despair, outside a Greek bank with his savings book and identity card strewn next to him on the ground. This illustrates the horror the Troika is deliberately inflicting upon the Greek population.

This image illustrates the core of the issue: ordinary Greeks tormented by EU politicians who pretend to care about people. This is not a Greek debt crisis, this is a Euro Crisis and they refuse to admit that what they designed was solely for the takeover of Europe at the cost of the future of everyone, from pensioners to the youth. Chatzifotiadis queued up at three banks in Greece’s second city of Thessaloniki on Friday in the hope of withdrawing pensions on behalf of him and his wife. When he went to a fourth bank, he was told he could not withdraw his €120; the ordeal simply became too much and he fell down in tears in total desperation. His comments were simply that he “cannot stand to see my country in this distress”. He continued to say, “That’s why I feel so beaten, more than for my own personal problems.”

This is just the tip of the iceberg. We are facing terrible times ahead because socialism is completely collapsing. Government employees have lined their pockets, which is precisely the endgame and how Rome collapsed. It was not the barbarians at the gate. It was that the Roman army was not paid and they began hailing their various generals as emperor and they attacked cities who did not support their choice. Only after weakening themselves, then the barbarians came in for easy pickings. If Russia really wants to take Europe, all they have to do is be patient. They will self-destruct for the Troika cannot see any change in thinking for that means they must admit that they were wrong from the outset.

Former Greek Finance Minister Yanis Varoufakis admitted that Germany appears to have a plan to force Greece outside the Eurozone, even though while he was in office he insisted that Grexit scenarios were a bluff to push the Greek government to accept harsh austerity measures. Talking with reporters at the Greek Parliament café, Varoufakis noted that Wolfgang Schaeuble is the only Eurozone Minister with a specific plan. He also said that the German Finance Minister completely controls the majority of the Eurogroup except for French Finance Minister Michel Sapin.

“Schaeuble has a plan for Greece’s exit from the Eurozone,” and added, “this is his best chance to succeed.” When asked if he believes the Germans are taking into account the estimated cost of a Grexit, Varoufakis argued that Schaeuble believes losses can be controlled. Furthermore, the former Greek Finance Minister stated that it is possible that his exit from the Greek government was due to Schaeuble’s pressure.

As for whether he believes that a deal will be achieved in the next 24 hours, he initially said “no comment” but later added: “I would like an agreement to be reached but only if it is also a solution. At the moment, we cannot judge the outcome.” People at the café called him “Minister” but he always answered: “I’m not a Minister. I’m a member of Parliament.” “Once a Minister, always a Minister,” he said, adding that he prefers to be an MP and be called Yanis. Asked to comment on the recent referendum results, he stated that the outcome was epic and grandiose, although he avoided to answer the question about whether the citizens voted “No” but the government is following the “Yes” direction.

Taken from Keiser Report episode 247 & 301 a look back at the dialogue between Max & Yanis in 2012 which should give some insight into the battle with financial terrorism unfolding in Greece.

“There’s quite precisely no common ground between the two belief systems, and yet self-proclaimed Christians who spout Rand’s turgid drivel at every opportunity make up a significant fraction of the Republican Party just now.”

Our age has no shortage of curious features, but for me, at least, one of the oddest is the way that so many people these days don’t seem to be able to think through the consequences of their own beliefs. Pick an ideology, any ideology, straight across the spectrum from the most devoutly religious to the most stridently secular, and you can count on finding a bumper crop of people who claim to hold that set of beliefs, and recite them with all the uncomprehending enthusiasm of a well-trained mynah bird, but haven’t noticed that those beliefs contradict other beliefs they claim to hold with equal devotion. I’m not talking here about ordinary hypocrisy. The hypocrites we have with us always; our species being what it is, plenty of people have always seen the advantages of saying one thing and doing another.

No, what I have in mind is saying one thing and saying another, without ever noticing that if one of those statements is true, the other by definition has to be false. My readers may recall the way that cowboy-hatted heavies in old Westerns used to say to each other, “This town ain’t big enough for the two of us;” there are plenty of ideas and beliefs that are like that, but too many modern minds resemble nothing so much as an OK Corral where the gunfight never happens. An example that I’ve satirized in an earlier post here is the bizarre way that so many people on the rightward end of the US political landscape these days claim to be, at one and the same time, devout Christians and fervid adherents of Ayn Rand’s violently atheist and anti-Christian ideology.

The difficulty here, of course, is that Jesus tells his followers to humble themselves before God and help the poor, while Rand told hers to hate God, wallow in fantasies of their own superiority, and kick the poor into the nearest available gutter. There’s quite precisely no common ground between the two belief systems, and yet self-proclaimed Christians who spout Rand’s turgid drivel at every opportunity make up a significant fraction of the Republican Party just now. Still, it’s only fair to point out that this sort of weird disconnect is far from unique to religious people, or for that matter to Republicans. One of the places it crops up most often nowadays is the remarkable unwillingness of people who say they accept Darwin’s theory of evolution to think through what that theory implies about the limits of human intelligence.

If Darwin’s right, as I’ve had occasion to point out here several times already, human intelligence isn’t the world-shaking superpower our collective egotism likes to suppose. It’s simply a somewhat more sophisticated version of the sort of mental activity found in many other animals. The thing that supposedly sets it apart from all other forms of mentation, the use of abstract language, isn’t all that unique; several species of cetaceans and an assortment of the brainier birds communicate with their kin using vocalizations that show all the signs of being languages in the full sense of the word—that is, structured patterns of abstract vocal signs that take their meaning from convention rather than instinct.

Pope Francis on Thursday urged the downtrodden to change the world economic order, denouncing a “new colonialism” by agencies that impose austerity programs and calling for the poor to have the “sacred rights” of labor, lodging and land. In one of the longest, most passionate and sweeping speeches of his pontificate, the Argentine-born pope also asked forgiveness for the sins committed by the Roman Catholic Church in its treatment of native Americans during what he called the “so-called conquest of America.” Quoting a fourth century bishop, he called the unfettered pursuit of money “the dung of the devil,” and said poor countries should not be reduced to being providers of raw material and cheap labor for developed countries.

Repeating some of the themes of his landmark encyclical “Laudato Si” on the environment last month, Francis said time was running out to save the planet from perhaps irreversible harm to the ecosystem. Francis made the address to participants of the second world meeting of popular movements, an international body that brings together organizations of people on the margins of society, including the poor, the unemployed and peasants who have lost their land. The Vatican hosted the first meeting last year. He said he supported their efforts to obtain “so elementary and undeniably necessary a right as that of the three “L’s”: land, lodging and labor.”