Marjory Collins “Crowds at Pennsylvania Station, New York” 1942

How is this going to affect Apple and Microsoft sales in China?

• WikiLeaks Says Just 1% Of #Vault7 Covert Documents Released So Far (RT)

WikiLeaks’ data dump on Tuesday accounted for less than 1% of ‘Vault 7’, a collection of leaked CIA documents which revealed the extent of its hacking capabilities, the whistleblowing organization has claimed on Twitter. ‘Year Zero’, comprising 8,761 documents and files, was released unexpectedly by WikiLeaks. The organization had initially announced that it was part of a larger series, known as ‘Vault 7.’ However, it did not give further information on when more leaks would occur or on how many series would comprise ‘Vault 7’. The leaks have revealed the CIA’s covert hacking targets, with smart TVs infiltrated for the purpose of collecting audio, even when the device is powered off. The Google Android Operating System, used in 85% of the world’s smartphones, was also exposed as having severe vulnerabilities, allowing the CIA to “weaponize” the devices.

The CIA would not confirm the authenticity of the leak. “We do not comment on the authenticity or content of purported intelligence documents.” Jonathan Liu, a spokesman for the CIA, is cited as saying in The Washington Post. WikiLeaks claims the leak originated from within the CIA before being “lost” and circulated amongst “former U.S. government hackers and contractors.” From there the classified information was passed to WikiLeaks. End-to-end encryption used by applications such as WhatsApp was revealed to be futile against the CIA’s hacking techniques, dubbed ‘zero days’, which were capable of accessing messages before encryption was applied. The leak also revealed the CIA’s ability to hide its own hacking fingerprint and attribute it to others, including Russia. An archive of fingerprints – digital traces which give a clue about the hacker’s identity – was collected by the CIA and left behind to make others appear responsible.

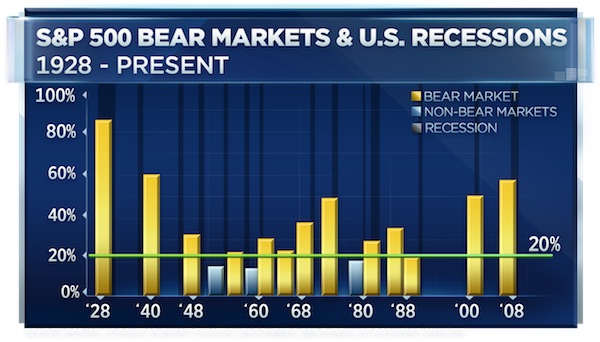

The Trump bull is alive for now.

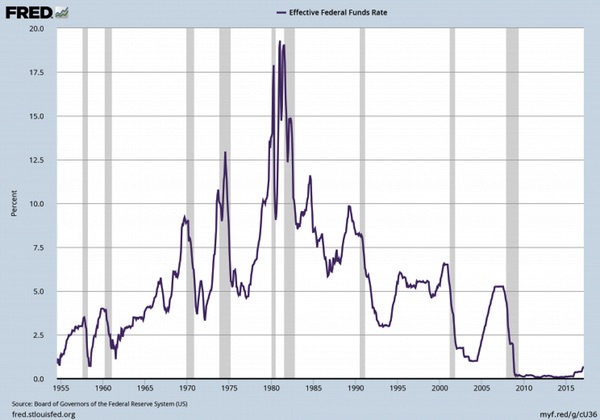

• US Private Sector Adds 298,000 Jobs In February – ADP (R.)

U.S. private employers added 298,000 jobs in February, well above economists’ expectations, a report by a payrolls processor showed on Wednesday. Economists surveyed by Reuters had forecast the ADP National Employment Report would show a gain of 190,000 jobs, with estimates ranging from 150,000 to 247,000. Private payroll gains in the month earlier were revised up to 261,000 from an originally reported 246,000 increase. The ADP figures come ahead of the U.S. Labor Department’s more comprehensive non-farm payrolls report on Friday, which includes both public and private-sector employment. Economists polled by Reuters are looking for U.S. private payroll employment to have grown by 193,000 jobs in February, down from 237,000 the month before. Total non-farm employment is expected to have changed by 190,000. The unemployment rate is forecast to tick down to 4.7% from the 4.8% recorded a month earlier.

How much of it will be put to good use, and how much merely siphoned off?

• Trump Begins to Map Out $1 Trillion Infrastructure Plan (WSJ)

President Donald Trump pushed his White House team on Wednesday to craft a plan for $1 trillion in infrastructure spending that would pressure states to streamline local permitting, favor renovation of existing roads and highways over new construction and prioritize projects that can quickly begin construction. “We’re not going to give the money to states unless they can prove that they can be ready, willing and able to start the project,” Mr. Trump said at a private meeting with aides and executives that The WSJ was invited to. “We don’t want to give them money if they’re all tied up for seven years with state bureaucracy.” Mr. Trump said he would was inclined to give states 90 days to start projects, and asked Scott Pruitt, the new head of the EPA, to provide a recommendation.

He expressed interest in building new high-speed railroads, inquired about the possibility of auctioning the broadcast spectrum to wireless carriers, and asked for more details about the Hyperloop, a project envisioned by Tesla founder Elon Musk that would rapidly transport passengers in pods through low-pressure tubes. “America has always been a nation of great promise, because we dream big,” Mr. Trump said. “We’re going to really dream big now.” The president called for a $1 trillion infrastructure plan last month in his address to a joint session of Congress and added that the projects would be financed through public and private capital. The White House was considering a repatriation tax holiday to generate about $200 billion in funding, but other sources also were being considered, a senior administration aide said.

In the meeting, the president said he aimed to win approval for an infrastructure plan once Congress finishes deliberations on health care and a reform of tax laws. Mr. Trump suggested that an infrastructure plan may be part of the tax-reform debate. “We’ll see what happens,” he said. Vice President Mike Pence, who sat across from the president during the meeting, said that Congress is “committed to the president’s vision.” “There’s a great of interest in Congress in doing this,” Mr. Pence said. “But there’s also just as much interest in listening to leaders in the private sector to identify the capital and identify the needs to be able to finance this in a way that really captures the energy of the American economy.”

Time to acknowledge demand isn’t coming back?

• US Oil Price Plunges Toward $50 As A Perfect Storm Brews (CNBC)

Oil is on track to break through the key psychological level of $50 a barrel after a ninth straight rise in U.S. crude stockpiles came at exactly the wrong moment, analysts said Wednesday. The amount of crude oil in U.S. storage rose to another record high on Wednesday, jumping 8.2 million barrels from the previous week, the Energy Information Administration reported. The increase was more than four times what analysts expected. Weekly figures also showed U.S. oil production continuing to tick up toward 9.1 million barrels a day, the highest level in more than a year. That provided further evidence that rising American output is confounding efforts by OPEC, Russia and 10 other exporters to reduce global oil inventories by curbing their own output. The data sent U.S. benchmark West Texas Intermediate crude prices plunging more than 5% to a nearly three-month low.

The plunge through a number of lows on Wednesday puts oil on a path to test the December low of $49.95 a barrel, said John Kilduff at energy hedge fund Again Capital. “From there you could accelerate,” he told CNBC, adding that $50 “was the fail-safe.” Kilduff’s downside target, once oil breaks below $50 a barrel, is $42. For the last three months, oil has traded in a range between $49.61 and $55.24. According to Kilduff, all the elements are in place for oil to break below its three-month range: lack of cohesion among OPEC members, bearish statements from oil ministers at CERAWeek conference by IHS Markit and subdued refinery activity as operators perform seasonal maintenance in the United States. On Tuesday, Saudi Oil Minister Khalid al-Falih warned at CERAWeek that the kingdom would only support OPEC’s intervention in markets for a “restricted period of time” and would not “underwrite the investments of others at our own expense and long-term interests.”

Snippets from an interview. The euro was doomed from the start because of conditions put on it.

• Professor Steve Keen On The Problem With Europe (DR)

But the trouble is, you see, they didn’t have to have a single currency combined with the 60% limit on government debt and the 3% limit on government deficits. If they simply had a currency and made no rules whatsoever about that, then it would have been feasible, potentially, to say okay, well it’s not working as well as we would like it to, but not imposing austerity on economies in a downturn, which is what they ended up doing courtesy of those rules. Maybe we need a treasury to make it work better, but it wasn’t just the fact that it was only the central bank, it was also the rules on government spending.

[..] another part of it, which is quite intriguing, I heard in Berlin just recently, is that also, one of the other rules they agreed to, or one of the other objectives they agreed to, not a rule, was to target a 2% rate of inflation. Now what you actually had happen was that Germany hit about 1%, France actually hit about 2%, Italy hit about 3%, the three major trading partners of course on the block. Well, that means, as a result, over every year, German manufacturers were gaining a 2% cost advantage over Italian manufacturers. Which ultimately means of course that people don’t buy Lamborghinis and Fiats anymore, they buy Mercedes, because for the same features they’re cheaper.

It’s not about labour productivity alone, it’s about the rate of inflation, which comes down to the rate of wage change, because the Germans suppressed the rate of wage change, the rate of inflation was lower, and that was 1% below the level they agreed to. Now, if they’d agreed to 2%, and France did 2%, and Italy maybe suppressed its wage change and they hit 2%, you wouldn’t have these imbalances. But they’ve built up over 15 – going on close to 20 years now – and those level of imbalances mean that, fundamentally, Italian industry can’t compete with German industry, not because of productivity differences so much but wage costs combined with that.

[..] That’s why Trump’s complaining about Germany having an undervalued currency, and he’s bloody right on that front. If you can run a 9% of GDP trade surplus, which is the level Germany’s now hit, a lot of that is with the rest of the world, the EU itself overall is balanced, so there’s a huge imbalance – Germany’s got a huge trade surplus with the rest of Europe, but it’s also got it with the rest of the world, and on that scale I think Germany’s trade balance now is the same scale as China’s. Now that’s ludicrous.

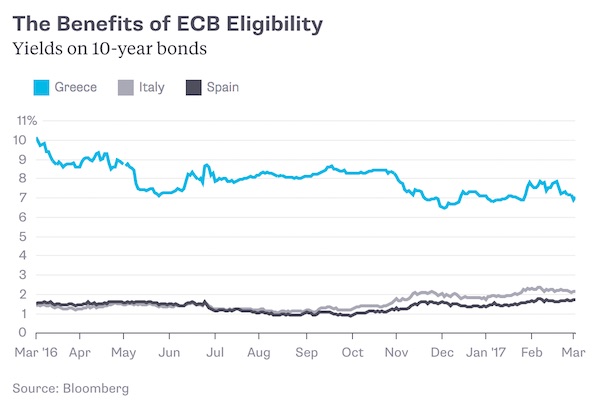

Perhaps the biggest problem with Europe is that transparency and the EU don’t mix. In this case it’s clear why: the ECB was used as a -very blunt- tool for political pressure. Their defense is basically: if we become transparent, we’re no longer independent. And people buy that?!

• Varoufakis Back In Brussels In Push For ECB Transparency (EUO)

Former Greek finance minister Yanis Varoufakis has joined forces with the German left-wing MEP Fabio De Masi in a bid to clarify whether the ECB had a legal right to limit the liquidity of Greece’s banks in 2015. The duo told journalists in Brussels on Wednesday (8 March) that they were collecting signatures for a petition to ECB president Mario Draghi, asking him to disclose two legal opinions commissioned by the bank. The first study was ordered in February, before the ECB decided to limit the access of Greek banks to ECB funding and opted instead to open access to the emergency liquidity assistance (ELA) – a fund with more restrictive access conditions. The decision was taken a few days after the radical left-wing Syriza party came to power, with Varoufakis as finance minister.

The second study, in June 2015, was about the ECB’s decision to freeze the amount of money available through the ELA after the Greek government’s decision to hold a referendum on the bailout conditions required by the country’s creditors. The measure was taken over concerns that Greek banks would become insolvent because of the deadlock in bailout talks. It also put more pressure on the Greek government to accept the lenders’ conditions. To avoid a bank run, where large numbers of people withdraw money from their deposit accounts at the same time, the government introduced capital controls. This meant that Greek people were only able to withdraw a maximum of €60 per day. The measure prevented a capital run, but also put pressure on Athens to agree to creditors’ terms for a third bailout.

Varoufakis, who was finance minister at the time, said this was a breach of the independence of the bank. “The ECB has the capacity to close down all the banks of a member state. At the same time, it has a charter which grants it – supposedly – complete independence from politics. And yet, there is no central bank, at least in the West, which has less independence of the political process,” Varoufakis said. He said Draghi was “completely reliant” on the decisions of an “informal group of finance ministers”, referring to the fact that the Eurogroup, which gathers the finance ministers of the 19 eurozone countries, isn’t enshrined in EU treaties. “It is apparent that Draghi didn’t feel that the was on solid legal ground when proceeding with the closing of Greek banks,” Varoufakis said.

[..] In September 2015, Fabio De Masi already asked Draghi for the opinions. But the ECB chief, in a letter made public by the MEP, said the bank does not plan to publish the legal opinions because this would “undermine the ECB’s ability to obtain uncensored, objective and comprehensive legal advice, which is essential for well-informed and comprehensive deliberations of its decision-making bodies”. “Legal opinions provided by external lawyers and related legal advice are protected by legal professional privilege (the so-called ‘attorney-client privilege’) in accordance with European Union case law,” Draghi said. “Those opinions were drafted in full independence, on the understanding that they can only be disclosed by the addressee and only shared with people who need to know in order to take reasoned decisions on the issues at stake,” he added.

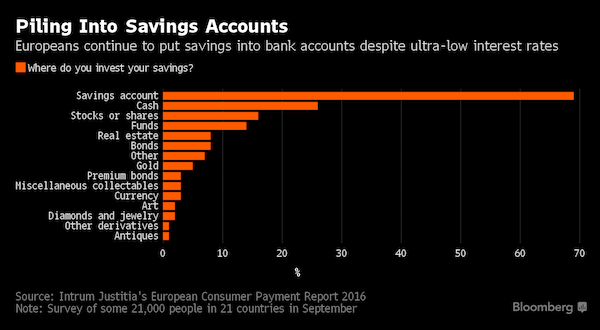

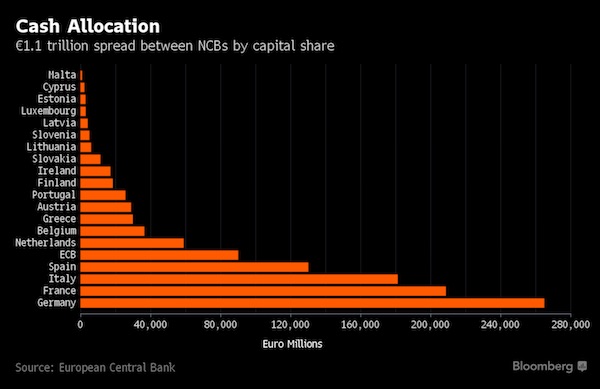

No cashless society there.

• Germans Really, Really Love the Euro (BBG)

As worries over the future of the euro zone heat up, the union’s biggest member is doubling down on the single currency in an underappreciated way. Germany’s central bank is by far the biggest issuer of cash in the bloc, with the Bundesbank the source of more euro banknotes in circulation than all of its peers combined. The size of the imbalance is underscored by new data from the ECB, showing nations’ contributions towards the Eurosystem’s consolidated financial statement. Each national central bank, or NCB, has a notional banknote allocation that’s tied to its share of Eurosystem capital. At the end of last year, there were €1.1 trillion euros ($1.25 trillion) in circulation, breaking down like this:

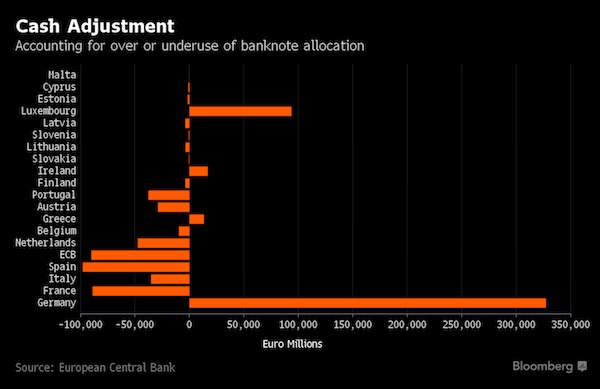

That accounts for how euro cash would be distributed in theory. In order to find out how much cash is actually issued you have to make adjustments that take into account variations in demand, which push the number higher in some countries and lower in others. The adjustments look like this:

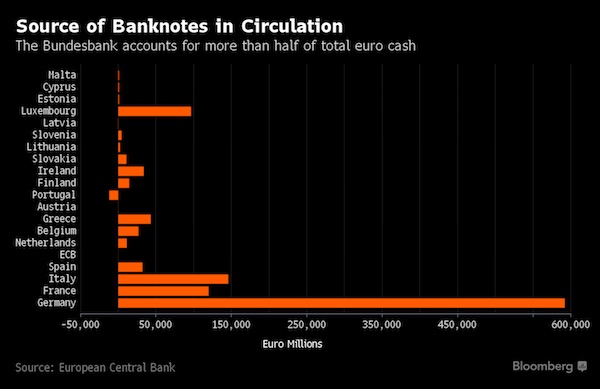

The Bundesbank has, since the introduction of the euro in 2002, put a net €327 billion into circulation above its on-paper allocation. By combining the figures in the two charts, we arrive at a true picture of the origin of banknotes in the European economy:

“The mainstream media are not honorable independent people. They are big business not much different from the banks.”

• The Meltdown in Politics (Martin Armstrong)

The bias of the press is getting so bad, they are undermining everything they were supposed to stand for. This is a critical aspect in the decline and fall of an empire, nation, or city state. Once the news is compromised, confidence not just in the press, but in everything crumbles. The mainstream media are not honorable independent people. They are big business not much different from the banks. They lobby for their special deals and the support the status quo. The New York Times at least admitted their coverage of the election was biased. They apologized, but nothing has really changed. “As we reflect on the momentous result, and the months of reporting and polling that preceded it, we aim to rededicate ourselves to the fundamental mission of Times journalism. That is to report America and the world honestly, without fear or favor, striving always to understand and reflect all political perspectives and life experiences in the stories that we bring to you. It is also to hold power to account, impartially and unflinchingly.”

Even if Trump met with Putin, exactly what does that infer? Did it alter the election? No. Even Obama admitted that no hack altered the vote count. So what is the issue? The press aids the Democrats in trying to blame Putin for Hillary’s loss. But there is not a single shred of evidence that ANY of the leaked emails from the Democrats was ever altered or was fake. The Democrats simply got caught with their hand in the cookie jar and blame Putin. So what is all this Russia thing about? It seems to be just a diversion to discredit Trump and stop the agenda of any reform. A simple technical analysis of Democrat v Republican shows that the former is in a major decline and their agenda has been dying. In fact, look out for 2018-2019. Sheer chaos is coming.

In Europe, political forces are also in a state of denial. The EU is collapsing and the politicians refuse to surrender their goals. Instead, they lash out at what they are calling “populism” as with the election of Trump, BREXIT, and the developments in France. The will of the people is not worth anything when it goes against their dreams. So in both cases, we are witnessing the demise of the West. All of this political fighting is setting the stage for the shift from the West to the East of financial power. The wheel of fortune spins. We lost. What is accomplished by overthrowing Trump? What is accomplished by forcing Europe to remain in the EU with unelected people controlling everything from Brussels? If the press succeeds in overturning Trump, what is accomplished? Do they really think everything can go back to the way it was before?

[..] the media in the USA has degenerated to fake news, but in Europe the very same trend has emerged. This is a serious nail in our coffin and mainstream media has indeed become the sword of our own destruction. Can we prevent this outcome? No. All we can do is hopefully learn from our mistakes and this time try to create a system that prevents such an oligarchy from rising. All Republics historically collapse into oligarchies. As we head into 2018, this is going to get really bad. This is going to be a turning point of great importance in the political world.

A president without a party. Or a program. Doesn’t seem to add up.

• Macron Faces A Really Big Problem If He Becomes French President (Con.)

Currently riding high in the polls, Emmanuel Macron, the self-styled “beyond left and right” candidate for the French election, has been tipped to become the next president in May. But if he does, will he actually run the country? This question might sound odd but the nuances of the French political system put Macron in a spot of bother. The president derives their power from the support of a majority in the lower house of parliament, the National Assembly. Macron was a minister for the Socialist Party government but quit in 2016 to form his own political movement. Now he doesn’t even have a party, let alone a majority. Although the constitution of the French Fifth Republic, created by Charles De Gaulle in 1958, extended presidential powers, it did not enable the president to run the country.

There are only a few presidential powers that do not need the prime minister’s authorisation. The president can appoint a prime minister, dissolve the National Assembly, authorise a referendum and become a “temporary dictator” in exceptional circumstances imperilling the nation. They can also appoint three judges to the Constitutional Council and refer any law to this body. While all important tasks, this does not, by any stretch of the imagination, amount to running a country. The president can’t suggest laws, pass them through parliament and then implement them without the prime minister. The role of a president is best defined as a “referee”. Presidential powers give the ability to oversee operations and act when the smooth running of institutions is impeded.

So a president is able to step in if a grave situation arises or to unlock a standoff between the prime minister and parliament, such as by announcing a referendum on a disputed issue or by dismissing the National Assembly. So, why does everyone see the president as the key figure? In a nutshell, it’s because the constitution has never been truly applied. There lies the devilish beauty of French politics. A country known since the 1789 revolution for its inability to foster strong majorities in parliament has succeeded, from 1962, in providing solid majorities.

This is what happens everywhere, in varying ways. In France, both establishment blocks look to be cast aside.

• French Insurgents Thrust Establishment Aside in Crucial Election (BBG)

The old order is fading in France. Every election since Charles de Gaulle founded the Fifth Republic more than half a century ago has seen at least one of the major parties in the presidential runoff and most have featured both. With Republicans and Socialists consumed by infighting and voters thoroughly fed up, polls suggest that neither will make it this year. For the past month, survey after survey has projected a decider between Emmanuel Macron, a 39-year-old rookie who doesn’t even have a party behind him, and Marine Le Pen, who’s been ostracized throughout her career because of her party’s history of racism. “We’ve gone as far as we can go with a certain way of doing politics,” said Brice Teinturier, head of the Ipsos polling company and author of a book on voters’ disillusionment. “Everyone feels the system is blocked.”

Claude Bartolone, the Socialist president of the National Assembly, said in an interview with Le Monde Tuesday he may back Macron because he doesn’t “identify” with the more extreme platform put forward by his party’s candidate Benoit Hamon. De Gaulle’s latest standard-bearer Francois Fillon has spent the past week facing down rebellions in his party triggered by a criminal probe of his finances. Former Prime Minister Manuel Valls hasn’t campaigned for Hamon since losing to him in the primary and Socialist President Francois Hollande hasn’t even endorsed his party’s candidate either. Instead, senior figures from the Socialist camp are endorsing Macron, with former Paris Mayor Bertrand Delanoe the latest to offer his backing on Wednesday. “There’s a breakdown of parties in France,” Francois Bayrou, a two-time centrist candidate who is now backing Macron, said Tuesday on RMC Radio. “There are hostile battles between factions within each party, which has ruined the parties and ruined the image of politics.”

Crazy that such differences still persist.

• Iceland First Country In The World To Make Firms Prove Equal Pay (Ind.)

On International Women’s Day, Iceland became the first country in the world to force companies to prove they pay all employees the same regardless of gender, ethnicity, sexuality or nationality, The country’s government announced a new law that will require every company with 25 or more staff to gain a certificate demonstrating pay equality. Iceland is not the first country to introduce a scheme like this – Switzerland has one, as does the US state of Minnesota – but Iceland is thought to be the first to make it a mandatory requirement. Equality and Social Affairs Minister Thorsteinn Viglundsson said that “the time is right to do something radical about this issue.” “Equal rights are human rights. We need to make sure that men and women enjoy equal opportunity in the workplace. It is our responsibility to take every measure to achieve that,” he said.

The move comes as part of a drive by the Nordic nation to eradicate the gender pay gap by 2022. In October, thousands of female employees across Iceland walked out of workplaces at 2.38pm to protest against earning less than men. After this time in a typical eight-hour day, women are essentially working without pay, according to unions and women’s organisations. Iceland has been at the forefront of establishing pay equality, having already introduced a minimum 40% quota for women on boards of companies with more than 50 employees. The country has been ranked the best in the world for gender equality by the World Economic Forum for eight years running, but despite this, Icelandic women still earn 14 to 18% less than men, on average.

“Cleaning up the plant [..] is expected to take 30 to 40 years, at a cost Japan’s trade and industry ministry recently estimated at 21.5tr yen ($189bn).” Uh, no, it will cost far more than $189 billion, and it’s to NOT clean up the plant. They have no idea how to do it. It’s all just fantasy.

• Fukushima Clean-Up Falters 6 Years After Tsunami (G.)

Barely a fifth of the way into their mission, the engineers monitoring the Scorpion’s progress conceded defeat. With a remote-controlled snip of its cable, the latest robot sent into the bowels of one of Fukushima Daiichi’s damaged reactors was cut loose, its progress stalled by lumps of fuel that overheated when the nuclear plant suffered a triple meltdown six years ago this week. As the 60cm-long Toshiba robot, equipped with a pair of cameras and sensors to gauge radiation levels was left to its fate last month, the plant’s operator, Tokyo Electric Power (Tepco), attempted to play down the failure of yet another reconnaissance mission to determine the exact location and condition of the melted fuel. Even though its mission had been aborted, the utility said, “valuable information was obtained which will help us determine the methods to eventually remove fuel debris”.

The Scorpion mishap, two hours into an exploration that was supposed to last 10 hours, underlined the scale and difficulty of decommissioning Fukushima Daiichi – an unprecedented undertaking one expert has described as “almost beyond comprehension”. Cleaning up the plant, scene of the world’s worst nuclear disaster since Chernobyl after it was struck by a magnitude-9 earthquake and tsunami on the afternoon of 11 March 2011, is expected to take 30 to 40 years, at a cost Japan’s trade and industry ministry recently estimated at 21.5tr yen ($189bn). The figure, which includes compensating tens of thousands of evacuees, is nearly double an estimate released three years ago. The tsunami killed almost 19,000 people, most of them in areas north of Fukushima, and forced 160,000 people living near the plant to flee their homes. Six years on, only a small number have returned to areas deemed safe by the authorities.

[..] Shaun Burnie, a senior nuclear specialist at Greenpeace Germany who is based in Japan, describes the challenge confronting the utility as “unprecedented and almost beyond comprehension”, adding that the decommissioning schedule was “never realistic or credible”. The latest aborted exploration of reactor No 2 “only reinforces that reality”, Burnie says. “Without a technical solution for dealing with unit one or three, unit two was seen as less challenging. So much of what is communicated to the public and media is speculation and wishful thinking on the part of industry and government. “The current schedule for the removal of hundreds of tons of molten nuclear fuel, the location and condition of which they still have no real understanding, was based on the timetable of prime minister [Shinzo] Abe in Tokyo and the nuclear industry – not the reality on the ground and based on sound engineering and science.”

And it will remain in recession for a long time.

• Eurostat: Greece Is The Only EU Country Still In Recession (NE)

Household consumption and a rebound in investment drove economic growth in the euro zone in the last three months of last year, the latest data from EU statistics office Eurostat shows. Eurostat confirmed its earlier estimate that the economy of the 19 countries sharing the euro grew 0.4% quarter-on-quarter and 1.7% year-on-year. It said household consumption added 0.2 % points to the final quarterly growth number and capital investment added another 0.1 points, rebounding from a 0.1 point negative contribution in the third quarter. Growing inventories added another 0.1 points and government spending another 0.1 points while net trade subtracted 0.1 points.

Greece was the only country that was in negative territory, with GDP declining by 1.1% compared with the last quarter of 2015 and by 1.2% compared to the third quarter of 2016. Combined, the eurozone continued steady recovery, with the economy growing by 1.7% year on year and 0.4% on a quarterly basis. Messages were positive in the eurozone core. Germany grew by 1.8% and France by 1.2%, while the third largest economy of the euro, Italy, increasing by 1%. Impressive was the growth of Spain as it reached 3%. Social protection spending in Greece represented 20.5 % of the country’s GDP in 2015.

This is slightly higher than both the Eurozone average ratio (20.1% of GDP) and the EU28 average ratio (19.2% of GDP). Social protection expenditure in EU member-states ranged from 9.6% of GDP in Ireland to 25.6% of GDP in Finland in that year. Eight member-states (Finland, France, Denmark, Austria, Italy, Sweden, Greece and Belgium) spent more than 20% of GDP on social protection while Ireland, the Baltic states, Romania, Cyprus, Malta and the Czech Republic spend less than 13%.

“Tax rates are expected to reach 26%, while pensions are being cut by as much as 22% by 2022.”

• Greek Farmers Clash With Riot Police In Athens Over Austerity (G.)

Farmers who travelled to Athens from Crete have clashed with riot police in the latest unrest on the streets of the Greek capital, prompted by the government’s austerity policies. The confrontation occurred outside the agriculture ministry, where farmers wielding staffs engaged with police firing teargas to prevent them from entering the building. More than 1,100 stockbreeders and farmers arrived on overnight ferries in the early hours of Wednesday, to protest against increases in tax and social security contributions demanded by the creditors keeping Greece afloat. Footage showed the farmers, many wearing black bandanas, smashing the windows of riot vans with shepherds’ staffs, setting fire to rubbish bins and hurling rocks and stones.

When the agriculture minister, Evangelos Apostolou, initially refused to meet a 45-member delegation representing protesters, anger peaked. “Dialogue is one thing, thuggery quite another,” the minister said, before attempts at further talks also foundered. Greek farmers, long perceived to be the privileged recipients of generous EU funds, have historically been exempt from taxation. However, the barrage of cuts and increases in the price of everything from fuel to fertilisers will hit them hard. Tax rates are expected to reach 26%, while pensions are being cut by as much as 22% by 2022. Prof George Pagoulatos, who teaches European politics and economy at the University of Athens, said: “Farmers, in many ways, are a classic example of one of Greece’s protected groups. “In certain rural constituencies, like Crete, they are also electorally very influential.”

Wages have become too low to pay for pensions. 23% unemployment. Almost half of Greeks depend on pensions to stay alive. More cuts are inevitable. The only way is down.

• It Takes 10 Workers In Greece To Pay One Pension (K.)

The constant decline in salaries and the rise of flexible forms of employment are undermining the sustainability of the country’s social security system despite the numerous interventions in terms of pensions. According to social security experts, the slide in the average salary means that it now takes the contributions of 10 workers to pay one pension; before the crisis it required the contributions of four workers. The deterioration of that ratio highlights the system’s viability problem. The main feature of that problem is that the contributions of today’s workers go in their entirety toward covering the pensions of today’s pensioners.

According to data from the new Single Social Security Entity (EFKA), the analysis of employers’ declarations from May 2016 showed that the average salary of 1.4 million workers with full employment amounted to €1,176 per month. The average monthly gross earnings of the 588,000 part-time workers amounted to just €394; their number increased by about 11% from a year earlier. The same data show that bigger enterprises pay higher salaries: Businesses with fewer than 10 employees have an average full-employment salary that amounts to just 58.9% of that paid to employees of companies with more than 10 workers.